Philippines Global Capability Centers Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

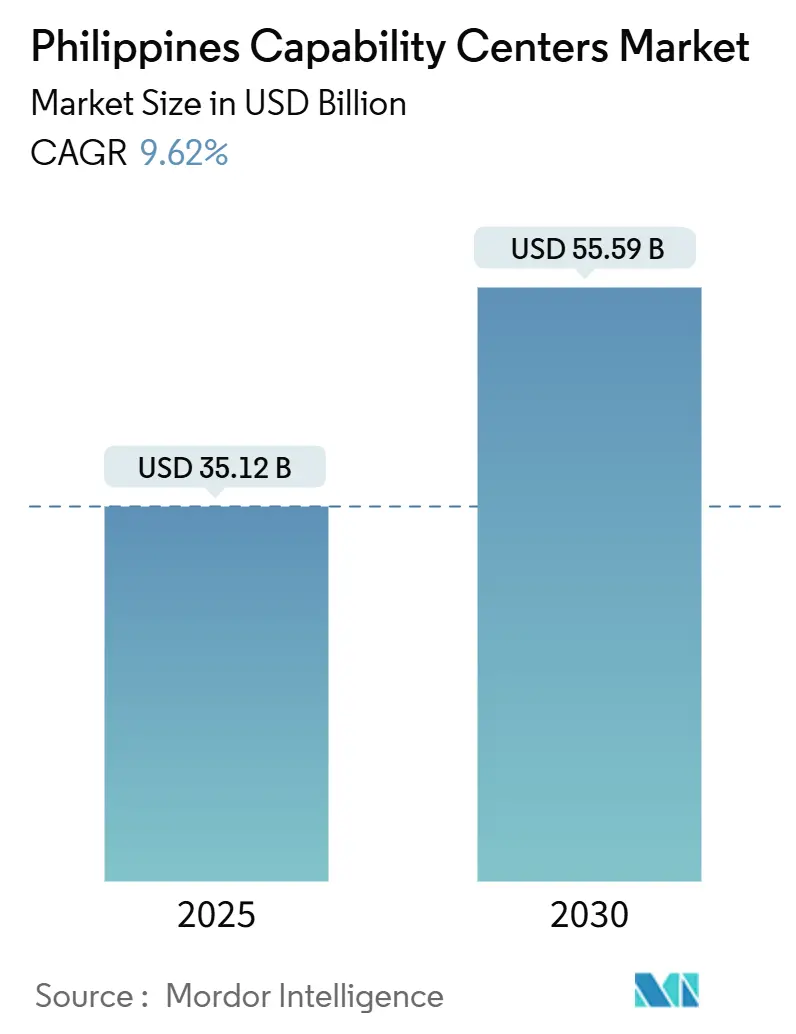

| Market Size (2025) | USD 35.12 Billion |

| Market Size (2030) | USD 55.59 Billion |

| Growth Rate (2025 - 2030) | 9.62% CAGR |

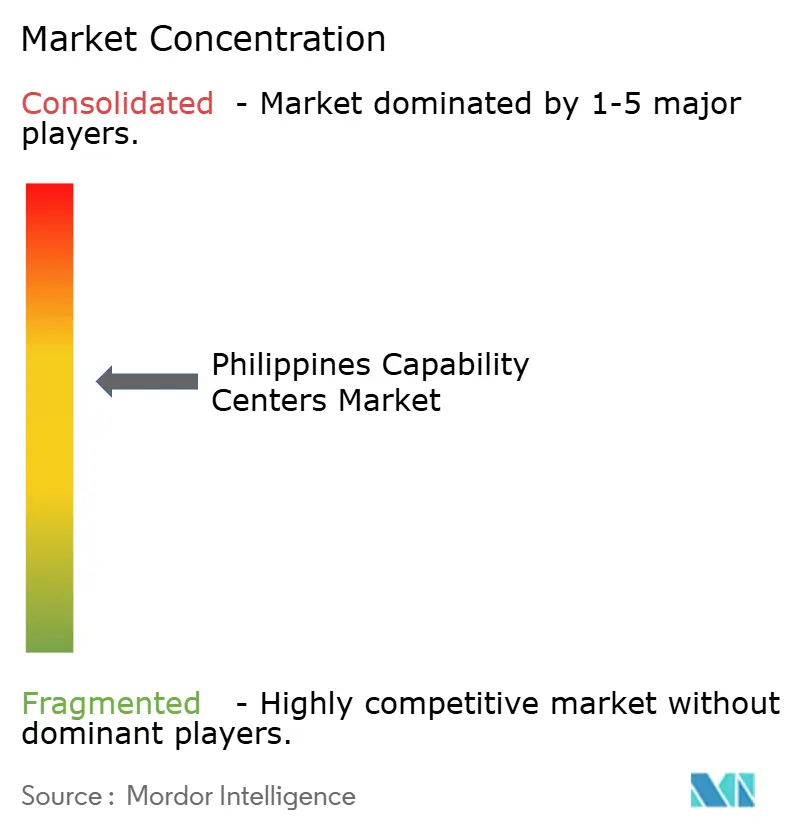

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Philippines Global Capability Centers Market Analysis by Mordor Intelligence

The Philippines Global Capability Centers market size stood at USD 35.12 billion in 2025 and is on track to reach USD 55.59 billion by 2030, translating into a 9.62% CAGR over the forecast period. The Philippines' Global Capability Centers market is experiencing strong momentum as multinational corporations diversify their service-delivery footprints, capitalize on English-proficient talent, and hedge against geopolitical risk across the Asia-Pacific. Government efforts, particularly the CREATE MORE Act, lower corporate taxes and streamline compliance, reinforcing investor confidence. Early adopters who opened GenAI Centers of Excellence report sizable productivity gains, strengthening the location’s appeal for higher-value digital work. At the same time, provincial digital-city programs help alleviate Metro Manila's saturation and expand the Philippines' Global Capability Centers market into cost-competitive secondary hubs.[1]Department of Finance, “CREATE MORE Act Implementation Guidelines,” DOF.gov.ph

Key Report Takeaways

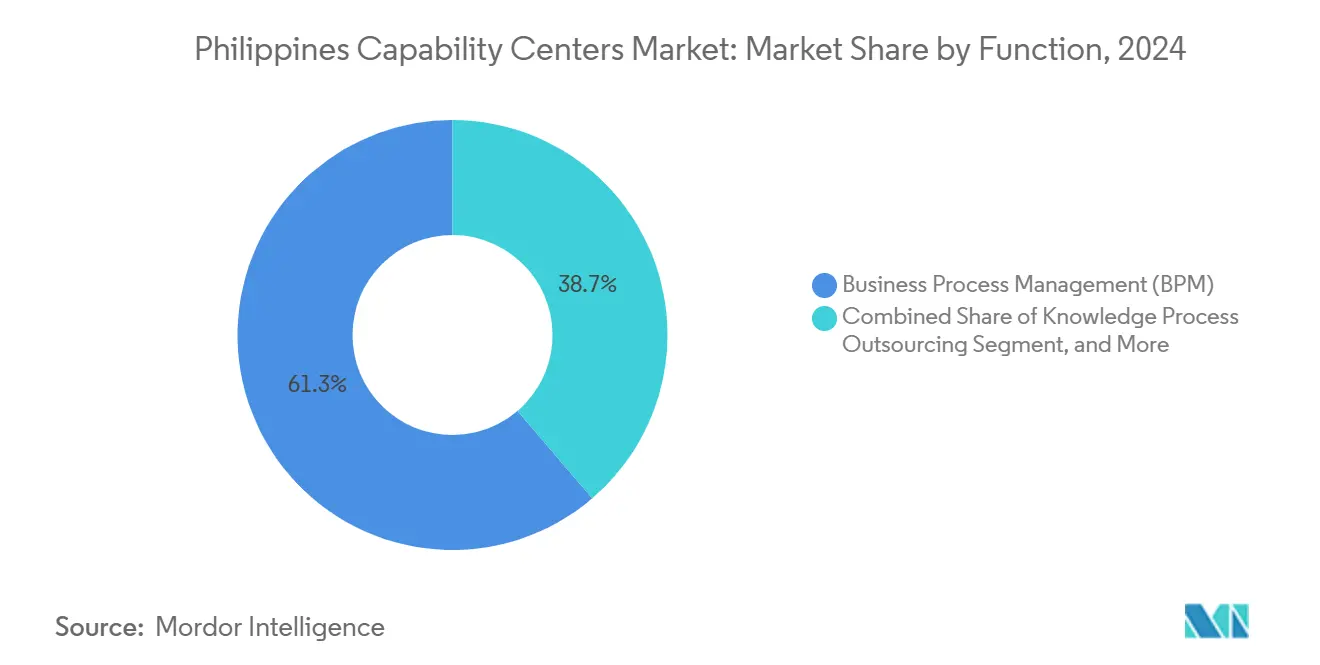

- By function, Business Process Management held 61.27% of the Philippines Global Capability Centers market share in 2024; Information Technology and Digital Services is forecast to expand at a 10.27% CAGR to 2030.

- By engagement model, captive centers commanded a 59.41% share of the Philippines Global Capability Centers market size in 2024, while hybrid Build-Operate-Transfer models are projected to register the highest CAGR at 10.42% through 2030.

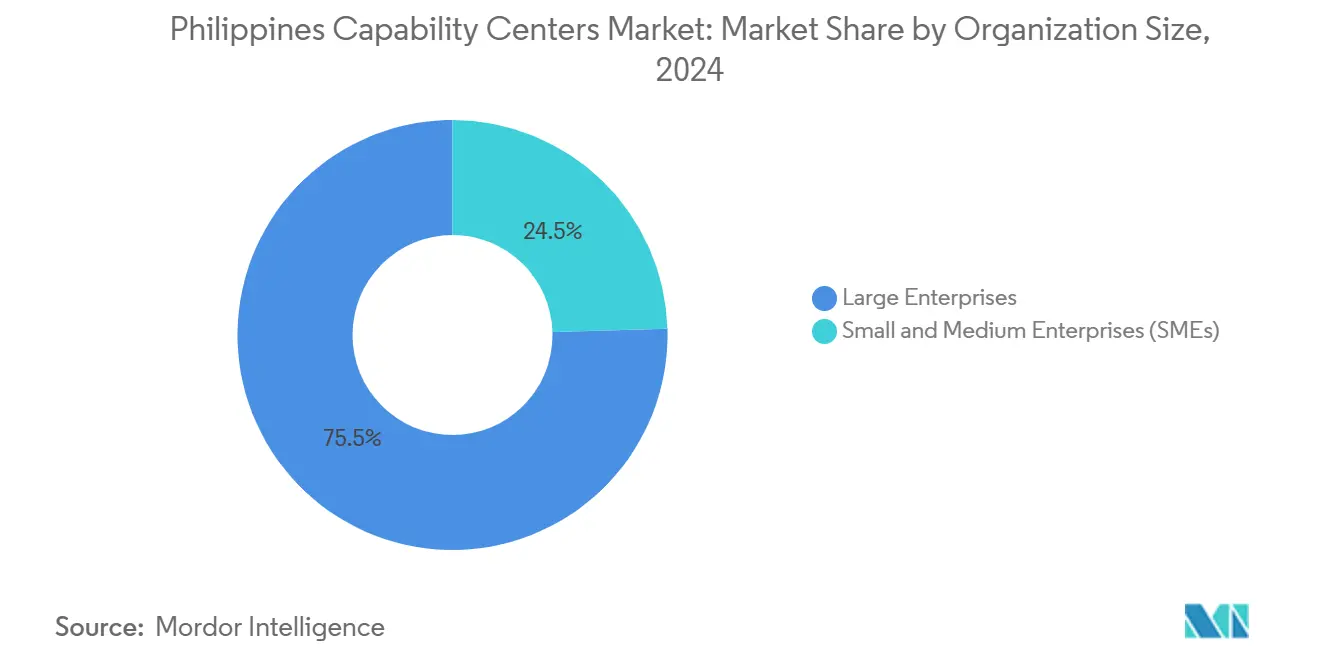

- By organization size, large enterprises accounted for 75.47% of the Philippines' Global Capability Centers market share in 2024; small and medium enterprises are expected to advance at an 11.23% CAGR between 2025 and 2030.

- By industry vertical, banking, financial services, and insurance are the fastest-growing segments, with a 10.21% CAGR to 2030. Meanwhile, telecom and IT continue to contribute the largest revenue share, at 33.56% in 2024.

Philippines Global Capability Centers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for digital transformation support | +2.8% | Global, concentrated in North America and Europe client markets | Medium term (2-4 years) |

| Philippine English proficiency and cultural affinity | +1.9% | Global, strongest for North America and Australia | Long term (≥ 4 years) |

| Competitive labor costs relative to peer APAC hubs | +1.6% | Asia-Pacific core, spillover to the Middle East and Africa | Short term (≤ 2 years) |

| Rapid scale-up of GenAI Centers of Excellence | +2.1% | Global, early adoption in Metro Manila and Cebu | Medium term (2-4 years) |

| Government CREATE and PPP Code reforms | +1.4% | National, with PEZA zones and digital cities | Long term (≥ 4 years) |

| Emergence of provincial digital cities | +0.8% | National gains in Cebu, Davao, and Clark | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Digital Transformation Support From Multinational Corporations

Enterprises are modernizing core systems, which drives new demand for cloud engineering, data analytics, and cybersecurity services delivered from Philippine centers. These projects require agile squads, so providers bundle specialists in product sprints rather than traditional shift work. As a result, hybrid engagement contracts now include outcome-based pricing tied to release schedules and security milestones. JPMorgan Chase expanded its staff in Manila to 20,000, placing developers, data scientists, and cyber analysts in a single agile campus.[2]JPMorgan Chase, “Annual Report 2024,” JPMorganChase.com Smaller software firms follow a similar path, leasing plug-and-play space that can double their headcount within a year. This sustained pipeline of project work converts the Philippines Global Capability Centers market into an engine for continuous digital innovation rather than episodic cost savings.

Philippine English Proficiency and Cultural Affinity With Western Markets

The country’s workforce ranks among Asia’s best on the EF English Proficiency Index, providing friction-free communication in voice, chat, and video interactions. Cultural familiarity with United States and European business etiquette speeds onboarding, because frontline teams already understand colloquial references and customer-service norms. Clients report shorter training cycles, which lowers ramp-up costs and improves first-call resolution rates for high-touch support roles. This soft-skill edge becomes more valuable as automation handles routine queries and escalations require nuanced dialogue. Companies, therefore, locate premium customer-experience pods in Metro Manila and Cebu, while routing commodity tickets to bots for triage and resolution. The blend of human empathy and language clarity anchors long-term contracts even when wage differentials narrow.

Competitive Labor Costs Relative to Peer Asia-Pacific Hubs

The average software engineer's pay sits near USD 20,241, still well below that of Singapore and Sydney, giving investors an immediate operating-margin boost.[3]CBRE, “Global Tech Talent Report 2024,” CBRE.com Rental costs in Bonifacio Global City are rising, yet remain roughly half of comparable Grade A space in Singapore, preserving location economics for at least three more years. Companies further trim their overhead by using coworking floors in provincial cities, where rents can be 40% lower than those in Manila equivalents. Wage inflation has hovered at single-digit levels since 2023, which is slower than regional peers such as India’s Bengaluru and Vietnam’s Ho Chi Minh City. Enterprises balance cost and capability by splitting teams: high-skill architects in Manila, larger test and support groups in Cebu or Davao. This tiered approach keeps the Philippines Global Capability Centers market competitive even as regional price gaps tighten.

Rapid Scale-Up of GenAI Centers of Excellence by Early Adopters

Professional-services majors such as PwC committed USD 50 million to build a 5,000-person AI hub that designs proprietary models for global clients. These centers report productivity gains of 25-40% in document review, pricing analysis, and claims processing once GenAI tools mature beyond the pilot stage. Philippine universities respond by adding prompt-engineering courses, feeding a talent pipeline that blends linguistics with coding. Providers pair data stewards with machine-learning engineers, creating hybrid roles that oversee algorithm fairness and regulatory compliance. Multinationals export the resulting frameworks to other sites, making the Philippines the reference location for GenAI implementation playbooks. Such success stories reinforce investor confidence and spark a clustering effect, where adjacent firms co-locate to share talent pools and training labs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying global competition from India, Poland, and Colombia | -1.8% | Global, especially in Europe and Latin America | Short term (≤ 2 years) |

| Persistent digital-infrastructure gaps (broadband cost and reliability) | -1.2% | National, acute in provincial areas | Medium term (2-4 years) |

| High exposure of voice-centric roles to GenAI displacement | -2.1% | Global affects traditional customer support | Short term (≤ 2 years) |

| Rising commercial real estate costs in Metro Manila CBDs | -0.9% | Metro Manila core, spillover to secondary districts | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Intensifying Global Competition From India, Poland, and Colombia

India extends incentives to tier-2 cities, Poland highlights European Union data-sovereignty compliance, and Colombia leverages near-shore proximity to the United States, collectively squeezing Philippine win rates on new bids.[4]IBPAP, “Competitive Analysis Brief 2024,” IBPAP.org Clients now issue multi-country RFPs, ranking locations on cybersecurity maturity and sustainability metrics in addition to cost. To stay in contention, Philippine operators certify to ISO 27701 for privacy management and publish carbon-neutral targets. Government agencies add double-deduction perks for green buildings to level the playing field. Providers also emphasize domain fluency, such as fintech risk analytics or healthcare coding, to win work less sensitive to wage gaps. These moves reshape competition from a race to the bottom on price into a contest of specialized value creation.

High Exposure of Voice-Centric Roles to GenAI Displacement

Conversational AI could automate up to 40% of call-center tasks within three years, reducing the demand for entry-level agents. Philippine firms run large reskilling programs that move staff into chat moderation, escalation management, and AI-supervisor positions. Early evidence suggests that blended teams can increase customer-satisfaction scores because bots resolve simple queries quickly, allowing humans to focus on empathy-driven tasks. Still, organizations face short-term redundancy costs and must navigate labor-code rules when rebalancing staffing levels. The National Privacy Commission issues AI guidelines, clarifying accountability for automated decisions and forcing providers to embed audit trails in new workflows. Success in this transition will determine whether legacy contact-center vendors evolve into high-margin, AI-enabled service orchestrators.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Function / Capability: Digital Services Drive Transformation Beyond Traditional BPM

Business Process Management captured 61.27% of the Philippines' Global Capability Centers market share in 2024, driven by its depth in finance, accounting, and customer service. Information Technology and Digital Services, however, is projected to post a 10.27% CAGR through 2030, reflecting enterprise demand for cloud engineering, cybersecurity, and analytics. The Philippines' Global Capability Centers market size for digital services is projected to expand as multinational firms relocate product engineering and data science teams from higher-cost geographies. Investments in ISO 27001 and SOC 2 compliance amplify trust in handling regulated data.

Engineering and R&D hubs add software prototyping and automation development, increasing the complexity of local work profiles. Knowledge Process Outsourcing, covering legal research and market intelligence, benefits from the same talent pipeline, enriching the Philippines' Global Capability Centers industry with domain-specific expertise. Multinationals cite the availability of STEM graduates and a maturing vendor ecosystem as reasons to deepen technology footprints, signaling sustained upside for non-voice segments.

By Engagement Model: Hybrid Structures Gain Traction for Flexibility

Captive centers accounted for 59.41% of the Philippines' Global Capability Centers market share in 2024, as financial institutions prefer direct governance over sensitive data flows. Yet hybrid Build-Operate-Transfer models are growing at 10.42% CAGR, blending rapid entry with eventual ownership transfer. The Philippines' Global Capability Centers market size within hybrid structures benefits from lower upfront capital and scalable workforce options, which are attractive to high-growth software firms.

Traditional outsource-only contracts decline as buyers seek tighter integration between onshore and offshore teams. Regulatory bodies such as the Bangko Sentral ng Pilipinas refine guidelines to accommodate layered governance, reassuring risk-averse sectors. The result is a portfolio approach: core IP in captives, specialized spikes managed by partners, all within a single Philippine footprint.

By Organization Size: SMEs Accelerate Adoption via Cloud Platforms

Large enterprises retained 75.47% of the Philippines Global Capability Centers market share in 2024, leveraging scale for end-to-end shared-service setups. Still, SMEs are projected to post an 11.23% growth trajectory, enabled by cloud-based delivery that removes the historical minimum-seat hurdle. The Philippines' Global Capability Centers market size among SMEs is increasing as SaaS solutions deliver plug-and-play finance, HR, and digital marketing support, eliminating the need for heavy capital expenditure.

PEZA’s incentive mix and flexible leasing models further democratize access. Smaller firms typically start with a single process but often expand rapidly once proof of concept is established. This influx diversifies sector exposure and stimulates provincial city uptake, fostering inclusive industry expansion beyond conglomerate dominance.

By Industry Vertical: BFSI Outpaces as Risk and Compliance Intensify

Telecom and IT held a 33.56% share of the Philippines Global Capability Centers market in 2024, reflecting early-mover advantages and technology alignment. Banking, financial services, and insurance, however, are expected to register a 10.21% CAGR to 2030, as tighter global regulations prompt institutions to consolidate risk analytics and Anti-Money-Laundering operations in compliant, cost-effective hubs. The Philippines' Global Capability Centers market size serving the BFSI sector, therefore, expands at a faster rate than the overall market growth.

The healthcare and life sciences industries employ the same rigorous standards for clinical data management and pharmacovigilance tasks, whereas the manufacturing and automotive industries focus on supply chain analytics and quality assurance. The widening vertical mix signals the Philippines Global Capability Centers industry’s transition from generic support to sector-specific solutions, raising entry barriers for new locations that lack comparable breadth.

Geography Analysis

Metro Manila hosts roughly 65% of employment, anchored by Bonifacio Global City, Makati CBD, and Ortigas. These districts combine Tier-III data centers, international schools, and proximity to regulators, making them the default choice for new entrants. The Philippines' Global Capability Centers market size, concentrated in Metro Manila, benefits from mature infrastructure but faces rising costs and talent competition.

Central Visayas, led by Cebu City, emerges as the top provincial alternative, delivering real estate savings of 40-50% compared to the capital region. EY Global Delivery Services scaled a 500-person site in Cebu in 2024 for audit-support functions, demonstrating the depth of local universities and the availability of English-fluent graduates. The resulting momentum lifts the Philippines' Global Capability Centers' market share in provincial locations.

Mindanao’s Davao and Luzon’s Clark Freeport Zone round out the geographic diversification playbook. Davao's city government aligns incentives with broadband rollouts, targeting niche sectors like agritech analytics. Clark leverages its proximity to Manila and access to international airports, attracting firms that require dual-site business continuity planning. These shifts spread economic benefit across the archipelago and ease Metro-centric saturation.

Competitive Landscape

The Philippines Global Capability Centers market exhibits moderate concentration, with financial majors JPMorgan Chase and Citigroup overseeing the largest captive centers, which collectively employ over 27,000 employees. Technology and consulting leaders, such as Accenture, PwC, and EY, operate multidisciplinary hubs ranging from AI labs to cybersecurity command centers. Their emphasis on GenAI accelerates capability depth and lifts the overall value proposition of the Philippines Global Capability Centers market.

Competition is increasingly shifting towards specialization over pure headcount. Shell Business Operations Manila differentiates through energy-sector digital twins, while HSBC Global Service Centre focuses on regulatory reporting and sanctions screening. New entrants target white-space niches, such as renewable-energy analytics or fintech compliance, raising competitive intensity while broadening service diversity.

To sustain edge, providers pursue ISO 27001, SOC 2 Type II, and industry-specific certifications that reassure risk-sensitive clients. Continuous upskilling programs, often in partnership with the Department of Science and Technology, feed a pipeline of AI engineers and data stewards that underpin premium services. Market observers, therefore, rate the Philippines Global Capability Centers market as strategically poised but vigilant against global alternatives.

Philippines Global Capability Centers Industry Leaders

Accenture Inc.

JPMorgan Chase and Co. Philippine Global Service Center

HSBC Global Service Centre Philippines Inc.

Citigroup Global Markets Asia Service Center

Chevron Holdings Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: PEZA announced the approval of PHP 87.5 billion (USD 1.52 billion) in investment pledges for IT-BPM and Global Capability Center (GCC) projects during the first nine months of 2025, representing a 65% increase compared to the same period in 2024. The approvals included 23 new Global Capability Center registrations and 47 expansion projects from existing operators across Metro Manila, Cebu, and Clark PEZA.

- September 2025: JPMorgan Chase completed the occupancy of its second tower in Uptown Bonifacio Global City, adding 70,000 sqm, including office space, to support its expanded workforce of 20,000 employees. The facility incorporates advanced AI-powered operations centers and cybersecurity command facilities serving the bank’s global operations JPMorgan Chase.

- August 2025: The Department of Finance released the final Implementing Rules and Regulations for the CREATE MORE Act, clarifying enhanced fiscal incentives for Global Capability Center investments, including extended income tax holidays and duty-free importation of capital equipment. The IRR provides specific guidelines for hybrid Build-Operate-Transfer arrangements and provincial digital city investments, as per the Department of Finance, Philippines.

- July 2025: Accenture Philippines announced a USD 120 million investment to establish three GenAI Centers of Excellence in Manila, Cebu, and Davao, targeting 3,500 new hires specializing in large language model development, prompt engineering, and AI-augmented business process design. The centers will serve clients across financial services, healthcare, and manufacturing sectors in Accenture Philippines.

Philippines Global Capability Centers Market Report Scope

The scope of the global capability center study for the market segmentation by the Function/Capability for (i) Information Technology (IT) and Digital Services segment is limited to Software Development, Cloud and Infrastructure Management, Cybersecurity, Data Analytics and AI/ML; (ii) Engineering / ER&D segment is limited to Product Design and Testing, Embedded Systems, Digital Twin / Simulation; (iii) Business Process Management (BPM) segment is limited to Finance and Accounting, HR, Payroll and Talent Management, Procurement, Customer Service; and (iv)Knowledge Process Outsourcing (KPO) segment is limited to Market Research and Insights, Risk and Compliance, Legal and Regulatory Support, Strategy and Consulting Support. Similarly, for segmentation by the Engagement Model, scope for (i) Hybrid Build-Operate-Transfer (BOT) is limited to Joint Venture / Strategic Partnership and Virtual Captive Model. The rest of the segment scope is as specified for the listed segment.

| Information Technology (IT) and Digital Services |

| Engineering / ER&D |

| Business Process Management (BPM) |

| Knowledge Process Outsourcing (KPO) |

| Captive (Self-Build)/ In-house |

| Build-Operate-Transfer (BOT) |

| Hybrid Build-Operate-Transfer (BOT) |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| Banking, Financial Services, and Insurance (BFSI) |

| Telecom and IT |

| Healthcare and Life Sciences |

| Manufacturing, Automotive and Industrial |

| Retail and Consumer Goods |

| Other Industry Verticals |

| By Function / Capability | Information Technology (IT) and Digital Services |

| Engineering / ER&D | |

| Business Process Management (BPM) | |

| Knowledge Process Outsourcing (KPO) | |

| By Engagement Model | Captive (Self-Build)/ In-house |

| Build-Operate-Transfer (BOT) | |

| Hybrid Build-Operate-Transfer (BOT) | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises (SMEs) | |

| By Industry Vertical | Banking, Financial Services, and Insurance (BFSI) |

| Telecom and IT | |

| Healthcare and Life Sciences | |

| Manufacturing, Automotive and Industrial | |

| Retail and Consumer Goods | |

| Other Industry Verticals |

Key Questions Answered in the Report

What is the projected value of the Philippines Global Capability Centers market by 2030?

The market is set to reach USD 55.59 billion by 2030, reflecting a 9.62% CAGR from 2025.

Which functional area is expanding fastest within Philippine Global Capability Centers?

Information Technology and Digital Services is the fastest, advancing at a 10.27% CAGR through 2030.

Why are hybrid Build-Operate-Transfer models gaining popularity?

They provide rapid entry, scalability, and eventual ownership transfer, supporting a 10.42% CAGR in the engagement-model segment.

How significant is provincial expansion to the Global Capability Center landscape?

Provincial hubs, such as Cebu, Davao, and Clark, now capture a rising share of employment, offering operating costs 20-30% lower than those in Metro Manila.

What is the biggest risk facing voice-centric Global Capability Center operations?

Up to 40% of routine customer-service roles are expected to be susceptible to GenAI automation within three years, putting pressure on firms to reskill their workforces.

Which industry vertical is predicted to grow fastest in Global Capability Center demand?

Banking, financial services, and insurance lead the way with a forecasted 10.21% CAGR, driven by heightened digital risk and compliance requirements.

Page last updated on: