PIM For Genomics and Life Science Computing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

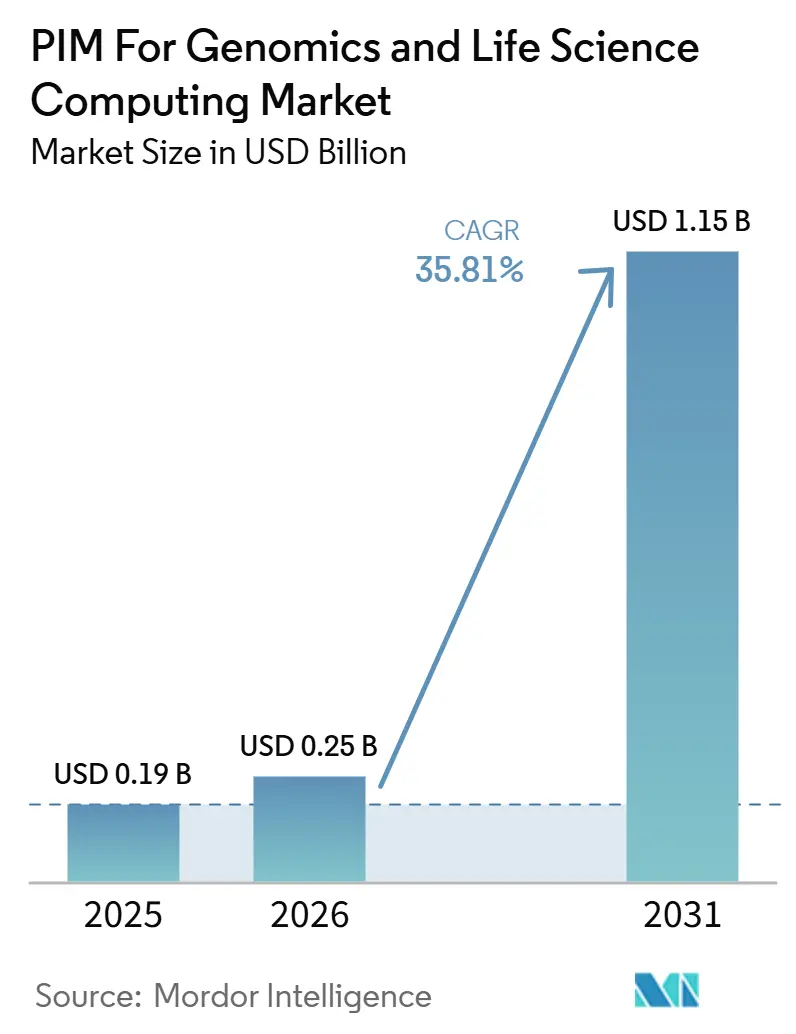

| Market Size (2026) | USD 0.25 Billion |

| Market Size (2031) | USD 1.15 Billion |

| Growth Rate (2026 - 2031) | 35.81% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

PIM For Genomics and Life Science Computing Market Analysis by Mordor Intelligence

The PIM for genomics and life science computing market size is projected to expand from USD 0.19 billion in 2025 and USD 0.25 billion in 2026 to USD 1.15 billion by 2031, registering a CAGR of 35.81% between 2026 and 2031. The PIM for the genomics and life science computing market is being driven by the rapid growth of multimodal biological data and the wider recognition that scientific data governance now affects research speed, compliance quality, and commercial readiness. Generic enterprise product information tools do not fully address FAIR data principles, regulated traceability, and scientific file types, which keeps demand focused on life-science-specific platforms. The 2026 baseline already shows that pharmaceutical and biotechnology organizations are redesigning data environments to support AI-ready workflows and cleaner metadata control. The PIM for the genomics and life science computing market is also being shaped by a clear split between vendors that adapt broad enterprise platforms for life science use and those that build from the ground up around genomics-native workflows. Cloud adoption, distributed research models, and tighter cross-border data rules are widening the opportunity for platforms that combine governance, collaboration, and regulatory readiness into a single stack.

Key Report Takeaways

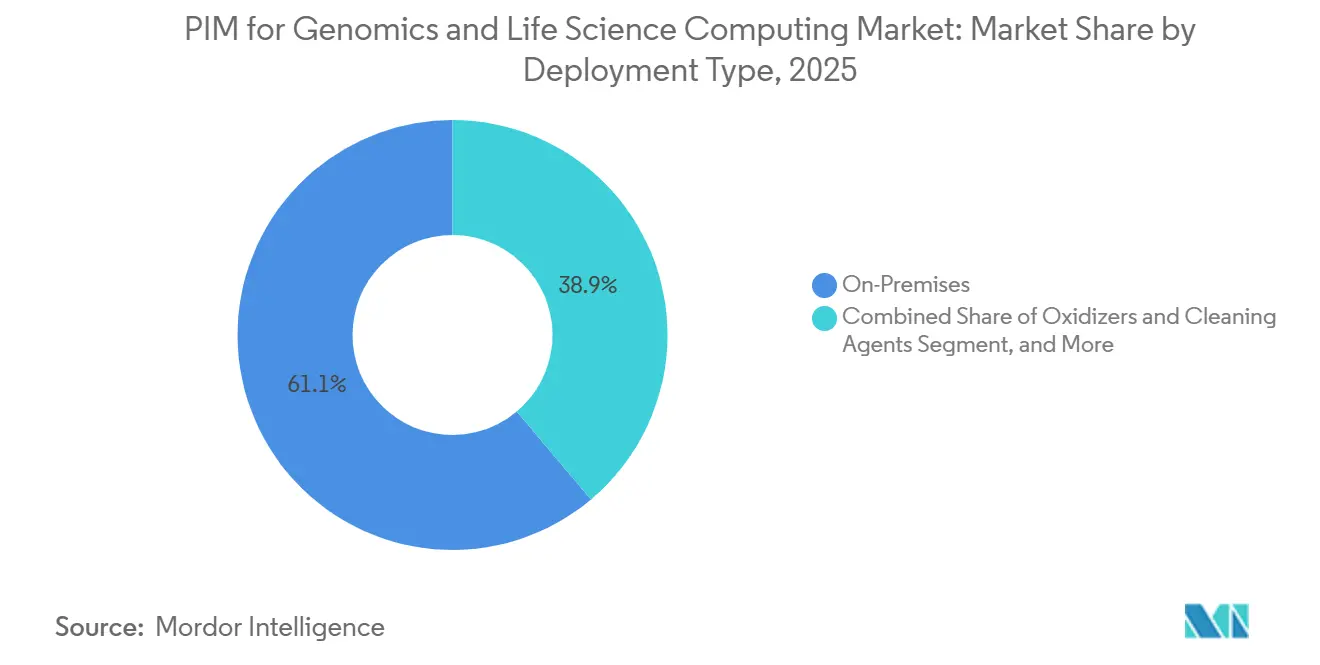

- By deployment type, on-premises held a 61.13% of the PIM for genomics and life science computing market in 2025, while cloud-based deployments are projected to expand at a 36.48% CAGR through 2031.

- By component, hardware accounted for 78.62% of the PIM for genomics and life science computing market in 2025, while software is projected to expand at a 36.42% CAGR through 2031.

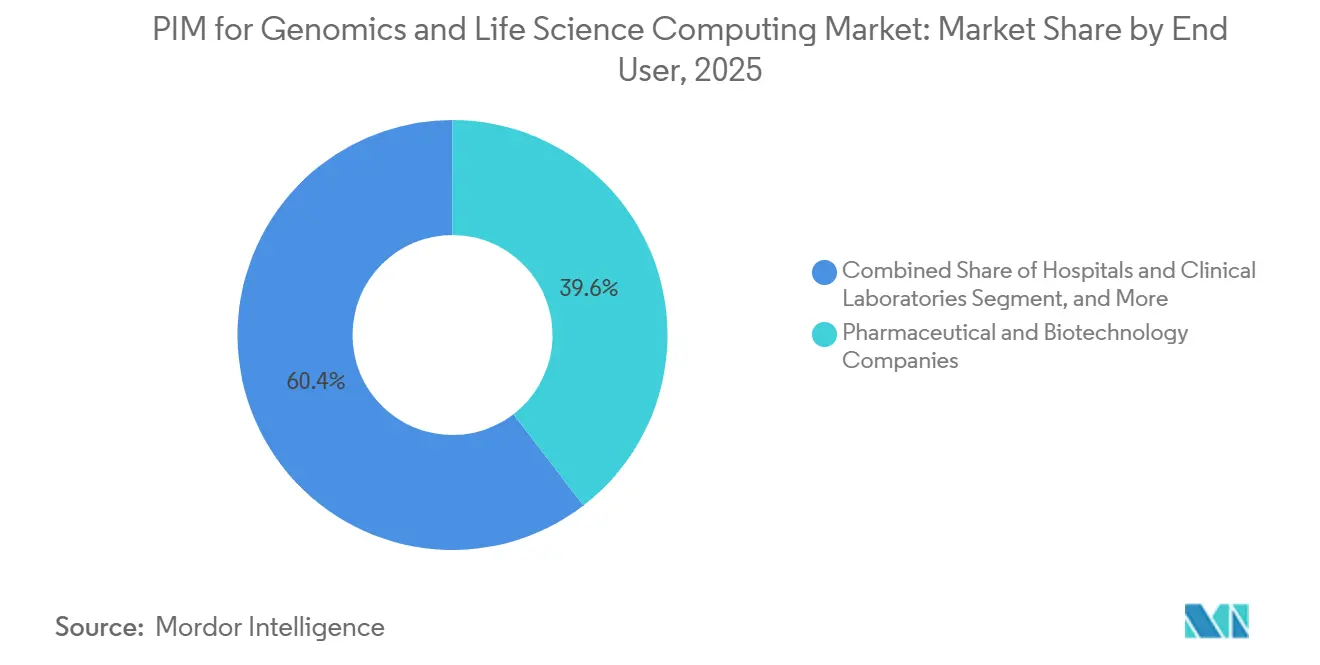

- By end user, pharmaceutical and biotechnology companies held 39.58% share in 2025, while hospitals and clinical laboratories are projected to advance at a 36.84% CAGR through 2031.

- By application, sequence alignment and mapping accounted for 35.19% share in 2025, while multi-omics analysis is projected to grow at a 37.02% CAGR through 2031.

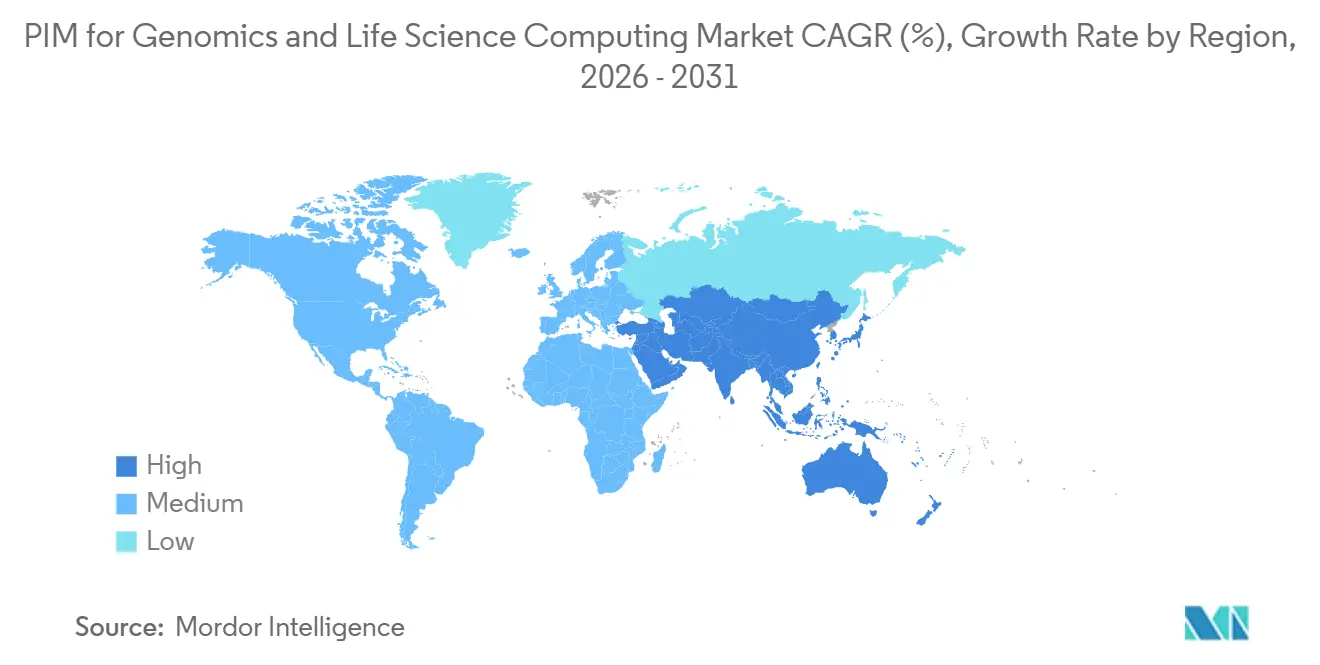

- By geography, North America held 46.67% share in 2025, while Asia-Pacific is projected to record the fastest regional CAGR at 36.73% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global PIM For Genomics and Life Science Computing Market Trends and Insights

AI-Driven Genomic Data Curation and Variant Interpretation

Artificial intelligence is changing the role of the PIM in the genomics and life science computing market from passive storage to active curation and interpretation. DNAnexus expanded this shift in May 2026, launching Omics Data Agent for no-code cohort creation and longitudinal queries, along with an AutoML Assistant that reduced model prototyping time by up to 80%. Illumina moved in the same direction in 2026 when DRAGEN v4.5 extended machine learning support for structural variant calling across germline and somatic use cases and added support for 5-base multiomic analyses. A 2026 study in the Journal of Translational Medicine showed that AI-assisted genomic analysis can combine phenotype standardization, pathogenicity ranking, and structured reporting in a traceable workflow for rare-disease diagnosis. These developments matter because curated evidence becomes easier to reuse once it is linked to consistent metadata, reporting logic, and version control. For the PIM for genomics and life science computing market, that means AI curation is moving from a premium feature to a core buying requirement for labs, biopharma teams, and regulated clinical users.

Rising Need For Interoperable Data Governance Across LIMS, EHR, and PIM Stacks

Interoperability is becoming a central demand in the PIM for genomics and life science computing market because laboratories, clinical systems, and product data environments now need shared governance rather than simple file exchange. QIAGEN Digital Insights showed this need in its November 2025 QCI Interpret update, which expanded expert curation coverage to around 1,100 genes and added multilingual reporting for global clinical genomics operations.[1]QIAGEN Digital Insights, “QCI Interpret November 2025 Release,” QIAGEN Digital Insights, digitalinsights.qiagen.com Illumina's Emedgene software also integrates with LIMS, EHR, and other IT systems while maintaining a lab-curated repository that can populate interpretation templates in a controlled way. ISO/TS 21405:2026 adds another layer by establishing a formal framework for IDMP ontology development and semantically interoperable medicinal product data. This keeps interoperability from being a one-time integration project, since metadata models, reporting structures, and governance rules have to remain aligned as systems change. The PIM for genomics and life science computing market is therefore benefiting from demand for platforms that can manage data context across research, clinical, and regulatory environments without breaking auditability.

Regulatory Pressure for Audit-Ready Traceability in Clinical and Product Data

Regulation is turning traceability into a platform requirement in the PIM for genomics and life science computing market, rather than a later-stage customization. The European Health Data Space regulation, adopted in February 2025, requires health data access bodies in each EU member state and creates structured secondary-use permit pathways for health data. ISO/TS 21405:2026 reinforces this direction by providing life science data teams with a formal method for representing the IDMP ontology in a FAIR-compliant way. DNAnexus has responded by positioning Trusted Regulatory Spaces for regulated cloud collaboration, with FISMA and FedRAMP authorizations, 21 CFR Part 11 validation, and integration with Veeva Vault for regulatory submissions and review. This matters because buyers are increasingly asking whether a platform is already audit-ready, not whether compliance features can be added later. The PIM for the genomics and life science computing market is gaining momentum as compliance expectations deepen into everyday data architecture and workflow design.

Increasing Demand for Cloud-Native Collaboration Across Distributed Research Networks

The PIM for genomics and life science computing market is being pushed toward cloud-native collaboration because multi-site research programs need controlled access to shared data without relying on a single local environment. Nature Genetics noted in 2026 that, as multi-omics moves closer to routine clinical care, the harder problem is no longer data generation but standardization and interpretation across growing complexity. DNAnexus reinforced this trend in May 2026 with the Omics Data Catalog, designed to make multimodal scientific data discoverable, governed, and reusable in a cloud environment. Illumina's February 2026 TruPath Genome launch also showed how distributed adoption can scale quickly, with more than 30 early-access customers including Broad Clinical Labs, GeneDx, Rady Children's Hospital, and Baylor College of Medicine. Cloud models matter here because collaboration now depends on governed metadata, reusable pipelines, and clear access rights across institutional boundaries. As a result, the PIM for the genomics and life science computing market is moving toward platforms that support AI readiness, shared workspaces, and compliance within a single operating model.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Integration Cost with Legacy Life Science Systems | -2.8% | Global, most acute in North America and Europe, where legacy GxP system penetration is deepest | Medium term (2-4 years) |

| Data Privacy, Sovereignty, and Compliance Complexity | -2.3% | EU, China, and the United Kingdom, with cross-border friction spilling into the Asia-Pacific | Long term (≥ 4 years) |

| Fragmented Scientific Data Models and Workflow Incompatibility | -1.8% | Global, with the highest friction in academic and multi-site research settings | Medium term (2-4 years) |

| Limited In-House Bioinformatics and Data Governance Skills | -1.4% | Emerging Asia-Pacific markets and smaller biopharma organizations globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Integration Cost with Legacy Life Science Systems

Legacy life science systems' slow adoption in the PIM for genomics and life science computing market because new tools must fit into validated environments that already support regulated work. Boehringer Ingelheim's One Medicine Platform, launched with Veeva in March 2025, connected clinical, regulatory, and quality data across its global R&D organization, which shows how broad these transformation programs need to be before value can be realized. Illumina's Emedgene material also highlights the number of interfaces involved, as the software connects to LIMS, EHR, and other IT systems while keeping interpretation workflows secure and structured. DNAnexus frames Trusted Regulatory Spaces around validated cloud collaboration, indicating that vendors now have to package compliance support with the platform itself. This increases the time, planning, and service burden associated with each rollout, especially when organizations are replacing long-standing workflows rather than adding isolated point tools. Vendors that reduce implementation friction are therefore in a stronger position as buyers compare migration effort against near-term productivity gains in the PIM for genomics and life science computing market.

Data Privacy, Sovereignty, and Compliance Complexity

Data privacy remains a structural restraint in the PIM for genomics and life science computing market because genomic data is treated as a special category of personal data under multiple legal regimes. A 2026 article in Frontiers in Genetics described a polycentric compliance environment in which the EHDS, GDPR, the Data Governance Act, and GA4GH standards overlap without creating automatic legal interoperability. The EHDS regulation adds further process obligations through national access bodies and secondary-use permit structures, affecting cross-border clinical and research data handling. The United Kingdom also tightened its stance in July 2026, when parliamentary guidance classified cross-border transfers of human genomic data as a high-harm risk and called for role-based assessments for international movement. These conditions force vendors to support jurisdiction-based controls for residency, access, and consent rather than rely on a single default operating model. The result is that the PIM for the genomics and life science computing market still faces slower cross-border scaling, even after technical data exchange has been resolved.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Type: On-Premises Dominance Masks a Cloud Acceleration Curve

On-premises deployment accounted for 61.13% of the PIM market share in genomics and life science computing in 2025, reflecting the weight of validated environments and stricter control expectations in regulated settings. That lead is tied to long-standing GxP practices, internal review routines, and the need to keep sensitive scientific records inside tightly managed infrastructures. Many buyers still view local control as the safer option, even though compliance, traceability, and data-handling policies have been built over several years. The segment also benefits from the fact that legacy LIMS, quality systems, and clinical applications are often easier to preserve than to replace in a single step. This keeps on-premises strong in the current revenue mix of the PIM for genomics and life science computing market, even as deployment preferences start to change.

Cloud-based deployment is projected to expand at a 36.48% CAGR through 2031, which makes it the fastest-growing deployment model in the PIM for genomics and life science computing market. DNAnexus's May 2026 launch of Omics Data Catalog and Omics Data Agent shows how cloud platforms are being built around governed discovery, reusable metadata, and direct AI interaction. Trusted Regulatory Spaces adds to that case by showing that regulated collaboration, audit support, and cloud access can now be combined in one controlled environment. Hybrid deployment is emerging as a practical middle path because organizations can keep sensitive records in existing local systems while running broader analytics and collaboration in the cloud. Over time, the PIM for genomics and life science computing market is likely to see cloud and hybrid models gain ground as validation playbooks improve and more buyers get comfortable with continuous platform updates.

By Component: Hardware Infrastructure Sets the Stage, But Software Defines the Value

Hardware accounted for 78.62% of the 2025 revenue base, which shows how much spending in the PIM for genomics and life science computing market has been tied to sequencers, high-performance computing assets, storage, and related infrastructure. That pattern reflects the heavy technical burden of next-generation sequencing, alignment, and high-volume data movement in production environments. Illumina's 2026 product activity supports this view, with TruPath Genome, distributed whole-genome sequencing for MRD research, and fireflyGO all pointing to continued investment in data generation and lab throughput. Hardware remains essential because no governance layer can create value if raw sequencing, compute performance, and storage reliability are weak. This means the installed hardware base still anchors a large part of the current structure of the PIM for genomics and life science computing market.

Software is projected to grow at a 36.42% CAGR, and that pace shows where differentiation is moving in the PIM for genomics and life science computing market. Illumina's DRAGEN v4.5 demonstrates this shift because the value is increasingly tied to better calling, broader assay support, and faster interpretation rather than to the instrument alone.[2]Illumina, “Illumina and SPT Labtech Unveil fireflyGO, Enabling Faster, Simpler Targeted Oncology Research,” Illumina, investor.illumina.com DNAnexus has made the same point from a different angle by adding conversational search, metadata cataloging, and AutoML support directly into its governed platform. Services remain smaller in share, but they stay commercially important because integration, validation, and workflow setup still shape how quickly customers can use the software layer. In the PIM for genomics and life science computing industry, the center of value is gradually shifting from equipment ownership toward software intelligence and managed data orchestration.

By End User: Pharma And Biotech Companies Lead, But Clinical Settings Accelerate Fast

Pharmaceutical and biotechnology companies held a 39.58% share in 2025, making them the largest end-user group in the PIM for the genomics and life science computing market. Their lead stems from the combination of large, multi-omics pipelines, strict documentation requirements, and pressure to shorten the time between data generation and decision-making. Large sponsors also have stronger reasons to integrate research, quality, and regulatory records under a single governance structure. Boehringer Ingelheim's One Medicine Platform illustrates this point because it was designed to link clinical, regulatory, and quality processes across global R&D operations. This keeps pharma and biotech at the center of current spending across the PIM for genomics and life science computing market.

Hospitals and clinical laboratories are projected to grow at a 36.84% CAGR through 2031, which marks the fastest rise among end users. Illumina's TruPath Genome and Emedgene materials demonstrate this, as they support lower hands-on time, richer interpretation, and tighter integration with clinical IT environments. Academic and research institutes remain important because federated genome programs continue to produce governed datasets for secondary analysis and collaborative use. CROs also gain relevance when sponsors want consistent data handling across multi-site trials and external service partners. In the PIM for genomics and life science computing industry, the user base is widening from biopharma-led adoption toward a broader mix that includes routine clinical care and outsourced development activity.

By Application: Sequence Alignment Anchors The Core, Multi-Omics Redefines The Ceiling

Sequence alignment and mapping held a 35.19% share in 2025, making it the largest application in the PIM for genomics and life science computing market. The segment stays large because almost every genomics workflow depends on reliable mapping before any downstream interpretation can begin. Illumina's DRAGEN and MRD-related releases show that performance, scale, and reproducibility in early-stage analysis still matter across research and clinical use cases. Sequence alignment also tends to anchor adjacent applications because variant calling, reporting, and target discovery all depend on clean upstream data. This is why the application base of the PIM for genomics and life science computing market still rests on core workflow reliability.

Multi-omics analysis is projected to grow at a 37.02% CAGR, which makes it the fastest-growing application area. Nature Genetics noted in 2026 that routine use of multi-omics now depends on better standardization and interpretation of growing biological complexity. A 2025 review in PMC also found that AI-driven multi-omics integration is changing precision oncology by moving beyond single-assay interpretation toward more individualized decision frameworks. The 2026 Journal of Translational Medicine study and Genomics.com's Mystra AI launch both show how interpretation, phenotype handling, and target discovery are moving closer to governed data platforms. In the PIM for genomics and life science computing market, that means the application ceiling is no longer set by data generation alone, but by how well platforms can connect, govern, and interpret multiple biological layers together.

Geography Analysis

North America held 46.67% of the PIM for the genomics and life science computing market in 2025, maintaining its position as the leading regional block. The region benefits from dense biotech and pharma clusters in the United States, especially in Massachusetts, California, and North Carolina, where research intensity and commercialization activity support faster platform adoption. Illumina's February 2026 TruPath Genome launch, which had over 30 early-access customers including Broad Clinical Labs, GeneDx, Rady Children's Hospital, and Baylor College of Medicine, reflects the depth of active genomics deployment in the region. Canada and Mexico add support through research networks and service delivery capacity, even though the United States remains the core demand center in the PIM for genomics and life science computing market. Europe remains the second-largest geography, supported by strong demand in Germany, the United Kingdom, and France, as well as by tighter governance expectations shaped by the EHDS and federated data-sharing models.

Asia-Pacific is projected to grow at a 36.73% CAGR through 2031, making it the fastest-growing geography in the PIM for genomics and life science computing market. The regional rise is supported by large national genomics programs, faster biopharma expansion, and growing investment in compute and cloud capacity for life science work. China's 1,000 Chinese Pangenome project, reported in Nature in 2026, generated 1,116 diploid genome assemblies and an imputation reference panel, which shows the scale of governed data infrastructure now being created in the region.[3]Nature, “The 1000 Chinese Pangenome Empowers Medical and Population Genetics,” Nature, link.springer.com Japan and India also strengthen regional demand through regulatory modernization, local biopharma expansion, and broader interest in precision medicine workflows. This makes Asia-Pacific the clearest growth engine for the PIM for genomics and life science computing market outside North America.

South America and the Middle East and Africa remain smaller in current size, but both regions are gaining relevance as global sponsors extend clinical programs and precision medicine infrastructure into new locations. Brazil stands out in South America because public health genomics activity is helping build a more durable base for data management needs. Saudi Arabia and the United Arab Emirates are also raising regional visibility through broader healthcare diversification and precision medicine investment plans. Across both regions, the PIM for genomics and life science computing market is likely to expand first through collaborative projects, clinical trial infrastructure, and cross-border governance needs rather than through immediate large-scale platform replacement.

Competitive Landscape

The PIM for the genomics and life science computing market remains moderately fragmented because no single vendor leads across deployment type, components, end users, and application layers simultaneously. Large enterprise software vendors such as IBM, Oracle, SAP, and Informatica bring broad data management experience, but their strengths remain rooted in general enterprise architecture rather than in genomics-native file types and scientific workflow logic. Domain-focused platforms such as Veeva Systems, Benchling, DNAnexus, QIAGEN, and Illumina are gaining traction because they align more closely with the day-to-day operational needs of regulated life science teams. This keeps competition active between platforms that start with enterprise-scale and those that start with scientific context. It also means the PIM for genomics and life science computing market is being contested at the workflow level, not only at the infrastructure level.

Strategic moves in 2025 and 2026 show how vendors are trying to widen that workflow control. DNAnexus partnered with Veeva around Trusted Regulatory Spaces, which linked regulated cloud collaboration with Veeva Vault submission and review processes.[4]DNAnexus, “DNAnexus Partners with Veeva to Advance Global Regulatory Collaboration in the Cloud with Trusted Regulatory Spaces,” DNAnexus, dnanexus.com Veeva also deepened enterprise stickiness through Boehringer Ingelheim's One Medicine Platform and through its long-term clinical and commercial partnerships with IQVIA. QIAGEN strengthened the laboratory interpretation layer in November 2025 by expanding QCI Interpret curation depth and multilingual reporting. Illumina continued to tighten the link between sequencing, bioinformatics, and governed interpretation through TruPath Genome, DRAGEN v4.5, and Emedgene.

White-space opportunities are still visible in semantic interoperability, mid-market adoption, and the point where molecular diagnostics data must move between genomics platforms and hospital systems. Standards alignment is becoming more important because buyers increasingly want platforms that can manage ontology-linked product data, reusable metadata, and secure multi-party access in one environment. The PIM for genomics and life science computing market is therefore rewarding vendors that can reduce the tradeoff between scientific specificity and enterprise governance. Vendors that solve cross-system data meaning, not only data movement, are likely to hold the strongest position as adoption broadens across clinical, research, and regulatory use cases.

PIM For Genomics and Life Science Computing Industry Leaders

Illumina, Inc.

Thermo Fisher Scientific Inc.

QIAGEN N.V.

DNAnexus, Inc.

SOPHiA GENETICS SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Genomics.com launched Mystra AI, an agentic AI platform for human genetics designed for drug target discovery and validation. The platform enables scientists and business development professionals to access genetic insights through a conversational interface without expert analytical knowledge, with outputs verified through proprietary tooling and methodologies, representing a direct bridge between PIM-governed genetic datasets and AI-driven drug discovery workflows.

- May 2026: DNAnexus announced a suite of AI-driven product innovations, including the Omics Data Agent, conversational GenAI for no-code cohort creation, AutoML Assistant, reducing ML model prototyping time by up to 80%, and the Omics Data Catalog, a centralized, governed metadata hub that makes multimodal scientific data discoverable and reusable as AI training fuel.

- May 2026: Illumina introduced the first distributed whole-genome sequencing solution for molecular residual disease research, built on NovaSeq X with Q70 quality scores and 35 billion read output. The distributed kit enables more clinical research labs to adopt MRD detection without centralized sequencing infrastructure, significantly expanding the addressable market for genomic data management.

- May 2026: Illumina and SPT Labtech unveiled fireflyGO, a benchtop liquid-handling and library-preparation platform integrated with the MiSeq i100 Series, designed to make NGS more accessible and scalable for targeted oncology research. This automation solution reduces barriers to genomic data generation in smaller laboratory settings.

Global PIM For Genomics and Life Science Computing Market Report Scope

PIM for Genomics and Life Science Computing refers to the market for processing-in-memory (PIM) technologies that accelerate data-intensive workloads in genomics and life science computing, including applications such as genome sequencing, bioinformatics, drug discovery, molecular modeling, and large-scale biomedical data analytics.

The PIM for Genomics and Life Science Computing Market Report is Segmented by Deployment Type (Cloud-Based, On-Premises, and Hybrid), Component (Hardware, Software, and Services), End User (Pharmaceutical and Biotechnology Companies, Academic and Research Institutes, Hospitals and Clinical Laboratories, Contract Research Organizations, and Other End Users), Application (Sequence Alignment and Mapping, Variant Calling and Interpretation, Multi-Omics Analysis, Clinical Genomics, Drug Discovery and Target Identification, and Population Genomics), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Cloud-Based |

| On-Premises |

| Hybrid |

| Hardware |

| Software |

| Services |

| Pharmaceutical and Biotechnology Companies |

| Academic and Research Institutes |

| Hospitals and Clinical Laboratories |

| Contract Research Organizations |

| Other End Users |

| Sequence Alignment and Mapping |

| Variant Calling and Interpretation |

| Multi-Omics Analysis |

| Clinical Genomics |

| Drug Discovery and Target Identification |

| Population Genomics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| Taiwan | |

| India | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Deployment Type | Cloud-Based | |

| On-Premises | ||

| Hybrid | ||

| By Component | Hardware | |

| Software | ||

| Services | ||

| By End User | Pharmaceutical and Biotechnology Companies | |

| Academic and Research Institutes | ||

| Hospitals and Clinical Laboratories | ||

| Contract Research Organizations | ||

| Other End Users | ||

| By Application | Sequence Alignment and Mapping | |

| Variant Calling and Interpretation | ||

| Multi-Omics Analysis | ||

| Clinical Genomics | ||

| Drug Discovery and Target Identification | ||

| Population Genomics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| Taiwan | ||

| India | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

How large is the PIM for genomics and life science computing space in 2026, and where is it headed by 2031?

The market is estimated at USD 0.25 billion in 2026 and is projected to reach USD 1.15 billion by 2031, with a 35.81% CAGR.

Which deployment model is growing fastest?

Cloud-based deployment is the fastest-growing model, with a forecast CAGR of 36.48% through 2031, even though on-premises still led with 61.13% share in 2025.

Who represents the largest buyer group?

Pharmaceutical and biotechnology companies are the largest end-user segment, with 39.58% share in 2025, driven by heavy multi-omics workflows and regulatory data needs.

What application is expanding the fastest?

Multi-omics analysis is the fastest-growing application, with a 37.02% CAGR, while sequence alignment and mapping remained the largest application at 35.19% share in 2025.

Which region leads adoption and which region is growing the fastest?

North America led with 46.67% share in 2025, while Asia-Pacific is projected to post the fastest regional growth at a 36.73% CAGR through 2031.

What is holding adoption back the most?

The main constraints are the cost and complexity of integrating with legacy validated systems, along with stricter privacy, sovereignty, and cross-border compliance requirements for genomic data.

Page last updated on: