Podiatry Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

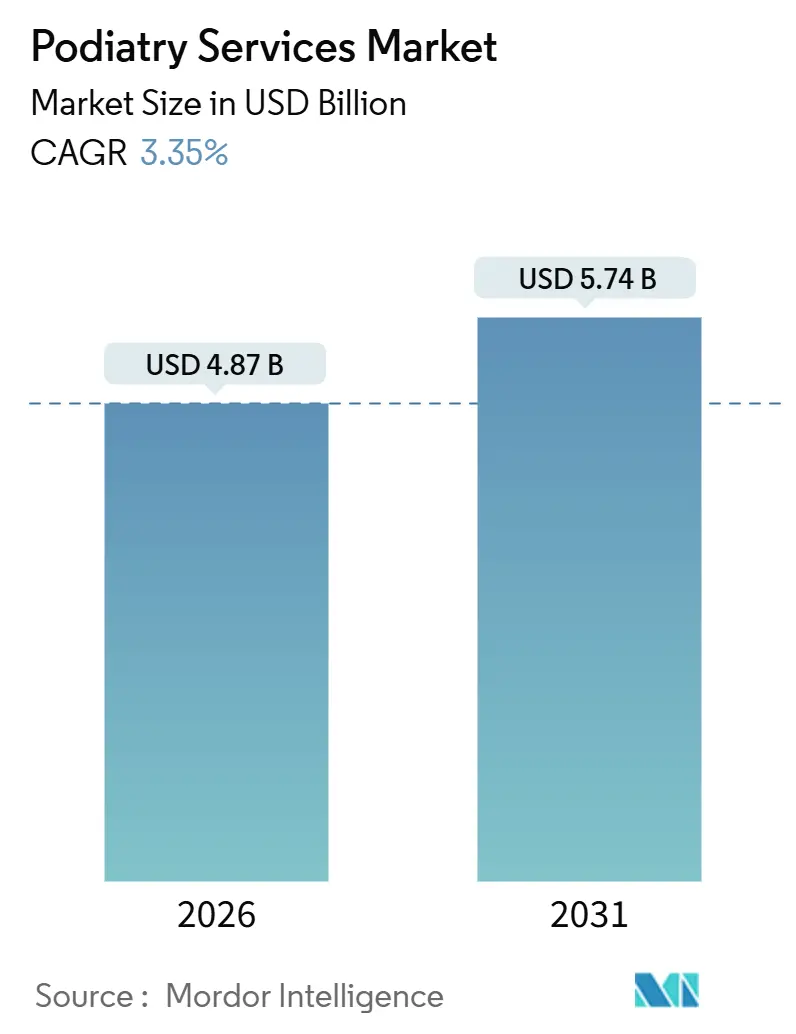

| Market Size (2026) | USD 4.87 Billion |

| Market Size (2031) | USD 5.74 Billion |

| Growth Rate (2026 - 2031) | 3.35% CAGR |

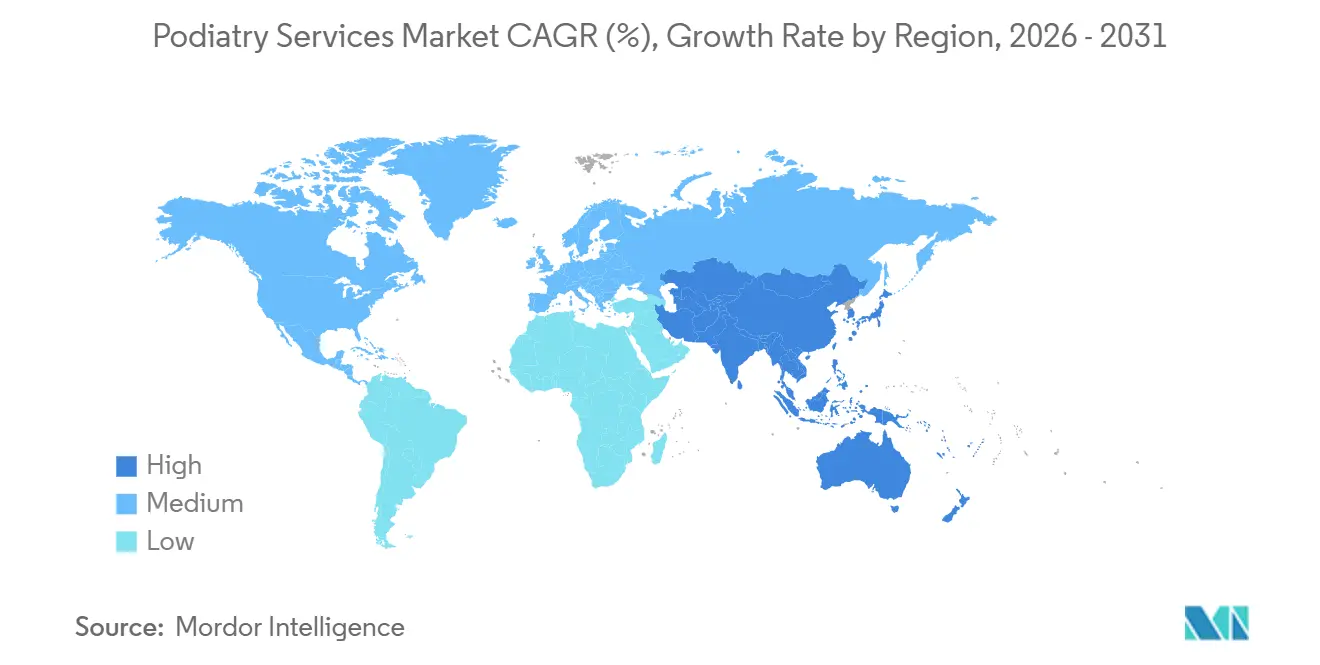

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Podiatry Services Market Analysis by Mordor Intelligence

The Podiatry Services Market size is estimated at USD 4.87 billion in 2026, and is expected to reach USD 5.74 billion by 2031, at a CAGR of 3.35% during the forecast period (2026-2031).

Robust demand comes from diabetes-related foot complications, an aging population with mobility disorders, and private equity consolidation that is knitting solo clinics into regional networks. Providers that integrate 3D-printed orthotics, remote wound monitoring, and AI-driven care coordination are widening their service mix, boosting average revenue per visit, and improving payer negotiations. At the same time, reimbursement pressure and practitioner shortages outside major cities curb expansion, prompting hub-and-spoke clinic models and increased reliance on mid-level podiatric assistants. Midsized practices that adopt population-health tools are outperforming peers that remain dependent on high-volume routine care, while hospital outpatient departments defend their share through bundled service offerings and integrated referral streams.

Key Report Takeaways

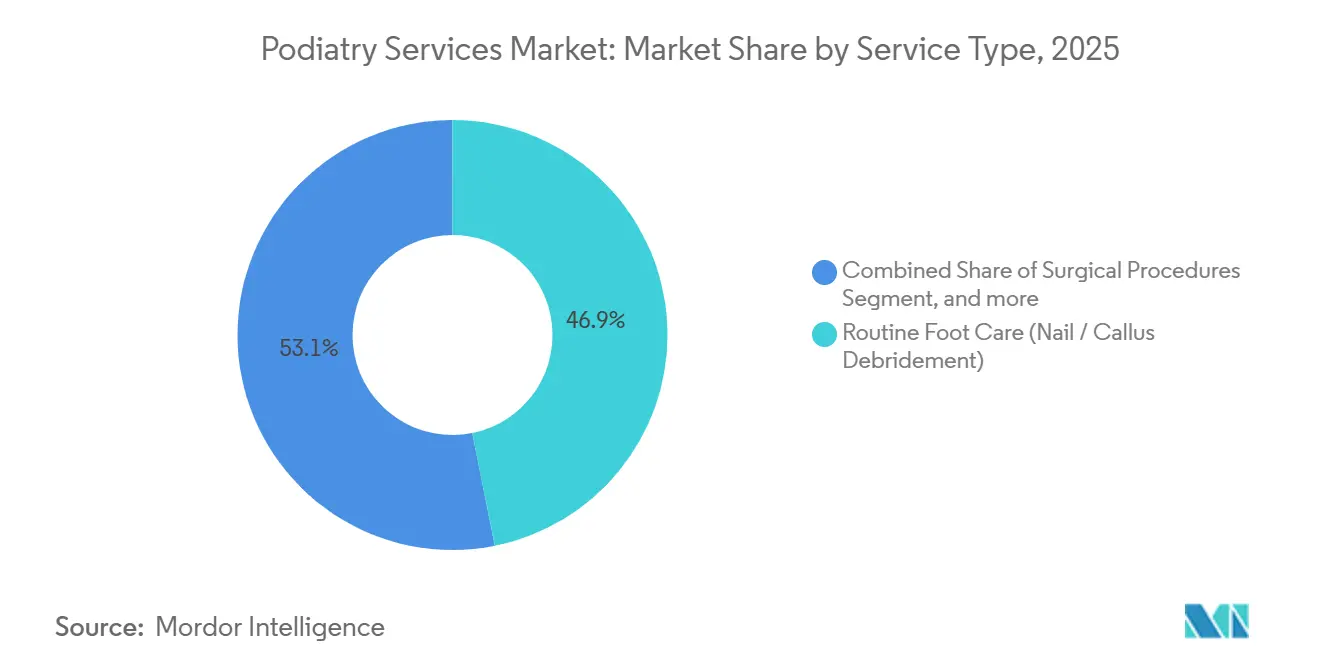

- By service type, routine foot care accounted for 46.87% in 2025, while sports podiatry is set to grow at a 5.43% CAGR through 2031.

- By patient demographics, adults accounted for 51.23% in 2025, whereas the pediatric segment is advancing at a 6.22% CAGR through 2031.

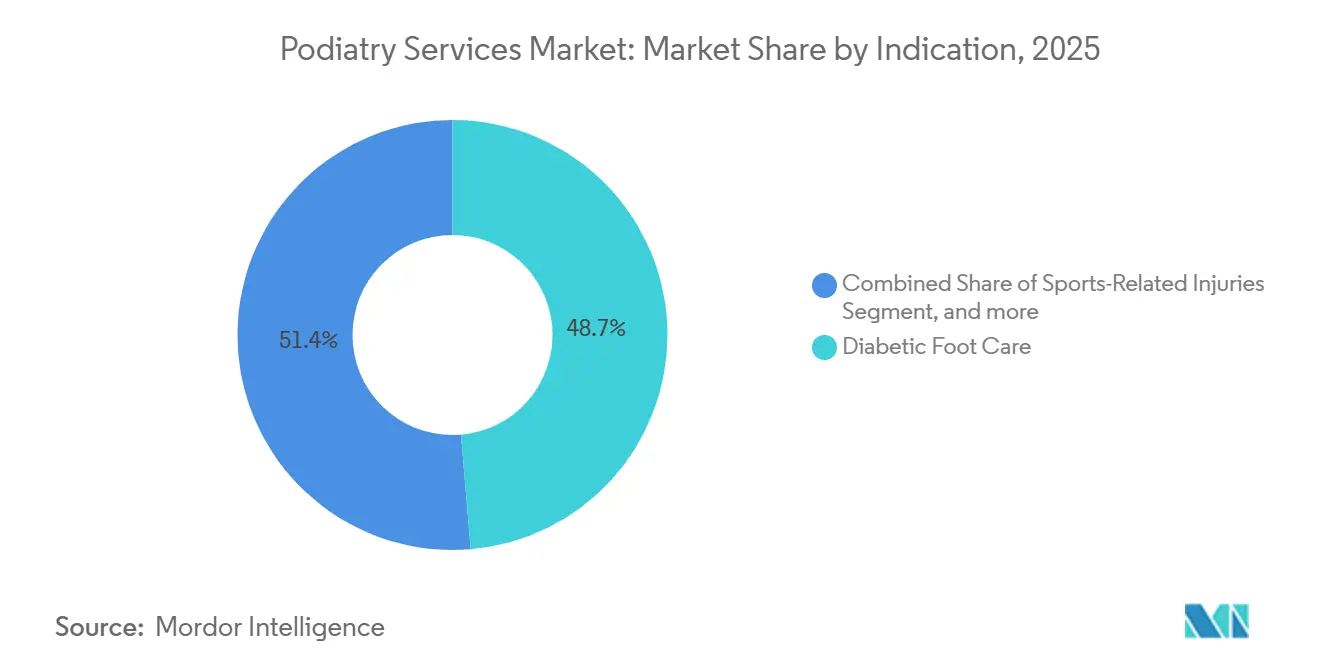

- By indication, diabetic foot care accounted for 48.65% in 2025, and sports-related injuries are growing at a 5.76% CAGR through 2031.

- By care setting, hospital outpatient departments accounted for 55.43% in 2025, while home care and community services are projected to expand at a 6.43% CAGR through 2031.

- By geography, North America led with a 41.99% share in 2025, and Asia-Pacific is forecast to post a 4.65% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Podiatry Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Chronic Disease Burden (Diabetes, Arthritis, Obesity) | +1.2% | Global, with highest intensity in North America, Europe, and urban Asia-Pacific | Long term (≥ 4 years) |

| Aging Population and Mobility-Related Foot Disorders | +0.9% | North America, Europe, Japan, South Korea | Long term (≥ 4 years) |

| Shift Toward Preventive Foot Care and Early Intervention | +0.5% | North America, Australia, select European markets | Medium term (2-4 years) |

| Expansion of Insurance Coverage and Value-Based Care Models | +0.4% | United States (Medicare Advantage, Medicaid expansion states), Canada | Medium term (2-4 years) |

| Technological Advancements in Diagnostics and 3D Orthotics | +0.3% | North America, Western Europe, Australia | Short term (≤ 2 years) |

| Private Equity-Driven Consolidation Expanding Clinic Networks | +0.2% | United States, Canada, Australia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Chronic Disease Burden Drives Podiatry Utilization at Scale

Diabetes remains the primary volume catalyst, with 40.1 million Americans living with the disease in 2024 and 15% to 25% expected to develop foot ulcers over their lifetime. Annual comprehensive foot exams are now embedded in the 2025 standards of care, locking in recurring visits for podiatry clinics. Obesity and arthritis compound pathology by raising plantar pressure and reducing joint flexibility, thereby elevating demand for orthotic interventions and outpatient surgeries. Each comorbid condition layers incremental revenue but also requires multidisciplinary coordination that small offices cannot easily deliver. Consolidated groups staffed with wound-care nurses and physical therapists can bundle services, lower downstream costs, and secure value-based contracts from payers that reward ulcer-prevention outcomes.

Aging Population and Mobility Disorders Expand the Addressable Market

The global cohort of adults aged 60 and above is set to hit 1.4 billion by 2030, and more than 80% of those referred to falls-prevention clinics present with foot problems. Toe weakness, hallux valgus, and ankle stiffness impair gait stability, heightening fracture risk and driving referrals to podiatrists for biomechanical assessments. U.S. initiatives such as STEADI include foot health as a modifiable fall-risk factor, funneling geriatric patients to podiatry earlier in disease progression. Japan and South Korea mirror this trend but face clinician shortages in cities outside Tokyo and Seoul, while Australia’s National Disability Insurance Scheme underpins podiatry access for older adults living independently. Providers that embed foot care within multidisciplinary geriatric teams secure longer care episodes and improve patient retention.

Preventive Foot Care and Early Intervention Shift Revenue Mix

Medicare Advantage expanded routine foot-care benefits for diabetic beneficiaries in 2024 and 2025, lowering out-of-pocket expenses and driving visit frequency. Public-awareness campaigns highlight the importance of early detection of pediatric foot abnormalities, legitimizing the use of custom orthotics and physiotherapy before bone maturity. Recreational runners increasingly demand gait analysis and custom insoles, a trend supported by studies showing running injury incidence as high as 79.3% depending on mileage and footwear. Wellness-oriented services diversify revenue and mitigate reimbursement risk, though they rely more on cash pay and commercial insurance than Medicare.

Technological Advancements in Diagnostics and 3D Orthotics Enhance Precision

The FDA cleared the Albert 3DFit Scanner in 2024, enabling precise capture of foot geometry and rapid orthotic fabrication through additive manufacturing[1]U.S. Food and Drug Administration, “510(k) Clearance for Albert 3DFit Scanner,” fda.gov. Variable-density printing permits custom pressure redistribution that traditional milling cannot match. Digital pressure heatmaps make pathology visible to patients and boost compliance with orthotic use. Remote patient-monitoring codes 99453, 99454, and 99457 reimburse podiatrists who track wound healing between visits, supporting home-care growth. Platforms such as Navina flag patients overdue for exams, automating outreach and raising preventive-care capture rates.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pressure on Reimbursement and Fee Schedules | −0.6% | United States, United Kingdom, Canada | Medium term (2–4 years) |

| Shortage of Qualified Podiatrists in Rural Areas | −0.4% | Rural United States, Canada, Australia, India | Long term (≥ 4 years) |

| Regulatory Scrutiny of Advanced Wound-Care Products | −0.3% | United States, European Union, Australia | Short term (≤ 2 years) |

| Substitution by Primary-Care and Orthopedic Providers | −0.2% | Global, most acute in rural and low-income areas | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Reimbursement Pressure and Fee-Schedule Adjustments Constrain Margins

The 2026 Physician Fee Schedule applied a 2.83% cut to certain evaluation and management codes, directly trimming podiatry revenue. Private insurers mirrored the reduction, indexing their own schedules to Medicare benchmarks. An improper-payment rate of 11.2% in 2024 prompted intensive audits and forced smaller clinics to divert resources to compliance activities. Value-based contracts offer greater revenue potential but require robust data analytics and risk management, reinforcing the attractiveness of scale.

Workforce Shortages in Rural and Underserved Areas Limit Access

Roughly 70% of the United States’ 15,000 practicing podiatrists cluster in urban zones, leaving many rural counties with no provider at all. Median provider age now exceeds 55, implying an upcoming retirement cliff. Telehealth extends reach for follow-ups but cannot replace in-person procedures such as nail debridement or injections. Similar gaps exist in regional Australia despite long-standing statutory recognition of the profession, while India trains fewer than 1,000 podiatrists for a population topping 1.4 billion. Hub-and-spoke clinics staffed by assistants and nurse practitioners offer a stop-gap solution but do not fully bridge the access divide.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Surgical Procedures Climb as Routine Care Commoditizes

Routine foot care held 46.87% of the podiatry services market share in 2025, a testament to its high-volume, low-complexity nature. However, fee-schedule compression and payer reclassification of maintenance visits have squeezed margins. Surgical procedures are capturing a larger slice of revenue as minimally invasive techniques shorten recovery times and drive patient acceptance. Same-day outpatient bunionectomies and hammertoe corrections, once hospital-based, now take place in specialized ambulatory centers, widening the candidate pool and improving throughput. Practices that invest in surgical suites and fluoroscopic imaging improve revenue per square foot and command higher referral rates from orthopedic partners. The fastest-growing niche within this segment is sports podiatry, projected to grow at a 5.43% CAGR to 2031, fueled by rising athletic participation and the widespread availability of motion-capture gait labs[2]Journal of Orthopaedic & Sports Physical Therapy, “Running Injury Incidence 2024,” jospt.org. Clinics that bundle biomechanical assessment with on-site orthotic fabrication differentiate their brand and capture discretionary consumer spend.

The adoption of 3D printers, such as HP’s Multi Jet Fusion platform, has slashed orthotic turnaround time from three weeks to as little as three days. Digital libraries allow clinicians to store and tweak orthotic designs, facilitating repeat orders and scaling cash-based revenue. Meanwhile, geriatric foot-care programs linked to falls-prevention initiatives deliver stable Medicare volumes. Together, these forces are shifting the podiatry services market toward higher-acuity, higher-margin services, widening the gap between tech-enabled groups and traditional high-throughput offices.

By Patient Demographics: Pediatric Care Gains Momentum

Adults controlled 51.23% of the podiatry services market in 2025, thanks to diabetes and occupational foot disorders. The geriatric cohort, though slower in volume growth, yields the highest revenue per patient because of multiple comorbidities and Medicare coverage expansions. Pediatric visits, however, are rising at a 6.22% CAGR through 2031, outpacing all other demographics. Parents now see value in early correction of flat feet, toe-walking, and in-toeing, shifting the paradigm from watchful waiting to proactive intervention. Clinics that house play-friendly waiting rooms and child-sized gait-analysis equipment are winning referrals from pediatricians.

Commercial insurers in affluent suburbs increasingly cover custom orthotics for children if prescribed to prevent future musculoskeletal disorders. In low-income populations, access depends on Medicaid participation, which many providers decline due to low reimbursement rates. Group practices that accept capitated contracts can cross-subsidize pediatric patients with higher margin adult services, capturing lifetime loyalty from families and solidifying local brand equity.

By Indication: Sports-Related Injuries Accelerate Revenue Diversification

Diabetic foot care accounted for 48.65% of market revenue in 2025, underscoring predictable demand aligned with Medicare and payer guidelines. Yet sports-related injuries stand out with a 5.76% CAGR to 2031 as participation in running, cycling, and court sports increases[3]Journal of Foot and Ankle Surgery, “Minimally Invasive Forefoot Surgery 2025,” jfas.org. These injuries encompass plantar fasciitis, Achilles tendinopathy, and stress fractures, conditions that require multi-visit rehabilitation and custom orthoses. Providers have responded by recruiting certified pedorthists and physical therapists to deliver end-to-end treatment in-house, boosting retention and ancillary revenue.

Structural abnormalities such as bunions and hammertoes remain a steady source of elective surgery volume. Fungal infections are gaining treatment alternatives in the form of laser therapy devices cleared in 2024, which appeal to patients wary of oral antifungals. Diversifying across indications cushions revenue volatility tied to any single reimbursement regime and supports a broadened payer mix that includes workers’ compensation and self-pay athletes.

By Care Setting: Home-Based Care Gains Ground Under Value-Based Incentives

Hospital outpatient departments accounted for 55.43% of market revenue in 2025, driven by integrated diagnostics and bundled facility fees. They are, however, ceding share to home care and community services, which are forecast to grow at a 6.43% CAGR through 2031 as CMS expands reimbursement for remote patient monitoring. Diabetic foot ulcer programs that send wound-care nurses to patient homes reduce readmissions and command higher per-member fees under Medicare Advantage plans. Independent podiatry clinics are responding by adding telehealth follow-ups and mobile wound-care vans, turning fixed-site liabilities, such as rent, into variable costs.

The podiatry services market size for home-care solutions is projected to climb steadily as payers align incentives with site-of-care shifts. Clinics leveraging AI platforms that flag care gaps can remotely triage patients and schedule home visits only when necessary, preserving clinician bandwidth and improving utilization rates. These operational efficiencies help smaller providers survive margin pressure while extending access to rural and high-deductible patient cohorts.

Geography Analysis

North America generated 41.99% of global revenue in 2025, anchored by the United States’ 40.1 million diabetic population and roughly 15,000 practicing podiatrists. Private equity inflows remain strong: Beyond Podiatry sold for USD 87 million in 2024, while Upperline Health raised USD 12.2 million in 2025 to fund clinic growth and AI platform rollouts. Canada’s provincial health plans reimburse podiatry only for diabetic care, yet a growing private-pay sector sustains national chains such as BioPed Footcare. Mexico’s nascent scene relies on out-of-pocket spending and medical tourism from border states, signaling future upside as insurance coverage deepens.

Asia-Pacific is the fastest-growing region at a 4.65% CAGR to 2031, driven by Australia’s mature regulatory framework and Healthia Limited’s 94-clinic footprint. China and India combine surging diabetes prevalence with a severe shortfall of trained podiatrists, inviting foreign providers to establish teaching partnerships and telehealth hubs. Statutory recognition in Japan and South Korea supports integration within hospital systems, yet high urban concentration leaves rural elders underserved. The podiatry services market size in Australia is expanding further as Pacific Equity Partners completes its USD 360 million buyout of Healthia, injecting capital for east-coast clinic densification.

Europe shows modest expansion as public-pay systems in the United Kingdom and Germany constrain reimbursement growth. Long wait times at National Health Service clinics push higher-income patients to private providers that offer faster access and sports biomechanics services. Southern European markets such as Italy and Spain remain under-penetrated but display rising private-pay demand in metropolitan areas. In South America and the Middle East, podiatry services complement broader orthopedic offerings in new private hospitals; however, podiatry services' market share remains fractional compared to orthopedic surgery and general practice due to limited workforce depth.

Competitive Landscape

The top 10 U.S. podiatry platforms account for roughly 20% of national revenue, suggesting moderate market fragmentation. Extremity Healthcare’s 2023 takeover of Upperline Health brought 150 providers under one roof, integrating wound-care protocols and centralized compliance units. Balance Health merged with Weill Foot & Ankle Institute the same year, amassing more than 160 providers across seven states and creating leverage in payer negotiations. Consolidators prioritize contiguous geographic footprints to maximize referral capture and to amortize IT infrastructure costs. Independent physicians retain strong local loyalty but feel pressure from audits, higher malpractice premiums, and requirements for technology investments.

Technology is the main differentiator. Upperline Health employs AI care-gap analysis to identify overdue diabetic patients, while Healthia Limited in Australia pilots remote wound-monitoring programs under National Health Service contracts in Wales. Clinics that install 3D scanners for orthotic design convert a larger share of visits into cash-pay device sales, boosting margins. Regulatory scrutiny around improper billing favors large groups with dedicated compliance teams; solo practitioners face disproportionate audit risk. Companies that master population-health analytics are the most likely acquirers in the ongoing roll-up race.

Emerging niches offer headroom. Pediatric podiatry remains underserved due to low reimbursement and limited subspecialty training, creating a white space for clinics that cater to young athletes and patients with structural abnormalities. Sports podiatry appeals to cash-paying consumers and corporate wellness programs looking to reduce worker downtime due to injury. Practices that diversify across these niches hedge against reimbursement cuts in diabetic wound care and position themselves for growth in wellness-oriented healthcare spending.

Podiatry Services Industry Leaders

US Foot & Ankle Specialists (USFAS)

Upperline Health

Healthia Limited (My FootDr)

Kaiser Permanente Podiatry Services

Village Podiatry Centers

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: FisioReact, the company revolutionizing access to at-home healthcare services, acquired FisioVen, a Madrid-based company offering at-home physiotherapy services.

- November 2024: Alliance Mobile Medical Services, LLC, a physician-led provider of advanced wound and podiatric care launched operations across San Antonio and the Dallas–Fort Worth Metroplex. The organization brings hospital-quality treatments directly to patients in skilled nursing facilities, assisted living communities, and home settings—bridging a long-standing gap in accessibility and continuity of care.

Global Podiatry Services Market Report Scope

As per the scope of the report, podiatry services focus on diagnosing, treating, and preventing foot and ankle conditions. They address issues such as injuries, deformities, infections, and chronic diseases, such as diabetes. Podiatrists also provide footwear advice and perform surgical procedures when necessary.

The Podiatry Services Market is Segmented by Service Type (Routine Foot Care, Surgical Procedures, Sports Podiatry, and Other Service Types), Patient Demographics (Pediatric, Adult, and Geriatric), Indication (Diabetic Foot Care, Sports-Related Injuries, Structural Abnormalities, and Fungal/Infectious Conditions), Care Setting (Hospital Outpatient, Podiatry Clinics, and Home Care), and Geography (North America, Europe, Asia-Pacific, MEA, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Routine Foot Care (Nail / Callus Debridement) |

| Surgical Procedures (Forefoot / Hindfoot) |

| Sports Podiatry |

| Other Service Types (Geriatric Foot Care; Orthotics & Biomechanical) |

| Pediatric |

| Adult |

| Geriatric |

| Diabetic Foot Care |

| Sports-Related Injuries |

| Structural Abnormalities |

| Fungal / Infectious Conditions |

| Hospital Outpatient Departments |

| Podiatry Clinics & Physician Offices |

| Home Care & Community Services |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest Of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest Of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest Of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest Of South America |

| By Service Type | Routine Foot Care (Nail / Callus Debridement) | |

| Surgical Procedures (Forefoot / Hindfoot) | ||

| Sports Podiatry | ||

| Other Service Types (Geriatric Foot Care; Orthotics & Biomechanical) | ||

| By Patient Demographics | Pediatric | |

| Adult | ||

| Geriatric | ||

| By Indication | Diabetic Foot Care | |

| Sports-Related Injuries | ||

| Structural Abnormalities | ||

| Fungal / Infectious Conditions | ||

| By Care Setting | Hospital Outpatient Departments | |

| Podiatry Clinics & Physician Offices | ||

| Home Care & Community Services | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest Of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest Of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest Of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest Of South America | ||

Key Questions Answered in the Report

How large is the podiatry services market today?

The podiatry services market size is USD 4.87 billion in 2026 and is projected to reach USD 5.74 billion by 2031.

Which service type is growing fastest in podiatry?

Sports podiatry leads growth, expanding at a projected 5.43% CAGR through 2031.

Why are private equity firms investing in podiatry clinics?

Consolidation creates regional networks that can negotiate better payer contracts, spread compliance costs, and deploy technology such as AI care-gap tools at scale.

How is technology changing podiatry practice operations?

3D foot scanners, additive manufacturing for orthotics, and remote wound monitoring codes enable faster device delivery, better patient engagement, and new revenue streams.

Which region offers the greatest growth potential outside North America?

Asia-Pacific, led by Australia, is forecast to post a 4.65% CAGR through 2031 because of statutory recognition, rising diabetes prevalence, and private equity capital inflows.

What regulatory pressures affect podiatry reimbursement?

U.S. fee-schedule cuts of 2.83% in the 2026 Physician Fee Schedule and an 11.2% improper-payment audit rate are tightening margins and increasing compliance costs.

Page last updated on: