Peritoneal Dialysis Catheters Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

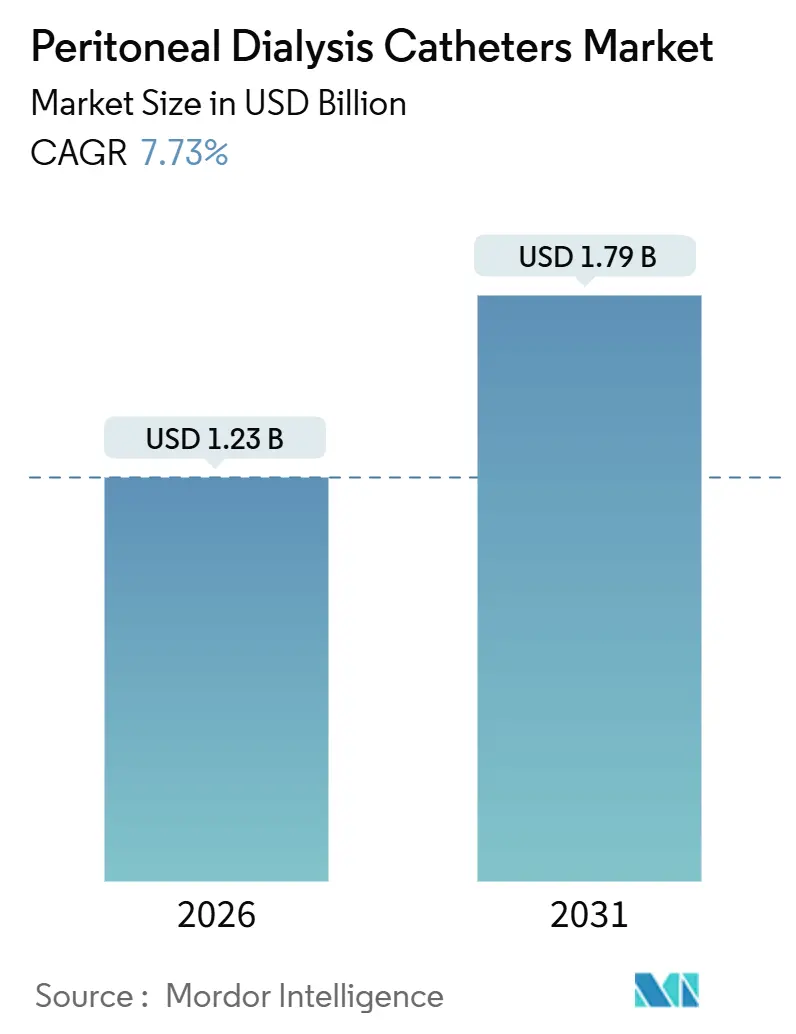

| Market Size (2026) | USD 1.23 Billion |

| Market Size (2031) | USD 1.79 Billion |

| Growth Rate (2026 - 2031) | 7.73% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Peritoneal Dialysis Catheters Market Analysis by Mordor Intelligence

The Peritoneal Dialysis Catheters Market size is estimated at USD 1.23 billion in 2026, and is expected to reach USD 1.79 billion by 2031, at a CAGR of 7.73% during the forecast period (2026-2031).

Payment reform that favors home-based renal replacement, the sunset of the ESRD Treatment Choices model, and sustained policy momentum behind Comprehensive Kidney Care Contracting and Kidney Care First underpin this expansion. Providers increasingly align clinical protocols with value-based incentives, accelerating the adoption of home modalities that rely on reliable long-dwell access devices. Catheter innovation is tracking these incentives: antimicrobial surfaces, weighted tips that resist migration, and embedded sensors are entering standard practice. On the demand side, chronic kidney disease prevalence is rising fastest in urban Asia-Pacific, while incident ESRD in high-income markets levels off, creating a mixed global growth pattern. Meanwhile, material cost pressures and infection-related technique failure present challenges that manufacturers must navigate through R&D and education initiatives.

Key Report Takeaways

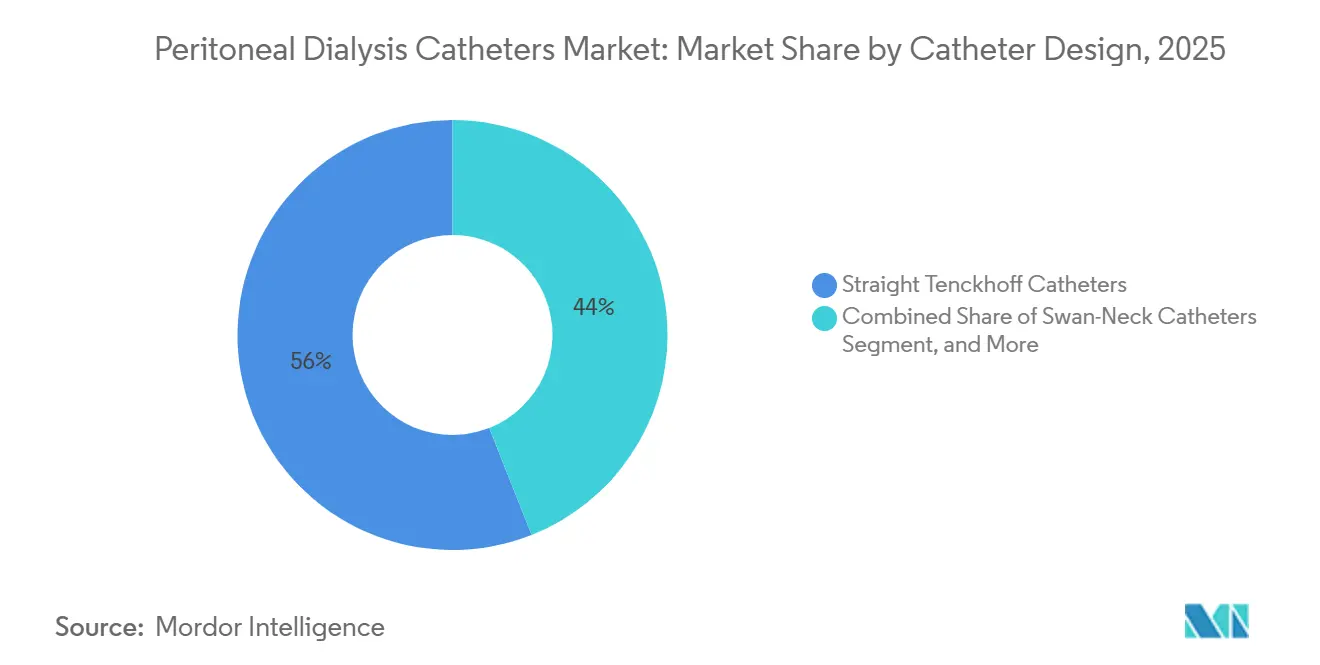

- By catheter design, straight Tenckhoff catheters led with 56.01% of the peritoneal dialysis catheters market share in 2025; self-locating and weighted-tip catheters are projected to expand at an 8.98% CAGR through 2031.

- By material, medical-grade silicone accounted for 69.87% of the peritoneal dialysis catheters market in 2025, while antimicrobial-impregnated variants are advancing at an 8.01% CAGR through 2031.

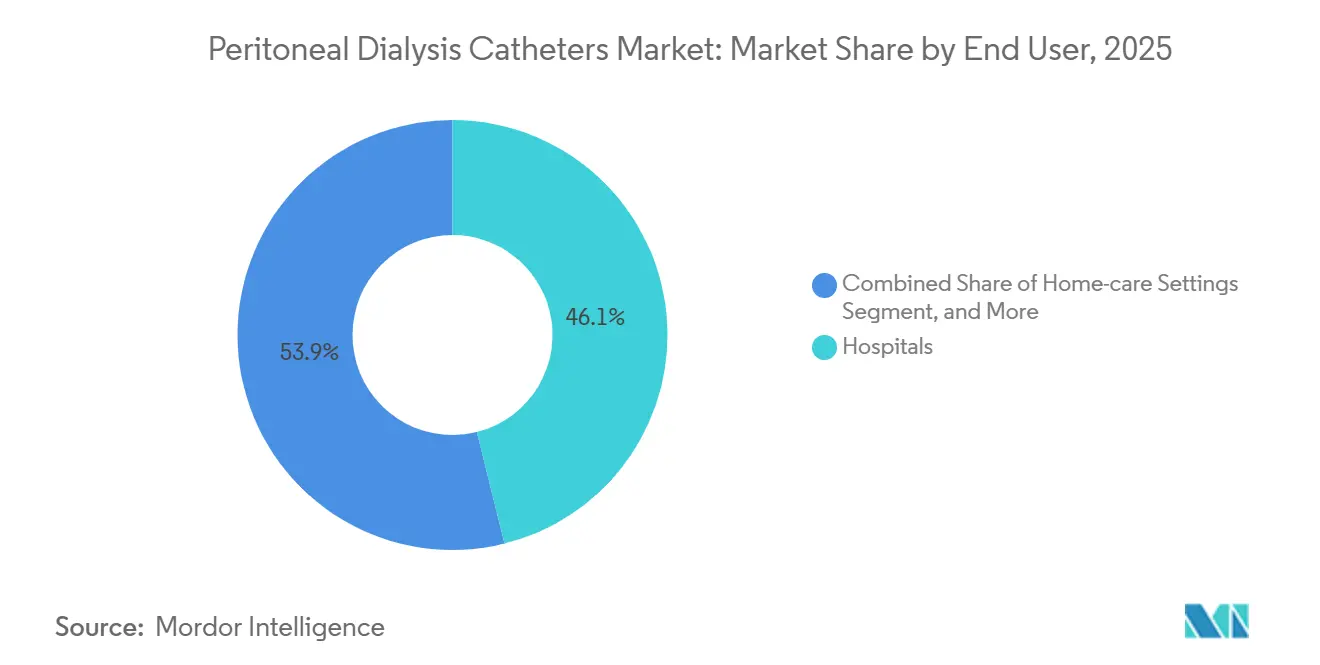

- By end user, hospitals held 46.12% share of the peritoneal dialysis catheters market size in 2025, and home-care settings are expanding at a 10.22% CAGR through 2031.

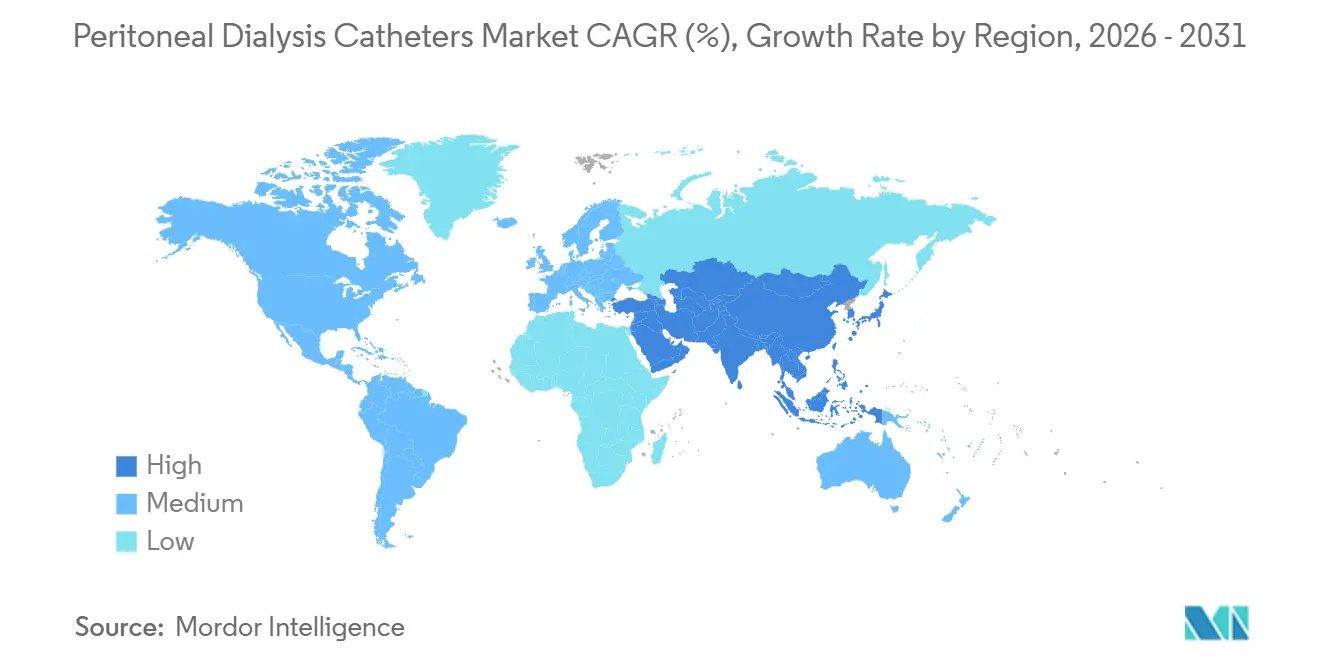

- By geography, North America captured 34.03% of the peritoneal dialysis catheters market share in 2025; Asia-Pacific is projected to grow at a 9.83% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Peritoneal Dialysis Catheters Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing CKD & ESRD Prevalence | +1.8% | Global, with highest concentration in North America, Europe, and urban Asia-Pacific | Long term (≥ 4 years) |

| Rising Adoption of Home-Based Dialysis | +1.5% | North America, Europe, Australia; emerging in China and Thailand | Medium term (2-4 years) |

| Technological Advances in Antimicrobial & Biocompatible Catheters | +1.2% | Global, led by North America and Europe; spillover to APAC | Medium term (2-4 years) |

| Favourable Reimbursement & Policy Support for Home Dialysis | +1.4% | North America (Medicare/Medicaid), select European markets, Australia | Short term (≤ 2 years) |

| Value-Based Renal-Care Payment Models Amplifying PD Uptake | +0.9% | United States (CKCC, KCF models); pilot programs in Canada | Medium term (2-4 years) |

| Expansion of Urgent-Start PD Protocols in AKI Management | +0.7% | North America, Europe, select APAC centers (Singapore, South Korea) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing CKD & ESRD Prevalence

Chronic kidney disease affects 35.5 million U.S. adults, or 14% of the population. The United States Renal Data System indicates that incident ESRD has stabilized at around 130,000 cases per year, yet total prevalence continues to rise because patients live longer.[1]United States Renal Data System, “2024 Annual Data Report,” ADR.usrds.org Incidence in India and China is increasing faster due to poorly controlled diabetes and hypertension, which together account for over 60% of new ESRD cases in urban Asia-Pacific cohorts. The WHO noted that nephrologist shortages are more than 10-fold higher in low-income countries, constraining training capacity. These epidemiological dynamics force manufacturers to supply both cost-sensitive emerging markets and technologically demanding mature regions, shaping product mix and price tiers.

Rising Adoption of Home-Based Dialysis

CMS maintained a USD 281.71 base payment rate for 2026 and preserved training add-ons that can exceed USD 150 per session, offsetting insertion and education costs.[2]CMS Innovation Center, “CKCC Model Overview,” Innovation.CMS.gov The 2025 coverage expansion for acute kidney injury patients introduced 20,000–30,000 new candidates annually. Australia’s home penetration surpassed 30% following nurse-led training programs. Thailand’s “PD First” mandate raised prevalence above 50% in public hospitals, demonstrating that regulation can alter longstanding facility-based practices.

Technological Advances in Antimicrobial & Biocompatible Catheters

ISPD updated its guideline in 2024 to set programs at 0.4 or fewer peritonitis episodes per patient-year.[3]International Society for Peritoneal Dialysis, “ISPD Peritonitis Guidelines 2024,” ISPD.org A 2025 European trial showed that silver-nanoparticle silicone catheters reduced biofilm formation by 68% and exit-site infections by 32% compared with uncoated devices. FDA clearance of Defencath, an antimicrobial lock solution, demonstrates regulatory openness to infection-control adjuncts that could migrate to PD. Manufacturers must balance softness for tissue compatibility with the rigidity required for weighted tips, prompting research into hybrid materials. Baxter’s field correction in 2025 highlighted the hurdles of integrating electronics into what has been a simple tube.

Favourable Reimbursement & Policy Support for Home Dialysis

CMS’s TDAPA and TPNIES deliver temporary payment uplifts for new PD equipment, lowering commercialization risk. Medicare Advantage, which covers 54% of beneficiaries in 2025, embeds home initiation metrics into Star Ratings, pushing insurers to promote PD. Ontario and British Columbia raised per-diem home PD funding by 12% in 2025, enabling programs to hire dedicated nurses. Commercial insurers UnitedHealthcare and Anthem launched bundled case-rate programs that package catheter insertion, training, and supplies, shortening administrative cycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Risk of Peritonitis & Catheter-Related Infections | -1.1% | Global, with higher incidence in emerging markets due to training gaps | Long term (≥ 4 years) |

| Limited PD Training Infrastructure in Emerging Economies | -0.8% | India, sub-Saharan Africa, Southeast Asia (excluding Singapore, Thailand) | Medium term (2-4 years) |

| Up-Front Cost of Advanced PD Catheters & Insertion Procedures | -0.5% | Emerging markets with out-of-pocket payment systems; select U.S. uninsured populations | Short term (≤ 2 years) |

| Silicone Raw-Material Price Volatility & Supply Constraints | -0.4% | Global, with supply concentrated in China and Southeast Asia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Risk of Peritonitis & Catheter-Related Infections

Peritonitis drives 25%–35% of technique failures and costs USD 5,000–8,000 per episode . Median U.S. rates are 0.48 episodes per patient-year, above ISPD’s 0.4 target. Exit-site infections occur in 15%–20% of patients annually, with Staphylococcus aureus and Pseudomonas aeruginosa being the most common pathogens. Rural India sees peritonitis 2.1 times higher than urban centers due to water quality and limited follow-up. High infection risk undermines payer confidence and slows modality expansion, especially in settings with scarce nurse support.

Limited PD Training Infrastructure in Emerging Economies

India has only 1,200 nephrologists for 1.4 billion people, a ratio of 0.9 per million, compared with 25 per million in the United States. Fewer than 500 certified PD nurses hamper patient education. Sub-Saharan Africa has nephrologists in only 12 of 47 countries. Brazil’s 2025 mobile simulation units cover mainly São Paulo and Rio, leaving rural areas underserved. Manufacturers must subsidize train-the-trainer programs and provide simplified insertion kits, elevating go-to-market costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Catheter Design: Tenckhoff Dominance Faces Weighted-Tip Challenge

Straight Tenckhoff devices delivered 56.01% of 2025 revenue, underscoring their clinical familiarity. Weighted-tip and self-locating formats, however, are growing at 8.98% CAGR on lower malposition rates. Coiled versions retain mid-teen share among patients with adhesions, while swan-neck types appeal in obese patients. Extended-length presternal units serve those with abdominal stomas and hernias. Regulatory clearance under the FDA 510(k) typically takes 3–6 months, with delays if novel materials emerge. Integrated ecosystems, such as Fresenius’s Harmony cycler coupled with tagged catheters, may lock clinicians into proprietary portfolios.

Weighted-tip designs cut malposition from 12% to 4% in European trials, but price premiums of 20%–30% curb uptake in cost-sensitive markets. As payers reward lower hospitalization, these devices gain traction in mature systems. With infection thresholds tightening, demand for self-locating models that reduce manipulations will likely accelerate through the outlook period.

By Material: Silicone Supremacy Challenged by Antimicrobial Innovation

Medical-grade silicone accounted for 69.87% of revenue in 2025 due to its biocompatibility and kink resistance. Antimicrobial-impregnated silicone is expanding at 8.01% CAGR as payers penalize peritonitis-linked admissions. Polyurethane serves high-strength niches but remains a minority choice due to stiffness and thrombogenicity. Silver ions, chlorhexidine, and antibiotic coatings each carry trade-offs around durability, tissue reaction, and antimicrobial resistance. Raw silicone costs remain 12% above 2023 levels following supply shocks in Shandong, pressuring margins. Manufacturers must prove infection reduction translates into lower total cost of care to justify price premiums.

Hydrogel and silicone-polyurethane hybrids target pediatric and allergy-sensitive segments. Early clinical data are promising, but the limited scale keeps per-unit costs elevated. Widespread adoption depends on robust, multi-center infection studies tied to value-based reimbursement.

By End User: Hospitals Retain Lead as Home-Care Surges

Hospitals accounted for 46.12% of 2025 demand, reflecting their role in the insertion and management of complications. Home-care environments are climbing at the fastest 10.22% CAGR as reimbursement for AKI home dialysis went live in 2025. Dialysis centers maintain a mid-30s share, which is critical for patients who need supervised exchanges. Skilled-nursing facilities and LTACHs occupy low-single-digit volume but will rise as comorbidities grow.

Remote monitoring platforms such as Baxter’s Claria with Sharesource cut hospitalization by 19% in a 2025 trial, saving USD 3,200 per patient annually. These savings strengthen the economic rationale for payers to shift to home settings, where catheter-related supply consumption per patient increases. Market incumbents offering integrated services are best positioned.

Geography Analysis

North America generated 34.03% of 2025 revenue under Medicare’s broad ESRD entitlement. The United States’ 14.1% home dialysis penetration signals headroom for catheter volumes. Canada’s 12% per-diem funding boost in 2025 will widen provincial home programs. The peritoneal dialysis catheters market in North America is expected to benefit from ongoing value-based reforms in nephrology care.

Asia-Pacific is advancing at a 9.83% CAGR, the fastest across regions, on the strength of China’s inclusion of PD supplies as essential medicines in 2024 and India’s urban middle class seeking home flexibility. China’s mandate that tertiary hospitals train two PD nurses per 100,000 population could double national prevalence to 16% by 2027. Thailand’s PD-First policy keeps incident penetration above 50%, anchoring regional growth.

Europe holds a stable mid-20s share. Germany reimburses PD at parity with hemodialysis, while the United Kingdom’s NHS actively steers modality mix to ease facility burden. PD prevalence varies ten-fold from 2% in Romania to 22% in the Netherlands, reflecting divergent staffing ratios and payment parity.

The Middle East & Africa account for a high-single-digit share. Gulf Cooperation Council investments in specialty hospitals are improving access, yet nephrologist scarcity limits uptake across much of Africa. South America holds a low-single-digit share, constrained by fiscal austerity; Brazil’s mobile simulation program is a bright spot but remains geographically narrow.

Competitive Landscape

The market is moderately concentrated. Vantive (formerly Baxter), Fresenius Medical Care, and Medtronic control significant revenue. Vantive’s January 31, 2025, spinout freed USD 4.5 billion in annual kidney revenue for targeted catheter investment. Medtronic cross-sells PD access in ICUs following its Acute Therapies acquisition.

Regional players Nipro, Terumo, B. Braun, and Cook Medical split the remainder, often focusing on price-sensitive geographies. Innovation white space includes antimicrobial catheters for diabetic cohorts and pediatric-specific designs. Digital health entrants aim to predict peritonitis using sensor-derived data, potentially shifting the advantage from hardware to analytics. ISO 13485 and 510(k) pathways favor incumbents with documented predicate devices, limiting disruptive entrants yet allowing steady incremental upgrades.

Peritoneal Dialysis Catheters Industry Leaders

B. Braun Melsungen AG

Baxter International Inc.

Fresenius Medical Care AG & Co. KGaA

Medtronic

Terumo Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Fresenius expanded HighVolumeHDF availability in Mexico through a 2-year pilot that broadens therapy options for patients with chronic kidney disease.

- January 2025: Fresenius Medical Care partnered with Mexico’s CCINSHAE to extend HighVolumeHDF across seven of 10 centers, improving access for uninsured patients.

- August 2024: Vantive completed separation from Baxter, creating a dedicated kidney-care company with USD 4.5 billion annual revenue and a focused PD catheter portfolio.

Global Peritoneal Dialysis Catheters Market Report Scope

The Peritoneal Dialysis Catheters Market refers to the global industry focused on the design, production, and distribution of indwelling access devices used to deliver chronic and acute peritoneal dialysis therapy. These catheters enable home-based and hospital-based dialysis treatment for patients with chronic kidney disease (CKD) and end-stage renal disease (ESRD).

The Peritoneal Dialysis Catheters Market Report is Segmented by Catheter Design (Straight Tenckhoff, Coiled/Pigtail, Swan-Neck, Self-locating/Weighted-tip, Extended-length Presternal), Material (Medical-grade Silicone, Polyurethane, Antimicrobial-impregnated Silicone, Other Polymers & Hybrids), End User (Hospitals, Dialysis Centres, Home-care Settings, Other Healthcare Facilities), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). Market Forecasts are Provided in Terms of Value (USD).

| Straight Tenckhoff Catheters |

| Coiled / Pigtail Catheters |

| Swan-Neck Catheters |

| Self-locating / Weighted-tip Catheters |

| Extended-length Presternal Catheters |

| Medical-grade Silicone |

| Polyurethane |

| Antimicrobial-impregnated Silicone |

| Other Polymers & Hybrids |

| Hospitals |

| Dialysis Centres |

| Home-care Settings |

| Other Healthcare Facilities |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Catheter Design | Straight Tenckhoff Catheters | |

| Coiled / Pigtail Catheters | ||

| Swan-Neck Catheters | ||

| Self-locating / Weighted-tip Catheters | ||

| Extended-length Presternal Catheters | ||

| By Material | Medical-grade Silicone | |

| Polyurethane | ||

| Antimicrobial-impregnated Silicone | ||

| Other Polymers & Hybrids | ||

| By End User | Hospitals | |

| Dialysis Centres | ||

| Home-care Settings | ||

| Other Healthcare Facilities | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the peritoneal dialysis catheters market?

It stood at USD 1.23 billion in 2026 and is forecast to reach USD 1.79 billion by 2031.

Which catheter design leads global sales?

Straight Tenckhoff catheters generated 56.01% of 2025 revenue.

Which region is growing fastest for peritoneal dialysis catheters?

Asia-Pacific is expanding at a 9.83% CAGR through 2031, driven by China and Thailand.

What drives the shift toward home-care settings?

CMS reimbursement for AKI home dialysis, remote monitoring technologies, and patient preference for flexibility.

How are manufacturers tackling peritonitis risk?

Through antimicrobial-impregnated silicone, weighted-tip designs that reduce manipulation, and connected sensors that enable early infection detection.

Page last updated on: