Peru Corrugated Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

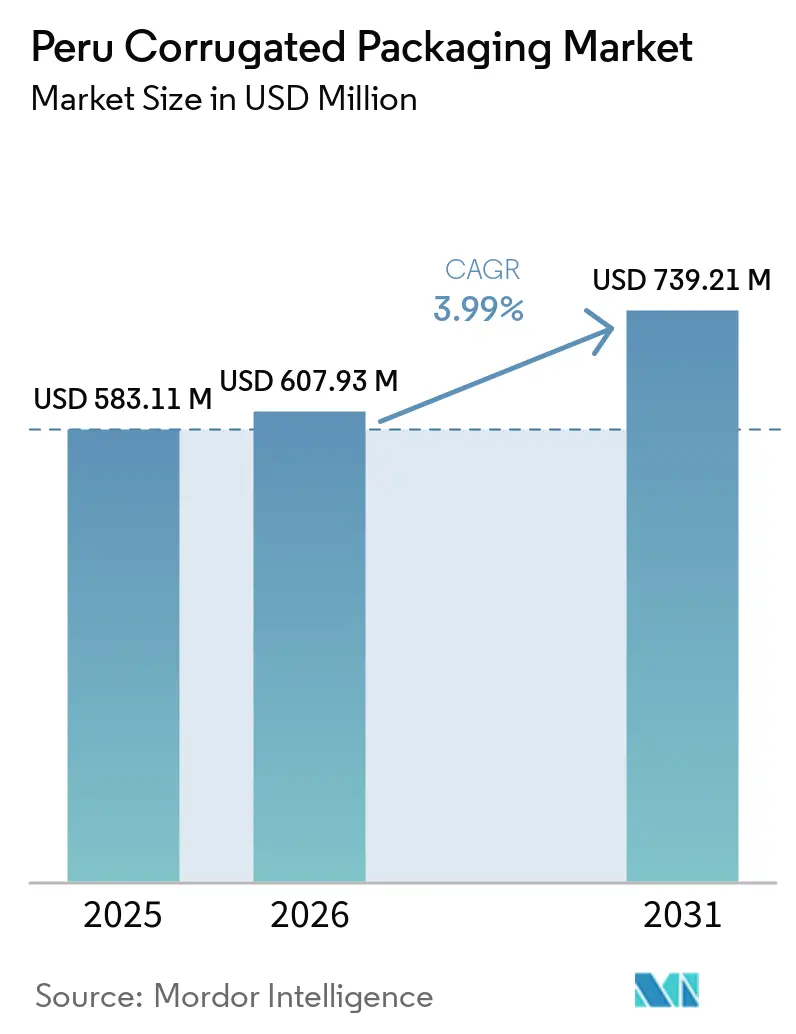

| Base Year Market Size (2025) | USD 583.11 Million |

| Market Size (2026) | USD 607.93 Million |

| Market Size (2031) | USD 739.21 Million |

| Growth Rate (2026 - 2031) | 3.99% CAGR |

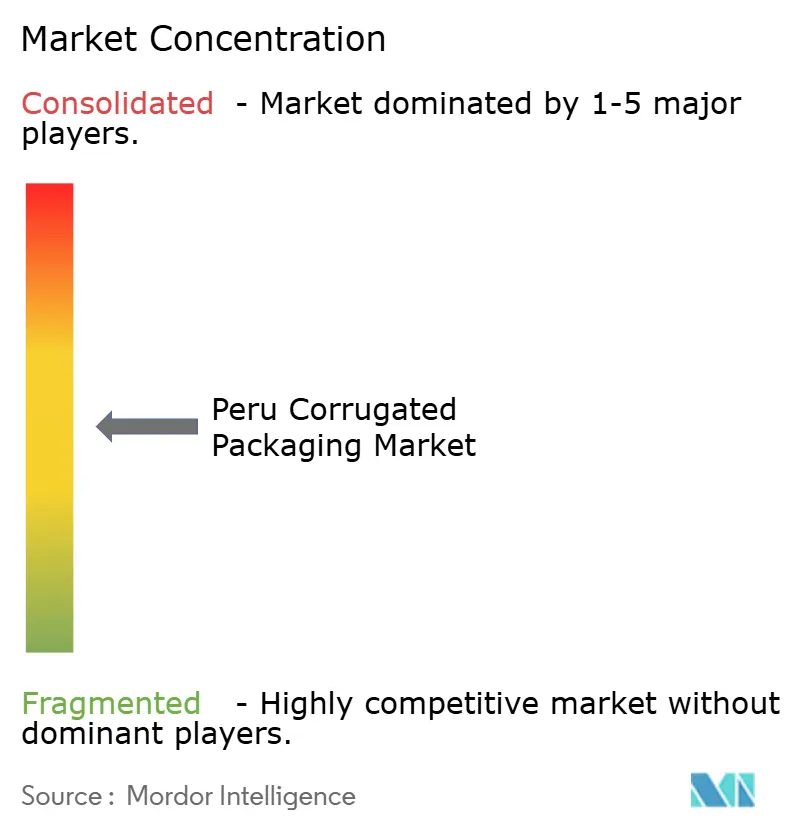

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Peru Corrugated Packaging Market Analysis by Mordor Intelligence

The Peru corrugated packaging market stood at USD 583.11 million in 2025, is valued at USD 607.93 million in 2026, and is forecast to reach USD 739.21 million by 2031, registering a CAGR of 3.99% between 2026 and 2031. Robust agro-export growth, a double-digit surge in domestic e-commerce, and a nationwide push for recyclable materials are reshaping specifications, flute selection, and plant-level technology investments across the Peru corrugated packaging market. Converters are scaling ventilated, moisture-resistant boxes for blueberries and grapes, accelerating lightweight E flute production for last-mile parcels, and adopting hybrid flexo-digital presses to serve shorter, SKU-rich print runs. Law 32434, effective January 2026, lowers the corporate income tax burden for agribusiness and refunds VAT on packaging inputs, freeing cash for exporters to upgrade cold-chain infrastructure and raise demand for transit packaging. Meanwhile, raw-material volatility and competition from flexible pouches continue to pressure margins, compelling converters to diversify fiber sources and emphasize corrugated recyclability.

Key Report Takeaways

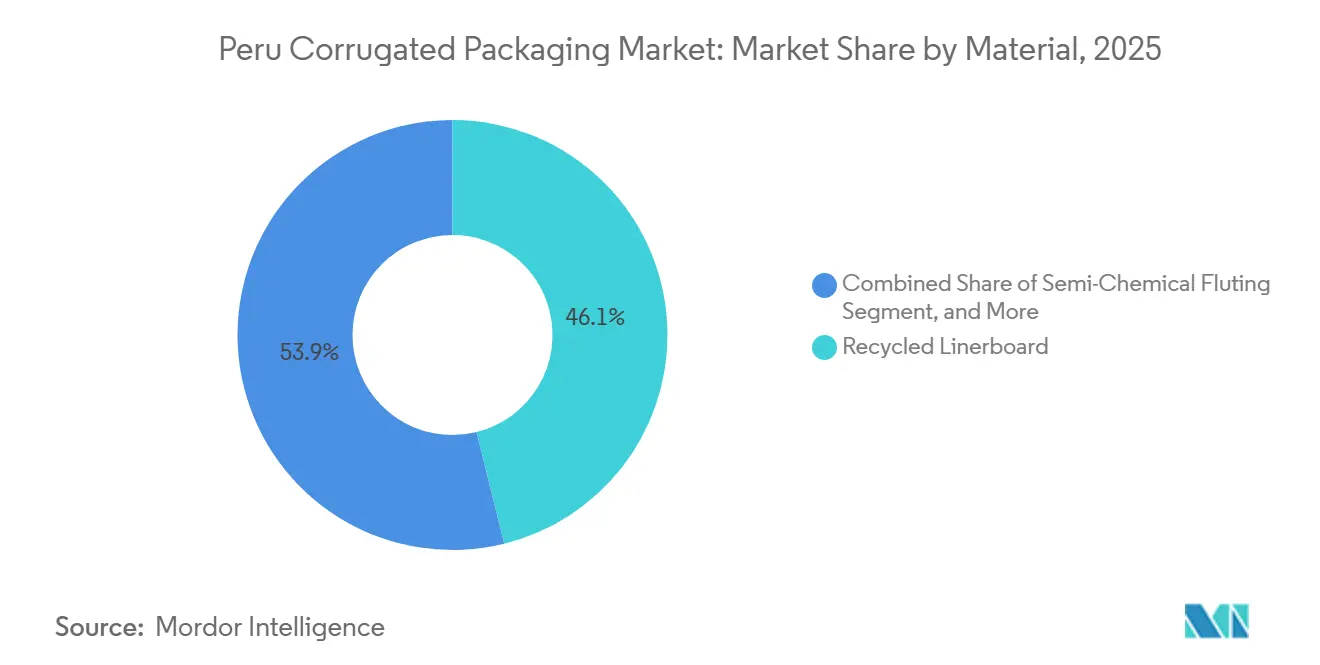

- By material, recycled linerboard captured 46.13% of the Peru corrugated packaging market share in 2025.

- By flute type, the Peru corrugated packaging market size for the E flute segment is forecast to advance at a 5.32% CAGR through 2031.

- By packaging type, regular slotted containers captured 41.34% of the Peru corrugated packaging market share in 2025.

- By wall type, the Peru corrugated packaging market for double-wall boxes is forecast to grow at a 4.18% CAGR through 2031.

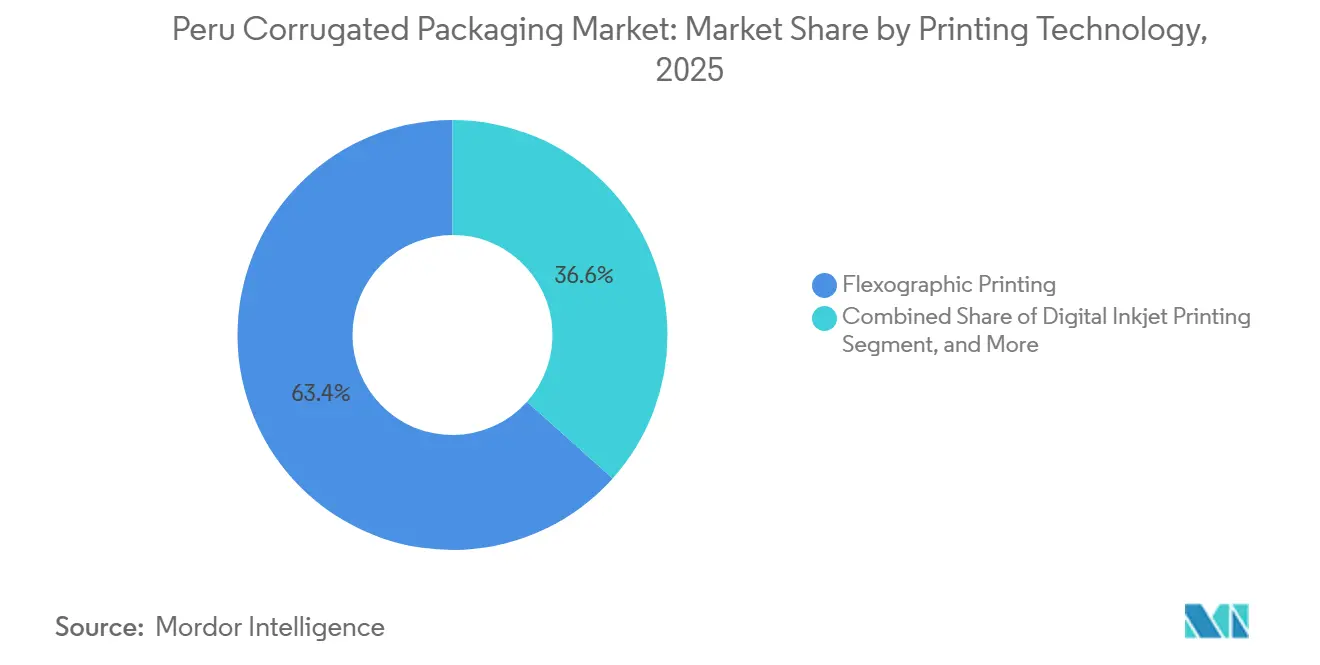

- By printing technology, flexographic printing captured 63.38% of the Peru corrugated packaging market share in 2025.

- By end-user industry, the Peru corrugated packaging market size for the e-commerce fulfillment centers segment is forecast to advance at a 5.28% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Peru Corrugated Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth of E-Commerce and Home Delivery in Peru | +1.20% | National, concentrated in Lima, Arequipa, Trujillo | Short term (≤ 2 years) |

| Expansion of Agro-Export Sector Requiring Ventilated Corrugated Packaging | +1.10% | Coastal valleys, export corridors to Callao | Medium term (2-4 years) |

| Rising Demand for Sustainable and Recyclable Packaging Materials | +0.80% | National, early compliance in Lima and export zones | Medium term (2-4 years) |

| Growing Penetration of Modern Retail Chains Driving Shelf-Ready Corrugated Displays | +0.50% | Urban centers expanding to secondary cities | Medium term (2-4 years) |

| Adoption of High-Speed Digital Printing for Short-Run SKU Proliferation | +0.30% | Lima industrial corridor, Trujillo | Long term (≥ 4 years) |

| Government Incentives for Sugarcane Bagasse-Based Containerboard Capacity | +0.20% | La Libertad, Lambayeque | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growth of E-Commerce and Home Delivery in Peru

E-commerce sales reached USD 37 billion in 2024 and are set to hit USD 59.5 billion by 2027, fueling a shift from bulk industrial shippers to branded parcels tailored for residential delivery.[1]Cámara Peruana de Comercio Electrónico, “Reporte de comercio electrónico 2024-2027,” CAPECE.PE Converters are ramping E and F flute boards that trim dimensional-weight fees while safeguarding contents during automated sortation. Subscription-box services for cosmetics and gourmet foods now request digitally printed boxes with embossing, windows, and water-based barrier coatings that survive the humid coastal rainy season. Platforms such as Mercado Libre and Linio are adding fulfillment hubs in Arequipa and Trujillo, decentralizing demand beyond Lima and pushing regional plants to install variable-data inkjet lines and real-time inventory systems. These dynamics collectively heighten velocity, customization, and sustainability requirements across the Peru corrugated packaging market.

Expansion of Agro-Export Sector Requiring Ventilated Corrugated Packaging

Peru ships roughly 80 million boxes of table grapes each season, with 45% bound for the United States, and exported USD 1.417 billion in packaging during 2024. Blueberries, avocados, and citrus increasingly rely on laser-ventilated, moisture-resistant cartons that maintain cold-chain integrity on 20- to 30-day voyages to Europe and Asia. Buyers now specify five-layer board and water-based coatings that replace wax treatments banned by several European retailers, prompting investments in CAD-driven die-cutting and coating lines. Trupal reported record output in 2025 after adding a die-cut press to handle seasonal spikes, underscoring how agro-export seasonality dictates capacity planning.[2]Asociación de Exportadores, “Exportaciones peruanas de envases alcanzan USD 1,417 millones,” CARTONYCORRUGADO.COM Certification to ISPM 15, BRCGS, and FSC standards has become a prerequisite for entry into the United Kingdom and German retail chains, reinforcing quality management upgrades across the Peruvian corrugated packaging market.

Rising Demand for Sustainable and Recyclable Packaging Materials

Single-use plastic restrictions under Law 30884 are redirecting brands toward fiber-based, curbside-recyclable formats. CARVIMSA achieved 100% renewable energy operations in 2024, avoiding 2,300 tonnes of CO₂, and set a 2050 decarbonization roadmap focused on lightweighting and closed-loop fiber recovery. Trupal blends up to 80% sugarcane bagasse into its corrugating medium, leveraging 9 million tonnes of annual cane harvests to reduce reliance on virgin pulp and enhance biodegradable credentials in the market. Prepared-foods packaging climbed 7.1% in 2024, widening opportunities for corrugated secondary packs sized for rectangular aseptic cartons that boost pallet density and curb emissions. These shifts foreground recycled linerboard optimization and renewable-fiber innovation across the Peru corrugated packaging industry.

Growing Penetration of Modern Retail Chains Driving Shelf-Ready Corrugated Displays

Chains such as Plaza Vea, Tottus, and Metro expanded footprints through 2025, enforcing shelf-ready packaging guidelines that favor E and B flute die-cut displays with tear strips, hand holes, and high-definition graphics. Suppliers in beverages, snacks, and personal care now integrate merchandising and logistics functions in a single printed box, cutting in-store labor and improving sell-through. Converters with litho-lamination and hybrid presses are capturing this business by offering photographic imagery and fine text down to 6-point type. Pack Peru Expo, slated for August 2026, will showcase automated die-cutters, inline inspection, and circular-economy solutions that support retailers’ efficiency and sustainability goals.[3]Pack Perú Expo, “Anuario Packaging 2025,” PACKPERUEXPO.COM Shelf-ready adoption deepens the need for print quality, structural accuracy, and fast artwork changeovers in the Peru corrugated packaging market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Recycled Fiber Prices | -0.60% | National, acute in Lima and coastal mills relying on imported OCC | Short term (≤ 2 years) |

| Competition from Flexible Plastic Pouches in Beverage and Personal Care | -0.40% | Urban markets, premium consumer segments | Medium term (2-4 years) |

| High Logistics Costs Across Mountainous Terrain Limiting Box Integrity | -0.30% | Andean highlands, Lima-Cusco-Puno routes | Long term (≥ 4 years) |

| Shortage of Skilled Flexo Technicians Hindering Quality Consistency | -0.20% | National, especially Lima and Trujillo industrial zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Recycled Fiber Prices

Tighter South America recovered paper flows, and China’s import quotas have driven erratic old-corrugated-container costs since 2024, squeezing converters that depend on recycled linerboard’s 46.13% share of Peru's corrugated packaging market input. Domestic collection shortfalls oblige mills to import fiber in United States dollars, exposing them to currency swings while they invoice customers in soles. Some plants respond by integrating upstream paper mills, exploring sugarcane bagasse or agricultural residues, and signing shorter-term supply contracts to hedge volatility. Yet when recycled-fiber prices spike, converters often default to virgin kraft pulp, undermining sustainability commitments and widening cost pass-through debates with agro-exporters. These pressures complicate pricing visibility and investment planning across the Peru corrugated packaging market.

Competition from Flexible Plastic Pouches in Beverage and Personal Care

Stand-up pouches' barrier performance, resealable spouts, and lightweight Appeal continue to erode corrugated demand for beverage multipacks and liquid personal-care refills. Peruplast’s USD 8.64 million upgrade to a seven-layer MDO polyethylene line, announced in 2026, boosts film output by roughly 10%, signaling sustained investment in flexible packaging.[4]Infomercado, “Peruplast invierte USD 8.64 millones,” INFOMERCADO.PE Retailers keen on shelf appeal favor glossy pouches, and brand owners spotlight shipping-cost savings versus box-and-bottle formats. Corrugated converters counter with hybrid shippers, pairing an outer box with an inner pouch, and market recyclability advantages under extended producer responsibility schemes. Nonetheless, flexible-format momentum restrains the growth trajectory of the Peru corrugated packaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Recycled Linerboard Dominates, Virgin Kraft Gains Traction

Recycled linerboard secured 46.13% of Peru corrugated packaging market share in 2025 as Lima-based recovery networks and cost sensitivity kept demand high. Virgin Kraft linerboard, however, is expected to outpace overall market growth at a 5.17% CAGR, led by blueberry and avocado exporters that require pristine surfaces for European and North American retail graphics. The Peru corrugated packaging market for premium agro-export cartons increasingly favors virgin fibers to meet burst-strength and moisture-resistance thresholds during 30-day sea voyages. Local mills such as Trupal use 80% sugarcane bagasse in corrugating media, bolstering renewable-content propositions and reducing exposure to pulp imports. Semi-chemical fluting, blending mechanical and chemical pulping, is gaining favor for double-wall boxes that must survive coastal humidity swings without delamination.

Secondary developments include water-based barrier coatings that replace paraffin wax, ensuring recyclability and compliance with retailer bans on non-recyclable treatments. CARVIMSA’s BRCGS AA+ and FSC chain-of-custody credentials appeal to exporters anxious about European packaging taxes and traceability. Yet recycled-fiber price volatility keeps material sourcing strategies fluid, encouraging converters to lock in multi-year kraft supply agreements while expanding domestic OCC collection initiatives.

By Flute Type: C Flute Retains Balance, E Flute Accelerates in Parcel Networks

C flute retained 38.23% share thanks to its 3.6 mm thickness that balances cushioning with material efficiency for general-purpose shippers and agro-export transit packs. E flute’s slender 1.6 mm profile, however, is forecast to expand at a 5.32% CAGR as e-commerce sellers pursue lighter parcels and sharper graphics. The Peru corrugated packaging market size linked to subscription-box and cosmetics fulfillment leans on E flute’s smoother print surface, which minimizes washboarding during litho-lamination. B flute remains the workhorse for heavier consumer electronics and glassware, where shock absorption overrides dimensional-weight penalties. Converters equipped with multi flute corrugators now toggle production daily to match order profiles, enhancing asset utilization and lead-time responsiveness.

Thin F flute and micro flute innovations serve luxury chocolates and skincare gift sets, enabling rigid yet sleek cartons that replace chipboard while staying recyclable. Meanwhile, A flute persists in fragile-goods niches, though its storage inefficiency limits broader appeal. Across flutes, demand patterns underscore how e-commerce growth, shipping tariffs, and in-store display standards jointly dictate board-profile selection in the Peru corrugated packaging market.

By Packaging Type: Regular Slotted Containers Lead, Custom Die-Cuts Strike Growth

Regular slotted containers captured 41.34% of revenue in 2025, favored for standardized dimensions that integrate with automated case packers across food, beverage, and industrial lines. Die-cut custom boxes, projected at a 4.95% CAGR, ride shelf-ready mandates and direct-to-consumer branding needs that emphasize opening rituals and graphics. Peru corrugated packaging market share gains for custom formats concentrate in fresh produce, where fine-tuned ventilation patterns preserve cold-chain freshness, and in cosmetics, where window cutouts and embossing heighten premium cues. Folding cartons built on E or F flute substrates accelerate in pharmaceuticals and snack bars, packing tightly on shelves while reducing shipping voids.

Point-of-purchase displays merge merchandising with logistics, shortening restock times for retailers and commanding higher converter margins. Pallet boxes fashioned from double-wall board anchor heavy-duty mining and automotive parts flows, providing reusable strength for multileg transport. Diversified packaging portfolios help converters buffer seasonal swings and defend margins within the Peru corrugated packaging market.

By Wall Type: Single-Wall Efficiency Meets Double-Wall Durability

Single-wall constructions accounted for 58.54% of the market in 2025, as cost-effective choices for domestic routes and controlled-environment warehousing. Double-wall formats, slated for 4.18% CAGR growth, answer export-grade compression and moisture challenges faced by fruit shippers navigating 1.5-meter pallet stacks and condensate inside refrigerated containers. The Peru corrugated packaging market size is attached to agro-export corridors, thus tilting toward dual-wall specifications, even though they add weight. Triple-wall cartons, while niche, secure ceramic collectors and heavy machinery parts against puncture during long-haul trucking over Andean switchbacks.

Converters market single-face corrugated wraps as a recyclable alternative to bubble wrap, winning over e-commerce brands that pursue plastic-free credentials. Investment in high-performance adhesives and humidity-resistant starch blends underpins efforts to curb box failures without excessive caliper or cost.

By Printing Technology: Flexo Dominance Faces Digital Disruption

Flexographic presses held a 63.38% share due to their high speed and low unit cost on runs exceeding 1,000 boxes. Digital inkjet, projected to grow at a 5.38% CAGR, empowers food and beverage owners to launch limited-edition products, regional flavors, and personalization campaigns without plate costs. The Peru corrugated packaging market, which is now tied to sub-500-unit runs, justifies investments in single-pass inkjet lines capable of photographic-quality printing and variable data. Hybrid flexo-digital systems further compress lead times, enabling converters to print solids and variable graphics in a single pass.

Litho-lamination remains the standard for wine, cosmetics, and confectionery gift packs that require offset-level color fidelity. Screen printing serves metallic or tactile finishes on point-of-sale displays, albeit at modest volumes. Inkjet’s higher per-unit ink spend keeps flexo ahead for commodity SKUs, yet margin mix is shifting as converters monetize quick-turn value.

By End-User Industry: Processed Foods Anchor Demand, E-Commerce Packs Accelerate

Processed foods comprised 29.38% of demand in 2025, buoyed by 7.1% growth in domestic food processing and a pivot to aseptic cartons that fit tighter in secondary cases. E-commerce fulfillment centers, expanding at a 5.28% CAGR, intensify need for crush-resistant, brandable parcels shipped through courier sortation hubs in Lima, Arequipa, and Trujillo. Fresh produce exporters sustain sizeable Peru corrugated packaging market share with ventilated, moisture-shielded crates for grapes, blueberries, and avocados destined for 30-day voyages. Beverage bottlers balance shrink-film economics against corrugated’s stack strength and retail presentation, especially in beer and premium water multipacks.

Electronics and appliance importers specify anti-static coatings and die-cut inserts to dodge returns, while cosmetics houses chase luxurious unboxing with E flute litho-laminated sleeves. Pharmaceutical distributors insist on tamper evidence and traceability labeling, driving bar-coded case requirements. Diverse end-user needs compel converters to broaden substrate, flute, and print offerings within the Peru corrugated packaging market.

Geography Analysis

Lima anchors the largest share of the Peru corrugated packaging market, leveraging its port access, food-processing clusters, and e-commerce hubs to sustain year-round demand for transit and shelf-ready boxes. Coastal valleys in Ica, La Libertad, and Piura add seasonal spikes tied to grape and blueberry harvests, prompting converters to adopt just-in-time schedules and surge labor during export windows. The northern corridor around Trujillo and Chiclayo benefits from sugarcane, rice, and seafood industries, while housing Trupal’s bagasse-based paper and box plants that feed regional clients.

Andean highland cities such as Cusco and Puno show emerging demand as retail chains push into the interior, yet rugged roads and high logistics costs temper the adoption of premium packaging. Arequipa in the south hosts dairy processing, textiles, and a growing cluster of e-commerce distribution centers, drawing converters to set up satellite plants that shorten lead times. The Amazon basin remains nascent but is trending upward with cacao and coffee exporters who value biodegradable packaging to reinforce organic storytelling.

Law 32434’s tax incentives free capital for agro-exporters to expand cold-chain assets, indirectly lifting corrugated transit-box orders nationwide. Concurrently, compliance with ISPM 15, BRCGS, and FSC standards has become critical for converters shipping to Europe and North America, spurring quality-system upgrades across every major Peruvian converting hub.

Competitive Landscape

The Peru corrugated packaging market is moderately fragmented. Trupal, CARVIMSA, and Smurfit Westrock head the pack, followed by regional specialists such as Forsac, Propacking, Ecopacking, and Packingtech. Trupal’s vertical integration into bagasse-based containerboard sheltered it from 2025 fiber-price swings and supported a 10% sales beat. CARVIMSA’s USD 8 million 2026 capex program targets efficiency gains across its Huachipa mill and six regional depots, reinforcing its quick-turn edge on export-grade orders. Smurfit Westrock’s March 2026 purchase of Ecuadorian assets hints at Andean consolidation, boosting procurement leverage and cross-border customer servicing.

Strategic moves include automated die-cutters, inline vision inspection, and ERP-driven scheduling that cut lead times from 10 days to three on repeat orders. Emerging disruptors deploy single-pass inkjet lines and smart-packaging add-ons like QR-enabled traceability and temperature strips. Converters tout sugarcane-bagasse medium, renewable-energy footprints, and closed-loop fiber partnerships to win sustainability-centric accounts. Technology adoption and raw-material integration therefore differentiate margins and bargaining power across the Peru corrugated packaging market.

Peru Corrugated Packaging Industry Leaders

Smurfit Westrock plc

Trupal S.A.

Cartones Villa Marina S.A. (CARVIMSA)

Ecopacking Cartones S.A.

Packingtech Peru S.A.C.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Smurfit Westrock completed the acquisition of corrugated assets in Ecuador, extending its Andean reach and opening synergy options with Peruvian operations.

- January 2026: Trupal closed 2025 with production records and sales 10% above plan, propelled by agro-export box demand, and confirmed further investments in converting capacity.

- December 2025: Grupo Comeca earmarked USD 8 million for CARVIMSA and Epinsa upgrades in 2026 to sustain double-digit corrugated growth.

- September 2025: Law 32434 took effect, granting agribusiness a 15% corporate tax rate through 2035 and VAT refunds on packaging inputs, improving cash flow for fruit exporters.

Peru Corrugated Packaging Market Report Scope

The Peru Corrugated Packaging Market report encompasses a comprehensive analysis of fiber-based and polymer-based corrugated materials used for the containment, protection, and transport of goods across diverse industrial and retail sectors. The market refers to the industry that produces multi-layered boards, typically consisting of a fluted medium sandwiched between linerboards, designed to provide high strength-to-weight ratios and crush resistance for secondary and tertiary packaging.

The Peru Corrugated Packaging Market Report is Segmented by Material (Virgin Kraft Linerboard, Recycled Linerboard, Corrugating Medium, Semi-Chemical Fluting, and Other Materials), Flute Type (A Flute, B Flute, C Flute, E Flute, and F Flute), Packaging Type (Regular Slotted Containers, Die-Cut Custom Boxes, Folding Cartons, Point-of-Purchase Displays, Pallet Boxes, and Other Packaging Types), Wall Type (Single-Wall, Double-Wall, Triple-Wall, and Single Face), Printing Technology (Flexographic Printing, Digital Inkjet Printing, Litho-Lamination, Screen Printing, and Other Printing Technologies), End-User Industry (Processed Foods, Fresh Food and Produce, Beverages, Electrical Products, Personal Care and Cosmetics, E-commerce Fulfillment Centers, Pharmaceuticals, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Kraft Linerboard |

| Recycled Linerboard |

| Corrugating Medium |

| Semi-Chemical Fluting |

| Other Materials |

| A Flute |

| B Flute |

| C Flute |

| E Flute |

| F Flute |

| Regular Slotted Containers |

| Die-Cut Custom Boxes |

| Folding Cartons |

| Point-of-Purchase Displays |

| Pallet Boxes |

| Other Packaging Types |

| Single-Wall |

| Double-Wall |

| Triple-Wall |

| Single Face |

| Flexographic Printing |

| Digital Inkjet Printing |

| Litho-Lamination |

| Screen Printing |

| Other Printing Technologies |

| Processed Foods |

| Fresh Food and Produce |

| Beverages |

| Electrical Products |

| Personal Care and Cosmetics |

| E-Commerce Fulfillment Centers |

| Pharmaceuticals |

| Other End-User Industries |

| By Material | Virgin Kraft Linerboard |

| Recycled Linerboard | |

| Corrugating Medium | |

| Semi-Chemical Fluting | |

| Other Materials | |

| By Flute Type | A Flute |

| B Flute | |

| C Flute | |

| E Flute | |

| F Flute | |

| By Packaging Type | Regular Slotted Containers |

| Die-Cut Custom Boxes | |

| Folding Cartons | |

| Point-of-Purchase Displays | |

| Pallet Boxes | |

| Other Packaging Types | |

| By Wall Type | Single-Wall |

| Double-Wall | |

| Triple-Wall | |

| Single Face | |

| By Printing Technology | Flexographic Printing |

| Digital Inkjet Printing | |

| Litho-Lamination | |

| Screen Printing | |

| Other Printing Technologies | |

| By End-User Industry | Processed Foods |

| Fresh Food and Produce | |

| Beverages | |

| Electrical Products | |

| Personal Care and Cosmetics | |

| E-Commerce Fulfillment Centers | |

| Pharmaceuticals | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current Peru corrugated packaging market size and its growth outlook?

The Peru corrugated packaging market size stands at USD 0.608 billion in 2026 and is projected to reach USD 0.739 billion by 2031 at a 3.99% CAGR.

Which material leads demand in Peruvian corrugated packaging?

Recycled linerboard leads with 46.13% market share thanks to established fiber-recovery networks and competitive pricing.

Why is E flute usage rising in Peru?

E flute's thin profile lowers parcel weight and offers a smooth surface for high-resolution graphics, making it ideal for fast-growing e-commerce and subscription-box applications.

How is Law 32434 influencing corrugated packaging demand?

The tax relief and VAT refunds granted to agribusiness under Law 32434 free up capital for exporters to invest in cold-chain expansion, indirectly boosting orders for ventilated transit cartons.

Which printing technology is gaining traction for short runs?

Digital inkjet printing is advancing at a 5.38% CAGR as brands seek personalized, low-volume campaigns without flexographic plate costs.

What are the main competitive advantages of leading Peruvian converters?

Vertical fiber integration, renewable-energy operations, hybrid flexo-digital press fleets, and regional depot networks underpin faster lead times and sustainability credentials.

Page last updated on: