Pigment Dispersion Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 29.24 Billion |

| Market Size (2031) | USD 35.84 Billion |

| Growth Rate (2026 - 2031) | 4.16% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

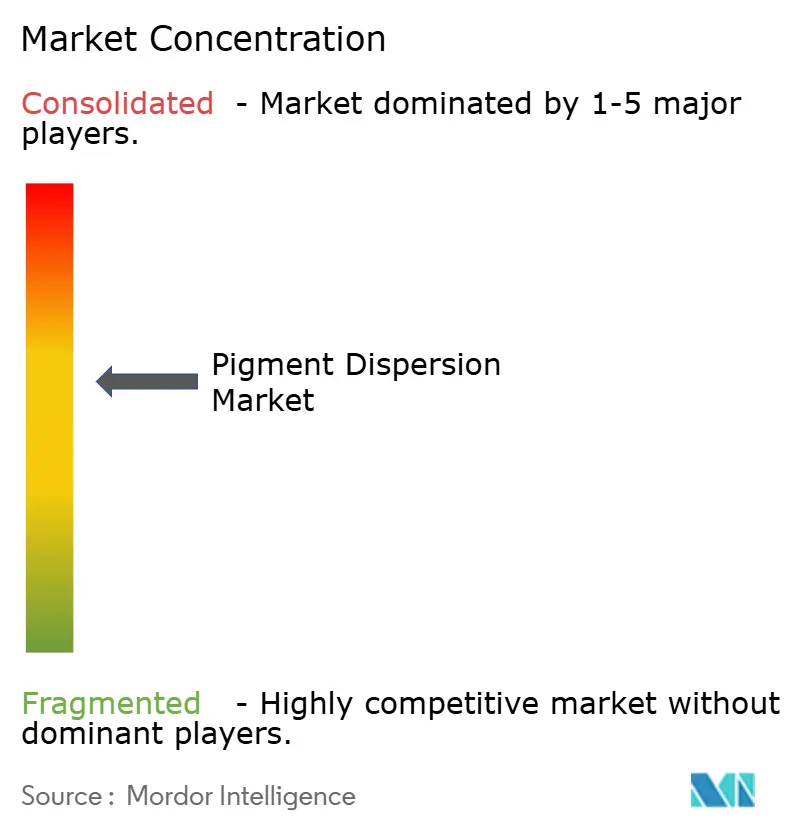

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pigment Dispersion Market Analysis by Mordor Intelligence

The Pigment Dispersion Market size is projected to expand from USD 27.17 billion in 2025 and USD 29.24 billion in 2026 to USD 35.84 billion by 2031, and is expected to register a CAGR of 4.16% between 2026 and 2031. The pigment dispersion market is supported by demand across architectural coatings, flexible packaging inks, plastic colorants, and digital textile printing systems, helping maintain volumes in developed and emerging economies. The shift toward waterborne systems is influencing the product mix, as tighter environmental regulations require formulators to reduce solvent use while meeting durability, color, and handling requirements in coatings and ink applications. Asia-Pacific remains a key region in the pigment dispersion market, supported by integrated pigment supply chains, construction activity, manufacturing capacity, and packaging demand linked to e-commerce and consumer goods distribution. Competition remains active as global specialty chemical producers and regional manufacturers invest in reformulation capabilities, product performance, and distribution reach. Recent consolidation has increased the scale of companies with broader pigment portfolios and technical service capabilities. The pigment dispersion market faces a higher operating threshold, as volatile raw material costs, stricter compliance requirements, and rising technology demands in milling and stabilization make scale, research and development (R&D) capabilities, and supply reliability more important than before.

Key Report Takeaways

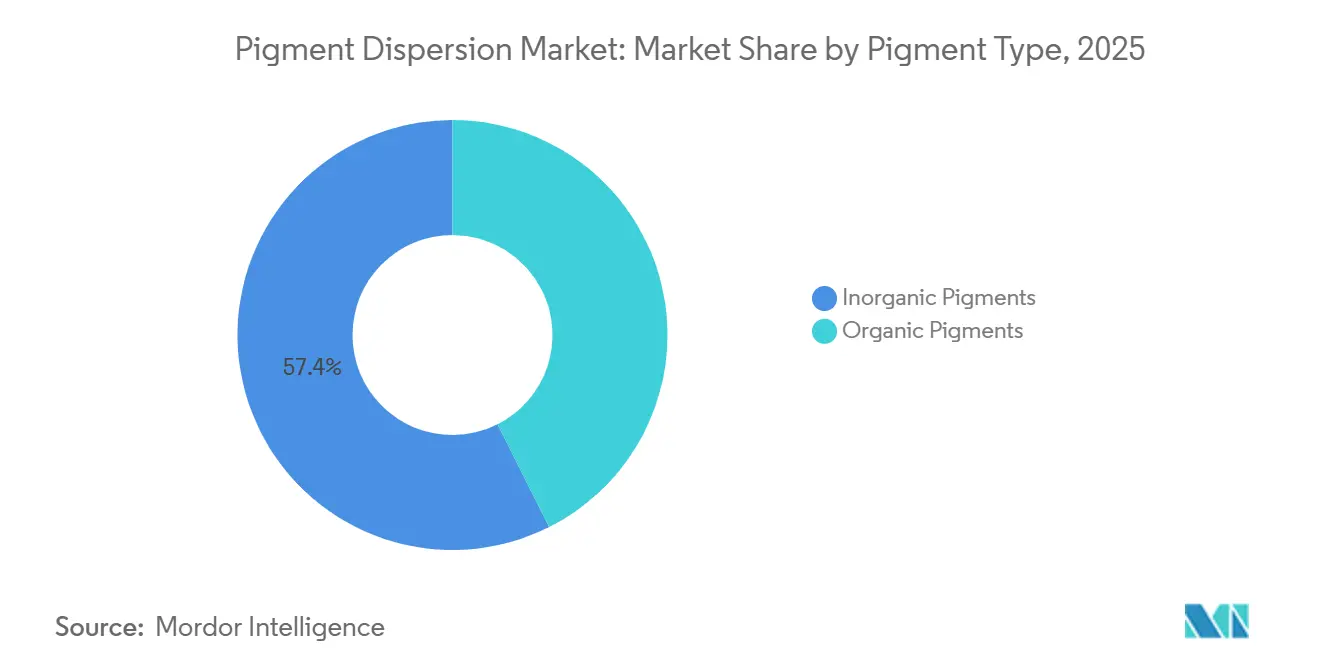

- By pigment type, inorganic pigments led with 57.42% revenue share in 2025, while organic pigments are forecast to expand at a 5.13% CAGR through 2031.

- By dispersion type, water-based dispersions held 55.76% of the Pigment dispersion market share in 2025 and are forecast to expand at a CAGR of 4.82% through 2031.

- By application, paints and coatings accounted for 32.44% of the Pigment dispersion market size in 2025, while printing inks are forecast to expand at a 4.74% CAGR through 2031.

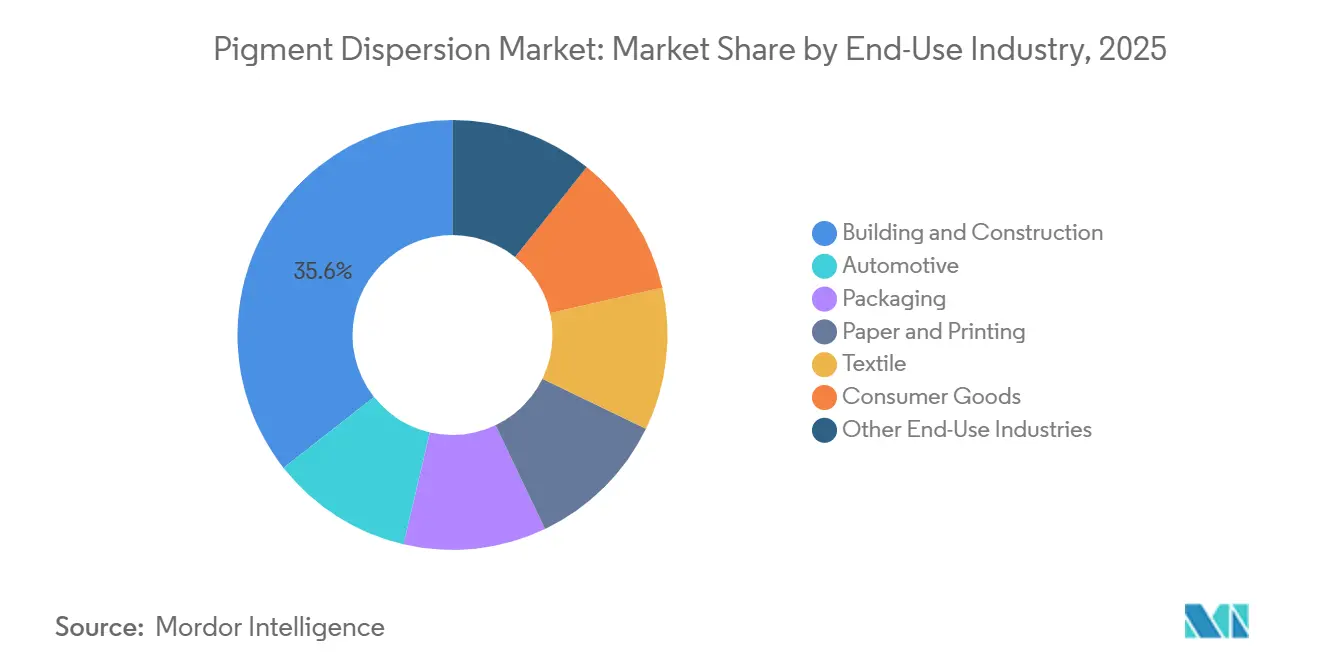

- By end-use industry, building and construction held 35.62% share in 2025, while packaging is forecast to expand at a 4.96% CAGR through 2031.

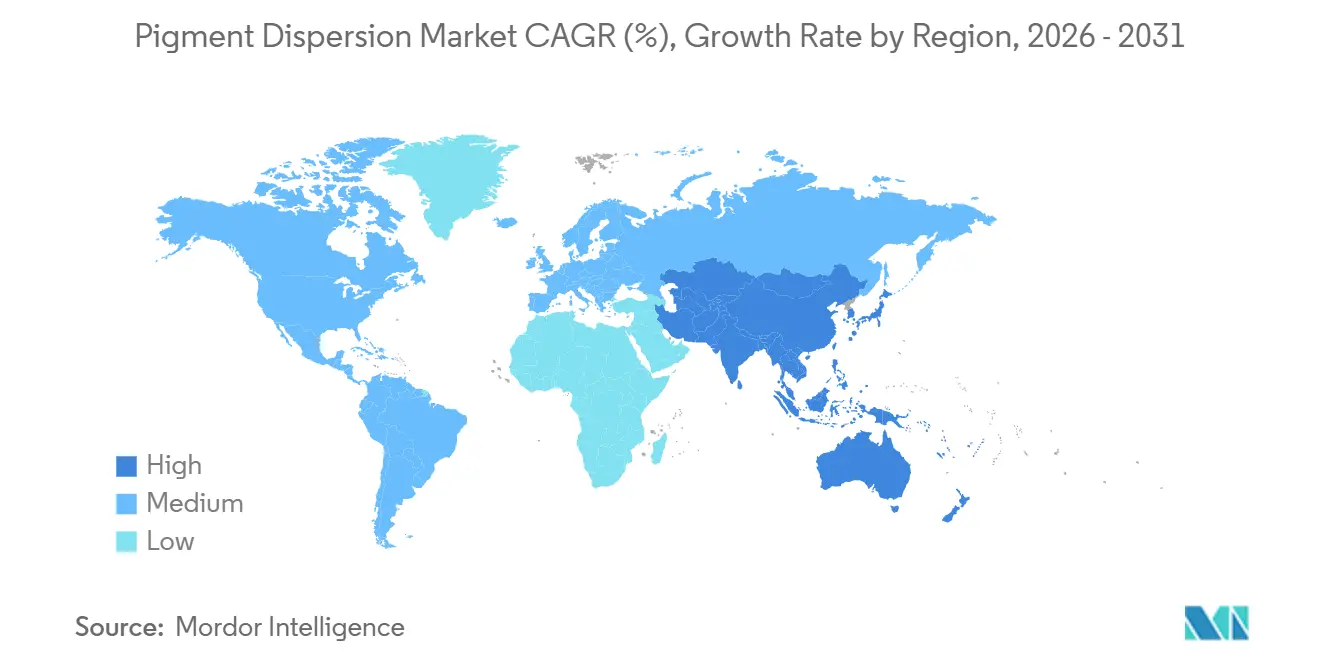

- By geography, Asia-Pacific represented 37.55% of global revenue in 2025 and is projected to grow at the fastest CAGR of 5.42% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Pigment Dispersion Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for waterborne and low-volatile organic compound (VOC) pigment dispersions | +1.4% | Global, with acute pull in the EU, North America, and China | Short term (≤ 2 years) |

| Rising demand from the building and construction sector | +0.6% | APAC core, Middle East, South America | Medium term (2-4 years) |

| Expansion of packaging and e-commerce demand | +0.8% | APAC core, with spillover to North America and Middle-East, and Africa (MEA) | Medium term (2-4 years) |

| Increasing use in plastics, cosmetics, and specialty textiles | +0.6% | Global, concentrated in APAC manufacturing clusters and EU specialty markets | Medium term (2-4 years) |

| Advancements in high-performance dispersion technologies | +0.5% | North America, Europe, Japan, South Korea | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Waterborne Pigment Dispersion Systems

The most notable shift in the pigment dispersion market is the ongoing replacement of solvent-based systems with waterborne alternatives across architectural, automotive, and industrial coating applications. The European Commission's December 2025 EU Ecolabel decision tightened criteria for decorative paints and related products, including lower VOC and semi-volatile organic compound (SVOC) thresholds for certain interior applications. This change is influencing formulation choices well beyond Europe, as suppliers often align global product platforms to the strictest major standard. Evonik's TEGO Dispers 780 W illustrates how the technology base is evolving alongside regulations. The product is solvent-free, non-hazardous, designed for high-quality waterborne pigment concentrates, and suitable for both organic and inorganic pigments, including food-related uses under relevant compliance frameworks. As the performance gap between waterborne and solvent-based systems continues to narrow, the pigment dispersion market is likely to favor producers that can support customers through reformulation, testing, and line conversion. Smaller formulators that depend on legacy solvent chemistry will face a more demanding transition in terms of equipment and skills.

Rising Demand from the Building and Construction Sector

The building and construction segment continues to support volume growth in the pigment dispersion market. This demand is tied to architectural coatings and construction materials that use titanium dioxide and iron oxides for opacity, durability, weather resistance, and consistent appearance across interior and exterior surfaces. Demand is strongest in Asia-Pacific and selected Middle East markets, where urbanization, infrastructure spending, and residential development sustain broad and recurring coatings consumption. The market impact extends beyond volume, as green building standards and low-emission coating preferences are raising specification levels. This supports higher-value water-based and technically refined dispersions over simpler solvent-heavy alternatives. As a result, the pigment dispersion market benefits from construction activity in two ways: through direct coating demand, and through a gradual shift toward formulations that require greater technical input and more consistent quality control.

Expansion of the Packaging Sector and E-commerce-Driven Demand

The pigment dispersion market is also benefiting from packaging demand, with the packaging end-use category recording the fastest growth rate among all end-use categories. This growth is tied to the steady expansion of e-commerce, branded consumer goods distribution, and flexible packaging formats that require high-quality ink performance across paper, film, and specialty substrates. Packaging inks are increasingly expected to balance color strength, adhesion, print consistency, migration control, and regulatory compliance, raising the technical requirements for pigment dispersion suppliers serving this channel. Low-migration and food-contact-compliant systems represent a key part of this demand, where qualification requirements reduce the number of credible suppliers and limit price competition once a producer is approved on a customer platform. For the pigment dispersion market, packaging represents not only an expanding-volume outlet but also a route into more specialized product grades where technical reliability and compliance support matter as much as delivered cost.

Advancements in High-Performance Dispersion Technologies

The pigment dispersion market is becoming more technology-sensitive as digital printing, high-speed inkjet systems, and advanced coating lines require tighter particle-size control, greater stability, and more predictable jetting or application behavior. Kodak states that its water-based KODACOLOR dispersions use proprietary micromedia milling technology to produce ultra-fine pigment particles as small as 11 nanometers, supporting improved color uniformity, higher saturation, broader gamut, and reduced printhead issues in industrial inkjet environments. Fujifilm describes its RxD dispersions as using a proprietary cross-linked polymer stabilization approach that locks each pigment particle in a stable matrix, with the platform positioned for demanding packaging, textile, industrial, and commercial printing applications that require long shelf life and tight particle control[1]Fujifilm Ink Solutions Group, “RxD Pigment Dispersions, Enabling High-Performance Aqueous Inkjet Inks,” Fujifilm Ink Solutions Group, fujifilmink.com. Evonik's January 2026 launch of TEGO Dispers 695 added another example of this direction, with a solvent-free, 100%-active hyperdispersant designed for radiation-curing and solventborne polyurethane inks, offering higher pigment loading, shorter grinding times, and improved storage stability. As these capabilities become standard customer expectations, the pigment dispersion market is likely to favor producers with proprietary process know-how over those that rely on more basic grinding and stabilization systems.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw material price volatility for titanium dioxide, sulfuric acid, and mineral-based inputs | -0.9% | Global, most acute in China, and export-oriented Asian manufacturers | Short term (≤ 2 years) |

| Compliance burden from environmental and chemical safety regulations | -0.6% | EU and North America primarily, with spillover to India and China | Medium term (2-4 years) |

| Volatility in petroleum-based solvents, resins, and organic pigment intermediates | -0.4% | Global, most acute in South and East Asia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Raw Material Price Volatility

The pigment dispersion market remains exposed to raw material price volatility, as titanium dioxide and other mineral inputs represent a significant share of cost formation for inorganic pigment systems. Titanium dioxide can account for 50% to 70% of inorganic pigment production costs, meaning even moderate input price swings can pressure margins across pigment producers, dispersion manufacturers, and downstream formulators. Tinox Chemie reported rutile titanium dioxide prices in the range of USD 1,821 to USD 1,959 per ton through mid-2026, while elevated sulfur-related cost pressure continued to affect sulfate-process economics, reflecting ongoing cost instability as an operating challenge in 2026[2]Tinox Chemie GmbH, “Market Outlook, Steady Pressure on Titanium Dioxide Amid High Costs and Weak Demand 2025-06-27 to 2025-07-04,” Tinox Chemie GmbH, tinoxchem.com. This is relevant to the pigment dispersion market because inorganic systems account for a large share of volume in construction and industrial applications, making it difficult for producers to substitute these inputs without affecting performance, opacity, or weather resistance. Companies with stronger procurement discipline, broader supplier networks, or upstream integration are better positioned to protect margins, while smaller participants face a greater risk of margin erosion or delayed cost pass-through to customers.

Compliance Burden from Environmental Regulations

The pigment dispersion market is also constrained by rising compliance burdens, as environmental and chemical-safety regulations are narrowing the formulation options available to producers. The European Commission's 2025 decision on decorative paints tightened criteria for volatile organic compound (VOC) and semi-volatile organic compound (SVOC) content, requiring dispersion suppliers to engineer products to meet downstream coating requirements, even when the final regulation is not written at the dispersion level. Borchers outlined the 2025 compliance environment by citing U.S. EPA VOC limits of up to 450 g/L for industrial coatings and 250 g/L for flat finishes, and noted that producers are promoting cobalt-free, oxime-free, and low-VOC alternatives to meet tightening requirements. For producers in export-oriented markets, the compliance challenge extends beyond product design, as testing, documentation, customer approvals, and reformulation cycles consume time and resources before a new grade can be commercially scaled. In the pigment dispersion market, this dynamic tends to widen the gap between larger firms with dedicated regulatory resources and smaller firms that must manage compliance alongside production and sales with more limited technical teams.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Pigment Type: Inorganic Pigments Anchor the Market While Organics Shift the Margin Mix

Inorganic pigments held a 57.42% share in 2025, placing them at the center of volume demand in the pigment dispersion market. Their position rests on the practical performance of titanium dioxide and iron oxides, which combine cost efficiency with UV resistance, thermal stability, chemical resistance, and opacity in construction-grade and industrial coating applications. These properties keep inorganic dispersions widely used in exterior architectural coatings, protective systems, and PVC-based building materials where weather exposure and service life are key purchasing criteria. The pigment dispersion market depends heavily on inorganic chemistry for its volume base, particularly in regions where construction and industrial coatings absorb large tons each year. This volume concentration also explains why raw material volatility in titanium dioxide directly affects pricing and margin performance across much of the value chain.

Organic pigments accounted for the remaining market share in 2025 and are projected to grow at a 5.13% CAGR through 2031, the fastest pace within this segment. Their appeal is strongest in end uses that prioritize chroma, brightness, design flexibility, and formulations that avoid heavy-metal-related concerns, particularly in printing inks, specialty textiles, and selected cosmetic systems. Sudarshan Chemical Industries Ltd completed the acquisition of Heubach Group in March 2025, expanding to 19 sites worldwide and strengthening its portfolio across organic, inorganic, pearlescent pigments, and liquid dispersions. This signals continued confidence in specialty pigment demand across global end markets. Within the pigment dispersion industry, the transaction combines scale with portfolio breadth, enabling a larger supplier to serve both commodity and higher-value color systems through a single platform. Inorganic pigments are therefore likely to remain the volume anchor, while organic pigments continue to influence product mix and margin development.

By Dispersion Type: Waterborne Systems Consolidate Market Leadership

Water-based dispersions held a 55.76% share in 2025 and are forecast to grow at a 4.82% CAGR through 2031, giving them both volume leadership and the fastest growth within this segment of the pigment dispersion market. Their expansion is linked to stricter environmental compliance requirements, broader sustainability procurement standards, and technical advances that have improved pigment wetting, stabilization, color development, and corrosion performance. The shift toward waterborne systems is particularly relevant in architectural coatings, packaging inks, and other applications where customers require lower-emission systems without compromising color strength or process consistency. This transition represents a move toward a different product standard that requires new additive chemistry, improved milling control, and closer formulation support. Once approved by customers, water-based systems can also benefit from longer commercial life because they align more closely with the direction of future regulation.

BASF describes Dispex Ultra PX 4290 as a solvent-free, high-molecular-weight dispersing agent for organic and inorganic pigments in aqueous coatings, printing inks, and adhesives, with benefits including higher pigment loading, reduced viscosity, improved flocculation stability, and improved gloss. Evonik similarly positions TEGO Dispers 780 W as a solvent-free solution for high-quality waterborne pigment concentrates, suitable across binder-containing and binder-free colorants, and compliant with claims relevant to food applications. Solvent-based dispersions retain a role in demanding industrial or specialty applications where adhesion, chemical resistance, or legacy process conditions favor solvent chemistry. Even so, the pigment dispersion industry is steadily reducing the broad-market role of these systems as customer preferences and regulations continue to shift toward lower volatile organic compound (VOC), more compliance-ready options. This leaves solvent-based products with strategic relevance in specific applications, but without the same broad market position they previously held.

By Application: Printing Inks Lead Growth as Digital Printing Reshapes Demand Architecture

Paints and coatings accounted for 32.44% of the pigment dispersion market in 2025, while printing inks are projected to expand at a 4.74% CAGR through 2031. Coatings remained the largest application because architectural and industrial uses continue to absorb significant pigment volumes, particularly during construction-linked demand cycles across Asia-Pacific and the Americas. Printing inks are growing faster because digital inkjet is expanding into packaging, textiles, and graphic arts, each of which requires tighter particle size distribution, higher re-dispersibility, and more consistent behavior during storage and printhead operation. This is changing the technical requirements of the pigment dispersion market, as suppliers must increasingly tailor formulations to specific print technologies rather than serve a broad ink category with largely interchangeable grades. As a result, dispersion stability, particle purity, and equipment compatibility play a larger role in customer selection.

Kodak states that its KODACOLOR range is supplied as ready-to-use, water-based, ultra-fine dispersions for inkjet inks, coatings, and related applications, with ultra-fine particles intended to improve print quality and reduce printhead problems. Fujifilm's RxD platform is similarly positioned for high-performance aqueous inkjet inks across packaging, textiles, industrial, and commercial printing, supported by a proprietary stabilization process and investment in aqueous dispersion manufacturing capacity. These developments indicate that the pigment dispersion market is dividing into more technically distinct sub-segments within inks, where supplier approval depends on application-specific performance rather than broad pigment availability alone. This favors companies with process IP, application laboratories, and the ability to support customers through qualification across multiple print environments. It also reduces the role of standard commodity grades in faster-growing digital formats, where performance issues can affect printhead life, image quality, or production uptime.

By End-Use Industry: Building and Construction Provides the Volume Floor, While Packaging Sets the Growth Pace

Building and construction accounted for 35.62% of the market in 2025, making it the largest end-use segment. This position reflects recurring demand for architectural coatings and construction materials across residential, commercial, and infrastructure activity, particularly in Asia-Pacific, the Americas, and parts of the Middle East. Because this segment relies on durable, cost-effective inorganic systems, it provides a stable volume base even when some specialty applications experience slower demand. The pigment dispersion market for packaging is projected to expand at a 4.96% CAGR through 2031, placing it ahead of all other end-use segments in terms of growth. This faster pace reflects how distribution changes, consumer goods packaging demand, and compliance-sensitive ink applications are exerting greater influence on market mix.

Automotive remains strategically important because coating systems in that end use require precise color matching, weather resistance, and reliable application behavior, even though overall volume growth is more measured than in construction or packaging. Textile applications are also evolving as digital inkjet adoption increases demand for fabric-compatible dispersions that deliver color depth and sharpness without the limitations of traditional pigment paste systems. The pigment dispersion industry is therefore balancing a mature but large construction base with faster-growing packaging and textile opportunities that favor technical specialization. As packaging requirements become more stringent around migration, substrate compatibility, and production efficiency, suppliers that combine compliance support with stable color performance are positioned to capture a larger share of new program wins. Across the pigment dispersion market, this mix shift is likely to increase the relative importance of high-service and higher-value end uses, even as building and construction continues to underpin total volume.

Geography Analysis

Asia-Pacific accounted for 37.55% of global revenue in 2025 and is projected to grow at a 5.42% CAGR through 2031, making it both the largest and the fastest-growing region in the pigment dispersion market. China remains central to this position, combining integrated pigment production, broad coatings demand, manufacturing scale, and a large customer base across packaging, plastics, and industrial applications. India is also gaining importance as housing expansion, urban development, and domestic manufacturing activity sustain upward demand for coatings and colorants. The pigment dispersion market in Asia-Pacific is supported by both base-volume demand and a gradual shift toward higher-specification water-based and specialty systems across major consuming sectors. Southeast Asia is poised for further growth, as packaging demand linked to e-commerce and consumer goods distribution is driving the need for inks and associated dispersion systems across several markets.

Japan and South Korea play distinct roles in the pigment dispersion market. Japan contributes more through higher-specification demand than through the largest regional tonnage, with its importance driven by automotive OEM coatings, electronics-related applications, advanced industrial finishes, and precision printing needs that require stable particle control and consistent formulation performance. North America and Europe continue to represent substantial value pools, supported by renovation activity, packaging conversion, automotive refinishing, and industrial coatings rather than by high levels of new construction growth. Europe also serves as an important regulatory benchmark, as product requirements shaped by volatile organic compound (VOC) and broader chemical compliance frameworks frequently influence global supplier standards and export-facing formulation strategies. In the United States and Canada, construction and refurbishment activity supports architectural coatings demand, while packaging quality expectations are increasing the need for reliable, lower-emission dispersion technologies.

Sun Chemical, a DIC Corporation subsidiary, highlighted water-based emulsions, water-based polyurethane dispersions, VOC-reducing solutions, and low-monomer materials at the European Coatings Show 2025, reflecting the premium formulation focus in the European and North American supply chain. South America contributes through agribusiness packaging, consumer goods, and residential construction coatings, with Brazil standing out as a significant demand center for titanium dioxide and iron oxide-based architectural systems. The Middle East and Africa remain smaller in terms of value-added local production, but construction programs and industrial development continue to support demand for imported pigment dispersions and concentrates. In these markets, technical service and distributor relationships can be as important as price, as customers often require support in adapting imported systems to local substrates, climate conditions, and application practices. Overall, the pigment dispersion market remains regionally diverse, with its growth center in Asia-Pacific, while Europe and North America continue to shape technical standards and compliance direction.

Competitive Landscape

The pigment dispersion market is moderately consolidated, with meaningful regional fragmentation beneath leading multinational and large regional suppliers. Competition is shaped by access to advanced dispersant chemistry, particle stabilization capabilities, regulatory compliance, and the ability to serve customers across multiple end-use categories with consistent performance. Sudarshan Chemical's completion of the Heubach acquisition in March 2025 changed the structure of the pigment dispersion market by creating a broader global pigment platform with 19 sites and a portfolio spanning organic, inorganic, and pearlescent pigments, as well as liquid dispersions. This acquisition provides a foundation to serve both scale-driven standard grades and more specialized color systems, while expanding the company's reach across customers and geographies. As consolidation continues, larger firms are likely to strengthen their bargaining position in procurement, technical service, and customer qualification.

Technology differentiation is becoming a more decisive factor in the pigment dispersion market, as customers focus on milling quality, shelf stability, pigment loading, grinding efficiency, and compatibility with increasingly demanding application systems. Kodak's emphasis on 11-nanometer particle capability in water-based inkjet dispersions and Fujifilm's cross-linked polymer stabilization platform are examples of how process know-how supports performance claims beyond simple color delivery. Evonik's 2025 and 2026 product launches follow the same pattern, with TEGO Dispers 780 W and TEGO Dispers 695 positioned around solvent-free design, compliance readiness, higher pigment loading, and shorter grinding times in target applications. The market rewards suppliers that can link product performance to measurable customer process benefits, not just pigment availability. This advantage is most pronounced in packaging inks, digital printing, and high-specification coatings, where a failed formulation can cause downtime, rework, or compliance risk.

Distribution and ecosystem partnerships are also shaping the competitive landscape, as many customers require application support close to their production base. ECKART America's appointment of Lintech International as its exclusive national coatings, adhesives, sealants, and elastomers (CASE) distribution partner in the United States, effective April 2025, expanded the route to market for ECKART's effect pigment portfolio and reinforced the importance of technical distribution in coatings and related applications. Runaya and ECKART's December 2024 joint venture in India linked specialty pigment ambitions with a localized, sustainability-oriented production base for aluminum granules and future pigment manufacturing. The pigment dispersion market offers room for regional producers, particularly in cost-sensitive or standard-grade categories, but the strategic direction favors companies with broader portfolios, stronger technical support, and the capital to keep pace with compliance and process innovation. This dynamic supports a market structure in which leadership is driven by technology and scale, while competitive pressure remains active in regional and application-specific niches.

Pigment Dispersion Industry Leaders

DIC Corporation

Sudarshan Chemical Industries Limited

Cabot Corporation

Penn Colors Inc.

Chromaflo Technologies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Evonik Industries AG launched TEGO Dispers 695, a solvent-free, 100%-active hyperdispersant for radiation-curing and solventborne polyurethane inks. The product enables higher pigment loadings without thixotropy and reduces grinding times. It targets formulators of UV flexo, litho, inkjet, and PU-based gravure inks for the packaging market, addressing production economics challenges in the flexible packaging print market.

- November 2025: Toyo Ink India (part of the artience Group) announced plans to expand liquid ink production at its Gujarat facility to approximately 1.5 times current capacity. The expanded plant is targeted for operational readiness in 2028 and is also intended to serve as a regional export hub for the artience Group's liquid ink and plastic colorant business across South and Southeast Asia.

Global Pigment Dispersion Market Report Scope

Pigment dispersions are stable, pre-ground suspensions of pigment particles in a liquid medium (water or solvent) or resin. They simplify manufacturing and artistic workflows by eliminating the need for dry-powder grinding, while ensuring consistent color strength, uniform particle size, and reduced dust hazards.

The pigment dispersion market is segmented by pigment type, dispersion type, application, end-use industry, and geography. By pigment type, the market is segmented into inorganic pigments and organic pigments. By dispersion type, the market is segmented into water-based and solvent-based. By application, the market is segmented into paints and coatings, printing inks, plastics, textiles, paper, cosmetics, and other applications. By end-use industry, the market is segmented into building and construction, automotive, packaging, paper and printing, textile, consumer goods, and other end-use industries. The report also covers market size and forecasts for pigment dispersion across 16 countries in major regions. The market sizes and forecasts are provided in terms of value (USD).

| Inorganic Pigments |

| Organic Pigments |

| Water-Based |

| Solvent-Based |

| Paints and Coatings |

| Printing Inks |

| Plastics |

| Textiles |

| Paper |

| Cosmetics |

| Other Applications |

| Building and Construction |

| Automotive |

| Packaging |

| Paper and Printing |

| Textile |

| Consumer Goods |

| Other End-Use Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Pigment Type | Inorganic Pigments | |

| Organic Pigments | ||

| By Dispersion Type | Water-Based | |

| Solvent-Based | ||

| By Application | Paints and Coatings | |

| Printing Inks | ||

| Plastics | ||

| Textiles | ||

| Paper | ||

| Cosmetics | ||

| Other Applications | ||

| By End-Use Industry | Building and Construction | |

| Automotive | ||

| Packaging | ||

| Paper and Printing | ||

| Textile | ||

| Consumer Goods | ||

| Other End-Use Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is current market size of Pigment Dispersion Market?

The Pigment Dispersion Market size is projected to expand from USD 27.17 billion in 2025 and USD 29.24 billion in 2026 to USD 35.84 billion by 2031, and is expected to register a CAGR of 4.16% between 2026 and 2031.

Which product category leads to demand today?

Inorganic pigments led the 2025 mix with a 57.42% share, as titanium dioxide and iron oxides remained important across construction and industrial coating applications.

Why are water-based systems gaining ground so quickly?

Water-based dispersions held 55.76% share in 2025 and are also the fastest-growing dispersion type, supported by lower-VOC requirements and better additive performance.

Which application is expanding the fastest?

Printing inks are forecast to grow at 4.74% CAGR through 2031 as digital inkjet use expands in packaging, textiles, and graphic arts.

Page last updated on: