Philippines Corrugated Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

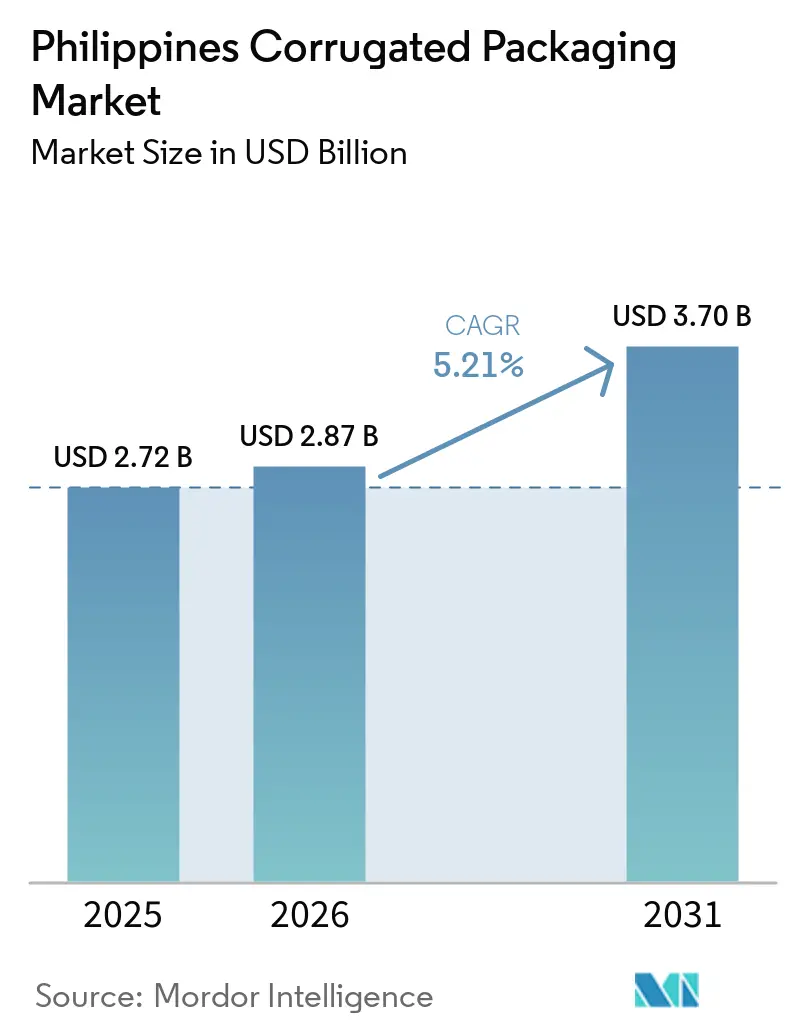

| Base Year Market Size (2025) | USD 2.72 Billion |

| Market Size (2026) | USD 2.87 Billion |

| Market Size (2031) | USD 3.70 Billion |

| Growth Rate (2026 - 2031) | 5.21% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Philippines Corrugated Packaging Market Analysis by Mordor Intelligence

The Philippines corrugated packaging market size is projected to expand from USD 2.72 billion in 2025 and USD 2.87 billion in 2026 to USD 3.7 billion by 2031, registering a CAGR of 5.21% between 2026 to 2031. Robust parcel flows from Lazada, Shopee, and TikTok Shop, rising excise‐tax pressure on single-use plastics, and the rapid build-out of cold-chain infrastructure are reinforcing demand for recyclable ship-ready boxes. Local mills are scaling recycled-linerboard capacity to hedge against imported virgin-pulp price swings, while converters are investing in digital presses to meet short-run orders from small and medium enterprises competing online. Upcoming deep-water ports in Cebu and Mindoro promise shorter transit times that will favor lighter fluting profiles and moisture-resistant coatings. At the same time, energy-efficient corrugators and water-based inks are gaining appeal as manufacturers seek to cut operating expenses amid electricity-tariff escalation.

Key Report Takeaways

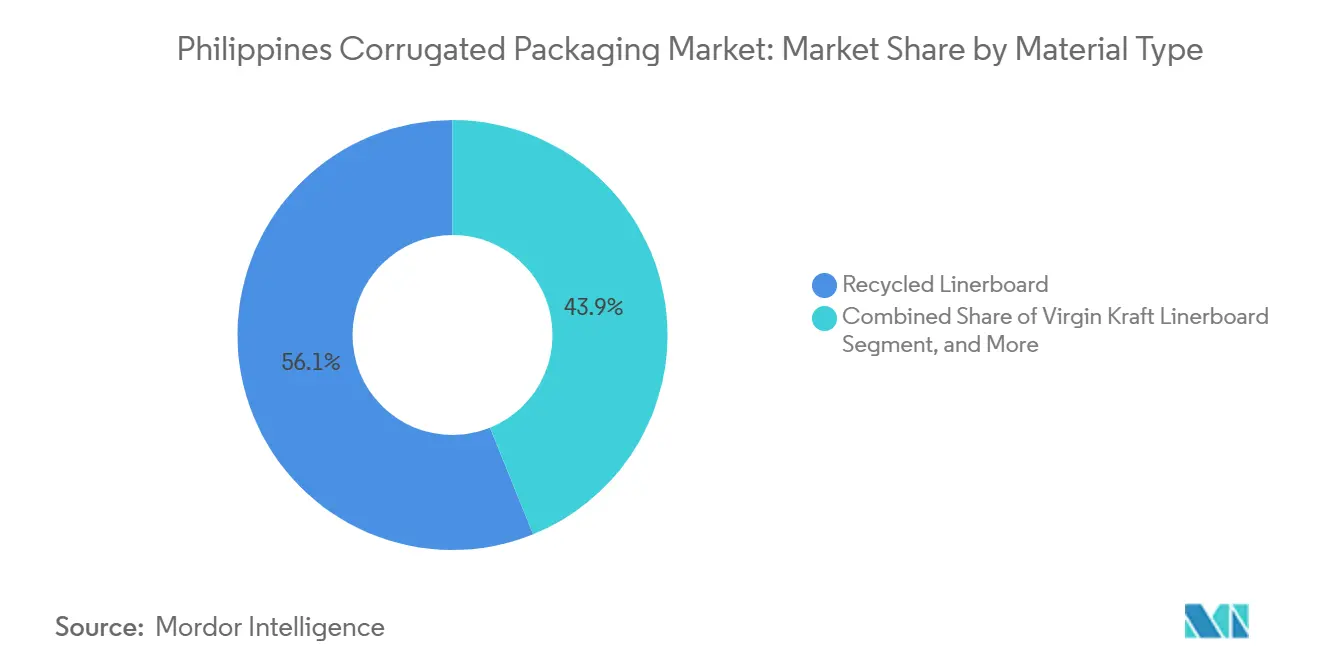

- By material type, the recycled linerboard segment captured 56.12% of the Philippines corrugated packaging market share in 2025.

- By flute type, the Philippines corrugated packaging market size for f flute is projected to grow at an 6.89% CAGR through 2031.

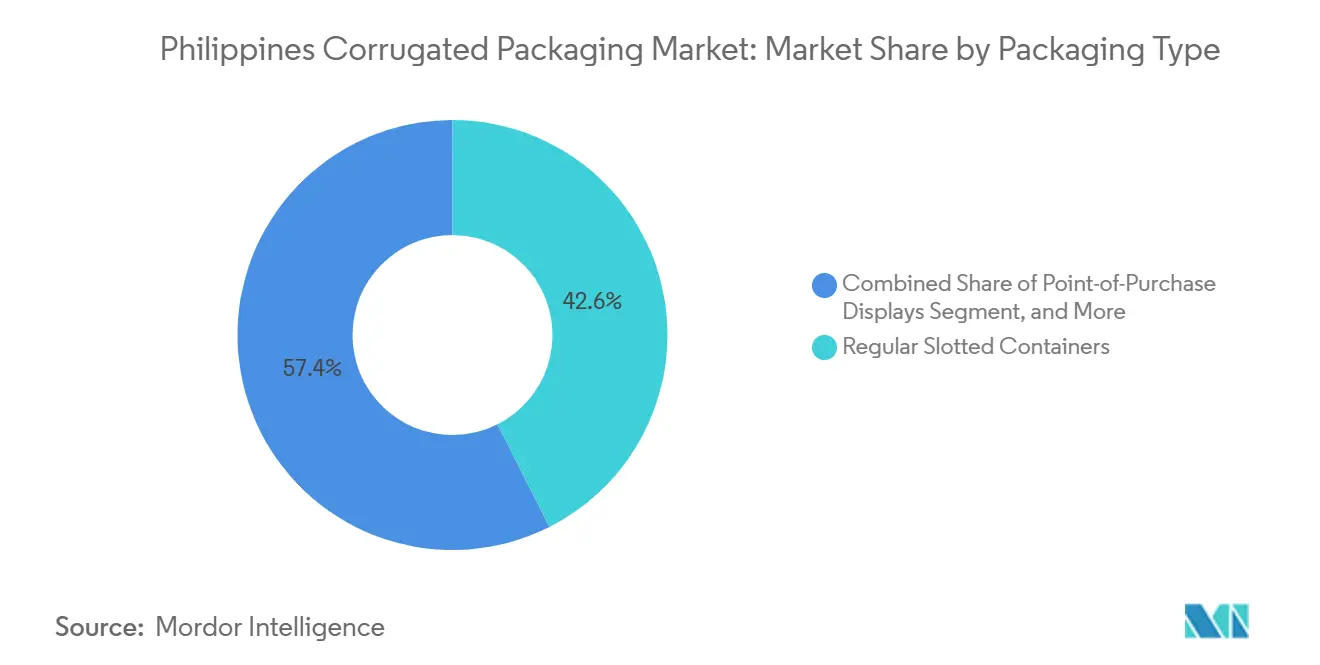

- By packaging type, the regular slotted containers segment captured 42.56% of the Philippines corrugated packaging market share in 2025.

- By wall type, the Philippines corrugated packaging market size for triple-wall is projected to grow at an 7.54% CAGR through 2031.

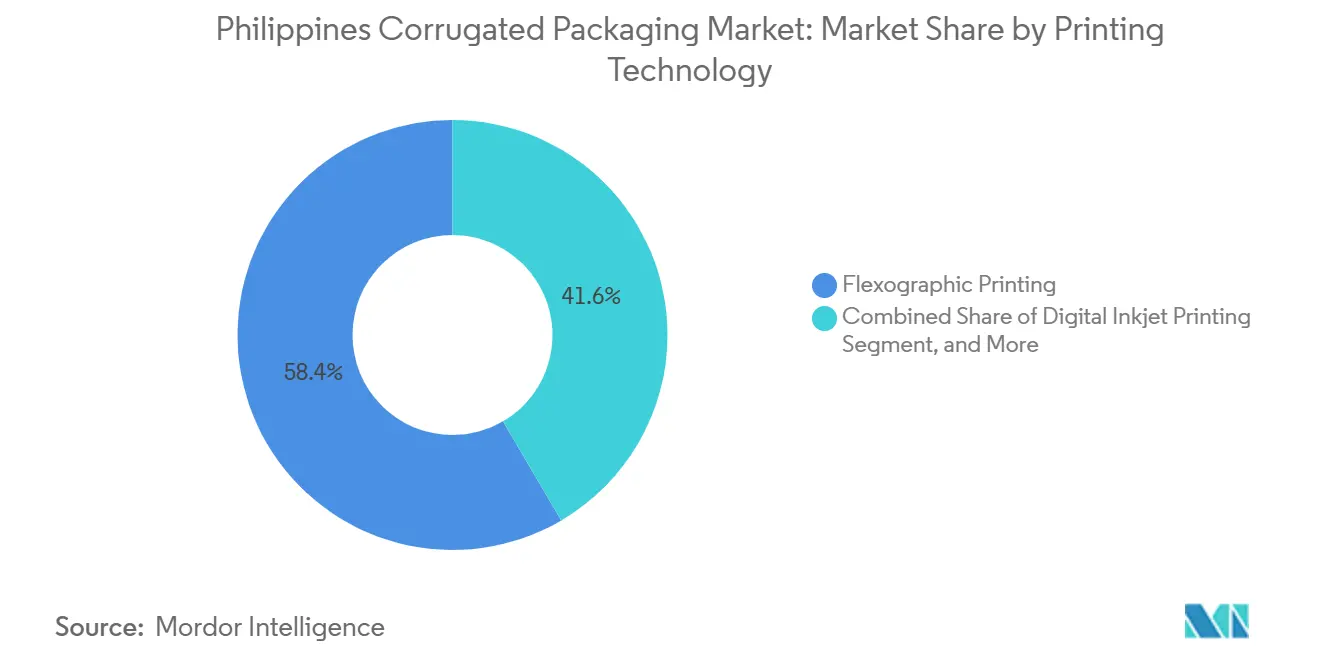

- By printing technology, the flexographic printing segment captured 58.43% of the Philippines corrugated packaging market share in 2025.

- By end-user industry, the Philippines corrugated packaging market size for e-commerce fulfillment centers is projected to grow at an 7.43% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Philippines Corrugated Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce Growth Accelerating Parcel Volumes | +1.8% | National, centered in Metro Manila, Cebu, Davao | Short term (≤ 2 years) |

| Government Restrictions on Single-Use Plastics Favoring Paper-Based Alternatives | +1.5% | National, earliest roll-out in Metro Manila and 489 LGUs | Medium term (2-4 years) |

| Rapid Shift Toward Sustainable and Recycled Fiber Packaging | +1.2% | National, driven by EPR compliance and export mandates | Medium term (2-4 years) |

| Expansion of Processed Food and Beverage Manufacturing Hubs | +1.1% | Luzon and Mindanao | Medium term (2-4 years) |

| Modernization of Inter-Island Logistics Networks Demanding Durable Lightweight Boxes | +0.8% | Visayas and Mindanao inter-island routes | Long term (≥ 4 years) |

| Adoption of Digital Printing Enabling Short-Run Customization for SMEs | +0.6% | National, highest in Metro Manila and Calabarzon | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

E-Commerce Growth Accelerating Parcel Volumes

Same-day and next-day delivery commitments have transformed the distribution landscape, swapping palletized store replenishment for millions of single-item drop-offs. Flash-sale peaks on 11-11 and 12-12 force corrugators to stock seasonal blanks and adjust flute combinations that limit freight weight while preserving edge-crush strength. Multi-modal legs across road, sea, and air magnify humidity exposure, steering merchants toward lighter recycled-fiber liners that still pass stacking tests. Fulfillment centers are standardizing box footprints so automated sorters can scan, label, and manifest parcels with minimal human touch. These shifts collectively raise volumes for the Philippines' corrugated packaging market, especially in Metro Manila’s parcel hubs.[1]Jades Cargo Services Inc., “How E-Commerce Growth Shapes Cargo Needs,” jadescargo.ph

Government Restrictions on Single-Use Plastics Favoring Paper-Based Alternatives

The Extended Producer Responsibility Act requires brand owners to recover 40% of their plastic packaging footprint in 2024, climbing to 80% by 2028, with fines up to USD 5 million for non-compliance. Simultaneously, the Department of Finance is pressing for a USD 100-per-kilogram excise tax on disposable plastic bags, potentially pushing retail bag prices up 94%. Local ordinances from Quezon City’s civic complex ban on plastic disposables to nationwide sachet phase-outs compound the pressure. Brand owners now specify corrugated secondary packs and fiber-based takeout containers that score favorably on recyclability audits. These mandates are nudging procurement managers to lock in extra corrugated volumes, fortifying the growth arc of the Philippines corrugated packaging market.

Rapid Shift Toward Sustainable and Recycled Fiber Packaging

Philippine National Standards PNS 2162 and PNS 2163 classify OCC quality, easing customs clearance and giving mills confidence to import segregated grades at scale. Local recovered-paper consumption rose from 1.5 million tonnes in 2021 to 1.7 million tonnes in 2022, satisfying roughly 85-90% of fiber needs. Brands exporting to the European Union now demand documented recycled-content minimums and chain-of-custody certificates, channeling orders toward mills with closed-loop sourcing. Pilot lines at the Department of Science and Technology’s Green Packaging Laboratory are testing pineapple-leaf-fiber partitions and pectin-coated liners, signaling longer-term potential for high-value bio-based substrates. Together, these forces deepen recycled-linerboard penetration across the Philippines corrugated packaging market.

Expansion of Processed Food and Beverage Manufacturing Hubs

Monde Nissin is investing PHP 7.53 billion (USD 132.5 million) in a new biscuit complex, set to commence operations in 2027. This move is projected to generate annual sales potential exceeding PHP 10 billion (USD 176 million), driving demand for cartons across the Graham and SkyFlakes lines. In 2025, Century Pacific Food allocated PHP 3-4 billion (USD 53-71 million) for the construction of new plants and offices. This investment complements their recent USD 40 million acquisition of a coconut plantation in Mindanao, poised to enhance exports of cartonized beverages and desiccated coconut. Each factory expansion not only boosts production but also necessitates additional corrugating runs for ship-ready trays, inner dividers, and prominently branded folding cartons.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Domestic and Imported Recovered Paper Prices | -1.3% | National, acute for Metro Manila and Calabarzon mills | Short term (≤ 2 years) |

| Port Congestion and Shipping Delays Inflating Lead Times and Costs | -0.9% | Metro Manila, Cebu, Batangas, with spillover to island routes | Short term (≤ 2 years) |

| Escalating Electricity Tariffs Increasing Corrugator Operating Expenses | -0.6% | Nationwide, heavier on Luzon-based energy-intensive mills | Medium term (2-4 years) |

| Substitution Threat From Flexible Plastics and Reusable Plastic Crates | -0.5% | Beverage and fresh-produce corridors nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Domestic and Imported Recovered Paper Prices

Import OCC quotes swung from USD 160 per tonne for European 95/5 to USD 230 per tonne for U.S. DS-OCC in 2024 as U.S. and EU collection rates dipped and Indonesian inspection fees rose. Local converters suffer double exposure: higher landed costs on imported grades and erratic street-price jumps when informal-sector collectors thin out supply. Only 44% of barangays operate functional materials-recovery facilities, with Metro Manila’s coverage at 20%, leaving mills vulnerable to cargo arrival lags and fiber quality downgrades. These shocks crimp gross margins and temper near-term investment appetite in the Philippines corrugated packaging market.

Port Congestion and Shipping Delays Inflating Lead Times and Costs

Truck shortages spiraled as haulers queued with empties lacking depot berths, escalating drayage fees, and stretching inbound linerboard lead times. The customs-broker community has urged carriers to slash empty free-time windows from 90 days to 60 days, but policy traction remains slow. For converters, each extra dwell day inflates working capital and threatens on-time delivery metrics, softening the CAGR trajectory of the Philippines corrugated packaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Recycled Fiber Dominance and Semi-Chemical Growth

Recycled linerboard captured 56.12% of the Philippines corrugated packaging market in 2025, reflecting structural dependence on domestic OCC streams. The Philippines' corrugated packaging market for recycled fiber continues to grow as mills blend locally baled cartons with imported Class A OCC to offset the scarcity of virgin pulp.[2]Lesprom, “United Pulp and Paper Starts Up OCC Line,” lesprom.com Semi-chemical fluting, forecast to grow at a 7.13% CAGR, is gaining favor among inter-island shippers seeking lighter grammages with similar stacking strength, a shift amplified by rising fuel surcharges. Virgin Kraft linerboard remains a niche for moisture-critical produce and pharmaceutical exports, where print gloss and wet-strength ratings justify the premium.

The corrugating medium benefits from United Pulp and Paper’s new 870-TPD OCC line, which filters contaminants using PrimeRotor screens to stabilize runnability. Demand for performance coatings is inching up as the Department of Agriculture spends PHP 3 billion (USD 52.8 million) on 99 hybrid-energy cold storages. Triple-wall blanks with wax or bio-coated liners prevent condensation damage on long reefers, creating a profitable specialty pocket within the broader Philippines corrugated packaging market share landscape. Imported OCC volatility continues to push mills toward captive collection centers that lock in fiber at predictable costs, strengthening margins even as power tariffs rise.

By Flute Type: B Flute Strength and F Flute Upside

B flute secured 41.37% market share in 2025 thanks to its balance of crush resistance, print surface, and compatibility with automatic case packers. Converters run continuous-knife setups that switch from B to C to E flute without major downtime, allowing rapid response to seasonal beverage trays or electronics shrink-wrap replacements. F flute, one-third the caliper of B, is projected for 6.89% CAGR as cosmetics and smart-watch sellers opt for slimmer parcels that fit courier pouches and reduce dimensional weight surcharges.

The Philippines corrugated packaging market size for F flute remains modest today yet offers higher unit margins because of multi-pass digital graphics. C flute maintains a foothold in heavy canned-goods packs, but brand owners eye upstream savings from thinner profiles. E flute doubles as a rigid alternative to folding cartons for pizza and apparel mailers, while A flute’s usage is confined to bulk agro-exports requiring superior cushioning. Thin-profile adoption aligns with port modernization that reduces voyage time, easing moisture-ingress risks and enabling merchants to shift toward lighter makeup.

By Packaging Type: RSC Pre-Eminence and Custom Box Momentum

Regular slotted containers accounted for 42.56% of 2025 shipments, retaining primacy as the universal blank for palletized loads, sea freight liners, and warehouse picking. However, die-cut custom boxes, projected to grow at a 7.43% CAGR, benefit from brand storytelling needs on online storefronts, where unboxing videos influence repeat sales. Automated flatbed plotters let converters sample small batches cost-effectively, catalyzing design iteration for start-ups.

Folding cartons bridge corrugated and SBS boards, supporting premium cosmetics and nutraceuticals that command fine litho-laminated sleeves. Point-of-purchase displays add incremental square-meter demand during seasonal campaigns, while pallet boxes in triple-wall formats are capturing fresh-produce flows into new cold storage facilities. As excise taxes raise plastic bag prices, takeout chains are switching to paper-based clamshells and carrier boxes, expanding ancillary tonnage for the Philippines corrugated packaging market.

By Wall Type: Single-Wall Scale and Triple-Wall Niche

Single-wall accounted for 63.97% of 2025 volumes, balancing material efficiency with stacking integrity for general merchandise. Double-wall options such as BC and BE cater to longer sea legs and cross-docking requirements in progressive distribution centers. Triple-wall’s forecast 7.54% CAGR mirrors the cold-chain boom: hybrid solar-powered storage and reefer vans call for 1-ton pallet boxes that withstand condensation.

The Philippines' corrugated packaging market for triple-wall packaging remains small but is rising as farm-to-port pilots in Northern Samar integrate stronger liners to prevent bulging under negative-pressure cooling. Converters are retrofitting corrugators with separate hot-plates and roll stands to handle heavyweight grammages without warp, positioning them for future apple-and-cherry imports once tariff agreements mature. Single-face rolls, meanwhile, continue as cushioning wraps inside mixed SKU e-commerce cartons.

By Printing Technology: Flexo Scale Meets Digital Agility

Flexographic presses accounted for 58.43% of 2025 revenues, thanks to their water-based ink systems and 300-meter-per-minute run speeds, which serve snack-food shippers at scale. Press retrofits with anilox-sleeve automation have cut makeready waste by up to 20%, partially offsetting electricity hikes. Digital inkjet printing, forecast to grow at a 7.81% CAGR, is unlocking hyper-localized box graphics, think barangay-level festival designs that enhance customer engagement on social feeds.

The Philippines corrugated packaging market share of digital remains below 10%, yet high gross margins lure early adopters. Litho-lamination underpins showroom-grade cartons for luxury confectionery and personal-care SKUs, while screen-printing serves niche metallic or tactile varnish effects. Hybrid workflows combining flexo flood coats with inkjet variable data are emerging, strengthening converters’ responsiveness to SME order cycles.

By End-User Industry: Food Core and E-Commerce Surge

Processed foods delivered 29.13% of shipments in 2025, anchored by biscuit, noodle, and canned-fish players scaling capacity in Luzon and Mindanao. Each new line drives parallel purchases of inner partitions and ship-ready outers. E-commerce fulfillment centers, forecast to grow at a 7.43% CAGR, are the Philippines' corrugated packaging industry’s fastest volume escalator as marketplaces outsource packaging to third-party logistics hubs.

Fresh produce is leveraging waxed triple-wall bins for mango, banana, and coconut exports, especially as new cold storage facilities stabilize temperature swings. Beverage brands need high-gloss litho wraps for shelf differentiation while withstanding condensation rings in humid retail aisles. Electronics OEMs deploy anti-static E flute inserts that mitigate shock during multi-modal hauls across the archipelago. These diverse end uses collectively bolster the growth outlook for the Philippines' corrugated packaging market.

Geography Analysis

Corrugated demand is concentrated in Luzon, which is home to Metro Manila’s ports, Bulacan’s 240,000-tonne mill, and Calabarzon’s export zones. These areas account for nearly half of the accredited cold-storage warehouses in the country. Central Visayas is poised for growth with the anticipated opening of the PHP 16.93 billion (USD 298 million) New Cebu International Container Port in 2028. This port will facilitate simultaneous calls of two 2,000-TEU vessels, alleviating feeder congestion.

The new facility will also reduce sailing times to Mindanao and Samar, enabling brands to use lighter flute calipers without sacrificing box integrity. In the Visayas, produce corridors, spearheaded by Northern Samar’s proposed container-barge terminal, target a daily shipment of 200 TEUs filled with seafood, bananas, and root crops. This necessitates the use of moisture-resistant triple-wall cartons, as highlighted.

Meanwhile, in Mindanao, as Century Pacific enhances its Misamis Occidental plant, demand for cartons in the coconut belt is rising. This upgrade not only boosts carton demand but also creates over 1,500 jobs, invigorating local corrugated conversions.[3]James A. Loyola, “CNPF Investing USD 40 Million in Misamis Coco Facility,” mb.com.ph Luzon’s dominance will gradually dilute as port and cold-chain investments pull finished-goods assembly closer to raw-material sources, yet Metro Manila will remain the decision-making and design hub of the Philippines corrugated packaging market.

Competitive Landscape

United Pulp and Paper, which commands roughly 25% of domestic linerboard capacity, eyes an expansion at its Bulacan mill, targeting an increase from 240,000 TPA to 400,000 TPA, contingent on the stability of OCC prices.[4]PaperMart, “United Pulp and Paper to Increase Capacity,” papermart.in This move underscores the company's scale advantage. Meanwhile, the firm's newly installed Andritz FibreSolve system enhances yield from heavily contaminated OCC, guaranteeing a consistent supply for clients with tight deadlines. In a strategic maneuver, San Miguel Yamamura Packaging Corporation is leveraging its glass and metal divisions to upsell corrugated cartons to beverage and sauce bottlers, driving an impressive 18.04% surge in operating profits in 2024.

Mid-tier players are ramping up efforts to seize regional market volumes. UET Box Manufacturing is channeling PHP 169.7 million (USD 3 million) to expand its floor space in Clark Freeport, a move strategically aligned with Central Luzon's logistics surge. In a bid for vertical integration, foreign players are making their mark; Austria's ALPLA has inaugurated a PHP 500 million (USD 8.8 million) blow-molding facility in Laguna, poised to cater to carton demands of its global clientele. The race for technological supremacy is palpable, with converters automating corrugators, adopting color-management systems, and experimenting with hybrid inkjet-flexo lines to capture the SME market.

While the top two suppliers dominate with a near-40 % combined market share, over 20 regional converters serve provincial hubs, ensuring competitive pricing on custom orders. The strategic spotlight shines on securing OCC sources, cold-chain-grade triple-wall formats, and agile digital printing, all in sync with EPR-driven short-order cycles. These market dynamics suggest a landscape with steady yet navigable entry barriers in the Philippines' corrugated packaging market.

Philippines Corrugated Packaging Industry Leaders

SCG Packaging Public Company Limited

San Miguel Yamamura Packaging Corp.

Valenzuela Packaging Container Corp.

Sunpack Container and Packaging Corp.

Basic Box Industries Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: ALPLA inaugurated its 200th global site, a PHP 500 million (USD 8.8 million) plant in Laguna, equipped with ISBM, compression, and EBM lines, underscoring a surge in packaging FDI.

- April 2026: Monde Nissin allocated PHP 7.53 billion (USD 132.4 million) to complete its new biscuit complex, slated for commissioning in 2027, boosting future carton volumes.

- February 2026: Groundbreaking began for the PHP 16.93 billion (USD 297.7 million) New Cebu International Container Port, targeting completion in 2028 to decongest cargo in Central Visayas.

- June 2025: The Department of Agriculture launched a PHP 3 billion (USD 52.8 million) program for 99 modular cold-storage units, which will require moisture-resistant triple-wall boxes.

Philippines Corrugated Packaging Market Report Scope

The Philippines Corrugated Packaging Market encompasses the production, distribution, and utilization of corrugated packaging materials within the country. This market primarily includes corrugated boxes, sheets, and containers used across industries such as food and beverage, electronics, pharmaceuticals, and other industries. The study analyzes market trends, growth drivers, challenges, and opportunities within the defined scope, providing insights into the market's current and forecasted performance.

The Philippines Corrugated Packaging Market Report is Segmented by Material (Virgin Kraft Linerboard, Recycled Linerboard, Corrugating Medium, Semi-Chemical Fluting, and Other Materials), Flute Type (A Flute, B Flute, C Flute, E Flute, and F Flute), Packaging Type (Regular Slotted Containers, Die-Cut Custom Boxes, Folding Cartons, Point-of-Purchase Displays, Pallet Boxes, and Other Packaging Types), Wall Type (Single-Wall, Double-Wall, Triple-Wall, and Single Face), Printing Technology (Flexographic Printing, Digital Inkjet Printing, Litho-Lamination, Screen Printing, and Other Printing Technologies), End-User Industry (Processed Foods, Fresh Food and Produce, Beverages, Electrical Products, Personal Care and Cosmetics, E-commerce Fulfillment Centers, Pharmaceuticals, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Kraft Linerboard |

| Recycled Linerboard |

| Corrugating Medium |

| Semi-Chemical Fluting |

| Other Materials |

| A Flute |

| B Flute |

| C Flute |

| E Flute |

| F Flute |

| Regular Slotted Containers |

| Die-Cut Custom Boxes |

| Folding Cartons |

| Point-of-Purchase Displays |

| Pallet Boxes |

| Other Packaging Types |

| Single-Wall |

| Double-Wall |

| Triple-Wall |

| Single Face |

| Flexographic Printing |

| Digital Inkjet Printing |

| Litho-Lamination |

| Screen Printing |

| Other Printing Technologies |

| Processed Foods |

| Fresh Food and Produce |

| Beverages |

| Electrical Products |

| Personal Care and Cosmetics |

| E-commerce Fulfillment Centers |

| Pharmaceuticals |

| Other End-User Industries |

| By Material Type | Virgin Kraft Linerboard |

| Recycled Linerboard | |

| Corrugating Medium | |

| Semi-Chemical Fluting | |

| Other Materials | |

| By Flute Type | A Flute |

| B Flute | |

| C Flute | |

| E Flute | |

| F Flute | |

| By Packaging Type | Regular Slotted Containers |

| Die-Cut Custom Boxes | |

| Folding Cartons | |

| Point-of-Purchase Displays | |

| Pallet Boxes | |

| Other Packaging Types | |

| By Wall Type | Single-Wall |

| Double-Wall | |

| Triple-Wall | |

| Single Face | |

| By Printing Technology | Flexographic Printing |

| Digital Inkjet Printing | |

| Litho-Lamination | |

| Screen Printing | |

| Other Printing Technologies | |

| By End-User Industry | Processed Foods |

| Fresh Food and Produce | |

| Beverages | |

| Electrical Products | |

| Personal Care and Cosmetics | |

| E-commerce Fulfillment Centers | |

| Pharmaceuticals | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the 2026 value of the Philippines corrugated packaging market?

The Philippines corrugated packaging market size is estimated at USD 2.87 billion in 2026, and it is forecast to reach USD 3.7 billion by 2031 at a 5.21% CAGR.

Which flute type is growing fastest in Philippine corrugated applications?

F flute is projected as the fastest-expanding profile, posting a 6.89% CAGR through 2031 as cosmetics and small-electronics brands choose thinner calipers that lower freight costs.

How will government plastic regulations influence corrugated demand?

Extended Producer Responsibility targets and proposed excise taxes on plastic bags are redirecting brand owners toward recyclable corrugated alternatives, adding more than 1.5% points to forecast CAGR.

Which region outside Luzon offers the next growth pocket for converters?

Central Visayas is expected to surge once the New Cebu International Container Port opens in 2028, shortening lead times and fueling demand from seafood and consumer-goods exporters.

What printing technology trend should SME shippers monitor?

Digital inkjet printing is expanding at 7.81% CAGR, providing cost-effective short-run graphics that help small sellers differentiate in crowded online marketplaces.

Who holds the largest individual share of Philippines linerboard capacity?

United Pulp and Paper controls about one-quarter of local market capacity and is evaluating an expansion to 400,000 tonnes per year, maintaining its lead among domestic producers.

Page last updated on: