Pharmaceutical Manufacturing Execution System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.51 Billion |

| Market Size (2031) | USD 4.02 Billion |

| Growth Rate (2026 - 2031) | 9.81% CAGR |

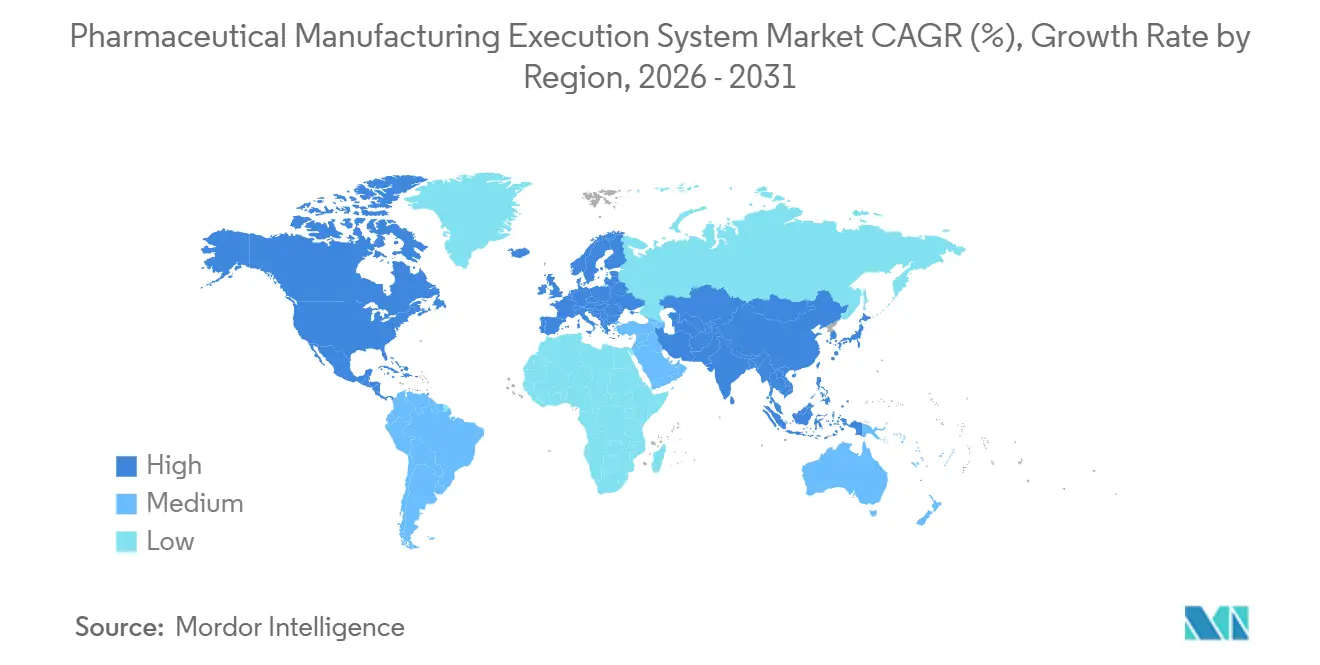

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

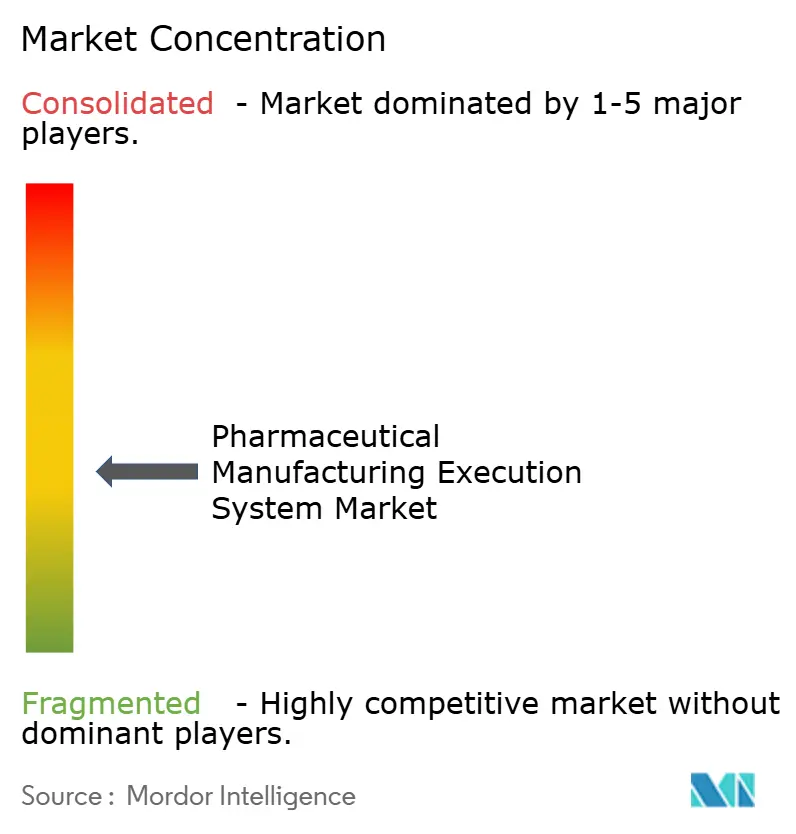

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pharmaceutical Manufacturing Execution System Market Analysis by Mordor Intelligence

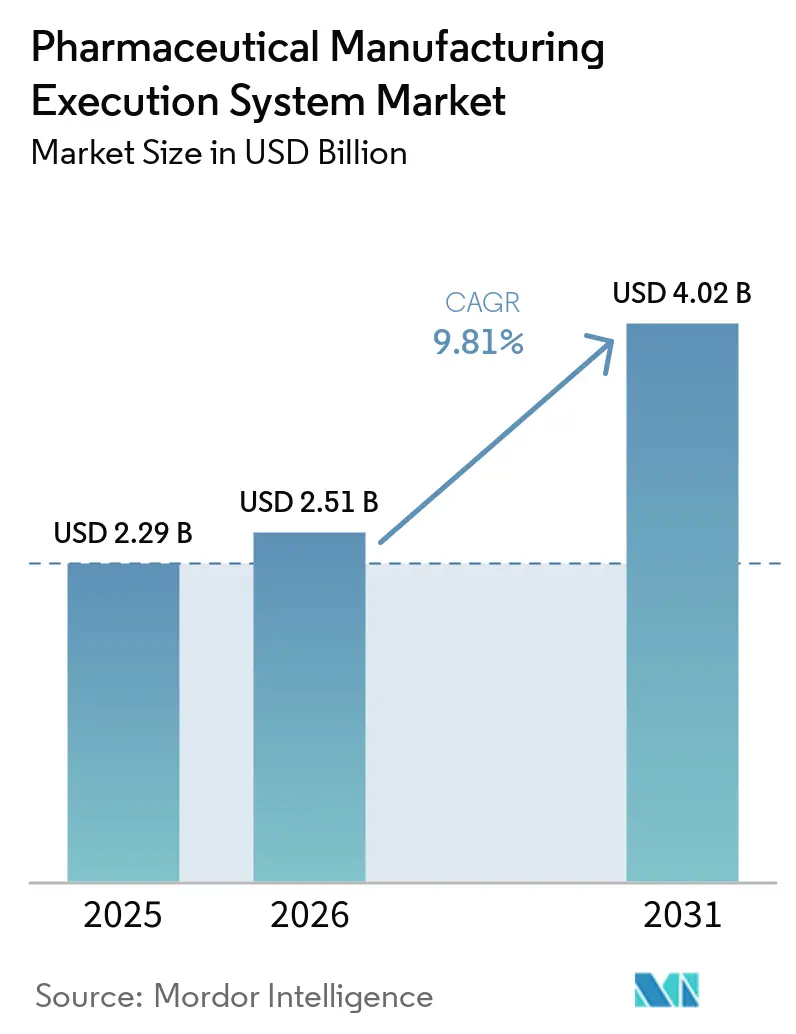

The Pharmaceutical Manufacturing Execution System Market size is expected to grow from USD 2.29 billion in 2025 to USD 2.51 billion in 2026 and is forecast to reach USD 4.02 billion by 2031 at 9.81% CAGR over 2026-2031.

Regulatory digitization, risk-based validation practices, and continuous pressure on data integrity and serialization continue to direct investment toward validated MES platforms that can orchestrate compliant operations across sites. The pharmaceutical manufacturing execution system market is also benefiting from cloud-native deployments that reduce infrastructure burden and speed global rollouts while maintaining validated state and auditability. In parallel, serialization and interoperable traceability requirements under mature regimes are embedding Level 4 connectivity and EPCIS messaging into core MES workflows for end-to-end visibility. Rapid growth in biologics and cell and gene therapies is expanding demand for MES capabilities that manage the chain of identity and the chain of custody with deterministic control, standardized checklists, and tight integration to scheduling, LIMS, and cold chain. The pharmaceutical manufacturing execution system market is therefore moving from discrete, site-level digitization to multi-plant, cloud-enabled architectures that standardize master recipes, shrink review cycles, and improve supply resilience.

Key Report Takeaways

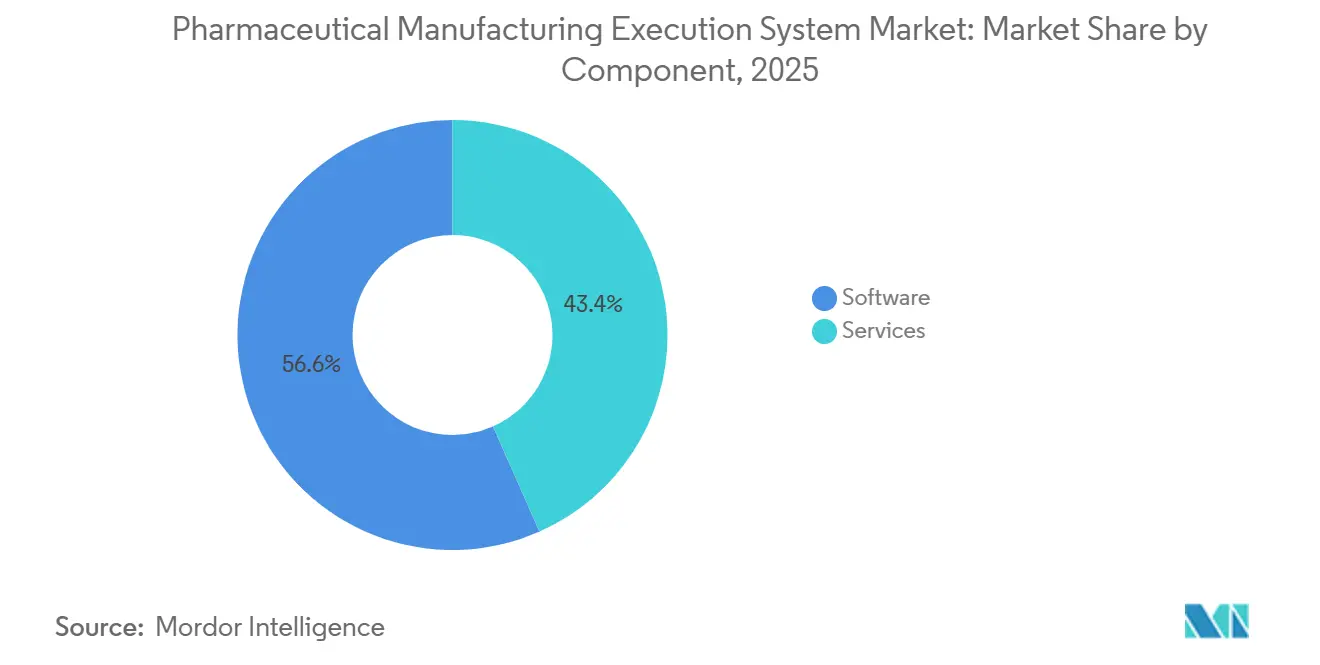

- By component, software captured 56.64% revenue share in 2025, while services is projected to post a 10.23% CAGR over 2026-2031 in the pharmaceutical manufacturing execution system market.

- By deployment, on-premise held 55.81% in 2025, and cloud/SaaS is forecast to expand at 13.65% CAGR through 2031.

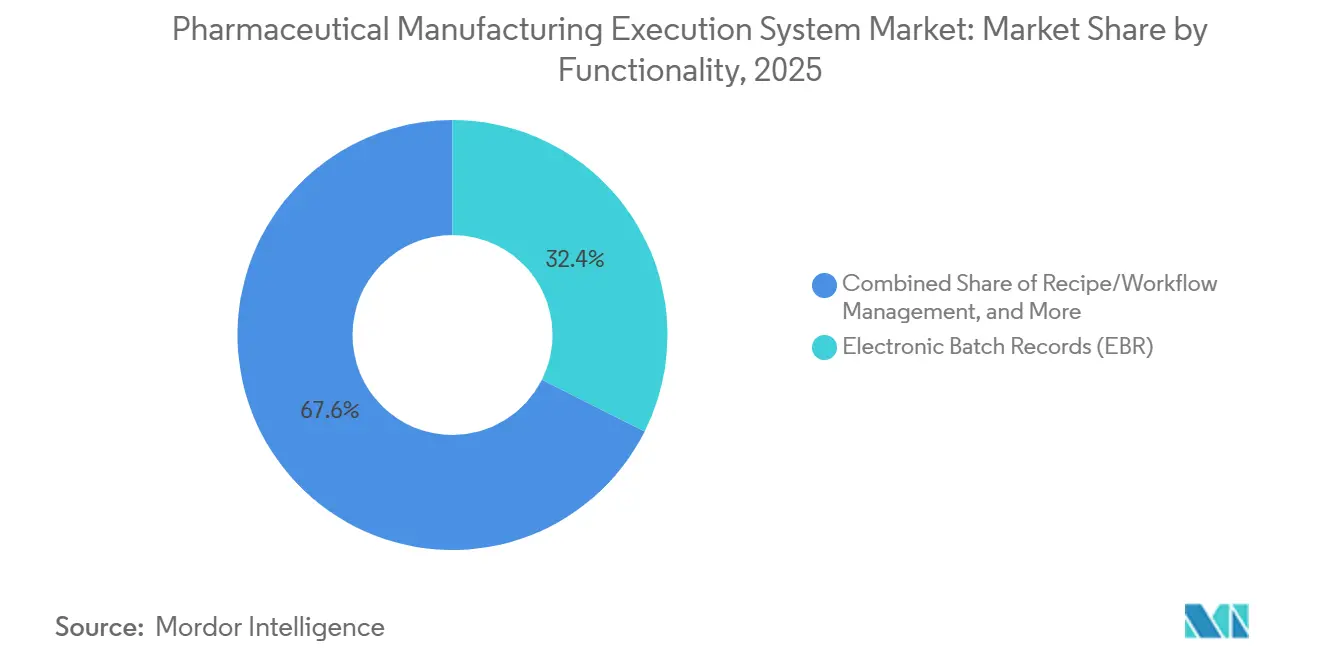

- By functionality, electronic batch records led with 32.40% in 2025, and serialization integration is advancing at a 12.78% CAGR to 2031 in the pharmaceutical manufacturing execution system market.

- By end user, pharmaceutical manufacturers accounted for 42.54% in 2025, while cell & gene therapy manufacturers are projected at a 14.93% CAGR between 2026 and 2031 in the pharmaceutical manufacturing execution system market.

- By geography, North America held 37.23% of the pharmaceutical manufacturing execution system market share in 2025, while Asia-Pacific recorded the highest projected CAGR at 15.83% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Pharmaceutical Manufacturing Execution System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Compliance and Data Integrity Requirements | +3.2% | Global, with higher weight in North America, EU due to FDA, EMA enforcement escalation | Short term (≤ 2 years) |

| Pharma 4.0 Digitalization Momentum (ISPE) | +2.1% | North America core, APAC fast followers | Medium term (2-4 years) |

| Need For Real-Time Visibility and End-to-End Traceability | +1.8% | Global, particularly critical in biologics hubs (US, EU, Singapore) | Short term (≤ 2 years) |

| Growth In Biologics, Cell and Gene Therapies | +2.4% | US biotech corridor, EU (Germany, Switzerland), early adopters in China/Singapore | Long term (≥ 4 years) |

| Computer Software Assurance (CSA) Enabling Risk-Based Validation | +1.3% | North America, progressive EU sites | Medium term (2-4 years) |

| Continuous Manufacturing (ICH Q13) and Real-Time Release | +1.6% | Early adopters in US, EU, pilots in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Compliance and Data Integrity Requirements Accelerate MES Investment

Regulated manufacturers are reinforcing validated electronic systems to align with 21 CFR Part 11 requirements for trustworthy electronic records, e-signatures, and audit trails that can support rigorous investigations. MES platforms address this with controlled workflows, time-stamped actions, and immutable audit logs that reduce error risk and strengthen data integrity.[1]Dot Compliance Team, “FDA 21 CFR Part 11 Compliance: What You Need to Know in 2026,” Dot Compliance Serialization and interoperable traceability are pushing deeper integration between MES and enterprise repositories to ensure unit-level, lot-level, and shipment-level visibility across the full product lifecycle. [2]SAP, “SAP Advanced Track and Trace for Pharmaceuticals,” SAP As manufacturers replace paper and hybrid records with digitized batch execution and review-by-exception, they compress cycle times and enhance release readiness with actionable deviations, signatures, and evidentiary completeness.[3]Honeywell, “Honeywell Unveils AI-Assisted Automation Platform to Transform Life Sciences Manufacturing Industry,” This compliance-driven shift is visible in project scoping and vendor assessments that prioritize validated templates, secure development lifecycles, and proven audit-readiness.[4]Rockwell Automation, “Rockwell Automation Launches PharmaSuite 12.00 to Accelerate Secure, Scalable Deployments,” The pharmaceutical manufacturing execution system market is therefore tilting toward platforms that can demonstrate full ALCOA-aligned data integrity and streamlined evidence generation for audits and inspections.

Pharma 4.0 Digitalization Momentum Reshapes Operational Models

Digitalization in operations is advancing toward cloud-ready, containerized, and low-code-enabled architectures that bring agility to validation and change control while preserving the validated state. MES platforms that unify shop-floor execution with quality and analytics create a common operating picture for operators, supervisors, and QA, which supports real-time decision-making and better batch disposition. Continuous improvement programs are also leaning on standardized master recipes and electronic work instructions to eliminate variability and reduce hold times, which is consistent with ambitions for real-time release. As low-code tools become embedded in MES ecosystems, process engineers can iterate workflows and forms faster without heavy custom code, which shortens design-validation cycles under risk-based approaches.[5]Tulip, “Manufacturing Execution System (MES) for Pharmaceutical,” The net effect is that the pharmaceutical manufacturing execution system market is aligning with Pharma 4.0 principles by converging execution, quality, serialization, and analytics with flexible deployment choices that scale from a single line to multi-plant networks.

Need for Real-Time Visibility Drives Review-by-Exception Adoption

Manufacturers are moving batch review from post-production to concurrent review-by-exception to shrink release cycles and reduce manual checks. In practical terms, MES applies acceptance rules to recorded actions and results, surfaces exceptions for human intervention, and routes issues into standardized CAPA workflows that accelerate closure. The same digital backbone enables real-time equipment dashboards and material genealogy, which supports faster rescheduling, targeted recalls, and more resilient responses to unplanned downtime. As teams gain confidence in contemporaneous data capture from MES and connected systems, reliance on paper records drops, and audit-readiness strengthens. The pharmaceutical manufacturing execution system market is, therefore, seeing sustained demand for RbE-enabling EBR modules and integrated deviation management because they deliver measurable time savings and quality consistency at scale.

Growth in Biologics, Cell and Gene Therapies Demands Specialized Execution Infrastructure

Biologics and cell and gene therapy programs require precise orchestration across patient scheduling, materials, analytics, and logistics, with an end-to-end chain of identity and chain of custody. Vendors are responding with specialized orchestration layers, closed-system hardware, and validated digital workflows to manage patient-specific runs without cross-contamination risk. Cloud-hosted MES deployments are gaining traction in clinical and early commercial CGT settings to simplify global operations while preserving data integrity and audit trails. As CGT programs scale, integration between MES, LIMS, serialization, and ERP becomes essential to maintain batch identity, coordinate apheresis-to-infusion timelines, and ensure correct dose tracking. This specialized need profile is lifting demand in the pharmaceutical manufacturing execution system market for capabilities that are natively patient-centric and interoperable across the clinical and commercial continuum.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Implementation Cost and Program Complexity | -1.4% | Mid-sized firms globally, acute in cost-sensitive APAC markets | Short term (≤ 2 years) |

| Integration with Legacy Systems and Data Silos | -0.9% | Mature pharma with brownfield sites (North America, Western Europe) | Medium term (2-4 years) |

| Validation Talent Gaps and CSV/CSA Transition Bottlenecks | -0.7% | Global, particularly acute in Asia-Pacific CDMOs | Medium term (2-4 years) |

| Master Data and Process Standardization Readiness Shortfalls | -0.5% | Multi-site pharma (North America, EU), rapid-growth CDMOs in APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Implementation Cost and Program Complexity Delay Mid-Market Adoption

Program complexity remains a barrier for organizations with lean IT and QA teams because MES is a transformation program rather than a simple software install. Cloud-native and managed service models are gaining favor because they reduce infrastructure ownership, streamline qualification, and shift more validation documentation to vendors that operate secure development and release practices. Low-code toolkits are also emerging to accelerate value by letting manufacturing teams configure validated workflows and forms faster with less custom code. Some vendors now package pre-validated content, consultancy hours, and industry templates to cut validation effort for emerging pharma and biotech teams. Even with these advances, many mid-market buyers pace deployments to align with change control capacity and site readiness, which can lengthen overall timelines despite technology gains. The pharmaceutical manufacturing execution system market continues to address this restraint with phased roadmaps, cloud-hosted pilots, and pre-built content that can be replicated across plants without rework.

Integration with Legacy Systems Fragments Digital Continuity

Heterogeneous brownfield sites must connect PLCs, SCADA, historians, LIMS, ERP, and serialization repositories into a coherent, governed data fabric without fragile point-to-point links. Many pharma companies identify legacy equipment integration as a primary barrier for MES success, which drives interest in connector-rich middleware and standardized interfaces that lower validation and maintenance overhead. Data silos also raise reporting costs and slow investigations, which is why projects increasingly include a governed data layer that unifies batch, quality, and supply records under a single compliance framework. Serialization mandates add to this integration agenda by requiring a tight association between batch context in MES and unit-level identifiers in enterprise repositories for global reporting. Vendors are responding with modular site managers, EPCIS 1.2 messaging, and cloud scaling that reduce custom interfaces while keeping data integrity guardrails intact. The pharmaceutical manufacturing execution system market is therefore moving toward vendor-agnostic connectors, pre-built integration packs, and lifecycle-managed cloud services that simplify integration across diverse plant estates.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Growth Reflects Complexity of Pharmaceutical IT Ecosystems

Software captured 56.64% of the pharmaceutical manufacturing execution system market share in 2025, and Services is projected to expand at 10.23% CAGR over 2026-2031, reflecting rising demand for expert-led deployment, validation, and lifecycle support. Buyers continue to prioritize vendors with proven EBR, deviation management, and serialization integration, along with secure development practices and robust audit trails. As organizations expand multi-site deployments, they also require sustained services to manage versions, regression testing, and release notes in line with quality systems. The pharmaceutical manufacturing execution system market is therefore seeing broader attach rates for training, managed validation, and 24x7 support to maintain a validated state across upgrades. On the workforce side, vendors and integrators are helping close skills gaps with certified curricula so operators, QA, and IT administrators can sustain compliant operations. This services-centric model is reinforced by cloud MES, where providers qualify infrastructure and deliver pre-validated content that reduces customer burden during deployments and routine updates.

Services growth also reflects the complexity of integrating MES with automation, quality, and enterprise systems in brownfield environments. Industry teams increasingly favor partners that bring pre-built connectors, validation templates, and recipe accelerators to shrink project timelines without sacrificing compliance. The pharmaceutical manufacturing execution system industry is adopting low-code tools to speed configuration of forms and workflows under change control, which in turn elevates demand for governance and lifecycle management services. Vendors are also bundling consultancy hours with new licenses and as-a-service offerings to align scope with risk-based assurance activities and site readiness. This migration toward service-led value delivery positions the pharmaceutical manufacturing execution system market for sustained services expansion as digital maturity advances across large pharma, biotech, and CDMOs.

By Deployment: Cloud/SaaS Gains Traction as Validation Burden Shifts to Vendors

On-premise deployments held 55.81% in 2025, while Cloud/SaaS is projected to be the fastest-growing path at 13.65% CAGR over 2026-2031 as buyers balance data sovereignty with agility and speed to value. Cloud-native MES and as-a-service models are reducing infrastructure ownership, enabling faster global rollouts, and standardizing upgrades with automated testing packages managed by the vendor. Containerized platforms add flexibility by allowing hybrid topologies that keep production execution close to the line while moving analytics and reporting to elastic cloud compute. Low-code capabilities in modern suites help process teams configure forms and workflows without heavy custom code, which compresses design cycles and reduces IT backlog. Providers are also strengthening cybersecurity controls with secure development practices, hardening guidance, and documentation packs that align with customer quality expectations for validated operations.

Hybrid models now serve as a pragmatic bridge as teams modernize brownfield plants while maintaining uptime and deterministic control for regulated steps. As CDMOs scale portfolios across regions, multi-tenant SaaS becomes attractive for standardized master recipes, client-specific quality workflows, and faster onboarding with centralized governance. Cloud orchestration of serialization further supports distributed supply networks by linking packaging events, commissioning, and shipment messages with batch context for downstream queries. The pharmaceutical manufacturing execution system market is therefore converging on deployment flexibility, where on-premise, private cloud, and public cloud options can be mixed to balance control, scalability, and compliance. Providers that deliver pre-validated content, managed updates, and secure-by-design stacks will continue to stand out as buyers look to simplify total cost of ownership without compromising audit-readiness.

By Functionality: Serialization Integration Emerges as Fastest-Growing Module

Electronic batch records remained the largest functionality in 2025 at 32.40%, while Serialization Integration is projected to be the fastest-growing capability at a 12.78% CAGR over 2026-2031 as interoperable traceability becomes a baseline expectation. DSCSA and related global directives require interoperable data exchange that binds serial numbers, lots, and shipments with batch execution context, which is pushing deeper integration between MES and Level 4 repositories. Modern serialization modules act as site managers and message hubs that unify packaging lines, MES, ERP, and national systems using standards like EPCIS with cloud scaling for peak events. In quality, deviation, and CAPA investigations, serialization data is now routinely referenced to narrow recall scope and identify suspect supplier lots faster. The pharmaceutical manufacturing execution system market is aligning EBR, deviation management, and serialization to support targeted recalls and faster disposition with strong data integrity.

As repositories expand and country-specific rules evolve, scalable interfaces and lifecycle-managed connectors are reducing custom code and validation rework. Cloud-native serialization platforms that can operate on-premise, in customer clouds, or as managed SaaS help harmonize operations across multi-region portfolios Integration with MES also brings timestamped audit trails with e-signatures to every commissioning, aggregation, and decommissioning event. For manufacturers, this convergence supports review-by-exception, golden batch analyses, and continuous improvements anchored in consistent, queryable data. The pharmaceutical manufacturing execution system market size for serialization-focused modules is thus positioned for sustained growth as compliance and supply chain resilience stay at the top of executive agendas.

By End User: Cell & Gene Therapy Manufacturers Drive Fastest Segment Expansion

Pharmaceutical manufacturers accounted for 42.54% in 2025, while Cell & Gene Therapy Manufacturers are projected to post a 14.93% CAGR in 2026-2031 as patient-specific operations require deep digital orchestration. Patient-centric manufacturing requires an end-to-end chain of identity and chain of custody that are enforced electronically at every step, which is creating demand for MES-integrated orchestration and QC control points. Vendors are releasing specialized orchestration and closed-system platforms that condense cleanroom footprints and allow a single operator to process multiple patient batches while maintaining isolation and traceability. Cloud MES is also entering clinical and early-commercial environments to speed global setup and keep validation documentation current with frequent updates under a managed service construct. The pharmaceutical manufacturing execution system market is therefore expanding coverage for COI checks, serialized dose tracking, and time-sensitive scheduling while ensuring compliant audit trails.

Biopharmaceutical manufacturers continue to standardize EBR and deviation management for complex biologics operations where high data volumes and continuous monitoring demand robust integrity controls. CDMOs lean on multi-tenant SaaS and template libraries to onboard clients fast and harmonize quality processes across diverse product portfolios. Interoperability with LIMS and serialization ensures that materials, samples, and doses remain tightly coupled to batch context for release and pharmacovigilance reporting. As a result, the pharmaceutical manufacturing execution system industry is broadening feature sets to support clinical-to-commercial transitions with standardized recipes, reference master data, and governed change control. The pharmaceutical manufacturing execution system market will continue to prioritize modules that handle serialized products, patient scheduling, and multi-site analytics that shorten time to scale.

Geography Analysis

North America held 37.23% of the pharmaceutical manufacturing execution system market share in 2025, anchored by mature regulatory frameworks and a deep base of innovators across biotech clusters. Buyer priorities in 2026 center on cloud-enabled MES deployments that preserve validated state while improving speed of change across multiple plants. Large pharma and leading CDMOs continue retrofits at legacy sites to standardize EBR, integrate serialization, and enable review-by-exception across diverse product portfolios. The region is also investing in closed-system cell therapy platforms and orchestration tools that unify scheduling, batch execution, and QC evidence in a compliant manner. This foundation supports continued growth in the pharmaceutical manufacturing execution system market as firms expand multi-site templates, strengthen data integrity, and build supply resilience.

Asia-Pacific is the fastest-growing region with a 15.83% CAGR over 2026-2031 for the pharmaceutical manufacturing execution system market size, driven by capacity build-outs in biologics and the scale-up of CDMO services. As manufacturers add new lines and facilities, demand is rising for standardized EBR, validated cloud options, and vendor-managed upgrades that reduce time to qualification. Regional CDMOs adopt modular MES content to onboard sponsors quickly and maintain harmonized quality practices across multi-client portfolios. Vendors are also working with customers on connector strategies for older equipment and point systems to minimize custom code and simplify validation. These priorities keep the pharmaceutical manufacturing execution system market focused on interoperability, cloud scaling, and secure-by-design operations across APAC’s expanding manufacturing footprint.

Europe continues to advance through standardized data governance, stronger cybersecurity expectations, and quality-by-design approaches that favor validated digital systems. Across the EU, harmonization of serialization, track-and-trace, and site-level qualification is prompting tighter coupling between MES, ERP, and enterprise repositories. The pharmaceutical manufacturing execution system market in Europe is also emphasizing cloud and hybrid deployments that preserve local control while centralizing analytics and master data. As vendors deepen low-code capabilities and pre-validated content, European manufacturers are accelerating upgrades without compromising validation discipline, especially in biologics clusters. These patterns reinforce steady demand in the pharmaceutical manufacturing execution system market as firms modernize operations, expand serialization coverage, and scale multi-site templates.

Competitive Landscape

The pharmaceutical manufacturing execution system market remains competitive with global automation majors, enterprise software providers, and cloud-native challengers addressing overlapping but distinct buyer needs. Vendors are differentiating with validated cloud services, pre-built EBR content, and proven integration to ERP and serialization repositories for faster time to value. Platforms that combine execution, quality, and analytics are gaining share within accounts as customers move from point digitization toward integrated operations and review-by-exception. Buyers continue to value configurable workflows, secure development, and end-to-end audit trails, which favor providers with validated templates and rigorous lifecycle management.

Strategic moves illustrate where the market is heading. Rockwell introduced a containerized release that supports hybrid and cloud deployment models with automated installers and cybersecurity built into the development process, which helps standardize rollouts across plants. Körber expanded a cloud-native serialization solution that integrates packaging lines, MES, and ERP while managing diverse country requirements under one lifecycle-managed platform. Honeywell launched an AI-assisted, cloud-native platform that links critical control with digital quality to reduce errors from paper-based methods and to accelerate digital introduction of new products. Siemens embedded low-code development that allows process teams to configure apps natively, which shortens design-validation cycles and supports Pharma 4.0 practices.

Service-led value delivery is also a defining theme. Vendors and integrators are packaging consultancy hours, pre-validated content, and automated testing that align with risk-based assurance approaches and reduce customer documentation overhead. Multi-tenant SaaS architectures target CDMOs that need shared templates and client-specific workflows, while closed-system platforms for cell therapy shrink cleanroom footprints and raise throughput per operator. Across these moves, the pharmaceutical manufacturing execution system market is trending toward modular, cloud-scalable, and interoperability-first strategies that accelerate deployments without diluting data integrity or audit readiness.

Pharmaceutical Manufacturing Execution System Industry Leaders

ABB Ltd.

Emerson Electric Co.

Honeywell International Inc.

Körber AG

Rockwell Automation, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Sartorius launched the Eveo Cell Therapy Platform, an integrated modular system for autologous cell therapy production, enabling a fourfold output increase within existing cleanroom spaces. One operator can process eight patient batches simultaneously, yielding over 350 doses annually compared to approximately 100 doses previously, potentially reducing CAR-T manufacturing costs by approximately 90% through compact design and workflow automation.

- May 2025: Rockwell Automation launched FactoryTalk PharmaSuite 12.00, introducing cloud-based deployment via Kubernetes containers with Linux compatibility, automated installation through the MICKA setup tool, and enhanced cybersecurity developed under certified secure development practices.

- April 2025: Honeywell introduced TrackWise Manufacturing, an AI-assisted, cloud-native platform among the first in life sciences to integrate digital and physical manufacturing environments. The containerized platform leverages Honeywell's Unit Operations Controller for critical control and embeds a quality framework for quality-by-design manufacturing, accelerating drug introduction while reducing errors and inefficiencies from paper-based methods.

Global Pharmaceutical Manufacturing Execution System Market Report Scope

As per the scope of the report, a pharmaceutical manufacturing execution System (MES) is a software-based system used to monitor, control, and document drug manufacturing processes in real time. It connects shop-floor operations with enterprise systems to ensure efficient production, data integrity, and process visibility. In pharmaceutical environments, MES is critical for managing electronic batch records, ensuring regulatory compliance, and enabling full traceability of materials and processes.

The pharmaceutical manufacturing execution system market is segmented by component, deployment, functionality, end user, and geography. By component, the market is segmented into software and services. By deployment, the market is segmented into on-premise and cloud / SaaS. By functionality, the market is segmented into electronic batch records (EBR), recipe/workflow management, equipment management, deviation & CAPA integration, serialization integration, and others. By end user, the market is segmented into pharmaceutical manufacturers, biopharmaceutical manufacturers, cell & gene therapy manufacturers, and CMOs / CDMOs. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers estimated market sizes and market trends for 17 countries across major regions worldwide. The report offers market value (in USD) for the above segments.

| Software |

| Services |

| On-Premise |

| Cloud / SaaS |

| Electronic Batch Records (EBR) |

| Recipe / Workflow Management |

| Equipment Management |

| Deviation & CAPA Integration |

| Serialization Integration |

| Others |

| Pharmaceutical Manufacturers |

| Biopharmaceutical Manufacturers |

| Cell & Gene Therapy Manufacturers |

| CMOs / CDMOs |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Software | |

| Services | ||

| By Deployment | On-Premise | |

| Cloud / SaaS | ||

| By Functionality | Electronic Batch Records (EBR) | |

| Recipe / Workflow Management | ||

| Equipment Management | ||

| Deviation & CAPA Integration | ||

| Serialization Integration | ||

| Others | ||

| By End User | Pharmaceutical Manufacturers | |

| Biopharmaceutical Manufacturers | ||

| Cell & Gene Therapy Manufacturers | ||

| CMOs / CDMOs | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected size and CAGR for the pharmaceutical manufacturing execution system market through 2031?

The pharmaceutical manufacturing execution system market size is projected to reach USD 4.02 billion by 2031, registering a 9.81% CAGR over 2026-2031.

Which deployment model is growing fastest in the pharmaceutical manufacturing execution system space?

Cloud/SaaS shows the fastest growth with a projected 13.65% CAGR over 2026-2031 as buyers adopt validated, vendor-managed services for speed and scalability.

What functionality areas are seeing the quickest uptake?

Serialization Integration is advancing fastest as interoperable traceability becomes mandatory and tightly coupled to MES workflows for end-to-end visibility and compliant reporting.

What is driving adoption of review-by-exception in batch release?

Digitized EBR with rule-based checks, integrated deviations, and concurrent QA review shortens release cycles and raises audit readiness compared to paper-heavy processes.

Why is MES demand rising in cell and gene therapies?

Patient-specific production requires rigorous chain of identity and custody, specialized orchestration, and integration with LIMS and serialization, which MES can unify with compliant audit trails.

How are vendors helping reduce MES program complexity and cost?

Vendors offer validated cloud services, pre-built templates, and consultancy hours to accelerate deployments while maintaining data integrity and validation discipline.

Page last updated on: