Photography Studio Software Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 0.72 Billion |

| Market Size (2030) | USD 1.36 Billion |

| Growth Rate (2025 - 2030) | 13.56% CAGR |

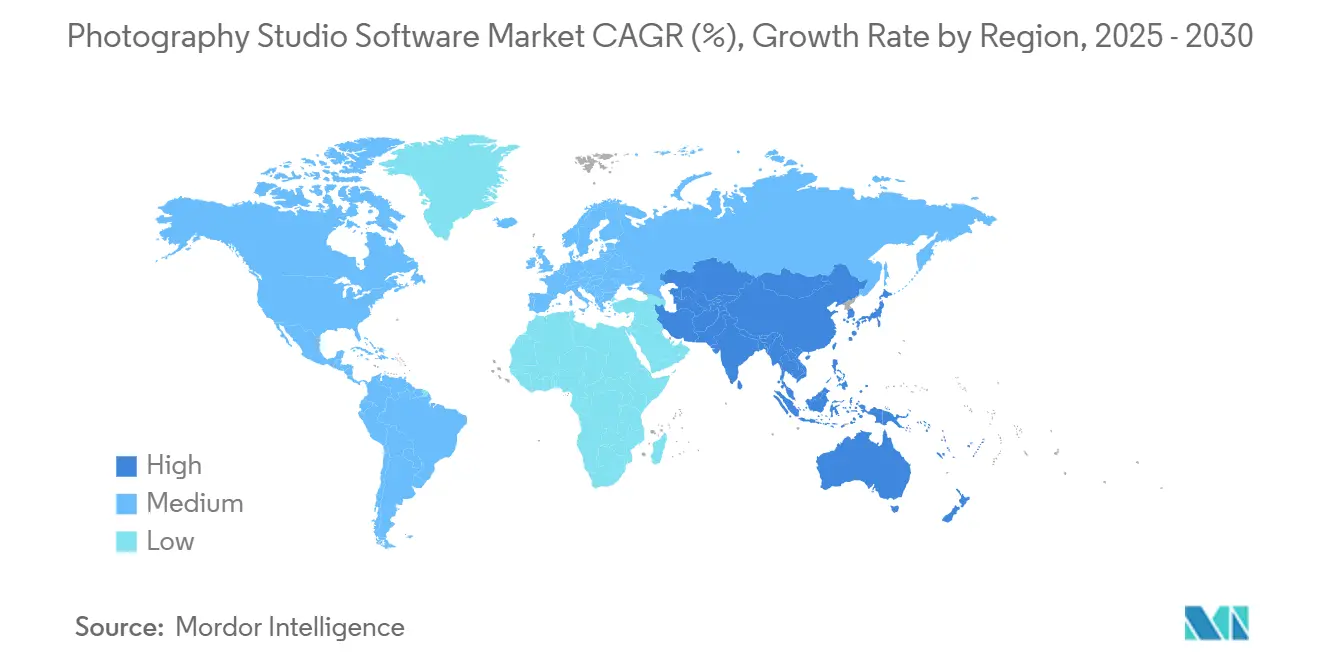

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

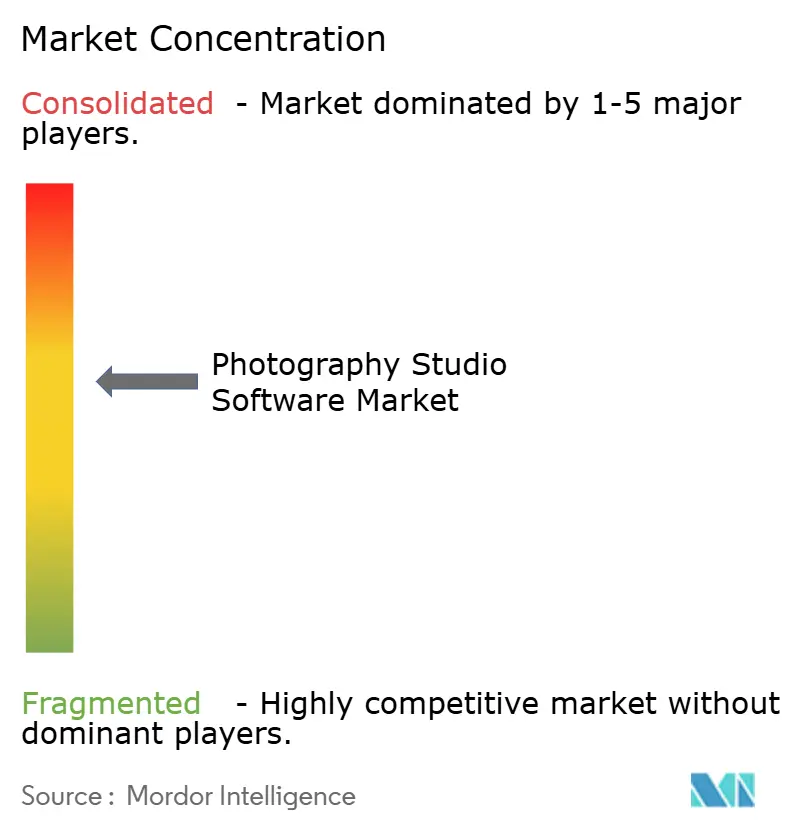

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Photography Studio Software Market Analysis by Mordor Intelligence

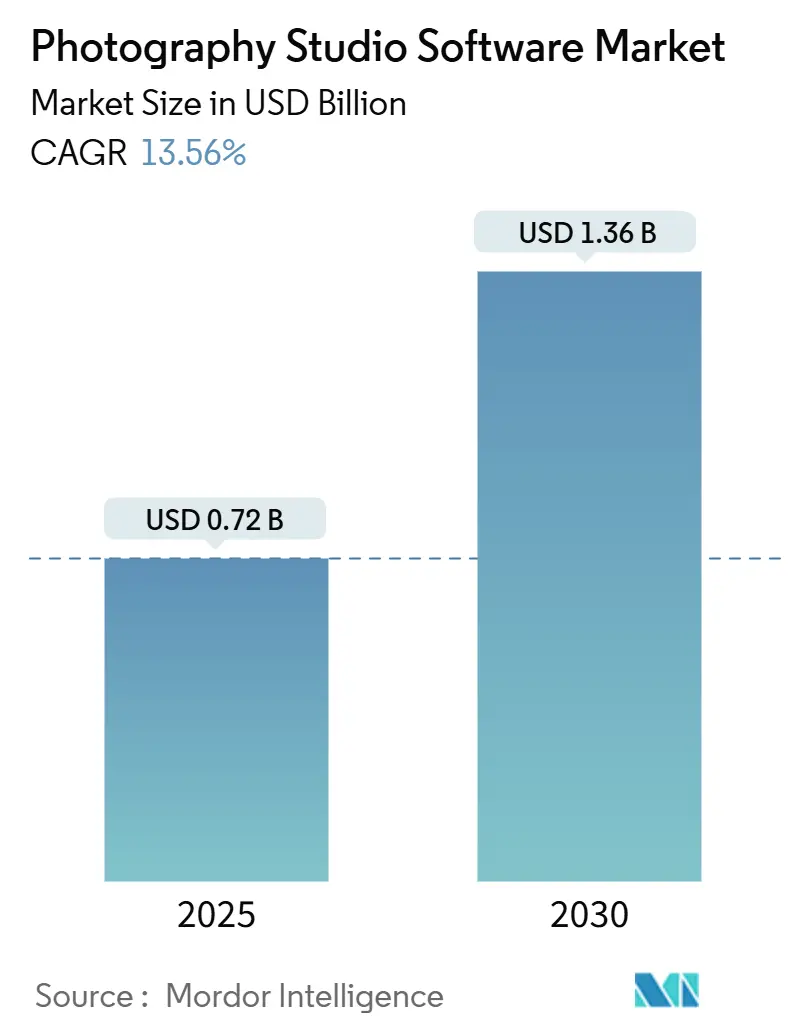

The photography studio software market size was USD 0.72 billion in 2025 and is projected to reach USD 1.36 billion by 2030, growing at a 13.56% CAGR from 2025 to 2030. Rapid cloud migration, the infusion of artificial intelligence into editing workflows, and rising demand for integrated booking and payment tools are reshaping competitive dynamics. Independent photographers value subscription pricing that eliminates large upfront fees, while multi-employee studios favor hybrid deployments that strike a balance between local file control and cloud-based collaboration. Investor enthusiasm is strong. Photoroom’s AI-first platform, which now processes more than 5 billion images annually, secured EUR 50 million (USD 56.5 million) in annual recurring revenue by early 2025, demonstrating the commercial traction of generative editing models. Consolidation pressure remains modest because specialized workflows for school portraits, high-volume e-commerce, and event documentation reward niche providers that can embed vertical-specific compliance and data-handling features. Nevertheless, headline risks around data privacy and vendor lock-in continue to influence procurement decisions, nudging studios toward vendors that publish transparent pricing and guarantee data portability.

Key Report Takeaways

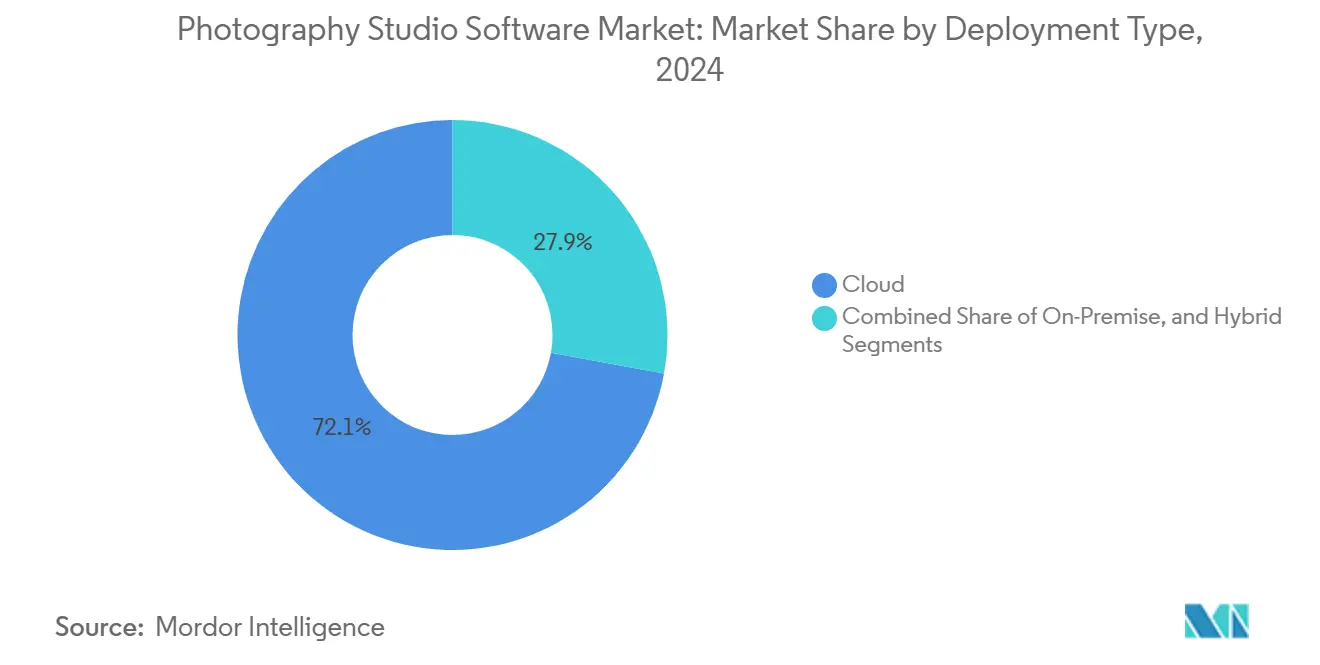

- By deployment type, cloud solutions led with a 72.14% market share of the photography studio software market in 2024, while hybrid architectures are projected to expand at a 15.68% CAGR through 2030.

- By feature set, scheduling and CRM tools held a 43.64% share of the photography studio software market size in 2024, whereas analytics and reporting modules are expected to advance at a 15.27% CAGR between 2025 and 2030.

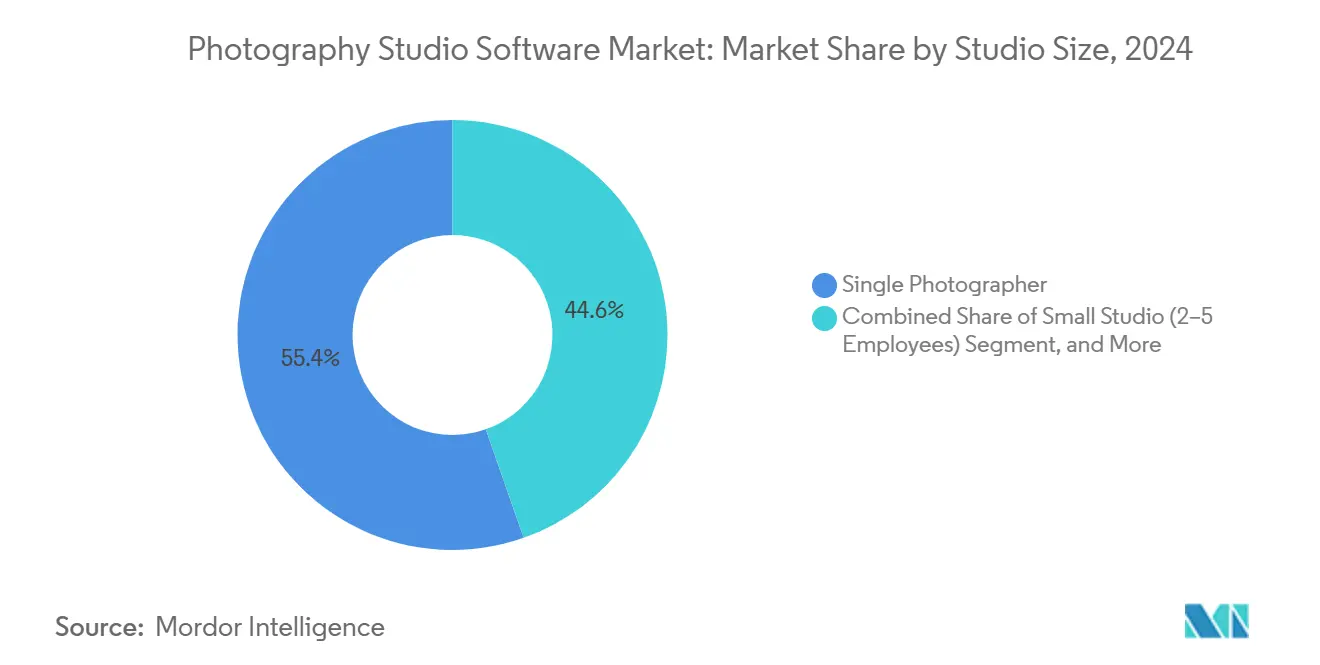

- By studio size, single-photographer operations captured 55.38% of the revenue in 2024, but mid-sized studios employing 6-15 staff members are forecasted to grow at a 14.46% CAGR to 2030.

- By end user, wedding and event photographers contributed 41.28% of 2024 spending, while commercial studios are expanding at 15.18% CAGR on the back of e-commerce image demand.

- By geography, North America accounted for 38.12% revenue in 2024; Asia Pacific is the fastest-growing region at 14.80% CAGR through 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Photography Studio Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid adoption of SaaS management platforms | +3.2% | North America and Europe, global spill-over | Short term (≤ 2 years) |

| Integrated client booking and payment solutions | +2.8% | North America and Asia Pacific | Medium term (2-4 years) |

| Expansion of social-media-driven photo sessions | +2.1% | Asia Pacific and North America | Medium term (2-4 years) |

| AI-based post-processing automation | +2.6% | North America and Europe, emerging globally | Medium term (2-4 years) |

| Emergence of hybrid in-person and virtual shoots | +1.4% | North America and Europe | Long term (≥ 4 years) |

| GDPR and data-privacy compliance requirements | +1.3% | Europe, spreading to North America and Asia Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of SaaS Management Platforms

Independent creatives are abandoning perpetual-license desktop packages in favor of subscription cloud suites that update automatically and flex with seasonal workloads. HoneyBook processed more than USD 13 billion in client payments and managed 28 million client relationships by early 2025, showing how network effects amplify platform stickiness. SaaS vendors leverage anonymized usage data to recommend winning workflows, creating a feedback loop that widens the capability gap versus standalone desktop tools. Mobile apps that enable on-location contract signing further strengthen value perception among freelancers who monetize agility.

Integrated Client Booking and Payment Solutions

Studios are replacing fragmented toolchains with unified systems that synchronize calendars, contracts, invoices, and payment gateways. Dubsado’s 2024 integration with Stripe Payment Links lifted booking conversions by 56% in three months for studios that enabled buy-now-pay-later options.[1]Stripe, “Payment Links Impact Study,” stripe.com Centralized data reduces reconciliation errors and accelerates cash collection, while automated reminders and digital signatures compress the lead-to-booking cycle from days to hours. Studios increasingly treat payment flexibility as a revenue lever, not an ancillary feature.

AI-Based Post-Processing Automation

Artificial intelligence is collapsing editing timelines that once consumed up to 80% of production hours. Photoroom’s Instant Diffusion model generates consistent product imagery 40% faster than earlier generative tools. Commercial operator Orendt Studios achieved an 82% reduction in turnaround time after adopting AI-assisted workflows, demonstrating how throughput gains lead to higher revenue per photographer. Vendors now embed AI inside familiar interfaces-ACDSee Photo Studio Ultimate 2025 runs GPU-accelerated AI locally, preserving privacy while boosting speed.

Rising Need for GDPR and Data-Privacy Compliance Features

The European Union’s General Data Protection Regulation imposes penalties of up to 4% of a company's global revenue, compelling studios to audit their data flows and demand compliance tooling from vendors. Platforms that automate consent capture, encrypt galleries, and deliver exportable audit logs win favor among small studios without in-house legal resources. Photoroom’s pursuit of SOC 2 certification reflects the new baseline for enterprise contracts that hinge on demonstrable governance controls.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High switching costs for established studios | -1.8% | North America and Europe | Short term (≤ 2 years) |

| Limited internet connectivity in developing regions | -1.2% | Rural Asia Pacific, Africa, South America | Medium term (2-4 years) |

| Saturation of low-cost and DIY tools | -0.9% | Global | Long term (≥ 4 years) |

| Data breaches eroding trust in cloud systems | -1.6% | North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Switching Costs for Established Studios

Studios entrenched in legacy ecosystems face weeks of disruption to migrate terabytes of RAW files, color profiles, and client histories. Capture One’s 344% price hike for multi-user plans in May 2024 triggered backlash, yet many customers absorbed the increase rather than endure downtime. Proprietary sidecar formats further complicate exits, while the cognitive cost of retraining staff delays adoption decisions even when superior alternatives exist.

Data Breaches Eroding Trust in Cloud Systems

Dropbox Sign’s April 2024 breach exposed emails, phone numbers, and API keys, reminding studios that client images can become liabilities if repositories are compromised.[2]United States Securities and Exchange Commission, “Form 8-K – Dropbox Inc.,” sec.gov Vulnerabilities like Synology’s CVE-2024-10443 (CVSS 9.8) reinforce skepticism toward public clouds. In response, ACDSee markets on-device AI that avoids server uploads, and hybrid architectures that keep master files on-premise are gaining traction among privacy-sensitive users.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Type: Hybrid Models Bridge Control and Collaboration

Hybrid deployments are the market’s fastest climber, advancing at 15.68% CAGR through 2030 as studios reconcile data-sovereignty rules with the convenience of browser-based collaboration. Excire Foto Office Edition, launched in February 2025 at USD 29.90-39.90 per user per month, illustrates the model, master files stay on-premise while cloud-synced metadata enables remote search.[3]Excire, “Foto Office Edition Launch,” excire.com Cloud still leads with 72.14% revenue in 2024 because freelancers value zero-maintenance infrastructure; however, large corporate clients, particularly those in healthcare and defense, continue to mandate local storage. On-premise solutions persist in air-gapped environments, yet they will cede an incremental share as bandwidth costs fall and edge caching reduces latency. Vendors that offer seamless data tiering, including hot files in the cloud and archives on network-attached storage, are well-positioned to capture both compliance-driven and performance-driven use cases. The photography studio software market size for hybrid solutions is projected to reach USD 480 million by 2030, reflecting the growing complexity of regulations.

Studios employing 6-15 staff members typify hybrid adopters because team members need concurrent access to catalogs without saturating internet links. NetX Hybrid Cloud and 4ALLPORTAL enable local rendering while serving low-resolution previews through fast content-delivery networks, satisfying both speed and cost constraints. As data-transfer pricing remains volatile, capacity planning favors architectures that let operators pin entire projects locally during peak season and migrate them to object storage afterward. Such flexibility shields profit margins when incoming booking volumes fluctuate. Regulatory catalysts add momentum, India’s draft Digital Personal Data Protection Act and Australia’s Privacy Act review mirror GDPR principles, suggesting hybrid demand will broaden beyond Europe.

By Feature Set: Analytics Ascend as Studios Pursue Margin Discipline

The scheduling and CRM modules generated 43.64% of the revenue in 2024, as every client engagement begins with a calendar slot and a contract, thereby cementing their position at the workflow core. Yet analytics and reporting tools are compounding at 15.27% CAGR as operators pivot from artistic intuition to data-led decision-making. PhotoDay’s 2024 dashboard displays real-time profitability per session, enabling studios to identify unprofitable service lines within weeks of collection. Creative Force measures SKU throughput and rework rates, enabling operations managers to optimize staffing levels. The photography studio software market size attributed to analytics could reach USD 180 million by 2030, assuming current growth velocities continue.

Competitive pressure accelerates analytics adoption because studios that quantify conversion funnels can underprice rivals while safeguarding margins. Sunshine Photo Cart’s Advanced Analytics highlights abandonment points between inquiry and booking, prompting micro-optimizations such as shorter contact forms or tiered packages that raise average order value. AI also appears in predictive modules that recommend upsell opportunities based on historical buying patterns. Once studios embed such insights, switching costs rise, enhancing vendor retention.

By Studio Size: Workflow Automation Elevates Mid-Sized Operations

Single-photographer businesses dominated revenue at 55.38% in 2024 and remain price-sensitive, favoring bundles that combine scheduling, invoicing, and basic galleries for less than USD 30 per month. However, mid-sized studios are scaling at 14.46% CAGR by automating production tasks that previously required headcount. smaX Photography utilizes ShootQ for scheduling and Imagen for AI editing to manage thousands of athlete portraits with a team of only five employees, maintaining lean labor ratios. The photography studio software market share captured by mid-sized studios is expected to rise as automation compresses delivery cycles.

Large studios, typified by Orendt’s 325-person workforce, orchestrate specialized stacks-tethered capture via Profoto ProStudio, production management via Creative Force, and custom DAM systems to process 300,000 SKUs annually. Their best-practice adoption trickles down; mid-market vendors now incorporate enterprise-grade masking and batch-rename functions into sub-USD 100 annual licenses, democratizing sophisticated workflows. As a result, mid-sized shops can pursue national contracts without scaling payroll commensurately.

By End User: Commercial Studios Industrialize High-Volume Imaging

Wedding and event specialists contributed 41.28% of 2024 demand, while commercial studios are expanding at a 15.18% CAGR, driven by e-commerce’s insatiable appetite for product imagery. Photoroom’s API processed 13 million Barbie social-media selfies for Warner Brothers, spotlighting high-volume use cases. The photography studio software market size for commercial studios is projected to surpass USD 400 million by 2030, as AI-driven background removal and automated color matching enable next-day catalog refreshes.

School photographers manage massive rosters under tight deadlines, relying on roster integrations and automated face recognition to streamline their workflow. Portrait studios leverage template-driven lighting and posing to preserve brand consistency across multiple storefronts. Competitive advantage now hinges on throughput efficiency; studios deploying AI culling report 300% productivity gains, reshaping labor economics so that one editor can finish work that once required three. Vendors offering vertical-specific compliance-such as parental consent tracking within school systems-build defensible niches.

Geography Analysis

North America generated 38.12% of 2024 revenue, driven by approximately 200,000 professional photographers and a subscription penetration rate exceeding 60% among full-time practitioners. United States studios prize fast customer support; same-day issue resolution is a table-stakes requirement during peak wedding season. Canada’s bilingual needs drive the development of localized interfaces, while Mexican operators utilize cloud tools to cater to destination weddings originating from the United States and Europe. Pricing sensitivity in Latin markets keeps perpetual-license options relevant, although hybrid approaches that cache images locally to manage bandwidth costs are gaining traction.

Europe’s demand profile is shaped by the GDPR, which elevates compliance tooling to a procurement priority one. Vendors offering SOC 2 Type II reports and granular consent workflows are particularly resonant in Germany and France, where regulators closely scrutinize automated decision-making. The United Kingdom remains a significant spender on AI-enabled editing, despite leaving the European Union, while Italy and Spain see a rising uptake among portrait and tourism photographers. Rundle Partners’ 2024 acquisition of Iris Booth underscores appetite for turnkey kiosks that bundle hardware and compliant software, simplifying rollout across multi-national corporate campuses.

Asia Pacific is growing at 14.80% CAGR through 2030, the fastest regional pace. Smartphone penetration above 70% in urban China and India fuels social-media-driven mini-sessions, creating demand for mobile-first booking apps. Japan and South Korea exhibit high per-capita software spend, favoring local language support and integrations with LINE and KakaoTalk. Australia mirrors North America in subscription adoption, while Indonesia and the Philippines lean on hybrid models because of inconsistent broadband. The Middle East and Africa region remains nascent but features bright spots such as the United Arab Emirates, where luxury-destination weddings drive premium software adoption.

Competitive Landscape

Competition is moderate, centered on feature arms races. HoneyBook leverages transaction data from USD 13 billion in processed payments to surface pricing benchmarks, reinforcing platform dependence. SmugMug’s deep integration with print labs embeds fulfillment workflows that discourage switching.

Disruptors like Imagen and Photoroom attract capital by positioning AI as the cost-reduction engine for high-volume post-production. Adobe’s bundle of Lightroom, Photoshop, and Creative Cloud storage retains gravitational pull, forcing rivals to differentiate via price or niche specialization. Privacy has become a battleground; ACDSee markets GPU-accelerated AI that never uploads files, targeting clients wary of cloud breaches.

Vertical integration trends are evident as vendors acquire complementary capabilities. Rundle Partners’ purchase of Iris Booth marries hardware kiosks with AI editing, creating an end-to-end self-service solution. Compliance certifications now influence enterprise deals; SOC 2, ISO 27001, and GDPR adequacy letters can command premium pricing. Overall, the top five vendors control roughly 45% of revenue, while the long tail of niche providers serves segment-specific needs, keeping the market moderately fragmented.

Photography Studio Software Industry Leaders

Sprout Studio Inc.

HoneyBook Inc.

17hats LLC

Studio Ninja Pty Ltd

Tave LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Adobe has launched Photoshop Elements 2025 and Premiere Elements 2025, featuring AI-powered tools such as Remove and Depth Blur.

- April 2025: ACDSee released Photo Studio Home 2025, featuring GPU-accelerated AI Super-Resolution and AVIF support.

- February 2025: Excire debuted Foto Office Edition, a network-enabled on-premise DAM priced from USD 29.90 per user per month.

- February 2025: ACDSee launched Photo Studio Professional 2025, featuring AI Object Masking and a new People Mode.

Global Photography Studio Software Market Report Scope

| Cloud |

| On-Premise |

| Hybrid |

| Scheduling and CRM |

| Post-Production Workflow |

| Financial Management |

| Marketing Automation |

| Analytics and Reporting |

| Single Photographer |

| Small Studio (2–5 Employees) |

| Mid-Sized Studio (6–15 Employees) |

| Large Studio (>15 Employees) |

| Wedding and Event Photographers |

| Portrait Studios |

| Commercial Studios |

| School Photography |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Kenya | |

| Rest of Africa |

| By Deployment Type | Cloud | |

| On-Premise | ||

| Hybrid | ||

| By Feature Set | Scheduling and CRM | |

| Post-Production Workflow | ||

| Financial Management | ||

| Marketing Automation | ||

| Analytics and Reporting | ||

| By Studio Size | Single Photographer | |

| Small Studio (2–5 Employees) | ||

| Mid-Sized Studio (6–15 Employees) | ||

| Large Studio (>15 Employees) | ||

| By End User | Wedding and Event Photographers | |

| Portrait Studios | ||

| Commercial Studios | ||

| School Photography | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the photography studio software market in 2025?

The photography studio software market size reached USD 720 million in 2025.

What is the expected CAGR through 2030?

Revenue is projected to grow at a 13.40% CAGR between 2025 and 2030.

Which deployment model is growing fastest?

Hybrid architectures are advancing at 15.68% CAGR as studios balance on-premise control with cloud scalability.

Which region is expanding most quickly?

Asia Pacific leads with a forecast 14.80% CAGR through 2030, driven by smartphone adoption and influencer-led demand.

How big is the opportunity in analytics tools?

Analytics and reporting modules are the fastest-growing feature set, climbing at 15.27% CAGR and projected to top USD 180 million by 2030.

What security concerns influence buying decisions?

Data breaches like the 2024 Dropbox Sign incident have raised demand for platforms offering on-device AI processing and SOC 2-certified cloud options.

Page last updated on: