Pet Food Machinery Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 4.75 Billion |

| Market Size (2031) | USD 6.20 Billion |

| Growth Rate (2026 - 2031) | 5.47% CAGR |

| Fastest Growing Market | Asia |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pet Food Machinery Market Analysis by Mordor Intelligence

The pet food machinery market is projected to grow from USD 4.50 billion in 2025 and USD 4.75 billion in 2026 to USD 6.20 billion by 2031, registering a CAGR of 5.47% between 2026 and 2031. The market is currently in a replacement and expansion cycle that followed the sharp rise in pet adoption. Demand is also shifting from standard dry kibble toward wet, fresh, premium, and therapeutic formats, increasing the need for processing lines with tighter control, better hygiene, and greater flexibility. Larger plant scales are also supporting market growth, where incremental improvements in line efficiency, waste reduction, and contamination control can justify capital spending decisions. The supplier base remains broad, leaving room for mid-sized and specialist providers to win projects based on format, process requirements, and service capability. The strongest opportunities are anticipated where premiumization, automation, hygienic design, and outsourced manufacturing models are expanding simultaneously.

Key Report Takeaways

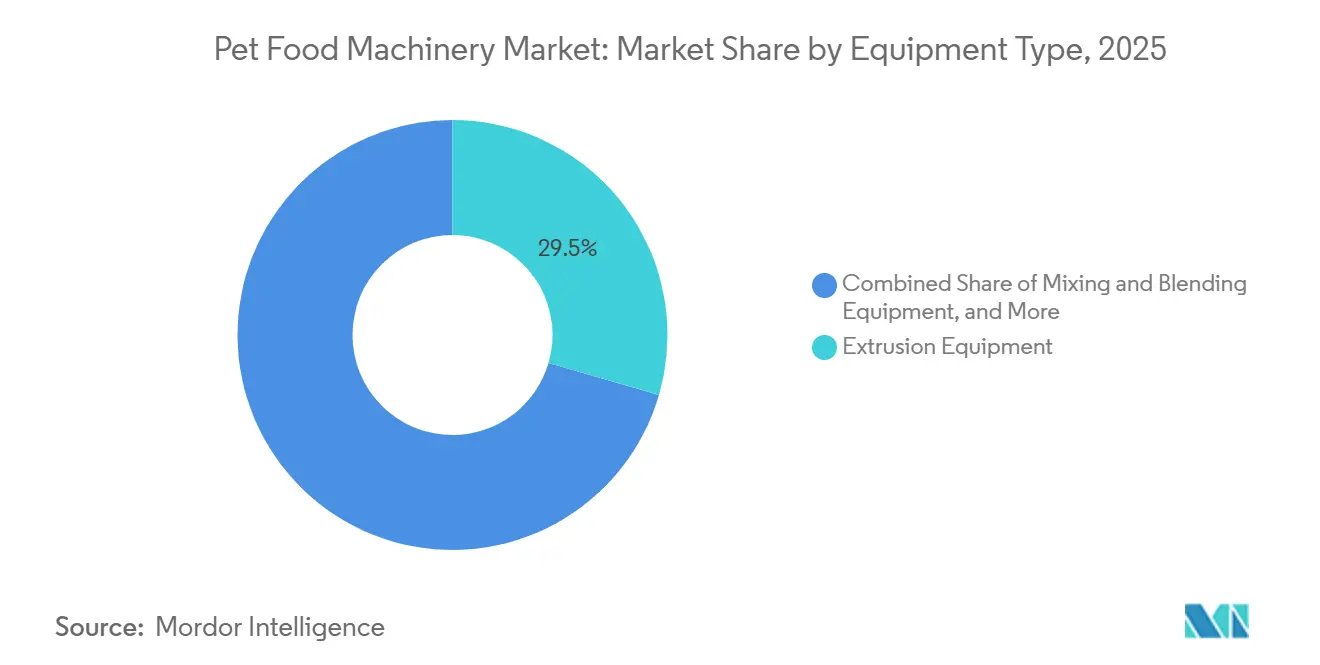

- By equipment type, extrusion equipment was the largest segment and, held 29.5% of the pet food machinery market share in 2025, while packaging equipment is the fastest-growing segment and is anticipated to expand at an 8.5% CAGR between 2026 and 2031.

- By process type, dry pet food processing lines were the largest segment, and held 41.2% of the pet food machinery market size in 2025, while veterinary diet processing lines are the fastest-growing segment and are anticipated to expand at a 9.4% CAGR between 2026 and 2031.

- By output format, kibbles were the largest segment and held 38.0% of the market share in 2025, while pet veterinary diets are the fastest-growing segment and are projected to expand at a 9.0% CAGR between 2026 and 2031.

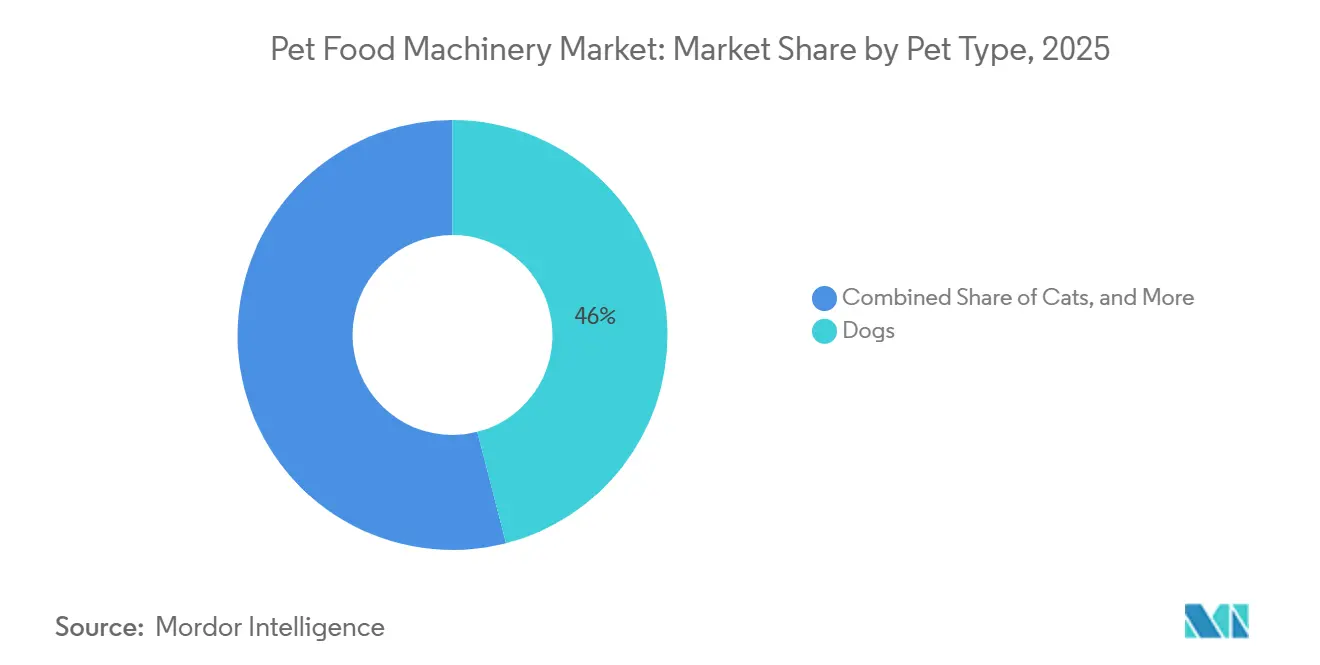

- By pet type, dogs were the largest segment and held 46.0% of the market share in 2025, while cats are the fastest growing segment and are anticipated to expand at a 9.2% CAGR between 2026 and 2031.

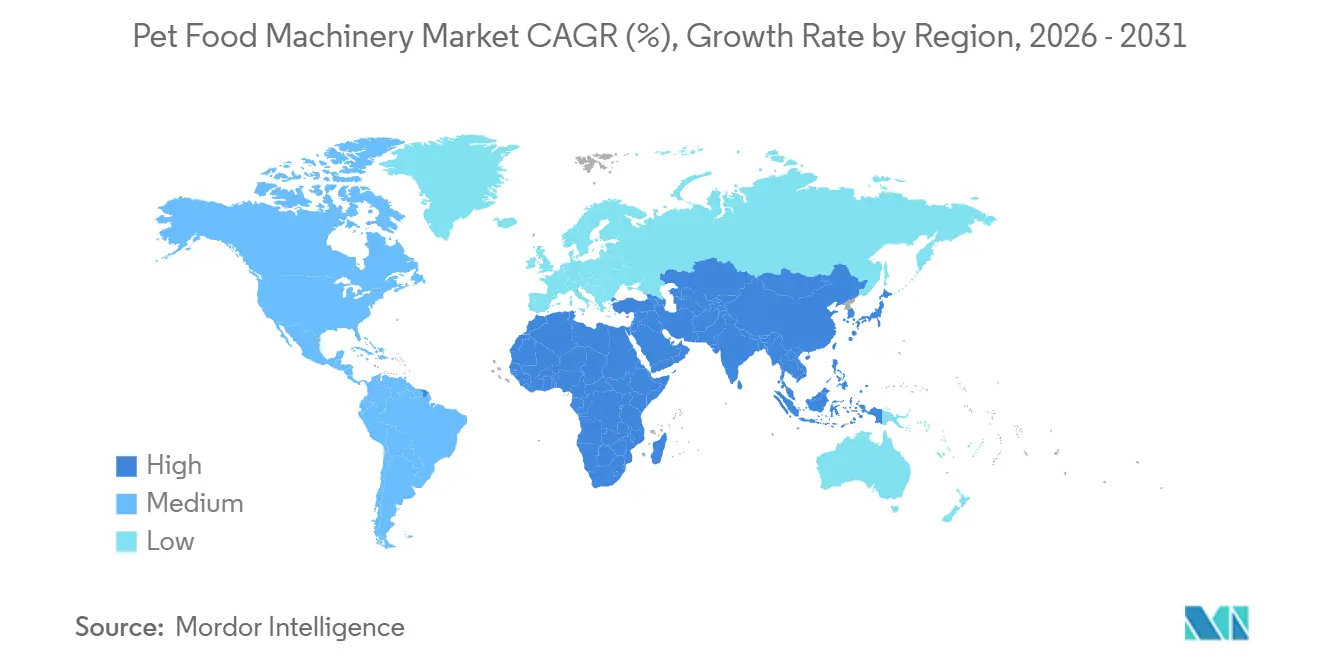

- By geography, North America was the largest segment and held 33.0% of the market size in 2025, while Asia is the fastest growing segment and is anticipated to expand at a 7.4% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Pet Food Machinery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premiumization of pet food production | +1.1% | Global, with peak intensity in Asia-Pacific and North America | Medium term (2-4 years) |

| Growth in functional and therapeutic pet food output | +0.9% | North America, with expansion into Europe and Asia-Pacific | Short term (≤ 2 years) |

| Automation demand to reduce recipe changeover losses | +1.0% | North America and Europe, spillover to Asia-Pacific | Long term (≥ 4 years) |

| Sustainability pressures on energy and water intensive lines | +0.7% | Europe core, spreading to North America and Asia-Pacific | Medium term (2-4 years) |

| Expansion of high-mix private label and contract manufacturing | +0.7% | Asia-Pacific, North America | Medium term (2-4 years) |

| Demand for hygienic, traceable, and low-contamination processing | +0.8% | Europe and North America, spillover to global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Premiumization of Pet Food Production

The pet food machinery market is being driven by the shift toward premium and super-premium products across major pet food categories. Premium lines require tighter process control, more frequent recipe changes, and stricter hygiene standards than standard kibble lines. As a result, producers are upgrading equipment specifications across intake, mixing, extrusion, drying, and coating stages. The Pet Food Institute reported in its 2025 production and ingredient analysis that demand for marine ingredients rose 95.0% and meat and poultry ingredients rose 34.0% between 2019 and 2024, reflecting the increasingly complex ingredient handling requirements in the pet food machinery market[1]Source: Pet Food Institute,“3 Key Takeaways from the 2025 Pet Food Production and Ingredient Analysis Report,” petfoodinstitute.org. This shift affects not only ingredient costs and product positioning, but also the frequency of plant recalibration and lot separation management. As premium portfolios expand, the pet food processing market is seeing growing interest in flexible lines that can maintain quality during shorter production runs and more frequent changeovers.

Growth in Functional and Therapeutic Pet Food Output

The market is also gaining support from the rise of functional and therapeutic products that require more controlled manufacturing conditions. Veterinary diets and nutritionally targeted products are moving from a narrow specialty position into broader retail and veterinary channels, lifting demand for precision coating, controlled drying, and segregated production environments. These formats often require post-extrusion application of heat-sensitive ingredients, along with improved documentation and validation at each production step. This shift affects capital planning, as producers increasingly need dedicated or semi-dedicated lines rather than shared-use infrastructure. In the pet food machinery market, this raises equipment intensity per stock-keeping unit and supports spending on systems designed for consistent formulation accuracy and contamination control.

Automation Demand to Reduce Recipe Changeover Losses

A stronger demand for automation is being seen as manufacturers seek to reduce losses associated with frequent recipe changes. A 2026 industry report from the Processing and Packaging Machinery Association (PMMI) and the Food Processing Suppliers Association (FPSA) showed that the United States animal feed and pet food processing machinery segment reached USD 329.0 million in, reflecting steady investment in processing upgrades[2]Source: Pet Food Processing Article,“SOTI Report: What’s driving processing investments?,” petfoodprocessing.net. In practical terms, automation is now driven less by labor replacement alone and more by yield protection, traceability, and reduced startup waste. Plants with a high product mix incur time-and-material costs during transitions, and these costs become more visible as premium and therapeutic portfolios expand. The market is therefore shifting toward control systems that help operators stabilize settings faster and more consistently reproduce validated production conditions.

Sustainability Pressures on Energy and Water Intensive Lines

The market is increasingly shaped by sustainability targets related to water use, cleaning cycles, waste reduction, and energy intensity. This is particularly relevant in wet, hygiene-sensitive production environments, where cleaning time and startup losses can materially affect costs and regulatory compliance. In May 2026, Bühler Group stated that its Nutrex 7 Series included Cleaning Lance and StepFlow functions, with early adopters reporting cleaning time reductions of 50.0% and waste reductions of up to 30.0% during startup and shutdown cycles[3]Source: Media Release,“Bühler ushers in a new era of extrusion systems with Nutrex 7 Series,” buhlergroup.com. These features are relevant because producers seek capacity gains without increasing utility loads or waste streams. In the market, sustainability requirements are increasingly factored into equipment selection rather than treated as a secondary benefit.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost of integrated processing lines | -0.6% | North America and Europe, with spread to Asia-Pacific | Medium term (2-4 years) |

| Skilled technician shortage for advanced automation systems | -0.5% | North America core, mirrored in parts of Europe | Long term (≥ 4 years) |

| Plant downtime risk during retrofitting and format switching | -0.4% | Europe, with impact across North America | Short term (≤ 2 years) |

| Ingredient variability increases equipment calibration complexity | -0.3% | Asia-Pacific, secondary impact in global markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Integrated Processing Lines

The high cost of complete processing lines remains a significant barrier in the pet food machinery market. Integrated systems that combine mixing, extrusion, drying, coating, and packaging require capital commitments that many mid-sized producers cannot easily approve, particularly in regions or channels where premium demand is still developing. This challenge is more pronounced in wet and hygienic formats, where cleaning systems, material selection, and layout design can substantially increase project costs. As a result, adoption slows in price-sensitive markets, pushing early-stage brands toward outsourced manufacturing rather than direct ownership. In the market, this cost barrier extends sales cycles and keeps many projects focused on staged upgrades rather than full-line replacements.

Skilled Technician Shortage for Advanced Automation Systems

The market also faces a shortage of technicians capable of operating, maintaining, and troubleshooting advanced automated systems. Digital controls, recipe management tools, and integrated hygiene features deliver value only when plant teams can use them consistently under commercial conditions. Some facilities can justify the equipment cost but still face challenges with commissioning depth, service response times, and internal skill transfer after installation. This makes buyers more cautious when comparing advanced solutions with simpler platforms, even when long-term economics favor automation. This labor constraint can slow the transition from mechanical upgrades to full digital process management.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Extrusion Leads as Hygienic Design Reshapes Procurement Standards

Extrusion equipment held 29.5% of the pet food machinery share in 2025, making it the largest equipment category. This position reflects the installed base supporting dry kibble production, which continues to anchor global pet food production and drives replacement demand, service revenue, and upgrade activity. Extrusion remains a central processing step in the market because it determines density, texture, cooking performance, and product consistency across mainstream formats. Even as product portfolios evolve, most manufacturers continue to view extrusion as the process stage where improvements in control and hygiene most directly influence downstream performance.

Packaging equipment is projected to grow at an 8.5% CAGR between 2026 and 2031, making it the fastest-growing equipment sub-segment. Growth in wet, premium, fresh-like, and single-serve products is driving demand for different seal types, material handling systems, and final pack configurations. Mixing and blending equipment remained the second-largest category in 2025, supporting both wet food preparation and precise ingredient incorporation for functional products. Automation and control systems are expanding from a smaller base as manufacturers place greater emphasis on traceability, repeatability, and reduced changeover losses. Grinding and milling equipment also remains relevant, as novel proteins and varied ingredient sizes require more controlled particle preparation before thermal processing.

By Process Type: Dry Lines Hold the Majority While Veterinary Diet Lines Accelerate

Dry pet food processing lines accounted for 41.2% of the pet food machinery market size in 2025, reflecting the size and maturity of global kibble capacity. This position is supported by the long operating life of installed dry lines, as producers often prefer retrofits and component upgrades over full conversion to other process configurations. The market retains a strong installed-base logic in dry processing, where line familiarity, throughput stability, and broad product compatibility remain relevant. Dry systems also continue to anchor many service and aftermarket relationships, given their central role in the category.

Veterinary diet processing lines are anticipated to expand at a 9.4% CAGR between 2026 and 2031, making them the fastest-growing process type. These lines require tighter process segregation, controlled coating steps, and more rigorous hygiene discipline than standard shared-use operations. Wet pet food processing lines are also growing, as premiumization is expanding demand for moist formats, even though dry processing remains dominant by installed capacity. Treats processing lines form a separate procurement stream, as forming, baking, cooling, and texture requirements differ materially from core kibble operations. Across the pet food machinery market, the growth of specialized lines is increasing the value of plants that can support different thermal profiles and product integrity requirements within the same site.

By Output Format: Kibbles Anchor the Base While Pet Veterinary Diets Drive Growth

Kibbles accounted for 38.0% of the pet food machinery market in 2025, maintaining their lead by output format. This position is supported by the existing base of single-screw and twin-screw extruders already optimized for direct-expanded and post-die-formed kibble production. Kibble remains the base format in the pet food machinery market, as it supports large, repeatable production runs across dog and cat food programs. This makes kibble-related equipment demand more stable than demand tied to newer formats, even as investment increasingly shifts toward higher-value niches.

Pet veterinary diets are anticipated to grow at a 9.0% CAGR between 2026 and 2031, placing them at the forefront of output-format expansion. These formulations require more controlled coating, validated kill steps, and cleaner process separation than standard products, which can drive equipment spending per line higher. Freeze-dried and jerky products are also outperforming because they rely on different equipment sets, making demand additive rather than a direct substitute for conventional extrusion lines. Canned and wet food formats are attracting a larger share of new-capacity decisions as premium and humanization trends continue to advance. Pet nutraceutical and supplement products are also appearing more frequently in machinery plans, as they require dosing, handling, and process consistency that traditional pet food lines may not provide.

By Pet Type: Dog Food Equipment Sets the Base While Cat Food Raises Flexibility Needs

Dogs accounted for 46.0% of the market share in 2025, making dogs the largest pet type segment. This share reflects both the size of the dog population and the larger average feed volumes per animal, which support high-volume production systems and steady replacement demand. Dog food lines, particularly in extrusion, drying, and coating, therefore contribute significantly to the installed-base stability of the pet food machinery market. This also explains why major original equipment manufacturers (OEMs) continue to view dog-related capacity as a core anchor for equipment utilization and aftermarket service.

Cat food is anticipated to expand at a 9.2% CAGR between 2026 and 2031, making it the fastest-growing pet type segment within the pet food machinery market. Nestlé opened a dedicated wet cat food facility in Rayong, Thailand, with an investment of USD 144 million (THB 5 billion), targeting markets in Asia-Pacific, Oceania, and Africa, which illustrates how cat-focused wet processing is attracting dedicated capital. Cat food innovation cycles are accelerating as wet, single-serve, and therapeutic formats gain traction in this category. This shortens the practical lifespan of lines that lack format flexibility. As a result, the market is seeing increased demand for systems capable of switching recipes, package styles, and moisture profiles with minimal disruption.

Geography Analysis

North America accounted for 33.0% of the market share in 2025, making it the largest regional market. The region benefits from a large premium pet food base, established manufacturing infrastructure, and consistent spending on replacement, expansion, and modernization. The North American market also benefits from deep supplier relationships, where large plants require not only equipment delivery but also service support, digital controls, and compliance-ready designs. These factors support a higher-value equipment mix compared to regions that are still in earlier stages of commercial development.

Asia-Pacific is anticipated to expand at a 7.4% CAGR between 2026 and 2031, making it the fastest-growing geography. Growth is driven by expanding commercial pet food manufacturing across China, Japan, India, and Southeast Asia, where rising pet ownership is shifting demand toward organized and branded formats. Thailand is emerging as a regional export base for pet food manufacturing, supporting stronger demand for modern wet and dry processing systems. In 2026, CPM Holdings, Inc.commissioned a TwinTech extrusion system for Shengmeng in Hebei Province, marking the Chinese producer's entry into commercial pet food manufacturing. This type of project indicates that the pet food machinery market in Asia-Pacific is expanding not only through local consumption, but also through new industrial capacity built around export and premium product requirements.

Europe remains an important market for pet food processing equipment, with activity largely tied to replacement, hygiene upgrades, and export-oriented original equipment manufacturers (OEM) manufacturing. Buyers in the region place significant emphasis on sanitary engineering, traceability, and durable design, which supports higher average equipment specifications. South America is gaining relevance as Brazil anchors regional production demand and suppliers establish commercial presence in the region. The Middle East and Africa remain smaller in absolute value but are attracting attention as first-generation large-scale facilities begin to appear. Overall, the pet food machinery market is expanding geographically, with mature regions focused on upgrades and emerging regions focused on foundational capacity buildouts.

Competitive Landscape

The market is moderately fragmented, with the top five players accounting for a moderate share of revenue in 2025. No single company controls the market, and project wins depend heavily on application fit, installed-base relationships, and service capability. The remaining market share is distributed across a wide range of regional and specialist suppliers, keeping the competitive landscape open and preventing any one player from setting terms across the full market. Competition is shifting away from throughput alone and toward system integration, hygiene performance, and digital control depth, reflecting the growing complexity of customer requirements in both dry and wet pet food production.

Bühler Group has stated its intention to standardize all machine and plant control systems on a single platform by 2030, signaling a move toward stronger digital lock-in and service continuity across its installed base. In April 2026, JBT Marel Corporation announced that Wenger and Extru-Tech would appear jointly under the JBT Marel brand at Petfood Forum 2026, demonstrating how the combined business is consolidating extrusion, high-pressure processing, and steam tunnel cooking under one offering. Buyers are responding positively to these platform strategies, as they increasingly prefer suppliers capable of supporting multiple processing steps and offering broader technical accountability. ANDRITZ AG is reinforcing its position through hygienic design and density control features, while CPM Holdings, Inc. is strengthening its role through integrated processing systems and wider support coverage. Clextral remains relevant in twin-screw extrusion for premium applications, and FAMSUN Group maintains a presence in Asian markets where feed-to-pet-food integration is expanding.

Below the top tier, the market still offers room for specialists and targeted suppliers. These companies compete where customers require focused expertise in grinding, conveying, turnkey plant design, or regional service rather than a full global platform. The broad field of active suppliers sustains price competition while also giving buyers flexibility to assemble line solutions by process stage. At the same time, the requirements for winning premium and regulated projects are rising, as customers increasingly demand digital traceability, cleanability, and validated process control within the same proposal. The market remains fragmented even as the leading players work to extend their advantage through bundled technology and recurring service offerings.

Pet Food Machinery Industry Leaders

GEA Group Aktiengesellschaft

Bühler AG (Bühler Group)

ANDRITZ AG

Clextral SAS (Legris Industries Group)

CPM Holdings, Inc. (Rosebank Industries plc )

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: CPM Holdings, Inc. acquired CFE Group Limited, its long-standing Europe, Middle East and Africa (EMEA) partner specializing in aftermarket services, refurbishment, and technical support. The acquisition strengthens CPM Holdings, Inc. aftermarket and refurbishment presence across the Europe, Middle East, and Africa region, adding die and roller shell refurbishment capabilities alongside local service infrastructure.

- April 2026: Wenger Manufacturing and Extru-Tech exhibited jointly under JBT Marel at Petfood Forum 2026 in Kansas City, United States for the first time, unveiling the PetFlex twin-screw extrusion platform and positioning the combined entity as a comprehensive provider spanning extrusion, high-pressure processing, and steam tunnel cooking.

- November 2025: Transavia SA, Romania's leading poultry producer, announced a USD 162 million (EUR 150 million) investment in the largest pet food factory in Romania, located in Ciugud, Alba County, with equipment installation scheduled to begin in early 2026 and production commencing in the second half of 2026.

Global Pet Food Machinery Market Report Scope

Pet food machinery involves the industrial equipment and systems used to process pet food products across dry, wet, treats, nutraceutical, and veterinary diet applications for pets. The process includes grinding, mixing, extrusion, drying, coating, automation, and packaging to support product safety, hygiene, traceability, texture consistency, and production efficiency.

The Pet Food Machinery Market Report is Segmented by Equipment Type (Extrusion Equipment, Mixing and Blending Equipment, Forming and Shaping Equipment, Drying and Cooling Equipment, Coating and Flavoring Equipment, Grinding and Milling Equipment, Packaging Equipment, Automation and Control Systems, and Other Equipment Types), by Process Type (Dry Pet Food Processing Lines, Wet Pet Food Processing Lines, Treats Processing Lines, Veterinary Diet Processing Lines, and Nutraceutical and Supplement Processing Lines), by Pet Food Output Format (Kibbles, Canned and Wet Food, Freeze-Dried and Jerky Products, Soft and Chewy Treats, Dental Treats, Powders and Supplements, and Other Pet Food Output Formats), by Pet Type (Dogs, Cats and Other Pets), and by Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Extrusion Equipment |

| Mixing and Blending Equipment |

| Forming and Shaping Equipment |

| Drying and Cooling Equipment |

| Coating and Flavoring Equipment |

| Grinding and Milling Equipment |

| Packaging Equipment |

| Automation and Control Systems |

| Other Equipment Types |

| Dry Pet Food Processing Lines |

| Wet Pet Food Processing Lines |

| Treats Processing Lines |

| Veterinary Diet Processing Lines |

| Nutraceutical and Supplement Processing Lines |

| Kibbles |

| Canned and Wet Food |

| Freeze-Dried and Jerky Products |

| Soft and Chewy Treats |

| Dental Treats |

| Powders and Supplements |

| Other Pet Food Output Formats |

| Dogs |

| Cats |

| Other Pets |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | France |

| Germany | |

| Italy | |

| Netherlands | |

| Poland | |

| Russia | |

| Spain | |

| United Kingdom | |

| Rest of Europe | |

| Asia-Pacific | Australia |

| China | |

| India | |

| Indonesia | |

| Japan | |

| Malaysia | |

| Philippines | |

| Taiwan | |

| Thailand | |

| Vietnam | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Equipment Type | Extrusion Equipment | |

| Mixing and Blending Equipment | ||

| Forming and Shaping Equipment | ||

| Drying and Cooling Equipment | ||

| Coating and Flavoring Equipment | ||

| Grinding and Milling Equipment | ||

| Packaging Equipment | ||

| Automation and Control Systems | ||

| Other Equipment Types | ||

| By Process Type | Dry Pet Food Processing Lines | |

| Wet Pet Food Processing Lines | ||

| Treats Processing Lines | ||

| Veterinary Diet Processing Lines | ||

| Nutraceutical and Supplement Processing Lines | ||

| By Pet Food Output Format | Kibbles | |

| Canned and Wet Food | ||

| Freeze-Dried and Jerky Products | ||

| Soft and Chewy Treats | ||

| Dental Treats | ||

| Powders and Supplements | ||

| Other Pet Food Output Formats | ||

| By Pet Type | Dogs | |

| Cats | ||

| Other Pets | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | France | |

| Germany | ||

| Italy | ||

| Netherlands | ||

| Poland | ||

| Russia | ||

| Spain | ||

| United Kingdom | ||

| Rest of Europe | ||

| Asia-Pacific | Australia | |

| China | ||

| India | ||

| Indonesia | ||

| Japan | ||

| Malaysia | ||

| Philippines | ||

| Taiwan | ||

| Thailand | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the pet food machinery market?

It stands at USD 4.8 billion in 2026 and is forecasted to reach USD 6.2 billion by 2031 at a 5.47% CAGR between 2026 and 2031.

Which equipment category leads demand?

Extrusion leads, with 29.5% share in 2025, because dry kibble still anchors the largest installed production base worldwide.

Which process type is growing the fastest?

Veterinary diet processing lines are growing the fastest, with a forecasted 9.4% CAGR between 2026 and 2031, supported by stricter hygiene and precision requirements.

Which region offers the strongest near-term expansion?

Asia-Pacific shows the fastest growth, with a 7.4% CAGR between 2026 and 2031, supported by new commercial capacity in China and Southeast Asia.

Page last updated on: