Polyester Filament Yarn Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

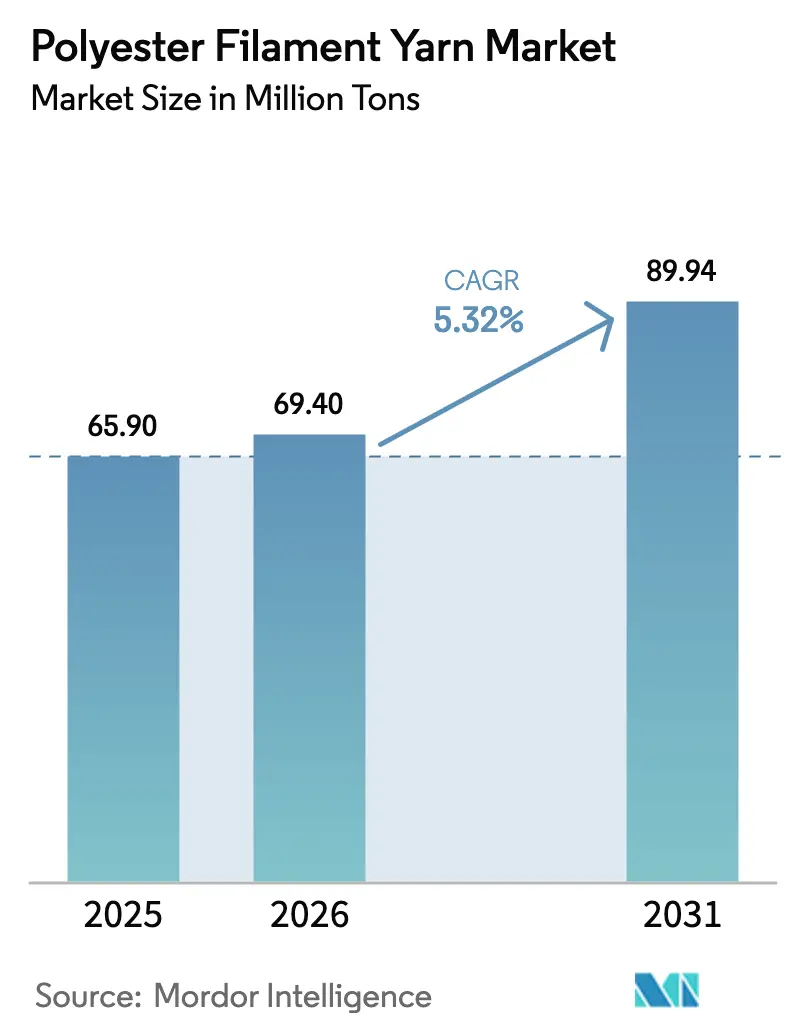

| Market Volume (2026) | 69.40 Million tons |

| Market Volume (2031) | 89.94 Million tons |

| Growth Rate (2026 - 2031) | 5.32% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Polyester Filament Yarn Market Analysis by Mordor Intelligence

The Polyester Filament Yarn Market size is expected to increase from 65.90 million tons in 2025 to 69.40 million tons in 2026 and reach 89.94 million tons by 2031, growing at a CAGR of 5.32% over 2026-2031. A plunge in purified terephthalic acid and monoethylene glycol prices during the 2025 petrochemical down-cycle locked in lower input costs for integrated producers, encouraging capacity additions while compressing merchant-spinner margins. Post-pandemic fashion cycles shortened further, pushing apparel brands to demand just-in-time yarn deliveries and tilting procurement toward vertically integrated suppliers that hold buffer inventories of pre-oriented and fully drawn yarn. Recycled polyester filament yarn gained traction as brands and regulators tightened circular-economy rules, creating a premium segment that now trades above virgin equivalents. Meanwhile, solution-dyed technology, 3-D seamless knitting, and other resource-saving innovations improved polyester’s value proposition against cotton and silk, sustaining long-run substitution in apparel, home furnishings, and industrial fabrics.

Key Report Takeaways

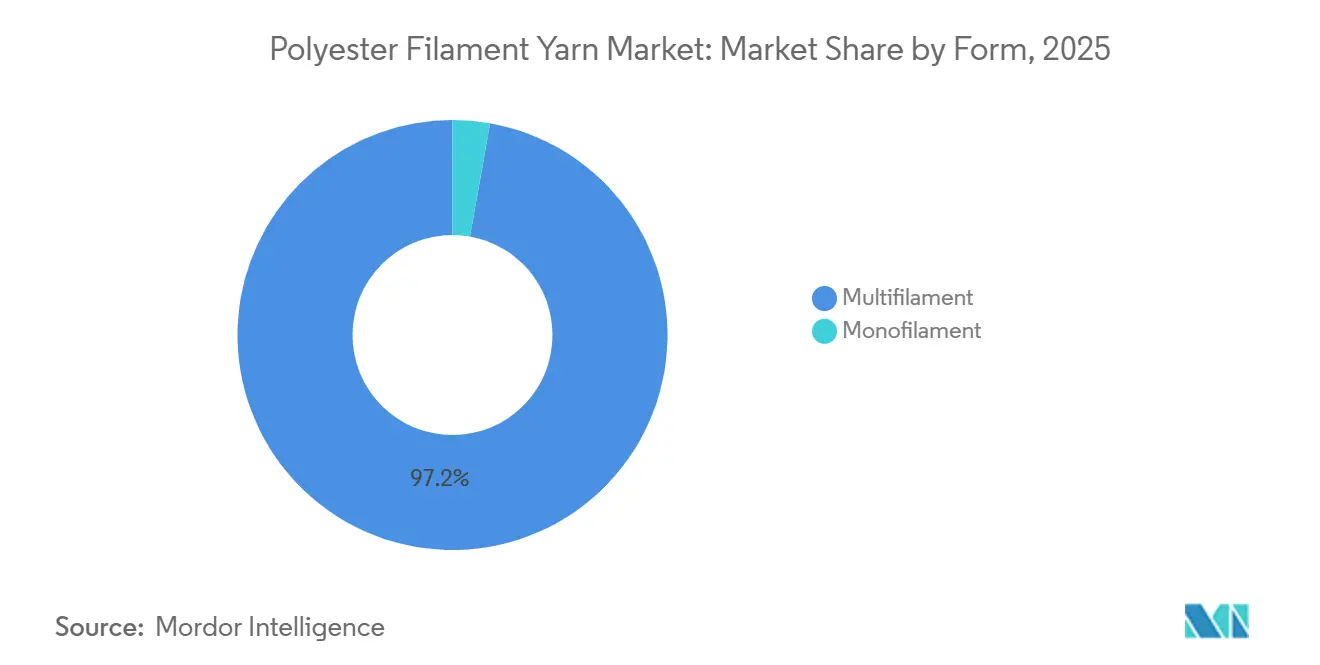

- By form, multifilament captured 97.21% of the 2025 volume and is advancing at a 5.39% CAGR through 2031.

- By product type, drawn textured yarn held 68.72% of the polyester filament yarn market share in 2025 and is advancing at a 5.87% CAGR through 2031.

- By denier, fine polyester filament yarn held 49.29% of the market share in 2025 and is advancing at a 5.73% CAGR through 2031.

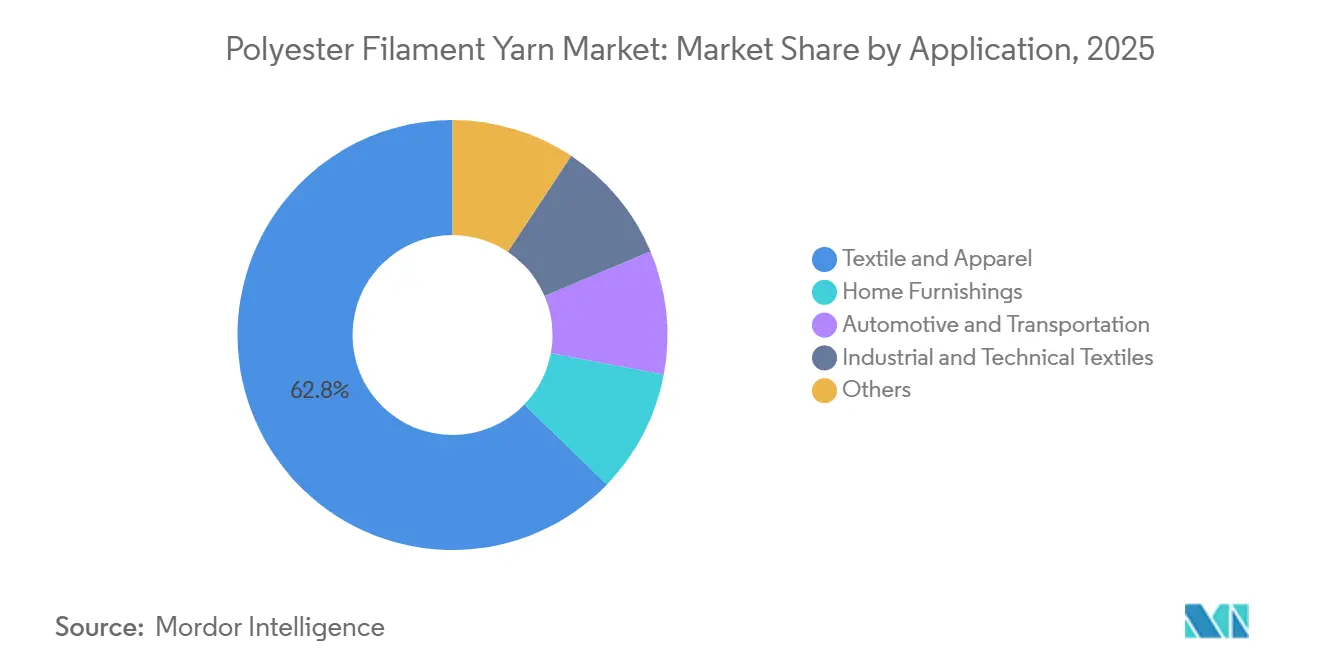

- By application, textile and apparel accounted for 62.75% of the polyester filament yarn market size in 2025, and industrial and technical textiles are expanding at a 7.88% CAGR through 2031.

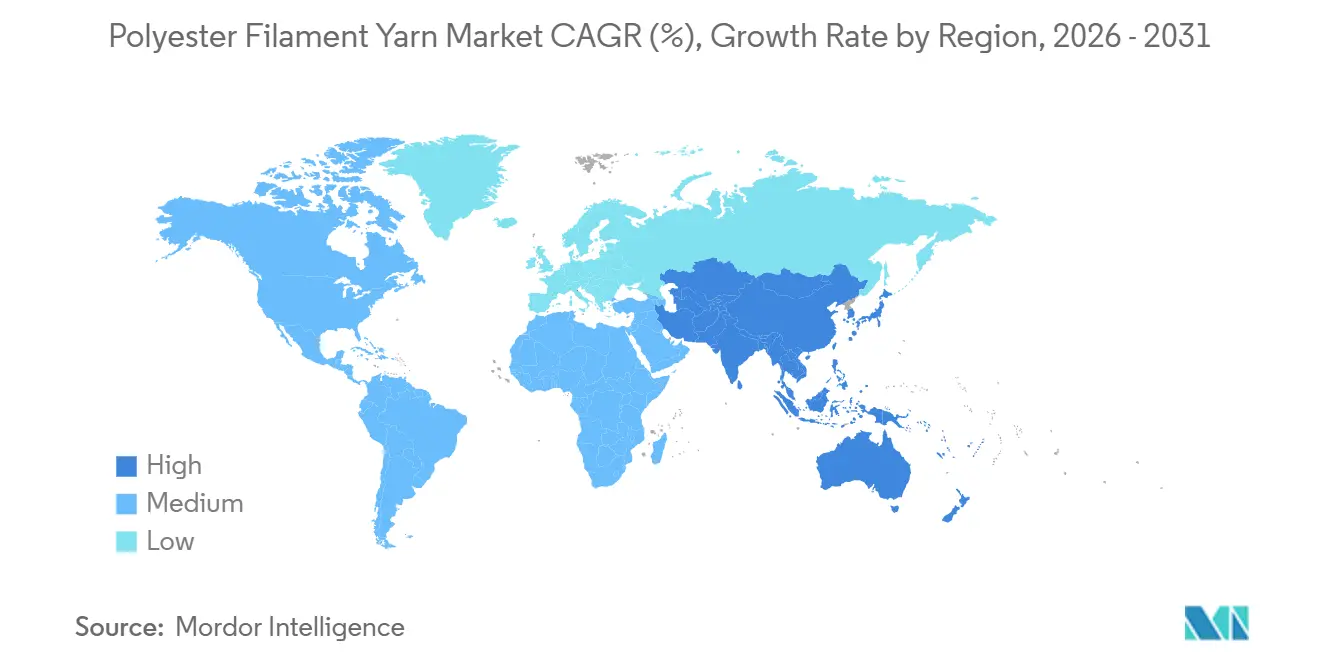

- By geography, Asia-Pacific commanded 92.11% revenue share in 2025 and is expanding at a 5.47% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Polyester Filament Yarn Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Apparel and fashion-led PFY demand boom | +1.2% | Global, with concentration in Asia-Pacific and Europe | Medium term (2-4 years) |

| Cost-to-performance edge vs. cotton and silk | +0.9% | Asia-Pacific core, spill-over to South America and MEA | Long term (≥ 4 years) |

| Capacity expansions and supply-chain localization in APAC | +1.5% | Asia-Pacific (China, India, Vietnam, Bangladesh) | Short term (≤ 2 years) |

| Recycled (rPFY) adoption to hit sustainability targets | +0.8% | Europe and North America, expanding to Asia-Pacific | Medium term (2-4 years) |

| 3-D knitted seamless-wear integration | +0.4% | Europe (Portugal, Italy), North America, Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Apparel And Fashion-Led PFY Demand Boom

In 2024, revenue surged, underscoring the dominance of polyester in ultra-short lead-time collections. The athleisure industry's preference for moisture-wicking polyester blends remained evident. Brands are now sidestepping traditional seasonal purchases, pushing spinners to stock pre-oriented and fully drawn yarn for swift downstream texturing. Inditex integrated recycled polyester into its core lines, aligning with the European Ecodesign digital passport rule that took effect in 2024[1]European Commission, “Ecodesign for Sustainable Products Regulation,” ec.europa.eu . This move differentiated the polyester filament yarn market into commodity virgin grades and premium certified-recycled lots, with the latter commanding premiums under long-term offtake agreements. Meanwhile, stagnant sales in 2024 shifted research and development focus towards bio-based polyester pilots, which are still in their nascent stages.

Cost-To-Performance Edge Vs. Cotton And Silk

In 2026, polyester's landed costs are projected to be significantly lower than cotton prices, a shift driven by heightened compliance expenses tied to U.S. forced-labor regulations on cotton. In a strategic move, Bangladesh eliminated the advance income tax on polyester feedstock, setting it to zero, while imposing a tax on cotton. This decision is accelerating the shift towards man-made fibers. Microfilament polyester, now available at under 50 denier, is achieving a silk-like texture at just a fraction of the price, leading to a surge in its adoption in mid-tier formal wear. Despite an anticipated overcapacity in 2025, industry giants managed to maintain double-digit profit margins, thanks to their strategy of pre-booking inexpensive PTA. The competitive landscape is increasingly favoring fully integrated value chains, which are better positioned to navigate fluctuations in feedstock prices.

Capacity Expansions And Supply-Chain Localization In APAC

In 2025, Beijing's "anti-innovation" policy curtailed new lines, a drop from previous levels in 2023. In 2025, India produced less than the demand, but Reliance's ambitious program is set to bridge this gap by 2027. In 2024, Vietnam extracted a significant amount, with a notable portion being re-exported to China. Meanwhile, STK Vietnam has set its sights on boosting the share of recycled yarn by 2027. Bangladesh's heavy reliance on imports underscores a significant opportunity for medium-scale recycling-integrated plants. These plants could sidestep potential Chinese backlash and avoid scrutiny from Western tariffs.

Recycled PFY Adoption To Hit Sustainability Targets

In 2023, global recycled capacity reached significant levels, with a staggering majority sourced from bottle-to-fiber loops, leaving textile-to-textile initiatives in the dust. Filatex India is poised to bridge this gap with its textile-waste unit, slated for a September 2026 launch. Meanwhile, Indorama's strategic takeover of Dhunseri not only underscores the industry's consolidation but also bolsters its ambitions, eyeing a substantial target by 2025. Responding to the EU's directive mandating 50% recycled polyester in garments by 2030, brands are scrambling to secure GRS-certified volumes, leading to a noticeable premium over traditional virgin supplies. Despite the promise of chemical recycling, its capacity remains stunted, hampered by higher costs compared to mechanical routes.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PTA and MEG price volatility | -0.7% | Global, acute in non-integrated producers | Short term (≤ 2 years) |

| Tightening environmental and VOC emission norms | -0.5% | Europe, China, expanding to India | Medium term (2-4 years) |

| Bio-based fiber substitution risk (PLA, PHA) | -0.2% | Europe and North America niche segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

PTA And MEG Price Volatility

In late 2025, a rebound in PTA spot prices lifted U.S. spreads, outpacing China's. This disparity opened the door for arbitrage opportunities for integrated majors. However, merchant spinners faced a pinch, with margins tightening. Meanwhile, as European prices climbed, Asian quotes took a dip, highlighting the amplified uncertainty from diverging MEG swings. In Bangladesh, a cash incentive on PET-flake exports is draining the domestic feedstock. This has led to a surge in chip imports, now commanding premiums. Given these dynamics, capacity growth is likely to concentrate around integrated refiners adept at navigating feedstock cycles, signaling an acceleration in consolidation.

Tightening Environmental And VOC Emission Norms

As part of its revised Industrial Emissions Directive, the EU is imposing stricter caps on VOCs, NOx, and particulates in textile finishing, with deadlines extending to 2028. China's updated GB 4287-2012 rule now requires continuous monitoring and catalytic oxidation[2]China MEE, “Revision of GB 4287-2012 VOC Standards,” mee.gov.cn . In Europe, Oxxynova, Artlant, INEOS, and Indorama's Rotterdam lines were shut down as retrofit expenses exceeded the value of their residual assets. While new plants in Asia are integrating VOC abatement from inception, older facilities in the West are shifting towards recycling lines, benefiting from lighter regulatory burdens.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Multifilament Locks In Dominance Across Applications

Multifilament held 97.21% of the 2025 volume and will climb at a 5.39% CAGR to 2031, supported by apparel, home-furnishing, and industrial buyers that value its drape, strength, and dyeability. Multifilament has solidified its central role in the polyester filament yarn market. While monofilament plays a crucial role in fishing lines, filtration, and sutures, its limited market share restricts its growth potential. Solution-dyed multifilament, which conserves significant water and energy compared to traditional piece-dyeing, is seeing increased adoption in upholstery and automotive interiors. Multifilament is also being utilized to produce lighter automotive carpets that align with the industry's fiber load requirements. The trend of body-mapped garments in seamless 3-D knitting relies on the elasticity of multifilament, boosting the demand for premium recycled variants certified in Portugal and Italy.

The expansion of multifilament is a response to evolving technical demands. Enhanced crimp control in polyester is yielding better pilling resistance, making it a preferred choice for bedding and curtains. Recycled multifilament has now secured a notable share of the denim market. The heightened demand for home-office furnishings post-2024 is bolstering the medium-denier multifilament market in seating upholstery. At the same time, fine-denier variants are witnessing a surge in demand for athleisure and medical gowns. In the medical realm, nano-silver coatings introduced during the spinning process are imparting antimicrobial properties, eliminating the need for a separate finishing bath. This innovation not only addresses hospital-acquired infection standards but also strengthens polyester's presence in medical textiles.

By Product Type: DTY Extends Lead On Texturing Versatility

Drawn textured yarn controlled 68.72% of the 2025 volume and will grow at a 5.87% CAGR, underscoring its preeminence in the polyester filament yarn market. While POY serves as a primary feedstock, FDY has carved out a niche, predominantly in woven shirting and industrial sewing threads. DTY, with its low-shrinkage and high-bulk characteristics, finds favor in applications ranging from single-jersey knits and spacer fabrics to soft-touch bedding. Integrated entities like Tongkun are channeling investments into captive texturing, aiming for lucrative EBITDA margins, a stark contrast to the returns managed by merchant texturizers. Furthermore, air-jet texturing enhances bulk without compromising tenacity, broadening DTY’s marketability, especially in warp-knit automotive seat covers.

Price trends further bolster DTY’s market position. The supply of recycled DTY remains constrained, as brands increasingly demand certified inputs, resulting in a notable premium. FDY continues to be a staple in woven shirting, prized for its low elongation and dimensional stability. Meanwhile, high-tenacity industrial yarn is witnessing a steady uptick in demand for applications like tire cords and conveyor belts, driven by heightened regulatory emphasis on vehicle safety.

By Denier: Fine-Denier Yarns Set The Pace

Fine-denier yarns accounted for 49.29% of 2025 volume and will expand at a 5.73% CAGR. This growth aligns with the fashion industry's shift towards lighter, breathable fabrics and the technical textile sector's demand for high surface-area filtration media. As their share rises, these fine-denier yarns are poised to play a central role in the future demand for polyester filament yarns. Meanwhile, medium-denier yarns, ranging from 150 to 300 denier, continue to be favored in upholstery and uniforms, prioritizing durability over drape. Coarse-denier yarns, exceeding 300 denier, remain steadfast in applications like webbing, geotextiles, and outdoor furniture.

Policy backing fuels the surge in fine-denier yarns. India's National Technical Textiles Mission is channeling funds into fine-denier research and development, targeting applications in medical disposables and geotextiles. In the automotive sector, seat-cover manufacturers are opting for sub-100 denier yarns, achieving a softer touch while maintaining abrasion resistance. This choice bolsters polyester's significant share in vehicle textile content. On another front, medium-denier yarns are reaping the benefits of solution-dye technology, a process that curtails water consumption in products like curtains and office seating. While coarse-denier yarns face competition from polypropylene in the geotextile arena, they carve out a niche in premium artificial-turf backings, leveraging polyester's inherent UV resilience.

By Application: Industrial Textiles Outstrip Apparel Growth

Textile and apparel claimed 62.75% of 2025 volume; however, industrial and technical textiles will race ahead at 7.88% CAGR, underscoring a structural pivot in the polyester filament yarn market. Infrastructure momentum lifts polyester geotextiles that resist UV and carry high tensile loads, while medical textile growth stems from sterilizable gowns and masks. Automotive makers specify PET for airbags, carpets, and seat covers, aligning with end-of-life vehicle recycling rules.

Home furnishings enjoy consistent growth, thanks to solution-dyed polyester's efficiency in reducing water and energy consumption. The athleisure trend bolsters apparel demand, with moisture-wicking blended knits witnessing growth. In industrial applications, polyester is supplanting cotton canvas in conveyor belts due to its superior dimensional stability. Agrotextiles are leveraging polyester shade nets to boost crop productivity. Additionally, filtration media are adopting fine-denier polyester melt-blowns, benefiting from their high surface area and thermal stability, making them ideal for HVAC and industrial dust-collection systems.

Geography Analysis

Asia-Pacific commanded 92.11% of 2025 volume and is set for a 5.47% CAGR through 2031. In 2025, China, adhering to anti-redundancy rules, curtailed new lines. However, integrated giants Hengli, Tongkun, and Rongsheng capitalized on the feedstock slump, securing affordable PTA and driving revenue growth. India's ambitious plan aims to add substantial PTA and polyester capacity by 2027, effectively closing its import gap. With a notable yarn output, Vietnam positions itself as a hub for tariff circumvention. Meanwhile, STK's capacity expansion and its vision for a high percentage of recycled yarn underscore a strong sustainability focus. In contrast, Bangladesh's heavy reliance on imports leaves it vulnerable to feedstock fluctuations.

North America, holding a small portion of the global share, is reaping benefits from near-shoring to Mexico and mandates for recycled content. UNIFI's Repreve line bolsters the region's recycled yarn capacity. However, the limited output of PTA and MEG keeps North American prices elevated compared to Asian standards. Additionally, the Uyghur Forced Labor Prevention Act is steering mid-tier brands towards polyester, amplifying local demand.

Europe's market share is dwindling as retrofitting plants to comply with stringent emission caps proves financially unviable. Concurrently, plant closures in Europe are liberating capacity for Asia and the Middle East. The EU's directive for a significant percentage of recycled polyester by 2030 is reshaping procurement strategies. Buyers are now pre-securing certified volumes, often at a premium. Notably, Italy's seamless-knit hubs and Germany's automotive-textile sector continue to thrive in high-margin niches.

South America is witnessing steady growth, primarily driven by Brazil's substantial consumer base. However, fluctuations in currency are tempering foreign direct investment. The Middle-East and Africa are advancing at a notable rate, bolstered by Saudi Aramco's PTA and PET facilities, which are establishing a competitive export platform. Yet, the region's limited downstream apparel manufacturing restricts its potential for value capture.

Competitive Landscape

The polyester filament yarn market is moderately consolidated. Technology adoption widens the gap. Integrated majors leverage predictive analytics to cut energy, while smaller mills struggle to fund automation. Capacity rationalization in Europe and Taiwan tightens supply, and anti-involution policies in China weed out sub-economic plants. Brand audits increasingly require ISO 14001 and GRS certification; non-compliant mills lose offtake contracts, intensifying consolidation pressure. Chemical-recycling startups target depolymerization but stay subscale due to cost gaps, leaving mechanical recycling dominant near-term.

Polyester Filament Yarn Industry Leaders

Xin Feng Ming Group

Hengli Group Co., Ltd.

Tongkun Holding Group Co., Ltd.

Zhejiang Hengyi Group Co., Ltd.

Jiangsu Eastern Shenghong Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: SASA Polyester began commercial operations at Türkiye’s largest PTA unit in Adana, integrating feedstock for filament yarn, fiber, and polymer streams.

- January 2025: Filatex India cleared an INR 155 crore expansion to add 19,800 MTPA POY, 14,400 MTPA FDY, and 14,400 MTPA DTY in Dahej, commissioning by Jun 2026.

Global Polyester Filament Yarn Market Report Scope

Polyester Filament Yarn (PFY) is a continuous, high-strength synthetic fiber used extensively in textiles, home furnishings, and industrial applications due to its durability and versatility. It is categorized by its structure (mono/multifilament), production method, and linear density (denier).

The market is segmented by form, product type, denier, application, and geography. By form, the market is segmented into monofilament and multifilament. By product type, the market is segmented into pre-oriented yarn (POY), fully drawn yarn (FDY), drawn textured yarn (DTY), and other product types. By denier, the market is segmented into fine, medium, and coarse. By application, the market is segmented into textile and apparel, home furnishings, automotive and transportation, industrial and technical textiles, and others (agriculture, sports, etc.). The report also covers the market size and forecasts in 16 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of volume (tons).

| Monofilament |

| Multifilament |

| Pre-Oriented Yarn (POY) |

| Fully Drawn Yarn (FDY) |

| Drawn Textured Yarn (DTY) |

| Other Product Types |

| Fine |

| Medium |

| Coarse |

| Textile and Apparel |

| Home Furnishings |

| Automotive and Transportation |

| Industrial and Technical Textiles |

| Others (Agriculture, Sports, etc.) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| Form | Monofilament | |

| Multifilament | ||

| Product Type | Pre-Oriented Yarn (POY) | |

| Fully Drawn Yarn (FDY) | ||

| Drawn Textured Yarn (DTY) | ||

| Other Product Types | ||

| Denier | Fine | |

| Medium | ||

| Coarse | ||

| Application | Textile and Apparel | |

| Home Furnishings | ||

| Automotive and Transportation | ||

| Industrial and Technical Textiles | ||

| Others (Agriculture, Sports, etc.) | ||

| Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How fast will global polyester filament demand grow to 2031?

Volume will rise from 69.40 million tons in 2026 to 89.94 million tons by 2031, reflecting a 5.32% CAGR driven by apparel, home furnishing, and technical-textile uptake.

Which product type leads consumption?

Drawn textured yarn captures 68.72% of 2025 volume and keeps the lead thanks to its bulk, stretch, and versatility across knitted apparel and automotive fabrics.

Why are recycled grades gaining share?

EU and brand mandates for garments to contain recycled polyester by 2030 push brands to pre-book certified yarn, allowing recycled filament to command price premiums.

Which region dominates production and consumption?

Asia-Pacific accounts for 92.11% of 2025 volume, anchored by large integrated complexes in China, India, and Vietnam.

What threatens non-integrated spinners?

Feedstock volatility in PTA and MEG compresses non-integrated margins, while stricter VOC rules and buyer sustainability audits raise compliance costs that smaller mills struggle to absorb.

Page last updated on: