Plasma Derived Medicine Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

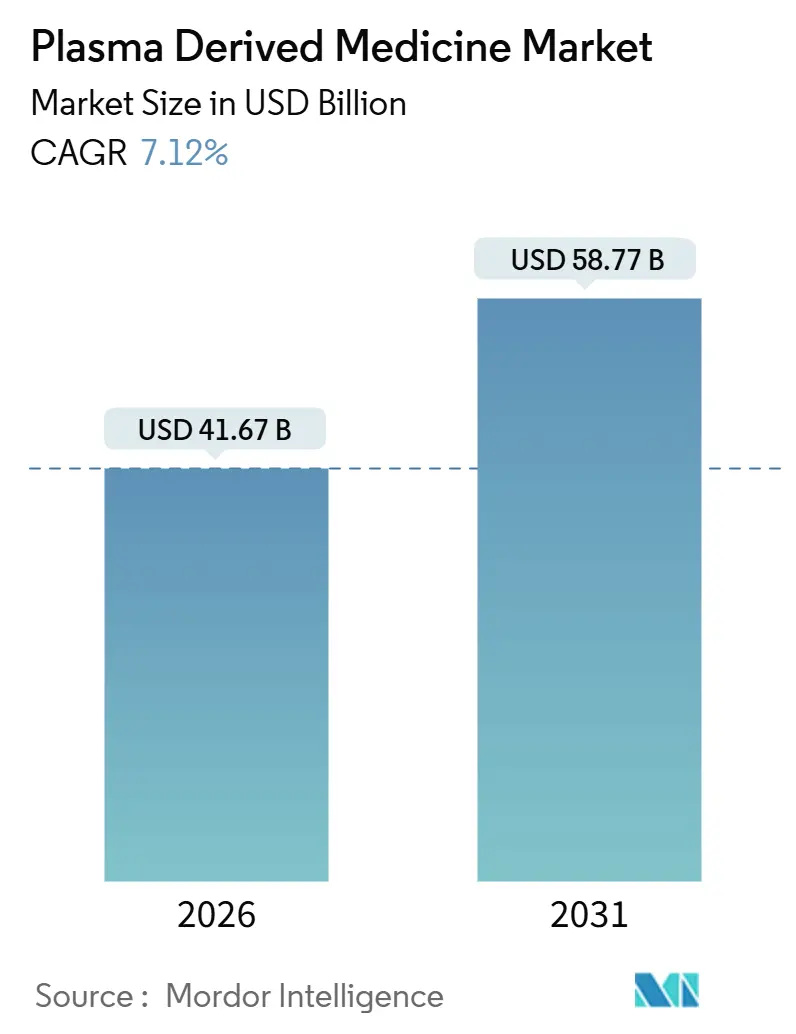

| Market Size (2026) | USD 41.67 Billion |

| Market Size (2031) | USD 58.77 Billion |

| Growth Rate (2026 - 2031) | 7.12% CAGR |

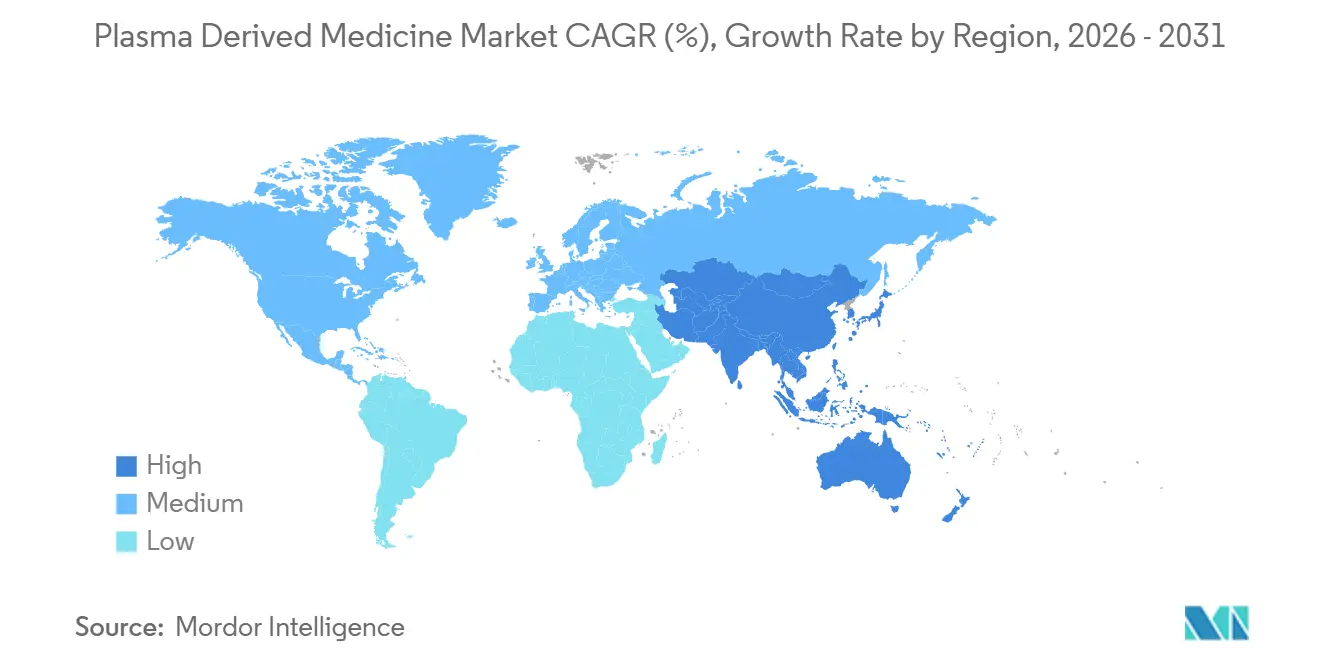

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Plasma Derived Medicine Market Analysis by Mordor Intelligence

The Plasma Derived Medicine Market size is estimated at USD 41.67 billion in 2026, and is expected to reach USD 58.77 billion by 2031, at a CAGR of 7.12% during the forecast period (2026-2031).

The growth trajectory reflects a structural shift toward home-based immunoglobulin therapy, national initiatives to achieve plasma self-sufficiency, and sustained capacity investments by vertically integrated fractionators. Governments in high-income countries are expanding reimbursement for subcutaneous immunoglobulin, while emerging markets such as Egypt and China are building domestic fractionation plants to curb dependence on United States imports. Capacity additions at CSL Behring, Takeda, and Octapharma are expected to narrow the global supply gap, yet seasonal donor shortfalls and complex regulatory pathways keep inventories tight. In parallel, the emergence of gene therapies and monoclonal antibodies is starting to displace plasma-derived coagulation factors in niche indications. Still, broad label coverage and decades-long safety records continue to anchor plasma products in first-line care.

Key Report Takeaways

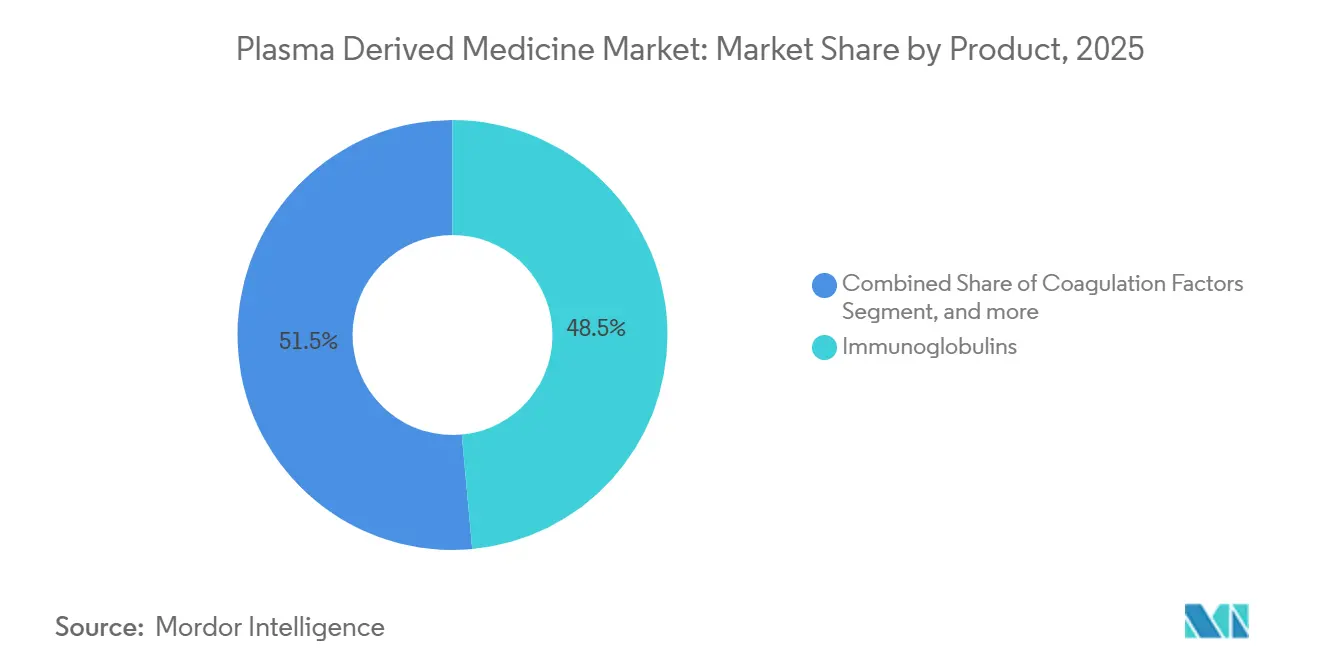

- By product category, immunoglobulins led with 48.54% of plasma derived medicine market share in 2025, whereas albumin is forecast to expand at a 9.54% CAGR through 2031.

- By application, pelvic inflammatory disease (PID) led with 25.32% of plasma derived medicine market share in 2025, whereas primary immune thrombocytopenia is forecast to expand at a 9.76% CAGR through 2031.

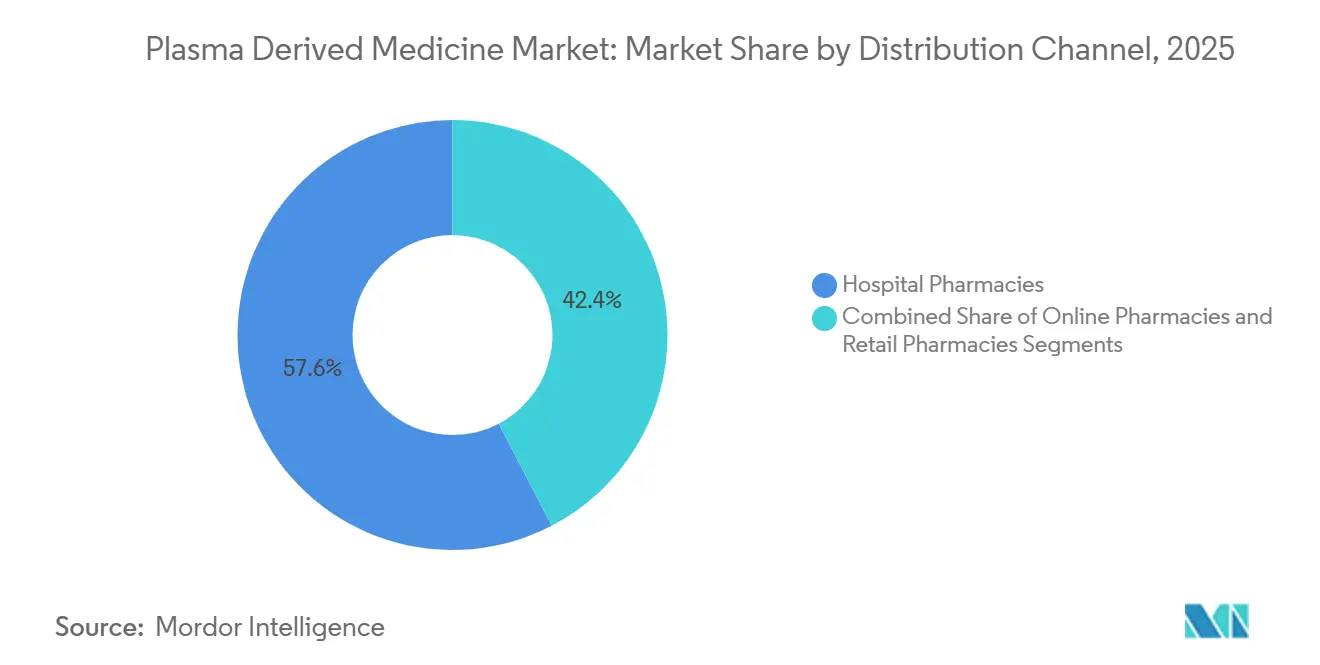

- By distribution channel, hospital pharmacies held 57.64% of the plasma derived medicine market size in 2025; online pharmacies are projected to register the fastest CAGR at 10.11% between 2026 and 2031.

- By end user, hospitals and clinics captured 54.32% revenue share in 2025, while the home-care segment is advancing at a 10.32% CAGR to 2031.

- By geography, North America commanded 43.12% revenue share in 2025, whereas Asia-Pacific is anticipated to post the highest regional CAGR at 8.54% during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Plasma Derived Medicine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Disease Burden | +1.2% | Global, acute pressure in North America, Europe, Japan | Long term (≥ 4 years) |

| Escalating Demand For Immunoglobulins | +1.8% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Capacity Expansion Initiatives | +1.5% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Technological Advancements In Plasma Processing | +1.0% | Global, led by major fractionation hubs | Medium term (2-4 years) |

| Shift Toward Home-Based Therapies | +1.3% | North America, Europe, urban Asia-Pacific | Short term (≤ 2 years) |

| Government Policies For Plasma Self-Sufficiency | +1.4% | U.K., Egypt, China, India | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Disease Burden

Global populations are aging, and expanded diagnostics are elevating the prevalence of primary immunodeficiency, chronic inflammatory demyelinating polyneuropathy, and multifocal motor neuropathy. The World Health Organization estimates that the proportion of individuals aged ≥60 will double from 12% in 2015 to 22% by 2050. Takeda secured Japanese approval in 2024 for GAMMAGARD LIQUID to treat myasthenia gravis, enlarging the eligible patient pool beyond classical immunodeficiency cohorts. Grifols’ Xembify gained European approval in October 2024 for chronic inflammatory demyelinating polyneuropathy, positioning subcutaneous immunoglobulin as a maintenance option. Longer treatment durations, coupled with label expansions by the FDA and EMA, are driving sustained volume growth even as biosimilars intensify competition in adjacent biologics.

Escalating Demand for Immunoglobulins

Clinical guidelines in North America and Europe continue to add neurological, dermatological, and hematological indications to immunoglobulin reimbursement lists. NHS England’s 2024 policy now funds therapy for 14 conditions, from Guillain-Barré syndrome to dermatomyositis. Production lead times of 7-12 months and the need to pool thousands of donations hard-wire supply rigidity[1]American Academy of Allergy, Asthma & Immunology, “IVIG Production and Supply,” AAAAI.ORG, aaaai.org. Octapharma began delivering immunoglobulins produced from UK-sourced plasma to NHS patients in March 2025, the country’s first domestic supply in almost three decades. CSL Behring’s Hizentra and Takeda’s Cuvitru dominate the subcutaneous segment, benefiting from payer-mandated step-therapy programs that prioritize at-home administration.

Capacity Expansion Initiatives

CSL Behring’s USD 800 million Facility F in Melbourne, operational since 2024, increased fractionation throughput by 50% through continuous chromatography. Takeda invested USD 230 million to modernize its Los Angeles site, enabling rapid switching between immunoglobulin and albumin products. Octapharma doubled albumin output at its Vienna plant after a EUR 200 million upgrade in 2024. Egypt’s EUR 280 million joint venture with Grifols secured EMA certification in December 2025, creating Africa’s first EU-grade plasma value chain. Lead times of three to five years mean that near-term shortages persist until these facilities reach full utilization.

Shift Toward Home-Based Therapies

Payers and patients prefer subcutaneous self-administration, which cuts treatment costs by 20-30% and eliminates venous access issues. Option Care Health reports that the typical immunoglobulin patient previously spent 90 hours per year in infusion suites. CVS Specialty leverages electronic health record integration to process over half of prescriptions without additional provider outreach, expediting home delivery. Optum Infusion Pharmacy employs more than 1,100 nurses and overturns 8 of 10 insurance denials, smoothing transitions from hospital to home. Grifols’ Xembify and Takeda’s Cuvitru are available in ready-to-use syringes, supported by virtual training modules that accelerate patient self-competence. Telehealth monitoring further reduces the need for in-person consultations, reinforcing the momentum toward decentralized care.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Plasma Supply | -0.9% | Global, pronounced in Europe and Asia-Pacific | Long term (≥ 4 years) |

| High Treatment Costs | -0.7% | Low- and middle-income markets, uninsured populations | Short term (≤ 2 years) |

| Complex Regulatory Landscape | -0.4% | Japan, India, EU, United States | Medium term (2-4 years) |

| Emergence Of Therapeutic Alternatives | -0.6% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Plasma Supply

Donor recruitment lags demand, creating chronic shortages that inflate raw-material costs. The American Red Cross reported a 40% decline in donors over two decades and a 7,000-unit shortfall during the 2024 holiday period[2]American Red Cross, “2024 National Blood Shortage,” REDCROSS.ORG, redcross.org. Europe sources roughly 40% of its plasma from the United States; EMA approval of Egypt’s plasma chain in 2025 aims to reduce that exposure. The United Kingdom collected 250,000 liters of plasma after lifting its 1998 ban yet targets only 25% immunoglobulin self-sufficiency by end-2025. U.S. donors receive USD 50-100 per session, whereas most European programs rely on unpaid volunteers, which constrains volume. Given a 7-12-month production cycle, seasonal disruptions propagate into prolonged inventory shortages across the plasma derived medicine market.

Emergence of Therapeutic Alternatives

Gene therapy fidanacogene elaparvovec cut factor IX use by 92% in the 2024 BENEGENE-2 trial[3]New England Journal of Medicine, “Fidanacogene Elaparvovec Trial Results,” NEJM.ORG, nejm.org. Nearly 60% of screened patients, however, were ineligible due to anti-AAV antibodies, preserving a sizeable demand base for plasma-derived factors. The FDA cleared Bkemv, an interchangeable Soliris biosimilar, in May 2024, introducing price competition in the complement-mediated disorders market. Recombinant C1-inhibitors and kallikrein inhibitors are gaining a hereditary angioedema share, while monoclonal antibodies such as rituximab offer indication-specific precision. Yet plasma products continue to hold the advantage of multi-indication approvals and lower per-dose costs in many health systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Albumin Accelerates as Critical-Care Protocols Tighten

Albumin accounted for a modest slice of 2025 revenue but is forecast to rise at a 9.54% CAGR, surpassing overall plasma derived medicine market growth. Trauma and burn guidelines increasingly specify plasma-derived albumin after synthetic colloids showed higher renal-failure risk. Immunoglobulins maintain dominance through expanded neurology and hematology labels, yet the market is diversifying as albumin use broadens in intensive care. Coagulation factors confront long-term headwinds from gene therapies, but a 59.5% exclusion rate for anti-AAV antibodies secures a residual patient base. Protease inhibitors, including Grifols’ THROMBATE III—FDA-approved for pediatric hereditary antithrombin deficiency in November 2025—hold niche but stable demand. The overall plasma derived medicine market size for albumin is projected to grow faster than immunoglobulins, underscoring shifting critical-care preferences.

Second-generation purification lines at Octapharma’s Vienna plant and modular skids at Takeda’s Los Angeles site bolster albumin output, aligning capacity with demand. Fractionators also explore high-concentration albumin formats to reduce infusion volumes. Although albumin pricing remains lower than immunoglobulins, rising volumes offset margin pressure. Immunoglobulin remains the core revenue pillar, but albumin’s burgeoning critical-care role illustrates portfolio diversification that de-risks dependence on any single protein class within the plasma derived medicine market.

By Application: ITP Therapies Record Fastest Uptick

Primary immune thrombocytopenia (ITP) therapies are projected to expand at a 9.76% CAGR to 2031, reflecting FDA approvals for Octapharma’s Panzyga and ADMA Biologics’ Asceniv in 2024. Pelvic inflammatory disease retained 25.32% of 2025 application revenue due to its broad clinical base, yet growth is moderate. Hemophilia demand edges downward as gene therapies launch, though many patients remain ineligible. Alpha-1 antitrypsin deficiency maintains steady uptake, supported by survival data from the RAPID trials. Subcutaneous C1-inhibitor gains hereditary angioedema share, displacing intravenous infusions.

The plasma derived medicine market share for ITP treatments is increasing as broader indications drive higher per-patient usage of immunoglobulins. Chronic inflammatory demyelinating polyneuropathy and Guillain-Barré syndrome also lift immunoglobulin volumes as maintenance protocols switch from hospital infusions to home-based regimens. Albumin applications in cirrhosis and hepatorenal syndrome grow in parallel with non-alcoholic steatohepatitis prevalence. Collectively, the application mix is tilting toward chronic autoimmune and liver disease indications, stabilizing demand against emerging therapeutic alternatives.

By Distribution Channel: E-Pharmacies Scale With Cold-Chain Integration

Hospital pharmacies delivered 57.64% of 2025 sales, reflecting the historical centrality of inpatient infusions. However, specialty e-pharmacies are forecast to grow at 10.11% CAGR as they integrate prior authorization, finance assistance, and cold-chain logistics. CVS Specialty processes more than half of immunoglobulin prescriptions electronically, trimming payer adjudication times. Option Care Health’s 170 infusion suites and Optum’s 30,000-patient base highlight the scale of outpatient transition. Retail pharmacies participate mainly through specialty divisions, handling limited volumes due to stringent storage and reimbursement protocols.

The plasma derived medicine market size attributed to e-pharmacies is set to climb as subcutaneous formats gain prevalence and home delivery reduces overall treatment cost. Cold-chain tracking, data-loggers, and temperature-controlled packaging are now standard, mitigating spoilage risk. E-pharmacies further differentiate by embedding telehealth consultations, enabling dose adjustments without clinic visits. Hospital pharmacies retain complex cases such as high-dose intravenous loads and adverse-event management, ensuring a multi-channel ecosystem.

By End User: Home-Care Gains Momentum Under Payer Pressure

Home-care settings are expected to post the fastest growth at 10.32% CAGR, propelled by payer mandates that require subcutaneous trials before authorizing hospital infusions. Hospitals and clinics still dominate acute treatments, notably for Guillain-Barré syndrome and severe infections, but their share is slowly eroding. Specialty infusion centers present an intermediary option, offering lower facility costs than hospitals and higher oversight than home settings. UPMC operates semi-private pods with zero-gravity chairs to attract stable patients who prefer a clinical environment.

The plasma derived medicine market share tied to home-care is expanding as training programs from Takeda, CSL Behring, and Grifols simplify self-administration. Telemonitoring platforms feed adherence data back to clinicians, minimizing in-person follow-ups. Payers cite 20-30% cost savings per treatment, reinforcing policy shifts toward decentralized care. Hospitals will continue handling patients with poor venous access or severe comorbidities, preserving a balanced end-user mix.

Geography Analysis

North America generated 43.12% of 2025 revenue, sustained by high per-capita immunoglobulin utilization and donor compensation models that supply roughly 65% of global plasma. The plasma derived medicine market size in Asia-Pacific is projected to expand fastest, at an 8.54% CAGR, as China, India, and Japan ramp domestic collection and fractionation. China’s National Medical Products Administration cleared multiple local immunoglobulin products in 2024-2025, aiding firms such as Hualan Biological Engineering to capture share from imports. India faces supply bottlenecks owing to low voluntary donation rates and bans on paid plasma; pending policy reforms could unlock unmet need.

Europe leans heavily on United States imports, prompting the United Kingdom to relaunch domestic collection. Octapharma delivered the first UK-sourced immunoglobulin batches in March 2026, aligning with government targets of 25% self-sufficiency in immunoglobulins by end-2025 and 80% in albumin by 2026. Egypt, certified by the EMA in December 2025, intends to serve regional demand in Africa and the Middle East once domestic needs are satisfied. South America and non-Egypt Africa remain import-dependent, procuring through government tenders due to limited fractionation infrastructure. Collectively, geographic diversification efforts indicate a gradual re-balancing of supply that could temper price volatility within the plasma derived medicine market.

Competitive Landscape

The top five players—CSL, Grifols, Takeda, Octapharma, and Kedrion—control about 70% of global fractionation capacity, reflecting moderate consolidation. CSL Behring’s Melbourne Facility F and Grifols’ Egyptian joint venture underscore strategic moves to secure regional plasma pools outside the mature U.S. donor base. Takeda’s modular skids in Los Angeles exemplify agile manufacturing that aligns batches with market signals. Octapharma leverages Vienna’s doubled albumin output to fulfill multi-year NHS contracts, while Kedrion strengthens its presence in Latin America through local collection partnerships.

Mid-tier firms pursue niche proteins: ADMA Biologics targets high-titer immunoglobulins for specific infections, and Kamada specializes in inhaled alpha-1 antitrypsin. Technology providers such as GEA supply automated fractionation systems that embed real-time analytics, reducing labor intensity for smaller players. Regulatory hurdles remain steep; FDA Biologics License Applications and EMA Plasma Master Files involve multi-year data packages and facility inspections. Gene therapies and biosimilars exert price pressure, yet plasma products retain competitive advantages in label breadth and cost per dose, sustaining their central role in the plasma derived medicine market.

Plasma Derived Medicine Industry Leaders

CSL Limited

Takeda Pharmaceutical

Grifols S.A.

Octapharma AG

Kedrion Biopharma

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Grifols, S.A., one of the global leaders in plasma-derived medicines and innovative healthcare solutions, received certification from the European Medicines Agency (EMA) for the entire value chain of Grifols Egypt for Plasma Derivatives (GEPD) in Egypt. The authority responsible for the scientific evaluation, supervision, and safety control of medicines in the European Union has endorsed that the entire Grifols Egypt plasma platform operates under the most demanding European standards of quality, safety, and regulatory control.

- December 2025: SKPlasma Core Indonesia, a joint venture

- November 2025: CSL, a biopharma company, expanded its United States presence over the next five years, resulting in approximately USD 1.5 billion in U.S. capital investments. These investments will generate hundreds of high-quality American jobs, strengthen U.S. manufacturing capabilities of plasma-derived therapies (PDTs), and help secure the U.S. medicine supply chain. This reflects CSL’s long-term commitment to meeting the growing clinical need for immunoglobulin (Ig).

Global Plasma Derived Medicine Market Report Scope

As per scope of the report, plasma-derived medicines are therapeutic products made from human blood plasma, containing essential proteins such as immunoglobulins, clotting factors, and albumin. They are used to treat various rare and chronic diseases, including immune deficiencies and bleeding disorders. These medicines are processed through fractionation and purification techniques to ensure safety and efficacy.

The Plasma Derived Medicine Market is Segmented by Product (Immunoglobulins, Coagulation Factors, Albumin, Protease Inhibitors, and Other Products), Application (Bleeding Disorders, Alpha-1 Antitrypsin Deficiency, Pelvic Inflammatory Disease, Hereditary Angioedema, CIDP, Guillain-Barré Syndrome, MMN, Liver Disease, ITP, Infections, and Other Applications), Distribution Channel (Hospital, Online, and Retail Pharmacies), End User (Hospitals & Clinics, Specialty Treatment Centers, and Home-Care), and Geography (North America, Europe, Asia-Pacific, MEA, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Immunoglobulins |

| Coagulation Factors |

| Albumin |

| Protease Inhibitors |

| Other Products |

| Bleeding Disorders |

| Alpha-1 Antitrypsin Deficiency (AATD) |

| Pelvic Inflammatory Disease (PID) |

| Hereditary Angioedema (HAE) |

| Chronic Inflammatory Demyelinating Polyneuropathy |

| Guillain-Barré Syndrome |

| Multifocal Motor Neuropathy |

| Liver Disease |

| Primary Immune Thrombocytopenia |

| Infections |

| Other Applications |

| Hospital Pharmacies |

| Online Pharmacies |

| Retail Pharmacies |

| Hospitals & Clinics |

| Specialty Treatment Centers |

| Home-Care Settings |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest Of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest Of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest Of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest Of South America |

| By Product | Immunoglobulins | |

| Coagulation Factors | ||

| Albumin | ||

| Protease Inhibitors | ||

| Other Products | ||

| By Application | Bleeding Disorders | |

| Alpha-1 Antitrypsin Deficiency (AATD) | ||

| Pelvic Inflammatory Disease (PID) | ||

| Hereditary Angioedema (HAE) | ||

| Chronic Inflammatory Demyelinating Polyneuropathy | ||

| Guillain-Barré Syndrome | ||

| Multifocal Motor Neuropathy | ||

| Liver Disease | ||

| Primary Immune Thrombocytopenia | ||

| Infections | ||

| Other Applications | ||

| By Distribution Channel | Hospital Pharmacies | |

| Online Pharmacies | ||

| Retail Pharmacies | ||

| By End User | Hospitals & Clinics | |

| Specialty Treatment Centers | ||

| Home-Care Settings | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest Of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest Of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest Of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest Of South America | ||

Key Questions Answered in the Report

What is the projected value of the plasma derived medicine market in 2031?

It is forecast to reach USD 58.77 billion, growing at a 7.12% CAGR.

Which product segment is growing fastest?

Albumin, advancing at a 9.54% CAGR due to expanded use in critical-care resuscitation.

Why are home-care settings gaining traction?

Payers save 20-30% per treatment and patients prefer the convenience of subcutaneous self-administration.

How severe is plasma supply risk?

Donor numbers have declined 40% in the United States over two decades, creating chronic shortages that restrain output.

Which region is expected to post the highest growth rate?

Asia-Pacific is projected to expand at an 8.54% CAGR as China, India, and Japan scale domestic fractionation.

Do gene therapies threaten plasma products?

They reduce factor consumption in eligible hemophilia patients but high antibody exclusion rates and broad label coverage keep plasma-derived therapies relevant.

Page last updated on: