Point-of-Care Middleware Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.57 Billion |

| Market Size (2031) | USD 1.06 Billion |

| Growth Rate (2026 - 2031) | 13.35% CAGR |

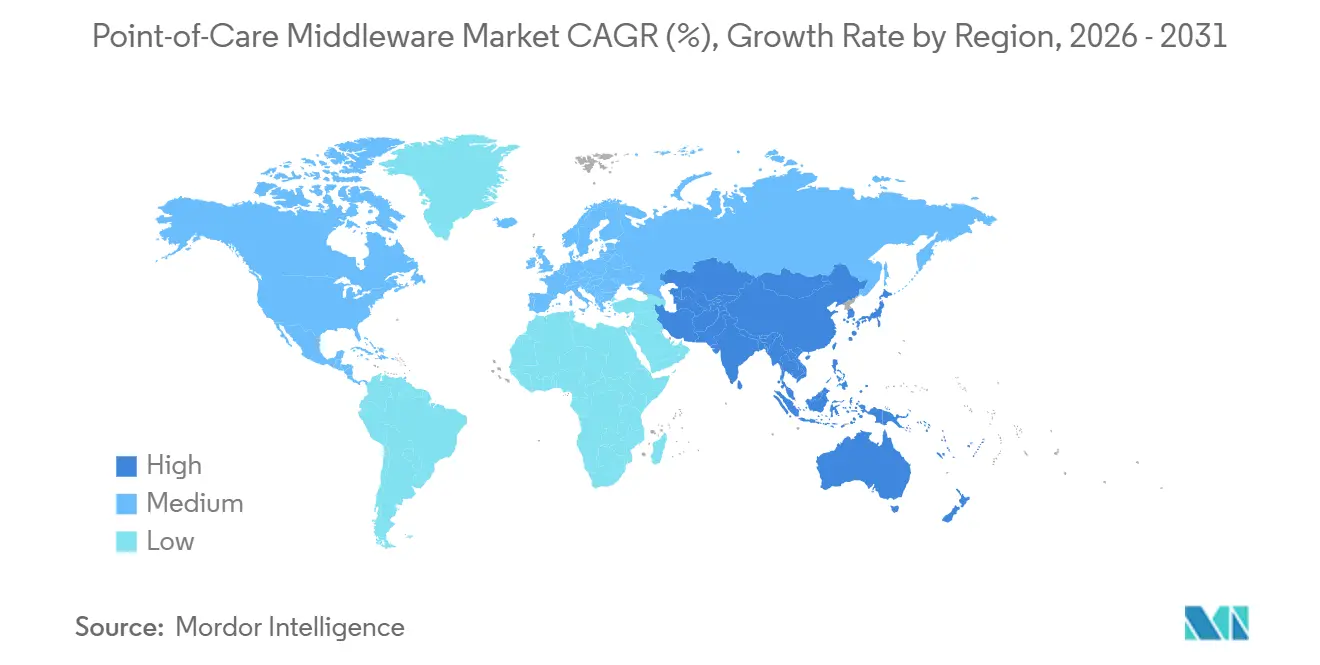

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

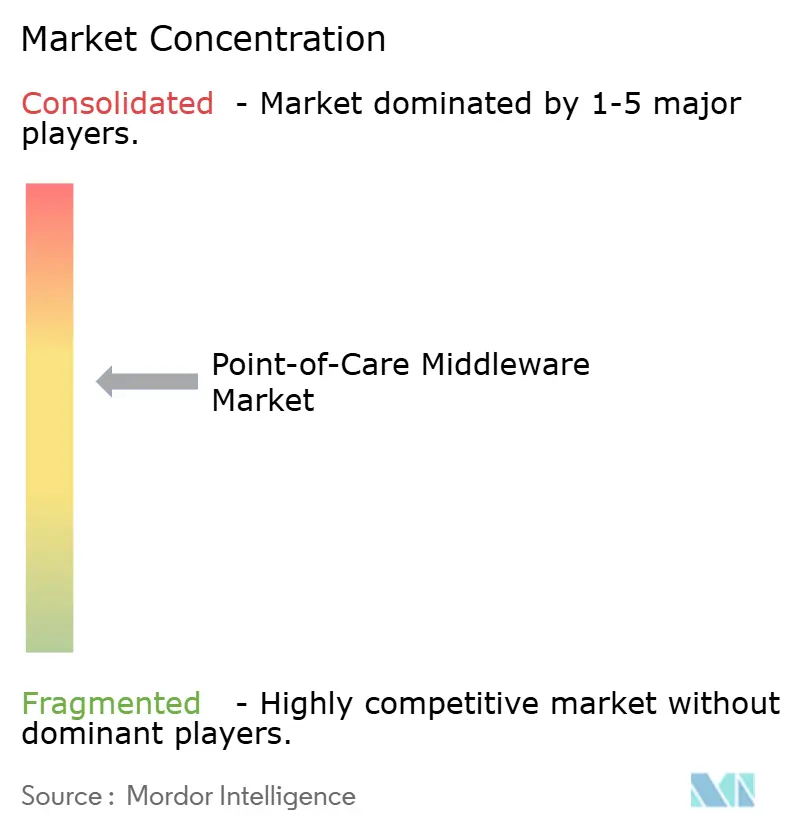

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Point-of-Care Middleware Market Analysis by Mordor Intelligence

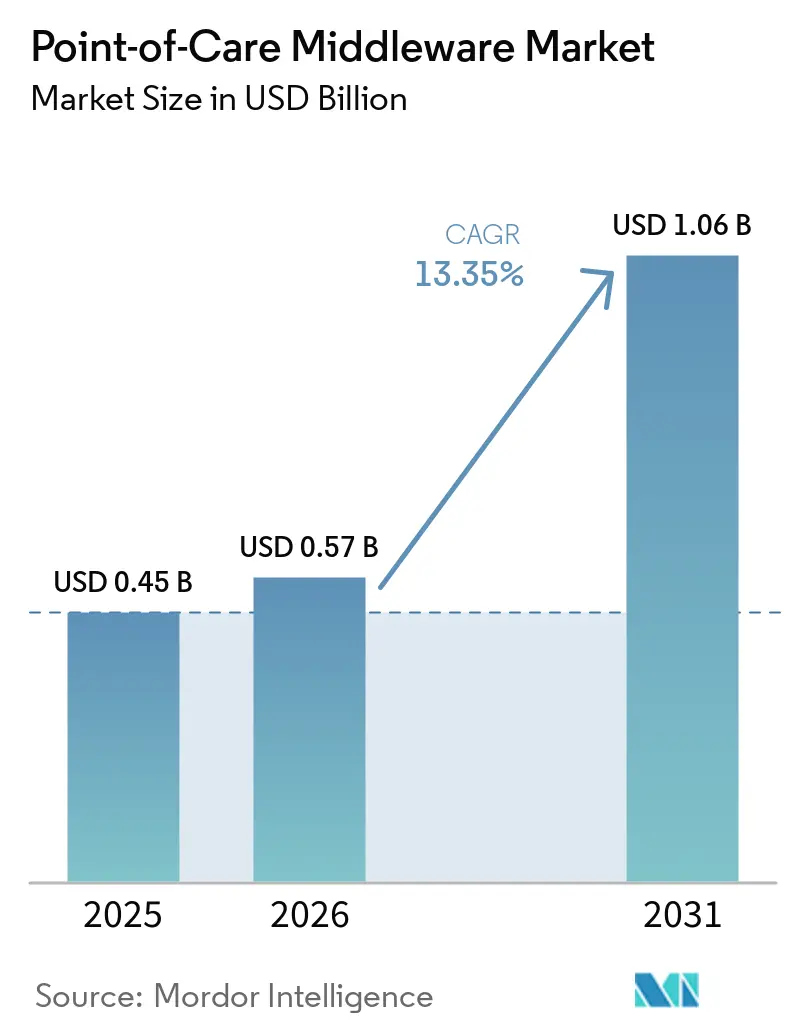

The Point-of-Care Middleware Market size was valued at USD 0.45 billion in 2025 and is estimated to grow from USD 0.57 billion in 2026 to reach USD 1.06 billion by 2031, at a CAGR of 13.35% during the forecast period (2026-2031).

The point-of-care middleware market is gaining from the steady shift of diagnostic activity away from central laboratories and into emergency rooms, clinics, community sites, and other near-patient settings where result flow must remain controlled and auditable. Middleware now sits at the center of this operating model because it connects instruments with EHR and LIS environments, supports governance across multiple sites, and lowers the operational risks that come with manual result entry. The point-of-care middleware market also benefits from strong vendor retention because once interfaces are validated and mapped into institutional workflows, replacing the software becomes time-consuming and disruptive for the customer. Regulatory pressure is also strengthening demand, as ISO 15189:2022 has widened accreditation expectations for POCT traceability and the FDA’s 2026 cybersecurity guidance has raised software and documentation requirements for connected products. Even with high interface costs, legacy firmware variation, and rising security obligations, the point-of-care middleware market is moving from departmental software toward critical infrastructure for distributed healthcare delivery.

Key Report Takeaways

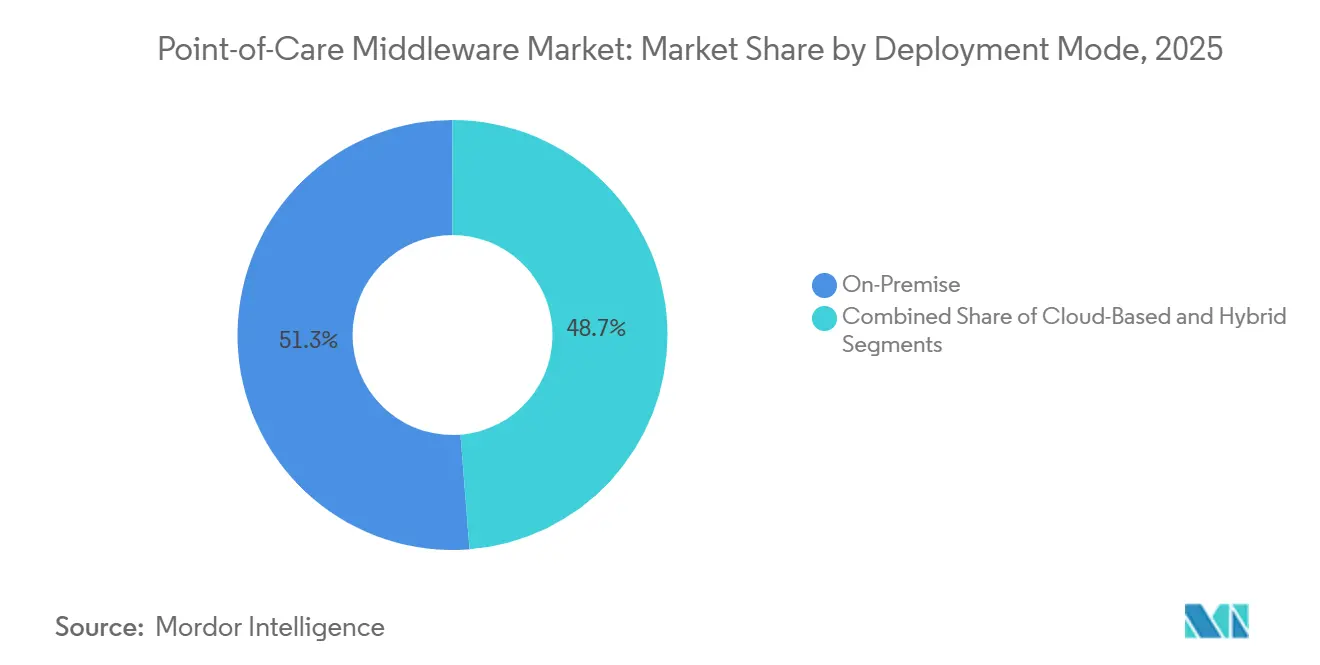

- By deployment mode, on-premise held 51.26% share of the point-of-care middleware market size in 2025, while cloud-based deployment is projected to expand at 15.67% CAGR through 2031.

- By application, glucose monitoring held 32.02% of the point-of-care middleware market share in 2025, while infectious disease device connectivity is projected to grow at 15.75% CAGR through 2031.

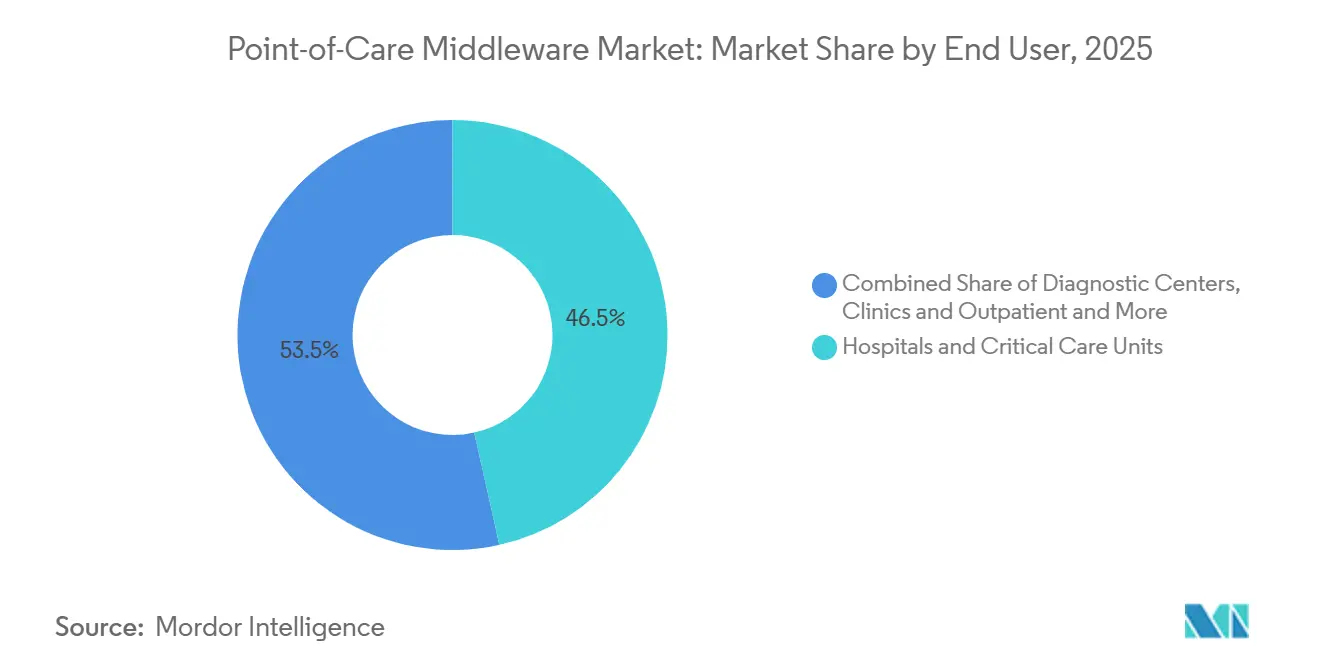

- By end user, hospitals and critical care units accounted for 46.51% of revenue in 2025, while diagnostic centers are forecast to advance at 14.98% CAGR through 2031.

- By geography, North America led with 38.47% share in 2025, while Asia-Pacific is expected to record a 15.13% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Point-of-Care Middleware Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Real-Time POCT To EHR And LIS Integration | +3.2% | Global, with highest intensity in North America and Europe | Short term (≤ 2 years) |

| Cloud-Based Fleet Management | +2.8% | North America and Europe, with early APAC adoption | Medium term (2-4 years) |

| Operator Competency And QC Automation | +2.1% | Global | Medium term (2-4 years) |

| Decentralized Testing Network Expansion | +2.5% | APAC, MEA, South America, with incremental North America gains | Medium term (2-4 years) |

| Hospital-At-Home Connectivity Needs | +1.6% | North America, Europe, Australia | Long term (≥ 4 years) |

| ISO 15189:2022 Traceability Pressure | +1.8% | Global, with highest relevance in ILAC-accredited markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Real-time POCT to EHR/LIS Integration Eliminates Clinical Data Latency

The point-of-care middleware market continues to draw its strongest support from the need to replace manual POCT transcription with automated and bidirectional result exchange across instruments, EHR systems, and laboratory platforms. That shift matters because transcription delays and mismatched patient records can weaken the clinical value of near-patient testing in high-volume care settings. Abbott stated that its point-of-care data management environment captures 225 million test results each year and supports more than 80,000 meters and devices that run patient tests every day across its connected base.

Once a health system has mapped POCT flows to specific HL7 v2.x or FHIR R4 message structures, a move to another middleware vendor usually requires broad interface revalidation across departments and sites. That process creates durable switching costs, which is why the point-of-care middleware market tends to show strong incumbent retention even when hospitals review technology stacks. The same integration pressure is reinforced by U.S. interoperability policy, which keeps compliant data exchange close to the center of purchasing decisions for connected diagnostic software.

Cloud-based Fleet Management Reshapes POC Economics at Scale

The point-of-care middleware market is also being reshaped by the limits of older on-premise architectures when health systems manage large fleets of devices across hospitals, clinics, and off-site locations. TELCOR reported that its QML middleware connects more than 2,700 hospitals and ambulatory locations, showing how centralized management has become a practical requirement in multi-site POCT operations[1]TELCOR, “TELCOR POC Device Connectivity Updates, Q3 2025,” TELCOR, telcor.com. Siemens Healthineers stated that its POCcelerator platform connects more than 250 POCT devices from over 70 manufacturers, while its Ci module provides KPI-level visibility into device performance, QC status, and operator activity.

These capabilities matter because cloud delivery lets vendors update device drivers, quality rules, and compliance settings across all connected sites at once rather than site by site. The point-of-care middleware market therefore gains not only from connectivity demand, but also from the operational savings that come from centralized oversight, better operator control, lower waste, and fewer local server burdens. Operator competency and QC automation fit directly into this shift because centralized platforms can apply common access rules, quiz delivery, and audit documentation without requiring local manual processes at each site.

Decentralized Testing Network Expansion Opens New Connectivity Surface

The point-of-care middleware market is expanding with the broader movement of testing into rural emergency departments, community clinics, pharmacy settings, and other non-laboratory environments. Saskatchewan Health Authority announced in November 2025 that it was extending its POCT program to 4 additional rural emergency departments, and it said the program had already prevented 214 potential service disruptions since launch in 2023. That type of expansion increases the number of care sites, device types, operators, and network conditions that must be managed under one governance structure. A peer-reviewed review of Australia’s decentralized COVID-19 molecular POCT network found that middleware upgrades were critical for preserving transmission integrity when testing guidelines changed during the program.

Roche Diagnostics also stated in 2025 that direct POCT to laboratory connectivity supports traceability, reduces transcription errors, and contributes to lower hospitalization and length-of-stay burdens. As this footprint spreads further into home-linked and community-led pathways, the point-of-care middleware market gains new demand from customers that need thin-client deployment, multi-vendor normalization, and reliable oversight outside traditional hospital infrastructure.

ISO 15189:2022 Traceability Requirements Raise the Accreditation Floor

The point-of-care middleware market is receiving additional support from accreditation pressure after ISO 15189:2022 absorbed the POCT requirements that were previously handled under ISO 22870. A 2024 review in Accreditation and Quality Assurance explained that the new edition established a unified standard for medical laboratory competence that explicitly covers point-of-care testing activity. The three-year transition period pushed many accreditation-linked buying decisions into 2024 and 2025, especially in markets where laboratory quality systems are actively enforced. The standard now places stronger weight on traceability, external quality comparability, continuity planning, operator competency records, and audit-ready documentation, all of which are difficult to manage with fragmented manual workflows.

Radiometer stated that AQURE 2.7 supports consumables and QC traceability, automated Westgard Rules enforcement, and Active Directory-linked operator management, which shows how product design is moving closer to accreditation workflow needs. This means the point-of-care middleware market is being pulled by quality governance needs as much as by pure connectivity needs, and that tends to favor vendors with stronger documentation depth and validated workflow controls.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Deployment And Interface Costs | -1.2% | Global, most acute in public health systems and MEA | Medium term (2-4 years) |

| Cybersecurity And Data-Privacy Exposure | -0.9% | Global, especially North America and Europe | Short term (≤ 2 years) |

| Legacy Device Firmware Fragmentation | -0.8% | Global, most acute in developing markets | Long term (≥ 4 years) |

| SBOM And Patch-Validation Burden | -0.6% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Deployment and Interface Costs Constrain Broad Market Penetration

The point-of-care middleware market still faces a meaningful adoption barrier because interface development between middleware, POCT devices, LIS systems, and EHR environments remains technically demanding and expensive. In large multi-vendor hospital environments, upfront interface and validation costs can move into six figures, especially when each device type needs separate testing, documentation, and workflow approval. The FDA’s final cybersecurity guidance from February 2026 adds new requirements around SBOM documentation, patch validation planning, and evidence of penetration testing for connected medical devices.

Those obligations raise engineering and implementation costs for vendors, and part of that burden is passed on to customers during deployment and support. The point-of-care middleware market is also affected by bundling behavior from major IVD manufacturers, which often makes open-platform connectivity to competing instruments more expensive for independent diagnostic operators. Public health systems in MEA and South America are more exposed to this issue because procurement budgets often prioritize analyzers and consumables ahead of digital infrastructure, even when the governance case for middleware is clear.

Cybersecurity and Data-Privacy Exposure Introduces Deployment Risk

The point-of-care middleware market carries added deployment risk because the software sits between sensitive patient data, connected instruments, and institutional networks. In July 2025, the FDA warned about cybersecurity vulnerabilities in certain connected patient monitors from Contec and Epsimed, including the possibility of unauthorized access and data exposure outside the healthcare environment. A 2025 security analysis published in Frontiers in the Internet of Things found that companion middleware applications in medical IoT environments could expose patient data to interception and extraction risks if controls are weak.

In Europe, software that qualifies as in vitro diagnostic medical device software under IVDR 2017/746 faces conformity assessment requirements, which adds another layer of work for vendors that want regional access. The point-of-care middleware market therefore demands sustained investment in encryption, role-based access control, patch governance, and breach response readiness. Smaller vendors feel this pressure most because they must absorb security spending while also supporting product updates for heterogeneous device fleets and older firmware environments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Mode: Cloud Migration Accelerates Despite On-Premise Installed-Base Dominance

On-premise deployment held 51.26% share of the point-of-care middleware market size in 2025, reflecting the large base of hospital installations that were already built around local servers, established IT controls, and data residency preferences. Many hospitals kept these environments because security policy, procurement history, and internal support models were already aligned with locally hosted software. Cloud-based deployment is projected to grow at 15.67% CAGR through 2031, showing that the fastest momentum is now moving toward centrally managed environments for distributed testing networks. That growth is tied to the rising need to support multiple facilities without maintaining local middleware infrastructure at every care site. Hybrid deployment remains the smallest category by share, yet it is drawing attention from organizations that want cloud analytics and centralized management without moving all patient identifiers off local systems.

In practical terms, cloud delivery gives vendors a simpler path to update device drivers, roll out compliance changes, and extend fleet visibility across large networks from one control point. That operating model becomes more attractive as organizations add outpatient clinics, urgent care settings, and community locations that would otherwise need separate server maintenance and local update cycles. Abbott positions AegisPOC as a web-based open platform with secure data center hosting, while Clinisys offers an Orchard point-of-Care SaaS option that supports customers seeking lighter infrastructure demands. Abbott’s Australia material also highlights ISO 27001 certification, and that kind of credential is becoming a practical filter in tenders where buyers look for tested governance rather than feature lists alone. Within the point-of-care middleware industry, this leaves on-premise systems in a strong installed position while cloud models gather new demand from customers that value scale, speed of updates, and lower operational overhead.

The point-of-care middleware market is therefore not moving through a simple replacement cycle, but through a gradual shift in what customers expect middleware to manage across space, staff, and compliance tasks. Hybrid models also remain relevant because they offer a middle path for institutions that must respect local governance requirements while still wanting shared analytics and remote fleet visibility. That keeps deployment choice tied closely to customer operating model rather than to a single universal architecture preference. The point-of-care middleware market will likely keep both models active through the forecast period because the installed base changes slowly and the new buying pipeline is more cloud oriented.

By Application: Glucose Monitoring Anchors Base Demand as Infectious Disease Testing Accelerates

Glucose monitoring held 32.02% of the point-of-care middleware market share in 2025, supported by the long-established base of blood glucose meters and related workflows in hospitals and critical care settings. This application remains central because glucose testing is frequent, operationally sensitive, and tightly linked to medication reconciliation, insulin dosing, and patient safety controls. Growth here is increasingly tied to middleware refresh cycles rather than to first-time device placement, as providers move away from older interfaces and toward real-time exchange with current EHR environments. Infectious disease device connectivity is projected to grow at 15.75% CAGR through 2031, making it the fastest-expanding application as molecular and rapid tests continue to spread into ambulatory and community settings. The point-of-care middleware market benefits from this shift because infectious disease testing often brings more varied instrument mixes, more frequent protocol changes, and a stronger need for normalized result handling across sites.

Roche received FDA 510(k) clearance and CLIA waiver in 2025 for a 15-minute cobas liat Bordetella PCR test, and that kind of launch adds another connected device type to distributed testing environments that must feed results into broader care pathways[2]Roche Diagnostics, “2025 in Review, Advancing Diagnostics through Total Integrated Solutions,” Roche Diagnostics, diagnostics.roche.com. Coagulation monitoring and cardiometabolic testing also remain important because they are moving deeper into emergency, procedural, and acute care workflows where structured data routing is needed for timely decisions. Hematology-related demand is supported by the wider role of blood-gas and hemostasis POCT in critical care, which increases the number of result streams that middleware must monitor.

Cancer marker testing is still early, but the direction matters because newer immunoassay panels will need configurable rule logic when they enter oncology and cardiology workflows outside central labs. Urinalysis demand appears more stable, yet it still supports the point-of-care middleware market through documentation needs tied to stewardship programs, nephrology monitoring, and audit-ready result capture. Within the point-of-care middleware industry, application breadth matters because vendors that can normalize many result types without heavy customization are better positioned in multi-vendor settings. That is why installed glucose workflows still anchor revenue while infectious disease connectivity drives a larger share of incremental growth.

By End User: Hospitals Lead While Diagnostic Centers Accelerate Fastest

Hospitals and critical care units accounted for 46.51% of end-user revenue in 2025, which made them the largest buyer group within the point-of-care middleware market. Their lead reflects both the high concentration of POCT devices in acute care settings and the stronger compliance burden that pushes hospitals toward formalized quality and operator oversight. Large tertiary centers often run dense fleets across emergency departments, ICUs, operating areas, and specialized units, which turns middleware into a central coordination layer rather than a back-office add-on. In these environments, the software must handle device configuration, user authorization, QC scheduling, exception handling, and result routing at the same time. Accreditation pressure reinforces this position because documented QC trails and operator competency records are difficult to sustain manually at hospital scale.

Diagnostic centers are projected to grow at 14.98% CAGR through 2031, making them the fastest-growing end-user segment in the point-of-care middleware market. This momentum reflects the need of independent and chain-based laboratory networks to manage multi-vendor POCT activity under a common governance model without building the same internal IT depth found in large hospitals. Clinics and outpatient settings remain comparatively underserved because smaller practices often lack dedicated support teams for interface validation, policy maintenance, and staff training. That gap creates room for vendors that can offer pre-configured deployment, automated access control, and self-service onboarding without large professional services demands. Clinisys states that its Orchard point-of-care module supports compliance quiz delivery and operator tracking, which shows how workflow automation is becoming a practical adoption tool in smaller organizations.

The point-of-care middleware market gains from this pattern because growth is no longer limited to major hospital systems. The broader point is that end-user demand is separating into 2 clear tracks, with hospitals buying for complexity management and diagnostic centers buying for standardization across expanding networks. Both tracks still reward vendors that reduce manual oversight and make compliance easier to sustain. As a result, the point-of-care middleware industry is widening its customer base without weakening the central role of acute care institutions.

Geography Analysis

North America held 38.47% of the point-of-care middleware market share in 2025, making it the largest regional cluster by revenue. The region’s lead came from high POCT device density, mature EHR penetration, and a policy environment where interoperability, accreditation, and cybersecurity all influence software buying decisions. Abbott states that its point-of-care data management platform connects more than 50% of U.S. hospitals, which shows how deep the installed base has become in the region. Canada is also contributing to demand, with Saskatchewan Health Authority stating in late 2025 that its POCT program had expanded to 14 locations and had prevented 214 potential emergency department service disruptions[3]Saskatchewan Health Authority, “Point of Care Testing Program to Be Introduced to Kipling and Three Other Communities,” Saskatchewan Health Authority, saskhealthauthority.ca. Mexico remains at an earlier stage, but hospital digitization and cross-system connectivity needs still support a gradual expansion path for the point-of-care middleware market across urban care networks. The FDA’s 2026 cybersecurity guidance and CLIA-linked oversight help keep middleware spending visible on capital agendas even when provider budgets tighten.

Asia-Pacific is projected to grow at 15.13% CAGR through 2031, which makes it the fastest-growing regional segment in the point-of-care middleware market. Australia offers a clear example of distributed demand, as the government-funded Aboriginal and Torres Strait Islander COVID-19 POC Testing Program operated across 105 clinics, performed 72,624 tests, and recorded a median transmission time of 1.4 hours, with middleware upgrades cited as important when testing rules changed. China and India are also expanding primary care and community testing capacity, which creates more sites that need controlled data flow, operator management, and device traceability. Japan and South Korea add premium demand because hospitals in those systems place higher value on documented quality management and structured data exchange. This leaves Asia-Pacific as the region where volume expansion and governance needs are advancing together rather than separately.

Europe remains a major regional block because Germany, the United Kingdom, and France continue to enforce accreditation and regulated software requirements that make middleware purchases harder to defer. ISO 15189:2022 has widened the traceability and documentation case for POCT oversight, while IVDR 2017/746 keeps qualifying software within a more formal regulatory frame. The Middle East and Africa region is earlier in adoption, yet GCC countries such as Saudi Arabia and the UAE are pushing hospital digitization under national transformation programs that support future middleware uptake. South Africa remains the most developed MEA market because private hospital groups are more active users of accreditation-aligned quality systems. Kenya’s PEPFAR-funded Diagnostic Network Optimisation initiative reduced HIV testing turnaround time from 7 days to 2 days across a decentralized referral network, which helps demonstrate the practical value of connected diagnostic oversight in resource-limited settings. South America, led by Brazil and Argentina, is still developing through private hospital and diagnostic chain adoption, while public procurement remains more exposed to budget timing and infrastructure trade-offs.

Competitive Landscape

The point-of-care middleware market remains moderately consolidated, with Abbott, Siemens Healthineers, Roche, and Radiometer holding strong positions because they bundle middleware with instrument portfolios that already sit inside hospital workflows. That structure gives device manufacturers a first look in many connectivity evaluations because customers often begin with the vendor already supplying a large share of their POCT hardware. Abbott’s installed presence in U.S. hospitals illustrates how this device-led relationship can shape middleware renewal and expansion decisions over time. At the same time, specialist vendors such as TELCOR, Relaymed, Clinisys, and Werfen remain relevant because many health systems operate mixed fleets and need broader multi-vendor support than a single-device ecosystem can provide. TELCOR stated in February 2026 that its platform connected more than 160 device types across more than 2,700 hospitals, which shows why device breadth is still one of the clearest competitive advantages for independent players.

Strategic moves in the point-of-care middleware market are increasingly tied to workflow depth and quality intelligence rather than to basic connectivity alone. Radiometer’s AQURE 2.7 added a Peer Quality Control module in 2025 that supports QC benchmarking against a global peer group and monthly traceability reporting, which extends the product toward accreditation analytics. Abbott continues to position AegisPOC as an open and web-based platform, while Clinisys is leaning into SaaS delivery and compliance workflow support for customers with fewer internal IT resources. Siemens Healthineers is also moving beyond simple connection management by emphasizing fleet visibility, KPI monitoring, and support for broad device interoperability through POCcelerator. These moves show that vendors are trying to strengthen their role in quality management, operating efficiency, and enterprise oversight rather than competing on interface counts alone.

Cybersecurity credentialing is becoming another clear line of separation in the point-of-care middleware market. The FDA’s February 2026 final guidance has effectively raised the product floor by requiring stronger evidence around secure development, SBOM readiness, and patch validation for connected medical devices. Abbott’s ISO 27001 positioning supports vendor qualification in tenders where buyers now look for security process maturity as part of core product evaluation. European IVDR conformity assessment adds another barrier for vendors that lack the resources to support formal software qualification and documentation at regional scale. Smaller regional suppliers therefore face pressure from both sides, with rising compliance costs on one side and bundled competition from large IVD manufacturers on the other. This keeps the point-of-care middleware market active and competitive, but it also points to further consolidation as niche vendors seek scale, partnerships, or acquisition pathways during the forecast period.

Point-of-Care Middleware Industry Leaders

Danaher Corporation (Radiometer Medical ApS)

Siemens Healthineers AG

F. Hoffmann-La Roche Ltd.

Abbott

TELCOR Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Labcorp and Epic integrated Labcorp's diagnostic tests into Epic's Aura platform, enabling U.S. clinicians to order tests and view results directly in the EHR without manual steps. In 2025, Labcorp conducted over 750 million tests globally. This builds on their earlier work with Invitae, streamlining diagnostic workflows through middleware.

- February 2026: The U.S. FDA issued new cybersecurity rules for medical devices, requiring SBOM documentation, patch-validation plans, and penetration testing proof for internet-connected devices, including POC middleware. Non-compliant premarket submissions will now be rejected, raising product standards in the market.

Global Point-of-Care Middleware Market Report Scope

As per the scope of the report, point-of-care middleware is software that acts as an intermediary layer between various medical devices, electronic health records (EHR), and clinical applications at the point of care. It facilitates seamless data exchange, integration, and communication among heterogeneous systems, enabling healthcare providers to access, share, and analyze patient information quickly and efficiently during clinical encounters.

The segmentation for the point-of-care middleware market is categorized by deployment mode, application, end user, and geography. By deployment mode, the market is divided into cloud-based, on-premise, and hybrid. By application, it includes glucose monitoring, infectious disease devices, coagulation monitoring, urinalysis, cardiometabolic monitoring, cancer markers, hematology, and other applications. By end user, the market is segmented into hospitals and critical care units, diagnostic centers, clinics and outpatient, and other end users. By geography, the market covers North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Cloud-Based |

| On-Premise |

| Hybrid |

| Glucose Monitoring |

| Infectious Disease Devices |

| Coagulation Monitoring |

| Urinalysis |

| Cardiometabolic Monitoring |

| Cancer Markers |

| Hematology |

| Other Applications |

| Hospitals and Critical Care Units |

| Diagnostic Centers |

| Clinics and Outpatient |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Deployment Mode | Cloud-Based | |

| On-Premise | ||

| Hybrid | ||

| By Application | Glucose Monitoring | |

| Infectious Disease Devices | ||

| Coagulation Monitoring | ||

| Urinalysis | ||

| Cardiometabolic Monitoring | ||

| Cancer Markers | ||

| Hematology | ||

| Other Applications | ||

| By End User | Hospitals and Critical Care Units | |

| Diagnostic Centers | ||

| Clinics and Outpatient | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is driving growth in point-of-care middleware through 2031?

Growth is being supported by the shift of testing into decentralized care settings, stronger integration needs between POCT devices and EHR or LIS platforms, and accreditation and cybersecurity requirements that make structured oversight harder to postpone.

How large is the point-of-care middleware space expected to become by 2031?

The point-of-care middleware market is forecast to reach USD 1.06 billion by 2031 from USD 0.57 billion in 2026, with a 13.35% CAGR over 2026 to 2031.

Which deployment model is growing the fastest in point-of-care middleware?

Cloud-based deployment is growing the fastest at 15.67% CAGR through 2031, even though on-premise systems still held the largest share at 51.26% in 2025 because of installed infrastructure and internal IT policies.

Which application area contributes the most demand today?

Glucose monitoring remained the largest application in 2025 with a 32.02% share, mainly because hospitals already run a large installed base of glucose devices that need reliable result routing and documentation.

Which end users are expanding fastest?

Diagnostic centers are expected to record the fastest growth at 14.98% CAGR through 2031, as independent and chain operators standardize oversight across multi-vendor testing environments.

Which region leads and which region is growing fastest?

North America led in 2025 with a 38.47% share, while Asia-Pacific is projected to grow the fastest at 15.13% CAGR through 2031 because of primary care expansion and wider use of distributed testing models.

Page last updated on: