Political Risk Insurance Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

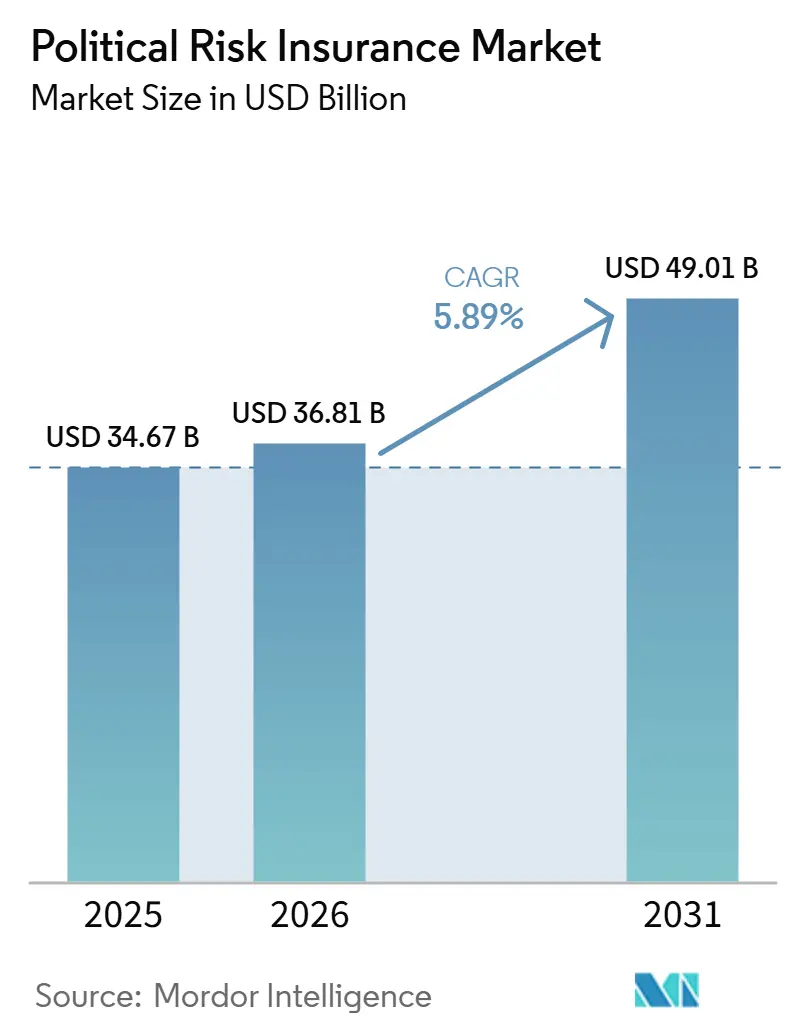

| Market Size (2026) | USD 36.81 Billion |

| Market Size (2031) | USD 49.01 Billion |

| Growth Rate (2026 - 2031) | 5.89% CAGR |

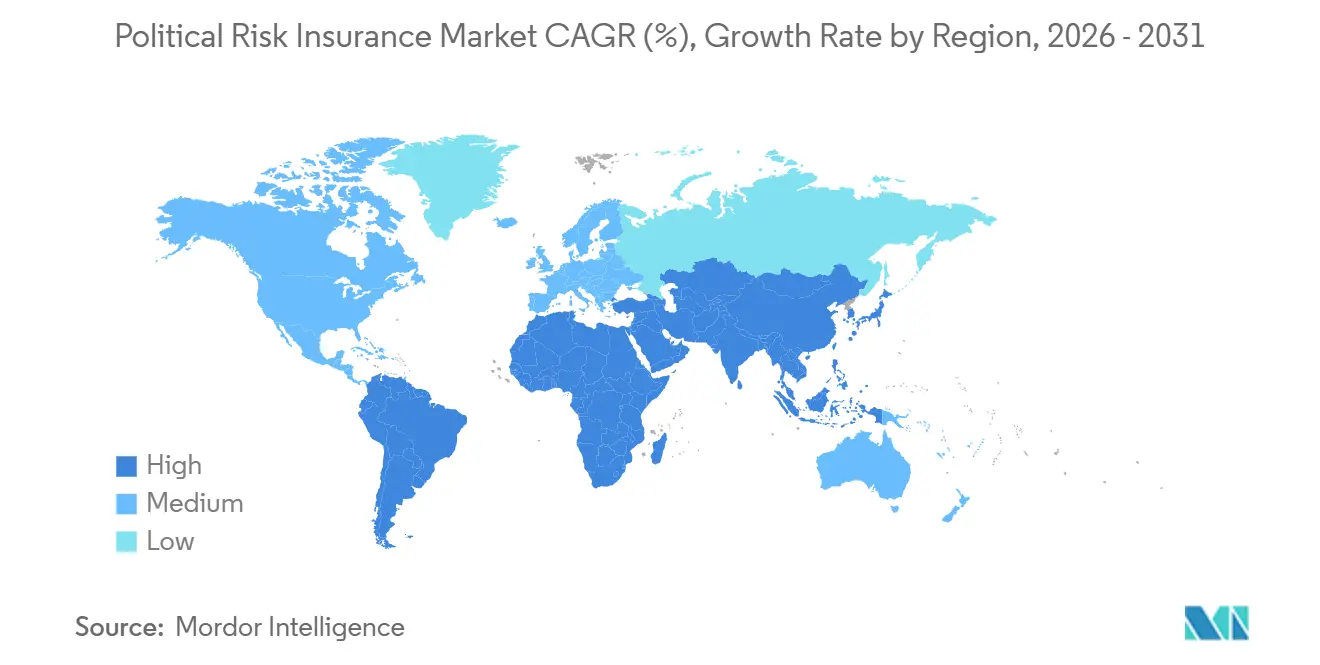

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

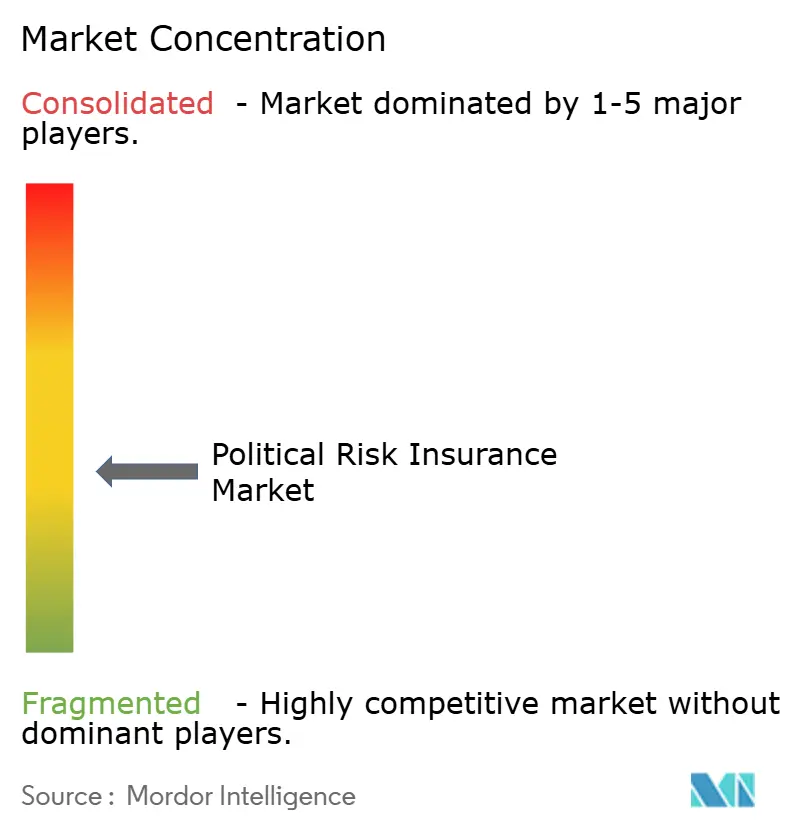

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Political Risk Insurance Market Analysis by Mordor Intelligence

The Political Risk Insurance Market size is projected to be USD 34.67 billion in 2025, USD 36.81 billion in 2026, and reach USD 49.01 billion by 2031, growing at a CAGR of 5.89% from 2026 to 2031.

The political risk insurance market is growing in a business climate where geopolitical disruptions are affecting trade, investment, financing, and supply chains across multiple regions simultaneously. Corporate buyers are also treating coverage more as a standard risk management tool than as a selective add-on, as survey evidence in 2026 showed both a high incidence of financial losses from geopolitical and trade disruption and a rise in insurance use among surveyed companies. The scope of demand has widened because buyers are no longer focused only on conventional expropriation or war scenarios, and are also responding to sanctions pressure, regulatory action, contested trade systems, and state-backed interference in cross-border operations. On the supply side, the political risk insurance market still has meaningful aggregate capacity. Still, it remains uneven across jurisdictions and harder to access in the most sensitive countries, even as global underwriting resources rise. This keeps the political risk insurance market attractive for carriers, brokers, export credit agencies, and multilateral institutions that can combine capacity, structuring expertise, and targeted product design for buyers facing more complex cross-border exposures.

Key Report Takeaways

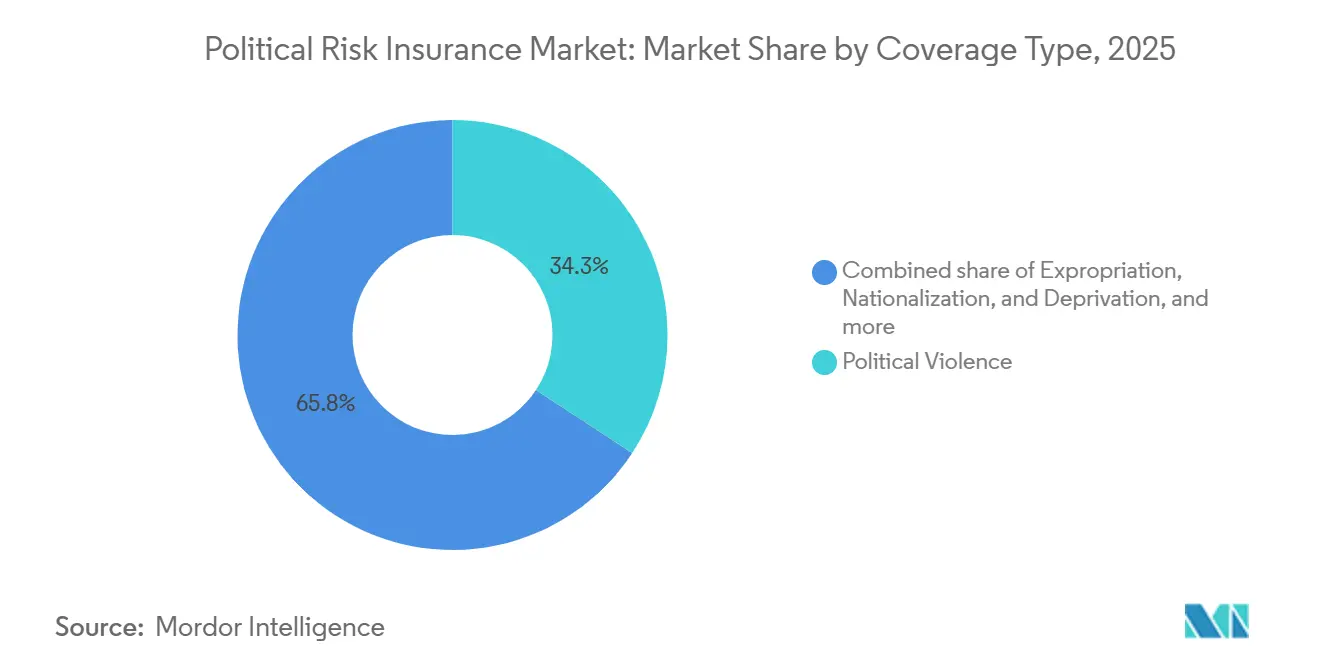

- By coverage type, political violence accounted for 34.25% of the political risk insurance market share in 2025, making it the largest coverage category. The same segment is projected to grow at 7.4% CAGR through 2031.

- By end user, project developers and sponsors accounted for 29.93% of the political risk insurance market share in 2025, while financial institutions are projected to grow at 7.0% CAGR through 2031.

- By distribution channel, brokers and intermediaries captured 52.77% of the political risk insurance market share in 2025, while digital and online platforms are projected to grow at 9.0% CAGR through 2031.

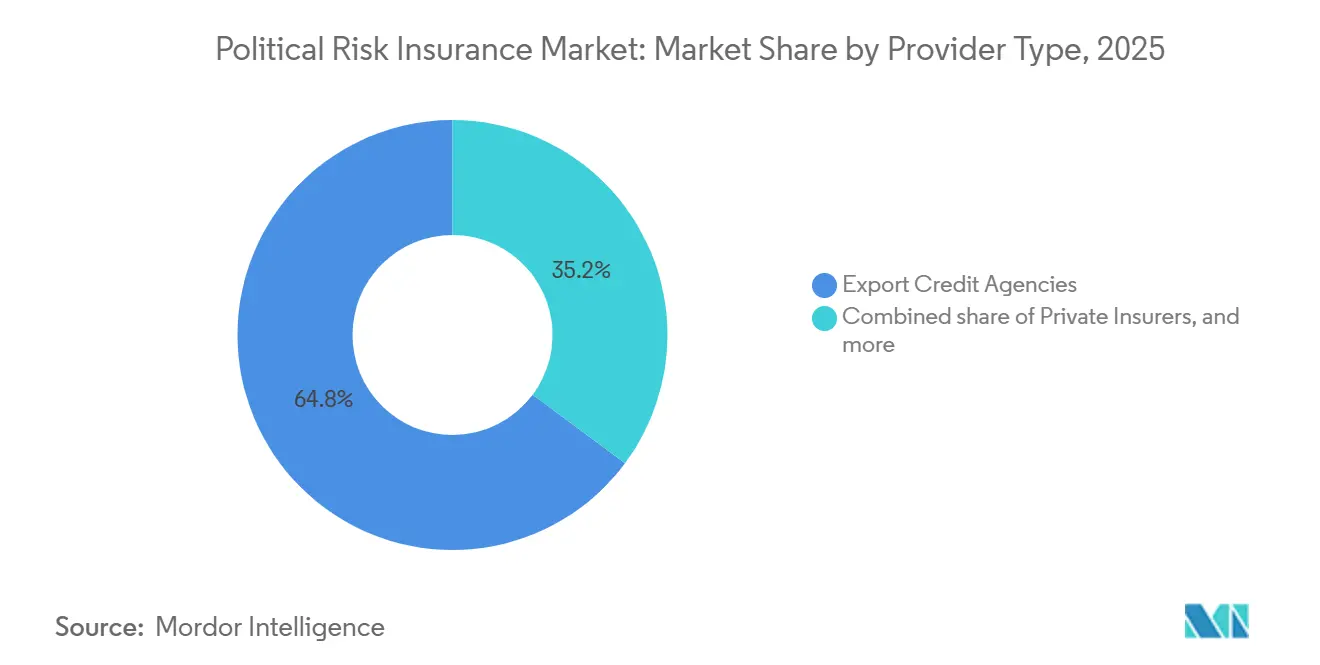

- By provider type, export credit agencies accounted for 64.82% of the political risk insurance market share in 2025, while multilateral institutions are projected to grow at 8.1% CAGR through 2031.

- By sector, energy and power led with 29.23% of the political risk insurance market share in 2025. The same segment is projected to grow at 7.8% CAGR through 2031.

- By geography, Asia-Pacific accounted for 36.59% of the political risk insurance market share in 2025, while the Middle East and Africa are projected to grow at a 7.2% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Political Risk Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Geopolitical Tension and Sanctions Escalation | +2.1% | Global, with concentration in Eastern Europe, the Middle East, and East Asia | Short term (≤ 2 years) |

| Cross-Border Investment Repatriation Protection Need | +0.9% | Asia-Pacific, Latin America, Sub-Saharan Africa | Medium term (2-4 years) |

| Trade Fragmentation and Tariff Uncertainty | +0.7% | Global, with a focus on North America, Asia-Pacific, and Southeast Asia | Short term (≤ 2 years) |

| FDI Derisking for Infrastructure and Energy Projects | +1.4% | Sub-Saharan Africa, Southeast Asia, Central Asia, Latin America | Medium term (2-4 years) |

| Digital Risk Monitoring and AI-Based Underwriting | +0.8% | Global, early gains in North America, the EU, and Singapore | Medium term (2-4 years) |

| Supply Chain Relocation into Higher-Risk Jurisdictions | +0.7% | Asia-Pacific core (Vietnam, India, Indonesia), spill-over to MEA and Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Geopolitical Tension and Sanctions Escalation

The political risk insurance market is being pushed forward by a sharper rise in political polarization, regulatory reversals, labor unrest, and state-backed intervention that now create loss events beyond older war and expropriation frameworks[1]Willis Towers Watson, “Political Risk Survey 2026,” WTW, wtwco.com. Survey evidence also showed that credit and political risk losses related to geopolitical events remained near the top of the historical range, with losses above USD 250 million for the third straight year in the survey series. That matters because buyers are not only reacting to isolated country shocks but also responding to contested trade, technology, information, and domestic political systems that can disrupt investment returns and payment flows across multiple jurisdictions at once. For underwriters, the shift from discrete incidents to system-wide contestation makes portfolio accumulation more difficult to manage, which raises the value of specialist analytics and tighter structuring discipline. In practice, this supports continued demand growth in the political risk insurance market, as buyers increasingly need cover for interconnected exposures to political violence, sanctions, regulatory action, and trade disruption, rather than a narrow set of legacy triggers.

FDI Derisking for Infrastructure and Energy Projects

The political risk insurance market is also gaining support from the need to protect large infrastructure and energy investments that depend on long-dated contracts, sovereign commitments, and stable transfer conditions. A major institutional driver came from Basel 3.1, which recognized credit insurance, including political risk cover for sovereign exposures, as an official risk mitigant and confirmed a 45% Loss Given Default floor for banks using this protection. That changes purchase behavior because some lenders can justify coverage based on capital efficiency even when their immediate expected loss view has not worsened. Multilateral activity is reinforcing this demand channel, as MIGA reached cumulative guarantee issuance above USD 100 billion in April 2026, and the World Bank Group Guarantee Platform is targeting annual issuance of USD 20 billion by 2030[2]World Bank, “Portfolio of Guarantees Pushes MIGA’s Total Issuance Over 100 Billion,” World Bank, worldbank.org . The September 2025 Côte d'Ivoire transaction, in which a combined MIGA political risk guarantee and an IBRD policy-based guarantee supported a EUR 433.3 million sustainability-linked loan, shows how the political risk insurance market is becoming increasingly central to blended finance structures for frontier-market infrastructure.

Digital Risk Monitoring and AI-Based Underwriting

Digital underwriting tools are improving how the political risk insurance market assesses submissions, prices exposures, and serves buyers that previously fell below the operational threshold for bespoke review. AI-enabled workflows are shortening review cycles and improving data extraction quality, which matters in a line where coverage decisions often depend on fragmented country, contract, and counterparty information. It also shows that digital placement and underwriting systems are expanding the practicality of online distribution, especially for smaller and more standardized submissions that do not require fully manual placement. This matters for the political risk insurance market because the cost of analysis has historically limited access for smaller buyers, even when their need for protection was real. As underwriting models become more structured and repeatable, the political risk insurance market gains a clearer path to broader participation without altering the core requirement for specialist judgment on high-risk, long-dated transactions.

Supply Chain Relocation into Higher-Risk Jurisdictions

The political risk insurance market is benefiting from supply chain relocation, as tariff pressure and strategic diversification are shifting manufacturing and sourcing to countries that often carry higher sovereign, regulatory, and transfer risk. IMF analysis confirmed that redirected greenfield investment has been flowing into economies such as Vietnam, India, and Indonesia under pressure from trade fragmentation[3]International Monetary Fund, “IMF Working Paper on Trade Fragmentation and FDI,” IMF, imf.org. Rhodium Group also noted that much of the manufacturing relocation out of China has favored emerging Asian markets first, creating deeper operating exposure in jurisdictions with structurally higher political risk than the original production base. This creates a gap because many existing programs were built around outbound investment from advanced economies and are less suited to new supply chains that run within or across emerging markets. As a result, the political risk insurance market is finding new demand from companies that moved production to reduce tariff exposure but then discovered they had taken on new convertibility, contract, and state-action risks that were not adequately insured.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Underwriting Capacity for High-Risk Countries | -0.9% | China, Taiwan, Sudan, Israel, West Africa, and the Gulf during active conflict | Short term (≤ 2 years) |

| High Premiums and Deductibles for Small and Mid-Sized Buyers | -0.6% | Global, with acute impact in MEA and Southeast Asia during elevated-risk periods | Medium term (2-4 years) |

| Complex Wordings, Exclusions, and Claims Friction | -0.5% | Global, particularly affecting new market entrants and smaller buyers | Long term (≥ 4 years) |

| Data Scarcity for Sovereign and Subsovereign Risk Modeling | -0.4% | Sub-Saharan Africa, Central Asia, and frontier markets broadly | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Underwriting Capacity for High-Risk Countries

The political risk insurance market still faces a basic supply constraint because capacity remains tightly restricted in a narrow but important set of high-risk jurisdictions. China, Taiwan, Sudan, Israel, and parts of West Africa are markets where carrier appetite is severely limited or effectively unavailable, and where even multicountry programs can face difficult review regardless of broader portfolio quality. This matters because the most urgent buyer demand often appears in exactly the countries where supply becomes least dependable, which weakens conversion from interest into bound premium. The issue is exacerbated when geopolitical stress affects multiple linked territories simultaneously, as reinsurers and primary markets then manage accumulation rather than treat each risk in isolation. For the political risk insurance market, this means aggregate global capacity can rise. At the same time, effective access in the most sensitive locations remains constrained, limiting growth in areas where protection need is often greatest.

High Premiums and Deductibles for Small and Mid-Sized Buyers

The political risk insurance market has historically served large multinational companies and major financial institutions better than smaller corporate buyers, and middle-market expansion is still in its early stages. Acute geopolitical events can push pricing and retention terms to levels that make meaningful protection difficult for firms with tighter budgets or lower policy limits. It is also noted that deductible structures have tightened in some cases, reducing the practical value of insurance for routine disruptions and shifting coverage toward more severe losses. Digital platforms may reduce part of this barrier by offering simpler covers, but complex cross-border transactions still require specialist broker input and tailored wording, which keeps distribution costs high. That leaves a meaningful share of the addressable base only partially served, slowing the pace at which the political risk insurance market can broaden beyond its traditional large-account core.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Coverage Type: Political Violence Anchors Demand Across a Widening Risk Definition

Political violence accounted for 34.25% of coverage in 2025, making it the largest coverage type in the political risk insurance market. Its position reflects a broad shift in buyer concerns, where conflict, terrorism, civil unrest, access denial, and infrastructure disruption increasingly affect the same investment case rather than being treated as separate exposures. Coverage language has widened beyond physical damage triggers and now more often addresses business interruption and secondary economic effects tied to unrest and targeted disruption. That wider interpretation matters because clients are seeking protection for how events interrupt operations, financing, and contract performance, not only for direct asset loss. In practical terms, this gives political violence a central role in the political risk insurance market because it responds to the type of event pattern that has become more common across trade corridors, energy hubs, and politically contested urban centers.

The segment also gains support from the way buyers structure multinational programs, especially when one placement needs to respond across several jurisdictions with different local legal and security conditions[4]AXA XL, “Political Violence Insurance, Asian Companies Seek Stability in Multinational Solutions,” AXA XL, axaxl.com. Asian companies, for example, have been adopting multinational insurance structures that combine master and local policies, showing how the issue is spreading beyond traditional conflict zones into broader regional risk management. It also points to greater relevance for expropriation, nationalization, deprivation, currency inconvertibility, and non-transfer restrictions, especially when governments use indirect regulatory tools or monetary controls rather than formal seizure. Breach of contract and non-honoring of cover are also becoming more important, as sovereign or state-linked counterparties face fiscal strain that threatens concessions and power purchase agreements. Together, these changes show that the political risk insurance market is treating coverage types less as isolated products and more as overlapping responses to a broader political disruption environment.

By End User: Financial Institutions Lead Growth as Infrastructure Finance Deepens

Financial institutions are projected to grow at 7.0% CAGR through 2031, making them the fastest-growing end-user group in the political risk insurance market. Their expansion reflects the combination of larger infrastructure finance pipelines and the regulatory value of cover under Basel 3.1, which gives banks a balance-sheet case for buying protection in addition to a loss-protection case. This matters because banks and lenders can sustain demand even when geopolitical headlines are less intense, since capital treatment and portfolio management remain active concerns. It also shows that multilateral development banks, development finance institutions, and export credit agencies are increasingly using the private credit and political risk market for facultative reinsurance of large sovereign exposures. That creates a more institutional demand profile for the political risk insurance market, where buying behavior is tied to financing structures and risk-transfer frameworks rather than solely to direct operating losses.

Project developers and sponsors held the largest end-user share at 29.93% in 2025, reflecting the political exposure within long-horizon infrastructure and energy assets in emerging markets. These buyers depend on stable permits, tariff frameworks, offtake agreements, transfer rights, and sovereign support arrangements, which makes multi-year protection a common financing requirement rather than a discretionary purchase. Multinational corporations are also expanding their programs to subsidiaries operating in frontier markets, while exporters and importers are using political risk and trade disruption cover to protect against payment interruptions and sanctions-related friction. Public sector and development institutions add another layer of demand because their own balance sheets can require insurance support when operating in higher-risk countries. This end-user mix shows that the political risk insurance market is being shaped by both direct corporate buyers and institutional capital providers, which broadens the base of recurring demand.

By Distribution Channel: Brokers Dominate While Digital Platforms Expand Access

Brokers and intermediaries retained 52.77% share in 2025, giving them the largest channel position and 52.77% of the political risk insurance market share that year. Their lead reflects the technical nature of many placements, where policy wording, layered capacity, country selection, and claims coordination still require specialist structuring. Large-ticket cross-border risks often involve multiple insurers and require aligning local and master policy terms, which keeps broker expertise central to placement quality. This is especially true where the insured exposure spans political violence, expropriation, contract frustration, and transfer risk in the same transaction. For these reasons, the political risk insurance market still relies heavily on brokers for complex placements even as digital tools improve speed and data handling across the workflow.

Digital and online platforms are projected to grow at 9.0% CAGR through 2031, making them the fastest-growing channel in the political risk insurance market. Their role is growing because structured data intake, faster submission triage, and online matching can reduce the time and cost of reviewing smaller, more standardized risks. The shift to AI-enabled exchanges and underwriting tools helps broaden access for buyers who were previously below traditional minimum premium thresholds. Even so, the channel shift is more about extending reach than replacing established intermediaries, since bespoke placements for politically sensitive assets still depend on negotiation and judgment. This leaves the political risk insurance market with a dual distribution model where brokers continue to dominate high-complexity risks. At the same time, digital channels expand participation and efficiency at the smaller end of the market.

By Provider Type: ECAs Hold the Largest Position While Multilaterals Scale Faster

Export credit agencies held a 64.82% share in 2025, making them the largest provider and accounting for 64.82% of the political risk insurance market that year. Their lead is consistent with ECAs' long-standing public policy role of supporting exporters and investors operating in strategic or higher-risk markets. UNCTAD analysis cited that ECAs accounted for 78% of total PRI issuance over the past decade, confirming the central role of public-backed capacity in this line of business. It also notes that deal composition is evolving, with more structured risk-sharing arrangements combining ECA guarantees with private-sector capital rather than relying solely on traditional guarantee formats. That change matters because it ties the political risk insurance market more closely to blended finance structures and to capital mobilization strategies that extend beyond classic export support.

Multilateral institutions are projected to grow at 8.1% CAGR through 2031, making them the fastest-growing provider group in the political risk insurance market. Their expansion is supported by MIGA crossing USD 100 billion in cumulative guarantee issuance in April 2026 and by the World Bank Group Guarantee Platform consolidating products and structuring capacity across the institution. The African Development Bank's admission as the Berne Union's first multilateral development institution full member also signals closer operating links between development finance and the broader insurance and reinsurance ecosystem. Private insurers remain important because they move faster on product design, digital underwriting, and tailored structures, especially where public providers cannot address smaller buyers or more specialized terms. This provider mix shows that the political risk insurance industry is not shifting away from public-backed supply, and is instead becoming more interconnected across ECAs, multilaterals, reinsurers, and private carriers.

By Sector: Energy and Power Leads While Digital Infrastructure Adds New Demand

Energy and power accounted for 29.23% of the market in 2025, making it the largest sector in the political risk insurance market. This lead reflects the capital intensity of power generation and transmission projects, especially where private sponsors depend on state-linked offtakers, regulated tariffs, concession stability, and transfer rights over long operating periods. The energy demand in the context of a large renewable investment pipeline and a rising use of guarantees and insurance to make financing workable in frontier and emerging markets. These exposures are not limited to expropriation risk, since they also include contract frustration, delayed payments, permit reversals, civil unrest, and currency transfer restrictions that can undermine project cash flow. That keeps the sector central to the political risk insurance market because few other verticals combine such large ticket sizes with such a persistent need for multi-year sovereign and regulatory protection.

The infrastructure and transportation remain a major secondary demand source, particularly where airports, ports, roads, and similar concessions depend on stable public contracts. Mining, oil and gas, and other natural resources are gaining relevance as resource nationalism leads governments to tighten control through regulation and state-backed intervention rather than through formal expropriation alone. Manufacturing and industrial are tied to the same relocation theme: expanding supply chains across Southeast Asia, Central Asia, and Mexico, which creates a need for coverage that had not always been built into prior programs. Financial services and banking demand reflect exposure to payment restrictions and monetary policy disruption in frontier markets. Digital infrastructure, including data centers, cloud nodes, and undersea cable landing stations, stands out as a newer growth area in the political risk insurance market because these assets increasingly sit in politically complex locations even as they support global digital traffic.

Geography Analysis

North America maintained a substantial position in the political risk insurance market in 2025 because the United States remained a major center for carriers, brokers, and public-backed capacity providers. The United States export credit activity in H1 2026 reached USD 31.5 billion, with visible exposure to nearshoring projects in Mexico and Central America. That matters because political risk demand in the region is shaped not only by domestic underwriting depth, but also by outbound and regional financing tied to supply chain realignment. South America presents a split profile, with Brazil and Mexico attracting investment linked to relocation and contract coverage needs. At the same time, Argentina continues to sustain demand around sovereign stress and currency restrictions. Europe remains the underwriting center of gravity for the political risk insurance market because London-market expertise, company-market carriers, and structured specialty capacity still play a central role in global placement and policy design.

Asia-Pacific held 36.59% share in 2025, giving it the largest regional position in the political risk insurance market. The region’s scale stems from heavy cross-border investment activity involving China, India, Southeast Asia, and Australia, which creates meaningful sovereign and sub-sovereign exposure for investors and lenders. Trade flows between China and the Global South rose sharply, underscoring the need for solutions that support cross-border trade, financing, and asset protection across nontraditional corridors. WTW identified India, Indonesia, Malaysia, and Vietnam as locations where underwriting capacity is available, and buyer interest is accelerating, showing that the region combines mature demand centers with a growing base of first-time buyers. This makes Asia-Pacific a key arena for the political risk insurance market, as it combines deep investment, relocation-driven manufacturing growth, and wide variation in country-level political and regulatory risk.

The Middle East and Africa are projected to grow at 7.2% CAGR through 2031, making it the fastest-growing geography in the political risk insurance market. The regional story is mixed because near-term conflict and long-term infrastructure demand are rising simultaneously, both increasing demand and straining available capacity. On the development side, the World Bank Group stated in May 2026 that it plans to more than double annual guarantee issuance in Africa to USD 6.4 billion by 2030, to support power access, job creation, and private investment mobilization. MIGA’s framework agreement with AMEA Power across Africa, the Middle East, and Central Asia further demonstrates how portfolio-based guarantees help investors manage multi-country project pipelines under a single structure. Saudi Arabia and the UAE are becoming increasingly important as both buyers and stress cases for market capacity. At the same time, countries such as Egypt and South Africa remain structurally important emerging markets where penetration still lags behind underlying investment potential.

Competitive Landscape

The political risk insurance market is moderately concentrated at the top, with Lloyd’s syndicates, AIG, AXA XL, Chubb, and Zurich among the most visible anchors of primary underwriting capacity. At the same time, the wider ecosystem includes more than 70 active carriers. More than 50 of these carriers held AA- or higher ratings from S&P, which supports buyer confidence but does not eliminate country-specific supply bottlenecks. The competitive landscape is also shaped by reinsurers such as Munich Re and Swiss Re, as well as a strong broker layer led by Marsh McLennan, Aon, and Willis. This means control over client access, market intelligence, and structured placement remains as important as the direct underwriting balance sheet. In effect, the political risk insurance market competes through a mix of capacity, claims credibility, wording quality, and distribution reach rather than solely through scale.

Strategic moves in 2025 and 2026 show how leading participants are responding to both demand growth and underwriting pressure. In March 2026, Chubb detailed the structure of the Gulf maritime insurance facility with the United States International Development Finance Corporation. This arrangement was expanded to USD 40 billion, with additional reinsurance support, and demonstrated how public-private structures can unlock capacity during acute stress. In July 2025, Willis launched the Undercover facility with Markel, combining cargo, war on land, terrorism, political violence, and confiscation cover into a single structure to reduce coverage gaps and claims disputes. In February 2026, Aon introduced a new USD 25 million war-risk facility for Ukraine with Kniazha Vienna Insurance Group and the United States DFC, extending its coordinated capital support for Ukraine to more than USD 490 million. These moves show that the political risk insurance market is relying on targeted facilities and partnership structures to address exposures that are difficult to serve through standard underwriting alone.

The most open white space still lies in the small- and mid-sized buyer segment and in frontier-market infrastructure, where protection needs are clear but capacity, affordability, or policy simplicity often remain limited. Digital distribution and AI-based underwriting are beginning to reduce friction for standardized risks, putting pressure on incumbents to improve speed and service even as their core advantage remains in complex structuring. That said, competitive differentiation is likely to stay strongest in long-dated, multi-country, and high-severity exposures where judgment, wording discipline, and claims handling carry more weight than processing speed. The political risk insurance industry, therefore, remains open to innovation, but not in a way that removes the value of established broker and underwriter expertise. Overall, the political risk insurance market remains contested but not easily disrupted because scaling in this line still depends on capital strength, country knowledge, and the ability to assemble workable cover across difficult jurisdictions.

Political Risk Insurance Industry Leaders

Lloyd's of London

AIG

Zurich Insurance Group

Chubb

Allianz

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Lloyds of London and Chubb launched a marine war risk consortium providing up to USD 400 million in insurance capacity, USD 200 million for hull and P&I risks, and USD 200 million for cargo, for vessels transiting the Strait of Hormuz, responding to unprecedented demand from shipping operators and commodity traders following the Iran conflict.

- May 2026: The World Bank Group announced its goal to more than double its annual guarantee issuance in Africa to USD 6.4 billion by 2030 under the World Bank Group Guarantee Platform, housed by MIGA. The initiative aims to connect approximately 190 million people to electricity and catalyze private investment at scale.

- April 2026: MIGA crossed USD 100 billion in cumulative guarantee issuance since its founding, marking the milestone with a USD 1.48 billion framework agreement with AMEA Power covering up to 23 renewable energy and battery storage projects across Africa, the Middle East, and Central Asia.

- March 2026: The DFC-Chubb USD 20 billion maritime reinsurance facility for Gulf shipping was expanded to USD 40 billion after AIG, Liberty Mutual Insurance, Berkshire Hathaway Specialty Insurance, Travelers, Starr, and CNA joined as reinsurance partners, effectively doubling available capacity for hull, cargo, and war risk cover in the Strait of Hormuz.

Global Political Risk Insurance Market Report Scope

| Expropriation, Nationalization, and Deprivation |

| Currency Inconvertibility and Non-Transfer Restrictions |

| Political Violence |

| Breach of Contract and Non-Honoring of Sovereign Obligations |

| Multinational Corporations |

| Financial Institutions |

| Exporters and Importers |

| Project Developers and Sponsors |

| Public Sector and Development Institutions |

| Direct Sales |

| Brokers and Intermediaries |

| Bancassurance and Strategic Partnerships |

| Digital and Online Platforms |

| Private Insurers |

| Export Credit Agencies |

| Multilateral Institutions |

| Energy and Power |

| Infrastructure and Transportation |

| Mining, Oil & Gas, and Natural Resources |

| Manufacturing and Industrials |

| Financial Services and Banking |

| Other (e.g., Agribusiness, Healthcare, Technology, etc.) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Indonesia | |

| Thailand | |

| Malaysia | |

| Singapore | |

| Vietnam | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Coverage Type | Expropriation, Nationalization, and Deprivation | |

| Currency Inconvertibility and Non-Transfer Restrictions | ||

| Political Violence | ||

| Breach of Contract and Non-Honoring of Sovereign Obligations | ||

| By End User | Multinational Corporations | |

| Financial Institutions | ||

| Exporters and Importers | ||

| Project Developers and Sponsors | ||

| Public Sector and Development Institutions | ||

| By Distribution Channel | Direct Sales | |

| Brokers and Intermediaries | ||

| Bancassurance and Strategic Partnerships | ||

| Digital and Online Platforms | ||

| By Provider Type | Private Insurers | |

| Export Credit Agencies | ||

| Multilateral Institutions | ||

| By Sector | Energy and Power | |

| Infrastructure and Transportation | ||

| Mining, Oil & Gas, and Natural Resources | ||

| Manufacturing and Industrials | ||

| Financial Services and Banking | ||

| Other (e.g., Agribusiness, Healthcare, Technology, etc.) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Thailand | ||

| Malaysia | ||

| Singapore | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the 2031 outlook for political risk insurance?

The political risk insurance market is forecast to reach USD 49.01 billion by 2031 from USD 36.81 billion in 2026, growing at a 5.9% CAGR over 2026-2031.

Which coverage category leads demand in this space?

Political violence was the largest coverage type in 2025, with a 34.25% share, reflecting broader concern about conflict, unrest, access denial, and related business interruption.

Which buyer group is expanding the fastest?

Financial institutions are the fastest-growing end-user segment, with a projected 7.0% CAGR through 2031 as lenders use cover in project finance and capital management.

Why do export credit agencies matter so much here?

Export credit agencies held a 64.82% share in 2025, underscoring that public-backed capacity remains central to supporting exporters and investors in higher-risk jurisdictions.

Which region offers the strongest growth potential?

The Middle East and Africa are projected to grow at 7.2% CAGR through 2031, supported by strong infrastructure demand and rising use of multilateral guaranteed structures.

How are digital tools changing underwriting and distribution?

Digital and online platforms are projected to grow at 9.0% CAGR through 2031 because faster submission triage and structured data workflows can broaden access for smaller and more standardized risks.

Page last updated on: