Polyester Fiber Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Volume (2026) | 83.02 Million tons |

| Market Volume (2031) | 119.19 Million tons |

| Growth Rate (2026 - 2031) | 7.50% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Polyester Fiber Market Analysis by Mordor Intelligence

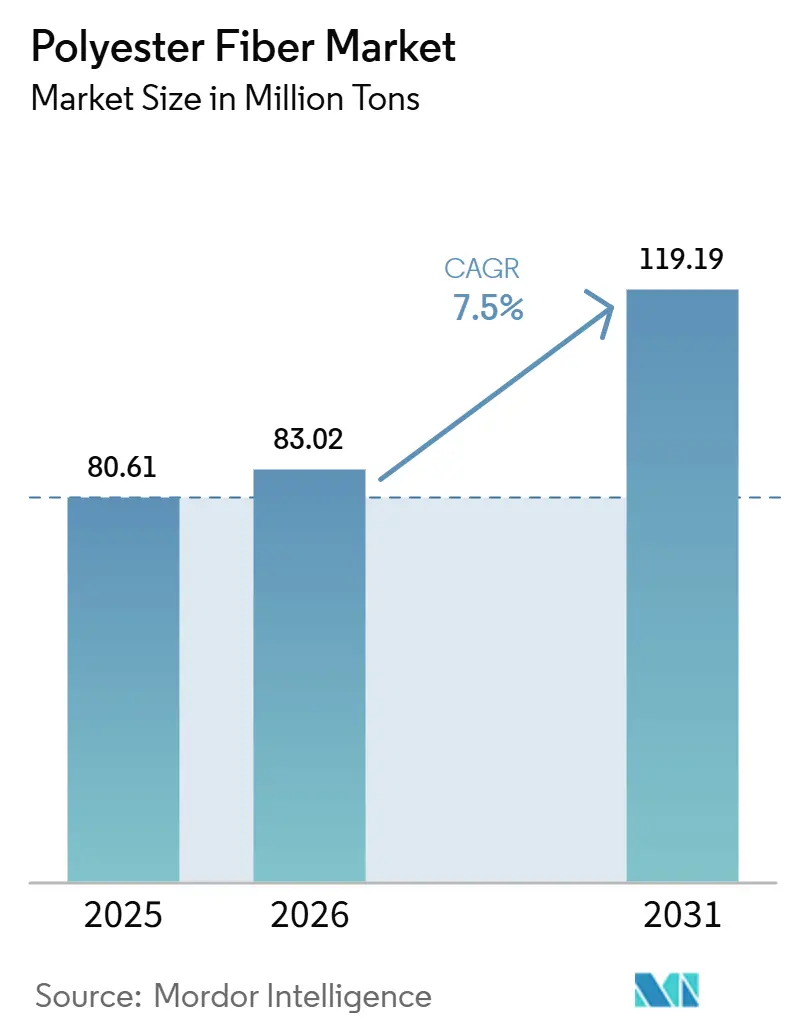

The Polyester Fiber Market size is expected to increase from 80.61 million tons in 2025 to 83.02 million tons in 2026 and reach 119.19 million tons by 2031, and is expected to grow at a CAGR of 7.50% over 2026-2031. The polyester fiber market is advancing because polyester retains a clear cost advantage over natural fibers, an advantage that has become more pronounced as cotton supply disruptions have raised relative input costs for garment and textile producers. The market is also benefiting from tighter circular-economy regulations, which are pushing brands and suppliers to secure recyclable and recycled material flows across apparel, footwear, and home textiles. Wider use in hygiene, filtration, and medical nonwovens is broadening the demand base beyond apparel, reducing dependence on a single end use. The market remains centered in Asia-Pacific, where large-scale manufacturing, deep export markets, and downstream textile integration continue to shape supply discipline and global trade flows. Competition is defined by the scale of integrated Chinese producers and by the push from diversified companies into recycled and specialty products, while feedstock volatility remains the main strategic issue affecting pricing discipline in 2026.

Key Report Takeaways

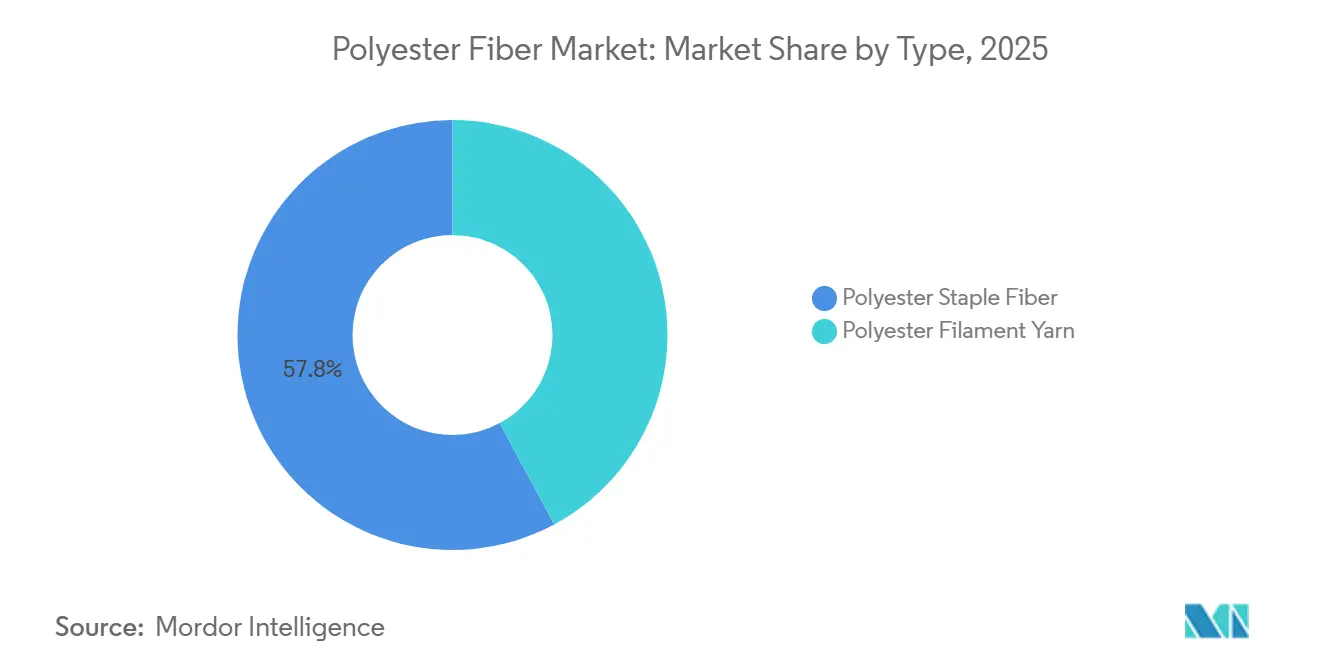

- By type, Polyester Staple Fiber held 57.84% share in 2025, while Polyester Filament Yarn is projected to grow at an 8.05% CAGR through 2031.

- By grade, Polyethylene Terephthalate Polyester accounted for 82.90% share in 2025, while Poly-1,4-Cyclohexylene-Dimethylene Terephthalate (PCDT) Polyester is forecast to expand at an 8.47% CAGR through 203.

- By form, Solid Polyester Fiber represented 75.48% share in 2025, while Hollow-Form Fiber is expected to record an 8.14% CAGR through 203.

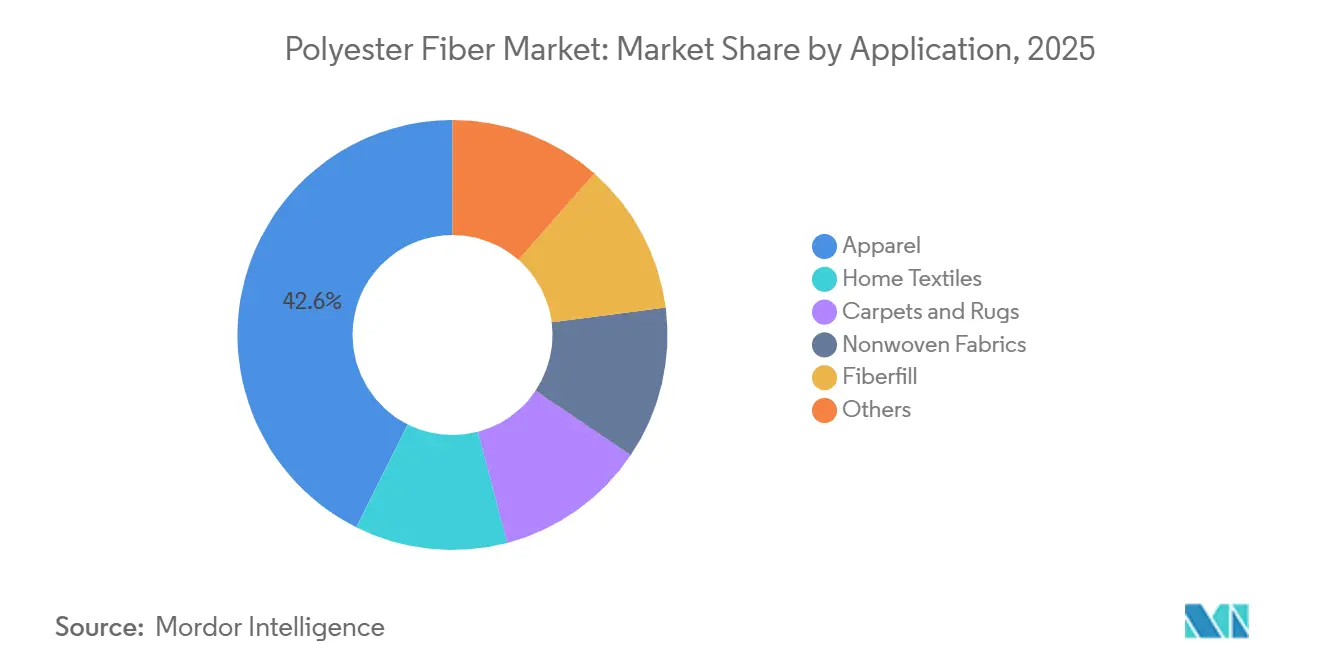

- By application, Apparel captured 42.61% share in 2025, while Nonwoven Fabrics is projected to advance at an 8.61% CAGR through 2031.

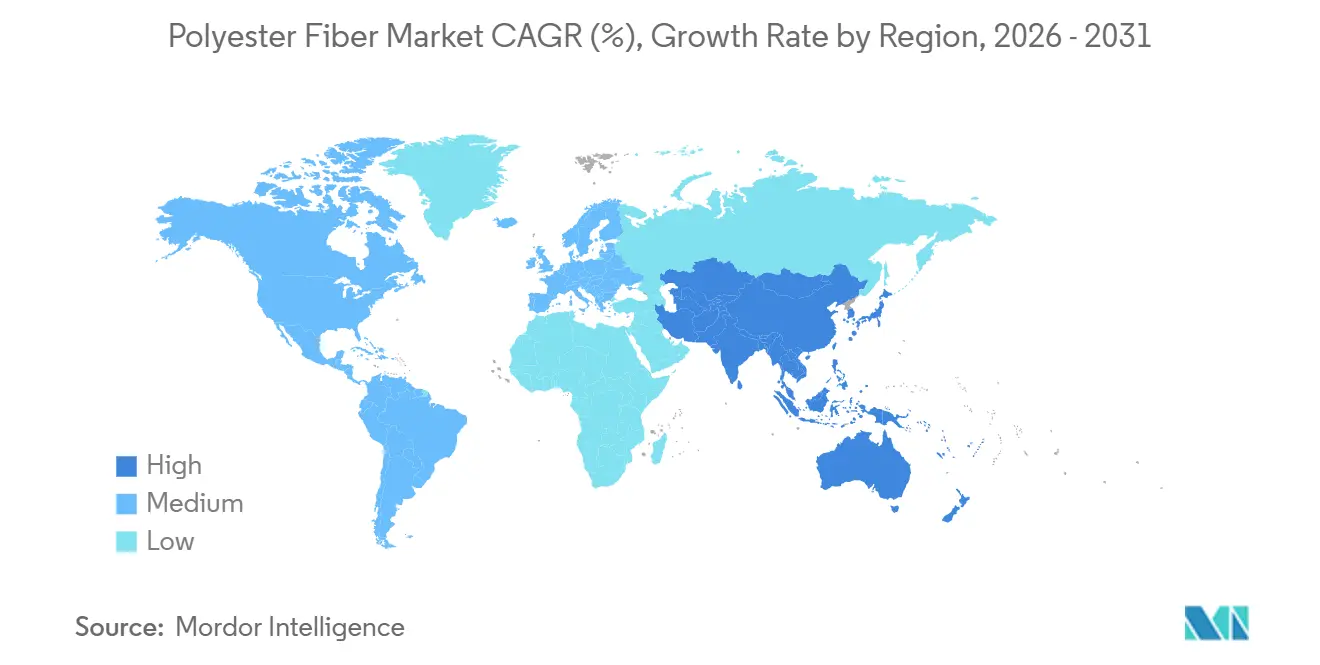

- By geography, Asia-Pacific held 57.23% share in 2025 and is also expected to be the fastest-growing region with an 8.24% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Polyester Fiber Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost-performance superiority over natural fibers | +2.1% | Global, with a concentration in South Asia and Southeast Asia | Short term (≤ 2 years) |

| Recycled polyester adoption and circular-economy mandates | +1.5% | Global, with the highest regulatory intensity in Europe and North America | Medium term (2-4 years) |

| Growth in nonwoven applications in hygiene, filtration, and medical uses | +1.2% | Asia-Pacific core, with spillover to the Middle East and Africa | Medium term (2-4 years) |

| Athleisure and performance-wear demand | +0.9% | North America and Europe, with growing relevance in the Asia-Pacific | Short term (≤ 2 years) |

| EU textile Extended Producer Responsibility (EPR) and mono-material design for recyclability | +0.7% | Europe, with global supply-chain influence | Medium term (2-4 years) |

| Mono-material product design enabling end-of-life fiber recovery | +0.5% | Europe, North America, and Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cost-Performance Superiority Sustains Substitution Against Natural Fibers

The polyester fiber market continues to gain volume as polyester maintains a structural landed-cost advantage over cotton across a wide range of textile applications. That gap widened in 2024 and 2025 as weather-related disruptions in the United States, India, and Pakistan tightened cotton availability and raised natural fiber premiums for textile buyers. This shift was most significant in school uniforms, workwear, and home textiles, where buyers prioritize price consistency, wash durability, and reliable supply over premium natural fiber positioning. The economics also altered blend structures in mixed fabrics, as mills increasingly shifted toward 70:30 or 80:20 polyester-cotton ratios from the more common 65:35 mix. As a result, each unit of fabric now contains more polyester than before, even when garment output does not increase at the same pace. Substitution therefore supports the polyester fiber market through both direct fiber replacement and a gradual increase in polyester intensity within existing textile formats.

Recycled Polyester Demand Accelerates Beyond Voluntary Brand Commitments

The polyester fiber market is entering a more compliance-driven recycling phase, as brands are no longer relying solely on voluntary sustainability targets to shape sourcing behavior. Textile circularity regulations in Europe are pushing suppliers toward recyclable construction, traceable inputs, and stronger end-of-life planning across textile categories[1]Textile Exchange, “Life Cycle Assessment for Polyester – Summary,” Textile Exchange, textileexchange.org. Textile Exchange reported in June 2026 that chemical recycling can process both post-consumer and post-industrial polyester waste while removing dyes and additives that thermomechanical routes cannot fully address. This expands the usable waste stream for recycled polyester and improves the quality of recycled output, thereby supporting stricter product specifications. Indorama Ventures reinforced this direction in November 2025 through its joint venture with Jiaren Chemical Recycling, targeting up to 100,000 tons of textile-recycled polyethylene terephthalate (PET) spinning capacity per year. As capacity builds and conversion economics improve, recycled polyester is becoming a more stable demand pillar within the polyester fiber market rather than a niche premium option.

Nonwoven Fabric Expansion Drives the Market's Fastest Application Growth

The fastest application growth in the polyester fiber market is occurring in nonwoven fabrics, which are projected to expand at an 8.61% annual growth rate through 2031. Demand is coming from hygiene products, medical barrier materials, filtration systems, and geotextiles, where product performance typically matters more than fashion cycles or seasonal discretionary spending. This gives polyester a demand base tied to essential consumption and industrial specifications rather than to apparel sell-through alone. Polyester also suits single-material nonwoven design, as its melt behavior supports thermal bonding routes that reduce binder use and can simplify end-of-life handling under emerging design regulations. Sourcing diversification into India and Southeast Asia is expanding the manufacturing footprint for nonwoven output, reducing dependence on a single-country supply base. These factors make nonwovens a stabilizing demand segment for the polyester fiber market during periods when apparel demand or commodity yarn margins soften.

Athleisure and Performance Wear Mainstream Polyester in Premium Segments

The polyester fiber market is also benefiting from sustained demand for polyester in athleisure and performance wear, where moisture management, durability, and easy-care properties remain essential. Brands are increasingly designing garments that transition between exercise, travel, and casual everyday use, which raises the value of fabrics with stretch compatibility, shape retention, and stable appearance after repeated washing. This trend is driving demand for advanced knitted and textured polyester structures rather than commodity yarn forms alone. Recycled polyester is also gaining importance in activewear collections, as brands seek material choices that align with sustainability messaging and sourcing commitments. Premium sports and lifestyle categories support polyester's movement up the value chain, even when broad apparel demand remains price sensitive. This supports a better product mix within the polyester fiber market and gives producers more room to differentiate beyond basic staple applications.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PTA and MEG feedstock cost volatility | -1.9% | Global, with the most acute exposure in Asia-Pacific and India | Short term (≤ 2 years) |

| Microfiber pollution and non-biodegradability concerns | -0.8% | Europe and North America, with expanding global relevance | Medium term (2-4 years) |

| China-led structural overcapacity and margin compression | -1.6% | Global, with pressure concentrated on non-integrated producers | Short term (≤ 2 years), Medium term (2-4 years) |

| Fine denier anti-dumping trade cases | -0.5% | North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

PTA and MEG Feedstock Volatility Compresses Downstream Margins

The polyester fiber market remains exposed to crude-linked volatility because PTA and MEG costs can shift faster than downstream producers can adjust finished fiber prices. Large upstream capacity has not resolved this issue, as utilization levels, processing margins, and trade sentiment continue to fluctuate with changes in energy markets and regional supply balances. Shipping disruptions through the Strait of Hormuz from late February 2026 added further uncertainty by raising concerns around crude and derivative movement. Producers often struggle to pass higher input costs through immediately when the downstream chain is already oversupplied and buyers resist price increases. This results in more severe margin compression for non-integrated producers, particularly those selling undifferentiated commodity products into competitive export channels. The polyester fiber market continues to grow in volume, but profitability can remain weak when feedstock shocks occur during periods of heavy capacity and cautious downstream buying.

Microfiber Pollution Concerns Escalate Toward Enforceable Regulation

The polyester fiber market also faces a structural environmental challenge from microfiber shedding and the broader debate around synthetic textile pollution. In Europe, Regulation (EU) 2023/2055 under REACH, and related textile product policy work under the Ecodesign for Sustainable Products Regulation (ESPR), are shifting the discussion from voluntary claims toward clearer disclosure and design obligations for synthetic materials[2]European Commission, “Commission Regulation (EU) 2023/2055 Restricting Synthetic Polymer Microparticles,” EUR-Lex, eur-lex.europa.eu. A 2025 study in Fashion and Textiles found that yarn hairiness accounted for 99.7% of the variance in polyester microfiber shedding, suggesting that process control may be one of the most practical near-term responses. While useful, this does not reduce the compliance burden, as producers still face pressure to document material identity, recycled content, and intended end-of-life pathways. Policy discussions in the United States are also moving toward filtration and product-level accountability, which could increase the environmental costs associated with polyester textiles. Until the polyester fiber market has low-cost and widely accepted technical standards for microfiber reduction, this issue will remain a persistent restraint on compliance planning and product development.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Polyester Filament Yarn Gaining Ground in Industrial and Performance Applications

Polyester Staple Fiber (PSF) held 57.84% of the polyester fiber market share in 2025, reflecting its wide use across apparel filling, home textiles, nonwovens, and fiberfill. This position is supported by its scale, processing familiarity, and broad downstream relevance across both basic and semi-technical applications. Commodity-blended yarns rely heavily on PSF inputs, which keeps demand resilient even when fashion cycles become uneven across export markets. The staple segment also benefits from its compatibility with cost-sensitive production systems that prioritize throughput, predictable spinning behavior, and flexible use across multiple end products, maintaining its position despite pressure from higher-value and more specialized yarn categories.

Polyester Filament Yarn (PFY) is the fastest-growing type in the polyester fiber market, with an 8.05% CAGR through 2031. Its continuous-strand structure provides higher tenacity and more stable technical performance in applications such as seat belt webbing, tire cord, reinforcement fabrics, and other engineered textiles. This makes PFY more aligned with industrial and mobility demand than staple fiber, supporting a different growth profile and value mix. Specialty sub-grades such as solution-dyed filament, bi-component filament, and textured filament also offer stronger margins than standard staple formats. As performance specifications tighten in technical textiles and interior materials, PFY is expected to capture a larger share of the polyester fiber market even without overtaking staple fiber in total volume.

By Grade: PET Dominance Entrenched, PCDT Carving Out Specialty Niches

PET polyester accounted for 82.90% of the polyester fiber market in 2025, reflecting its broad presence across mainstream textile and non-textile applications. PET combines strength, processability, and established recycling pathways in a way that few alternative polyester grades can match at scale. Its compatibility with existing bottle-to-fiber systems is particularly relevant as recycled-content requirements become more formal across sourcing contracts and product development roadmaps. This gives PET an advantage not only in virgin production but also in recycled feedstock integration, where capital and collection systems are already more mature. This combination keeps PET central to both volume growth and circularity planning in the polyester fiber market.

PCDT polyester is projected to record an 8.47% CAGR through 2031, making it the fastest-growing grade in the polyester fiber market. Its stronger elastic recovery, higher laundering stability, and better chemical resistance support use in demanding applications such as automotive upholstery, heavy-duty carpets, premium furnishings, and hospitality textiles. These end uses are less tolerant of dimensional instability and appearance loss, which allows PCDT to command a price premium over standard PET in selected specifications. The segment also benefits from a narrower competitive supply base, which can support pricing power for incumbents already serving these specialty requirements. As vehicle interiors and commercial textile applications place more value on durability and stable aesthetics, PCDT is expected to continue expanding its role within the polyester fiber market from a smaller but more specialized base.

By Form: Hollow Fiber Redefines Insulation Performance in Diverse End Uses

Solid polyester fiber represented a 75.48% share in 2025, making it the default form across apparel, home textiles, and several industrial yarn applications. Its broad adoption reflects reliable physical properties, straightforward processability, and suitability for almost all major downstream fiber-conversion routes. Producers and converters value solid fiber because it fits existing machinery with fewer handling adjustments and delivers consistent output quality. This makes solid fiber the practical choice in large-volume categories where cost control and operational simplicity matter more than specialized insulation or loft performance. Within the polyester fiber market, solid form remains the anchor segment even as demand diversifies into more functional structures.

Hollow-form fiber is the fastest-growing form in the polyester fiber market, with an 8.14% CAGR through 2031. Its internal air space improves thermal insulation at lower weight, giving it a fit in outdoor gear, sleeping bags, bedding, and selected automotive seating applications. This value proposition is relevant in categories where warmth-to-weight performance, loft retention, and comfort perception more directly influence purchase decisions. Hollow structures also align with premium bedding and insulation-focused products, where brands often use fill composition as a point of differentiation. The ability to combine insulation performance with recycled polyester content adds a further commercial advantage as buyers increasingly seek both comfort and sustainability credentials. These factors explain why hollow fiber is growing faster than the broader polyester fiber market despite starting from a smaller base than solid fiber.

By Application: Apparel Dominates While Nonwovens Accelerates

Apparel captured 42.61% of the polyester fiber market in 2025, reflecting the scale of garment manufacturing across Bangladesh, Vietnam, Cambodia, and India. Polyester remains central to mass-market apparel because it offers cost efficiency, easy processing, consistent dyeing, and dependable availability across export-oriented supply chains. The apparel segment draws support from two distinct demand streams, with technical sportswear expanding in higher-income markets while value apparel continues to grow in emerging manufacturing hubs. This mix gives polyester relevance across basic woven fabrics, knitted garments, linings, and performance blends. Apparel therefore remains the largest application in the polyester fiber market, combining structural scale with wide product diversity.

Nonwoven fabrics represented the fastest-growing application in the polyester fiber market, advancing at an 8.61% CAGR through 2031. Growth is supported by hygiene product demand in South Asia and Southeast Asia, stable medical procurement requirements, and wider use in filtration and geotextile applications. This gives nonwovens a multi-vertical growth base that is less dependent on consumer fashion cycles and more connected to healthcare, infrastructure, and environmental control needs. Polyester is well positioned in filtration nonwovens, as tightening air-quality and water-treatment standards increase demand for durable, specification-driven media. The segment is also supported by the persistence of barrier-fabric standards that remained in institutional purchasing after the pandemic period. These factors are allowing nonwovens to outpace the broader polyester fiber market and expand polyester use into less cyclical end markets.

Geography Analysis

Asia-Pacific held 57.23% of the polyester fiber market share in 2025 and is projected to grow at an 8.24% CAGR through 2031. The region has the deepest roots in the polyester fiber market, as production infrastructure, textile conversion, export logistics, and downstream demand are all concentrated here. China remains the largest manufacturing base, and its scale continues to shape global pricing, trade flows, and capacity utilization decisions across the polyester value chain. India is developing a more independent growth path as integrated investment strengthens domestic upstream and downstream capacity. Southeast Asia is also growing in importance, with countries such as Vietnam and Indonesia absorbing both Chinese-origin fiber and new investment in weaving and nonwoven capacity. These combined factors suggest that Asia-Pacific is likely to maintain its influence over the polyester fiber market during the forecast period.

Europe and North America show different demand patterns within the polyester fiber market, but both are being shaped by stricter product and material accountability requirements. In Europe, textile circularity regulations and broader ecodesign frameworks are pushing suppliers toward recycled-content integration, stronger traceability, and more recyclable product construction. North America faces a similar need for dependable supply and compliance readiness, although its regulatory environment is less centralized than Europe's. Anti-dumping measures on fine denier polyester filament add further supply uncertainty, which can create openings for domestic or regionally aligned suppliers that offer continuity and specification control.

South America and the Middle East and Africa remain smaller portions of the polyester fiber market, but both regions show structural growth potential. Brazil and Argentina continue to anchor South American demand, with textile and nonwoven development drawing material from Asian suppliers while local resin and conversion capabilities develop. In the Middle East and Africa, downstream textile investment is gaining attention within broader industrial diversification programs, particularly in the Gulf. South Africa remains the most developed sub-Saharan textile market, although infrastructure constraints and currency volatility continue to limit the pace at which the polyester fiber market can expand across the wider region.

Competitive Landscape

The polyester fiber market is moderately fragmented at the production level, with the largest capacity concentrated among major Chinese producers such as Xin Feng Ming Group, Shenghong Holding Group, Tongkun Group, Sinopec Yizheng Chemical Fibre, and Hengli Group. These companies benefit from vertical integration, scale purchasing, and export reach, which give them strong control over utilization strategy during periods of weak downstream pricing. Their presence keeps pressure on smaller regional producers, particularly those without upstream integration or a clear specialty position. Even so, the market is not controlled by one dominant supplier, and competitive outcomes vary widely by grade, form, and end-use specialization. This creates space for differentiated players to compete beyond the pure commodity-volume segment.

Non-Chinese companies in the polyester fiber market are responding by emphasizing recycled content, technical capability, and value-added product positioning rather than matching Chinese producers on scale. Indorama Ventures formed a joint venture with Jiaren Chemical Recycling in November 2025 to build up to 100,000 tons per year of textile-recycled PET spinning capacity. Reliance Industries is also expanding along the polyester value chain, with a focus on specialty fibers and downstream applications, reflecting a push toward better margin quality rather than higher commodity output. Smaller participants such as Unifi, Inc. and Märkische Faser GmbH are gaining traction in segments where brand-certified recycled polyester programs reward traceability, chain-of-custody assurance, and product consistency.

Technology is becoming a more important competitive factor in the polyester fiber market as fiber architecture now matters as much as basic capacity in several growth segments. Hollow cross-sections, bi-component structures, solution-dyed variants, and advanced recycled formulations are helping suppliers protect margins in segments less exposed to raw material price fluctuations. Chemical textile-to-textile recycling represents another area of opportunity, as no single producer has yet established significant scale or pricing power in that part of the chain. The next phase of competition in the polyester fiber market is likely to be shaped less by headline tonnage and more by the ability to combine circularity, technical performance, and supply reliability into repeatable commercial offerings.

Polyester Fiber Industry Leaders

Indorama Ventures Public Company Limited

Alpek Polyester

TORAY INDUSTRIES, INC.

Reliance Industries Limited

Far Eastern New Century Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: Teijin Frontier and Asahi Kasei Advance confirmed that their joint venture, TA Frontier, is on track to begin operations in October 2026. The venture focuses on high-tenacity recycled polyester filament yarns for industrial and apparel applications, combining Teijin Frontier's fiber production capabilities with Asahi Kasei Advance's materials trading expertise to support supply chain resilience in certified recycled-content filament.

- May 2026: Ester Industries and Loop Industries' joint venture, ELITe, signed an MOU with the Government of Gujarat to establish India's first large-scale chemical polyester recycling facility. The agreement supports domestic circular fiber infrastructure and aims to reduce India's dependence on virgin PET imports.

Global Polyester Fiber Market Report Scope

Polyester fiber is a synthetic material derived from petroleum-based chemicals. It is durable, quick-drying, and resistant to wrinkles and shrinking. Accounting for over half of the global fiber market, it is widely used in clothing, upholstery, and as a lightweight filling for pillows and toys.

The polyester fiber market is segmented by type, grade, form, application, and geography. By type, the market is segmented into polyester staple fiber and polyester filament yarn. By grade, the market is segmented into polyethylene terephthalate polyester and PCDT polyester. By form, the market is segmented into solid and hollow. By application, the market is segmented into apparel, home textiles, carpets and rugs, nonwoven fabrics, fiberfill, and others. The report also covers the market size and forecasts for polyester fiber in 18 countries across major regions. The market sizes and forecasts are provided in terms of volume (tons).

| Polyester Staple Fiber |

| Polyester Filament Yarn |

| Polyethylene Terephthalate Polyester |

| PCDT Polyester |

| Solid |

| Hollow |

| Apparel |

| Home Textiles |

| Carpets and Rugs |

| Nonwoven Fabrics |

| Fiberfill |

| Others |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Polyester Staple Fiber | |

| Polyester Filament Yarn | ||

| By Grade | Polyethylene Terephthalate Polyester | |

| PCDT Polyester | ||

| By Form | Solid | |

| Hollow | ||

| By Application | Apparel | |

| Home Textiles | ||

| Carpets and Rugs | ||

| Nonwoven Fabrics | ||

| Fiberfill | ||

| Others | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is current market size of Polyester Fiber Market?

The Polyester Fiber Market size is expected to increase from 80.61 million tons in 2025 to 83.02 million tons in 2026 and reach 119.19 million tons by 2031, and is expected to grow at a CAGR of 7.50% over 2026-2031.

Which application is growing the fastest through 2031?

Nonwoven Fabrics is the fastest-growing application, with an 8.61% CAGR through 2031, supported by hygiene, filtration, medical, and geotextile demand.

Why does polyester keep gaining against natural fibers?

Polyester keeps winning share because it offers a clear cost advantage, stable processing performance, and broader supply availability, especially when cotton prices are under pressure.

Which region matters most for global supply and demand?

Asia-Pacific is the key region, holding 57.23% share in 2025 and posting the fastest growth at an 8.24% CAGR, which keeps it central to global trade and production.

Page last updated on: