Pet Dental Health Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

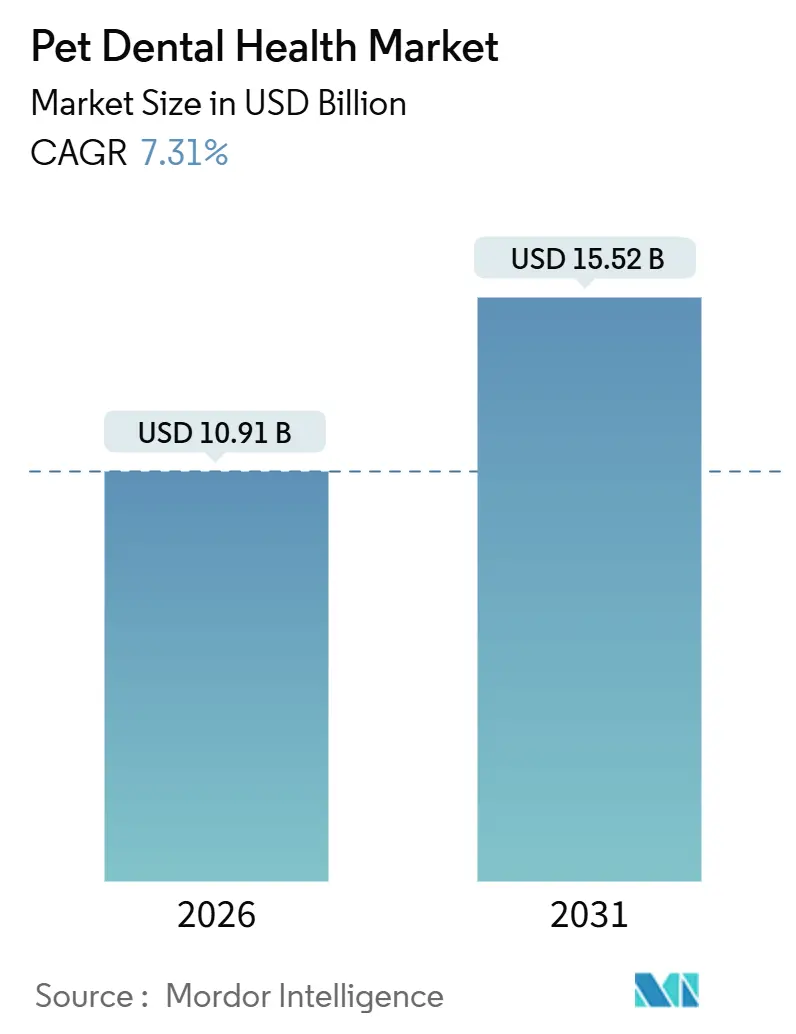

| Market Size (2026) | USD 10.91 Billion |

| Market Size (2031) | USD 15.52 Billion |

| Growth Rate (2026 - 2031) | 7.31% CAGR |

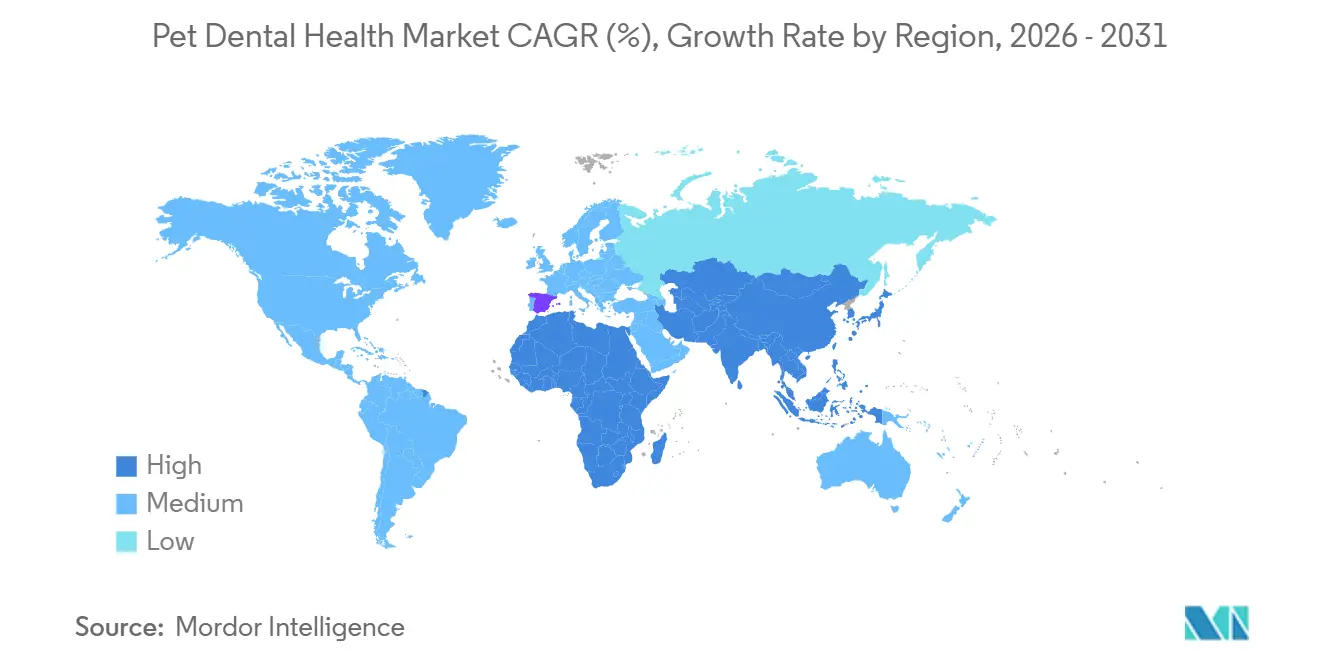

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pet Dental Health Market Analysis by Mordor Intelligence

The Pet Dental Health Market size is estimated at USD 10.91 billion in 2026, and is expected to reach USD 15.52 billion by 2031, at a CAGR of 7.31% during the forecast period (2026-2031).

Periodontal disease affects 80%–90% of adult dogs and cats, yet only 2%–8% of owners brush their pets’ teeth, so demand for professional cleanings and compliance-friendly home-care products remains resilient.[1]American Veterinary Medical Association, “AVMA Pet Ownership and Demographics Sourcebook,” American Veterinary Medical Association, avma.org Diagnostic protocols increasingly integrate the oral-systemic health link, with insurers adding dental riders and clinics purchasing cone-beam CT and ultrasonic scalers to meet new standards of care.[2]American Animal Hospital Association, “2025 AAHA Dental Care Guidelines for Dogs and Cats,” American Animal Hospital Association, aaha.org Consumables such as VOHC-certified chews and water additives are expanding shelf presence as retailers exploit rising wellness spending by millennial and Gen Z owners.[3]American Pet Products Association, “Pet Industry Statistics & Trends,” American Pet Products Association, americanpetproducts.org On the software side, AI-assisted imaging review and automated reminder modules lift appointment adherence, broadening the revenue base for the pet dental health market.

Key Report Takeaways

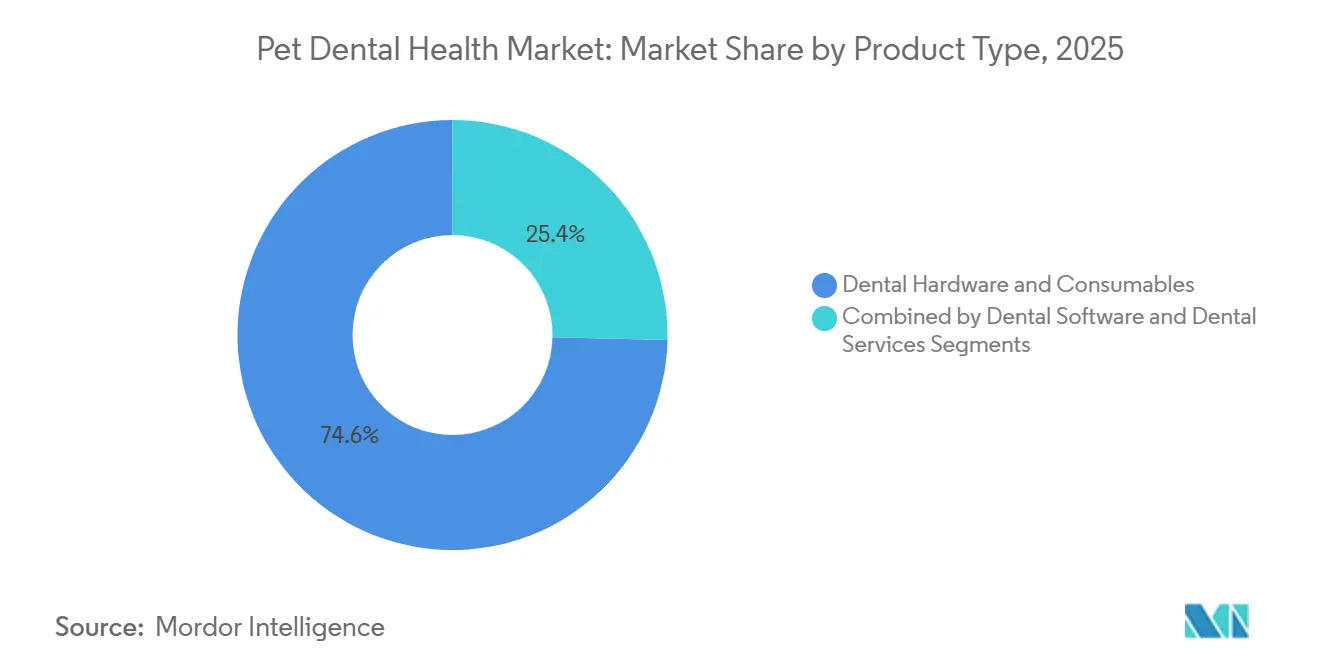

- By product type, Dental Hardware & Consumables captured 74.63% of the pet dental health market share in 2025, whereas Dental Software is projected to expand at an 11.25% CAGR through 2031.

- By animal type, dogs held 69.83% share of the pet dental health market size in 2025, while the feline segment is advancing at a 9.24% CAGR through 2031.

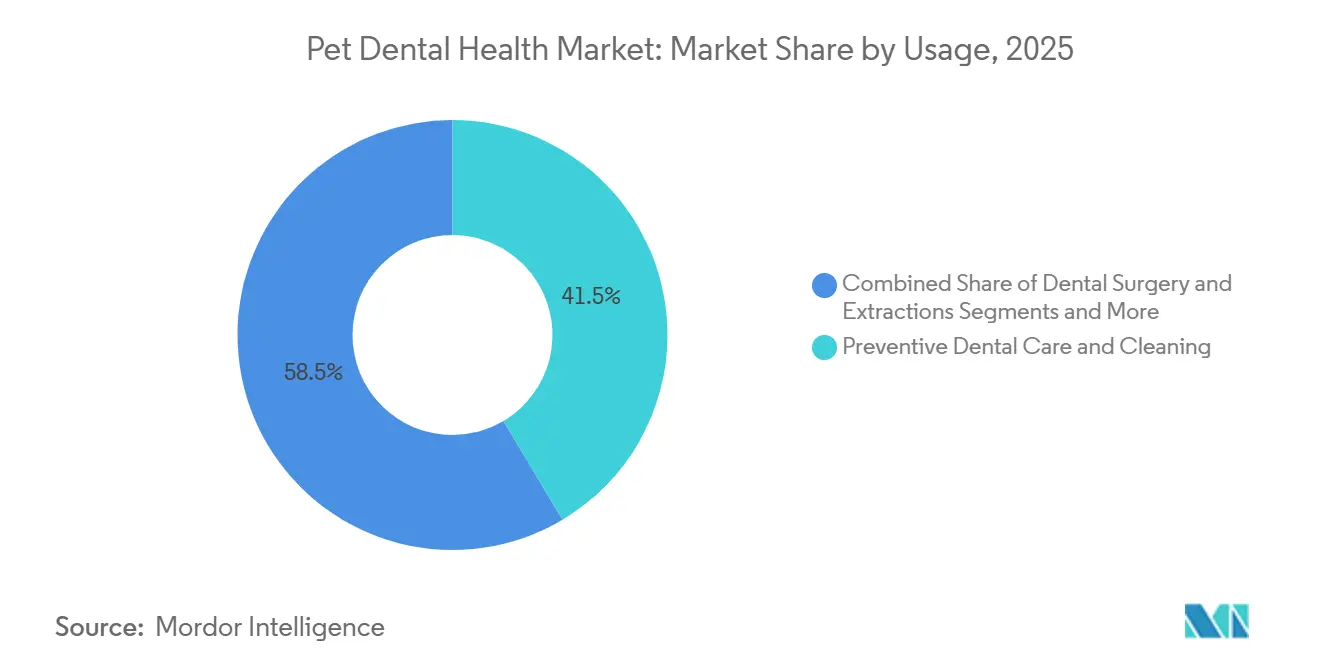

- By usage, Preventive Dental Care & Cleaning accounted for 41.46% share of the pet dental health market size in 2025, and Diagnostic Imaging is progressing at a 9.14% CAGR through 2031.

- By end user, Veterinary Hospitals represented 42.53% share of the pet dental health market size in 2025, whereas Home Care / Individual Pet Owners is forecast to grow at a 10.55% CAGR to 2031.

- By geography, North America commanded 44.24% revenue in 2025, and Asia-Pacific is leading with a 9.35% CAGR forecast to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Pet Dental Health Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Pet Ownership & Humanization | +1.2% | Global, with strongest gains in North America and Asia-Pacific urban centers | Medium term (2–4 years) |

| Growing Awareness of Oral-Systemic Health Link | +1.4% | North America and Europe, expanding to Asia-Pacific via veterinary education programs | Long term (≥4 years) |

| Expansion of Veterinary Insurance & Clinics | +1.1% | North America leads; Asia-Pacific and Middle East emerging | Medium term (2–4 years) |

| Advances in Imaging, AI & Minimally Invasive Tech | +1.3% | North America and Europe early adopters; Asia-Pacific following | Long term (≥4 years) |

| Emerging Microbiome-Based Personalized Oral Care | +0.9% | Global, with R&D concentrated in North America and Europe | Long term (≥4 years) |

| Adoption of VOHC Certification Influencing Product Trust | +0.8% | North America and Europe; limited recognition in developing markets | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Rising Pet Ownership & Humanization

Household pet ownership hit 94 million in the United States in 2024 and continues to climb as younger adults delay parenthood, raising discretionary spending on preventive services that anchor the pet dental health market. Wellness visits that include oral assessments rose 12% year over year in 2024, signaling a pivot toward routine prevention. Subscription kits offering VOHC-certified consumables now enjoy prime retail placement because they align with owners’ time constraints. Retailers and e-commerce marketplaces, sensing stable re-order rates, have expanded shelf facings for dental chews and water additives. These shifts build recurring revenue streams for the pet dental health market while normalizing dental care as part of everyday pet wellness.

Growing Awareness of Oral-Systemic Health Link

A 2024 peer-reviewed study showed dogs with severe periodontal disease faced 2.8 times higher chronic kidney disease risk, elevating dental care to a recognized core health pillar. Cardiologists now screen for oral pathology during endocarditis work-ups, and the 2025 AAHA guidelines incorporate dentistry alongside vaccination and parasite control. Insurers reacted by lowering deductibles for cleanings, reducing downstream claims and fortifying the pet dental health market. Clinics consequently invest in digital radiography and cone-beam CT to meet earlier intervention targets. The oral-systemic narrative has therefore moved from academia into mainstream practice, reinforcing sustained demand.

Expansion of Veterinary Insurance & Clinics

Written premiums climbed to USD 4.7 billion in 2024 with dental coverage standard in 78% of policies, defraying costs for anesthesia-based procedures. Corporate groups added general-practice sites at a 6% annual rate, embedding dental suites equipped with digital imaging and ultrasonic scalers. Denser clinic networks shorten travel times, boosting uptake of annual dental exams. Insurance offset reduces sticker shock for owners, and clinics recoup equipment outlays through higher procedure volume. This interplay secures a reliable growth lane for the pet dental health market.

Advances in Imaging, AI & Minimally Invasive Tech

Cone-beam CT units such as NewTom 5G XL VET produce 0.1 mm resolution scans, enabling pre-surgical visualization of root fractures without exploratory surgery. A 2025 study reported 34% more periodontal defects detected with CBCT versus two-dimensional radiographs. AI algorithms embedded in practice-management software flag abnormalities in seconds, empowering general practitioners to deliver specialist-level diagnostics. Equipment leasing lowers barriers, and decision-support overlays simplify owner education, increasing acceptance of indicated treatments. These technological gains lift the diagnostic component of the pet dental health market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Professional Dental Procedures | -0.9% | Global, most acute in price-sensitive markets and rural areas | Short term (≤2 years) |

| Low Owner Compliance & Pet Resistance to Home Care | -1.1% | Global, with cultural variations in pet-care norms | Medium term (2–4 years) |

| Limited Access to Specialized Veterinary Dentistry in Developing Regions | -0.7% | Asia-Pacific (excluding Japan, South Korea), Middle East & Africa, South America | Long term (≥4 years) |

| Regulatory Ambiguity on Efficacy Claims for Pet Oral Products | -0.5% | Global, particularly affecting over-the-counter consumer products | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High Cost of Professional Dental Procedures

Anesthesia-based cleanings range from USD 300 to USD 1,500, with anesthesia representing up to 40% of the bill. A 2024 AVMA survey found 38% of owners declined recommended dental care due to cost. Price sensitivity peaks in households earning below USD 50,000 and in rural communities where travel compounds expense. Delays allow disease progression until extraction becomes inevitable, raising total treatment costs. This economic barrier tempers volume growth in the pet dental health market despite underlying need.

Low Owner Compliance & Pet Resistance to Home Care

Only 2%–8% of owners brush daily, and 64% abandon new routines within 90 days because pets resist or results appear slow. Behavioral hurdles are higher in cats, whose stress responses complicate brushing. Consequently, home-care lapses shift disease burden to clinics, amplifying the high-cost restraint. While passive-delivery formats help, they still underperform mechanical plaque removal. The gap between ideal and achievable compliance restrains full realization of the pet dental health market’s preventive potential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Software Outpaces Hardware in Growth

Dental Software is climbing at an 11.25% CAGR through 2031, triple the pace of Dental Hardware & Consumables, which controlled 74.63% of 2025 revenue within the pet dental health market size. Integrated practice-management platforms automate dental exam templates, dispatch reminders, and embed AI radiology review that identifies bone loss in under 10 seconds. These tools raise treatment acceptance and increase throughput without additional staff.

Hardware & Consumables remain the revenue anchor, yet commoditization pressures intensify as private-label chews undercut branded SKUs. Service contracts that bundle scaler calibration and sensor replacement shift one-time sales into recurring fees and fortify vendor-clinic relationships. Leasing models now place USD 100,000 cone-beam CT systems into mid-tier clinics at USD 2,000 per month, democratizing advanced imaging and adding depth to the pet dental health market.

By Animal Type: Feline Segment Gains Momentum

Dogs generated 69.83% of 2025 animal-type revenue, but cats are tracking a 9.24% CAGR through 2031, the highest within the pet dental health market share. Feline-specific issues such as tooth resorption and chronic gingivostomatitis prompted new guidelines that emphasize early detection, stimulating VOHC-certified diets and palatable water additives for cats.

Brands like Hill’s Prescription Diet t/d Feline and Virbac Aquadent FR3SH broaden feline offerings to 18% of VOHC-accepted products. Rising cat ownership in urban apartments and the relative ease of oral-gel delivery over brushing enhance commercial prospects. Consequently, the feline segment represents the primary incremental volume lever for companies active in the pet dental health market.

By Usage: Diagnostic Imaging Surges Ahead

Preventive Dental Care & Cleaning delivered 41.46% of 2025 usage revenue, yet Diagnostic Imaging is advancing at a 9.14% CAGR as CBCT visualization displaces two-dimensional radiographs. CBCT multiplanar reconstruction spotted 34% more periodontal defects, cutting repeat anesthesia and revision surgeries. Owners accept imaging fees when presented with high-resolution overlays that clarify hidden pathology.

Meanwhile, advanced interventions such as endodontics and orthodontics remain niche but command premium pricing, especially in working dogs and social-media companion animals. Endodontic root canals preserve bite strength at USD 1,000–2,500 per tooth, whereas orthodontic alignments address both functional and cosmetic malocclusion. These services elevate average transaction value, enriching the pet dental health market size at the upper end of the care spectrum.

By End User: Home Care Disrupts Traditional Channels

Veterinary Hospitals held 42.53% of end-user revenue in 2025, securing high-value anesthesia and imaging procedures. Yet Home Care / Individual Pet Owners is expanding at a 10.55% CAGR, nearly double hospital growth, as subscription kits and telehealth counseling reduce friction for owners.

PetSmile’s USD 20 quarterly shipment and Dutch’s virtual consultations bring VOHC-approved consumables directly to doorsteps, bypassing clinic markup. Veterinary clinics respond by adding retail shelves and e-commerce portals, but the convenience advantage tilts momentum toward direct-to-consumer formats. This shift redistributes value across the pet dental health market while preserving professional services for advanced care.

Geography Analysis

Asia-Pacific leads growth at a 9.35% CAGR through 2031 as urban household formation fuels pet adoptions in China, India, and South Korea. Rising disposable incomes lift per-pet spending, and regulatory harmonization eases import of VOHC-accepted products. Japan’s aging population allocates more than USD 1,200 per pet annually, normalizing premium dental diets and cone-beam imaging. Limited specialist density persists, so teledentistry platforms gain popularity, extending expertise into secondary cities.

North America maintained 44.24% revenue in 2025, supported by 6.4 million insured pets generating USD 4.7 billion in premiums and a dense network of board-certified dentists. Category saturation is evident as 68% of dog owners and 52% of cat owners purchased at least one dental product in 2024, directing future gains toward premiumization rather than penetration. Europe mirrors this trajectory, with the United Kingdom, Germany, and France hosting mature VOHC portfolios and established residency programs.

The Middle East & Africa and South America trail but show affluent pockets—GCC states and São Paulo—where expatriate demand sustains high-end dental suites. Infrastructure gaps keep procedure volume low, but e-commerce plants early seeds of growth. Combined, these patterns reveal a dual opportunity for the pet dental health market: penetration in developing economies and product sophistication in mature regions.

Competitive Landscape

Multinational pet-food leaders Mars Petcare and Nestlé Purina leverage grocery and e-commerce scale to push dental treats like Dentastix and DentaLife, though private-label competition compresses margins. Colgate-Palmolive’s Hill’s Prescription Diet t/d dominates veterinary-exclusive dental diets, prescribed by 42% of U.S. veterinarians, yet dependence on clinic channels exposes it to direct-to-consumer disruption. Equipment suppliers Henry Schein, Patterson, and Midmark anchor the professional segment, bundling financing, installation, and maintenance, which secures multi-year revenue streams and heightens switching costs.

White-space innovation centers on microbiome therapies and AI decision-support. Kane Biotech’s enzyme-based DentaPet reduced plaque by 40% in 28 days, and IDEXX embeds AI overlays that highlight lesions during routine exams, shortening time-to-treatment. Telehealth platforms such as Dutch marry remote consultation with doorstep product delivery, capturing convenience-oriented owners. Subscription models like PetSmile automate compliance, lifting owner participation beyond single-digit baselines.

Regulatory ambiguity remains a hurdle; the FDA’s laissez-faire stance on efficacy claims permits parity messaging from uncertified chews, diluting brand equity. Companies investing in VOHC validation secure 15%–20% price premiums and higher veterinarian endorsement, differentiating amid commoditization. Overall, the pet dental health market exhibits moderate fragmentation, with scale advantages balanced by specialized niches.

Pet Dental Health Industry Leaders

Dechra Pharmaceuticals plc

Colgate-Palmolive

Mars Petcare

Virbac

Nestlé Purina PetCare

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Phibro Animal Health nationally launched Restoris piezoelectric dental gel, delivering a dual mechanism to restore canine oral health.

- September 2025: Pet Honesty introduced Fresh Breath Dental Bites for cats, blending palatability with plaque control.

- May 2025: Woof rolled out Doggy Dental Mix, a water-activated powder designed to pair with the Pupsicle enrichment toy.

- February 2025: Fera Pets debuted Dental Support supplement, featuring botanicals, enzymes, and postbiotics for dogs and cats.

Global Pet Dental Health Market Report Scope

Pet dental health is defined as the comprehensive oral care provided to animals, which includes veterinary cleanings (such as scaling and polishing), exams, X-rays, and treatments aimed at preventing periodontal disease. It focuses on removing plaque, tartar, and infections.

The Pet Dental Health Market Report is segmented by Product Type, Animal Type, Usage, End User, and Geography. By Product Type, the market is segmented into Dental Hardware & Consumables (Toothpaste, Toothbrushes, Dental Chews & Treats, Oral Rinses & Water Additives, Dental Wipes & Sprays, Veterinary Dental Diets, Dental Equipment & Instruments, Dental Imaging & Diagnostics Hardware), Dental Software (Practice Management & EMR Integration, Imaging & PACS Platforms, AI Radiology & Decision-Support Tools, Client Education & Compliance Apps), and Dental Services (Preventive Care Plans & Subscriptions, Equipment Installation & Maintenance, Others). By Animal Type, the market is segmented into Dogs, Cats, Horses, and Other Companion Animals. By Usage, the market is segmented into Preventive Dental Care & Cleaning, Diagnostic Imaging, Dental Surgery & Extractions, Endodontic & Periodontal Procedures, and Orthodontic & Prosthodontic Procedures. By End User, the market is segmented into Veterinary Hospitals, Veterinary Clinics, Home Care / Individual Pet Owners, and Academic & Research Institutes. By Geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends across major regions globally. Market Forecasts are Provided in Terms of Value (USD).

| Dental Hardware & Consumables | Toothpaste |

| Toothbrushes | |

| Dental Chews & Treats | |

| Oral Rinses & Water Additives | |

| Dental Wipes & Sprays | |

| Veterinary Dental Diets | |

| Dental Equipment & Instruments | |

| Dental Imaging & Diagnostics Hardware | |

| Dental Software | Practice Management & EMR Integration |

| Imaging & PACS Platforms | |

| AI Radiology & Decision-Support Tools | |

| Client Education & Compliance Apps | |

| Dental Services | Preventive Care Plans & Subscriptions |

| Equipment Installation & Maintenance | |

| Others |

| Dogs |

| Cats |

| Horses |

| Other Companion Animals (rabbits, etc.) |

| Preventive Dental Care & Cleaning |

| Diagnostic Imaging |

| Dental Surgery & Extractions |

| Endodontic & Periodontal Procedures |

| Orthodontic & Prosthodontic Procedures |

| Veterinary Hospitals |

| Veterinary Clinics |

| Home Care / Individual Pet Owners |

| Academic & Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Dental Hardware & Consumables | Toothpaste |

| Toothbrushes | ||

| Dental Chews & Treats | ||

| Oral Rinses & Water Additives | ||

| Dental Wipes & Sprays | ||

| Veterinary Dental Diets | ||

| Dental Equipment & Instruments | ||

| Dental Imaging & Diagnostics Hardware | ||

| Dental Software | Practice Management & EMR Integration | |

| Imaging & PACS Platforms | ||

| AI Radiology & Decision-Support Tools | ||

| Client Education & Compliance Apps | ||

| Dental Services | Preventive Care Plans & Subscriptions | |

| Equipment Installation & Maintenance | ||

| Others | ||

| By Animal Type | Dogs | |

| Cats | ||

| Horses | ||

| Other Companion Animals (rabbits, etc.) | ||

| By Usage | Preventive Dental Care & Cleaning | |

| Diagnostic Imaging | ||

| Dental Surgery & Extractions | ||

| Endodontic & Periodontal Procedures | ||

| Orthodontic & Prosthodontic Procedures | ||

| By End User | Veterinary Hospitals | |

| Veterinary Clinics | ||

| Home Care / Individual Pet Owners | ||

| Academic & Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the studied market?

The pet dental health market size stands at USD 10.91 billion in 2026.

How fast is the market expected to grow?

The market is forecast to expand at a 7.31% CAGR and reach USD 15.52 billion by 2031.

Which product category is expanding the quickest?

Dental Software is projected to post an 11.25% CAGR through 2031 as practices adopt AI-enabled platforms.

Which region is leading future growth?

Asia-Pacific is advancing at a 9.35% CAGR thanks to rising urban pet ownership and regulatory harmonization.

What is the main barrier to wider procedure uptake?

High procedure cost, especially for anesthesia-based cleanings costing USD 300–1,500, remains the primary obstacle.

How are owners accessing dental care products at home?

Subscription kits and telehealth services deliver VOHC-certified consumables directly to households, fueling a 10.55% CAGR in the home-care channel.

Page last updated on: