Personal Use Facial And Skin Therapy Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

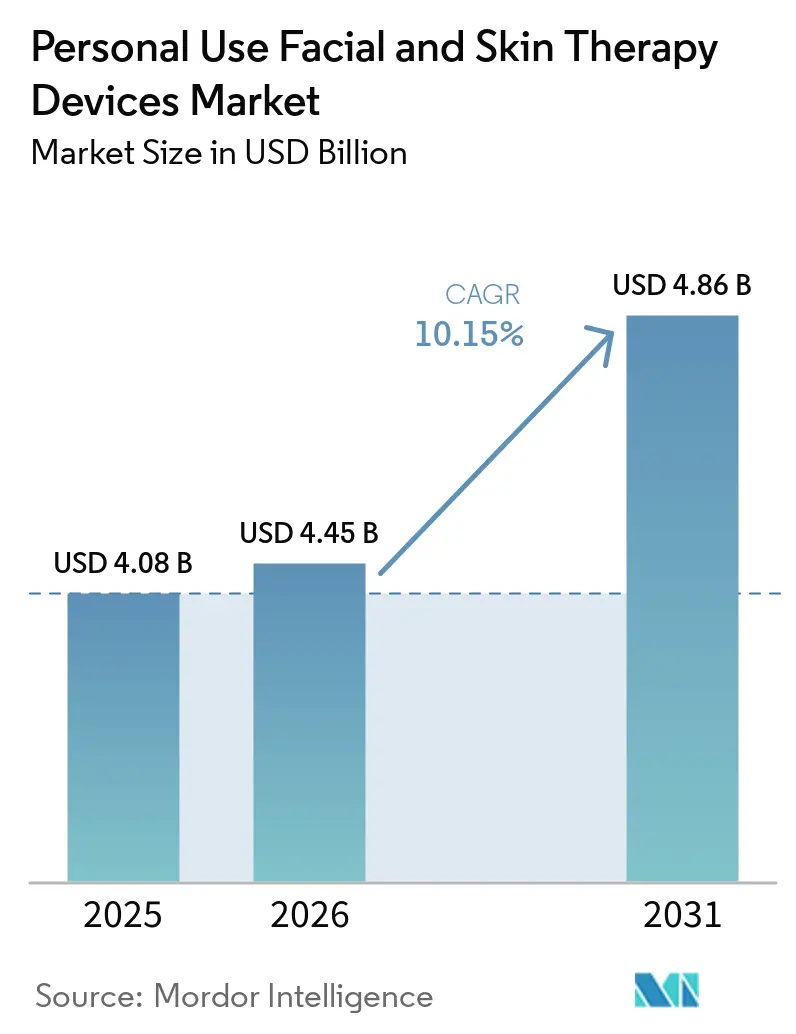

| Market Size (2026) | USD 4.45 Billion |

| Market Size (2031) | USD 4.86 Billion |

| Growth Rate (2026 - 2031) | 10.15% CAGR |

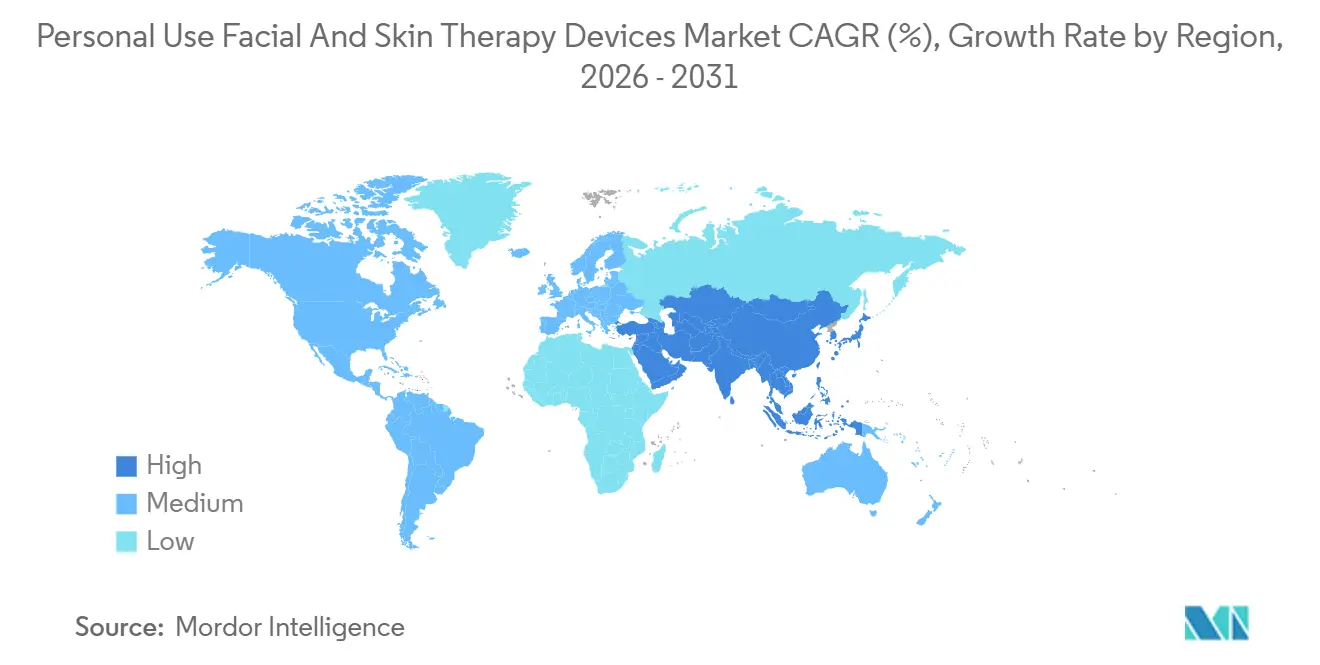

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Personal Use Facial And Skin Therapy Devices Market Analysis by Mordor Intelligence

The Personal Use Facial And Skin Therapy Devices Market size is expected to increase from USD 4.08 billion in 2025 to USD 4.45 billion in 2026 and reach USD 4.86 billion by 2031, growing at a CAGR of 10.15% over 2026-2031.

Demand is shifting from single-function mechanical brushes to multifunction, energy-based formats that deliver clinical wavelengths and pair with smartphone guidance. Rapid new-product cycles, direct-to-consumer launches, and AI-driven personalization are encouraging consumers to divert professional-treatment budgets toward at-home alternatives. Online retail adoption is accelerating as device makers bundle consumables, subscription refills, and firmware upgrades that lock users into brand ecosystems. Simultaneously, regulatory re-classifications in the European Union and tightening safety oversight by the FDA are raising the cost of non-compliant entries, indirectly favoring manufacturers with strong quality systems and clinical data.

Key Report Takeaways

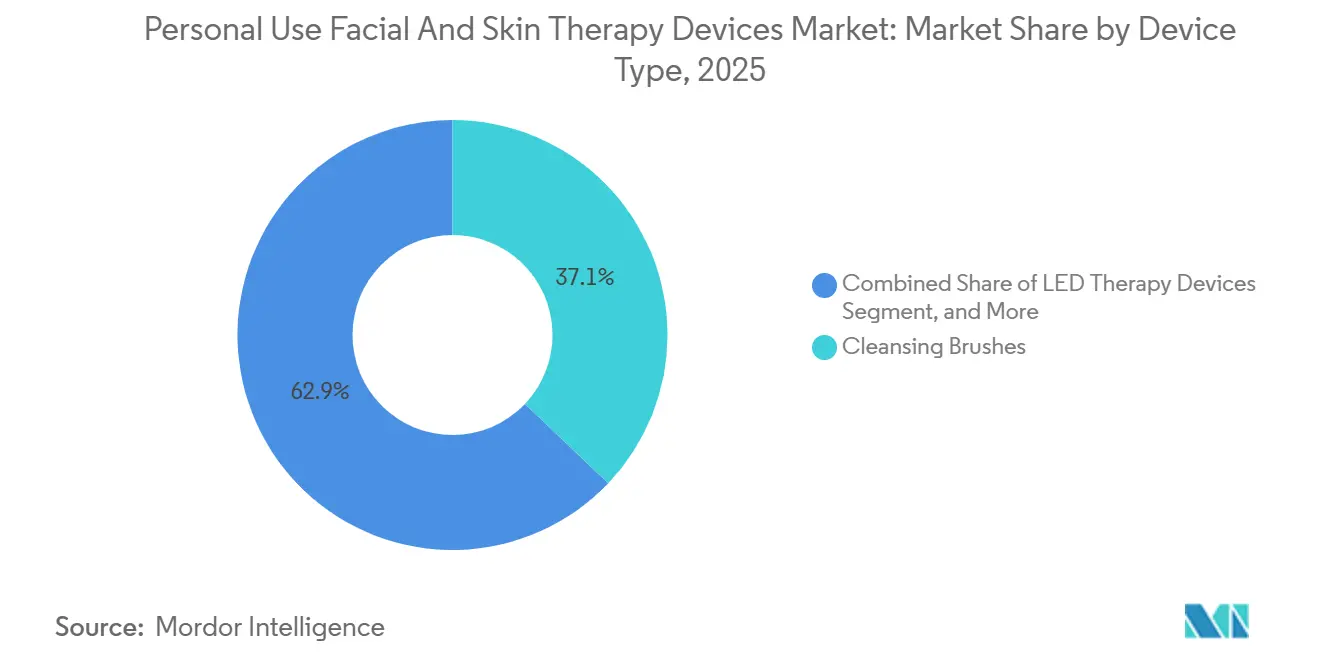

- By device type, cleansing brushes led with 37.12% revenue share of the personal use facial devices market in 2025, whereas LED therapy devices are advancing at a 12.16% CAGR through 2031.

- By technology, rotational and vibrational systems held 29.38% of the personal use facial devices market share in 2025, but LED and laser light platforms are forecast to grow at 11.65% annually.

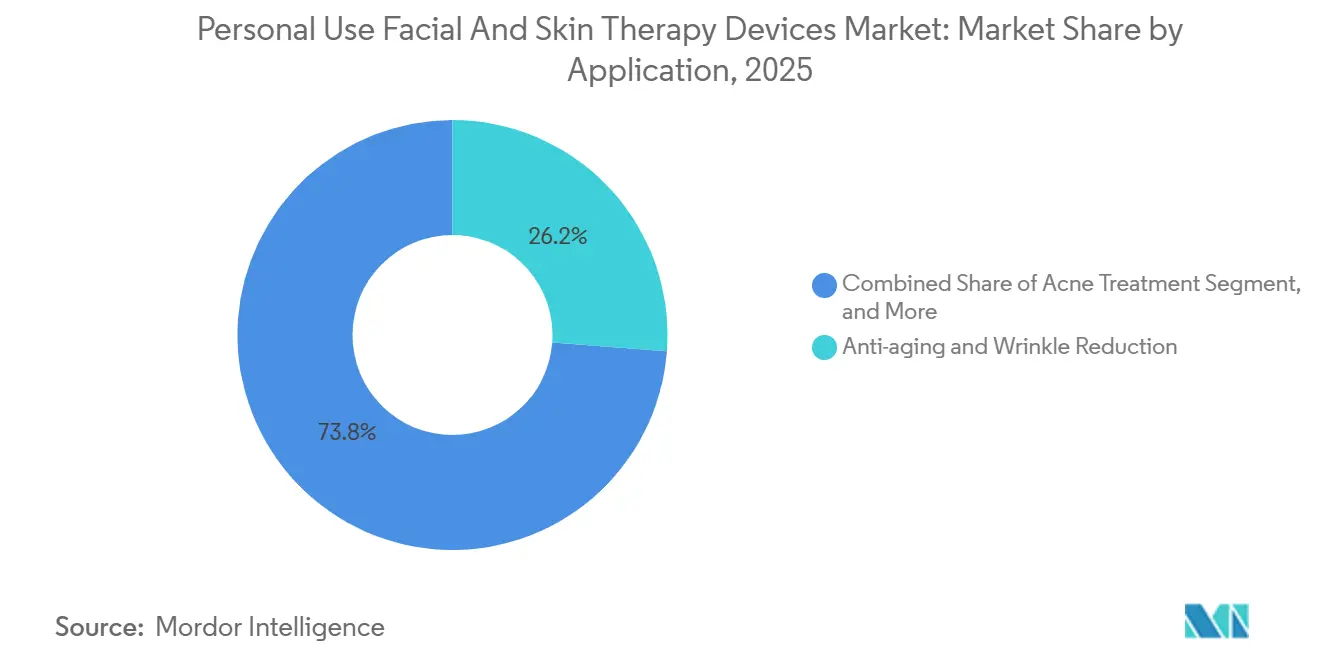

- By application, anti-aging and wrinkle reduction accounted for 26.21% of demand in 2025, while hyperpigmentation and spot correction represent the fastest trajectory at a 13.08% CAGR to 2031.

- By distribution channel, online retail captured 48.03% of value in 2025 and is expanding at 14.81% per year, reflecting direct-to-consumer strategies that minimize specialty-store fees.

- By geography, North America generated 41.83% of 2025 revenue, yet Asia-Pacific is the fastest region at a 13.03% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Personal Use Facial And Skin Therapy Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Adoption of At-Home Beauty Devices | +2.8% | Global, with highest penetration in North America and Asia-Pacific | Medium term (2-4 years) |

| Social Media & Influencer-Led Demand for Clinic-Like Results | +2.1% | Global, particularly strong in North America, South Korea, China | Short term (≤ 2 years) |

| Integration of Smartphone Connectivity & Personalized Routines | +1.9% | North America, Europe, Asia-Pacific urban centers | Medium term (2-4 years) |

| Miniaturization & High-Density Batteries Enabling Portability | +1.5% | Global, with accelerated adoption in Asia-Pacific and Middle East | Long term (≥ 4 years) |

| Rising Disposable Income in Emerging Economies | +1.2% | Asia-Pacific (India, Southeast Asia), Latin America, Middle East | Long term (≥ 4 years) |

| Regulatory Easing for Low-Energy Devices | +0.8% | North America, select Asia-Pacific markets (Japan, Australia) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of At-Home Beauty Devices

Consumers are moving treatments from clinics into bathrooms because cumulative subscription costs for professional facials exceed one-time hardware outlays over a single year. South Korean manufacturer APR shipped 2 million Medicube units in the first nine months of 2025, with repeat purchases and gifting normalizing device ownership among 25-to-45-year-old professionals. Brands now bundle conductive gels or wavelength-specific serums to capture recurring revenue, mirroring the razor-and-blade model. Samsung’s AI Beauty Mirror, introduced at CES 2026, demonstrates how diagnostics and personalized coaching transform hardware into an engagement platform. Companies that lack proprietary consumables risk ceding margin to ecosystems that integrate device, software, and refill synergy. [1]Samsung Electronics, “Samsung CES 2026 Media Kit,” samsung.com

Social Media and Influencer-Led Demand for Clinic-Like Results

Short-form video has collapsed the awareness-to-purchase funnel, with TikTok tutorials showcasing instant pore-reduction that static ads cannot match. Yet heightened exposure invites scrutiny. The UK Advertising Standards Authority removed LED mask posts in 2025 for unauthorized medical claims, pushing brands to collaborate with dermatologists, publish peer-reviewed data, and tighten influencer guidance.[2]UK Advertising Standards Authority, “LED Mask Adjudications 2025,” asa.org.uk South Korean exports of beauty devices to the United States accounted for more than half of all K-beauty online sales in 2025, propelled by dermatologist-backed content that positions hardware as an essential step in multi-layered skincare. Firms relying on unvetted endorsements risk regulatory backlash and eroded credibility.

Integration of Smartphone Connectivity and Personalized Routines

Bluetooth chips and companion apps shift value from physical motors to software experiences. NuFACE’s Trinity+ device delivers timed passes, progress photos, and firmware updates that encourage adherence and boost stickiness. Amorepacific’s WANNA-BEAUTY AI app layers generative AI make-up suggestions on top of treatment routines, converting a single-function gadget into a daily advisory service. Data privacy concerns in California and the EU compel manufacturers to process biometric images on the device, encrypt transmissions, and obtain granular consent. Vendors providing transparent opt-in flows will thrive, while cloud-dependent laggards face fines and class actions.

Miniaturization and High-Density Batteries Enabling Portability

Advances in soft lithium-ion chemistry support week-long charge cycles that make LED arrays and RF generators truly cordless. A 2024 Nature study demonstrated microscale batteries are adequate for wearables, and beauty-device brands have already adapted the chemistry. L’Oréal’s Light Straight + Multi-styler employs near-infrared elements within glass plates to straighten hair at 320 °F, three times faster than older irons, proving that small form factors can host energy-dense modules. Manufacturers signing exclusive battery-supply agreements or patenting thermal-management systems will command premiums and extend replacement cycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Safety Concerns & Risk of Improper Use | -1.4% | Global, with heightened scrutiny in North America and EU | Short term (≤ 2 years) |

| Counterfeit & Low-Quality Devices Eroding Trust | -1.1% | Global, particularly acute in Asia-Pacific and Middle East | Medium term (2-4 years) |

| Limited Clinical Evidence for Some Modalities | -0.7% | North America, Europe (markets with high evidence standards) | Medium term (2-4 years) |

| Fragmented Regulatory Standards Across Regions | -0.6% | Global, most impactful for companies operating in EU, US, China simultaneously | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Safety Concerns and Risk of Improper Use

FDA MAUDE databases recorded second-degree burns from intense pulsed light units and retinal injuries from prolonged LED exposure during 2025.[3]U.S. Food and Drug Administration, “MAUDE Adverse Event Report Database,” fda.gov At-home users often maximize settings for faster results, unlike clinicians who tailor fluence to skin response. The EU’s Medical Device Regulation now assigns Class IIa status to several LED and RF products, extending clinical-evaluation requirements and post-market surveillance. Brands have reacted with auto-shutoff timers, skin sensors, and contraindication apps, yet these additions inflate bills of material. Liability insurance is climbing, and recalls remain a headline risk.

Counterfeit and Low-Quality Devices Eroding Trust

Hong Kong Customs seized USD 23 000 worth of fake LED masks in June 2025, underscoring rampant gray-market trade. Counterfeits frequently omit required wavelengths or deliver insufficient irradiance, delivering no benefit and exposing users to burns. Some perpetrators label LED toys as “laser” systems, muddying terminology and confusing consumers. Brands are deploying blockchain authentication and tamper-evident boxes, but cross-border marketplaces remain porous. Firms tolerating unpoliced distribution will face margin compression and reputational damage.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: LED Therapy Devices Displace Brushes

Cleansing brushes held 37.12% of revenue in 2025, yet LED therapy units are advancing at a 12.16% CAGR through 2031. Foreo’s silicone Luna line, with antimicrobial credits and quarterly app updates, retains share among cleansing loyalists, but LED masks offering 630 nm red and 830 nm near-infrared wavelengths deliver collagen-stimulation claims that brushes cannot match. Multi-function headsets combining LED, microcurrent, and radiofrequency secure premium positioning. Brands without proprietary diode arrays or patented electrode layouts face commoditization as white-label copies flood e-commerce channels. Device makers that evidence synergistic effects in peer-reviewed trials will justify USD 400-plus price points, safeguarding gross margins.

Second-generation LED masks incorporate flexible printed circuits that conform to facial contours, delivering even irradiance while maintaining skin contact. L’Oréal’s 2026 prototype illustrates how material science can unlock comfortable wear and hands-free operation. Manufacturers integrating replaceable filter lenses, auto-dimming sensors, and app-based session tracking will extend replacement cycles and add software-driven upsell routes.

By Technology: Photonic Modalities Lead Future Growth

Rotational and vibrational motors controlled 29.38% of technology revenue in 2025, but photonic systems are projected to grow 11.65% per year. The personal use facial devices market share of LED and laser technologies will widen as dermatologists publish meta-analyses affirming 415 nm blue light for acne and 630 nm red light for collagen remodeling. Microcurrent and EMS devices cleared under FDA product code NFO add app coaching and compliance reminders, pushing repeat adherence. Ultrasonic scrubbers at 24–28 kHz remain popular in East Asia for exfoliation, yet limited peer-reviewed validation caps their premium price ceiling.

Infrared heat devices are migrating from hair care into facial toning, with embedded temperature sensors preventing thermal overexposure. Partnerships, such as MTG and Aisin’s Hydraid project, illustrate cross-industry innovation where automotive-grade polymers fortify beauty hardware. Brands lacking semiconductor sourcing or battery R&D alliances will lag photonic leaders that iterate at smartphone speed.

By Application: Hyperpigmentation and Spot Correction Accelerate

Anti-aging and wrinkle reduction represented 26.21% of demand in 2025, but hyperpigmentation and spot correction are rising at a 13.08% CAGR. The personal use facial devices market size for pigmentation management is expanding fastest in Asia, where melasma prevalence and post-inflammatory marks drive purchase urgency. Clear FDA paths for over-the-counter blue-light acne masks draw younger cohorts who wish to avoid pharmaceuticals. Skin rejuvenation devices, although overlapping with anti-aging, target overall luminosity rather than line reduction, requiring nuanced marketing.

Hair-removal devices dominate IPL subsegments but face salon laser competition. Brands that tailor fluence to Fitzpatrick IV–VI skin mitigate post-treatment hyperpigmentation risks and win trust among diverse users. Adoption of multi-mode handsets that toggle between acne, pigment, and wrinkle protocols will blur application categories, but manufacturers that publish randomized controlled trials across ethnicities will earn dermatologist endorsements.

By Distribution Channel: Online Retail Gains Structural Advantage

Online platforms accounted for 48.03% of revenue in 2025 and continue at a 14.81% CAGR. Specialist pages on Amazon, Tmall, and Sephora integrate AR try-on tools and dermatologist Q&A to replace in-store demos. Subscription refills for conductive gels and replacement attachments increase lifetime value and reduce price elasticity.

Specialty stores still provide tactile experience, but their share is slipping as consumers rely on influencer unboxings and video tutorials. Direct sales, including social-commerce party models, remain significant in Southeast Asia and Latin America, yet regulators eye aggressive commission structures. Pharmacies and drugstores compete on entry-level devices under USD 100, but limited shelf staff curtails education. Incumbents are adopting omnichannel data lakes, combining loyalty programs with online browsing histories to personalize promotions and curb customer-acquisition costs.

Geography Analysis

North America commanded 41.83% of 2025 value, benefiting from predictable FDA clearances and high disposable income. Consumers upgrade from cleansing brushes to LED masks and microcurrent tools every two to three years, so growth stems more from replacement cycles than first-time adopters. U.S. dermatologists frequently recommend at-home LED sessions between in-clinic RF microneedling, reinforcing mainstream acceptance. Canadian retailers promote bilingual packaging and Health Canada registration to assure French-speaking consumers, while Mexico leverages near-shoring logistics to shorten lead times and localize Spanish-language apps.

Asia-Pacific is expanding at a 13.03% CAGR. South Korea’s exports rose 42% year on year in the first half of 2025 as brands leveraged post-pandemic appetite for at-home luxury. China’s cross-border e-commerce channels let shoppers bypass daigou gray markets, spurring imports of FDA-cleared laser handsets. Japan’s aging population fuels demand for non-invasive wrinkle solutions, and local R&D emphasizes meticulous safety standards, raising the bar for foreign entrants. Southeast Asia shows early-stage penetration, but rising internet connectivity and influencer marketing foreshadow rapid upside from 2027.

Europe faces tougher margins as the EU Medical Device Regulation reclassifies LED masks and RF rollers into Class IIa, mandating costly clinical dossiers and vigilance reporting. Germany, France, and Italy remain resilient due to premium positioning and strong pharmacy networks. The Middle East, led by United Arab Emirates, buys luxury devices as status symbols, often bundling them with private‐label skincare at duty-free outlets. Latin America grows from a small base, with Brazil and Argentina absorbing currency volatility through installment payment plans and local influencer campaigns in Portuguese and Spanish.

Competitive Landscape

The personal use facial devices market remains moderately fragmented. CurrentBody acquired Tria Beauty in 2024, uniting LED, laser, and microcurrent under a single Beauty Tech Group and signaling accelerated consolidation. Shiseido and Ya-Man’s Effectim joint venture leverages Japanese manufacturing precision and cosmetic science to address Chinese consumers who value “Made in Japan” credibility. In March 2026, Amorepacific invested in Viol Medical to bring microneedle RF technology into portable formats, demonstrating how cosmetics groups court medical-device expertise to widen moats.

Rising disruptors such as RoseSkinCo and BEPLEA exemplify direct-to-consumer momentum; both brands launched on Amazon Japan in 2026 and capitalized on influencer seeding and aggressive search-engine optimization. Technology remains the key battleground. Brands negotiating exclusive rights to battery chemistries, diode wavelengths, or AI algorithms secure price leadership. Those reliant on contract manufacturers risk speed-driven competition that erodes price points. Regulatory clearances act as defensive walls: each FDA 510(k) carrying predicate claims for wrinkle reduction or acne treatment blocks copycats for several years and reassures cautious dermatologists.

Personal Use Facial And Skin Therapy Devices Industry Leaders

L’Oréal S.A.

Procter & Gamble

Illuminage Beauty Inc.

Koninklijke Philips N.V.

Conair Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Amorepacific and Viol Medical signed a memorandum of understanding to collaborate on integrating beauty and medical-device technologies, with Amorepacific making a strategic investment in Viol Medical to access its microneedle radiofrequency expertise (Sylfirm X, Scarlet, CELLINEW platforms) and develop products bridging professional treatments and at-home beauty devices for global consumers.

- January 2026: L'Oréal unveiled two CES 2026 Innovation Award-winning products: the Light Straight + Multi-styler, a hair straightener using patented near-infrared light to operate at 320°F (versus conventional 400°F+ flat irons) and deliver 3x faster, 2x smoother results; and a flexible LED Face Mask co-developed with I-Smart Developments, emitting 630 nm red and 830 nm near-infrared wavelengths for firming and smoothing skin. Both products are slated for global launch in 2027, with the LED mask subject to FDA 510(k) clearance.

- February 2025: Shenzhen Kaiyan Medical Equipment received FDA 510(k) clearance (K242593) for the CurrentBody LED 4-in-1 Zone Facial Mapping Mask (models MK-90C, MK-90M, MK66RB-F, MK-90N), expanding CurrentBody's portfolio of FDA-cleared over-the-counter light-based wrinkle-reduction devices and reinforcing its position in the LED therapy segment.

- January 2025: Amorepacific won its sixth consecutive CES Innovation Award for the WANNA-BEAUTY AI app, a generative AI-driven makeup application co-created with KAIST that analyzes user photos for skin tone and facial features, provides personalized makeup recommendations, and enables virtual try-ons via voice-activated chatbot, positioning Amorepacific in AI-driven personalization and digital beauty services.

Global Personal Use Facial And Skin Therapy Devices Market Report Scope

The personal use facial and skin therapy devices market comprises portable, electronic, or battery-operated tools designed for at-home aesthetic treatments, including anti-aging, acne, cleansing, and rejuvenation. These devices offer professional-grade technologies such as LED light therapy, radiofrequency, and microcurrent to enhance skin health, texture, and tone.

The personal use facial and skin therapy devices market report is segmented by device type, technology, application, distribution channel, and geography. By device type, the market is segmented into cleansing brushes, LED therapy devices, microcurrent devices, dermal rollers, ultrasonic skin scrubbers, multi-function devices, and others. By technology, the market is segmented into rotational/vibrational, ultrasonic, microcurrent/EMS, LED/laser light, thermal/heat, iontophoresis, plasma & radiofrequency. By application, the market is segmented into acne treatment, anti-aging & wrinkle reduction, skin rejuvenation & brightening, hair removal, hyperpigmentation & spot correction, and others. By distribution channel, the market is segmented into online retail, specialty stores, direct sales, pharmacies & drugstores. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers estimated market sizes and market trends for 17 countries across major regions worldwide. The report offers market value (in USD) for the above segments.

| Cleansing Brushes |

| LED Therapy Devices |

| Microcurrent Devices |

| Dermal Rollers |

| Ultrasonic Skin Scrubbers |

| Multi-function Devices |

| Others |

| Rotational/Vibrational |

| Ultrasonic |

| Microcurrent/EMS |

| LED/Laser Light |

| Thermal/Heat |

| Iontophoresis |

| Plasma & Radiofrequency |

| Acne Treatment |

| Anti-aging & Wrinkle Reduction |

| Skin Rejuvenation & Brightening |

| Hair Removal |

| Hyperpigmentation & Spot Correction |

| Others |

| Online Retail |

| Specialty Stores |

| Direct Sales |

| Pharmacies & Drugstores |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Device Type | Cleansing Brushes | |

| LED Therapy Devices | ||

| Microcurrent Devices | ||

| Dermal Rollers | ||

| Ultrasonic Skin Scrubbers | ||

| Multi-function Devices | ||

| Others | ||

| By Technology | Rotational/Vibrational | |

| Ultrasonic | ||

| Microcurrent/EMS | ||

| LED/Laser Light | ||

| Thermal/Heat | ||

| Iontophoresis | ||

| Plasma & Radiofrequency | ||

| By Application | Acne Treatment | |

| Anti-aging & Wrinkle Reduction | ||

| Skin Rejuvenation & Brightening | ||

| Hair Removal | ||

| Hyperpigmentation & Spot Correction | ||

| Others | ||

| By Distribution Channel | Online Retail | |

| Specialty Stores | ||

| Direct Sales | ||

| Pharmacies & Drugstores | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the personal use facial devices market?

The personal use facial devices market size reached USD 4.45 billion in 2026 and is on course for USD 4.86 billion by 2031.

How fast will LED therapy devices grow within this space?

LED therapy devices are forecast to expand at a 12.16% CAGR through 2031, outperforming mechanical cleansing brushes.

Which region offers the highest growth potential for at-home facial devices?

Asia-Pacific leads with a projected 13.03% CAGR, fueled by South Korean exports, Chinese cross-border e-commerce, and Japanese demand for non-invasive anti-aging tools.

Which distribution channel dominates sales of beauty devices?

Online retail holds nearly half of global revenue and is advancing at 14.81% annually as brands emphasize direct-to-consumer models.

What key factors restrain market growth?

Safety incidents, counterfeit proliferation, limited clinical backing for certain modalities, and fragmented regulations collectively trim the market CAGR by nearly 4%.

Page last updated on: