PET Radiotracer Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

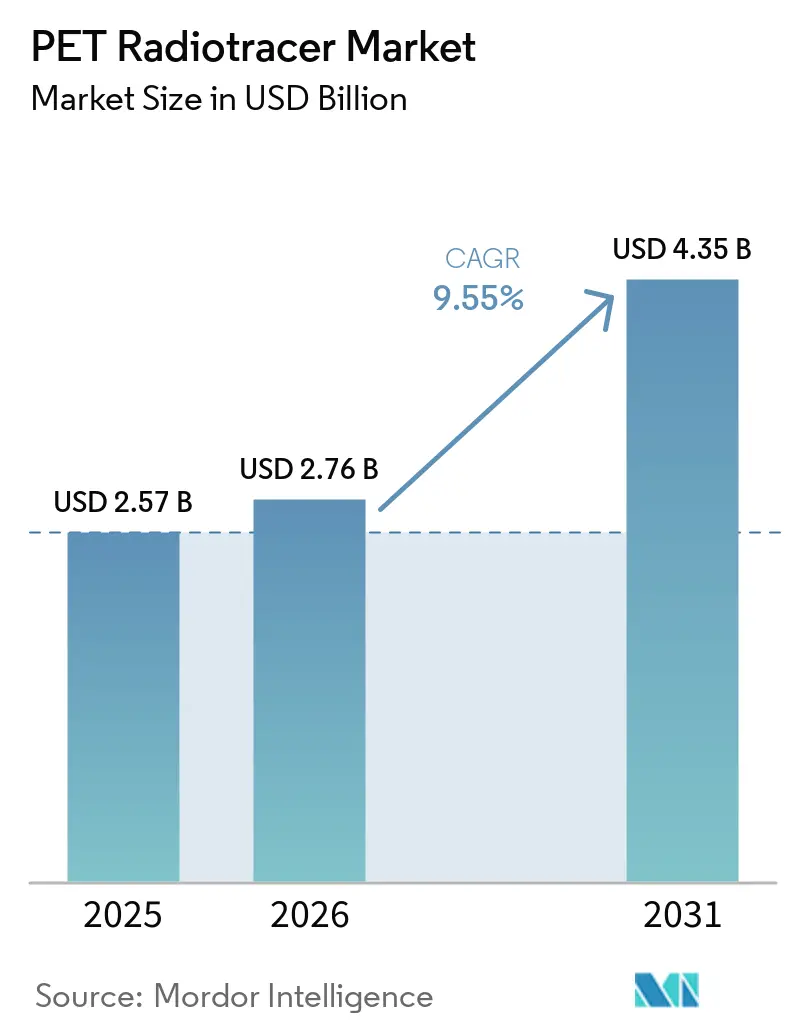

| Market Size (2026) | USD 2.76 Billion |

| Market Size (2031) | USD 4.35 Billion |

| Growth Rate (2026 - 2031) | 9.55% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

PET Radiotracer Market Analysis by Mordor Intelligence

The PET Radiotracer Market size is expected to grow from USD 2.57 billion in 2025 to USD 2.76 billion in 2026 and is forecast to reach USD 4.35 billion by 2031 at 9.55% CAGR over 2026-2031.

Policy reform in the United States that unbundled high-cost diagnostic radiopharmaceuticals above the payment threshold stabilized economic incentives for innovative tracers, enabling commercial models that persist beyond pass-through status and supporting broader access in outpatient settings. Clinical practice is shifting as oncology and neurology indications embed PET not only for diagnosis but also for treatment selection and longitudinal monitoring, illustrated by PSMA-PET and amyloid-PET use cases that are now prerequisites in many care pathways.

Supply-side investments by manufacturers and CDMOs, alongside generator and cyclotron technology advances, aim to close capacity gaps that have historically constrained distribution and scheduling flexibility for short half-life tracers. Consolidation and vertical integration strategies by leading radiopharmaceutical companies highlight a strategic pivot toward resilient isotope supply, last-mile distribution, and scalable manufacturing that together reinforce sustainable growth for the PET radiotracer market. Geographically, demand leadership in North America is complemented by rapid capacity buildouts and localization efforts in Asia-Pacific, which together reduce single-point failure risks and support faster adoption of new PET agents across high-burden disease areas.

Key Report Takeaways

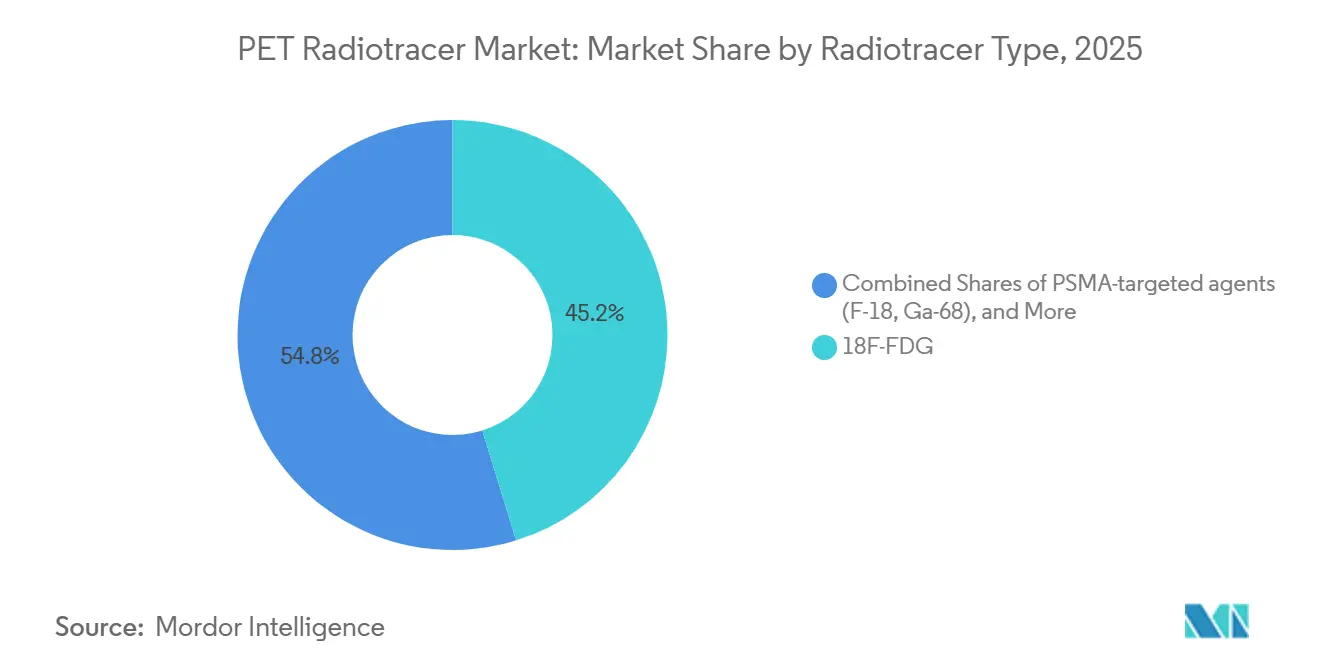

- By radiotracer type, 18F-FDG led with 45.22% revenue share in 2025, while PSMA-targeted agents are projected to expand at a 13.27% CAGR through 2031.

- By isotope, fluorine-18 commanded 67.51% share in 2025, and gallium-68 is set to grow at a 13.44% CAGR over 2026-2031.

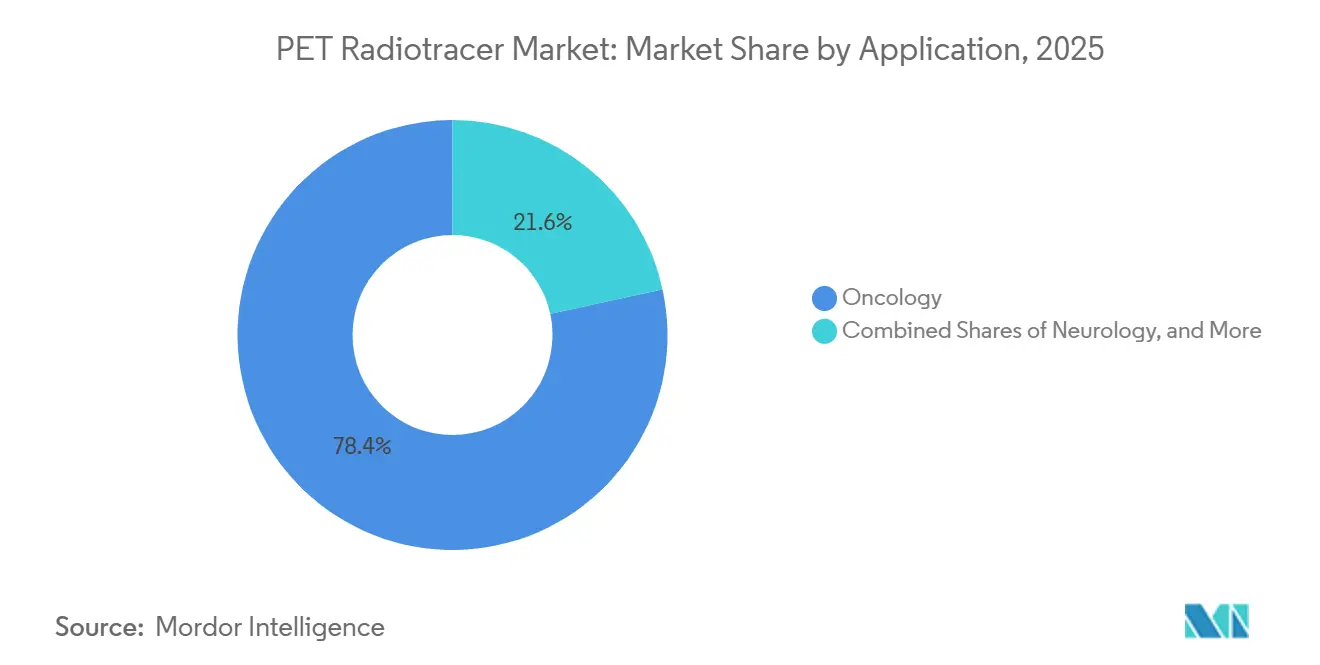

- By application, oncology accounted for a 78.43% share of the PET radiotracer market size in 2025 and is advancing at a 10.24% CAGR through 2031.

- By end user, hospitals held 56.21% share in 2025, while diagnostic imaging centers recorded the highest projected growth at a 9.94% CAGR to 2031.

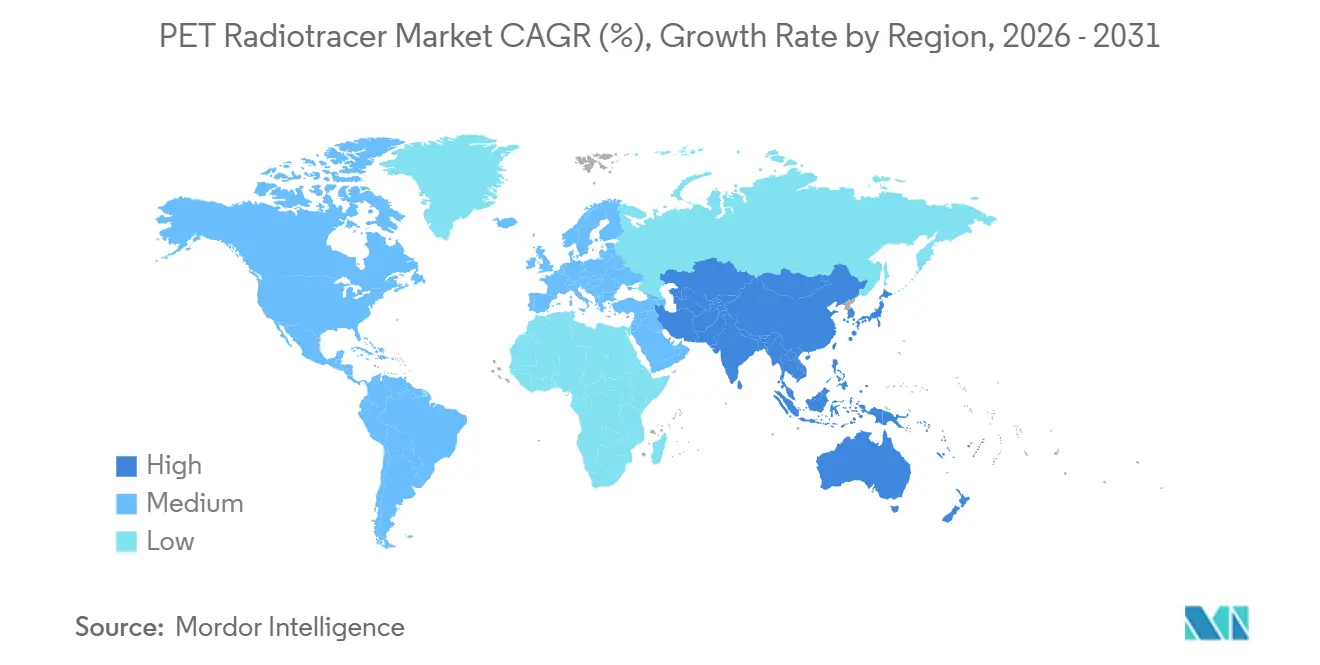

- By geography, North America represented 42.32% in 2025, and Asia-Pacific is forecast to grow at a 13.95% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global PET Radiotracer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Oncology Burden and PET Procedure Growth | +2.1% | Global, with concentrated demand in North America, Western Europe, and Asia-Pacific urban corridors | Short term (≤ 2 years) |

| US CMS Separate Payment Boosts Tracer Access | +1.8% | North America, with indirect influence on European private-payer models and APAC reimbursement benchmarking | Medium term (2-4 years) |

| PSMA-PET Adoption and Product Proliferation | +2.3% | Global, with accelerated adoption in APAC (Japan licensing deals, Korea KIRAMS trials, China clinical validation) | Short term (≤ 2 years) |

| Alzheimer's Care Pathways Expand Amyloid/tau PET | +1.5% | North America and Western Europe initially; gradual APAC diffusion pending local anti-Aβ therapy approvals | Medium term (2-4 years) |

| Consolidation and CDMO Capacity Expand Supply | +1.2% | Global, with concentrated deployment in U.S. (Nucleus, NorthStar, Evergreen), Belgium (SpectronRx), Japan (Telix Yokohama) | Long term (≥ 4 years) |

| Ga-68 Generator Access Enables Decentralized PET | +0.9% | APAC core (South Korea KAERI tech, Japan RIKEN), spill-over to Southeast Asia, Latin America, and African markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Oncology Burden and PET Procedure Growth

Rising cancer incidence, including a projected 334,000 new U.S. prostate cancer cases and more than 36,000 deaths in 2026, intensifies reliance on PET for staging, response assessment, and recurrence detection where other modalities have limitations. The ongoing integration of theranostic care models links diagnostic PSMA-PET and somatostatin receptor PET with radioligand therapies, which increases imaging frequency per patient as treatment pathways require confirmation scans. Evidence from the PSMAfore study supporting earlier PSMA-based therapy adoption and better radiographic progression-free survival has encouraged use of PET earlier in the disease trajectory.

In Asia-Pacific, the rapid buildout of cyclotrons and PET facilities, complemented by reactor-based lutetium-177 capacity in China, enhances availability for theranostic protocols. East Asian clinical experience showing 62.5% PSA response rates to PSMA radioligand therapy supports expanding adoption across diverse patient profiles.

US CMS Separate Payment Boosts Tracer Access

The U.S. policy to separate payment for diagnostic radiopharmaceuticals above the high-cost threshold, effective January 2025, restructured hospital outpatient economics and preserved product viability after pass-through, which reduces the historical volume cliff that discouraged innovation. The indexed threshold increased to USD 655 for 2026, reinforcing inflation protection and signaling stability in reimbursement design for premium PET tracers.

While CMS pays based on mean unit cost from hospital claims rather than average sales price, the decoupled payment approach curbs margin compression and sustains product availability in both hospitals and outpatient centers. Transitions from pass-through to regular payment can create rate volatility for lower-utilization products, yet the framework still improves access relative to prior bundled-payment dynamics. Over the medium term, private insurers and international payers are likely to study U.S. policy for reference, which may influence broader reimbursement benchmarks for the PET radiotracer market.

PSMA-PET Adoption and Product Proliferation

PSMA-PET became central to care pathways because approved PSMA radioligand therapies require imaging confirmation of target expression, which adds diagnostic volumes on top of existing use in staging and recurrence assessment. Piflufolastat F-18 surpassed 760,000 U.S. scans and gained FDA approval in March 2026 for a manufacturing-optimized formulation designed to raise batch sizes by about 50%, enabling wider geographic distribution from centralized cyclotrons. Competitive products using gallium-68 kits enable generator-based preparation with improved shelf life, which supports adoption in smaller hospitals that do not operate on-site cyclotrons. In Asia, licensing and local manufacturing moves, such as the Japan agreement to commercialize piflufolastat F-18, position faster uptake in a mature imaging ecosystem. Clinical response data from East Asian cohorts reinforce the real-world effectiveness of PSMA-directed strategies, which supports ongoing expansion of the PET radiotracer market in oncology.

Alzheimer’s Care Pathways Expand Amyloid/tau PET

In February 2026, FDA labeling updates authorized the use of florbetapir, flutemetamol, and florbetaben to select patients for anti-amyloid-beta therapies, which moved amyloid-PET from research use to routine clinical decision-making and treatment monitoring. Coverage policy changes have improved practical access, with Medicare transitioning amyloid-PET coverage to contractor discretion, which enables regional policy evolution while providers adapt operational workflows. MRI remains mandatory for ARIA surveillance during anti-amyloid treatment, but amyloid-PET is now central for confirming eligibility and establishing baseline pathology, which increases sustained imaging demand over multi-year courses.

Appropriate use criteria published in 2025 expanded scenarios where amyloid and tau PET are recommended, aligning clinical guidance with the availability of disease-modifying therapies. Tau-PET development, including MK-6240, indicates future roles in patient stratification as anti-tau agents progress in clinical development.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High PET/CT Capex and Siting Constraints | -0.7% | Emerging markets (Southeast Asia, Latin America, Sub-Saharan Africa) and smaller community hospitals in developed regions | Medium term (2-4 years) |

| Short Half-lives and Isotope/Parent Shortages | -1.1% | Global, acute in regions reliant on HFR Netherlands, BR-2 Belgium; U.S. domestic Mo-99 offset delayed to 2027 (SHINE)Global, acute where reactor outages coincide | Short term (≤ 2 years) |

| Staffing and GMP Compliance Bottlenecks | -0.9% | North America and, Western Europe (aging workforce, training program decline), Southeast Asia (infrastructure gaps), and parts of APAC | Long term (≥ 4 years) |

| Tariff/trade Uncertainties Raise Generator Input Costs | -0.5% | Primarily the European Union primarily (HALEU, enriched isotope dependencies); indirect pressure onwith global pricing structuresprice spillovers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High PET/CT Capex and Siting Constraints

PET/CT acquisition and installation budgets remain significant, which limits adoption in settings where throughput cannot meet return thresholds within standard equipment lifecycles. Facilities face additional costs for hot cells, cleanrooms, and compliance with GMP-grade manufacturing and handling standards, and these costs are coupled with licensing complexity across national regulatory bodies. Approval timelines, zoning restrictions, and community opposition can add to delays and create uneven geographic distribution of PET capacity. Analysis published in 2025 indicated that extending hours on short-axial-field-of-view scanners is less efficient than upgrading technology, but many providers still rely on extended hours due to capital constraints. Limited domestic production and uneven reimbursement environments in some countries exacerbate disparities in access, concentrating PET services in a few metropolitan corridors.

Short Half-lives and Isotope/Parent Shortages

Aging research reactors and maintenance overlaps can disrupt molybdenum-99 and technetium-99m supply chains, as seen during the 2024 HFR outage that combined with other maintenance windows to curtail supply for several weeks. Short half-lives prevent stockpiling, so disruptions quickly cascade into missed or deferred procedures. Global reviews emphasize the need for diversified production, streamlined regulation, and system readiness to reduce risks of recurrent supply gaps across medical radioisotopes. Options such as cyclotron-based gallium-68 production can complement generator reliance and mitigate some risks, although these solutions vary in feasibility across markets[2]International Atomic Energy Agency, “Cyclotron-based Gallium-68 for Cancer Detection,” IAEA, iaea.org. Reactor upgrades and new-build timelines extend into the next decade in parts of Europe, so near-term resilience leans on process efficiency, alternative production routes, and better outage coordination at the regional level.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Radiotracer Type: FDG Anchors Volume as PSMA Commands Premiums

Fluorine-18 FDG accounted for 45.22% share of the PET radiotracer market size in 2025, reflecting entrenched use across oncology, neurology, and cardiology and a large installed base of cyclotrons and PET/CT systems. FDG’s broad clinical applicability keeps baseline volumes steady, although growth rates are moderating as disease-specific agents expand in scenarios where glucose metabolism is less informative. PSMA-targeted agents are the fastest-growing radiotracer class at a 13.27% CAGR through 2031, as they serve both diagnostic and therapy-selection roles in prostate cancer pathways.

Piflufolastat’s trajectory, including an FDA-cleared manufacturing-optimized formulation in March 2026 that increases batch sizes by about 50%, supports broader geographic coverage from central production hubs[1]Lantheus Holdings, Inc., “Lantheus Announces FDA Approval of PYLARIFY TruVu (piflufolastat F 18) Injection,” GlobeNewswire, globenewswire.com. Generator-based gallium-68 kits enable same-day preparation with improved shelf life, which helps smaller hospitals without cyclotrons offer PSMA-PET imaging. East Asian evidence of strong PSA response to PSMA radioligand therapy, despite different genomic profiles compared with Western populations, supports a broadening addressable base for PSMA-driven diagnostic volumes.

Clinical workflow changes underscore why PSMA agents amplify demand rather than substitute for other tests in the PET radiotracer market. Each candidate for PSMA-directed therapy requires PET confirmation of target expression, which adds scans even when the diagnostic pathway is already in place. Competitive dynamics across four FDA-cleared PSMA agents collectively expand capacity and reach through differentiated formats and logistics, resulting in wider access and more flexible scheduling for providers. In parallel, somatostatin receptor tracers, amyloid agents, and bone tracers extend addressable uses in neuroendocrine tumors, Alzheimer’s disease, and metastatic surveillance. Pipeline activity in fibroblast activation protein and other targets may add future options across solid tumors, though near-term growth remains most intense in prostate cancer and neuroendocrine indications. Together, these trends reinforce diversified growth drivers across modalities for the PET radiotracer market.

By Isotope: Fluorine-18 Volume Dominance Meets Gallium-68 Growth

Fluorine-18 held 67.51% share in 2025 on the strength of FDG ubiquity and scale advantages in centralized cyclotron networks that serve regional imaging centers within the 110-minute half-life window. Hub-and-spoke production architectures enable redundancy and help providers manage scheduling risks for high-throughput sites in major metropolitan areas. Gallium-68 is the fastest-growing isotope class at a 13.4% CAGR through 2031, driven by generator-based access for PSMA and somatostatin receptor imaging where sites prefer flexible, on-demand preparation. Generator costs and supply constraints have been hurdles in some markets, though technological improvements and domestic generator initiatives are beginning to address longevity and efficiency.

Cyclotron-based gallium-68 production offers higher yields and regional distribution potential that can complement or replace generators in select geographies, subject to regulatory and process requirements[3]International Atomic Energy Agency, “Cyclotron-based Gallium-68 for Cancer Detection,” IAEA, iaea.org. Fluorine-18’s scale economics are reinforced by continuous investment in PET manufacturing infrastructure across growth corridors. Examples include multi-site PET network expansions and capacity additions that aim to reduce delivery lead times and increase supply resilience for high-demand tracers.

Ongoing isotope innovation, such as zirconium-89 for immuno-PET and copper-64 for theranostic pairs, diversifies the clinical toolkit and aligns with the shift toward precision oncology where imaging and therapy decisions are closely coupled. Localization of isotope production in Asia-Pacific further reduces import dependence and supports scalable commercial supply in large countries with rising PET volumes. These changes strengthen the PET radiotracer market by balancing centralized efficiency with decentralized access.

By Application: Oncology Supremacy Spans Diagnostics and Therapeutics

Oncology accounted for 78.43% of the PET radiotracer market share in 2025 and is expected to grow at a 10.24% CAGR through 2031, reflecting the addition of therapy-selection imaging on top of diagnostic use. PSMA-PET volumes have climbed as label expansions for radioligand therapy moved into earlier lines of treatment, which increases the number of patients requiring confirmation scans before therapy. Clinical evidence for improved progression-free survival has accelerated adoption, while high prostate cancer incidence in key markets ensures continued demand for precise staging and surveillance. Neuroendocrine tumors rely on somatostatin receptor imaging to inform lutetium-177 DOTATATE therapy, while FDG-PET remains valuable across many solid tumors for staging and response assessment. Emerging targets such as FAP and TROP-2 are under evaluation and may add incremental diagnostic options as data matures.

Neurology volumes are smaller but rising as amyloid-PET transitions into routine eligibility determination and monitoring for anti-amyloid therapies, which embeds PET into long-term care pathways. Tau-PET is moving toward potential approval, which could enable richer stratification for anti-tau clinical programs as those therapies advance. Cardiology continues to use PET for myocardial perfusion and viability under reimbursement policies that, in many cases, remain bundled for lower-cost tracers, which shapes the commercial outlook relative to oncology and neurology. Collectively, application dynamics show that therapy-linked imaging will remain a primary engine of growth for the PET radiotracer market.

By End User: Hospitals Anchor Share as Imaging Centers Accelerate

Hospitals held 56.21% share in 2025, supported by integrated PET/CT departments, on-site radiopharmacy capabilities, and multidisciplinary care pathways that rely on rapid imaging-to-treatment handoffs. High patient throughput and the ability to host cyclotrons or manage advanced generator systems reinforce the hospital role in same-day radiotracer preparation and administration for short half-life agents. Diagnostic imaging centers are the fastest-growing end-user group with a projected 9.94% CAGR through 2031, as separate payment for eligible tracers better aligns outpatient economics with the demands of modern radiopharmacy operations. Vertical integration moves by leading companies, including acquisitions of radiopharmacy networks and isotope platforms, target last-mile control and improved scheduling reliability for freestanding centers.

Network expansions across the United States and Asia-Pacific are designed to increase site density within viable distribution radii for fluorine-18 and to broaden access for gallium-68 generator users. In Japan, manufacturing footprints are being developed to support one of the world’s largest nuclear medicine markets and to ensure reliable supply to imaging centers and hospitals. These operational shifts support the long-term movement of routine PET imaging toward outpatient settings while hospitals concentrate on complex cases, acute care needs, and research-linked procedures. Together, these end-user trends improve capacity utilization and reinforce sustained growth for the PET radiotracer market.

Geography Analysis

North America led with 42.32% in 2025, supported by multiple FDA approvals, clear reimbursement frameworks, and recent capacity investments across CDMOs and radiopharmacies that together add meaningful throughput and resilience. The region has also seen substantial M&A in radiopharmaceuticals, which strengthens integrated supply chains and scales commercial infrastructure to handle growing volumes of PSMA and amyloid imaging. Ongoing policy refinements in Medicare outpatient payment systems sustain economic incentives for high-value tracers, and that environment continues to influence private payer decisions and facility planning. The concentration of clinical trial activity and a large installed base of PET/CT scanners also support continued leadership of the PET radiotracer market in North America.

Asia-Pacific is the fastest-growing region with a 13.95% CAGR through 2031, driven by the localization of isotope production, the expansion of PET manufacturing networks, and high-density healthcare infrastructure in countries like Japan and South Korea. Japan’s mature ecosystem for nuclear medicine, combined with recent licensing and manufacturing agreements, positions rapid adoption for PSMA and neurology-focused tracers as regulatory pathways mature. In South Korea, domestic production initiatives for multiple isotopes, including advances in gallium-68 generator technology, aim to reduce import reliance and broaden access for mid-tier hospitals. China’s reactor-based lutetium-177 batch production provides strategic support for regional theranostic adoption and reduces exposure to overseas supply constraints. Together, these developments reinforce a multi-country expansion where the PET radiotracer market size for Asia-Pacific is set to accelerate over the forecast horizon.

Europe continues to address structural vulnerabilities linked to aging reactors, transport logistics, and enriched material dependencies, while also investing to expand domestic production and harmonize regulatory frameworks for radiopharmaceuticals. EU-level recommendations seek to diversify raw material supply, improve certification processes, and continue strategic initiatives to build a more resilient supply chain. New capacity additions from industry players, including expanded PET networks in Western Europe, aim to enhance reliability of tracer supply for oncology, neurology, and cardiology programs.

In South America, regional collaboration programs that emphasize capacity building, quality systems, and training are designed to improve availability and foster adoption of theranostics, while targeted national approvals streamline market entry for select radiopharmaceuticals. These regional moves, along with agency guidance and industry investment, help sustain momentum for the PET radiotracer market.

Competitive Landscape

Competition in diagnostics features multiple approved PSMA-PET agents that expand access and diversify logistics options, while radioligand therapeutics exhibit more concentrated shares under a smaller set of sponsors. Lantheus has repositioned toward PET diagnostics while divesting legacy SPECT assets, a strategy supported by acquisitions that add amyloid and theranostic-enabling platforms and by operational focus on high-value tracers. Its March 2026 FDA approval for a manufacturing-optimized formulation of piflufolastat F-18 demonstrates emphasis on supply scalability and geographic reach from central cyclotrons. The company’s portfolio strategy aligns with continued growth in theranostic-linked indications and neurology imaging.

Telix has pursued vertical integration by adding isotope production technologies and acquiring a large U.S. radiopharmacy network, aiming to control upstream inputs and last-mile delivery that are critical for reliable PET supply. This approach strengthens scheduling reliability for hospitals and imaging centers while enabling rapid deployment of production methods for zirconium-89, gallium-68, and copper-64. GE HealthCare has advanced into radiopharmaceutical commercialization in Japan through licensing and acquisitions, leveraging an installed imaging hardware base to accelerate tracer penetration and enhance scanner utilization.

Large pharmaceutical companies expanded into radiopharmaceuticals via major acquisitions, which builds therapeutic portfolios that can pair with diagnostic PET strategies. AstraZeneca’s agreement to acquire Fusion and BMS’s completion of the RayzeBio acquisition indicate top-tier commitment to alpha- and beta-emitting therapies in oncology. European producers expanded PET footprints to increase site density and reduce delivery risk for short half-life agents, which enhances resilience and strengthens CDMO partnerships[4]Curium Pharma, “Nucleis Acquisition,” Curium Pharma, curiumpharma.com. These strategic moves collectively reinforce supply chains and integration across discovery, production, and distribution, which in turn supports durable growth for the PET radiotracer market.

PET Radiotracer Industry Leaders

Siemens Healthineers AG

Cardinal Health

Curium

Jubilant Radiopharma

China lsotope & Radiation Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Lantheus received FDA approval for PYLARIFY TruVu (piflufolastat F-18 injection), a manufacturing-optimized formulation of its fluorine-18 PSMA-PET tracer engineered to increase batch sizes approximately 50% and enhance radioactive concentration, enabling larger-geography coverage from centralized cyclotron production sites despite fluorine-18's 110-minute half-life.

- September 2025: Lantheus Holdings and GE HealthCare announced exclusive licensing agreement for GE to develop, manufacture, and commercialize piflufolastat F-18 (PYLARIFY) in Japan.

Global PET Radiotracer Market Report Scope

As per the scope of the market, PET radiotracers are radioactive pharmaceutical agents used in Positron Emission Tomography (PET) imaging to visualize metabolic and molecular activities within the body. These tracers contain a positron‑emitting radioisotope linked to a biologically active molecule and are administered intravenously under medical supervision for disease diagnosis, staging, and treatment monitoring, primarily in oncology, neurology, and cardiology.

The PET Radiotracer Market Report segments the market by radiotracer type, including 18F‑FDG, PSMA‑targeted agents (F‑18 and Ga‑68), somatostatin receptor agents (Ga‑68 DOTATATE/DOTATOC/DOTANOC), amyloid agents (F‑18 florbetapir, flutemetamol, florbetaben), 18F‑NaF, and others such as neurology amino‑acid tracers and inflammation and infection tracers. The market is further categorized by isotope, covering fluorine‑18, gallium‑68, carbon‑11, zirconium‑89, copper‑64, and other isotopes including oxygen‑15, nitrogen‑13, and rubidium‑82. By application, the market includes oncology, neurology, cardiology, and others, such as inflammation and infection imaging, drug development, and theranostic selection, while end users comprise hospitals, diagnostic imaging centers, and others, including academic and research institutes and nuclear medicine clinics. Geographically, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| 18F-FDG |

| PSMA-targeted Agents (F-18, Ga-68) |

| Somatostatin Receptor Agents (Ga-68 DOTATATE/DOTATOC/DOTANOC) |

| Amyloid Agents (F-18 florbetapir, flutemetamol, florbetaben) |

| 18F-NaF |

| Others (Neurology Amino-Acid Tracers, Inflammation & Infection Tracers) |

| Fluorine-18 |

| Gallium-68 |

| Carbon-11 |

| Zirconium-89 |

| Copper-64 |

| Others (Oxygen-15, Nitrogen-13, Rubidium-82, etc) |

| Oncology |

| Neurology |

| Cardiology |

| Others (Inflammation & Infection, Drug Development & Theranostic Selection) |

| Hospitals |

| Diagnostic Imaging Centers |

| Others (Academic & Research Institutes, Nuclear Medicine Clinics) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Radiotracer Type | 18F-FDG | |

| PSMA-targeted Agents (F-18, Ga-68) | ||

| Somatostatin Receptor Agents (Ga-68 DOTATATE/DOTATOC/DOTANOC) | ||

| Amyloid Agents (F-18 florbetapir, flutemetamol, florbetaben) | ||

| 18F-NaF | ||

| Others (Neurology Amino-Acid Tracers, Inflammation & Infection Tracers) | ||

| By Isotope | Fluorine-18 | |

| Gallium-68 | ||

| Carbon-11 | ||

| Zirconium-89 | ||

| Copper-64 | ||

| Others (Oxygen-15, Nitrogen-13, Rubidium-82, etc) | ||

| By Application | Oncology | |

| Neurology | ||

| Cardiology | ||

| Others (Inflammation & Infection, Drug Development & Theranostic Selection) | ||

| By End User | Hospitals | |

| Diagnostic Imaging Centers | ||

| Others (Academic & Research Institutes, Nuclear Medicine Clinics) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the PET radiotracer market?

The PET radiotracer market size is projected to expand from USD 2.57 billion in 2025 and USD 2.76 billion in 2026 to USD 4.35 billion by 2031, registering a 9.55% CAGR between 2026 and 2031.

Which applications are driving the fastest demand increase?

Oncology drives the largest and fastest growth, accounting for 78.43% in 2025 and advancing at a 10.24% CAGR through 2031, as PSMA-PET becomes central to therapy selection and monitoring.

Which region will see the fastest expansion through 2031?

Asia-Pacific is the fastest-growing geography with a projected 13.95% CAGR through 2031, supported by localization of isotope production, PET network expansion, and strong hospital infrastructure.

Which tracer types and isotopes will lead growth?

PSMA-targeted agents lead growth at a 13.27% CAGR among tracer types, and gallium-68 leads among isotopes at a 13.44% CAGR through 2031, propelled by generator access and kit-based convenience.

How does U.S. reimbursement policy affect adoption?

The CMS separate payment for eligible high-cost diagnostic radiopharmaceuticals sustains post pass-through viability, improving access and encouraging outpatient PET adoption.

What supply-side actions are companies taking to support growth?

Companies are scaling CDMO capacity, localizing isotope production, and vertically integrating radiopharmacies and isotope platforms to improve reliability and last-mile delivery to imaging sites.

Page last updated on: