Polio Vaccines Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

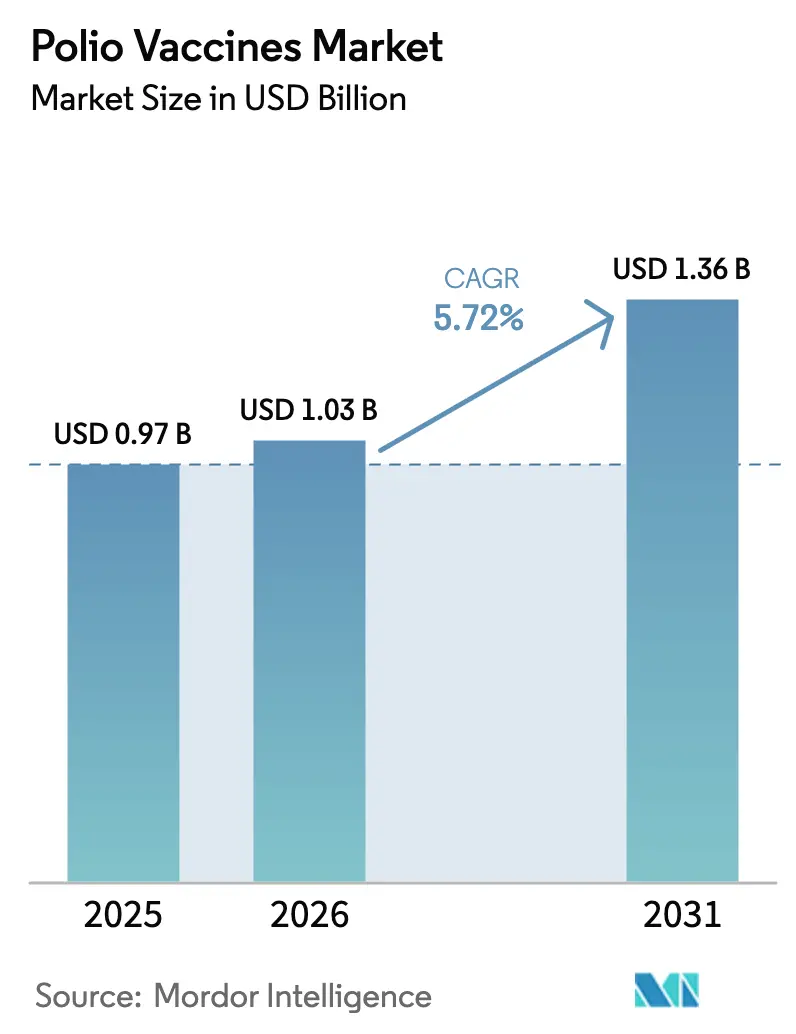

| Market Size (2026) | USD 1.03 Billion |

| Market Size (2031) | USD 1.36 Billion |

| Growth Rate (2026 - 2031) | 5.72% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Polio Vaccines Market Analysis by Mordor Intelligence

The Polio Vaccines Market is expected to grow from USD 0.97 billion in 2025 to USD 1.03 billion in 2026 and is forecasted to reach USD 1.36 billion by 2031 at 5.72% CAGR over 2026-2031.

The market expansion is driven by two key factors: increasing demand for inactivated polio vaccine (IPV) in high-income routine immunization schedules and the critical role of novel oral polio vaccine type 2 (nOPV2) in outbreak response campaigns across fragile regions. Afghanistan and Pakistan remain the primary regions for wild poliovirus type 1 transmission, reporting 68 cases in 2024. However, circulating vaccine-derived poliovirus type 2 outbreaks have declined by 50% year-on-year to 196 cases, reflecting the early success of nOPV2 in the field. Manufacturers capable of addressing both high-margin IPV demand and surge-capacity nOPV2 requirements are strategically positioned to benefit as procurement agencies shift focus from emergency interventions to routine immunization programs.

Key Report Takeaways

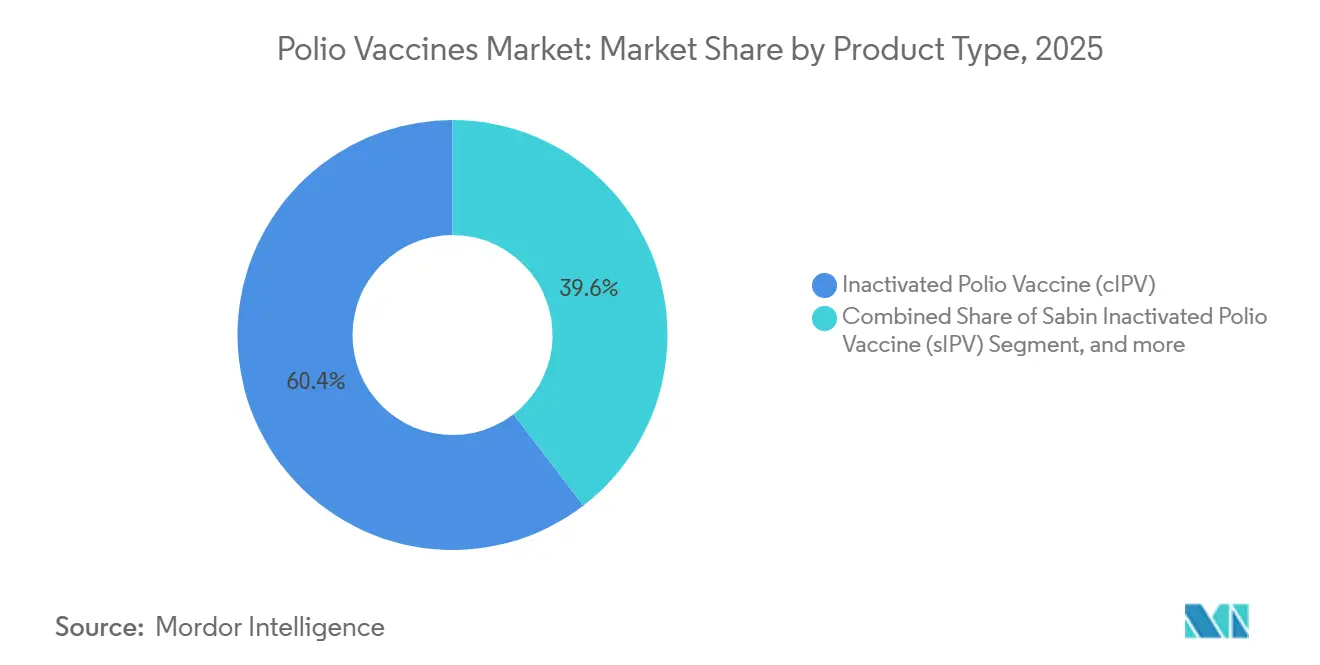

- By product type, conventional IPV commanded 60.43 of % polio vaccine market share in 2025, whereas oral polio vaccine formulations are forecast to expand at a 7.65% CAGR through 2031.

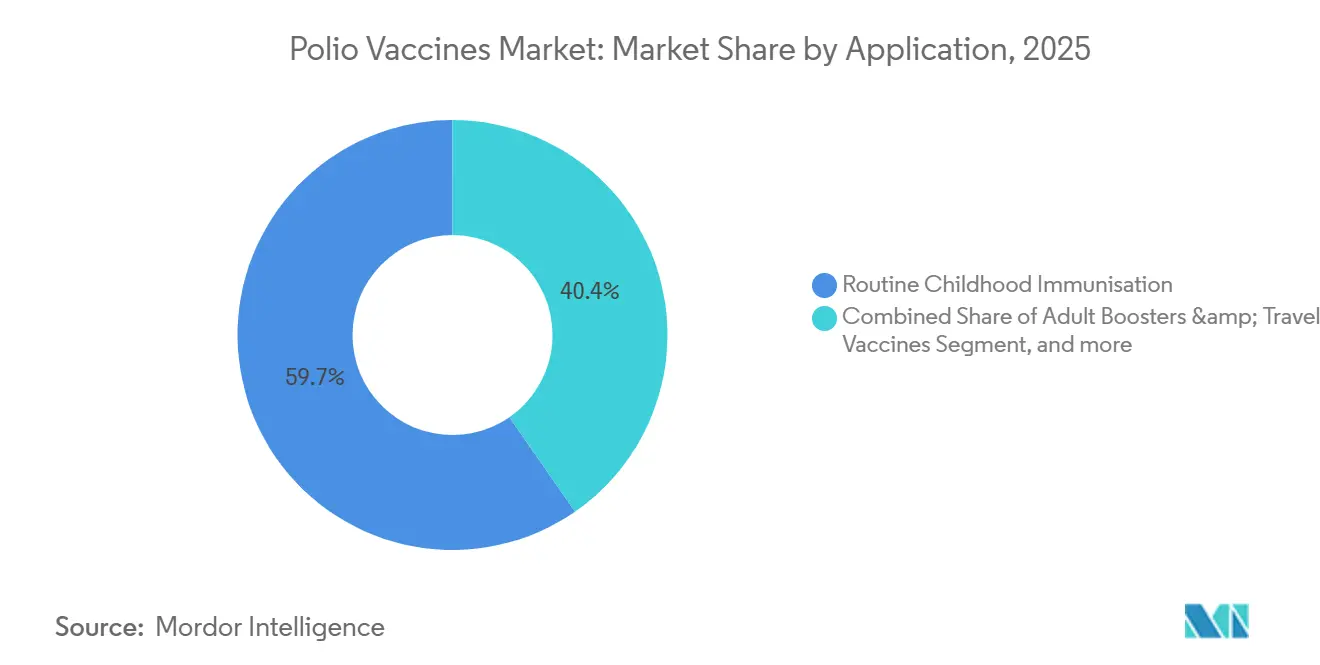

- By application, routine childhood immunization accounted for 59.65% of the polio vaccine market in 2025, while adult boosters and travel vaccines represent the fastest-growing use cases, with an 8.33% CAGR to 2031.

- By end user, hospitals and clinics accounted for 55.87% of 2025 revenue, while public health agencies and government programs are advancing at an 8.43% CAGR through 2031.

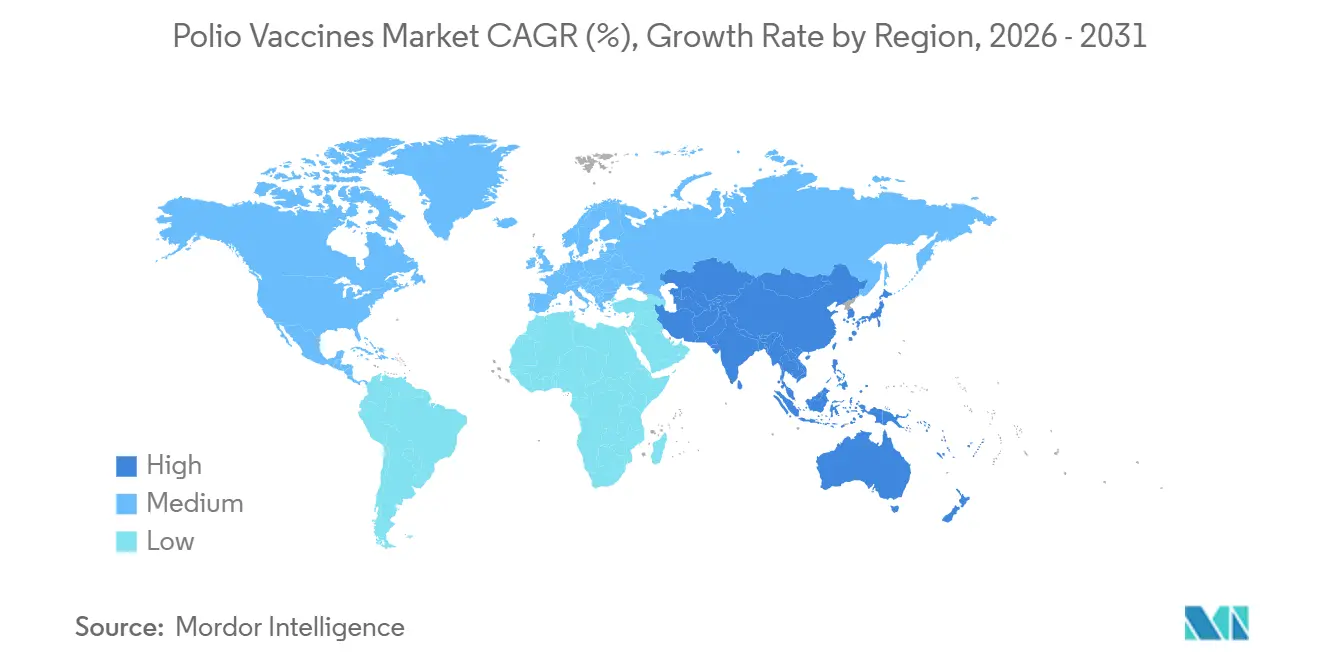

- By geography, North America accounted for 43.76% of 2025 revenue, but Asia-Pacific is poised for the highest growth at a 6.43% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Polio Vaccines Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Global Polio Eradication Funding Momentum | +0.8% | Pakistan, Afghanistan, DRC, Yemen, spill-over to global programs | Medium term (2-4 years) |

| Transition From OPV To Safer IPV Regimens | +1.2% | Asia-Pacific, Middle East & Africa | Long term (≥4 years) |

| Adoption Of Hexavalent Combination Vaccines | +0.9% | Europe, North America, Latin America | Short term (≤2 years) |

| Growth In Government Immunization Budgets | +0.7% | Asia-Pacific, Sub-Saharan Africa | Medium term (2-4 years) |

| Expansion Of Regional Manufacturing Capacity | +0.6% | India, Indonesia, China, Brazil | Long term (≥4 years) |

| Supply-Chain Digitalization And Cold-Chain Upgrades | +0.5% | Kenya, Nigeria, Bangladesh, Indonesia | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Global Polio Eradication Funding Momentum

GPEI extended its strategic plan to 2029 and secured an additional USD 2.4 billion, setting the 2022-2029 envelope at USD 6.9 billion, although the 2026 operating budget tightened to USD 786 million as donors pivoted from emergency response to routine immunization co-financing. Saudi Arabia’s USD 500 million pledge in 2024 earmarked funds for nOPV2 procurement and cold-chain upgrades across the Organization of Islamic Cooperation member states. The revised financing model rewards manufacturers with dual-platform portfolios; Bio Farma shipped 1.2 billion nOPV2 doses to 42 countries since late 2023, whereas Sanofi and Pfizer dominate IPV routines in donor-supported schedules. GPEI’s goal to halt wild poliovirus type 1 by end-2027 compresses the window for high-volume monovalent OPV tenders, driving a measured but durable expansion of IPV procurement. Suppliers lacking WHO prequalification for both IPV and nOPV2 risk exclusion as UNICEF rationalizes its vendor base.

Transition From OPV To Safer IPV Regimens

Withdrawal of trivalent OPV in 2016 and the phased removal of bivalent OPV led 162 countries—84% of WHO members—to incorporate a second IPV dose by April 2025, doubling per-capita vaccine requirements. The epidemiological rationale is compelling: IPV eliminates the reversion risk that produced 196 cVDPV2 cases in 2024, down from 395 a year earlier. Middle-income adopters such as Indonesia, Egypt, and Morocco integrated IPV into combination vaccines to streamline clinic workflows. Cost pressures favor attenuated Sabin IPV (sIPV), which trims biosafety overhead by 20-25%, yet only Bio Farma and Sinovac operate commercial-scale sIPV lines. WHO’s Global Action Plan III biocontainment deadline of 2028 raises the entry bar, forcing smaller producers to pursue contract partnerships or exit entirely. UNICEF’s 2025 tender illustrates the supply gap; it sought 120 million IPV doses but received firm offers for only 95 million, lifting spot prices 15-20%.

Adoption Of Hexavalent Combination Vaccines

Hexavalent formulations that bundle DTaP, IPV, hepatitis B, and Hib antigens captured 18% of IPV-containing volumes in 2025, up from 12% in 2023. Merck’s Vaxelis gained licensure in Brazil and Mexico during 2024, while GSK’s Infanrix Hexa entered Indonesia’s private pediatric channel in 2025. Combination shots reduce cold-chain footprint by 40% per child and cut administration costs 25-30%, but their USD 15-20 unit price still outstrips the USD 2-3 cost of standalone IPV, restricting uptake in low-income countries. Patent expiries for leading formulations between 2027 and 2028 may open emerging markets to biosimilars, intensifying competitive churn. In the interim, standalone IPV suppliers face margin compression as middle-income physicians migrate toward single-visit regimens.

Growth In Government Immunization Budgets

Immunization budgets in Asia-Pacific and Sub-Saharan Africa climbed 12% in 2025 to USD 4.8 billion as states assumed co-financing once covered by GAVI subsidies. India lifted its Universal Immunization Programme outlay 18% to INR 38 billion (USD 456 million), prioritizing IPV2 rollout nationwide, while Nigeria boosted polio allocations 22% to NGN 45 billion (USD 58 million). Domestic-manufacturing incentives align with the trend; India’s Production-Linked Incentive scheme earmarked INR 6 billion (USD 72 million) in 2024 to expand IPV capacity at Serum Institute and BIBCOL. Fiscal stress can still derail plans—Pakistan trimmed its 2025 vaccine budget 8%—but the overall trajectory favors multi-year procurement contracts, giving scale producers predictable volume visibility.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Manufacturing And Cold-Chain Costs | -0.6% | Global; pronounced in Sub-Saharan Africa, South Asia | Long term (≥4 years) |

| Vaccine Hesitancy And Misinformation | -0.4% | Pakistan, Afghanistan, Nigeria, DRC | Short term (≤2 years) |

| Regulatory And Biocontainment Complexity | -0.5% | India, China, Eastern Europe | Medium term (2-4 years) |

| Shrinking OPV Demand Threatening Supply Viability | -0.3% | Global legacy OPV producers in Asia and Eastern Europe | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High Manufacturing and Cold-Chain Costs

IPV must remain at 2-8 °C from factory to clinic, adding USD 0.80-1.20 per dose in logistics, a burden that can equal 40% of landed cost in Sub-Saharan Africa. WHO’s GAP III biocontainment rules compel biosafety-level-3 retrofits costing USD 15-25 million per line, driving some regional firms to mothball production lines. Cold-chain fragility aggravates wastage; grid failures in Nigeria and DRC caused 18-22% temperature excursions in 2025 shipments, inflating effective cost per usable dose by nearly one-third. Blockchain data-loggers piloted in Kenya reduced wastage 12%, yet upfront investment remains prohibitive for the lowest-income markets. Rising diesel prices for off-grid refrigerators further erode margins, reinforcing the advantage of vertically integrated suppliers with proprietary distribution.

Vaccine Hesitancy and Misinformation

Refusal clusters in Pakistan’s Khyber Pakhtunkhwa and Balochistan provinces accounted for 42% of the country’s 41 wild-polio cases in 2024. Social-media misinformation linking polio shots to infertility surged 28% during January-June 2024, correlating with coverage drops documented in The Lancet Infectious Diseases. Afghanistan tallied 27 cases the same year, mostly in Taliban-controlled districts where vaccinators face security threats. Conflict zones complicate deployment: Gaza’s August 2024 emergency campaign reached 90% coverage, below the 95% herd-immunity threshold. Hesitancy is not confined to fragile states; U.S. kindergarten exemption rates rose to 3.1% in 2024, up from 2.6% in 2022[1]Centers for Disease Control and Prevention, “School Vaccination Coverage—United States 2024,” cdc.gov. Community-engagement interventions increase uptake but add USD 0.15-0.25 to program costs per dose, underscoring the tension between public-health imperatives and supplier profitability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Combination Vaccines Challenge Standalone IPV Economics

Standalone conventional IPV dominated 60.43% of revenue in 2025, underpinned by Sanofi’s IMOVAX Polio and Pfizer’s IPOL in higher-income programs. Oral formulations—bivalent OPV, monovalent OPV, and nOPV2—are tracking a 7.65% CAGR as GPEI channels outbreak resources into genetically stabilized nOPV2[2]GPEI, “nOPV2 Supply and Deployment Update,” polioeradication.org. Sabin IPV accounts for less than 8% of output today, yet its 20-25% cost savings over conventional IPV attract ministries in Southeast Asia and East Africa. Combination vaccines captured 18% of IPV-containing doses in 2025 and are advancing at a 6.8% CAGR, driven by Merck's Vaxelis penetration in Latin America and GSK’s Infanrix Hexa rise in private Indonesian clinics. This evolving mix forces producers to choose between cost-leadership in UNICEF tenders or investment in complex, higher-margin combination R&D.

nOPV2’s sole WHO-prequalified line resides at Bio Farma, making the supply chain vulnerable; technology transfers to Bilthoven Biologicals and Panacea Biotec will not reach commercial output before 2028. Bivalent OPV volumes slid 60% between 2024 and 2025, leaving smaller OPV manufacturers with stranded assets unless they pivot rapidly. Combination-vaccine entrants face a long regulatory runway—approvals average 4-5 years per jurisdiction—granting incumbents time to cement provider loyalty. Over the forecast horizon, demand bifurcates: donors prize ultra-low-cost IPV, whereas private insurers and pay-out-of-pocket consumers accept premium pricing for fewer clinic visits.

By Application: Adult Boosters Offer Niche Upside

Routine childhood schedules generated 59.65% of polio vaccines market revenue in 2025, reflecting the near-global rollout of IPV2. Supplemental immunization activities and outbreak response represented 28% of doses, largely in South Asia, Yemen, and parts of Central Africa. Adult boosters and travel vaccinations, though small in volume, are projected to grow 8.33% annually through 2031 as immigration authorities tighten border-entry requirements adjacent to endemic zones. Sanofi’s IMOVAX Polio captured 65% of the U.S. adult-booster channel in 2025, commanding a USD 45-50 list price—roughly 15-fold the tender price for pediatric IPV—demonstrating the margin upside available in private markets. Routine schedules still dictate scale; each additional IPV2 adopter can increase national demand by 40-50%. Yet maintenance of high coverage requires sustained budget lines, stable procurement, and resilient cold chains.

Supplemental campaigns depend on geopolitical stability. In Pakistan, 2024 mobile teams reached 78% of planned children in Khyber Pakhtunkhwa after security incidents curtailed door-knocks, while Gaza’s emergency August 2024 round narrowly missed threshold coverage. Adult-booster uptake remains patchy; only 12 countries strongly enforce vaccination proof for travelers from endemic regions, constraining growth to risk-aware individuals, NGOs, and military agencies. Over the forecast window, the application mix will hinge on whether WPV1 elimination remains on schedule; earlier eradication would slow monovalent demand while cementing routine IPV procurement.

By End-User: Public Agencies Gain Share as Private Channels Seek Differentiation

Hospitals and clinics held 55.87% of 2025 revenue, supplying both mandatory infant doses and elective travel boosters. Public health agencies are forecast to post an 8.43% CAGR through 2031, buoyed by middle-income countries absorbing obligations formerly financed by GAVI. International organizations—UNICEF, WHO, and GAVI—procured 22% of global volume in 2025, funnelling doses into fragile settings. Private providers booked only 15% of doses but captured 28% of revenue because combination vaccines and boosters carry premium margins.

Budget secularization shifts bargaining power. Indonesia’s graduation from GAVI support in 2024 placed USD 18 million of annual IPV purchases directly onto its treasury, opening the door to multi-year supply contracts that favor efficient producers like Serum Institute. On the private side, Merck and GSK deploy volume rebates to hold share, squeezing clinic margins from 35-40% in 2023 to 28-32% in 2025. UNICEF tenders remain price-sensitive; the 2025 IPV call reduced average winning bids to USD 2.40, down 14% from 2023, intensifying the squeeze on smaller standalone suppliers. Divergent incentives between public volume and private convenience ensure parallel channels with limited cross-substitution.

Geography Analysis

North America accounted for 43.76% of global revenue in 2025, driven by premium combination vaccines and adult booster demand in the United States and Canada, even as total dose volume plateaued amid rising exemption rates. Europe contributed 28% of revenue, with Germany, France, and the United Kingdom relying heavily on hexavalent schedules led by Sanofi and GSK. Asia-Pacific delivered the highest volume growth, posting a 6.43% CAGR expected through 2031 as India’s Production-Linked Incentive scheme targets 150 million IPV doses annually by 2027 and Indonesia scales nOPV2 capacity to 800 million doses by late 2026.

Middle East & Africa generated 18% of 2025 revenue but exhibits diverse trajectories: Saudi Arabia’s USD 500 million GPEI grant accelerates procurement, whereas Nigeria grapples with cold-chain failures that waste up to 22% of shipments. South America supplied 10% of revenue, led by Brazil’s adoption of Vaxelis through the PAHO Revolving Fund and Argentina’s more cautious approach amid fiscal austerity.

Revenue-per-dose differentials illustrate broader market economics. OECD markets account for 38% of doses yet supply 72% of revenue, benefiting from 8-10× price premia. Conversely, Asia-Pacific and Africa collectively deliver 62% of doses but only 28% of revenue, pressing suppliers toward cost-optimization and scale efficiencies.

Competitive Landscape

Global revenue remains moderately concentrated: Sanofi, GSK, and Pfizer accounted for 58% of 2025 sales, driven by dominance in hexavalent vaccines and adult boosters. Cost-leadership niches are occupied by Bio Farma, Serum Institute of India, and Beijing Tiantan Biological Products, which collectively command the largest share of government-tender IPV. Bio Farma’s monopoly on WHO-qualified nOPV2, now responsible for 1.2 billion doses, represents a single-point risk that GPEI addresses through technology transfers to Bilthoven Biologicals and Panacea Biotec, with commercial output expected from 2028. Hexavalent vaccines form an oligopolistic arena, whereas standalone IPV markets in the Asia-Pacific host eight to ten regional players, dragging UNICEF tender prices downward.

Incumbents pursue divergent strategies. Sanofi is consolidating IPV production into its Lyon facility and plans to discontinue standalone IMOVAX Polio in favor of Hexaxim, reinforcing a premium positioning[3]Sanofi Investor Presentation Q3 2024, sanofi.com. Serum Institute invested USD 120 million in 2024 to double its IPV capacity, aiming to address UNICEF’s 28% supply gap from 2026 onward. Technology innovation focuses on biocontainment upgrades and cold-chain relief; LG Chem has filed four patents for thermostable IPV adjuvants with six-month stability at 25 °C. Potential disruptors include mRNA-based polio candidates from BioNTech and Moderna, but commercialization is unlikely before 2030.

Polio Vaccines Industry Leaders

Sanofi

GSK plc

Serum Institute of India

Bharat Immunologicals & Biologicals Corporation (BIBCOL)

Beijing Tiantan Biological Products

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Afghanistan launched its first polio vaccination campaign, aiming to protect over 7.3 million children under 5 years old against poliovirus, the Ministry of Public Health reported.

- January 2024: Sanofi and Biovac, a Cape Town, South Africa-based biopharmaceutical company, partnered to produce inactivated polio vaccines (IPV) in Africa. This agreement is designed to enable regional manufacturing of polio vaccines to serve the potential needs of over 40 African countries.

Global Polio Vaccines Market Report Scope

As per the scope of the report, polio vaccines are vaccines designed to protect against poliomyelitis, a highly infectious viral disease that can cause paralysis. There are two main types: the oral polio vaccine (OPV) and the inactivated polio vaccine (IPV). They work by stimulating the immune system to prevent infection and transmission of the poliovirus.

The Polio Vaccines Market is Segmented by Product Type (Inactivated Polio Vaccine (cIPV), Sabin Inactivated Polio Vaccine (sIPV), Oral Polio Vaccine (bOPV, mOPV, nOPV2), and Combination Vaccines Containing IPV), Application (Routine Childhood Immunisation, Supplemental Immunisation Activities / Outbreak Response, and Adult Boosters & Travel Vaccines), End-User (Public Health Agencies & Government Programmes, Hospitals & Clinics, International Organisations & NGOs, and Private Providers), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Inactivated Polio Vaccine (cIPV) |

| Sabin Inactivated Polio Vaccine (sIPV) |

| Oral Polio Vaccine (bOPV, mOPV, nOPV2) |

| Combination Vaccines Containing IPV |

| Routine Childhood Immunisation |

| Supplemental Immunisation Activities / Outbreak Response |

| Adult Boosters & Travel Vaccines |

| Public Health Agencies & Government Programmes |

| Hospitals & Clinics |

| International Organisations & NGOs |

| Private Providers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest Of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest Of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest Of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest Of South America |

| By Product Type | Inactivated Polio Vaccine (cIPV) | |

| Sabin Inactivated Polio Vaccine (sIPV) | ||

| Oral Polio Vaccine (bOPV, mOPV, nOPV2) | ||

| Combination Vaccines Containing IPV | ||

| By Application | Routine Childhood Immunisation | |

| Supplemental Immunisation Activities / Outbreak Response | ||

| Adult Boosters & Travel Vaccines | ||

| By End-User | Public Health Agencies & Government Programmes | |

| Hospitals & Clinics | ||

| International Organisations & NGOs | ||

| Private Providers | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest Of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest Of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest Of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest Of South America | ||

Key Questions Answered in the Report

How large is the polio vaccines market in 2026?

The polio vaccines market size stands at USD 1.03 billion in 2026 and is projected to grow to USD 1.36 billion by 2031.

Which region generates the highest revenue from polio vaccines?

North America leads on value, contributing 43.76% of 2025 revenue, mainly through premium-priced combination vaccines and adult boosters.

Why is nOPV2 critical to current eradication efforts?

NOPV2 delivers genetic stability that lowers reversion risk, enabling safer outbreak response; it has already reduced cVDPV2 cases by 50% year-on-year.

What is driving the shift toward hexavalent combination vaccines?

Health systems favor single-visit immunization that lowers cold-chain and administration costs, despite higher per-dose prices compared with standalone IPV.

How do cold-chain costs affect polio vaccine economics?

Maintaining IPV at 2-8 °C can add up to USD 1.20 per dose in logistics overhead, a significant share of final cost in low-resource settings.

Who controls the majority of nOPV2 supply?

Indonesia’s Bio Farma holds the sole WHO-prequalified nOPV2 line, supplying 1.2 billion doses since December 2023.

Page last updated on: