Plant-Based Meat Nutrition Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 12.10 Billion |

| Market Size (2031) | USD 29.13 Billion |

| Growth Rate (2026 - 2031) | 19.29% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Plant-Based Meat Nutrition Market Analysis by Mordor Intelligence

The Plant-Based Meat Nutrition Market size is projected to expand from USD 10.10 billion in 2025 and USD 12.10 billion in 2026 to USD 29.13 billion by 2031, registering a CAGR of 19.29% between 2026 to 2031.

Quick-service restaurants (QSRs) are now focusing on increased menu penetration and fortifying dishes to address micronutrient gaps, surpassing traditional shelf-placement strategies. In Europe, the rapid growth of private-label adoption, along with continuous-production retrofits that lower the cost of goods sold, is transforming the competitive landscape. Furthermore, precision-fermented lipids are gaining traction by replicating the mouthfeel of animal fats. Ingredient scale-up contracts, such as Roquette’s 125,000-metric-ton pea-protein plant, indicate a structural cost reduction, enabling premium sensory profiles to target the mass market. Meanwhile, the Asia-Pacific region is experiencing a recovery, with innovations in local cuisines such as dumplings, hot-pot balls, and stir-fry strips avoiding the sensory benchmarks set by Western staples like burgers and sausages.

Key Report Takeaways

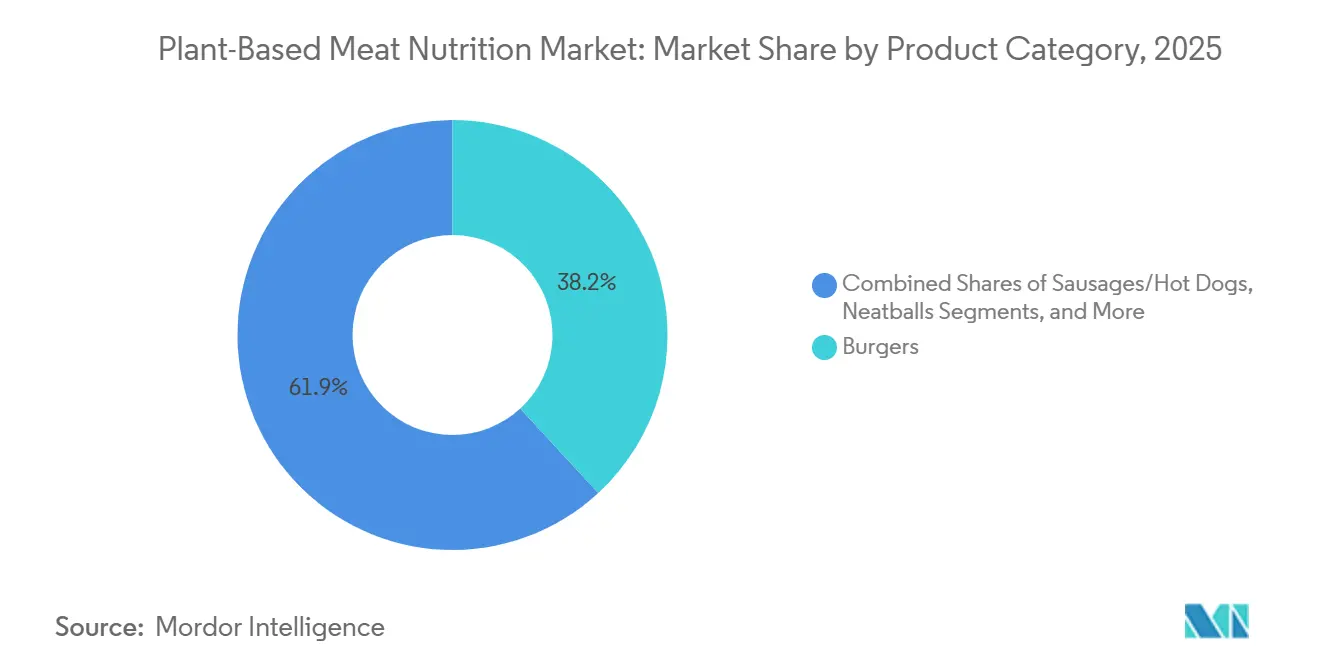

- By product category, burgers held 38.15% of the plant-based meat nutrition market share in 2025, while sausages and hot dogs are forecast to grow at a 21.35% CAGR through 2031.

- By source protein, soy captured 46.29% share of the plant-based meat nutrition market size in 2025; faba, chickpea, and lentil blends are advancing at a 22.16% CAGR.

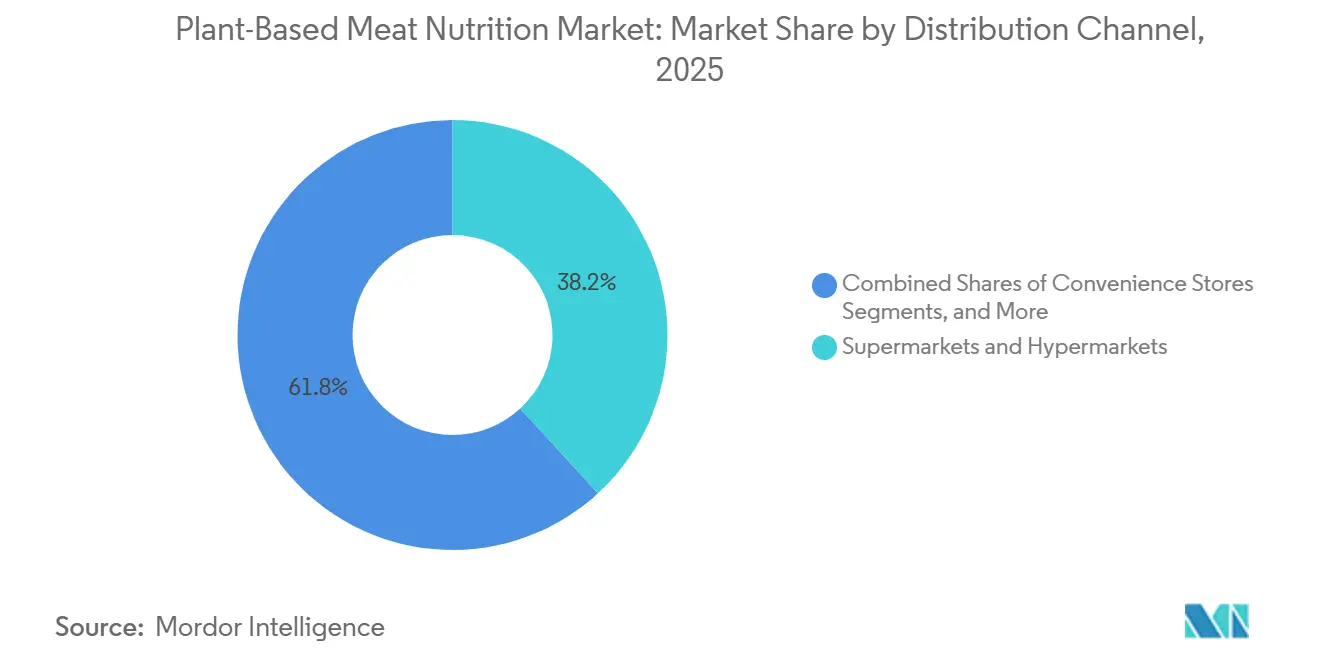

- By distribution channel, supermarkets and hypermarkets accounted for a 38.16% share in 2025, whereas foodservice and HoReCa segments will expand at a 22.89% CAGR to 2031.

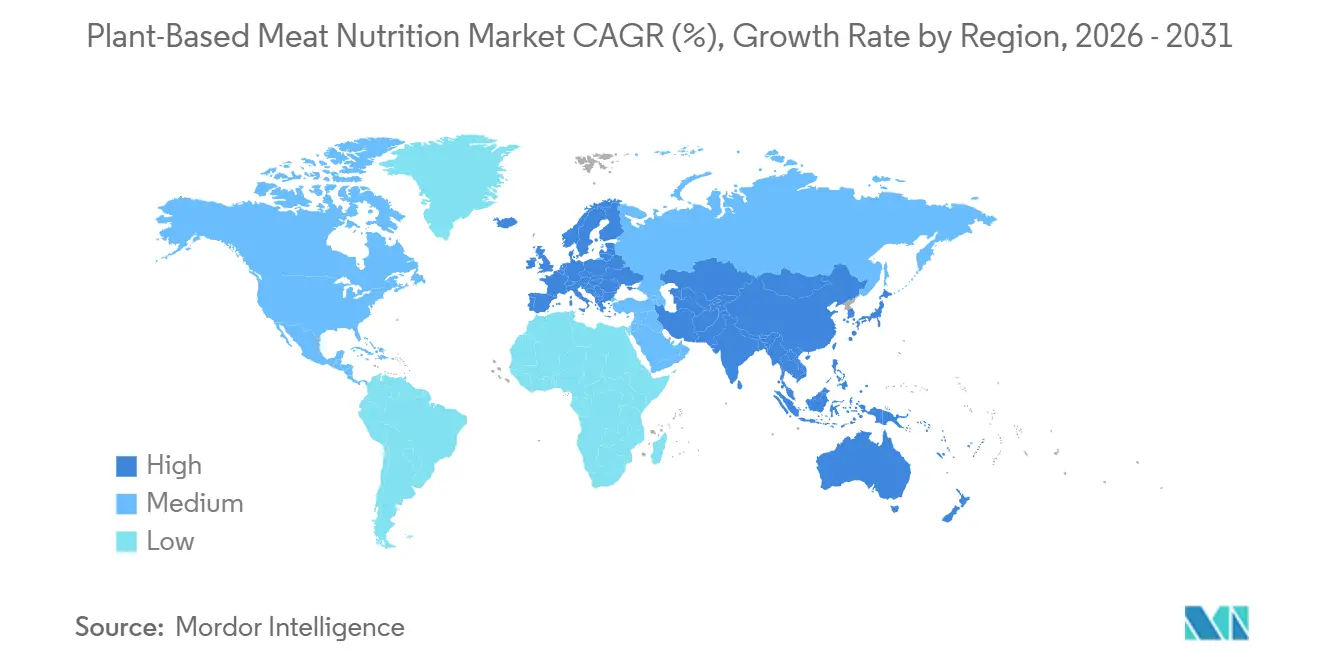

- By geography, North America retained 32.18% of the plant-based meat nutrition market share in 2025, yet Asia-Pacific is projected to register a 22.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Plant-Based Meat Nutrition Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Taste-and-texture parity progress (high-moisture extrusion, flavor systems) | +4.2% | Global, with early gains in North America and Western Europe | Medium term (2-4 years) |

| Foodservice/QSR menu penetration and co-branded launches | +5.1% | North America, Europe, APAC urban centers | Short term (≤ 2 years) |

| Retail and private-label expansion, improved shelf placement | +3.8% | Europe core, North America secondary, emerging APAC | Medium term (2-4 years) |

| Ingredient scale-up (soy/pea/mycoprotein) reducing costs | +4.6% | Global, with capacity concentration in North America and Northern Europe | Long term (≥ 4 years) |

| Fortification (B12, Iron, Zinc, Omega-3) closing nutrition gaps | +2.9% | Global, regulatory influence strongest in EU and North America | Medium term (2-4 years) |

| Structured fats/oleogels and fermentation-derived lipids lowering saturated fat | +3.4% | North America and EU, spill-over to APAC premium segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Taste-and-Texture Parity Progress (High-Moisture Extrusion, Flavor Systems)

High-moisture extrusion (HME) now aligns plant proteins into anisotropic fibers that replicate the mouthfeel of whole-muscle chicken. Twin-screw systems operating at 60-70% moisture reduce residence time and enable in-line flavor injection, cutting cycle time by 40% at Alpha Foods facilities. Fermentation-derived heme from Impossible Foods and precision-fermented lipids from Nourish Ingredients replicate Maillard browning and enhance umami depth, driving repeat-purchase intent beyond 40% in controlled trials.

Foodservice/QSR Menu Penetration and Co-Branded Launches

Bypassing retail slotting fees, QSRs offer affordable trial formats that position plant proteins as mainstream. McDonald’s expanded the McPlant burger to 600 U.S. outlets in 2024 and maintains year-round availability across the United Kingdom.[1]McDonald’s, “McPlant Expansion Fact Sheet,” mcdonalds.com Beyond Meat’s agreement with Yum! Brands integrates plant-based proteins into 55,000 outlets, normalizing consumption across breakfast, lunch, and snacking occasions. Heura Foods is extending category reach into airlines and cruise lines, increasing high-frequency exposures that build sensory familiarity.

Retail and Private-Label Expansion, Improved Shelf Placement

European grocers are leveraging private-label strategies to protect margins and differentiate their offerings. Lidl GB tripled its Vemondo Plant! lineup to 28 SKUs in 2024 and targets a 25% plant-protein share of total protein sales by 2030. U.S. retailers are adopting similar approaches: Beyond Meat expanded to over 2,000 Walmart stores in 2025, transitioning from specialty aisles to refrigerated meat cases and capturing cross-category impulse purchases. THIS utilized its April 2026 deli-slices launch to secure partnerships with three national chains, benefiting from reduced flavor-masking requirements in cured-meat analogs.

Ingredient Scale-Up (Soy/Pea/Mycoprotein) Reducing Costs

Roquette’s Manitoba facility produces 125,000 tons of pea isolate, securing multiyear contracts with Beyond Meat to shield margins from commodity price fluctuations.[2]Enifer, “PEKILO Mycoprotein Factory Announcement,” enifer.com Lantmännen’s SEK 1.2 billion investment in pea protein targets an annual capacity of 7,000 tons with neutral flavor profiles suitable for clean-label claims. Enifer’s 3,000-ton PEKILO mycoprotein plant, funded by EUR 36 million in 2024, achieves production costs below USD 2.00 per kilogram, positioning fungal proteins on cost parity with soy isolates.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Sensory gap vs. Conventional meat and inconsistent cooking performance | -3.7% | Global, most acute in North America and Europe | Short term (≤ 2 years) |

| Price premium and input cost volatility (proteins, oils, capacity) | -4.9% | Global, with highest elasticity in price-sensitive APAC and Latin America | Medium term (2-4 years) |

| Labeling restrictions/clean-label pressures increasing compliance complexity | -2.1% | Europe and North America regulatory cores, spill-over to export markets | Long term (≥ 4 years) |

| Retail assortment rationalization and slotting fees constraining shelf space | -2.8% | North America and Western Europe, emerging in organized retail APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Sensory Gap Vs. Conventional Meat and Inconsistent Cooking Performance

Home cooks expecting beef-like doneness often experience frustration when plant-based patties, grilled at temperatures above 200°C, char externally while remaining undercooked internally. This issue hampers repeat purchases. Brands pursuing clean-label claims face difficulties as off-notes, described as “beany” or “earthy,” are linked to residual saponins in pea and faba isolates. Additionally, year-to-year crop variability can cause water-holding capacity to fluctuate by up to 15%, necessitating mid-cycle reformulations and diminishing brand trust.

Price Premium and Input Cost Volatility (Proteins, Oils, Capacity)

In 2025, plant-based ground meat in U.S. supermarkets was priced at an 80% premium compared to conventional beef, limiting the category's penetration to less than 3% of total meat sales.[3]Good Food Institute, “Plant-Based Chicken Market Update,” gfi.org Drought conditions in Canada caused pea-protein isolate prices to vary between USD 4.50 and 6.20 per kilogram in 2024-2025. Sunflower oil prices increased by 25% due to disruptions in the Black Sea, driving up formulation costs for products reliant on liquid oils for juiciness.[4]Lantmännen, “Investment in Pea-Protein Production,” lantmannen.com Capacity constraints persist, with Roquette’s plant operating at nearly 95% utilization and new-contract lead times exceeding 18 months.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Category: Sausages Surge as Breakfast and Snack Occasions Multiply

Sausages and hot dogs are projected to grow at a 21.35% CAGR, surpassing burgers, which are expected to maintain a 38.15% share of the plant-based meat nutrition market in 2025. Quick-service restaurant (QSR) breakfast menus and stadium concessions are increasingly incorporating plant-based options, appealing to casual diners seeking convenient handheld formats. Nugget and wing applications use breading and sauce layers to mask lingering legume off-flavors, resulting in repeat-purchase rates 10-15 percentage points higher than those for uncoated patties. Europe’s deli-slice growth highlights a cost-efficient sub-category, as reduced thermal load and shorter extrusion lengths lower capital expenditure and enhance protein functionality.

The premium burger segment is evolving. In late 2025, a rapid update to heme-flavor systems reduced metallic aftertaste scores by 30% in sensory panels, stabilizing market share in North America. Meatball and ready-meal kits are gaining traction among time-pressed households, but their placement in the frozen aisle limits impulse purchases, highlighting the challenge of balancing convenience with visibility. The diversification of product categories is outpacing freezer capacity, forcing retailers to prioritize high-velocity products.

By Source Protein: Faba and Chickpea Blends Take on Soy’s Allergen Challenges

Soy maintained a 46.29% market share in 2025, driven by its functional reliability and competitive pricing below USD 3.00 per kilogram. However, the market for faba- and chickpea-blend products is expected to grow at a 22.16% CAGR, as brands focus on allergen-friendly and GMO-free labels that resonate with European parents. Pea proteins dominate North American products due to their scalability, but green off-notes require expensive flavor-masking systems, challenging clean-label objectives.

Mycoprotein is emerging as a significant opportunity. Biomass fermentation processes deliver complete amino-acid profiles without straining agricultural land, achieving production costs comparable to soy isolates. Wheat-gluten fibers provide superior striation in high-moisture extrusion but face limitations due to celiac concerns. Lentil blends offer natural red-brown coloration that mimics cooked beef, reducing the need for caramel color and improving additive-free scores in the EU. Over the forecast period, diversifying protein sources mitigates supply risks and aligns with increasingly stringent clean-label regulations in OECD markets.

By Distribution Channel: Foodservice Skips Slotting Fees, Boosts Trials

Supermarkets and hypermarkets accounted for 38.16% of the 2025 volume, supported by aggressive private-label initiatives. However, foodservice channels are expected to grow at a 22.89% CAGR, driving the plant-based meat nutrition market by introducing price-sensitive diners to subsidized trial portions, which improve sensory acceptance. Co-branded products, such as plant-based nuggets and toppings, streamline market entry compared to the fragmented retail buyer process.

Convenience stores are expanding into hot-hold plant-based sausages, increasing category visibility during breakfast hours. Online grocery platforms are attracting high-income vegan shoppers with subscription bundles, but high frozen fulfillment fees of USD 30-40 per parcel reduce net margins and limit participation in value-tier segments. Specialty natural-food retailers, while representing less than 5% of total plant-protein sales, remain critical for flavor and format innovation.

Geography Analysis

In 2025, North America claimed a dominant 32.18% share of the plant-based meat nutrition market, driven by expansions from major players like Walmart and McDonald’s, which extended their reach beyond coastal early adopters. Declining costs and advancements in fortification position the market for mid-teens growth, despite ongoing debates over dairy-style naming conventions under FDA jurisdiction. Additionally, Canada’s Prairie grain belts, supplying local pea protein, help U.S. brands mitigate foreign-exchange risks.

Europe, influenced by the EU Green Deal and ISO 8700:2025 harmonization, is increasing institutional procurement of plant proteins for school lunch programs. However, a proposal from the European Parliament in October 2025 to ban 29 meat-related descriptors introduces branding uncertainties, potentially delaying new SKU launches until resolutions are reached. While Germany and the U.K. lead in volume, Spain’s growth in cold cuts highlights format-specific market opportunities.

Asia-Pacific is set to outpace others with the fastest CAGR at 22.05%. Dominant e-commerce platforms JD.com and Douyin collectively account for over 40% of China's plant-based meat sales, enabling swift market rollouts and real-time consumer insights. Japan and South Korea maintain premium prices exceeding USD 14 per pound, but limited cold-chain infrastructure outside major cities restricts broader market scaling.

Competitive Landscape

In a fragmented market, the top five players accounted for less than 40% of the 2025 revenue. This fragmentation allows regional specialists to outperform global giants in flavor localization and agile sourcing. Major meat players like Cargill and Tyson utilize their refrigerated networks to introduce blended burgers. Meanwhile, dedicated disruptors are turning to venture funds to support their extrusion lines and fermentation tanks. Enifer and The Protein Brewery, having secured a combined EUR 66 million in 2024-2025, highlight investor confidence in biomass fermentation's potential to challenge the dominance of soy and pea, aiming for costs below USD 2.00 per kilogram.

Patent portfolios act as strategic defenses. With over 100 patents, Impossible Foods protects its soy leghemoglobin, while Heura Foods, with its patented thermo-mechanical extrusion, offers a cleaner EU label by eliminating methylcellulose. Upstart brands leverage direct-to-consumer channels for detailed data, accelerating flavor iterations. However, rising digital advertising costs are putting pressure on their unit economics. As capacity tightens, contract manufacturers are emerging, providing asset-light scalability but at the cost of reducing margins.

Brands from earlier generations, once dominant with coconut-oil burgers, have lost shelf space to newer lines enriched with vitamins and lower in saturated fats, aligning with cardiology recommendations. Retailers are streamlining their assortments, focusing on velocity leaders and cutting back on SKUs that do not meet the benchmark of 15 units sold per store weekly. As a result, attributes like supply-chain resilience, fortification, and culinary versatility are becoming the new benchmarks of competition.

Plant-Based Meat Nutrition Industry Leaders

Beyond Meat, Inc.

Impossible Foods Inc.

Conagra Brands, Inc.

Maple Leaf Foods Inc.

Cargill, Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: THIS debuted York-style plant-based deli slices in Waitrose, Sainsbury’s, and Morrisons, targeting cold-cut demand and leveraging lower processing costs relative to whole-muscle analogs.

- May 2025: Heura Foods obtained a EUR 20 million European Investment Bank loan to fund R&D and new extrusion equipment, complementing a EUR 40 million Series B led by Upfield.

- May 2025: Beyond Meat secured USD 100 million financing from Ahimsa Holdings to sustain Walmart distribution and finance continuous-production retrofits that cut cost of goods sold to USD 4.23 per kilogram

Global Plant-Based Meat Nutrition Market Report Scope

As per the scope of the report, plant-based meat nutrition refers to the specific profile of macronutrients, vitamins, and minerals found in meat substitutes made entirely from plant-derived ingredients. While designed to mimic the taste, texture, and appearance of conventional animal meat, their chemical and nutritional structures are fundamentally different.

The plant-based meat nutrition market is segmented by product category, source protein, distribution channel, and geography. By product category, the market includes burgers, ground/minced, sausages/hot dogs, nuggets/tenders/wings, deli slices/cold cuts, meatballs, ready meals/prepared, seafood analogues, and jerky/snacks. By source protein, it is segmented into soy, pea, wheat/gluten, mycoprotein (biomass fermentation), faba/chickpea/lentil, rice/other cereals, and canola/rapeseed & novel plant sources. By distribution channel, the categories include supermarkets & hypermarkets, convenience stores, online/e-commerce, specialty health/natural stores, foodservice/HoReCa, direct-to-consumer (D2C) brand sites, and B2B ingredients supply to manufacturers. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Burgers | |

| Ground/Minced | |

| Sausages/Hot Dogs | Overall Market size numbers |

| Nuggets/Tenders/Wings | |

| Deli Slices/Cold Cuts | |

| Meatballs | |

| Ready Meals/Prepared | Segmentation market share and growth forecasts |

| Seafood Analogues | |

| Jerky/Snacks |

| Soy |

| Pea |

| Wheat/Gluten |

| Mycoprotein (biomass fermentation) |

| Faba/Chickpea/Lentil |

| Rice/Other Cereals |

| Canola/Rapeseed & Novel Plant Sources |

| Supermarkets & Hypermarkets |

| Convenience Stores |

| Online/E-commerce |

| Specialty Health/Natural Stores |

| Foodservice/HoReCa |

| Direct-to-Consumer (D2C) Brand Sites |

| B2B Ingredients Supply to Manufacturers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of APAC | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of MEA | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Category | Burgers | |

| Ground/Minced | ||

| Sausages/Hot Dogs | Overall Market size numbers | |

| Nuggets/Tenders/Wings | ||

| Deli Slices/Cold Cuts | ||

| Meatballs | ||

| Ready Meals/Prepared | Segmentation market share and growth forecasts | |

| Seafood Analogues | ||

| Jerky/Snacks | ||

| By Source Protein | Soy | |

| Pea | ||

| Wheat/Gluten | ||

| Mycoprotein (biomass fermentation) | ||

| Faba/Chickpea/Lentil | ||

| Rice/Other Cereals | ||

| Canola/Rapeseed & Novel Plant Sources | ||

| By Distribution Channel | Supermarkets & Hypermarkets | |

| Convenience Stores | ||

| Online/E-commerce | ||

| Specialty Health/Natural Stores | ||

| Foodservice/HoReCa | ||

| Direct-to-Consumer (D2C) Brand Sites | ||

| B2B Ingredients Supply to Manufacturers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of APAC | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of MEA | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the plant-based meat nutrition space today and where is it headed by 2031?

Sales reached USD 12.1 billion in 2026 and are forecast to climb to USD 29.3 billion by 2031, reflecting a 19.29% CAGR over 2026-2031.

Which product format is growing fastest?

Sausages and hot dogs are projected to post a 21.35% CAGR through 2031, outpacing burgers and nuggets.

What protein sources are gaining momentum beyond soy?

Faba-, chickpea-, and lentil-based blends are set to expand at a 22.16% CAGR as brands pursue allergen-friendly and clean-label formulations.

Why are QSR partnerships critical for category growth?

Foodservice bypasses retail slotting fees, offers subsidized trial portions, and now drives the strongest incremental volume gains thanks to nationwide rollouts at chains like McDonalds and KFC.

Which region offers the highest growth trajectory?

Asia-Pacific is expected to register a 22.05% CAGR as China's rebound and localized formats such as dumplings and hot-pot slices accelerate adoption.

How concentrated is competitive rivalry in this field?

The top five suppliers hold under 40% of global sales, signaling moderate concentration and ample room for regional specialists and new entrants to scale.

Page last updated on: