Pharma Predictive Analytics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

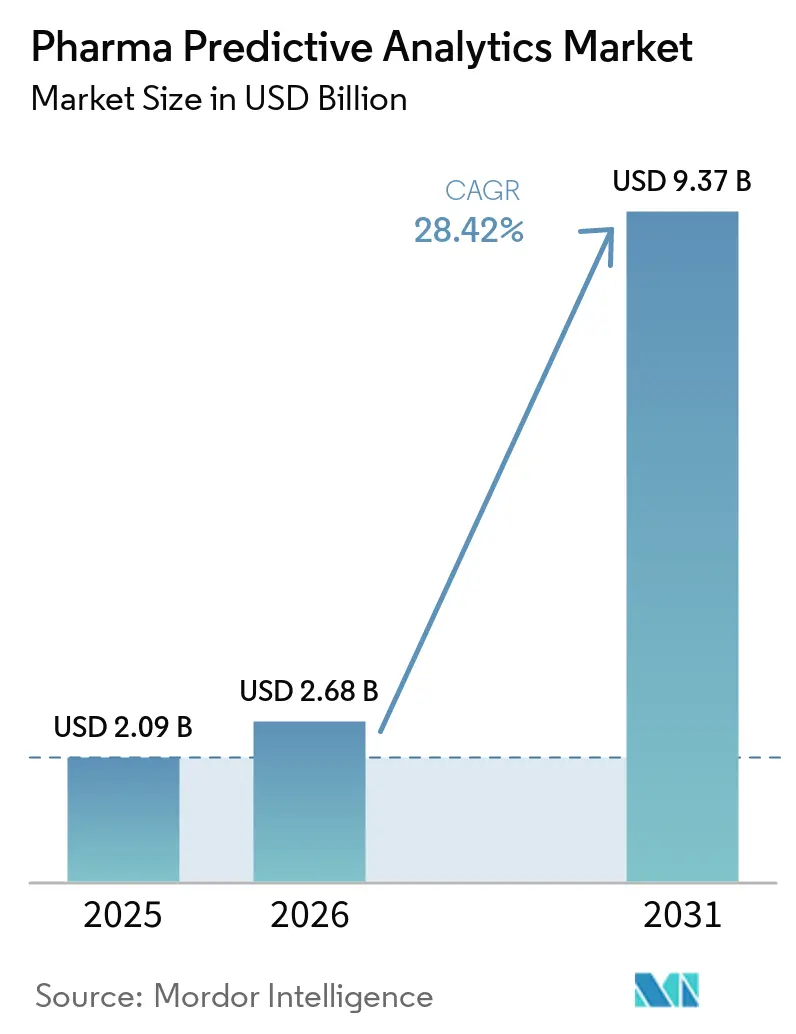

| Market Size (2026) | USD 2.68 Billion |

| Market Size (2031) | USD 9.37 Billion |

| Growth Rate (2026 - 2031) | 28.42% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pharma Predictive Analytics Market Analysis by Mordor Intelligence

The Pharma Predictive Analytics Market size is expected to increase from USD 2.09 billion in 2025 to USD 2.68 billion in 2026 and reach USD 9.37 billion by 2031, growing at a CAGR of 28.42% over 2026-2031.

The pharma predictive analytics market is expanding because pharmaceutical companies are shifting from retrospective reporting toward forward-looking systems that guide discovery, trial design, safety monitoring, and commercial planning in one operating layer. Lower clinical success rates and the high cost of development have made predictive tools part of the core operating discipline rather than an optional digital add-on. The pharma predictive analytics market is also benefiting from wider use of AI and ML, the rapid growth of regulatory-usable real-world data, and stronger adoption of multi-modal models in precision medicine. Competition is centered on integrated platforms, regulated workflows, proprietary data assets, and service depth, which favors vendors that can bundle software, data, and implementation support into a single enterprise relationship. The strongest opportunities in the pharma predictive analytics market sit with companies that can combine compliant data infrastructure, validated models, and therapeutic expertise across discovery, clinical development, and post-approval evidence generation.

Key Report Takeaways

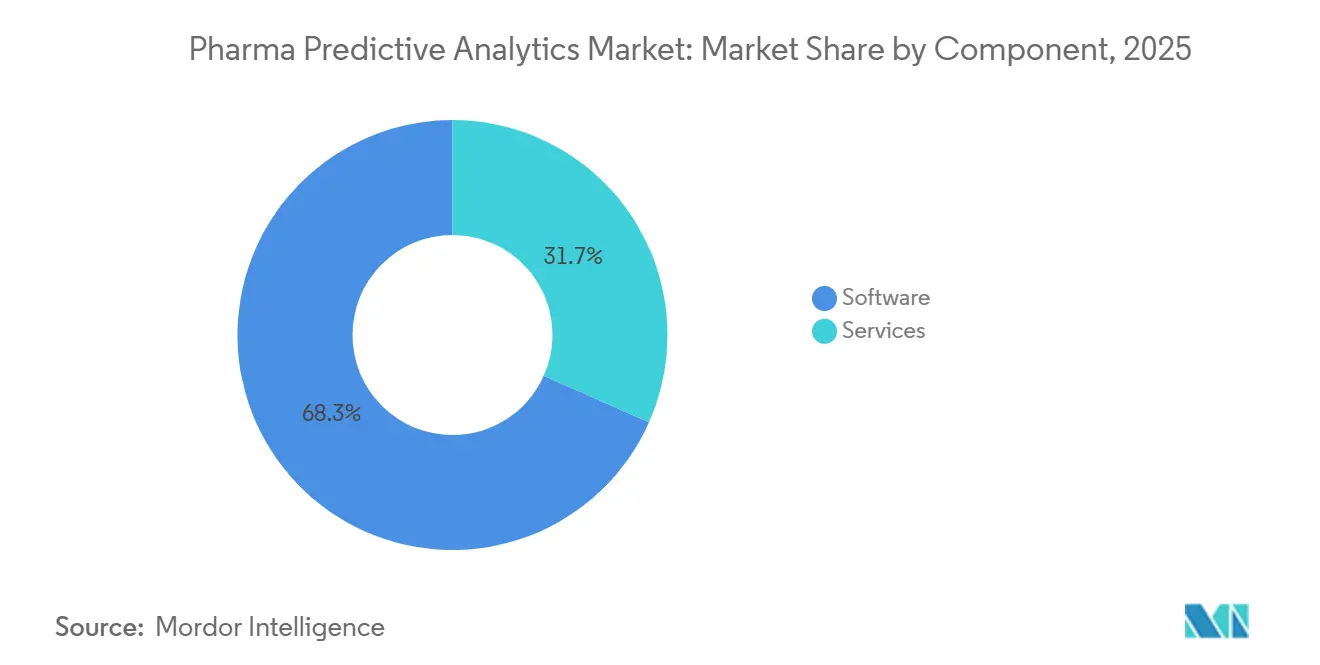

- By component, software held 68.34% of the pharma predictive analytics market size in 2025, while services are projected to expand at a 28.93% CAGR through 2031.

- By deployment, on-premise held 64.82% of the pharma predictive analytics market share in 2025, while cloud-based deployment is forecast to grow at a 29.36% CAGR through 2031.

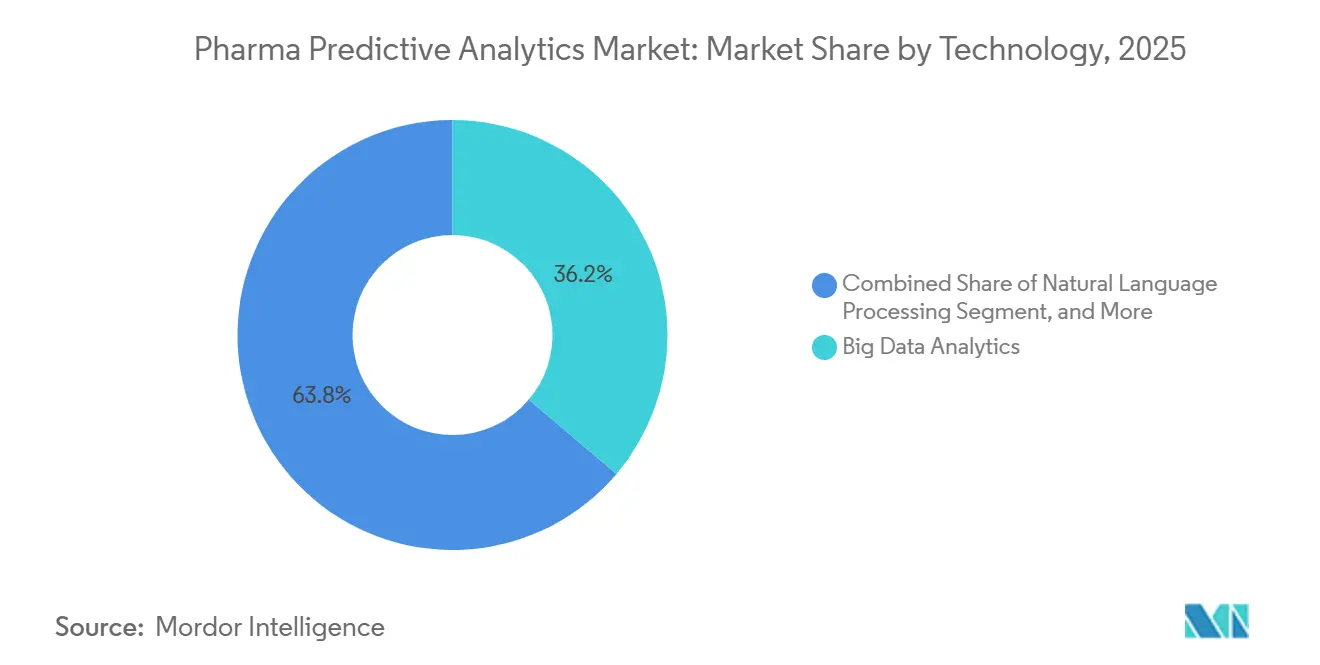

- By technology, big data analytics accounted for 36.18% share in 2025, while AI and ML are projected to grow at a 30.42% CAGR through 2031.

- By data source, clinical trial data held 28.53% share in 2025, while real-world evidence data is forecast to expand at a 31.23% CAGR through 2031 in the pharma predictive analytics market.

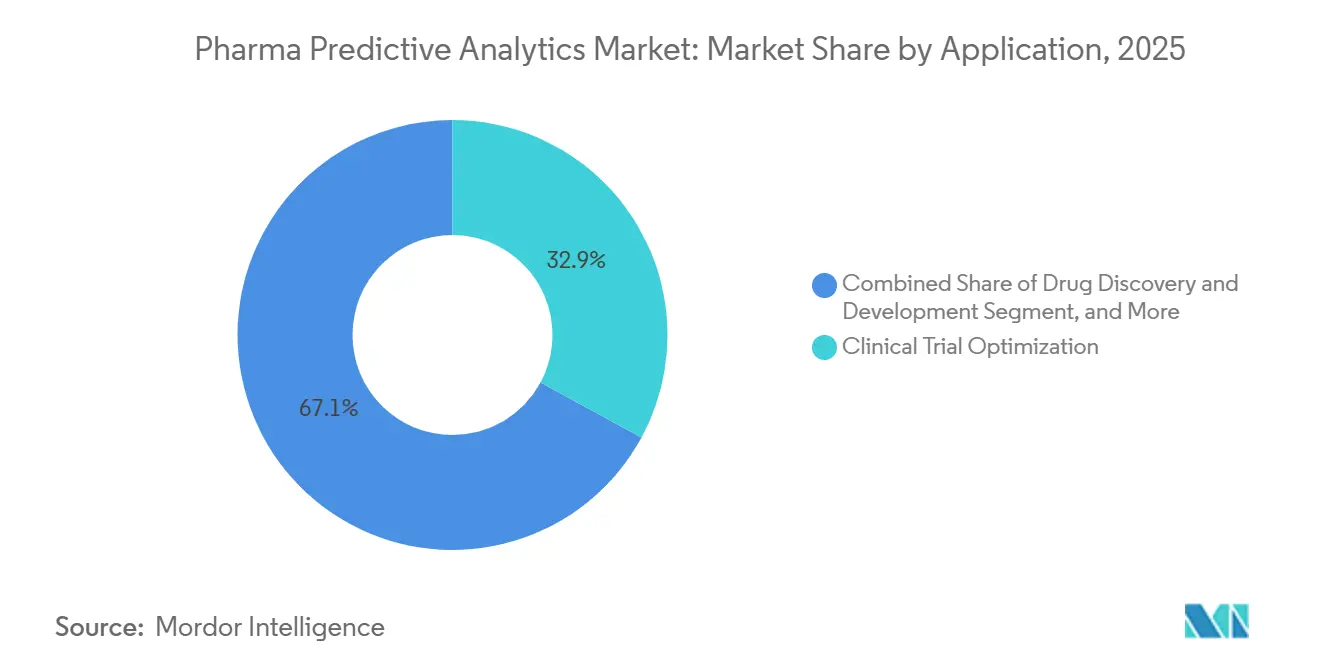

- By application, clinical trial optimization accounted for 32.95% of the pharma predictive analytics market size in 2025, while precision medicine is expected to grow at a 31.87% CAGR through 2031.

- By therapeutic area, oncology led with 33.92% share in 2025, while neurology is projected to rise at a 32.58% CAGR through 2031 in the pharma predictive analytics market.

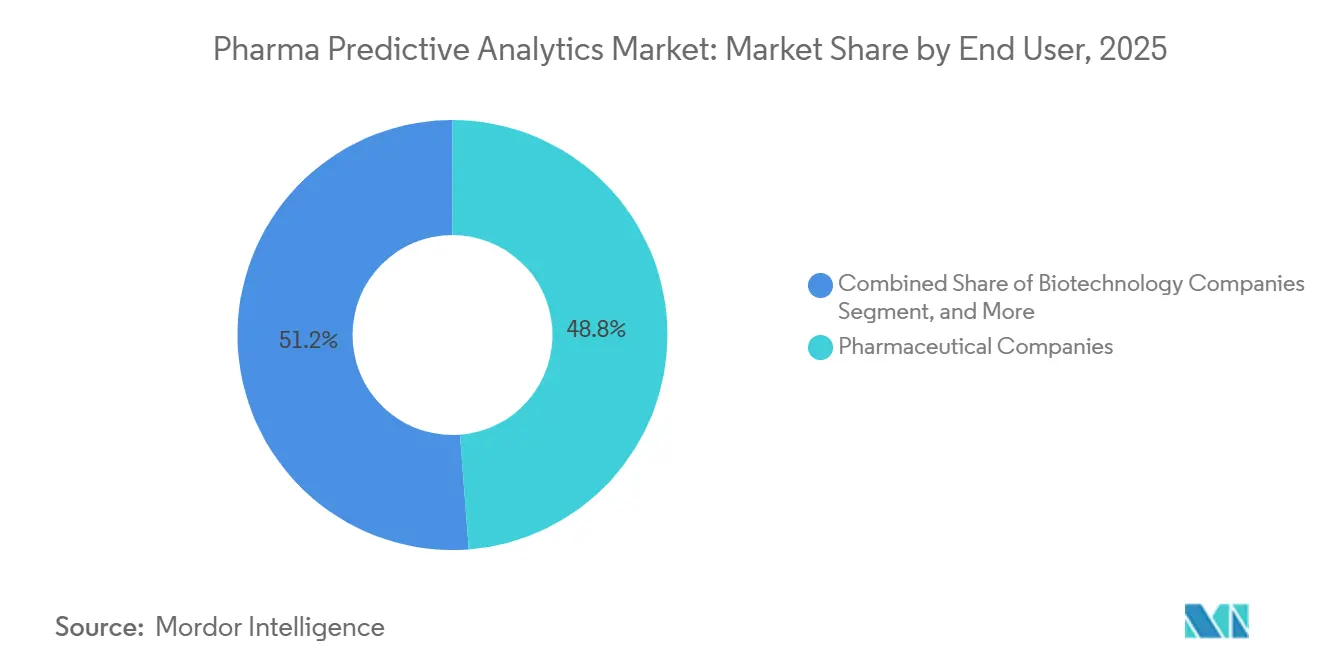

- By end user, pharmaceutical companies held 48.75% share in 2025, while contract research organizations are forecast to record the fastest growth at a 33.74% CAGR through 2031.

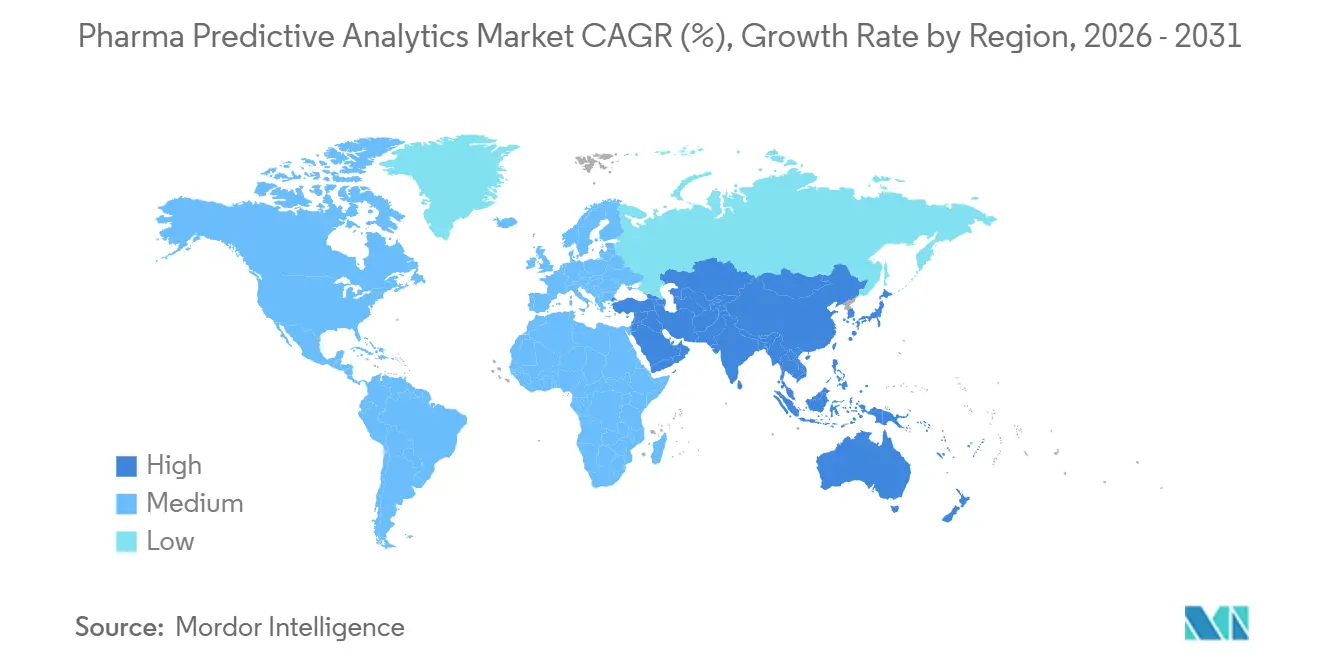

- By geography, North America led with 36.46% revenue share in 2025, and Asia-Pacific is forecast to register a 32.98% CAGR to 2031 in the pharma predictive analytics market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Pharma Predictive Analytics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption of AI & ML In Drug Discovery | +2.8% | Global, with concentration in North America and Europe | Short term (≤ 2 years) |

| Growing Volume of Healthcare & Real-World Data | +1.9% | Global, highest data density in North America and the EU | Medium term (2-4 years) |

| Increasing Focus on Personalized & Precision Medicine | +1.6% | North America, Europe, and advanced APAC markets | Medium term (2-4 years) |

| Need to Reduce Clinical-Trial Costs & Improve Success Rates | +1.5% | Global, with early gains in high-cost markets such as the US, the EU, and Japan | Short term (≤ 2 years) |

| Emergence of Federated Learning for Cross-Institution Analytics | +1.2% | The EU, North America, and APAC core markets such as Japan and South Korea | Medium term (2-4 years) |

| Accelerating Regulatory Sandboxes for Real-Time Trial Analytics | +0.9% | The UK, the US, and the EU, with spillover to Israel and Singapore | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of AI & ML in Drug Discovery

The pharma predictive analytics market is seeing a stronger commitment to AI-led drug discovery from large pharmaceutical and technology companies. In January 2026, NVIDIA and Eli Lilly announced a co-innovation AI lab with planned investment of up to USD 1 billion over 5 years to connect wet-lab and dry-lab learning systems in a continuous loop.[1]NVIDIA and Eli Lilly, “NVIDIA and Lilly Announce Co-Innovation AI Lab to Reinvent Drug Discovery in the Age of AI,” Merck states in March 2026 that its KERMT deep-learning model, trained on more than 11 million molecules, is already cutting early development timelines by 30% or more by screening out weak candidates before costly synthesis.[2]Merck, “Our AI Model KERMT Is Helping to Advance Drug Discovery,” In the pharma predictive analytics market, the clearest near-term value of ML sits in hit-to-lead optimization because that stage produces large data volumes and repeated failure patterns that models can learn from quickly. This is also pushing drug developers to formalize validation, documentation, and credibility standards for AI outputs before they are used in regulated submissions.

Growing Volume of Healthcare & Real-World Data

The pharma predictive analytics market is gaining momentum from the simultaneous expansion of data volume and regulatory usability in real-world evidence. In December 2025, the FDA removes a major barrier by allowing sponsors to use de-identified real-world datasets in submissions without requiring individual patient-level data in every case.[3]American Association of Blood Banks, “FDA Eases Access to Real-World Evidence in Drug and Device Reviews,” In March 2026, the agency adopts ICH M14, which creates clearer standards for the design and reporting of non-interventional pharmacoepidemiological studies used in post-approval safety assessment.[4]Reva Anada, “FDA Issues Final Guidance on Non-Interventional Studies Using Real-World Data for Drug and Biologic Safety,” The practical effect in the pharma predictive analytics market is that companies with FHIR-ready and audit-ready data environments can turn these changes into a competitive advantage faster than companies still relying on fragmented records. Europe is reinforcing the same direction through the EMA's DARWIN network, which already connects 20 data partners and covers 130 million patients across the region.[5]Christine Bahls, “In Focus, Top Takeaways from FDA Final Guidance on Real-World Evidence,”

Increasing Focus on Personalized & Precision Medicine

The pharma predictive analytics market is being shaped by precision medicine, where models now need to combine genomic, proteomic, imaging, and clinical data in a single analytic workflow. Novo Nordisk and OpenAI announced in April 2026 that they are applying advanced AI models to complex biological and clinical datasets to improve patient stratification and biomarker-led trial design. In December 2025, China's global health drug discovery institute launches the AI Kongming platform as an open-access end-to-end AI drug R&D system and reports several-fold improvements in candidate molecule hit rates across tuberculosis, malaria, and rare disease programs. In the pharma predictive analytics market, early movers in AI-stratified precision trials are also creating structured outcome datasets that can be used to retrain models and improve future trial design. That feedback loop strengthens the value of analytics platforms that can connect biomarker discovery, patient selection, and outcome tracking in one environment.

Need to Reduce Clinical-Trial Costs & Improve Success Rates

The pharma predictive analytics market is benefiting from demand for tighter control over trial cost, time, and attrition. Low approval rates mean that predictive failure remains common, so analytics tools are increasingly being treated as portfolio risk controls rather than only workflow accelerators. Recursion reports in February 2026 that its AI-native operating system reduces site selection time from months to hours and cuts the median candidate discovery timeline from 42 months to 17 months. In the pharma predictive analytics market, this changes investment logic because spending on analytics platforms can defer weaker trial decisions before they absorb larger clinical budgets. The strongest uptake is likely to continue in discovery programs, protocol design, site selection, and portfolio review, where measurable cycle-time gains can be captured first.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-Privacy & Multi-Jurisdiction Compliance Complexity | -1.8% | Global, most acute in the EU under GDPR, the US under HIPAA, and multi-jurisdiction trial operators | Medium term (2-4 years) |

| High Implementation & Integration Costs | -1.4% | Global, with the highest burden on mid-size pharma and emerging-market CROs | Short term (≤ 2 years) |

| Algorithmic Bias Triggering Regulatory Push-Back | -0.9% | North America and the EU, with spillover to core APAC markets | Long term (≥ 4 years) |

| Shortage Of Curated Domain-Specific Labeled Datasets | -0.7% | Global, with the highest severity in rare disease and neurology subsegments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-Privacy & Multi-Jurisdiction Compliance Complexity

The pharma predictive analytics market still faces material friction from privacy rules and model-governance obligations that differ across regions. In the United States and Europe, expectations now extend beyond basic data handling and into transparency, bias control, documentation, and post-deployment monitoring for high-risk AI systems. The EU AI Act is scheduled for full enforcement for high-risk AI systems in August 2026, which increases the compliance load for many pharma analytics applications. In the pharma predictive analytics market, this means data governance can no longer sit only with legal teams because model development, testing, and deployment now need the same compliance structure. Vendors and sponsors with unified architectures built around standards such as CDISC and FHIR will absorb these requirements faster than organizations working across disconnected data estates.

High Implementation & Integration Costs

The pharma predictive analytics market also faces resistance from the cost and complexity of connecting new platforms with legacy clinical systems, EHR environments, and regulatory workflows. These projects often require IQ, OQ, and PQ validation packages in GxP settings, which adds time, specialist labor, and documentation burden before any value is realized. The gap is most visible between large pharmaceutical companies and smaller organizations, because IQVIA states in March 2026 that 19 of the top 20 pharmaceutical companies already use IQVIA agents in their workflows. In the pharma predictive analytics market, that early deployment advantage can compound as incumbent users improve data quality, refine models, and standardize processes ahead of smaller peers. The result is a two-speed adoption pattern where platform-scale buyers move first, and mid-size firms adopt more slowly or rely on service-led models.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Dominates, Services Scale on Capability Gaps

Software held 68.34% share in 2025, while services are forecast to grow at a 28.93% CAGR through 2031. The pharma predictive analytics market still leans toward software because enterprise buyers want integrated analytics suites that can support discovery, clinical, safety, and commercial teams on a common platform. Cloud-native architecture has also made large deployments easier to manage across functions, which helped software expand faster during the early adoption phase. At the same time, service demand is rising because many pharmaceutical companies now need domain-specific support to extract usable value from tools they already deployed.

That shift is changing vendor positioning in the pharma predictive analytics market because buyers increasingly prefer a single provider for both platform delivery and implementation support. In March 2026, IQVIA launches IQVIA.ai as a unified agentic AI platform with more than 150 intelligent agents, which reflects a bundled platform-and-services model rather than a standalone software sale. This bundling strategy raises switching costs and narrows the room for smaller service specialists in the pharma predictive analytics industry. Regulatory qualification also remains important because enterprise buyers continue to screen for software environments that can be validated under GxP and related quality expectations.

By Deployment: On-Premise Holds Ground, Cloud-Based Accelerates Fastest

On-premise retained 64.82% share in 2025, while cloud-based deployment is projected to grow at a 29.36% CAGR through 2031. The pharma predictive analytics market still has a large on-premise base because major pharmaceutical companies continue to prioritize IP protection, internal control, and compatibility with legacy data centers. This is especially true in environments where compound data, patient records, and model outputs need tight access control. Cloud adoption is rising quickly, but it is not replacing local infrastructure in a uniform way.

Instead, the pharma predictive analytics market is moving toward hybrid architectures where sensitive data stays on-premise, and collaboration or inference layers shift to the cloud. IQVIA and NVIDIA state in January 2025 that their collaboration uses NVIDIA DGX Cloud while maintaining healthcare-grade controls for data integrity and compliance. In Japan, AI Data Inc. launched AI PharmaCDS on IDX in November 2025 as a high-security domestic cloud environment, which shows how data residency requirements are shaping deployment design in APAC. These patterns suggest that the pharma predictive analytics market will continue to support on-premise, sovereign cloud, and private cloud models alongside broader public cloud adoption.

By Technology: Big Data Foundational, AI & ML Defines the Growth Curve

Big data analytics held 36.18% share in 2025, while AI and ML are projected to grow at a 30.42% CAGR through 2031. The pharma predictive analytics market still depends on big data infrastructure because model performance falls when data pipelines are fragmented, have low volume, or are poorly curated. That is why storage, integration, and processing layers remain foundational even as AI gains more attention. AI and ML are growing faster because their value is now visible in candidate optimization, patient stratification, and pharmacovigilance signal detection.

NLP is also becoming more important in the pharma predictive analytics market because large volumes of clinical notes, regulatory text, and scientific literature still sit in unstructured form. IBM Research presents an agentic AI platform at ACS Spring 2026 that uses natural-language prompts to coordinate molecule generation and screening workflows at scale. The FDA's internal use of Project Elsa in 2025 also signals that text-based AI tools are becoming more acceptable inside regulated environments, even if governance expectations remain high. Over time, the pharma predictive analytics market is likely to favor platforms that combine big data infrastructure, AI model layers, and NLP interfaces in one stack.

By Data Source: Clinical Trial Data Leads, RWE Grows Fastest

Clinical trial data held 28.53% share in 2025, while real-world evidence data is forecast to grow at a 31.23% CAGR through 2031. The pharma predictive analytics market continues to treat trial data as the primary evidence base because it remains central to regulatory decision-making and protocol-led evaluation. Even so, its relative weight is starting to dilute as more real-world sources become accepted in development and post-approval workflows. That change is supporting broader use of EHR, claims, and genomic data inside predictive models.

In March 2026, the FDA adopted ICH M14 and strengthened the regulatory foundation for non-interventional real-world data in safety assessment. A 2025 study in Therapeutic Innovation & Regulatory Science finds that EHRs appeared in 75% of RWE study designs used in FDA labeling expansions from 2022 to 2024. In January 2026, ConcertAI and Foundation Medicine integrated genomic and clinical records covering 500,000 oncology patients, which shows how high-value data fusion is becoming a competitive asset in the pharma predictive analytics market. The value in the pharma predictive analytics industry is shifting toward platforms that can normalize and govern several evidence sources at once instead of relying on one dataset class.

By Application: Clinical Trial Optimization Anchors Revenue, Precision Medicine Accelerates

Clinical trial optimization accounted for 32.95% of the pharma predictive analytics market size in 2025, while precision medicine is expected to grow at a 31.87% CAGR through 2031. The pharma predictive analytics market still derives much of its current revenue from trial optimization because site selection, recruitment, and protocol design offer measurable returns and clear budget relevance. That position is supported by direct operating examples where analytics compresses timelines and improves execution. Precision medicine is expanding faster because biomarker-led trial design and multi-omics integration are creating more use cases for predictive modeling.

Recursion states in February 2026 that its platform cuts site selection time from months to hours, which reinforces why trial optimization remains the anchor use case. Parexel expands its patient safety offering in April 2026 through the acquisition of Vitrana, an AI-enabled pharmacovigilance platform, showing that adjacent applications such as safety analytics are also drawing investment. The pharma predictive analytics market is also likely to benefit from regulatory openness to stronger use of confirmatory real-world evidence in selected approvals. As those pathways become more established, outcome prediction and precision segmentation should widen the addressable scope of the pharma predictive analytics market.

By Therapeutic Area: Oncology Leads with Data Density, Neurology Fastest Growing

Oncology held 33.92% share in 2025, while neurology is forecast to grow at a 32.58% CAGR through 2031. The pharma predictive analytics market remains strongest in oncology because that field has the deepest concentration of structured multi-omics datasets, biomarker programs, and outcome-linked clinical evidence. Oncology also benefits from active regulatory interest in real-world evidence and accelerated evidence generation pathways. Neurology is growing faster because high unmet needs and complex disease heterogeneity make predictive tools more valuable in both development and patient monitoring.

A 2025 npj Digital Medicine study covering 146 multiple sclerosis centers in 32 countries, and 44,886 patients reports an ROC-AUC of 0.8398 for 2-year disability progression prediction under a federated learning framework. That result matters for the pharma predictive analytics market because it shows that complex neurological data can already support large-scale predictive modeling across institutions. In oncology, broader acceptance of real-world evidence continues to support advanced analytics use cases in trial design and post-approval evidence generation. This keeps oncology in the lead today while giving neurology one of the strongest future expansion paths in the pharma predictive analytics market.

By End User: Pharmaceutical Companies Anchor Share, CROs Drive Fastest Growth

Pharmaceutical companies held 48.75% share in 2025, while contract research organizations are projected to grow at a 33.74% CAGR through 2031. The pharma predictive analytics market still centers on pharmaceutical companies because they fund large enterprise deployments and invest directly in internal AI capabilities. Biotechnology companies are also increasing adoption, especially when smaller internal teams rely on external platforms to extend data science capacity. CROs are expanding faster because sponsors are outsourcing analytics-intensive work alongside traditional trial execution.

This is changing the structure of the pharma predictive analytics market because analytics capability is becoming part of CRO selection rather than an added service. In April 2026, Worldwide Clinical Trials and Medidata announced a strategic partnership to embed Medidata AI across the clinical trial lifecycle, which shows how CROs are moving toward deeper analytics integration even if the competitive field remains uneven. Smaller CROs without embedded analytics capability may face more pricing pressure as sponsors prefer providers that can combine execution, data management, and predictive modeling in one contract. This will likely support more capability partnerships and targeted consolidation across the pharma predictive analytics market.

Geography Analysis

North America accounted for 36.46% of the pharma predictive analytics market size in 2025. It remained the largest regional cluster because the region combines deep pharmaceutical R&D spending, broad real-world data assets, and earlier regulatory clarification around AI-supported evidence generation. The pharma predictive analytics market also benefits in North America from stronger institutional capacity to document, validate, and operationalize AI tools inside regulated drug development settings. FDA actions on AI in regulatory decision-making and real-world evidence have helped create a more usable compliance baseline for companies working across development and post-approval analytics. The main structural constraint across the region remains data interoperability because fragmented EHR networks still limit how easily sponsors and vendors can build high-quality datasets at scale.

Europe remains a significant center in the pharma predictive analytics market because the region combines advanced research clusters with a stricter compliance framework that raises the quality bar for enterprise platforms. The EU AI Act is increasing implementation burden, but it is also formalizing expectations around governance, transparency, and post-market oversight for high-risk AI systems. Germany, France, the United Kingdom, and Italy continue to anchor regional deployment through established biotech ecosystems and strong public-private research capacity. Europe's regulatory pathway is also becoming more operational, as the EMA issued its first qualification opinion on an AI methodology in 2025 for AIM-NASH in liver-biopsy image analysis.

Asia-Pacific is projected to grow at a 32.98% CAGR through 2031 and stands as the fastest-growing region in the pharma predictive analytics market. Growth is being driven by digital health mandates, industry-academic collaboration, and a broader push by domestic pharmaceutical companies to build stronger analytics capability. Japan, South Korea, and China account for most of the current activity. Takeda begins AI demand forecasting across around 100 products in August 2025, while South Korea is funding a 5-year AI drug development program, and China launched Fosun Pharma's PharmAID Decision Intelligent Agent Platform in February 2025, showing the range of regional deployment models. South America is still an earlier-stage opportunity, but outsourcing-led clinical activity is beginning to create demand for analytics infrastructure that can support future expansion in the pharma predictive analytics market.

Competitive Landscape

The pharma predictive analytics market shows moderate concentration at the enterprise tier, where IQVIA, Medidata Solutions, Oracle Health Sciences, and Optum benefit from established platforms, broad customer access, and integrated data environments. Beneath that layer, the pharma predictive analytics market remains fragmented across specialist vendors focused on federated learning, multimodal AI, pharmacovigilance, or disease-specific analytics. This mix creates a competitive structure where scale matters for enterprise accounts, but niche capability still matters in technical buying decisions. The result is a market where large platforms set broad standards while smaller firms compete through differentiated workflows and data assets.

One leading strategy in the pharma predictive analytics market is vertical integration. In March 2026, IQVIA launched IQVIA.ai with more than 150 intelligent agents and noted adoption by 19 of the top 20 pharmaceutical companies, which reinforces the value of combined platform depth and workflow reach. Another strategy is data exclusivity, as shown by ConcertAI's January 2026 integration of genomic and clinical records from 500,000 oncology patients with Foundation Medicine. Recursion represents a third path, where platform differentiation comes from an AI-native operating system tied directly to internal discovery workflows and scaled experimental data generation. These approaches are different in design, but all of them aim to raise switching costs and improve measurable return for pharmaceutical clients.

The pharma predictive analytics market still has clear white-space opportunities in pharmacovigilance automation, rare disease analytics, neurology-focused modeling, and federated real-world evidence platforms that can satisfy several jurisdictions at once. In April 2026, Parexel acquired Vitrana to strengthen patient safety automation, which shows that safety analytics remains a live investment area. In April 2026, Certara entered a definitive agreement to sell its regulatory and medical writing business to veristat. As governance standards rise, the pharma predictive analytics market is likely to see more consolidation because smaller vendors may find it harder to fund the validation, documentation, and compliance depth that enterprise buyers now expect.

Pharma Predictive Analytics Industry Leaders

Aetion

IQVIA

Medidata Solutions

Optum

Oracle Health Sciences

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Parexel acquired Vitrana, an AI-enabled, end-to-end pharmacovigilance technology platform, expanding Parexel's patient safety solutions with intelligent automation and AI capabilities applicable across pharmacovigilance, regulatory submissions, and clinical development.

- April 2026: Novo Nordisk and OpenAI announced a strategic partnership to integrate advanced AI across drug discovery, manufacturing, and commercial operations, with pilot programs expected across all functions by late 2026; the partnership specifically targets AI-driven patient stratification and biomarker discovery.

- April 2026: Certara entered a definitive agreement to sell its regulatory and medical writing business to Veristat for up to USD 135 million, sharpening its focus on model-informed drug development and AI-integrated modeling and simulation.

Global Pharma Predictive Analytics Market Report Scope

As per the scope of the report, pharma predictive analytics refers to the use of advanced statistical methods, artificial intelligence (AI), and machine learning (ML) to analyze pharmaceutical and healthcare data to predict future outcomes. It helps in forecasting drug development success, patient responses, clinical trial results, and disease progression. Leveraging data from sources like EHRs, clinical trials, and real-world evidence enables faster decision-making and improved R&D efficiency. Ultimately, it supports more accurate, cost-effective, and patient-centric drug development and commercialization strategies.

The pharma predictive analytics market is segmented by component, deployment, analytics type, technology, data source, application, therapeutic area, end user, and geography. By component, the market is segmented into software and services. By deployment, the market is segmented into on-premise and cloud-based. By technology, the market is segmented into artificial intelligence (AI) & machine learning (ML), natural language processing (NLP), big data analytics, and others. By data source, the market is segmented into electronic health records (EHRs), clinical-trial data, genomic data, claims & billing data, real-world evidence (RWE) data, and others. By application, the market is segmented into drug discovery & development, clinical-trial optimization, patient outcome prediction, pharmacovigilance & drug safety, precision medicine, and others. By therapeutic area, the market is segmented into oncology, cardiovascular diseases, neurology, infectious diseases, and others. By end user, the market is segmented into pharmaceutical companies, biotechnology companies, contract research organizations (CROs), and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers estimated market sizes and market trends for 17 countries across major regions worldwide. The report offers market value (in USD) for the above segments.

| Software |

| Services |

| On-Premise |

| Cloud-Based |

| Artificial Intelligence (AI) & Machine Learning (ML) |

| Natural Language Processing (NLP) |

| Big Data Analytics |

| Others |

| Electronic Health Records (EHRs) |

| Clinical-Trial Data |

| Genomic Data |

| Claims & Billing Data |

| Real-World Evidence (RWE) Data |

| Others |

| Drug Discovery & Development |

| Clinical-Trial Optimization |

| Patient Outcome Prediction |

| Pharmacovigilance & Drug Safety |

| Precision Medicine |

| Others |

| Oncology |

| Cardiovascular Diseases |

| Neurology |

| Infectious Diseases |

| Others |

| Pharmaceutical Companies |

| Biotechnology Companies |

| Contract Research Organizations (CROs) |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Software | |

| Services | ||

| By Deployment | On-Premise | |

| Cloud-Based | ||

| By Technology | Artificial Intelligence (AI) & Machine Learning (ML) | |

| Natural Language Processing (NLP) | ||

| Big Data Analytics | ||

| Others | ||

| By Data Source | Electronic Health Records (EHRs) | |

| Clinical-Trial Data | ||

| Genomic Data | ||

| Claims & Billing Data | ||

| Real-World Evidence (RWE) Data | ||

| Others | ||

| By Application | Drug Discovery & Development | |

| Clinical-Trial Optimization | ||

| Patient Outcome Prediction | ||

| Pharmacovigilance & Drug Safety | ||

| Precision Medicine | ||

| Others | ||

| By Therapeutic Area | Oncology | |

| Cardiovascular Diseases | ||

| Neurology | ||

| Infectious Diseases | ||

| Others | ||

| By End User | Pharmaceutical Companies | |

| Biotechnology Companies | ||

| Contract Research Organizations (CROs) | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is driving growth in pharma predictive analytics?

Growth is being supported by broader AI and ML use in discovery, rising regulatory acceptance of real-world data, and stronger precision medicine workflows that depend on multi-source modeling.

How large will pharma predictive analytics become by 2031?

The sector is forecast to reach USD 9.37 billion by 2031 from USD 2.09 billion in 2025, advancing at an 28.42% CAGR during 2026-2031.

Which deployment model is growing the fastest in pharmaceutical analytics platforms?

Cloud-based deployment is the fastest-growing model with a projected 29.36% CAGR through 2031, while on-premise still held the largest share in 2025.

Which application area currently generates the most revenue?

Clinical trial optimization led with a 32.95% share in 2025 because sponsors can link analytics directly to site selection, recruitment, and protocol efficiency.

Which therapeutic area offers the strongest current demand for predictive analytics tools?

Oncology held the largest share at 33.92% in 2025 because it has the densest combination of multi-omics data, biomarker programs, and outcome-linked evidence.

Which end-user group is adopting these tools the fastest?

CROs are projected to grow at a 33.74% CAGR through 2031 as sponsors increasingly outsource analytics-intensive functions along with trial execution.

Page last updated on: