Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

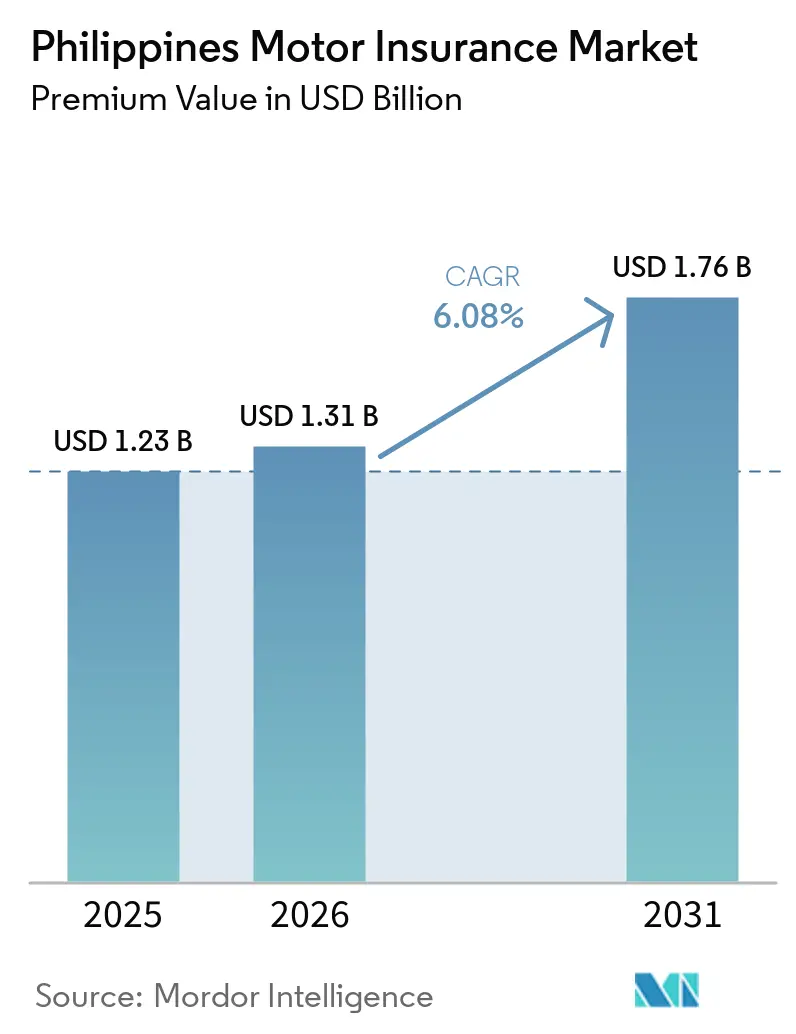

| Base Year Market Size (2025) | USD 1.23 Billion |

| Market Size (2026) | USD 1.31 Billion |

| Market Size (2031) | USD 1.76 Billion |

| Growth Rate (2026 - 2031) | 6.08% CAGR |

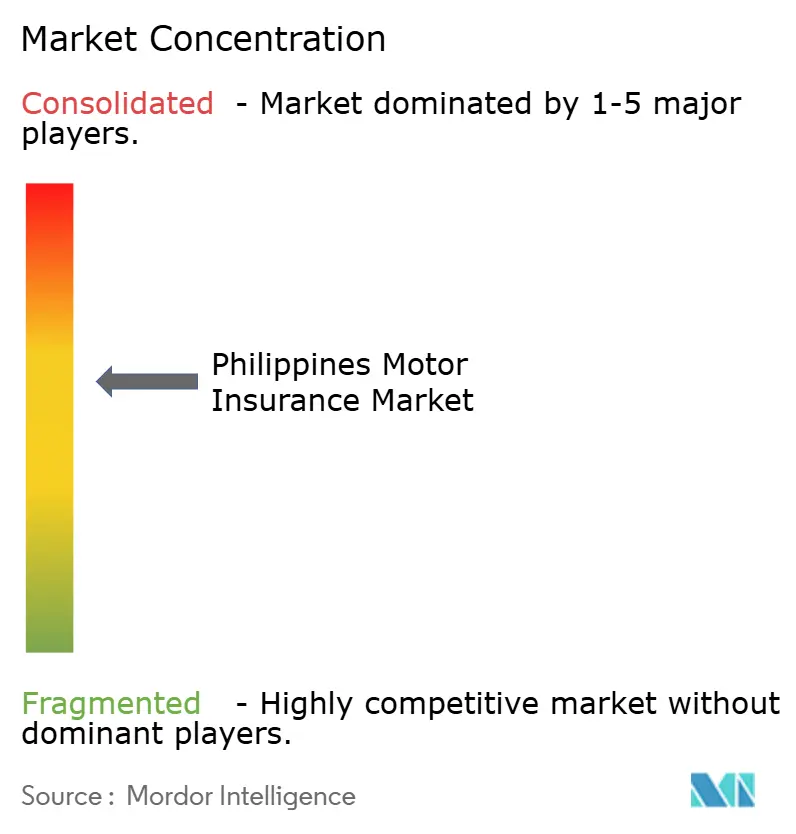

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Philippines Motor Insurance Market Analysis by Mordor Intelligence

The Philippines Motor Insurance Market size in terms of premium value is projected to expand from USD 1.23 billion in 2025 and USD 1.31 billion in 2026 to USD 1.76 billion by 2031, registering a CAGR of 6.08% between 2026 to 2031.

Market growth is set to be shaped by mandatory Compulsory Third Party Liability requirements for vehicle registration, stronger regulatory enforcement, and a shift toward digital distribution that expands access and improves verification at the point of registration. Established insurers hold a sizable share, while specialized players and embedded distribution channels pursue targeted niches arising from rising EV adoption, telematics use cases, and microinsurance products. Higher EV registrations and policy incentives under the Electric Vehicle Industry Development Act support future premium pools, while integration between the Land Transportation Office and insurers for online pre-validation reduces fraud and supports compliant market growth.[1]Joann Villanueva, “Registered EVs expected to reach 35K by end of 2025,” Philippine News Agency, pna.gov.ph Macroeconomic stability, rising insurance density, and bancassurance cross-sell continue to underpin the Philippines motor insurance market as consumer protection rules and digital transformation strengthen market integrity.

Key Report Takeaways

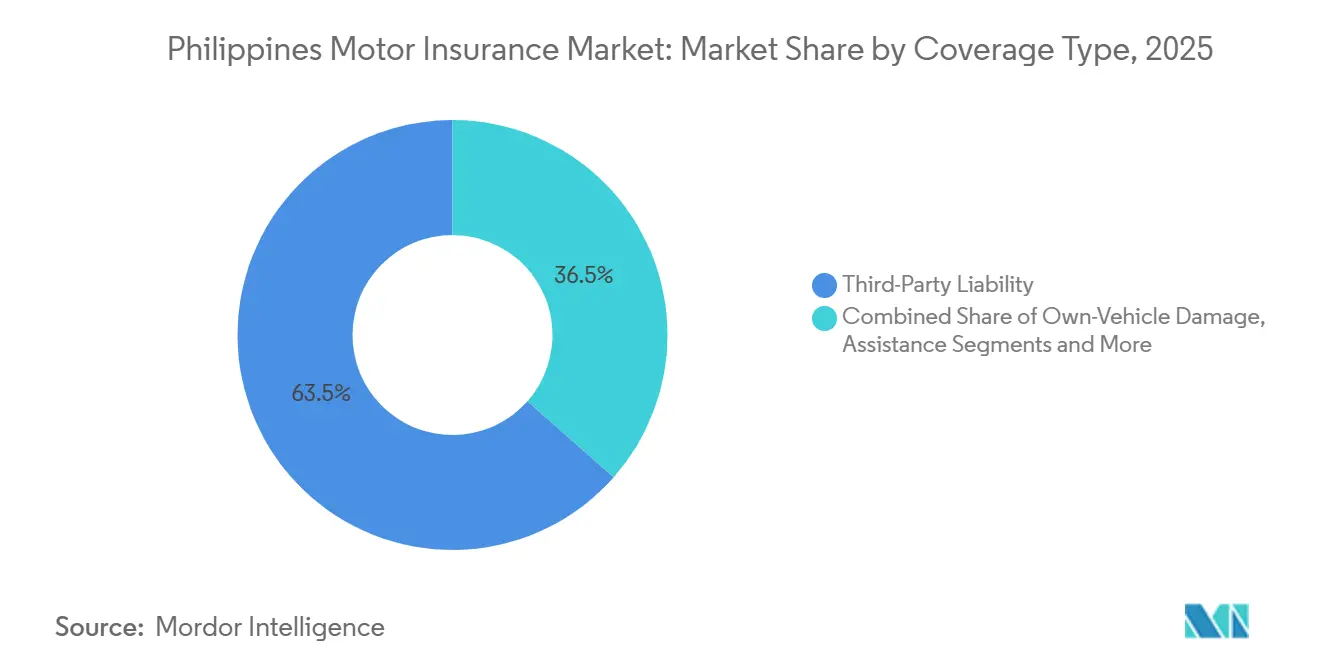

- By coverage type, third-party liability coverage led with 63.50% of the Philippines motor insurance market size in 2025, while own-vehicle damage is forecast to expand at a 9.56% CAGR through 2031.

- By vehicle type, passenger cars commanded 56.80% of the Philippines motor insurance market size in 2025, while commercial vehicles are projected to post a 12.66% CAGR through 2031.

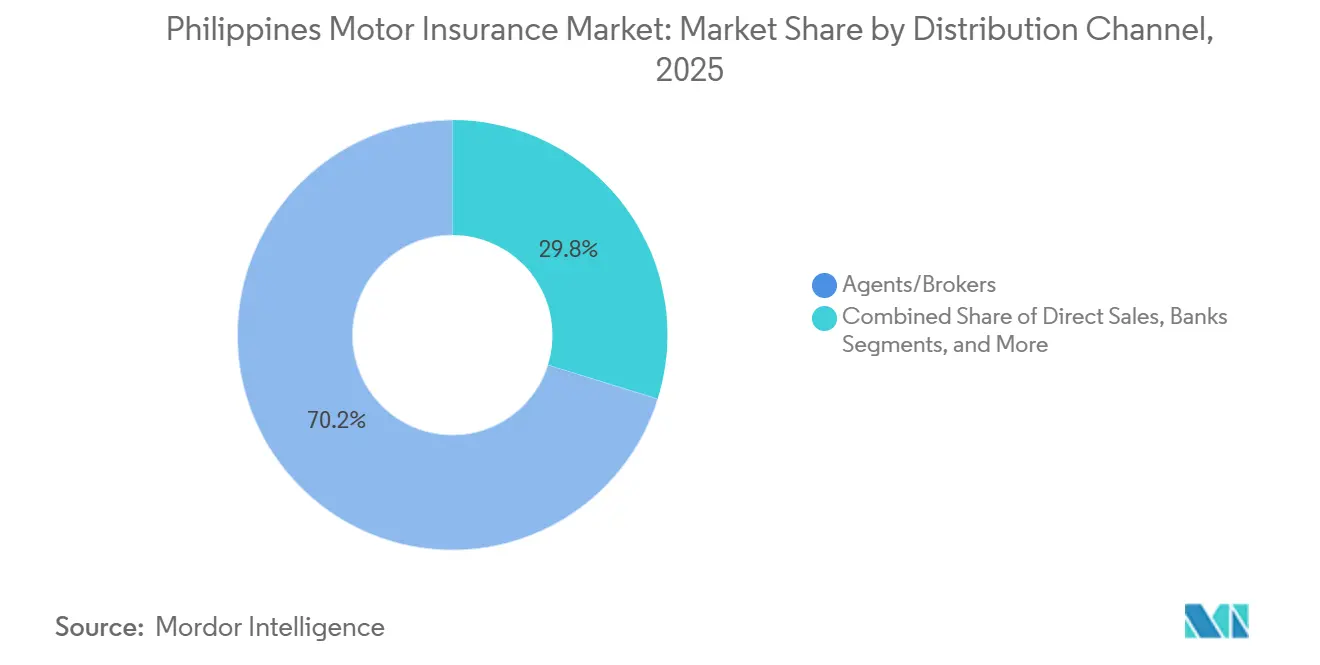

- By distribution channel, agents and brokers held 70.20% of the Philippines motor insurance market size in 2025, while digital platforms and other emerging channels are set to grow at a 9.23% CAGR through 2031.

- By powertrain, internal combustion engine vehicles accounted for 58.70% of the Philippines motor insurance market size in 2025, while electric vehicles are expected to advance at a 10.93% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Philippines Motor Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory CTPL for registration | +1.8% | National, with the highest enforcement in Metro Manila, Cebu, and Davao | Medium term (2-4 years) |

| Growth in the vehicle fleet and motorization | +1.5% | National, spill-over from urban centres to provincial areas | Long term (≥ 4 years) |

| Motor's dominant share in non-life premiums | +1.2% | National, with concentration in NCR and Calabarzon | Medium term (2-4 years) |

| Macroeconomic growth and rising insurance density | +0.9% | National, with early gains in Metro Manila, Makati, and BGC | Long term (≥ 4 years) |

| High accident and economic loss burden | +0.8% | Metro Manila, Quezon City, and major provincial highways | Short term (≤ 2 years) |

| Regulatory strengthening and enforcement actions | +0.6% | National, with Insurance Commission and LTO coordination | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Mandatory CTPL For Registration

Mandatory CTPL ties insurance to vehicle registration, which sustains a large and recurring policy base across the Philippines motor insurance market as annual renewals reinforce compliance at the Land Transportation Office. The Insurance Commission doubled minimum third-party liability limits in March 2024 and raised no-fault indemnity, which increased the cover value and expanded premium pools for licensed CTPL providers[2]Insurance Commission, “INSURANCE PENETRATION, DENSITY RISE IN Q1 2025 VIS-À-VIS Q1 2024,” Insurance Commission, insurance.gov.ph. Online pre-validation of Certificates of Coverage through LTO and DBP Data Center enables real-time verification during registration, which reduces fraudulent certificates and helps stabilize pricing economics for the Philippines motor insurance market. Motor car insurance’s prominent role in non-life premiums creates steady inflows that help carriers maintain coverage availability and product variety in the Philippines motor insurance market. As digitization improves transparency at the point of registration, insurers can align pricing with risk and streamline distribution, which supports broader compliance and healthier growth profiles across the Philippines motor insurance market.

Growth In Vehicle Fleet and Motorization

Vehicle registrations and the shift to newer propulsion technologies generate incremental policy opportunities across the Philippines motor insurance market, as each new unit requires at least CTPL, and many opt for broader cover over time. EV registrations rose strongly, and the Electric Vehicle Industry Development Act framework supports adoption through fiscal incentives and policy targets that extend premium potential into new risk categories. The Department of Energy’s roadmap outlines multi-year EV expansion under clean energy scenarios, which encourages insurers to tailor products for battery risks, charging infrastructure liabilities, and evolving repair ecosystems in the Philippines motor insurance market[3]Felix William B. Fuentebella, “Evolution in Motion,” Department of Energy, liveablecities.ph. Growth is no longer confined to Metro Manila as digitized verification and online distribution enable insurers to reach provincial areas more efficiently across Visayas and Mindanao. Expansion in emerging economic corridors and logistics hubs increases commercial fleet exposure, which adds volume and diversifies risk in the Philippines motor insurance market. Together, these dynamics sustain a long-term growth runway as motorization deepens and product sophistication rises in the Philippines motor insurance market.

Motor’s Dominant Share in Non-Life Premiums

Motor car insurance contributed a leading share of non-life premiums, which anchors revenue stability and supports technology investments that improve underwriting and claims in the Philippines motor insurance market. Carriers leverage this scale to upgrade core platforms, speed up product launch cycles, and standardize processes that reduce friction across distribution and service. The segment’s retail nature supports cross-sell through bancassurance and direct channels, which helps expand protection beyond CTPL and deepens customer relationships in the Philippines motor insurance market. Reinsurance and capital strength enable insurers to keep coverage available while calibrating rates to match loss experience in catastrophe-prone regions, which helps sustain market continuity during hardening cycles. The Philippines motor insurance market benefits from a broad base of recurring premiums and short-tail characteristics that help carriers balance portfolios and fund digital initiatives with predictable cash flows. These factors reinforce the motor’s role as a growth engine for broader non-life expansion in the Philippines motor insurance market.

Macroeconomic Growth and Rising Insurance Density

Macro fundamentals and rising insurance participation support steady premium inflows in the Philippines motor insurance market as households gain the capacity to add cover beyond mandatory CTPL. Insurance density increased year over year in 2025, signalling higher per-person spending on risk protection that strengthens the base for comprehensive motor products. Stable domestic demand supported by remittances and gradual monetary easing helps auto financing and new policy origination in the Philippines motor insurance market. The broader policy environment that improves digital verification and consumer protection builds trust and reduces friction in claims and services. These shifts reinforce a steady transition from basic liability to wider coverage as the Philippines motor insurance market matures. Over time, greater financial inclusion and targeted education can support deeper product penetration across regions in the Philippines motor insurance market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low overall insurance penetration | -1.2% | National, with acute gaps in Visayas and Mindanao | Medium term (2-4 years) |

| Affordability constraints for households | -0.9% | Provincial areas and low-income urban communities | Short term (≤ 2 years) |

| Fake CTPL and unauthorized sellers | -0.7% | Metro Manila, Cebu, and areas with weak LTO enforcement | Short term (≤ 2 years) |

| Road safety and infrastructure gaps are raising loss costs | -1.1% | Metro Manila, Commonwealth Avenue, and flood-prone corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Low Overall Insurance Penetration

Insurance penetration remains below regional benchmarks, which limits the addressable base for voluntary motor cover beyond the mandatory CTPL in the Philippines motor insurance market. While density and penetration improved in 2025, the aggregate level suggests significant room to grow through financial education and easier purchasing journeys. Market participants are expanding digital channels and bancassurance to close awareness and access gaps across the Philippines motor insurance market. Greater inclusion can shift more motorists from CTPL-only to comprehensive and add-ons, which raises average premiums and deepens protection over time. Progress relies on trust-building and frictionless verification at the point of vehicle registration to support consistent take-up in the Philippines motor insurance market. Over the medium term, better enforcement and wider digital reach can help narrow gaps across regions in the Philippines motor insurance market.

Affordability Constraints For Households

Inflation and household budget priorities can limit willingness to purchase comprehensive cover for many motorists, which constrains the pace of optional policy growth in the near term within the Philippines motor insurance market. Monetary easing since late 2024 has helped lower borrowing costs, yet insurance spending still competes with essentials in lower-income segments. Microinsurance initiatives and digital-first products with very low premiums demonstrate a path to scale, which supports inclusion and can serve as gateways to broader protection in the Philippines motor insurance market. Partnerships between mobile wallets and insurers show momentum for low-cost accident cover that can be bundled and distributed efficiently to large user bases. Over time, rising insurance density and improved digital experiences can support a gradual shift from CTPL-only toward comprehensive options in the Philippines motor insurance market. These measures help mitigate affordability barriers while improving consumer protection in the Philippines motor insurance market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Coverage Type: CTPL Anchors While Comprehensive Gains Momentum

Third-party liability coverage led with 63.50% of the Philippines motor insurance market share in 2025, supported by the compulsory requirement linked to annual vehicle registration at the Land Transportation Office. The March 2024 increase in mandatory CTPL benefits broadened policy value, which lifted premium capacity and helped formalize the base for recurring renewals in the Philippines motor insurance market. Better verification through the LTO and DBP Data Center reduces fake certificates, which stabilizes pricing and improves the customer experience at registration. As digital distribution and bancassurance mature, more motorists consider add-ons that fit specific needs, which slowly shifts coverage beyond basic liability in the Philippines motor insurance market. These moves reinforce CTPL’s role as the entry point while creating space for incremental value through tailored products in the Philippines motor insurance market.

Own-vehicle damage is the fastest-growing optional cover, supported by rising insurance density and product innovation that makes comprehensive protection easier to buy and manage in the Philippines motor insurance market. The Philippines motor insurance market size for own-vehicle damage is projected to expand at a 9.56% CAGR between 2026 and 2031 as digital workflows and partnerships lower friction and improve access. Wider add-on adoption, such as roadside assistance and accident riders, supports policy differentiation as insurers serve varied consumer profiles across regions. Bancassurance partners also cross-sell motor cover to loan and deposit clients, which raises attach rates and broadens protection beyond CTPL in the Philippines motor insurance industry. As unit economics improve through technology and scale, carriers can sustain product breadth and service quality in the Philippines motor insurance market.

By Vehicle Type: Passenger Cars Lead, Commercial Surges

Passenger cars commanded 56.80% of the Philippines motor insurance market share in 2025, reflecting their larger base in urban centres and sustained consumer preference for private mobility. Carriers maintain steady renewal volumes from multi-year vehicle finance, and they use technology to reduce friction in quotes, binding, and claims for car owners in the Philippines motor insurance market. As macro stability and insurance density improve, a portion of CTPL-only policies migrate toward broader cover, which supports average premium growth for passenger cars. Bancassurance channels add reach by bundling motor products at the point of financing, which strengthens cross-sell in the Philippines motor insurance market. Digital verification and improved claims response contribute to higher satisfaction for passenger car policyholders in the Philippines motor insurance market.

Commercial vehicles are set to outpace overall market growth as logistics, e-commerce, and provincial development raise fleet needs across the Philippines motor insurance market. The Philippines motor insurance market size for commercial vehicles is projected to expand at a 12.66% CAGR between 2026 and 2031 as operators seek cover for vehicle damage, cargo liability, and business disruption. Risk solutions tailored to fleet operators, including driver programs and route risk management, support lower loss ratios and improved retention in the Philippines motor insurance market. Insurers are also aligning with road safety action plans and infrastructure schedules to refine pricing and improve service reliability for commercial clients. These factors combine to maintain the commercial segment’s strong growth momentum in the Philippines motor insurance industry.

By Distribution Channel: Agents Dominate, Digital Disrupts

Agents and brokers retained 70.20% of the share in 2025, leveraging personal relationships for complex risks and regional reach across the Philippines motor insurance market. As compliance improves through verification and stronger market conduct, agency distribution remains central for commercial fleets and tailored solutions. Bancassurance continues to expand access by embedding offers in retail and SME customer journeys, which sustains cross-sell in the Philippines motor insurance market. Direct channels support price transparency and speed of issuance for simple policies, which complements the agency model for broader coverage. The mixed model helps carriers serve diverse customer preferences within the Philippines motor insurance market.

Digital platforms and emerging embedded channels are projected to grow at a 9.23% CAGR through 2031 as partnerships with fintechs and marketplaces streamline comparison and purchase across the Philippines motor insurance market. Banks are also embedding in-app marketplaces that apply AI for recommendations, which extends reach to digitally active customers in the Philippines motor insurance industry. Insurers continue to upgrade core platforms to enable instant quotes, straight-through issuance, and faster claims for online buyers. Digital and agency models operate in tandem, which helps maintain service quality while improving access in the Philippines motor insurance market. As verification integrates with registration, digital distribution gains further credibility and scale in the Philippines motor insurance market.

By Powertrain: ICE Prevails, EVs Electrify Growth

Internal combustion engine vehicles accounted for 58.70% share in 2025, reflecting their large installed base and associated supply chains that support readily available repairs across the Philippines motor insurance market. ICE vehicles remain the mainstream risk pool for CTPL and comprehensive cover, and they anchor premium revenues during the EV transition. Insurers continue to refine pricing as loss experience and parts costs evolve, while supporting quicker claims turnaround through standardized processes. As fleet composition shifts, ICE-focused underwriting remains essential for stability in the Philippines motor insurance market. Over the forecast period, ICE will coexist with accelerating EV adoption and hybrid uptake in the Philippines motor insurance market.

Electric vehicles gained momentum, supported by fiscal incentives under EVIDA and a multi-year roadmap that targets significant EV penetration by 2040 in the Philippines motor insurance market. The Philippines motor insurance market size linked to EVs is projected to expand in line with a 10.93% CAGR for EV policies from 2026 to 2031 as carriers introduce battery and charging-related cover. Public charging infrastructure is scaling toward multi-year targets, and insurers are adapting products for battery degradation and fire risk unique to EVs. Policy coordination around EV licensing and safety standards further supports orderly growth in the Philippines motor insurance market. With improved data and repair ecosystems, EV underwriting can mature and diversify premium sources in the Philippines motor insurance market.

Geography Analysis

Premium volumes concentrate in Metro Manila and other Luzon corridors where vehicle density and economic activity are highest, which shapes account distribution and claims dynamics in the Philippines motor insurance market. Corridors with high incident counts, such as EDSA and C-5, carry elevated risk, and carriers calibrate pricing and limits accordingly to maintain technical margins. Luzon’s concentration aligns with the largest base of vehicle registrations and institutional presence, which supports multi-channel distribution in the Philippines motor insurance market. Improved accident response initiatives by local authorities target reductions in incident severity and faster resolution times that can moderate loss costs. Over time, infrastructure projects in key corridors aim to improve safety and resilience, which supports steady growth in the Philippines motor insurance market.

Beyond Metro Manila, Cebu and other urban centres in Visayas show rising vehicle registrations and commercial activity that expand policy demand in the Philippines motor insurance market. Online verification of CTPL and digital policy issuance makes it easier to serve provincial motorists, which reduces friction in renewals and claims. Growth corridors that benefit from logistics and port development sustain demand for fleet cover and cargo-related protections. As local distributors and banks expand in these areas, multi-channel sales can deepen penetration in the Philippines motor insurance market.

Mindanao’s urban centres, including Davao and Cagayan de Oro, are gaining investment in roads and coastal infrastructure that improve the movement of goods and people, which supports future motor policy growth in the Philippines motor insurance market. With digitized verification scaling beyond the capital, compliance and service delivery improvements can narrow regional gaps across the Philippines motor insurance market. As road safety plans spread to secondary cities, loss ratios may moderate over time and improve underwriting outcomes. Combined, these geographic trends balance concentration in NCR with emerging growth across regions in the Philippines motor insurance market.

Competitive Landscape

The Philippines motor insurance market remains moderately concentrated, with established carriers leading gross premiums written and setting the pace on digital transformation and underwriting discipline. Market leaders invest in core platform upgrades to reduce time-to-market and automate service, which supports better customer experience and operating leverage across the Philippines motor insurance market. Upgrades in catastrophe modelling and analytics also strengthen risk selection and capital allocation. As compliance strengthens and digital verification reduces fraud, competitive focus shifts to pricing precision and service differentiation in the Philippines motor insurance market. The base of recurring CTPL premiums supports investments that improve straight-through processing and claim resolution in the Philippines motor insurance market.

Consolidation is an active theme as select players combine to gain scale and improve operating efficiency in the Philippines motor insurance market. Embedded distribution partnerships deepen ties with financial services and e-commerce ecosystems, which help carriers extend reach into new segments at lower acquisition cost. Company-led sustainability and end-of-life vehicle initiatives align with circular economy goals and improve recovery values for insured fleets. Digital product launches through mobile wallets position insurers to tap large user bases, which supports inclusion and incremental premiums in the Philippines motor insurance market. Broadly, competitive strategies reinforce technology, partnerships, and capital strength as advantages in the Philippines motor insurance market.

Capital buffers and reinsurance costs shape pricing and product breadth, while bancassurance partners with strong balance sheets can compete effectively during pricing cycles in the Philippines motor insurance market. Hardening reinsurance conditions heighten the need for underwriting discipline and adequate rates to sustain coverage availability. Carriers with upgraded systems and integrated distribution can move faster to address EV risks, embedded offers, and microinsurance propositions at scale across the Philippines motor insurance market. Regulatory modernization and digital verification create a healthier operating environment that rewards compliant players and sharpens competitive differentiation in the Philippines motor insurance market. Over the medium term, these shifts are set to elevate product quality and service standards in the Philippines motor insurance market.

Philippines Motor Insurance Industry Leaders

Malayan Insurance Company, Inc.

Pioneer Insurance & Surety Corporation

Prudential Guarantee & Assurance, Inc.

BPI/MS Insurance Corporation

Intact Financial Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: RCBC partnered with Igloo to launch an embedded digital insurance marketplace on the Pulz banking app, featuring AI-powered product recommendations for retail users.

- October 2025: GCash and BPI MS Insurance launched PasaHERO Protect, an affordable accident insurance product priced at PHP 15 per month for public transport users through the GInsure platform.

- August 2025: FPG Insurance Company and The Mercantile Insurance Company announced a definitive merger agreement to create a non-life insurance powerhouse in the Philippines, combining scale and operational capabilities across property, motor, and casualty lines.

- July 2025: Toyota Motor Philippines endorsed Standard Insurance Co., Inc. as the second model End-of-Life Vehicle dismantling facility under the Toyota Global 100 Dismantlers Project, with a USD 0.30 million (PHP 17.8 million) investment in a technical centre in Naic, Cavite.

Philippines Motor Insurance Market Report Scope

Motor Insurance is a type of insurance policy that covers the customers' vehicles from potential risks financially. The policyholder's car or two-wheeler is provided financial security against damages arising out of accidents and other threats. The Philippines motor insurance market is segmented by type (compulsory third-party liability insurance, comprehensive motor car insurance) and by distribution channel (agency, banks, direct, and others).

By Coverage Type

| Third-Party Liability | |

| Own-Vehicle Damage | Collision |

| Comprehensive (Theft, Glass, Fire, etc.) | |

| Assistance & Add-ons (Roadside, Legal) |

By Vehicle Type

| Passenger Cars |

| Commercial Vehicles |

By Distribution Channel

| Direct |

| Agents/Brokers |

| Banks |

| Embedded Channels (OEM, Affinity, etc.) |

| Digital Platforms and Other Emerging Channels |

By Powertrain

| ICE Vehicles |

| Electric Vehicles |

| Hybrid Vehicles |

| Others (Hydrogen FCEV, LPG/CNG, etc.) |

| By Coverage Type | Third-Party Liability | |

| Own-Vehicle Damage | Collision | |

| Comprehensive (Theft, Glass, Fire, etc.) | ||

| Assistance & Add-ons (Roadside, Legal) | ||

| By Vehicle Type | Passenger Cars | |

| Commercial Vehicles | ||

| By Distribution Channel | Direct | |

| Agents/Brokers | ||

| Banks | ||

| Embedded Channels (OEM, Affinity, etc.) | ||

| Digital Platforms and Other Emerging Channels | ||

| By Powertrain | ICE Vehicles | |

| Electric Vehicles | ||

| Hybrid Vehicles | ||

| Others (Hydrogen FCEV, LPG/CNG, etc.) | ||

Key Questions Answered in the Report

What is the size and growth outlook of the Philippines motor insurance market in 2026 and beyond?

The Philippines motor insurance market size is USD 1.31 billion in 2026 and is projected to reach USD 1.76 billion by 2031 at a 6.08% CAGR, supported by mandatory CTPL, digitized verification, and rising insurance density.

Which coverage types lead growth in the Philippines motor insurance market, and why?

Third-party liability leads due to compulsory registration rules, while own-vehicle damage is the fastest-growing optional cover as digital workflows improve access and consumers seek broader protection beyond CTPL.

How are digital platforms changing distribution in the Philippines motor insurance market?

API-based integrations and embedded bank marketplaces enable real-time comparison, instant quotes, and straight-through issuance, which expands access while agency channels continue to serve complex and commercial risks.

What role do EVs play in the Philippines motor insurance market through 2031?

EV registrations are rising under EVIDA policy support and infrastructure goals, which creates demand for battery and charging-related coverage and contributes to a projected 10.93% CAGR for EV policies.

Which regions contribute most to premiums in the Philippines motor insurance market?

Premiums concentrate in Metro Manila and Luzon corridors due to high vehicle density and economic activity, while Visayas and Mindanao are supported by digitized CTPL verification and expanding distribution.

What recent developments are reshaping the Philippines motor insurance market in 2025-2026?

Key moves include a non-life merger announcement, embedded bank marketplaces, mobile wallet accident products, and platform upgrades by leading insurers, all improving scale, access, and service.

Page last updated on: