Plastic Healthcare Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

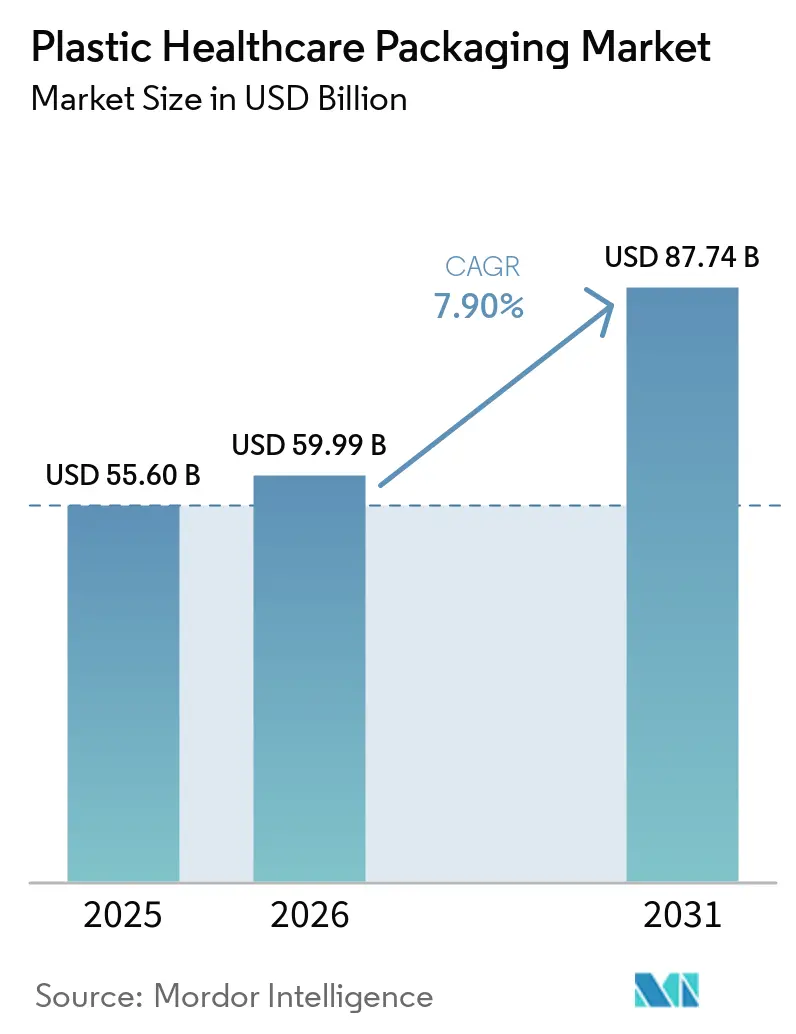

| Market Size (2026) | USD 59.99 Billion |

| Market Size (2031) | USD 87.74 Billion |

| Growth Rate (2026 - 2031) | 7.90% CAGR |

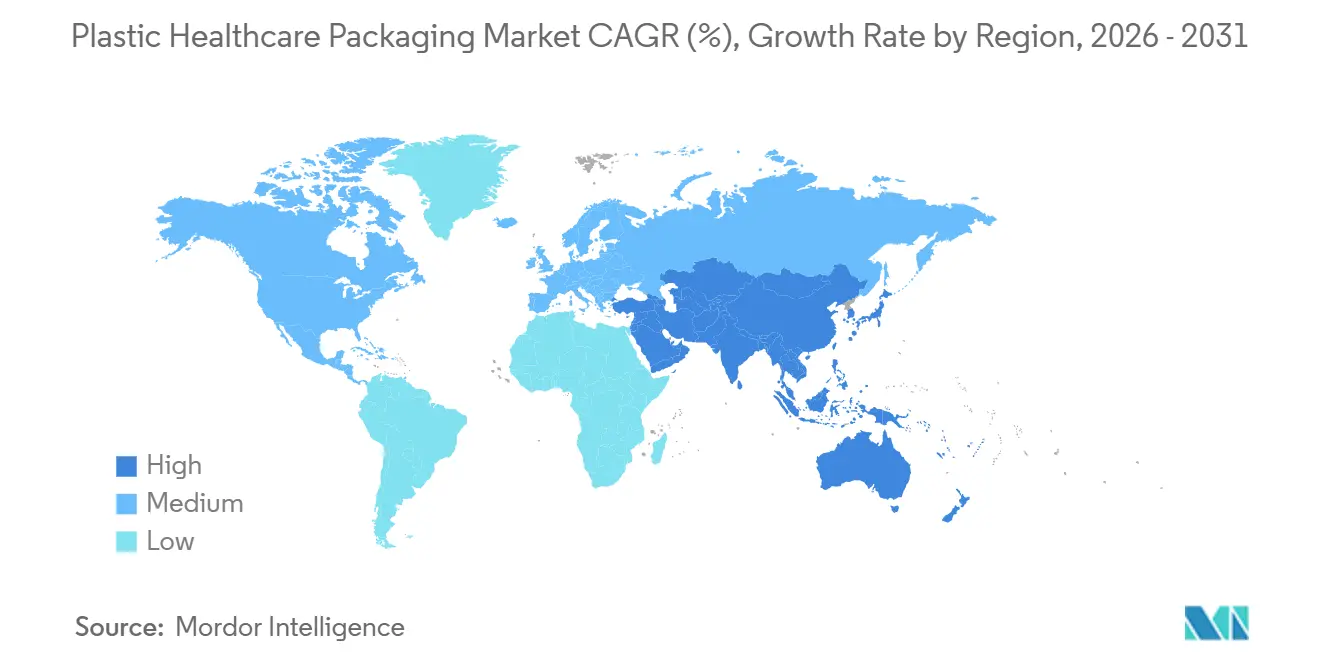

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

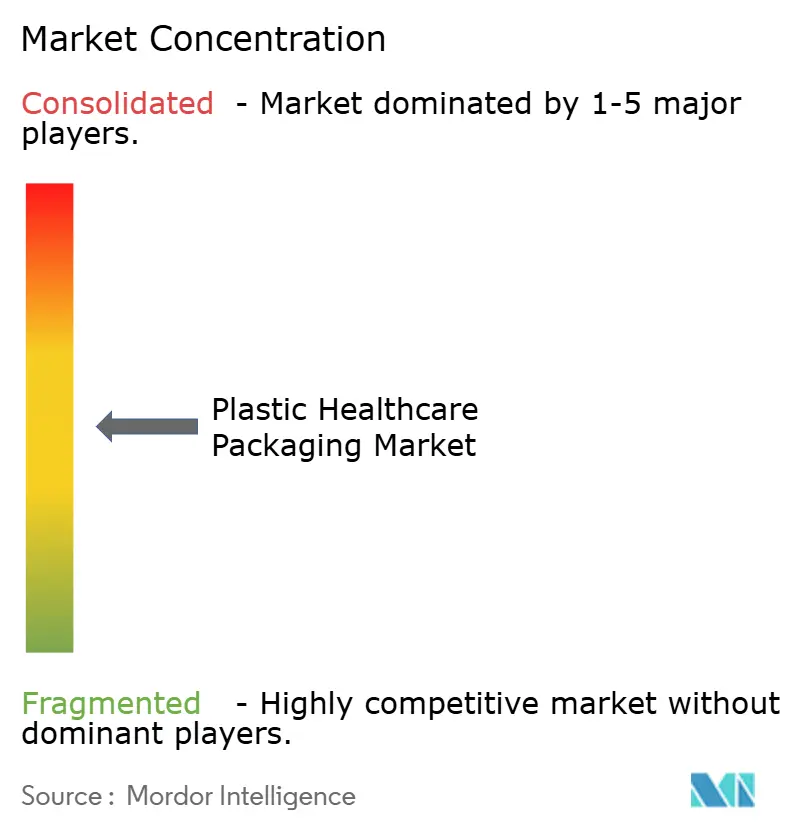

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Plastic Healthcare Packaging Market Analysis by Mordor Intelligence

The Plastic Healthcare Packaging Market size is projected to expand from USD 55.60 billion in 2025 and USD 59.99 billion in 2026 to USD 87.74 billion by 2031, registering a CAGR of 7.90% between 2026 to 2031.

Driven by robust biologics pipelines and a shift towards home-based treatments, buyers are increasingly opting for advanced polymer formats over traditional glass. This transition is supported by investments in cyclic-olefin copolymer (COC) and cyclic-olefin polymer (COP) containers, which effectively address persistent extractables challenges. Furthermore, the integration of digital drug delivery systems with near-field communication (NFC) tags is pushing the industry towards plastics compatible with in-mold electronics. On the sustainability front, fee structures are encouraging the adoption of monopolymer blisters. These solutions align with existing recycling streams while maintaining barrier integrity, ensuring the plastic healthcare packaging market remains resilient, even in regions implementing stricter regulations on single-use items. Vendors are increasingly employing strategies that combine vertical integration, automation, and advanced smart labels. These data-rich labels facilitate real-time compliance with track-and-trace regulations and enhance transaction efficiency in a supply chain facing capacity constraints.

Key Report Takeaways

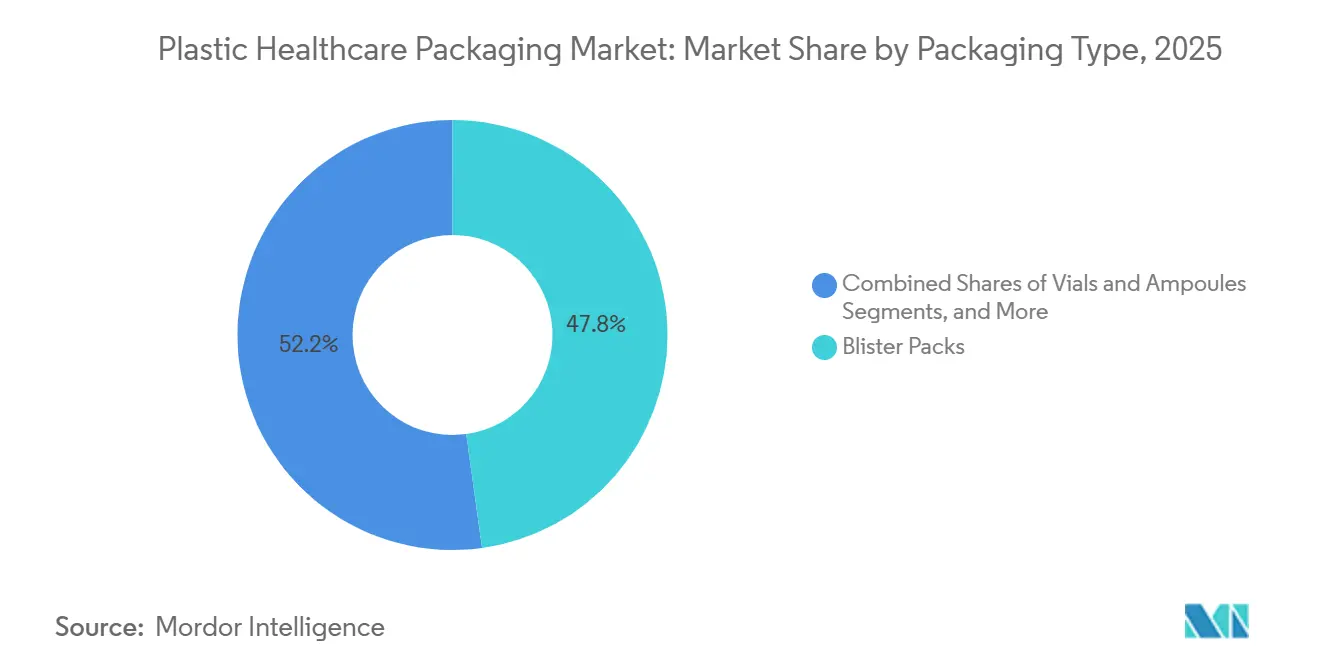

- By packaging type, bottles and jars led with 47.80% of the plastic healthcare packaging market share in 2025, while vials and ampoules are projected to register an 11.80% CAGR through 2031.

- By material, high-density polyethylene accounted for 33.45% of the plastic healthcare packaging market size in 2025; polypropylene is poised for a 12.50% CAGR over 2026-2031.

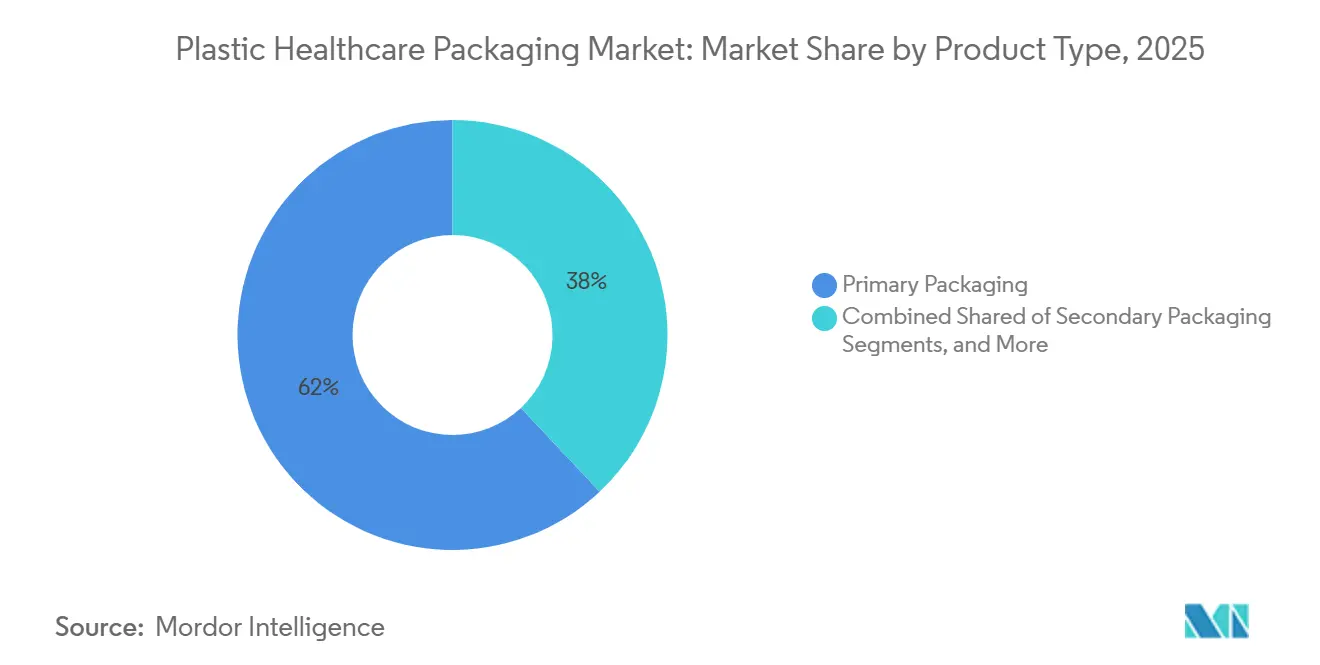

- By product type, primary packaging captured 62.0% of volume in 2025 and is forecast to expand at a 9.40% CAGR to 2031.

- By technology, injection molding held 54.68% share of the plastic healthcare packaging market size in 2025, whereas 3D printing is advancing at a 14.70% CAGR.

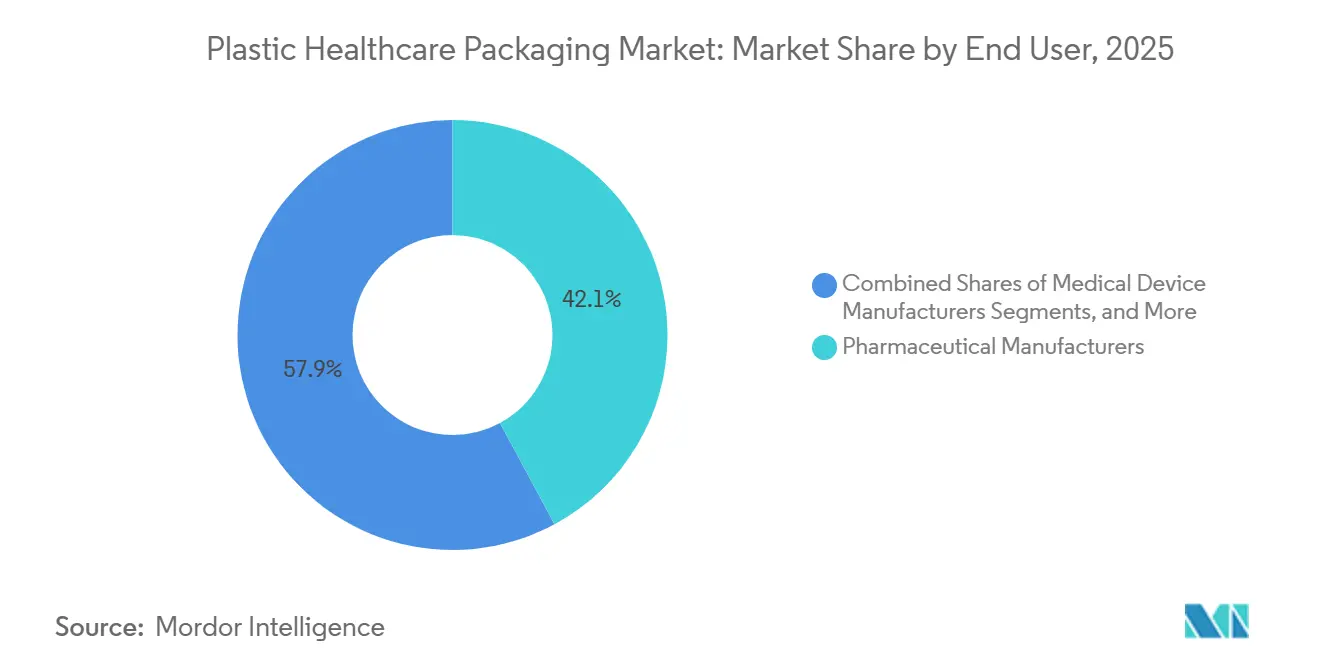

- By end user, pharmaceutical manufacturers absorbed 42.13% of shipments in 2025, while nutraceutical companies are expanding at an 8.80% CAGR.

- By geography, North America represented 38.67% revenue share in 2025; Asia-Pacific is advancing at a 9.80% CAGR, the fastest pace among regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Plastic Healthcare Packaging Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Biologics boom increasing need for high-barrier plastic containers | 2.1% | Global, with concentration in North America and Europe for mRNA vaccines; Asia-Pacific for biosimilars | Medium term (2-4 years) |

| Home-healthcare shift fueling demand for unit-dose formats | 1.8% | North America and Europe leading; Asia-Pacific adoption accelerating in urban centers | Short term (≤ 2 years) |

| Smart NFC-enabled packs for adherence and anti-counterfeiting | 1.3% | Europe (FMD compliance); North America (DSCSA); spillover to Middle East and Africa | Medium term (2-4 years) |

| Adoption of cyclic-olefin polymers for mRNA vaccine vials | 1.5% | North America and Europe for vaccine production; Asia-Pacific for fill-finish operations | Short term (≤ 2 years) |

| Cost advantage of plastic versus glass in sterile applications | 1.3% | Europe (FMD compliance); North America (DSCSA); spillover to Middle East and Africa | Medium term (2-4 years) |

| Stricter drug-traceability rules favoring tamper-evident packs | 1.5% | North America and Europe for vaccine production; Asia-Pacific for fill-finish operations | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Biologics Boom Increasing Need for High-Barrier Plastic Containers

Monoclonal antibodies, cell therapies, and gene-editing products now represent over 40% of investigational drug filings.[1]U.S. Food and Drug Administration, “Drug Supply Chain Security Act Overview,” fda.gov These modalities require ultra-low moisture vapor transmission rates, a standard consistently achieved by COC and COP. These resins also eliminate the tungsten leachables associated with molded glass, reducing the risk of protein aggregation during long-term storage. Starting January 2026, the European Pharmacopoeia will implement benchmarks for COC and COP, standardizing extractables testing and streamlining approval processes across Europe. Companies such as West Pharmaceutical Services and Daikyo Seiko are leveraging this regulatory clarity by scaling up production of FluroTec-coated elastomer closures, which ensure over 99% drug-contact neutrality. Additionally, Catalent and Recipharm are enhancing production capabilities by installing blow-fill-seal lines with a capacity of 400 units per minute, incorporating automated particulate inspection to maintain ISO 13485 compliance. These advancements collectively reinforce the growing prominence of polymers in the plastic healthcare packaging market.

Home-Healthcare Shift Fueling Demand for Unit-Dose Formats

Healthcare payers in the United States and Europe are incentivizing in-home infusion by offering reimbursements at 30-50% lower rates compared to hospital-based treatments. This trend is driving manufacturers to repackage therapies into prefilled syringes and single-dose blisters. Solutions like Becton Dickinson’s BD Effivax and Gerresheimer’s Gx RTF syringes simplify nursing procedures by eliminating the need for reconstitution, significantly reducing medication errors among elderly patients managing multiple prescriptions. The FDA’s 2024 draft guidance emphasizes the importance of user-friendly packaging, accelerating the adoption of tamper-evident, child-resistant blisters. These developments are creating a sustained demand trajectory for the plastic healthcare packaging market through 2031.

Smart NFC-Enabled Packs for Adherence and Anti-Counterfeiting

The implementation of serialization lines across Europe has exceeded 50,000 units, driven by the need for compliance with anti-counterfeiting regulations. With NFC tags now available at a cost-effective price point, real-time authentication is becoming increasingly accessible for mid-tier generic manufacturers. Pharmaceutical companies are integrating these encrypted chips with patient-engagement applications to track dosage events and provide refill reminders. In the United States, regulatory requirements mandating interoperable electronic product codes by November 2027 are expected to further accelerate the adoption of NFC-enabled plastic primary containers in the region.

Adoption of Cyclic-Olefin Polymers for mRNA Vaccine Vials

The 2026 European Pharmacopeia monographs will formally approve the use of COC and COP for parenteral vaccines, removing previous regulatory restrictions that limited these materials to diagnostic applications.[2]European Medicines Verification Organisation, “Falsified Medicines Directive Update,” emvo-medicines.eu Leading companies such as SCHOTT Pharma and Gerresheimer are collaborating with CDMOs to validate COC vials in compliance with ISO 8362-1 and USP <381> standards, expediting the market introduction of next-generation RSV and dengue vaccines. The transition from glass, which is prone to delamination and tungsten contamination, reduces production line stoppages and rejection rates, driving double-digit growth in the plastic healthcare packaging market.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Escalating sustainability regulations on single-use plastics | −1.4% | Europe, North America, spillover to Asia-Pacific | Long term (≥ 4 years) |

| Rising recalls tied to extractables and leachables in polymers | −0.9% | Global, heightened U.S. and EU oversight | Short term (≤ 2 years) |

| Volatility in medical-grade resin supply & prices | −1.5% | Europe, North America, spillover to Asia-Pacific | Long term (≥ 4 years) |

| Glass-to-plastic conversion hesitancy for injectable biologics | −0.8% | Global, heightened U.S. and EU oversight | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Europe Tightens Grip on Single-Use Plastics with New Regulations

Europe's Packaging and Packaging Waste Regulation (PPWR) requires all packaging to be recyclable by 2030 and establishes a 30% recycled-content target for PET by the same year.[3]European Commission, “Packaging and Packaging Waste Regulation,” environment.ec.europa.eu Although medical packaging has temporary exemptions, producers must provide evidence of no viable alternatives, driving a shift toward monomer blisters. In Germany, pharmaceutical companies are now obligated to fund collection networks, adding costs of EUR 0.05–0.15 per blister pack, which reduces profit margins for generic products. These financial challenges undermine the value proposition of PVC-PVDC laminates, despite their superior barrier properties, potentially limiting growth in the plastic healthcare packaging market beyond 2030.

FDA's New Guidelines Heighten Scrutiny on Polymers

Effective January 2025, the FDA's Q3E guideline enforces comprehensive solvent-screen extractions, significantly increasing the analytical workload for each new container system. Simultaneously, updates to ISO 10993-18 demand more detailed GC-MS and LC-MS protocols, potentially extending validation timelines by up to a year and adding USD 200,000–500,000 in upfront testing expenses. These regulatory requirements are redirecting research and development investments toward higher-cost fluoropolymer coatings and tungsten-free molding processes. While these measures limit short-term flexibility in the plastic healthcare packaging market, they also create opportunities for suppliers with proven low-leachables solutions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Type: Vials and Ampoules Lead the Charge in Biologics

Vials and ampoules are projected to grow at an 11.8% CAGR from 2026 to 2031, surpassing all other formats in the plastic healthcare packaging market. Pharmaceutical manufacturers increasingly prefer COC and COP vials for high-value biologics due to their ability to prevent delamination during lyophilization cycles and resist breakage during cold-chain logistics. In 2025, bottles and jars accounted for 47.8% of the plastic healthcare packaging market, driven by HDPE's chemical resilience for solid orals and nutraceuticals. However, growth is slowing as payers transition to adherence-friendly blister cards. Serialization mandates from both the EU FMD and the U.S. DSCSA emphasize batch-level traceability, which integrates more effectively into blister webs and unit-dose syringes than bulk bottles, signaling a long-term market shift.

By Material: Polypropylene Rises with Sterilization Edge

Polypropylene is leading resin growth, with a projected CAGR of 12.5%. Its ability to endure autoclave sterilization at 121 °C for 20 minutes and withstand gamma doses up to 50 kGy makes it a preferred choice. Its high heat-deflection temperature enables the re-use of tooling across parenteral closures, syringe barrels, and inhaler bodies, enhancing economies of scale for converters. In 2025, HDPE held 33.45% of the plastic healthcare packaging market, supported by its affordability and moisture barrier properties. However, regulatory measures, such as France's EPR fee on non-recyclable PVC-PVDC blisters, are accelerating the shift toward all-PP structures, further driving polypropylene's growth.

By Product Type: Primary Packaging Dominates Revenue Streams

Primary packaging accounted for 62% of shipments in 2025 and is expected to grow at a 9.4% CAGR through 2031. Prefilled syringes, single-dose vials, and NFC-ready blisters are driving capital expenditure plans as they reduce dosing errors and support remote care delivery. The FDA’s human-factors guidance is raising ergonomic standards for these packs, prompting suppliers to improve features such as plunger glides and child-resistant depths.

By Technology: 3D Printing Revolutionizes Personalized Medicine

Injection molding retained a 54.68% share of the plastic healthcare packaging market in 2025, benefiting from rapid sub-10-second cycle times and extensive validation. However, 3D printing is advancing at a 14.7% CAGR, driven by its ability to achieve large-scale production and enable micro-channel geometries that are unattainable with traditional molding. This technology is paving the way for controlled drug release in personalized therapies.

By End User: Nutraceuticals Surge as Pharma Growth Stabilizes

Pharmaceutical manufacturers accounted for 42.13% of unit shipments in 2025. However, their growth is stabilizing as patent cliffs reduce blockbuster revenues, and the focus shifts to biosimilars, which require smaller, high-value containers. Nutraceutical firms are expanding at an 8.8% CAGR, driven by wellness trends and regulatory requirements for child-resistant closures under the U.S. Poison Prevention Packaging Act. HDPE bottles remain the preferred choice for fish-oil softgels and herbal tablets, balancing moisture protection and portability.

Geography Analysis

In 2025, North America accounted for 38.67% of the revenue, driven by DSCSA deadlines that accelerated blister serialization and NFC-label adoption across prescription portfolios. The U.S. leads the region, supported by Medicare Advantage reimbursements favoring at-home injections. Meanwhile, Canada aligns closely with FDA standards, facilitating smoother cross-border operations. As global sponsors shift focus from Asia, Mexico's contract-drug manufacturing hubs are benefiting, providing a boost to local plastics converters.

Asia-Pacific is set to lead with a projected 9.8% CAGR from 2026 to 2031. China's National Medical Products Administration, aligning its extractables guidance with ICH Q3E, has expedited approvals for COC vials from Gerresheimer’s Zhangjiagang facility. In India, Lonza's upcoming expansion will add two billion annual capsule shells and closures by late 2026. Southeast Asian nations, spearheaded by Singapore, are incentivizing pharma cleanroom investments with tax credits, encouraging local production of polypropylene syringes and PET inhaler bodies.

Europe maintained a share in the mid-20s percentage range in 2025, bolstered by stringent compliance norms. The Falsified Medicines Directive spurred widespread serialization, while Germany's VerpackG mandates EPR costs on every unit, shifting focus towards recyclability. In France, CITEO's fees on PVC blisters have prompted many generic firms to transition to PP/PET hybrids. While Southern European markets are slower to adopt new materials, they are still investing in code-aggregation hardware to adhere to pan-EU traceability mandates, sustaining demand in the plastic healthcare packaging sector.

Competitive Landscape

The plastic healthcare packaging arena is moderately fragmented, with the top five players commanding a 25-30% revenue share. West Pharmaceutical Services and Gerresheimer, each holding mid-single-digit market positions, boast comprehensive portfolios that include elastomeric closures, vials, and prefilled syringes. Both have invested over USD 100 million in aseptic fill-finish expansions, integrating 100% vision inspection and NFC labelers to align with EU FMD serialization standards.

Just below the top tier, Catalent, SCHOTT Pharma, and Nipro carve out niches with offerings like BFS, COC vials, and glass-polymer hybrids. Regional players, such as Plastic Ingenuity in North America and Selenis in Europe, leverage their thermoforming skills and recycled-content resins to achieve PPWR objectives. Disruptors like Triastek and Laxxon Medical are revolutionizing the landscape by 3D-printing dosage forms on demand, a strategy that minimizes inventory and could reshape supply-chain dynamics.

Across the board, automation plays a pivotal role. Converters utilize collaborative robots for demolding closures, while machine-learning vision systems detect particulate contamination in real-time, reducing scrap by up to 25% on high-volume bottle lines. Compliance standards like ISO 15378 and the FDA’s aseptic processing guidelines benefit established players with extensive validation records. However, they also draw contract packagers who are investing in versatile modular cleanrooms, adept at switching between clinical trials and commercial production, ensuring a dynamic competitive environment in the plastic healthcare packaging market.

Plastic Healthcare Packaging Industry Leaders

Amcor plc

Gerresheimer AG

Berry Global Group

Becton Dickinson & Co.

West Pharmaceutical Services

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Grand River Aseptic Manufacturing announced a USD 100 million prefilled-syringe facility in Michigan targeting 50 million units of annual capacity.

- March 2026: Plastic Ingenuity acquired Germany’s Spezi-Pack, securing European thermoforming capacity for pharmaceutical trays.

- September 2025: INCOG BioPharma completed a 113 000 sq ft expansion in North Carolina, adding 100 million units of prefilled-syringe output with NFC smart labels.

- July 2025: Bora Pharmaceuticals installed a tube-filling line in Ontario capable of 7-15 million semi-solid units annually.

Global Plastic Healthcare Packaging Market Report Scope

As per the scope of the report, plastic healthcare packaging refers to specialized plastic materials such as polyethylene, polypropylene, and PVC, utilized to contain, protect, and preserve pharmaceutical products, medical devices, and tools. It ensures sterility, prevents contamination, and provides tamper-proof, lightweight, and durable protection for drugs and devices throughout the supply chain, from manufacturers to patients.

The plastic healthcare packaging market is segmented into, by packaging type, material, product type, technology, end user, and geography. By packaging type, the market is segmented into bottles & jars, blister packs, vials & ampoules, pouches & bags, tubes, syringes, and others. By material, the market is segmented into HDPE, LDPE / LLDPE, PP, PVC, PET, and others. By product type, the market is segmented into primary packaging, secondary packaging, and tertiary packaging. By technology, the market is segmented into injection molding, blow molding, extrusion, thermoforming, fill & seal, and 3D printing. By end user, the market is segmented into pharmaceutical manufacturers, medical device manufacturers, nutraceutical & dietary supplement manufacturers, home healthcare providers, diagnostic & clinical laboratories, and contract packaging organizations. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers estimated market sizes and trends for 17 countries across major regions worldwide. The report offers market size and forecasts in value (USD) for the above segments.

| Bottles & Jars |

| Blister Packs |

| Vials & Ampoules |

| Pouches & Bags |

| Tubes |

| Syringes |

| Others |

| HDPE |

| LDPE / LLDPE |

| PP |

| PVC |

| PET |

| Others |

| Primary Packaging |

| Secondary Packaging |

| Tertiary Packaging |

| Injection Molding |

| Blow Molding |

| Extrusion |

| Thermoforming |

| Fill & Seal |

| 3D Printing |

| Pharmaceutical Manufacturers |

| Medical Device Manufacturers |

| Nutraceutical & Dietary Supplement Manufacturers |

| Home Healthcare Providers |

| Diagnostic & Clinical Laboratories |

| Contract Packaging Organizations |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Packaging Type | Bottles & Jars | |

| Blister Packs | ||

| Vials & Ampoules | ||

| Pouches & Bags | ||

| Tubes | ||

| Syringes | ||

| Others | ||

| By Material | HDPE | |

| LDPE / LLDPE | ||

| PP | ||

| PVC | ||

| PET | ||

| Others | ||

| By Product Type | Primary Packaging | |

| Secondary Packaging | ||

| Tertiary Packaging | ||

| By Technology | Injection Molding | |

| Blow Molding | ||

| Extrusion | ||

| Thermoforming | ||

| Fill & Seal | ||

| 3D Printing | ||

| By End User | Pharmaceutical Manufacturers | |

| Medical Device Manufacturers | ||

| Nutraceutical & Dietary Supplement Manufacturers | ||

| Home Healthcare Providers | ||

| Diagnostic & Clinical Laboratories | ||

| Contract Packaging Organizations | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large will the plastic healthcare packaging market be by 2031?

The plastic healthcare packaging market size is projected to reach USD 87.74 billion by 2031, expanding at a 7.90% CAGR over 2027-2031.

Which packaging type is growing the fastest?

Vials and ampoules are forecast to grow at an 11.8% CAGR through 2031 as COC and COP replace glass in biologics.

Why is polypropylene gaining traction in healthcare packaging?

Polypropylene tolerates autoclave and gamma sterilization, triggering a 12.5% CAGR in its uptake for prefilled syringes and closures.

Which region is expected to be the most dynamic?

Asia-Pacific is set to record a 9.8% CAGR to 2031 thanks to major capacity additions in China and India.

How are sustainability regulations affecting material choices?

Europes PPWR and national EPR fees are pushing converters toward recyclable monopolymer blisters and away from PVC-PVDC laminates.

What role does 3D printing play in the sector?

3D printing is advancing at a 14.7% CAGR, enabling personalized-dose tablets that bypass traditional molding and reduce inventory risk.

Page last updated on: