Personalization Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

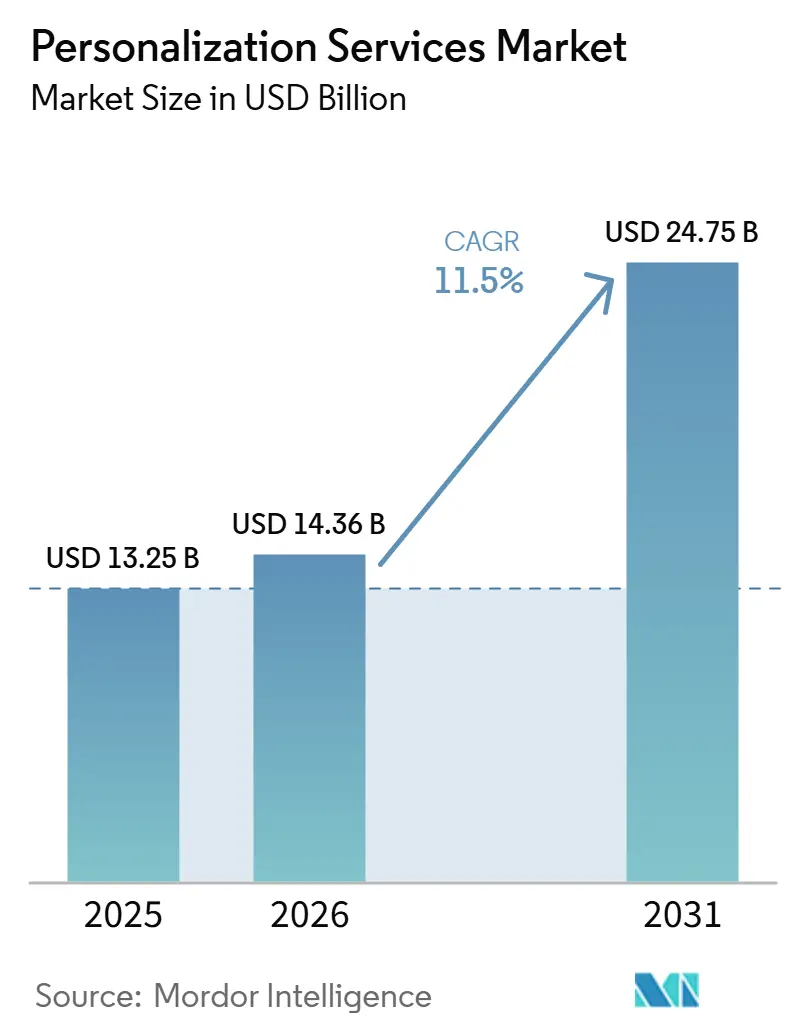

| Market Size (2026) | USD 14.36 Billion |

| Market Size (2031) | USD 24.75 Billion |

| Growth Rate (2026 - 2031) | 11.50% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Personalization Services Market Analysis by Mordor Intelligence

The Personalization Services Market size is projected to expand from USD 13.25 billion in 2025 and USD 14.36 billion in 2026 to USD 24.75 billion by 2031, registering a CAGR of 11.50% between 2026 and 2031. Growth is being shaped by the move from broad digital targeting to individualized engagement across web, mobile, commerce, and service channels. Enterprises are investing more in first-party data systems, real-time decision tools, and AI-led workflow automation because these tools improve how customer interactions are managed at scale. The Personalization Services Market is also seeing stronger demand for integration, consulting, and managed support because many enterprises still face operational gaps between their data systems and execution tools. Competition is tightening as platform vendors expand their product offerings and acquire companies, while specialist vendors focus on speed, flexibility, and vertical use cases. The strongest opportunities are emerging where buyers need privacy-aware architecture, reduced implementation burden, and ongoing optimization support rather than a one-time platform deployment.

Key Report Takeaways

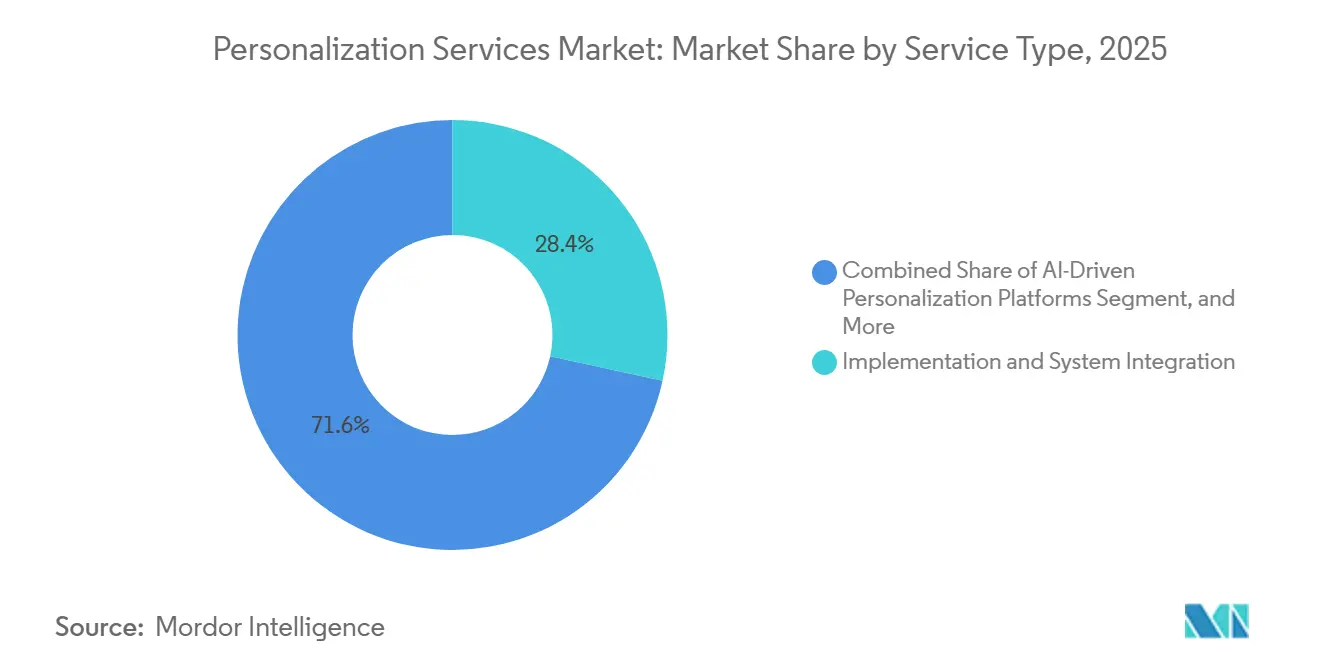

- By service type, implementation and system integration accounted for 28.41% share of the Personalization Services Market size in 2025, while AI-driven personalization platforms are projected to expand at a 14.82% CAGR through 2031.

- By deployment, cloud-based deployment held 71.26% share in 2025, while hybrid deployment is projected to expand at a 13.69% CAGR through 2031.

- By technology, web personalization platforms led with 24.83% revenue share in 2025, while managed personalization services are projected to advance at a 15.43% CAGR through 2031.

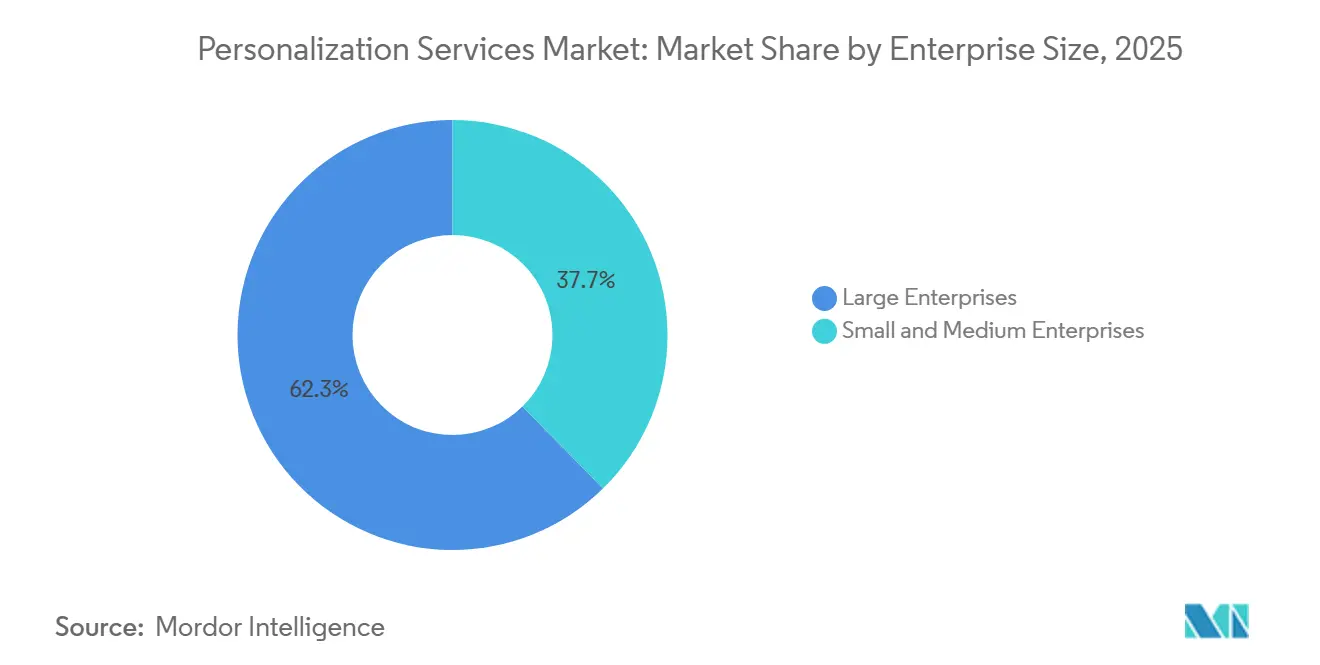

- By enterprise size, large enterprises held 62.34% share in 2025, while small and medium enterprises are projected to grow at a 14.17% CAGR through 2031.

- By end-user industry, retail and e-commerce accounted for 26.19% of the market share in 2025, while healthcare and life sciences are projected to expand at a 13.84% CAGR through 2031.

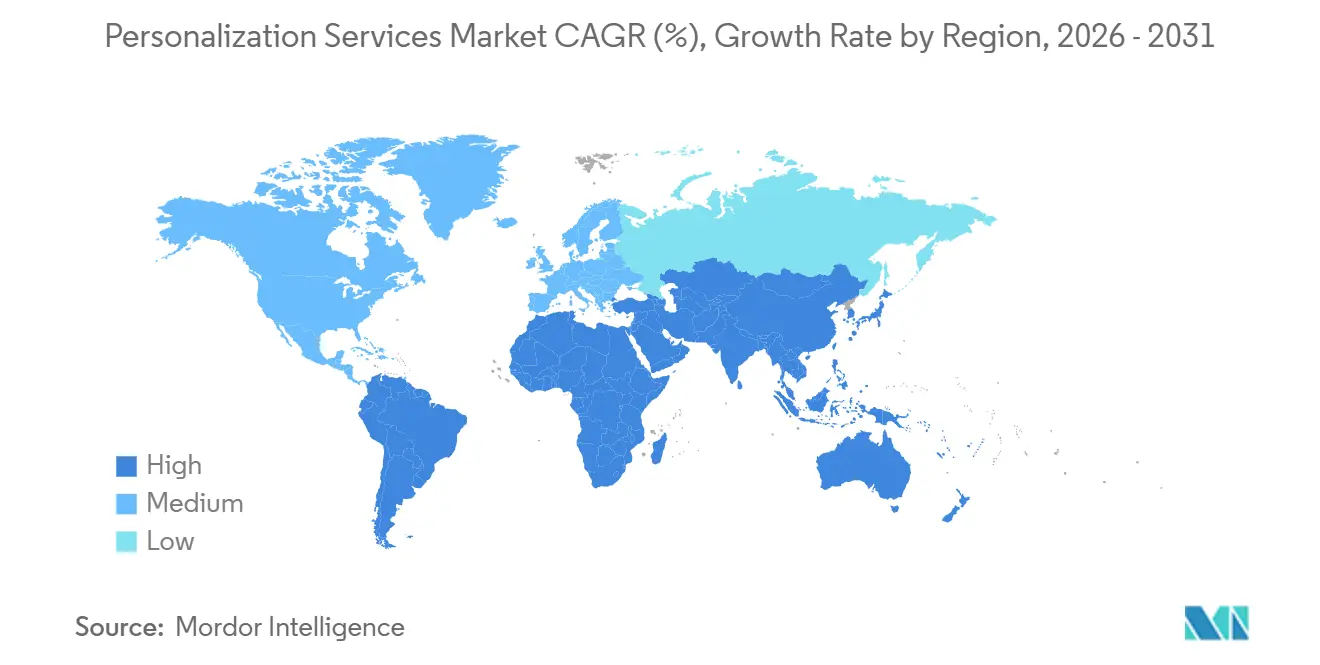

- By geography, North America held 34.72% of the Personalization Services Market share in 2025, while Asia-Pacific is projected to expand at a 14.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Personalization Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Real-Time Customer Experience Orchestration | +2.3% | Global, strongest in North America and Asia-Pacific | Medium term (2-4 years) |

| Wider Adoption of AI-Led Recommendation and Decision Engines | +2.5% | Global, strongest in Asia-Pacific and North America | Short term (≤ 2 years) |

| Expansion of First-Party Data Activation Across Digital Touchpoints | +1.9% | Global, with strong concentration in North America and Europe | Medium term (2-4 years) |

| Need for Higher Conversion Rates Across E-Commerce and Retail Funnels | +1.7% | Global, strongest in North America, Asia-Pacific, and Europe | Short term (≤ 2 years) |

| Privacy-First Personalization Architecture Driving Enterprise Investment | +1.4% | Europe and North America, with spillover to Asia-Pacific | Long term (≥ 4 years) |

| Unification Of Marketing, Service, and Commerce Data In One Stack | +1.2% | Global, with early concentration in North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Real-Time Customer Experience Orchestration

Real-time orchestration has moved closer to the center of enterprise customer strategy in the Personalization Services Market. Enterprises now want systems that can react to customer behavior in real time, rather than waiting for fixed campaign cycles. Adobe introduced CX Enterprise in April 2026, and the launch centered on agentic AI across audience assembly, content decisions, and journey execution.[1]Adobe, “Adobe Redefines Customer Experience Orchestration Vision In The Agentic AI Era,” Adobe News, news.adobe.com Amperity also introduced real-time site personalization and cart abandonment tools in May 2026, which showed that instant recognition and triggered recovery journeys are becoming more operationally accessible. This shift is driving demand for integration and consulting support, as many enterprises still run disconnected marketing, commerce, and service systems. It is also widening the advantage for vendors that can shorten the path from data capture to action across the full customer journey.

Wider Adoption of AI-Led Recommendation and Decision Engines

AI-led recommendation tools are one of the clearest growth engines in the Personalization Services Market because buyers can connect them directly to conversion and relevance goals. The market is moving away from rule-based recommendation logic and toward models that can interpret behavioral, transactional, and contextual signals together. Databricks introduced CustomerLake in 2026 as an agentic CDP within its lakehouse environment, and the launch showed how autonomous campaign analysis and audience activation are moving closer to standard deployment practice.[2]Databricks, “Introducing CustomerLake, The Agentic CDP Embedded In Databricks,” Databricks, databricks.com Salesforce also completed the Cimulate acquisition in March 2026, which added AI-powered product discovery and agentic commerce capability to its broader platform stack. These developments are reducing the distance between product discovery, recommendation logic, and execution. They are also increasing demand for managed support because enterprises need continuous tuning after the initial rollout.

Expansion of First-Party Data Activation Across Digital Touchpoints

First-party data activation is becoming more central to the Personalization Services Market as enterprises adjust to the decline of third-party tracking methods. Tealium reported in 2025 that 72% of companies were doubling down on first-party data strategies, suggesting a broad structural shift in how personalization programs are built.[3]Tealium, “2025 State Of The CDP,” Tealium, tealium.com Twilio Segment also reported that its customers synced nearly 10 trillion rows of data to cloud data warehouses in 2025, demonstrating the scale now involved in customer data unification and activation. This matters because each personalized interaction generates more behavioral data, which gives early adopters a stronger feedback loop over time. Privacy rules are reinforcing the same trend because enterprises increasingly need cleaner consent records, stronger governance controls, and clearer identity resolution before activation can happen at scale.

Need for Higher Conversion Rates Across E-Commerce and Retail Funnels

Retail and e-commerce buyers continue to invest in the Personalization Services Market because personalization remains closely tied to conversion performance. The strongest spending is shifting from isolated tools toward broader operating models that can coordinate search, merchandising, messaging, and post-purchase engagement in one flow. This is helping managed personalization services gain traction because many brands do not want to scale internal teams at the same pace as their personalization programs. In the current market structure, that pattern supports the fastest-growing technology delivery model, where managed personalization services are forecast to grow at a 15.43% CAGR through 2031. The practical change is that buyers no longer view personalization as a one-time implementation project. They increasingly expect ongoing model monitoring, workflow adjustments, and customer journey optimization as part of the service relationship.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Weak Personalization Performance Caused by Poor Data Quality | -1.3% | Global, most acute in emerging markets and mid-market enterprises | Medium term (2-4 years) |

| Enterprise Concerns over Consent Management and Data Governance | -1.0% | Europe and North America, with growing relevance in Asia-Pacific | Long term (≥ 4 years) |

| High Integration Complexity with Legacy MarTech and CRM Environments | -0.9% | Global, most acute in large enterprises with long technology histories | Medium term (2-4 years) |

| Talent Gaps in Personalization Strategy, Model Operations, and Measurement | -0.7% | Global, with sharp pressure in Asia-Pacific and South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Weak Personalization Performance Caused by Poor Data Quality

Poor data quality remains one of the clearest operational limits on the Personalization Services Market. In 2025, a report found that 76% of organizations had less than half of their CRM data accurate and complete, even though 90% recognized CRM data as central to operations. That gap matters because weak records not only reduce recommendation precision but also create poor customer experiences that are harder to correct after launch. Many enterprises still manage customer information across CRM, commerce, loyalty, marketing automation, point-of-sale, and mobile systems, and every break in that chain raises the risk of identity and messaging errors. This keeps demand high for data cleaning, identity resolution, and customer data platform services before broader personalization goals can be met. It also slows returns for vendors that enter the account before the buyer has fixed its core customer data foundation.

Enterprise Concerns Over Consent Management and Data Governance

Consent management and governance requirements continue to slow parts of the Personalization Services Market, especially in regulated regions and sectors. GDPR requires a stronger review of processing that can create high risk for individuals, and personalization programs that use automated decision logic often fall within that wider control environment.[4]GDPR.EU, “General Data Protection Regulation,” GDPR.EU, gdpr.eu The burden rises further when enterprises operate across the European Union, the United States, and the Asia-Pacific, because consent rules, storage requirements, and data-handling practices do not align neatly across jurisdictions. This can force companies to build different workflows and infrastructure layers for different markets. The result is longer deployment cycles, more legal and technical review, and higher vendor selection pressure. It also increases demand for service providers that can combine personalized delivery with governance design, documentation, and support, as well as auditable operating practices.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Integration Depth Keeps Revenue Concentrated In Implementation Work

Implementation and system integration held 28.41% share in 2025, and that position reflects the amount of work required to connect personalization tools with CRM, CDP, commerce, and execution systems. In the Personalization Services Market, buyers still face large operational gaps between the platform they purchase and the outcomes they expect. This is why implementation revenue remains concentrated even as the technology itself becomes easier to access. Strategy, design, support, and training services continue to matter because enterprises need more than software licenses to run personalized engagement across channels. AI-driven personalization platforms are projected to grow at a 14.82% CAGR through 2031, and that pace shows where future service demand is moving as automation becomes more central to delivery.

The next shift in this segment is not the removal of services, but the change in which services matter most after launch. Training and enablement are gaining relevance because many buyers still lack in-house teams that can manage AI-led decision systems over time. OECD findings in 2026 showed that AI integration remained uneven across organizations of different sizes, with time constraints and skill gaps still the main barriers. That same pressure supports advisory and managed delivery work because enterprises want performance continuity after implementation. Managed personalization support is therefore becoming a practical extension of deployment rather than a separate optional layer. In this part of the Personalization Services industry, vendors that can combine system integration with post-launch operating support are likely to hold stronger client relationships.

By Deployment: Cloud Leadership Continues While Hybrid Adoption Gains Structural Importance

Cloud-based deployment accounted for 71.26% of the mix in 2025, which made it the clear operating base for most programs in the Personalization Services Market. Buyers continue to prefer cloud environments because they reduce provisioning time and support elastic processing for high-volume customer signals. That advantage remains important for recommendation logic, journey automation, and multichannel execution workloads. At the same time, the market is not moving along a simple one-way path from on-premises to the cloud. Hybrid deployment is projected to grow at a 13.69% CAGR through 2031, which shows that compliance, residency, and system control issues are shaping the next phase of adoption.

The practical meaning of hybrid growth is that some buyers want cloud-scale speed without giving up local control over sensitive data. This is especially visible in regulated sectors where full cloud migration remains difficult for legal or operational reasons. Braze responded to this pattern in April 2026 by adding European Union-hosted infrastructure for its AI decisioning environment, aligning its offer more closely with data residency requirements. For many enterprises, hybrid architecture is becoming a stable long-term model rather than a temporary transition stage. That supports demand for deployment planning, architecture design, and integration services spanning both cloud-native and controlled local environments. It also keeps the Personalization Services Market tied closely to compliance-aware infrastructure work.

By Technology: Web Platforms Lead Current Spend While AI-Native Layers Shape Future Demand

Web personalization platforms led with a 24.83% share in 2025, reflecting the maturity of web testing, dynamic content delivery, and behavioral targeting tools. This gives the Personalization Services Market a large installed base in channel-specific technology that many enterprises already understand. Mobile app personalization and omnichannel platforms are also gaining ground as brands try to create more consistent journeys across devices and touchpoints. Customer data platforms remain central because they act as the unifying layer behind activation across all these technology categories. Twilio Segment reported a 57% surge in predictive trait volumes in 2025, indicating that CDP usage is moving deeper into real-time activation rather than remaining at the data-collection stage.

The fastest operational change is happening where enterprises no longer want to manage the full personalization stack alone. Managed personalization services are projected to expand at a 15.43% CAGR through 2031, underscoring that execution complexity is now a service issue as much as a software issue. Bloomreach made Loomi Marketing Agent generally available in June 2026, and the product turned a natural-language prompt into a built campaign workflow. That example shows how AI-native layers are reducing manual configuration while increasing expectations for always-on optimization. Buyers are therefore looking for vendors that can manage model performance, workflow design, and campaign adaptation together. In the Personalization Services Market, technology leadership is increasingly linked to operating simplicity after deployment.

By Enterprise Size: Large Enterprises Lead Revenue While Smaller Firms Create The Faster Growth Path

Large enterprises held a 62.34% share in 2025, and that lead came from deeper data, larger digital teams, and greater ability to absorb long implementation cycles. In the Personalization Services Market, those companies still account for most of the spending because their revenue base makes personalization returns easier to justify. Large buyers also tend to run more channels, more products, and more customer records, which raises the value of integrated personalization systems. Small and medium enterprises, however, are projected to grow at a 14.17% CAGR through 2031, making them the faster-moving demand pool. The Personalization Services Market size for small and medium enterprises is therefore expanding through models that reduce coding needs, shorten setup time, and limit upfront operational burden.

OECD work in 2026 showed sustained uptake of AI tools among smaller enterprises, especially when off-the-shelf solutions reduced setup friction and investment requirements. That pattern helps explain why SME demand is moving toward modular and outcome-led service models rather than full consultative programs. Bloomreach strengthened its position in this space in April 2026 with Loomi AI for Shopify, which was built to support personalization across multiple touchpoints without coding or IT support. This kind of product-market fit is changing how smaller buyers enter the Personalization Services Market. It also means service providers need simpler deployment paths, faster onboarding, and clearer operating value for smaller accounts. In the Personalization Services industry, SME growth is creating a separate delivery model rather than just a smaller version of enterprise demand.

By End-User Industry: Retail Holds The Largest Base While Healthcare Expands The Fastest

Retail and e-commerce accounted for a 26.19% share in 2025, making it the largest end-user group in the Personalization Services Market. The reason is direct: retail programs can connect personalization activity to conversion, basket value, merchandising, and repeat engagement more quickly than most other sectors. BFSI remained another large user group because digital banking and financial product journeys increasingly rely on targeted recommendations and next-step guidance. Media, telecom, manufacturing, and public sector demand also continued to build, although each uses personalization in different ways. Healthcare and life sciences are projected to grow at a 13.84% CAGR through 2031, and that faster pace is shifting attention toward patient engagement and navigation use cases.

Healthcare growth is being shaped less by traditional promotion and more by individualized communication that supports care decisions and access. UnitedHealthcare introduced Avery in March 2026 as a generative AI companion that personalizes health navigation using member benefits and demographic information. That move showed how personalization in healthcare is moving into practical service delivery rather than staying limited to information portals. The sector is also becoming more important because member experience and engagement quality are now stronger parts of how large health organizations think about performance. In the Personalization Services Market, this creates room for vendors that can combine regulated data handling with adaptive communication tools. It also broadens the demand base beyond the retail-centered model that defined earlier market development.

Geography Analysis

North America held a 34.72% share in 2025, making it the largest regional block in the Personalization Services Market. The region benefits from mature cloud infrastructure, deep enterprise software adoption, and a large concentration of major customer experience and marketing technology vendors. The United States accounts for most of this position because it combines large enterprise buyers with vendors that continue to expand their personalization service capabilities. Canada and Mexico add regional depth, with financial services and retail use cases supporting adoption. The North American Personalization Services Market share also reflects shorter feedback loops between vendor product development and enterprise deployment, which helps move projects from procurement to execution more quickly.

Europe remains a major demand center, but the operating environment is increasingly shaped by privacy and governance requirements. GDPR and related transparency expectations push enterprises to build personalization systems on a stronger consent and documentation base than in many other regions. Germany, the United Kingdom, and France continue to lead regional demand, especially across financial services, automotive, and e-commerce. South America is still earlier in its growth cycle, with Brazil and Argentina leading adoption while privacy regulation continues to influence data infrastructure decisions.

Asia-Pacific is projected to expand at a 14.21% CAGR through 2031, making it the fastest-growing geography in the Personalization Services Market. Mobile-first digital behavior, large online commerce ecosystems, and stronger enterprise use of AI-enabled operating models are supporting growth. India is emerging as a high-opportunity market for e-commerce and healthcare use cases, while China and Southeast Asia continue to support broader platform adoption through scale and deep digital engagement. The Middle East and Africa remain at an earlier stage, but national digital transformation efforts in Saudi Arabia and the United Arab Emirates are helping create a stronger foundation for future personalization demand.

Competitive Landscape

The Personalization Services Market remains moderately fragmented, as platform providers, systems integrators, and specialists compete across different parts of the value chain. No single vendor controls the full-service opportunity, even though several large software providers maintain strong enterprise relationships and broad product portfolios. This keeps competition active around implementation speed, integration depth, deployment flexibility, and managed support quality. The market is also becoming more layered, with some vendors selling platforms, others focusing on service delivery, and others combining both through acquisitions and product expansion. In the Personalization Services Market, that mix favors companies that can connect data, orchestration, content, and execution without adding too much operating complexity for the buyer.

Salesforce continued building a broader full-stack position in 2026 through deals that added agentic commerce, customer agent, and content capabilities. The Cimulate acquisition strengthened AI-led product discovery, while the agreement to acquire Fin expanded customer-agent capabilities within the Agentforce ecosystem. Adobe also expanded its position with CX Enterprise, which tied open standards and agentic orchestration more directly to enterprise experience management.

Specialist vendors are building durable positions by solving more focused operating problems inside the Personalization Services Market. MoEngage strengthened its offer in June 2026 through the Aampe acquisition, which added per-user autonomous decisioning capability to customer engagement workflows. Bloomreach also pushed further into lower-friction execution with Loomi tools for both enterprise campaign automation and Shopify-based activation. This leaves a clear opening in mid-market accounts where buyers want stronger outcomes than self-service tools can offer, but do not want the cost and timeline of large enterprise programs.

Personalization Services Industry Leaders

Adobe Inc.

Salesforce, Inc.

Oracle Corporation

SAP SE

IBM Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: MoEngage, the agentic customer engagement platform, acquired San Francisco-based Aampe in an all-cash deal reportedly worth tens of millions of dollars, adding per-user AI agent infrastructure that enables autonomous 1:1 decisioning across channel, timing, and message for every individual customer. The deal positioned MoEngage as a contender for enterprise buyers seeking personalization granularity beyond segment-level orchestration.

- June 2026: Bloomreach made its Loomi Marketing Agent generally available, converting a single natural-language prompt into a fully built campaign workflow. The release targeted the growing demand for agentic, low-operational-overhead personalization infrastructure among B2C retailers.

- May 2026: Amperity unveiled AI assistants and real-time site personalization and cart abandonment tools at its Amplify 2026 event, enabling brands to recognize customers instantly, convert anonymous visitors to known profiles, and trigger recovery workflows in-session.

- April 2026: Adobe rebranded and restructured its Experience Cloud suite as CX Enterprise, embedding agentic AI through Adobe Brand Intelligence and Adobe Engagement Intelligence to deliver personalization at scale across every customer touchpoint, built on open MCP and A2A standards.

Global Personalization Services Market Report Scope

The personalization services market refers to the ecosystem of professional, managed, and support services that help organizations deliver highly tailored, relevant experiences to customers across digital and physical touchpoints. This market excludes the actual software licenses or platform subscriptions, focusing entirely on the human expertise required to strategize, implement, integrate, and optimize personalization technologies. These technologies include web and mobile app personalization platforms, customer data platforms (CDPs), AI-driven tools, recommendation engines, and omnichannel solutions deployed across cloud, on-premise, and hybrid environments. The services cater to organizations of all sizes across diverse industries, including retail, BFSI, healthcare, and media, enabling them to leverage data analytics and machine learning to drive customer engagement, increase conversion rates, build brand loyalty, and maximize the return on investment from their personalization technology stacks.

The Personalization Services Market Report is Segmented by Service Type (Personalization Strategy and Consulting, Implementation and System Integration, Personalization Design and Experience Optimization, Managed Personalization Services, Support and Maintenance, and Training and Enablement), Deployment (Cloud-Based, On-Premise, and Hybrid), Technology (Web Personalization Platforms, Mobile App Personalization Platforms, Customer Data Platforms (CDPs), Recommendation and Decisioning Engines, AI-Driven Personalization Platforms, and Omnichannel Personalization Platforms), Enterprise Size (Large Enterprises, and Small And Medium Enterprises), End-User Industry (Retail and E-Commerce, BFSI, Healthcare and Life Sciences, IT and Telecom, Media and Entertainment, Industrial Manufacturing, Government and Public Administration, and Other End-User Industries), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Personalization Strategy and Consulting |

| Implementation and System Integration |

| Personalization Design and Experience Optimization |

| Managed Personalization Services |

| Support and Maintenance |

| Training and Enablement |

| Cloud-Based |

| On-Premise |

| Hybrid |

| Web Personalization Platforms |

| Mobile App Personalization Platforms |

| Customer Data Platforms (CDPs) |

| Recommendation and Decisioning Engines |

| AI-Driven Personalization Platforms |

| Omnichannel Personalization Platforms |

| Large Enterprises |

| Small And Medium Enterprises |

| Retail and E-Commerce |

| BFSI |

| Healthcare and Life Sciences |

| IT and Telecom |

| Media and Entertainment |

| Industrial Manufacturing |

| Government and Public Administration |

| Other End-User Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Service Type | Personalization Strategy and Consulting | ||

| Implementation and System Integration | |||

| Personalization Design and Experience Optimization | |||

| Managed Personalization Services | |||

| Support and Maintenance | |||

| Training and Enablement | |||

| By Deployment | Cloud-Based | ||

| On-Premise | |||

| Hybrid | |||

| By Technology | Web Personalization Platforms | ||

| Mobile App Personalization Platforms | |||

| Customer Data Platforms (CDPs) | |||

| Recommendation and Decisioning Engines | |||

| AI-Driven Personalization Platforms | |||

| Omnichannel Personalization Platforms | |||

| By Enterprise Size | Large Enterprises | ||

| Small And Medium Enterprises | |||

| By End-User Industry | Retail and E-Commerce | ||

| BFSI | |||

| Healthcare and Life Sciences | |||

| IT and Telecom | |||

| Media and Entertainment | |||

| Industrial Manufacturing | |||

| Government and Public Administration | |||

| Other End-User Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current and projected size of the Personalization Services Market?

The Personalization Services Market stood at USD 14.36 billion in 2026 and is projected to reach USD 24.75 billion by 2031, growing at an 11.50% CAGR over 2026-2031.

Which region leads demand for personalization services?

North America led with 34.72% share in 2025 because of mature cloud infrastructure, strong enterprise software adoption, and the presence of major vendors.

Which region is expanding the fastest through 2031?

Asia-Pacific is projected to grow at a 14.21% CAGR through 2031, supported by mobile-first digital behavior and expanding AI adoption across large commerce ecosystems.

Which service area brings in the most revenue today?

Implementation and system integration held 28.41% share in 2025, showing that deployment complexity still drives a large share of service spending.

Which end-user group is creating the biggest revenue base?

Retail and e-commerce led with 26.19% share in 2025 because personalization outcomes can be tied more directly to conversion, basket value, and repeat engagement.

What is changing most in vendor strategy across this space?

Vendors are moving toward fuller service stacks, AI-led workflow automation, and managed delivery models, while acquisitions continue to connect data, content, and decisioning capabilities.

Page last updated on: