Philippines Customer Data Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

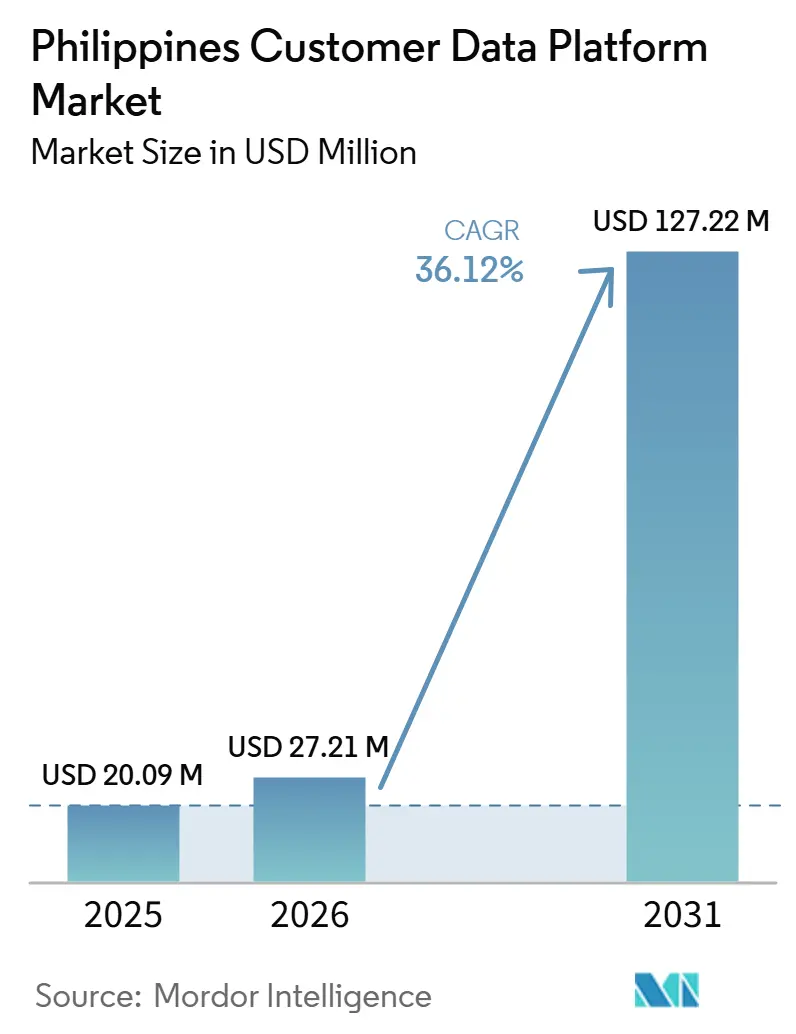

| Base Year Market Size (2025) | USD 20.09 Million |

| Market Size (2026) | USD 27.21 Million |

| Market Size (2031) | USD 127.22 Million |

| Growth Rate (2026 - 2031) | 36.12% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Philippines Customer Data Platform Market Analysis by Mordor Intelligence

The Philippines customer data platform market size is projected to expand from USD 2009 million in 2025 and USD 27.21 million in 2026 to USD 127.22 million by 2031, registering a CAGR of 36.12% between 2026 to 2031. The Philippines customer data platform market is being lifted by a faster shift toward first-party data, as brands put more effort into owned customer records, consented engagement, and measurable activation. Adoption is also rising because enterprises are moving into cloud-native customer experience stacks without spending years on older on-premises marketing systems first. Real-time personalization is becoming a practical buying need rather than a future option, especially in retail, telecom, banking, and digital services, where customer interactions now happen across multiple channels at the same time. Regulated sectors are supporting demand for hybrid architectures because they want cloud-scale activation while still keeping tighter control over sensitive customer and financial records. Talent shortages and uneven integration readiness still slow some programs, which is why part of the Philippines customer data platform market remains in staged rollout rather than full activation.

Key Report Takeaways

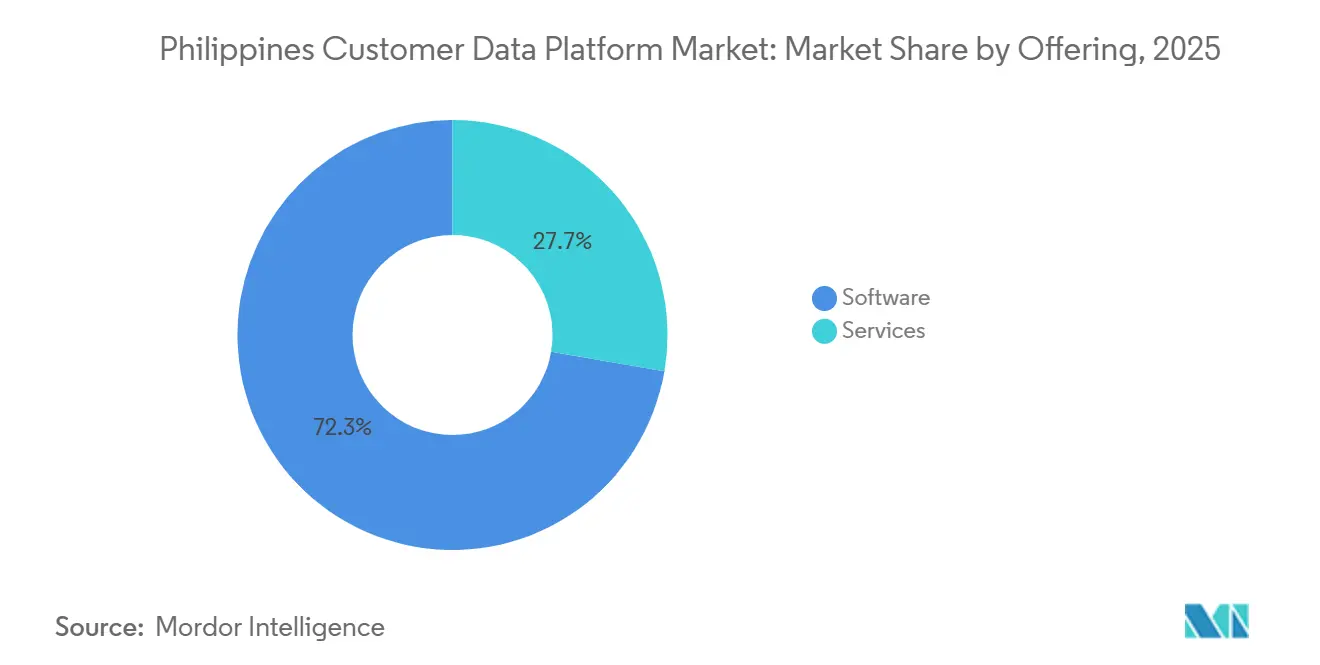

- By offering, software held 72.31% share of the Philippines customer data platform market size in 2025, while services are projected to expand at a 36.87% CAGR through 2031.

- By deployment mode, cloud accounted for 68.42% of the Philippines customer data platform market size in 2025, while hybrid is projected to grow at a 37.28% CAGR through 2031.

- By organization size, Large Enterprises held 68.27% of the Philippines customer data platform market share in 2025, while Small and Medium Enterprises are projected to expand at a 37.34% CAGR through 2031.

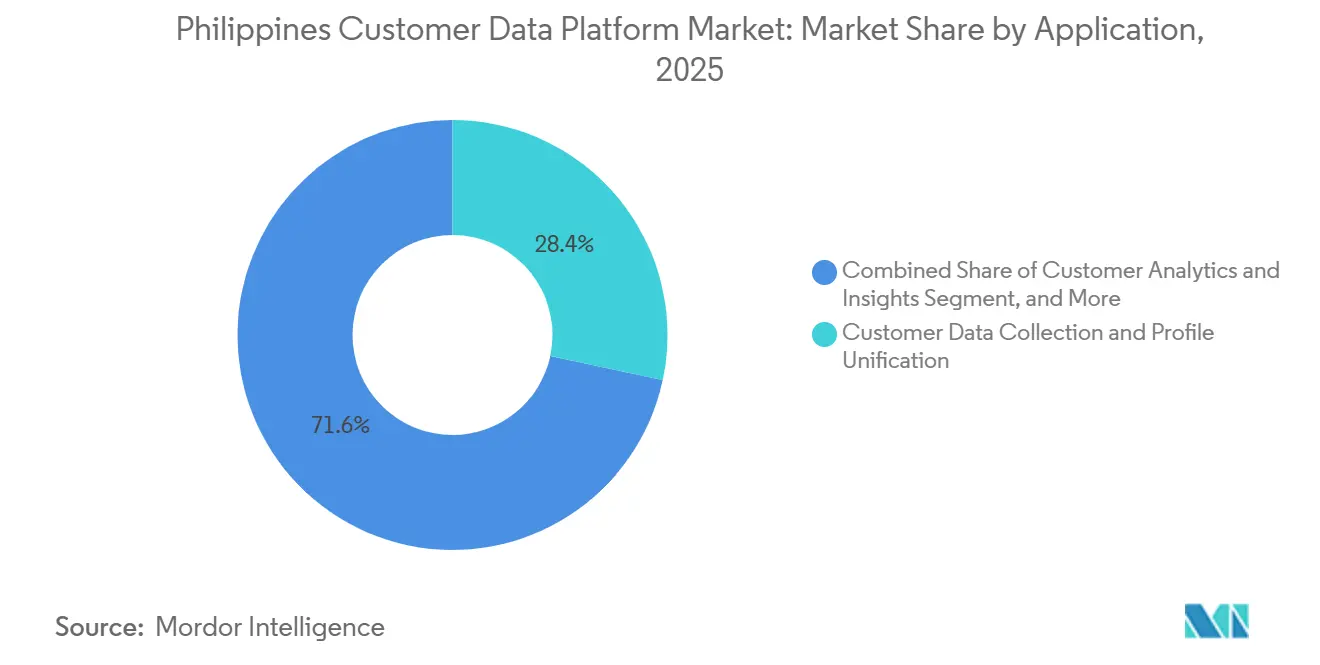

- By application, customer data collection and profile unification accounted for 28.36% of the market in 2025, while audience segmentation and personalization are projected to grow at a 37.54% CAGR through 2031.

- By end-user industry, retail and e-commerce held 31.85% of the market in 2025, while healthcare and life sciences are projected to expand at a 37.81% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Philippines Customer Data Platform Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising First-Party Data Urgency After Third-Party Cookie Deprecation | +8.2% | Global, amplified in the Philippines under stricter privacy expectations | Short term (≤ 2 years) |

| Fast-Growing Omnichannel Retail and E-Commerce Activation Needs | +7.0% | Philippines and broader Southeast Asia | Short term (≤ 2 years) |

| Rapid Adoption of Cloud-Native MarTech and Composable Stacks | +6.1% | Asia-Pacific, with strong relevance in Southeast Asia | Medium term (2-4 years) |

| AI-Driven Real-Time Personalization and Next-Best-Action Use Cases | +5.5% | Global, with strong Asia-Pacific relevance | Medium term (2-4 years) |

| Rise of Super-App, Messaging, and Mobile Wallet Customer Journeys | +4.1% | Philippines, Indonesia, and Southeast Asia | Short term (≤ 2 years) |

| Demand for Local Language and Channel-Aware Customer Data Orchestration | +2.9% | Philippines-specific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising First-Party Data Urgency After Third-Party Cookie Deprecation

Privacy changes have already pushed marketers away from borrowed identifiers and toward customer data they collect and govern inside their own channels. Adobe reported in 2024 that 78% of global brands had adopted a customer data platform (CDP) to build a first-party data strategy, which shows how quickly this shift has moved into mainstream budget planning.[1]Adobe, “Adobe Study: Brands Make Progress Weaning Off Third-Party Cookies, Yet Feel Less Prepared Than Ever for a World Without Them,” Adobe Blog, adobe.com That change matters in the Philippines because brands need one system that can connect browsing, shopping, loyalty, and service interactions without depending on fading third-party signals. The Philippines customer data platform market benefits as spending moves toward identity resolution, consent capture, and governed profile unification inside owned media and commerce environments. As confidence in external targeting declines, CDPs move from a campaign support tool into core customer infrastructure. This shift also supports longer platform relationships because the data model, governance rules, and activation logic become harder to replace once they are embedded.

Fast-Growing Omnichannel Retail and E-Commerce Activation Needs

Retail and e-commerce in the Philippines now depend on coordinated engagement across marketplaces, social channels, messaging apps, stores, and loyalty programs. Infobip expanded its omnichannel platform across all 137 SM Supermalls in April 2026, which showed how large retailers are centralizing triggers across Viber, SMS, and email rather than managing each channel in isolation. Lazada Philippines said its generative AI personalization tool tripled its contribution to sales during the June 2025 campaign versus the comparable December 2024 event, which reinforces the commercial value of faster audience and offer decisions.[2]Philstar.com, “Lazada Banks on AI, Product Assortment to Sustain Growth,” Philstar.com, philstar.com That operating model favors a CDP because commerce teams need one profile and one decision layer across every touchpoint. The Philippines customer data platform market, therefore, gains when retailers move beyond campaign reporting and start demanding real-time orchestration during peak events. The same pattern also strengthens demand from brands that sell through both direct and indirect channels, because customer journeys no longer fit inside one system of record.

Rapid Adoption of Cloud-Native MarTech and Composable Stacks

Enterprises are skipping long on-premises buildouts and moving into cloud-native customer experience stacks that can be deployed faster and expanded in phases. Tealium launched its AI Partner Ecosystem in April 2026 with more than 1,300 prebuilt connectors, which showed how vendors are positioning CDPs as live orchestration layers inside wider cloud architectures. Tealium then released Context API in June 2026 to give AI agents and applications governed access to real-time customer context without forcing heavy data duplication. These launches show how fast the architecture is moving toward low-latency activation and more flexible data access. The Philippines customer data platform market benefits from this model because buyers can modernize faster without rebuilding every legacy system at once. It also supports regulated enterprises that want cloud-scale activation while keeping tighter control over how sensitive records are processed.

AI-Driven Real-Time Personalization and Next-Best-Action Use Cases

AI now matters because brands want customer data to trigger immediate action, not just better reporting. Amplitude introduced Agentic AI Analytics in February 2026, which shortened the path from behavioral data to action inside product and growth teams. Finex said Insider's Sirius AI is already being used by brands including Watsons, Cebu Pacific, and Robinsons Bank to generate audience segments and personalization workflows more quickly. This changes the buying case for customer data platforms because marketers can work from unified data without waiting on long manual engineering cycles for every campaign or use case. The Philippines customer data platform market will keep benefiting as early users show that next-best-action, churn prevention, and tailored messaging are easier to scale when data and activation sit in one system. It also raises buyer expectations, because future platform decisions will increasingly favor vendors that combine unification, governance, and decisioning in one operating layer.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Shortage of CDP, Data Engineering, and RevOps Talent | -3.1% | Global, with stronger pressure in the Philippines | Medium term (2-4 years) |

| Fragmented Legacy Data and Weak System Integration Readiness | -2.5% | Philippines and emerging Southeast Asian markets | Long term (≥ 4 years) |

| Data Privacy Compliance Complexity and Consent Governance Burden | -1.8% | Philippines-specific | Medium term (2-4 years) |

| Budget Sensitivity Among Mid-Market Buyers and Long Payback Cycles | -1.2% | Philippines SME market | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shortage of CDP, Data Engineering, and RevOps Talent

Demand for customer data platform skills is rising faster than local supply, which leaves many buyers with the platform but not the operating team needed to use it well. Finex described a market where enterprises have invested heavily in data infrastructure but still struggle to activate personalization and loyalty programs at scale. Insider and Hungry Workhorse launched customer data platform champs in August 2025 to train CTOs, CMOs, and CRM leaders in advanced operations, generative AI, and multi-channel journey design. Salesforce also said in November 2025 that it would train 12,000 Filipinos in CRM and AI skills over 5 years, which underlines how large the capability gap has become. Until staffing improves, some implementations will remain partly activated even after the underlying software goes live. This keeps the Philippines customer data platform market growing, but it stretches time to value and favors vendors that offer stronger onboarding, managed services, and enablement.

Fragmented Legacy Data and Weak System Integration Readiness

Many deployments slow down because customer data still sits across separate systems that were built or purchased at different times. CPA Australia found that 62% of Filipino small businesses received more than 10% of revenue from online sales in 2025, which suggests many potential users are still operating mixed physical and digital models that do not generate clean, unified data flows by default. Banks face a similar issue because payment, customer, and service data often remain distributed across disconnected platforms, which complicates any attempt to build one reliable financial profile. The Philippines customer data platform market faces longer implementation cycles when connectors have to be customized for local payment rails, messaging channels, and older core systems. Vendors that reduce this integration burden will have a clear advantage in both enterprise and mid-market accounts. The same challenge also explains why buyers increasingly value prebuilt connectors, templated data models, and phased rollout plans instead of large one-step transformations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Software Anchored Revenue While Services Drove Growth

Software held 72.31% of the Philippines Customer Data Platform market in 2025, reflecting the weight of subscription-based platform licensing across enterprise accounts. The segment led because enterprises preferred packaged suites that could unify customer data and connect with broader experience, analytics, and engagement systems. Larger buyers also favored vendors with existing regional delivery models and proven activation tools, which reduced deployment risk at the point of purchase. Software demand also benefited from the need to connect marketing, commerce, analytics, and service data inside one governed operating environment. Amplitude's Agentic AI Analytics launch in February 2026 showed how software vendors are widening platform value beyond storage and reporting into faster action from behavioral data.[3]Amplitude, “Amplitude Introduces Agentic AI Analytics for the Next Era of Product Experiences,” Amplitude Investor Relations, amplitude.com

Services are projected to expand at a 36.87% CAGR through 2031, making them the fastest-growing subsegment in the Philippines customer data platform market. That growth reflects rising demand for implementation support, identity stitching, consent design, use-case rollout, and post-deployment optimization after the initial license purchase. Many companies that bought platforms earlier are now spending more on data quality repair, workflow tuning, and activation support than on additional licenses. In the Philippines customer data platform industry, this pattern shows that software selection is only the first stage of value creation. Service partners benefit as enterprises shift spending from platform acquisition to improving adoption and measurable outcomes inside existing accounts.

By Deployment Mode: Cloud Led Adoption While Hybrid Gained in Regulated Accounts

Cloud deployment held 68.42% of the Philippines customer data platform market in 2025. The segment led because cloud CDPs shorten implementation time, simplify upgrades, and reduce the infrastructure burden on internal teams. Regional cloud infrastructure also gives Philippine enterprises workable latency for many real-time use cases without requiring local hardware ownership. Cloud models fit buyers who want subscription pricing, easier vendor support, and simpler access for distributed teams. On-premises deployments still matter for selected government and BFSI environments where internal control and legacy dependencies remain strong.

Hybrid deployment is projected to grow at a 37.28% CAGR through 2031, making it the fastest-rising mode in the Philippines customer data platform market. This mix fits enterprises that want cloud-scale activation while keeping sensitive processing closer to internal systems. It also reduces the disruption of moving every data asset at once, which matters in heavily governed environments. In the Philippines customer data platform industry, hybrid models let buyers modernize in phases instead of pursuing a risky full-stack replacement. Vendors that balance governance, latency, and activation speed should capture more regulated demand, a direction reflected in Tealium's 2026 product push around AI connectivity and governed real-time context.

By Organization Size: Large Enterprises Dominated While SMEs Accelerated

Large Enterprises held 68.27% of the Philippines customer data platform market share in 2025. Early adoption concentrated among banks, telecom operators, and large retailers with bigger budgets, wider data estates, and stronger internal technology teams. These buyers also had a greater urgency to replace third-party targeting with owned customer identity and governed activation. BPI used a 360-degree customer view that combined demographic and transactional data for churn prediction and product pre-qualification. RCBC also highlighted its enterprise data platform and AI roadmap in 2026, which showed how large institutions are linking data foundations to fraud detection and personalized journeys.

Small and Medium Enterprises are projected to expand at a 37.34% CAGR through 2031, making them the fastest-growing size segment in the Philippines customer data platform market. Affordable platforms, lighter deployment models, and stronger local outreach are opening the category to firms that once viewed CDPs as enterprise-only tools. Salesforce's local expansion and Tagalog-language AI support showed that vendors now see MSMEs as a real growth lane rather than a distant opportunity. Even so, SMEs remain more exposed to weak integration, thinner skills, and tighter payback requirements than large accounts. The segment should keep growing, but value realization will depend on whether smaller firms clean up core sales, marketing, and finance data before layering advanced activation.

By Application: Unification Held the Base While Personalization Expanded Fastest

Customer Data Collection and Profile Unification accounted for 28.36% of the Philippines customer data platform market size in 2025. That position reflects its role as the base layer for every other CDP use case, since buyers usually need one trusted profile before they can improve segmentation, orchestration, analytics, or consent governance. Inquiro showed the scale of this opportunity with more than 94 million unique profiles and over 400 cohorts inside its data environment.[4]Philstar.com, “Philippines Firms Tap New Tech to Boost Customer Engagement,” Philstar.com, philstar.com This foundational demand keeps data collection and profile building central even as the category matures. Consent and preference management also moved higher on buyer agendas as profiling and automated processing came under closer scrutiny.

Audience Segmentation and Personalization is projected to grow at a 37.54% CAGR through 2031, making it the fastest-growing application in the Philippines customer data platform market. The reason is simple, profile unification without downstream activation rarely produces a visible commercial return. L'Oréal Philippines used unified customer data to support AI-powered skin and hair analysis, product recommendations, and personalized messaging across channels. As buyers mature, more budgets should shift from basic data assembly to real-time decisioning, journey orchestration, and governed personalization. This makes the application mix likely to move from foundational data work toward measurable revenue and retention use cases over the forecast period.

By End-User Industry: Retail Led the Base While Healthcare Shaped the Next Wave

Retail and e-commerce held 31.85% of the Philippines Customer Data Platform market size in 2025. The segment led because brands now manage customer journeys across marketplaces, social channels, owned apps, loyalty programs, and physical stores at the same time. That operating model creates fragmentation unless one platform can reconcile identities and trigger actions across every touchpoint. National Book Store's June 2026 deployment of enterprise OMS and WMS across more than 260 stores and all online channels showed how operational unification can become a precursor to customer data unification. BFSI remained the most important secondary vertical because banks use unified data for cross-sell, churn prevention, and service personalization while managing strict governance needs.

Healthcare and Life Sciences is projected to expand at a 37.81% CAGR through 2031, making it the fastest-growing end-user segment in the Philippines customer data platform market. Digital health mandates and interoperability work changed the pace of demand in this segment by making patient data exchange a near-term operational requirement. PhilHealth's move away from eKonsulta and toward interoperable EMR systems raised the need for connected patient data environments. The June 2026 FHIR Connectathon at the University of the Philippines Manila then showed live health data exchange across EMR systems using the Philippine Core FHIR Implementation Guide. That sequence makes healthcare one of the clearest expansion paths for the Philippines customer data platform market through 2031.

Geography Analysis

The Philippines customer data platform market is projected to expand at a 36.12% CAGR from 2026 to 2031, which places it among the faster-growing opportunities in Asia-Pacific. That pace reflects a mobile-first consumer base, dense engagement across social, commerce, and messaging environments, and growing enterprise pressure to unify customer records. Adoption is also moving quickly because many companies are building cloud-native customer experience stacks without passing through a long on-premises transition first. Global vendors and service partners have responded by deepening local coverage, partner ties, and vertical outreach in banking, retail, telecom, and healthcare.

The market stood at USD 27.22 million in 2026, and a large share of active enterprise demand remains centered in Metro Manila. Makati, Bonifacio Global City, and Ortigas continue to anchor deployments because they house corporate headquarters, shared service operations, and regional technology teams. Even so, the next wave of use cases is extending beyond the capital as brands build mobile-led journeys for customers who interact through SMS, wallets, marketplaces, and chat apps. This makes phone-based identity resolution more important than browser-based tracking in many campaigns. It also means that brands trying to scale nationally must manage uneven data quality between dense urban markets and provincial areas with thinner digital footprints.

The Philippines customer data platform market will reach USD 127.22 million by 2031 if regulated sectors move from pilot programs into broader activation. Retail and e-commerce will keep pulling demand, but healthcare and BFSI may contribute more strongly as interoperability and consent requirements become more formal. Capacity constraints in data infrastructure and the cost of connecting older systems can still slow real-time activation in some accounts. Vendors that support local channels, flexible deployment, and governance-heavy use cases should be best placed to capture the next round of spending.

Competitive Landscape

The Philippines customer data platform market remains moderately concentrated in large enterprise accounts, while mid-market and SME demand is more open. Global platforms such as Adobe Experience Platform, Tealium, and Twilio Segment are often evaluated because customer data platform buying is frequently tied to wider experience, analytics, or communications decisions. Their position is strengthened by deep connector libraries, enterprise support models, and mature activation capabilities. The category is still contestable because language needs, sector rules, and local channel integration create room for newer challengers.

Tealium reinforced its position in 2026 by launching its AI Partner Ecosystem with more than 1,300 prebuilt connectors. It followed that move in June 2026 with Context API, which gives AI agents and applications governed access to real-time customer context. Bloomreach also expanded its reach in June 2026 by joining Databricks CustomerLake as a launch partner for agentic customer data platform workflows.[5]Bloomreach, “Bloomreach Deepens Partnership With Databricks, Extending AI Personalization Across Email, Web, and More Through New CustomerLake Integration,” Bloomreach News, bloomreach.com Amplitude was added to the pressure in February 2026 with Agentic AI Analytics, which moved product teams closer to action from behavioral data. These moves show that competition is shifting from basic unification toward AI-ready activation and lower-latency execution.

The strongest white space remains in SME offerings and in regulated verticals such as healthcare and government. InfiniVAN's July 2025 work with the University of the Philippines on LikásGPT showed an early attempt to build customer-facing data tools around 12 Philippine languages and dialects. That kind of localization matters because imported platforms often need adaptation around language, consent workflows, and local channel behavior. Competitive pressure will keep rising as global suites move down-market and local or regional providers build more Philippine-specific solutions.

Philippines Customer Data Platform Industry Leaders

Adobe Inc.

Salesforce, Inc.

Oracle Corporation

SAP SE

Twilio Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Bloomreach announced it is a launch partner for Databricks CustomerLake, a new agentic CDP that connects AI models, customer data, and real-time marketing execution in a single platform without data duplication. The partnership extends Bloomreach's AI personalization suite to warehouse-native architectures, positioning it for enterprise accounts building composable stacks on Databricks.

- June 2026: Tealium launched Context API, expanding its Moments API to add a governed, low-latency context layer over historical warehouse data. The solution enables autonomous AI agents and applications to access real-time behavioral signals from CDPs without moving or duplicating underlying enterprise data assets.

- May 2026: Tealium unveiled AI at the Edge, AI Decisioning, and expanded composable CDP capabilities as new in-platform features, reinforcing its positioning as an enterprise data orchestration layer for AI-powered customer experience applications.

- February 2026: Amplitude introduced a suite of Agentic AI Analytics, including a Global Agent and four specialized agents, along with Model Context Protocol updates connecting behavioral data to AI tools from Anthropic, OpenAI, and GitHub. The product advancement narrows the gap between product analytics and CDP use cases for Philippine enterprise software teams.

Philippines Customer Data Platform Market Report Scope

The Philippines customer data platform market comprises platforms and services that enable organizations to collect, integrate, and manage customer data from multiple sources into unified, centralized profiles. These solutions support identity resolution, real-time data integration, customer segmentation, personalization, and analytics, helping enterprises in the Philippines deliver consistent omnichannel customer experiences. The market includes CDP solutions used across industries such as retail, banking, and telecom, where businesses require scalable martech capabilities to improve customer engagement, comply with evolving data privacy regulations, and support AI-powered personalization.

The Philippines Customer Data Platform Market Report is Segmented by Offering (Software, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid) Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Customer Data Collection and Profile Unification, Audience Segmentation and Personalization, Marketing Campaign and Customer Journey Orchestration, Customer Analytics and Insights, Consent and Preference Management, and Other Applications), and End-User Industry (Retail and E-Commerce, Banking, Financial Services, and Insurance (BFSI), Healthcare and Life Sciences, IT and Telecom, Media and Entertainment, Industrial Manufacturing, Government and Public Administrationm and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization |

| Marketing Campaign and Customer Journey Orchestration |

| Customer Analytics and Insights |

| Consent and Preference Management |

| Other Applications |

| Retail and E-Commerce |

| Banking, Financial Services, and Insurance (BFSI) |

| Healthcare and Life Sciences |

| IT and Telecom |

| Media and Entertainment |

| Industrial Manufacturing |

| Government and Public Administration |

| Other End-User Industries |

| By Offering | Software |

| Services | |

| By Deployment Mode | Cloud |

| On-Premises | |

| Hybrid | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Application | Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization | |

| Marketing Campaign and Customer Journey Orchestration | |

| Customer Analytics and Insights | |

| Consent and Preference Management | |

| Other Applications | |

| By End-User Industry | Retail and E-Commerce |

| Banking, Financial Services, and Insurance (BFSI) | |

| Healthcare and Life Sciences | |

| IT and Telecom | |

| Media and Entertainment | |

| Industrial Manufacturing | |

| Government and Public Administration | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the 2026 size of the Philippines customer data platform market?

The Philippines customer data platform market stood at USD 20.09 million in 2025, reached USD 27.21 million in 2026 and is forecast to reach USD 127.22 million by 2031 at a 36.12% CAGR.

Which offering led revenue in the Philippines customer data platform space in 2025?

Software led with a 72.31% share in 2025, while services are projected to grow faster at a 36.87% CAGR through 2031.

Why are retailers adopting CDPs so quickly in the Philippines?

Retailers now manage marketplaces, social commerce, apps, loyalty programs, and stores together, which makes one unified customer profile and activation layer far more valuable.

Which deployment model is growing fastest through 2031?

Hybrid deployment is the fastest-growing model at a 37.28% CAGR because regulated buyers want cloud agility with tighter control over sensitive data handling.

Why is healthcare becoming a strong growth area for CDP vendors?

Healthcare and Life Sciences is projected to grow at 37.81% CAGR as interoperability efforts and patient data exchange needs push providers toward more connected data environments.

What is changing competition among CDP vendors in the Philippines?

Competition is moving from basic data unification toward AI-ready activation, governed real-time context, local language support, and better integration with Philippine-specific channels.

Page last updated on: