Point-of-Care Regenerative Medicine and Autologous Biologics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

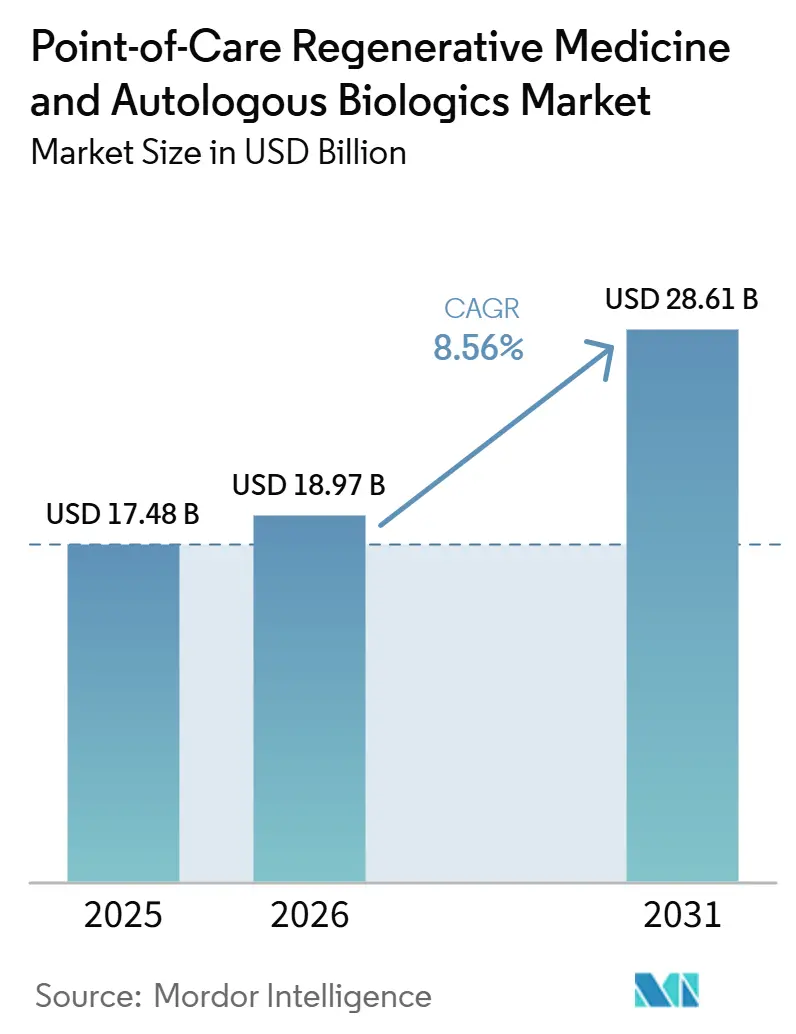

| Market Size (2026) | USD 18.97 Billion |

| Market Size (2031) | USD 28.61 Billion |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Point-of-Care Regenerative Medicine and Autologous Biologics Market Analysis by Mordor Intelligence

The Point-of-Care Regenerative Medicine & Autologous Biologics Market size was valued at USD 17.78 billion in 2025 and is estimated to grow from USD 18.97 billion in 2026 to reach USD 28.61 billion by 2031, at a CAGR of 8.56% during the forecast period (2026-2031).

The Point-of-Care Regenerative Medicine & Autologous Biologics Market is gaining momentum as demand rises for single-visit autologous procedures, particularly in orthopedic and sports medicine settings. Reimbursement support in outpatient and ambulatory surgery centers is improving the practicality of same-day biologic use and supporting higher procedure volumes. The market is shifting toward closed-system processing and standardized kits as providers prioritize contamination control, workflow consistency, and documentation quality. Competition is centered on compact centrifuge systems, training-led adoption, and distribution partnerships, while near-term opportunities remain strongest in applications with clearer procedural pathways or indication-specific regulatory support.

Key Report Takeaways

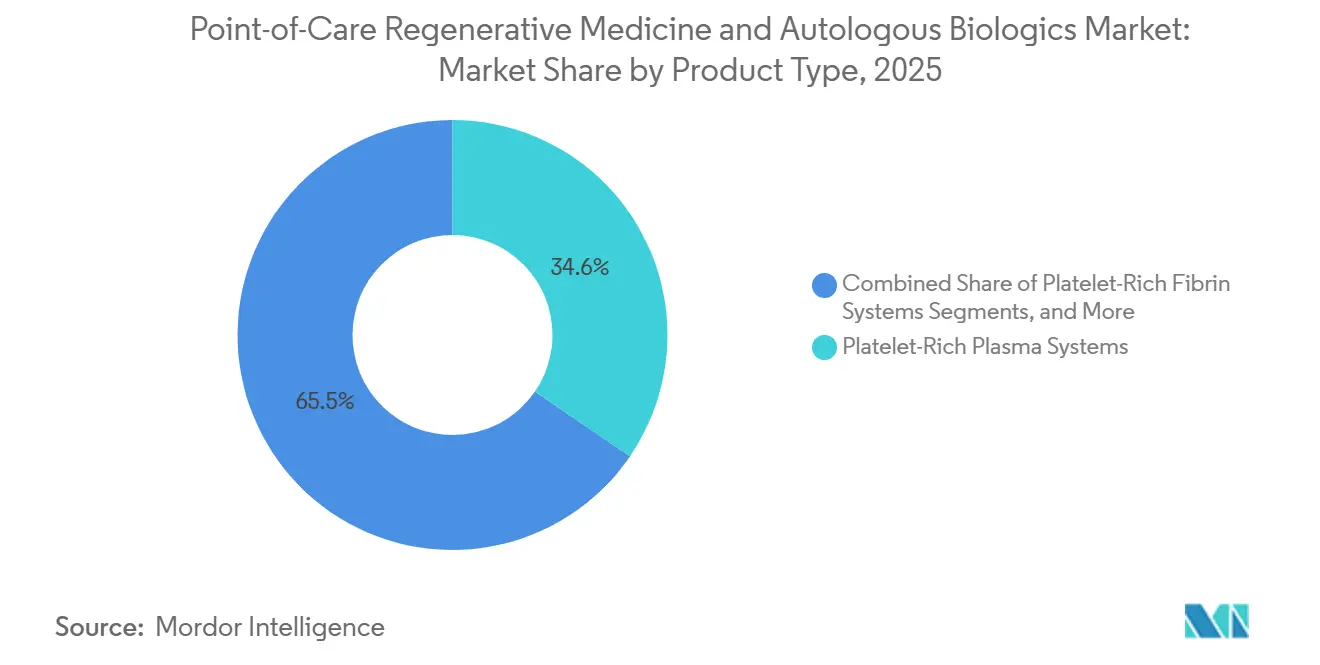

- By product type, platelet-rich plasma systems held 34.55% of revenue in 2025, while bone marrow concentration systems are projected to grow at 11.02% through 2031.

- By application, orthopedics and sports medicine accounted for 37.45% of revenue in 2025, while wound care is projected to expand at 10.80% through 2031.

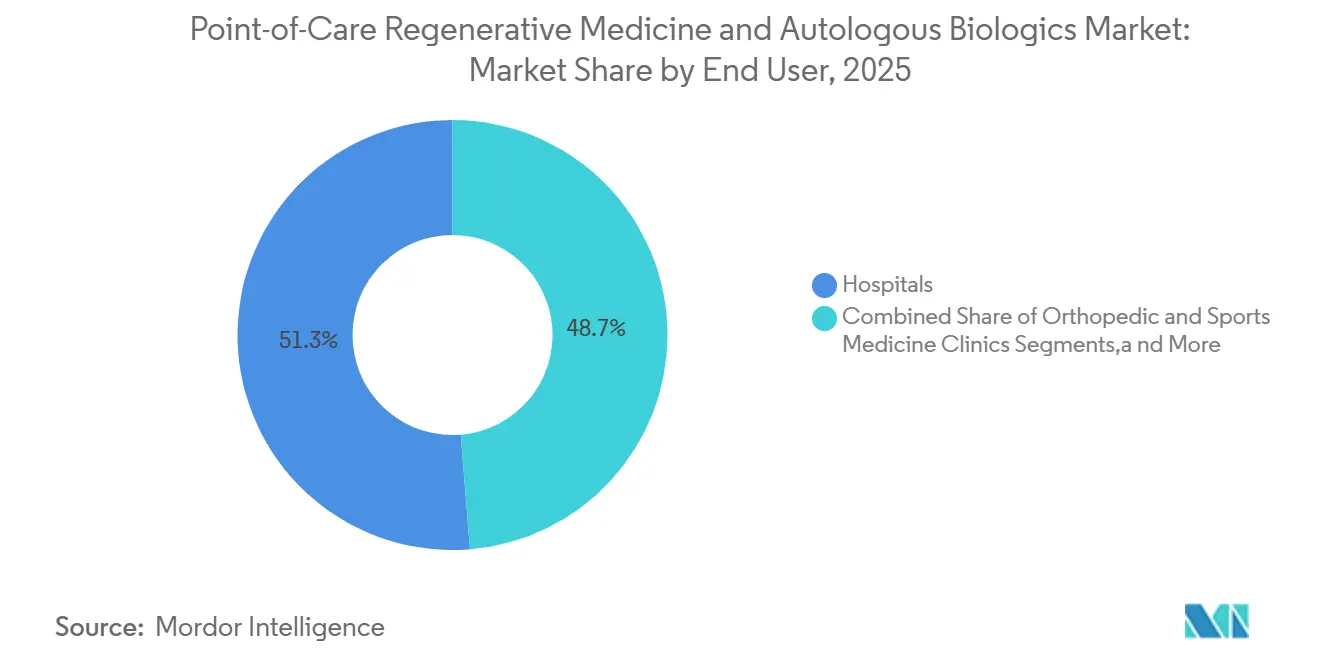

- By end user, hospitals represented 51.30% of revenue in 2025, while specialty and ambulatory surgery centers are projected to advance at 9.77% through 2031.

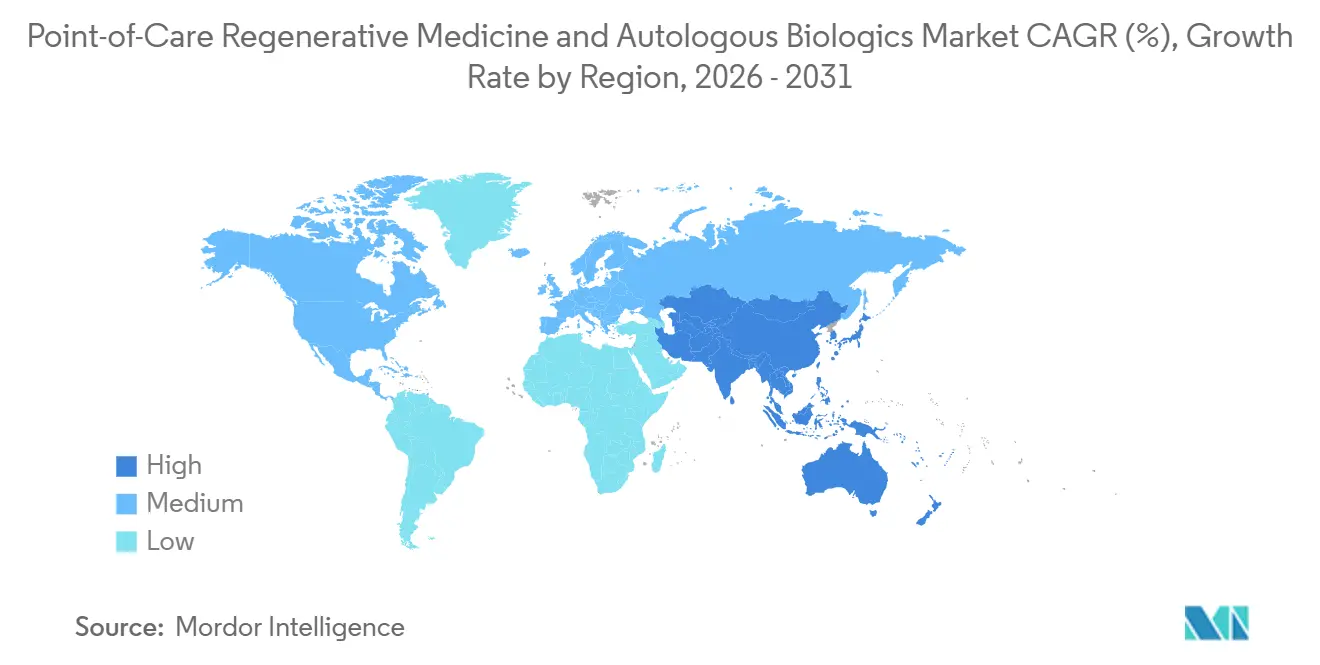

- By geography, North America captured 39.45% of revenue in 2025, while Asia-Pacific is projected to grow at 12.45% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Point-of-Care Regenerative Medicine and Autologous Biologics Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Growing demand for same-day orthobiologic procedures | +2.2% | Global, concentrated in North America and Western Europe | Medium term (2-4 years) |

| Rising shift toward closed-system point-of-care processing | +1.8% | Global, with early adoption in North America and rapid follow-through in Asia-Pacific | Medium term (2-4 years) |

| Expanding clinical use in orthopedics and sports medicine | +1.5% | North America and Europe, with strong uptake in Australia and South Korea | Long term (≥ 4 years) |

| Broader adoption in wound care and aesthetic medicine | +0.9% | North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| Reimbursement pull from outpatient and ASC settings | +1.3% | North America primarily, with emerging relevance in Europe | Short term (≤ 2 years) |

| Integration of digital workflow tracking and standardized kit protocols | +0.6% | North America and Europe, with spillover into Asia-Pacific and Middle East and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Same-Day Orthobiologic Procedures

The Point-of-Care Regenerative Medicine & Autologous Biologics Market is seeing stronger demand for same-day autologous treatments in orthopedic care. Hospitals and insurers are pressuring providers to reduce repeat visits and lower total episode costs, supporting single-session biologic use when workflows allow. A 2025 multicenter retrospective study published in the Journal of Experimental Orthopedics is expected to report a mean KOOS total improvement of 26.2 points at 20.5 months for one-stage minced cartilage autograft combined with PRP, strengthening the clinical case for a same-day model.[1]Vericel Corporation, “Vericel Announces FDA Approval of New State-of-the-Art Advanced Therapy Manufacturing Facility,” Vericel Investor Relations, investors.vcel.com Training infrastructure also supports adoption, as surgeons often standardize on the systems and preparation methods they first learn in practical settings.

Rising Shift Toward Closed-System Point-of-Care Processing

Closed-system centrifugation is becoming a baseline expectation in the Point-of-Care Regenerative Medicine & Autologous Biologics Market, especially in accredited outpatient settings. Providers increasingly prefer systems that keep blood or marrow within a controlled pathway, as contamination risk and handling variability have direct clinical and liability implications. EmCyte Corporation’s PurePRP SupraPhysiologic platform reflects this buyer preference, offering a fully closed circuit and more than 8x baseline platelet concentration through a double-spin method. Group purchasing organizations are accelerating this shift, as many hospital buyers now treat closed architecture as a procurement requirement rather than a premium option.

Expanding Clinical Use in Orthopedics and Sports Medicine

Orthopedics and sports medicine continue to provide the strongest clinical base for the Point-of-Care Regenerative Medicine & Autologous Biologics Market. This application area is projected to hold 37.45% of revenue in 2025, supported by growing use in knee osteoarthritis and related musculoskeletal conditions. A 2026 network meta-analysis indexed in PubMed, covering 56 randomized controlled trials and 5,251 patients, is expected to show that PRP formulation features, including leukocyte content and activation status, can materially affect functional outcomes in knee osteoarthritis.[2]Johnson & Johnson, “DePuy Synthes Enters Exclusive U.S., Canada and Australia Distribution Agreement for CGBIO’s NOVOSIS,” Johnson & Johnson Media Center, jnj.com Guidance published in EFORT Open Reviews in 2025 is also expected to show that formal orthobiologic recommendations remain concentrated in a limited number of musculoskeletal uses, creating a clinical gap and a product development opportunity.[3]U.S. Food and Drug Administration, “2025 Biological Device Application Approvals,” FDA Center for Biologics Evaluation and Research, fda.gov

Reimbursement Pull From Outpatient and ASC Settings

Reimbursement changes in outpatient care are giving the Point-of-Care Regenerative Medicine & Autologous Biologics Market a stronger near-term push in the United States. The CMS CY 2026 Hospital Outpatient Prospective Payment System and ASC Payment System Final Rule is expected to include a 2.6% payment rate increase and remove 285 primarily musculoskeletal procedures from the Inpatient-Only List, making them eligible for ASC-based reimbursement effective January 1, 2026. This change would expand the reimbursement pathway for orthobiologic procedures previously tied to inpatient episodes or broader bundled care settings. Section 4135 CAA, effective January 2025, is also expected to introduce separate Medicare payment for non-opioid biologics used as surgical supplies in ASC settings, improving the procedural case for autologous PRP and fibrin products in outpatient use.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Variable clinical evidence across indications and products | -1.2% | Global, with the strongest effect in United States and European payer markets | Long term (≥ 4 years) |

| Regulatory ambiguity around minimal manipulation and homologous use | -0.9% | North America and Europe, with secondary impact in Asia-Pacific | Medium term (2-4 years) |

| Physician skill dependence and procedure variability | -0.6% | Global | Medium term (2-4 years) |

| Under-reported reimbursement friction for multi-use kits and ancillaries | -0.5% | North America primarily, with secondary impact in Europe and Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Variable Clinical Evidence Across Indications and Products

Clinical evidence in the Point-of-Care Regenerative Medicine & Autologous Biologics Market varies widely across indications, preparation methods, and patient groups. The international guideline landscape remains limited and fragmented, reflecting an uneven evidence base across products and use cases. A 2025 randomized controlled trial found no long-term superiority of bone marrow aspirate concentrate over PRP in knee osteoarthritis, challenging the premium positioning of some higher-cost systems. When comparative efficacy remains unclear, formulary committees and payers prioritize cost control over premium adoption, creating price pressure for vendors without strong head-to-head clinical data.

Regulatory Ambiguity Around Minimal Manipulation and Homologous Use

Regulatory interpretation remains a key constraint in the Point-of-Care Regenerative Medicine & Autologous Biologics Market. In the United States, the FDA HCT/P framework under 21 CFR Part 1271 sets different expectations based on whether a product qualifies as minimally manipulated and is intended for homologous use. In Europe, Regulation 1394/2007 creates a stricter pathway for products such as enzymatically processed SVF, while mechanically processed systems may remain within a lower-burden route. This divergence influences product strategy, as workflows that fit one regulatory pathway in the United States may face a different commercialization burden in Europe.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: PRP Systems Anchor Revenue While Bone Marrow Gains Momentum

Platelet-rich plasma (PRP) systems are expected to hold 34.55% of the Point-of-Care Regenerative Medicine & Autologous Biologics Market share by product type in 2025, supported by broad adoption across orthopedics, wound care, aesthetics, and dentistry. No other product category offers a comparable procedural range across surgical and clinic-based settings. This versatility keeps PRP systems central to the market, particularly where providers require familiar, lower-complexity biologic workflows. The regulatory pipeline is also expected to remain active through 2025 and 2026, with FDA CBER approvals covering products such as the ENDORET Kit in October 2025 and the Precise Cell Concentration System in February 2026.

Bone marrow concentration systems are the fastest-growing product segment, with the Point-of-Care Regenerative Medicine & Autologous Biologics Market size for this segment projected to expand at an 11.02% CAGR through 2031. Demand is driven by spinal fusion augmentation and complex joint procedures, where providers seek higher progenitor cell concentrations than PRP alone can typically deliver. Adipose-derived cell processing systems are gaining traction in wound care and aesthetic medicine through closed, enzyme-free mechanical systems that preserve stromal tissue architecture. Platelet-rich fibrin (PRF) systems remain smaller in revenue terms but are becoming more relevant in dentistry and oral surgery, while ISO 13485-compliant manufacturing is now a baseline requirement in regulated markets.

By Application: Orthopedics Leads as Wound Care Accelerates

Orthopedics and sports medicine are expected to account for 37.45% of application revenue in 2025, making this the largest application area in the Point-of-Care Regenerative Medicine & Autologous Biologics Market. This leadership reflects strong procedure volumes in outpatient orthopedic clinics, where providers can use PRP, PRF, and bone marrow concentration within a single care episode. The segment also benefits from expanding musculoskeletal evidence, although protocol quality and standardization still vary by use case. Orthopedics remains the market’s core volume base due to provider familiarity and consistent case flow supporting repeated kit use.

Wound care is the fastest-growing application, with a projected 10.80% CAGR through 2031. This application benefits from a clearer pathway under CMS NCD 270.3, which links Medicare wound management coverage to devices with the relevant FDA clearance for that indication. This framework reduces reimbursement uncertainty compared with some orthopedic uses. Aesthetic medicine is also becoming a meaningful contributor through SVF-assisted fat grafting and exosome-enriched PRP protocols, especially in Germany, South Korea, and Australia, while dentistry and oral surgery continue to rely on PRF for guided tissue regeneration.

By End User: Hospitals Dominate as ASCs Broaden Their Scope

Hospitals are expected to represent 51.30% of end-user revenue in 2025, keeping them the largest care setting in the Point-of-Care Regenerative Medicine & Autologous Biologics Market. Their position is supported by use in bone marrow concentration, adipose processing, and complex orthobiologic procedures that require imaging guidance, anesthesia support, or multidisciplinary care. Hospital programs are increasingly managing autologous biologics as part of internal cost and supply decisions rather than isolated department purchases. This shift is significant because a single-visit autologous procedure with kit costs of USD 1,500 to USD 3,000 can replace multi-visit allograft protocols that cost several times more in total.

Specialty and ambulatory surgery centers (ASCs) are the fastest-growing end-user segment, with a projected 9.77% CAGR through 2031. Their growth is closely linked to the 2026 CMS expansion, which made 285 primarily musculoskeletal procedures eligible for ASC-based reimbursement. Orthopedic and sports medicine clinics remain the main engine for PRP adoption because they combine high case volumes with physician-led operating models that support kit differentiation and repeated procedural use. Academic and research centers continue to support evidence development for future payer decisions, while dental and aesthetic clinics remain niche channels tied to PRF use in implantology and adipose-derived systems in medical tourism markets such as South Korea, Thailand, and Turkey.

Geography Analysis

North America is expected to account for 39.45% of the Point-of-Care Regenerative Medicine & Autologous Biologics Market share in 2025, making it the largest regional block. The region benefits from high orthopedic procedure volumes, a mature ambulatory surgical center (ASC) base, and an active FDA clearance environment for autologous biologic systems. The CMS 2026 rule is also expected to expand the outpatient procedure base and add USD 450 million in Medicare ASC expenditures, supporting near-term demand for orthopedic and related biologic procedures. The United States remains the leading adoption market for premium closed-system PRP and bone marrow concentration platforms, while Canada and Mexico are advancing gradually through hospital procurement programs and cross-border technology transfer.

Europe remains strategically important in the Point-of-Care Regenerative Medicine & Autologous Biologics Market, although regulatory and reimbursement conditions remain complex. Germany and the United Kingdom lead regional adoption, while France is expanding PRP use in chronic wound care through newer hospital-based programs. The distinction between the EU advanced therapy medicinal product framework and the medical device route continues to favor mechanically processed autologous systems over enzymatically isolated SVF platforms. Italy and Spain support steady demand through private aesthetic medicine ecosystems, where adoption depends less on insurance coverage.

Asia-Pacific is the fastest-growing region, with the Point-of-Care Regenerative Medicine & Autologous Biologics Market size in this geography projected to expand at a CAGR of 12.45% through 2031. Japan has developed a structured regulatory pathway for autologous blood product procedures under its Regenerative Medicine Safety Act, supporting kit standardization while increasing compliance requirements. South Korea is expected to add momentum with Miracell’s April 2026 U.S. FDA 510(k) clearance for its SMART M-CELL system, while China and India remain the region’s largest volume-driven growth engines, and the Middle East, Africa, and South America contribute through hospital upgrades, private-pay aesthetic care, and medical tourism in major urban centers.

Competitive Landscape

The Point-of-Care Regenerative Medicine & Autologous Biologics Market is moderately fragmented, with no company holding more than a mid-teen share across all product lines. Large orthopedic platforms, including Stryker, Johnson & Johnson through DePuy Synthes, and Smith+Nephew, compete by integrating biologic systems into broader surgical and musculoskeletal care pathways. Specialized players, such as EmCyte Corporation and Regen Lab SA, differentiate through compact centrifuge design, shorter cycle times, and concentration consistency, which are critical in high-throughput clinic settings with limited laboratory infrastructure. In 2025 and 2026, companies are expected to prioritize distribution partnerships over building all commercial channels internally, with DePuy Synthes expected to expand this strategy in May 2026 through its exclusive distribution agreement with CGBIO for NOVOSIS in the United States, Canada, and Australia, following an earlier February 2025 arrangement across several Asian markets.

Mergers and acquisitions are expected to further influence the Point-of-Care Regenerative Medicine & Autologous Biologics Market. Smith+Nephew is expected to complete its acquisition of Integrity Orthopaedics in January 2026, adding the Tendon Seam rotator cuff repair system and strengthening its biologic augmentation position in shoulder repair. White-space opportunities remain strongest in cardiovascular and neurological point-of-care systems, adipose processing platforms with broader cleared claims, and digital workflow tools that verify biologic quality in real time. Patent activity around centrifugation profiles, closed-system valve design, and microfluidic separation is also increasing, particularly among Korean and Israeli developers.

Regulatory compliance is shaping competition in the Point-of-Care Regenerative Medicine & Autologous Biologics Market, as FDA 510(k) requirements and ISO 13485 certification create entry thresholds that smaller vendors may find difficult to meet. This barrier helps established manufacturers protect market access in a fragmented landscape. Companies adding digital traceability, including batch-level platelet concentration documentation, are likely to strengthen their position with hospital purchasing groups seeking better quality reporting. Ongoing FDA approvals expected across 2025 and 2026 are likely to increase system availability, support price competition in entry-level kits, and help premium closed platforms maintain stronger margins.

Point-of-Care Regenerative Medicine and Autologous Biologics Industry Leaders

Zimmer Biomet Holdings, Inc.

Stryker Corporation

Medtronic plc

B. Braun SE

Smith and Nephew plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: DePuy Synthes, a Johnson & Johnson company, signed an exclusive distribution agreement with CGBIO for NOVOSIS across the United States, Canada, and Australia, expanding its regenerative orthopedics portfolio.

- May 2026: Royal Biologics and Jellagen formed an exclusive partnership to commercialize Collagen Type Zero, a jellyfish-derived collagen biomaterial, across North American wound care and biologics markets.

- April 2026: Organogenesis Holdings Inc. completed its rolling Biologics License Application submission to the FDA for ReNu, a cryopreserved amniotic suspension allograft for symptomatic knee osteoarthritis.

- April 2026: Royal Biologics received FDA clearance for Fibrinet PRF Wound Matrix for managing exuding cutaneous wounds, including diabetic and venous ulcers.

- April 2026: Miracell, based in South Korea, obtained U.S. FDA 510(k) clearance for its SMART M-CELL system, covering PRP and bone marrow concentration in an integrated centrifuge-plus-kit system.

Global Point-of-Care Regenerative Medicine and Autologous Biologics Market Report Scope

As per the scope of the report, point-of-care regenerative medicine & autologous biologics refers to treatments where a patient's own (autologous) biological materials, such as blood or tissue, are processed and administered on-site during a single medical visit to stimulate healing, reduce inflammation, and repair damaged tissues or joints.

The point-of-care regenerative medicine and autologous biologics market is segmented by product type, application, end user, and geography. By product type, the market includes platelet-rich plasma systems, bone marrow concentration systems, adipose-derived cell processing systems, platelet-rich fibrin systems, and other autologous biologic concentration systems. By application, the market is segmented into orthopedics and sports medicine, wound care, aesthetic medicine, dentistry and oral surgery, cardiovascular and vascular applications, and neurology and other applications. By end user, the market is segmented into hospitals, specialty and ambulatory surgery centers, orthopedic and sports medicine clinics, aesthetic clinics, dental clinics, and academic and research centers. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers market sizes and forecasts in terms of value (USD) for the above segments.

| Platelet-Rich Plasma Systems |

| Bone Marrow Concentration Systems |

| Adipose-Derived Cell Processing Systems |

| Platelet-Rich Fibrin Systems |

| Other Autologous Biologic Concentration Systems |

| Orthopedics and Sports Medicine |

| Wound Care |

| Aesthetic Medicine |

| Dentistry and Oral Surgery |

| Cardiovascular and Vascular Applications |

| Neurology and Other Applications |

| Hospitals |

| Specialty and Ambulatory Surgery Centers |

| Orthopedic and Sports Medicine Clinics |

| Aesthetic Clinics |

| Dental Clinics |

| Academic and Research Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Platelet-Rich Plasma Systems | |

| Bone Marrow Concentration Systems | ||

| Adipose-Derived Cell Processing Systems | ||

| Platelet-Rich Fibrin Systems | ||

| Other Autologous Biologic Concentration Systems | ||

| By Application | Orthopedics and Sports Medicine | |

| Wound Care | ||

| Aesthetic Medicine | ||

| Dentistry and Oral Surgery | ||

| Cardiovascular and Vascular Applications | ||

| Neurology and Other Applications | ||

| By End User | Hospitals | |

| Specialty and Ambulatory Surgery Centers | ||

| Orthopedic and Sports Medicine Clinics | ||

| Aesthetic Clinics | ||

| Dental Clinics | ||

| Academic and Research Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2026 size of point-of-care regenerative medicine and autologous biologics?

The sector stands at USD 18.97 billion in 2026 and is projected to reach USD 28.61 billion by 2031 at a 8.56% CAGR.

Which product type leads revenue generation?

Platelet-rich plasma systems led product revenue with 34.55% in 2025 because they are used across orthopedics, wound care, aesthetics, and dentistry.

Which application is growing the fastest through 2031?

Wound care is the fastest-growing application with a projected 10.80% CAGR, supported by a clearer reimbursement path tied to indication-specific clearance.

Why are ambulatory surgery centers becoming more important?

Specialty and ambulatory surgery centers are expected to grow at 9.77% CAGR as 2026 CMS changes expanded outpatient reimbursement for 285 primarily musculoskeletal procedures.

Which region leads today and which one is growing the fastest?

North America led with 39.45% of revenue in 2025, while Asia-Pacific is projected to post the fastest growth at 12.45% CAGR through 2031.

What is the main barrier to wider adoption?

The biggest constraint remains uneven clinical evidence across indications and products, which affects payer confidence, formulary decisions, and premium pricing support.

Page last updated on: