Peak Flow Meter Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

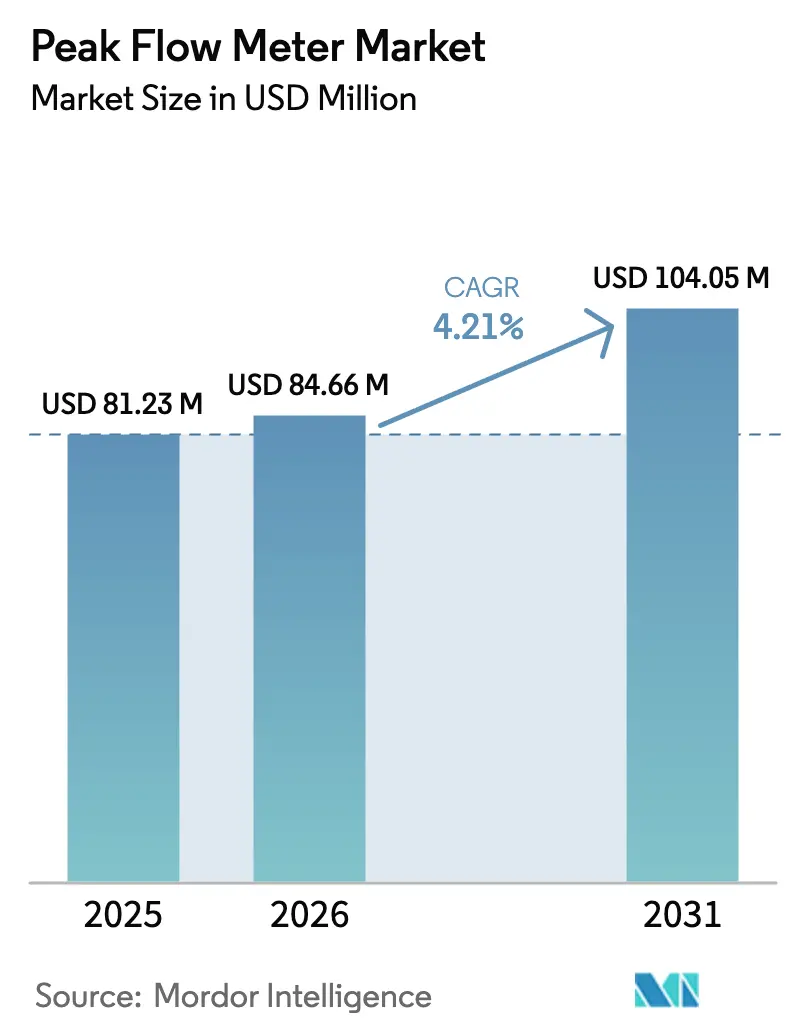

| Market Size (2026) | USD 84.66 Million |

| Market Size (2031) | USD 104.05 Million |

| Growth Rate (2026 - 2031) | 4.21% CAGR |

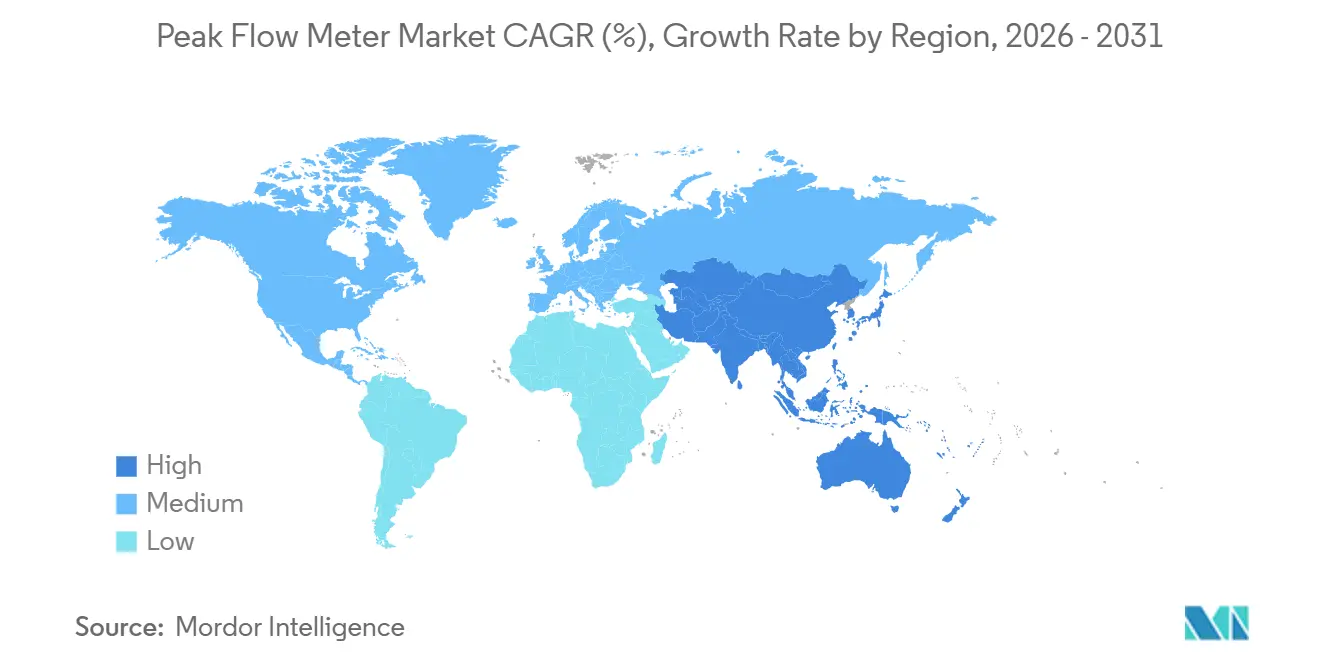

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Peak Flow Meter Market Analysis by Mordor Intelligence

The peak flow meter market size is expected to grow from USD 81.23 million in 2025 to USD 84.66 million in 2026 and is forecast to reach USD 104.05 million by 2031 at 4.21% CAGR over 2026-2031.

Widening prevalence of asthma and other chronic respiratory diseases, growing payer support for remote physiologic monitoring, and a decisive pivot toward smart, connected devices together underpin this expansion. Medicare’s 2026 reimbursement update shifted clinical purchasing toward Bluetooth- and cellular-enabled units, accelerating replacement of legacy mechanical meters. At the same time, tightening air-quality regulations in the Asia-Pacific, additional ISO and FDA interoperability standards, and a visible uptick in hospital‐to‐home care transitions sustain multi-year demand from both institutional and direct-to-consumer channels. Competitive tension is intensifying as mid-tier respiratory specialists consolidate and multinational device firms re-platform around software-centric business models.

Key Report Takeaways

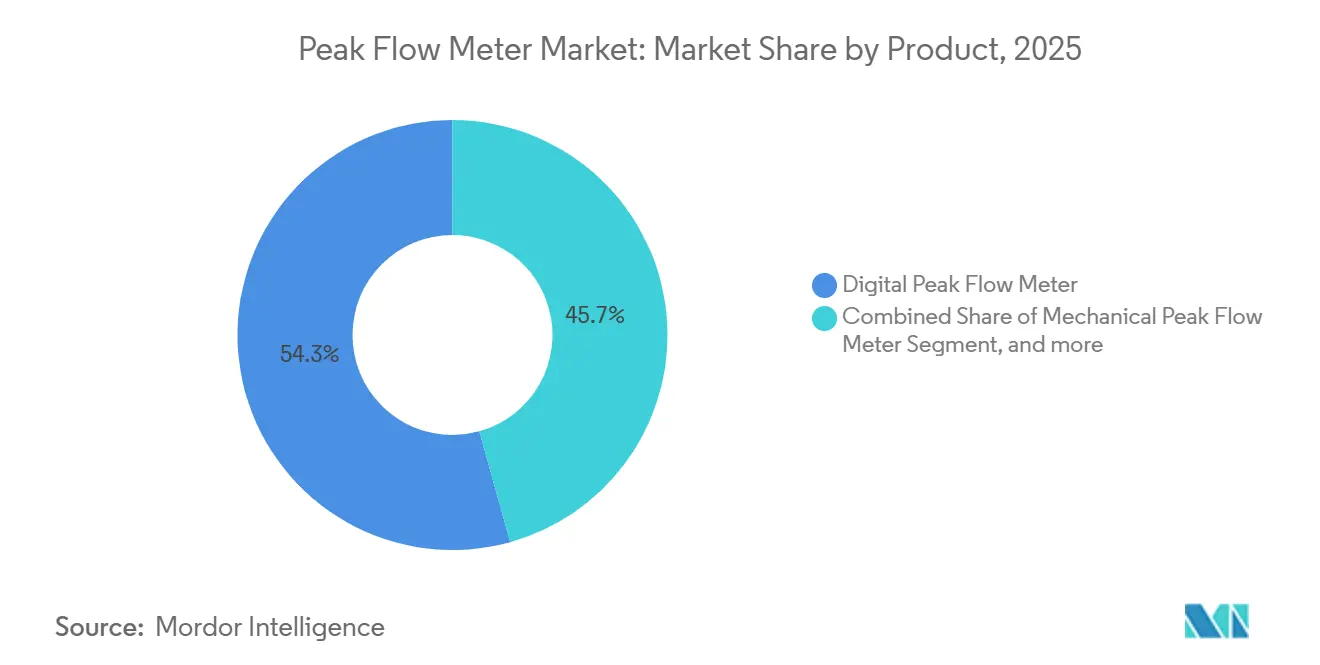

- By product, digital peak flow meters led with 54.32% revenue share in 2025; the smart/connected segment is projected to advance at a 6.43% CAGR through 2031.

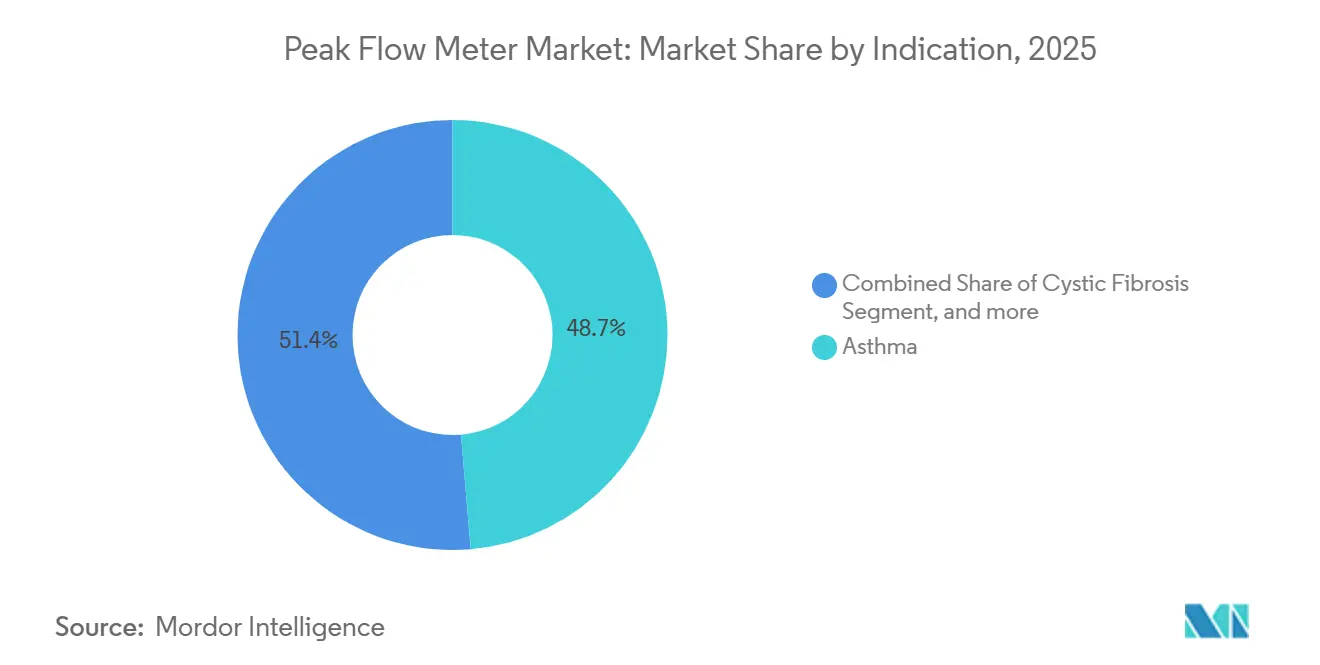

- By indication, asthma accounted for 48.65% of 2025 revenue, while cystic fibrosis applications are projected to grow at a 6.54% CAGR to 2031.

- By end user, hospitals and clinics accounted for 56.43% of revenue in 2025; home-care settings are on course for a 7.11% CAGR through 2031.

- By geography, North America captured 42.65% of 2025 global sales, whereas Asia-Pacific is forecast to post a 5.43% CAGR out to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Peak Flow Meter Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Global Burden of Chronic Respiratory Disorders | +1.2% | Global, with highest concentration in Asia-Pacific and Europe | Long term (≥ 4 years) |

| Expansion of Home Healthcare and Remote Patient Monitoring | +1.5% | North America & Europe, spill-over to Asia-Pacific urban centers | Medium term (2-4 years) |

| Technological Convergence with Digital Health Platforms | +0.9% | North America, Western Europe, early adoption in GCC and Australia | Medium term (2-4 years) |

| Favorable Reimbursement and Value-Based Care Initiatives | +1.1% | North America, select European markets (UK, Germany, Netherlands) | Short term (≤ 2 years) |

| Increasing Air Pollution and Occupational Exposure Levels | +0.8% | Asia-Pacific core, Middle East, Latin America industrial zones | Long term (≥ 4 years) |

| Growing Healthcare Investments in Emerging Economies | +0.7% | Asia-Pacific (China, India, Indonesia), Middle East (GCC), Latin America (Brazil, Mexico) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Global Burden of Chronic Respiratory Disorders

The World Health Organization counts 569.2 million chronic respiratory disease cases worldwide, including 262.4 million asthma patients and 212.3 million COPD cases. Pediatric asthma prevalence is climbing fastest in urban Asia-Pacific, broadening the addressable base for lightweight, child-friendly devices. Cystic fibrosis adds disproportionate consumption because guidelines call for daily lung-function checks; 68% of U.S. patients aged 6 and older already perform home monitoring weekly[1]Cystic Fibrosis Foundation, “2024 Patient Registry Annual Data Report,” cff.org. As death rates fall but absolute cases rise due to population aging and urbanization, the recurring demand for disposable mouthpieces and device calibration accessories persists. Portable peak flow meters, therefore, remain a primary frontline tool across primary care, pulmonology, and expanding home-care settings.

Expansion of Home Healthcare and Remote Patient Monitoring

Medicare introduced CPT codes 99454, 99457, and 99458 in 2026, reimbursing for the remote collection of 16 days of physiologic data per 30-day cycle and the associated clinician interventions. Hospitals eager to trim readmissions, coupled with clinicians seeking new revenue streams, are prescribing connected peak flow meters that autopush data to electronic records. American Hospital Association surveys show 60% of U.S. hospitals maintain at least one remote monitoring program[2]American Hospital Association, “Digital Health Adoption Survey 2025,” aha.org. This shift reallocates growth from institutional capital budgets toward prescription-driven and out-of-pocket channels, prompting vendors to bundle devices with telehealth apps and coaching services for higher lifetime value.

Technological Convergence with Digital Health Platforms

Tenovi’s Bluetooth meter, paired with a cellular gateway, illustrates next-generation design: readings sync to the cloud in seconds, enabling personalized alerts and trend dashboards. FDA recognition of IEEE/ISO 11073-10421 spells faster EHR integration[3]U.S. Food and Drug Administration, “Recognized Consensus Standards List,” fda.gov. Vendors are layering predictive analytics that flag likely exacerbations 48-72 hours ahead, giving clinicians an early window to adjust therapy. Safety’s FDA-cleared meter integrates medication reminders to address adherence lapses. Manufacturers without proprietary software now pursue partnerships with established digital-health platforms or risk hardware commoditization.

Favorable Reimbursement and Value-Based Care Initiatives

The Home Health Value-Based Purchasing model now ties agency pay to improvements in dyspnea, making objective lung-function data economically critical. Commercial payers in the U.S. mirror this trend, though heterogeneous prior-authorization rules complicate small-vendor access. In contrast, many European and Latin American systems still evaluate device coverage through cost-effectiveness scoring, which constrains the uptake of premium smart meters despite clinical enthusiasm. This policy split is prompting suppliers to build two-tier portfolios: feature-rich connected units for reimbursed markets and stripped-down mechanical meters for cost-sensitive geographies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Price Sensitivity in Low-and Middle-Income Regions | -0.6% | Asia-Pacific (excluding Japan, Australia), Latin America, Middle East & Africa (excluding GCC) | Long term (≥ 4 years) |

| Competition from Multifunction Pulmonary Diagnostic Systems | -0.4% | North America, Europe, specialty respiratory centers globally | Medium term (2-4 years) |

| Regulatory and Quality Compliance Complexities | -0.3% | Global, with highest friction in emerging markets lacking harmonized standards | Short term (≤ 2 years) |

| Limited Clinical Training and Patient Adherence Challenges | -0.5% | Global, particularly acute in home-care settings and pediatric populations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Price Sensitivity in Low- and Middle-Income Regions

Out-of-pocket payment dominates healthcare financing across much of Asia-Pacific, Latin America, and Africa, capping feasible retail prices below USD 20 for basic models. Public tenders often mandate lowest-bid compliance, sidelining Bluetooth units that retail at USD 80-150. Currency swings further suppress demand when local denominations weaken against the U.S. dollar. Without multilateral subsidy programs, vendors must choose between wafer-thin margins or pulling back from these territories.

Competition from Multifunction Pulmonary Diagnostic Systems

Specialty clinics gravitate toward integrated devices that combine peak flow, spirometry, and pulse oximetry, trimming capital budgets and streamlining billing. Units from Vyaire Medical and Cosmed cost USD 5,000-10,000 and now occupy exam-room footprints once held by single-function meters. Peak flow meter manufacturers respond by emphasizing portability and remote-care suitability, but as multifunction platforms miniaturize, differentiation hinges increasingly on software and data services.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Connectivity Drives Differentiation

Digital models held 54.32% revenue share in 2025, but smart/connected units are on track for a 6.43% CAGR, eclipsing the broader peak flow meter market by over 200 basis points. Medicare’s 16-day data rule effectively steers prescribers toward meters that transmit readings automatically, and commercial insurers mirror this stance with preferred-vendor rosters. Mechanical devices remain price-sensitive in some regions while facing relentless discounting as offshore manufacturing scales. Smart meters list for USD 80-150 and justify premiums through automated alerts and EHR integration. Early independent audits suggest that connected units lift measurement frequency by 30-40% compared with manual logbooks, though long-term adherence still demands robust care-team workflows. FDA recognition of IEEE/ISO 11073-10421 catalyzes plug-and-play interoperability, creating a technical moat around well-engineered connected offerings.

The peak flow meter market for smart devices is projected to reach USD XX million by 2031, capturing a growing share of total revenue as payers hardwire connectivity into coverage policies. Digital devices without real-time upload functions risk a demand cliff once smartphone penetration exceeds 80% in most developed economies. Mechanical meters will persist, particularly where broadband access is unreliable, yet generate limited profit due to commoditized pricing. Vendors that couple hardware sales with subscription-based analytics and coaching can unlock recurring revenue and cushion primary-device margin erosion, positioning themselves for sustained leadership as remote monitoring scales globally.

By Indication: Cystic Fibrosis Outpaces Asthma

Asthma accounted for 48.65% of segment revenue in 2025, reflecting its widespread prevalence and the guideline-driven emphasis on self-monitoring. Nevertheless, cystic fibrosis is slated to grow at a 6.54% CAGR through 2031, buoyed by precision-medicine protocols that mandate daily lung-function checks to detect subclinical decline. The Cystic Fibrosis Foundation reports that 68% of U.S. patients aged 6 and above adopted weekly home monitoring, a frequency dramatically higher than observed in routine asthma care. COPD patients, numbering 212.3 million globally, remain underserved by standalone meters, instead leaning on multi-parameter tools that track oxygen saturation alongside airflow. Occupational lung health and post-viral sequelae offer adjacent growth niches but currently represent low-single-digit shares.

Segment leaders are tailoring product variants to cystic fibrosis use cases, for example, extending flow-range capability and integrating registry uploads. The peak flow meter market share for cystic fibrosis is expected to climb by several points as therapy personalization imperatives widen. Asthma retains volume dominance; however, growth hinges on solving adherence challenges through user-centric apps and clinician-prompted interventions. COPD prospects may improve once bundled devices that merge peak flow, SpO2, and symptom tracking reach price parity with single-function meters, unlocking broader payer acceptance.

By End-User: Home Care Accelerates

Hospitals and clinics accounted for 56.43% of 2025 revenue, owing to their gatekeeper role in diagnosis and device initiation. Yet home-care channels are forecast to grow at a 7.11% CAGR through 2031, capturing share as value-based programs reward early detection of exacerbations and consumer comfort with telehealth rises. The peak flow meter market size in home settings is projected to nearly double, buoyed by clinician stipend codes that cover device provisioning and monthly data review. Sports-medicine deployment remains a niche but growing field, with elite teams incorporating airflow metrics into athlete recovery protocols.

Institutional buyers still influence product standards and training curricula, so vendors must maintain dual sales motions: capital-equipment style engagement with hospitals and DTC marketing to informed consumers. Recurring revenue from software subscriptions and consumables strengthens the manufacturer's economics in home channels, offsetting thinner margins on hardware. The supply chain must, however, support rapid drop-ship logistics, patient onboarding, and multilingual app interfaces, adding operational complexity compared with hospital bulk orders.

Geography Analysis

North America, which accounts for 42.65% of 2025 global sales, benefits from Medicare CPT 99454 reimbursement, strong alignment with commercial payers, and widespread EHR integration that simplifies data flows. Over 60% of U.S. hospitals run at least one remote patient monitoring program, and peak flow data now feeds directly into quality-improvement dashboards, reinforcing purchase decisions. Canada trails the U.S. on reimbursement breadth, yet provincial telehealth funding is expanding, sustaining moderate growth. Mexico, while price-sensitive, shows early tender activity for mechanical meters supplied through public respiratory health campaigns.

Asia-Pacific is poised for the fastest regional uplift, registering a 5.43% CAGR to 2031. Escalating particulate pollution, combined with aging demographics in China and Japan, underpins steady demand. China’s Healthy China 2030 strategy finances chronic-disease monitoring pilots across high-smog provinces, including subsidies for connected lung-function devices in community clinics. India’s National Digital Health Mission lays the technical groundwork for tele-pulmonology, but heterogeneous state budgets slow the nationwide rollout. Mature economies such as Australia exhibit high penetration of Bluetooth units, whereas many Southeast Asian markets still rely on mechanical meters costing less than USD 20 because broadband reach and formal reimbursement remain limited.

Europe presents a mixed picture. Germany, the United Kingdom, and the Netherlands fund remote respiratory monitoring under national insurance schemes, yet stricter cost-effectiveness assessments cap premium pricing. Southern and Eastern European states face tighter budgets and slower ramp-ups in MDR compliance, stalling new product introductions. Meanwhile, Gulf Cooperation Council countries expand hospital digitization programs, fueling orders for connected meters, although the broader Middle East and Africa market wrestles with infrastructure gaps and high price sensitivity. South America follows comparable dynamics: Brazil’s public system prioritizes infectious-disease needs, but private insurers in urban centers embrace tele-respiratory offerings, creating a two-speed adoption profile.

Competitive Landscape

Roughly 20 vendors compete, splitting share across multinational conglomerates—Philips, Omron, ResMed—and respiratory-focused specialists such as Vitalograph and Trudell Medical. Consolidation momentum is evident: Trudell’s November 2024 acquisition of Vyaire’s respiratory diagnostics unit brought together pulmonary function testing, aerosol delivery, and peak flow assets into a single respiratory portfolio. 3M’s spin-off of its healthcare arm to Solventum in April 2024 freed up market space for rivals to court its former institutional clients. Strategic thrusts cluster in three directions: 1) embedding IoT and AI analytics to shift emphasis from hardware to data services; 2) geographic push into urban Asia-Pacific corridors; 3) niche focus, especially pediatrics and workplace health, where customized features command premiums.

Regulatory depth and broad distribution channels give established players a buffer, yet start-ups wield agility in software differentiation. Tenovi and Safey illustrate direct-to-consumer and clinician-prescribed, app-centric models that circumvent the slow hospital procurement cycle. As predictive analytics mature, vendors that can demonstrate fewer asthma-related ED visits gain an edge in value-based purchasing negotiations. Meanwhile, mechanical-meter specialists face shrinking addressable margins and may seek alliances to bolt on connectivity modules or risk attrition.

Peak Flow Meter Industry Leaders

Koninklijke Philips N.V.

Vyaire Medical Inc.

Vitalograph Ltd.

DeVilbiss Healthcare LLC

ResMed Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Vapotherm and Flight Medical Innovations extended their collaboration to include respiratory device data-integration software, enhancing fleet-wide tele-monitoring capabilities.

- August 2024: Trudell Medical finalized its acquisition of Vyaire Medical’s respiratory diagnostics business, creating a vertically integrated respiratory platform.

- June 2024: Vapotherm signed a definitive merger agreement to go private, securing funding for product development free from quarterly earnings constraints.

Global Peak Flow Meter Market Report Scope

As per the scope of the report, a peak flow meter is a portable device used to measure the maximum airflow speed during exhalation. It helps monitor lung function and detect breathing problems such as asthma. Patients use it regularly to track their respiratory health.

The Peak Flow Meter Market is Segmented by Product (Mechanical, Digital, and Smart/Connected), Indication (Asthma, COPD, Cystic Fibrosis, and Other Indications), End-User (Hospitals & Clinics, Home-Care, Specialty Respiratory Centers, and Sports Medicine & Fitness Centers), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Mechanical Peak Flow Meter |

| Digital Peak Flow Meter |

| Smart/Connected Peak Flow Meter |

| Asthma |

| Chronic Obstructive Pulmonary Disease (COPD) |

| Cystic Fibrosis |

| Other Indications |

| Hospitals & Clinics |

| Home-Care Settings |

| Specialty Respiratory Centers |

| Sports Medicine & Fitness Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Mechanical Peak Flow Meter | |

| Digital Peak Flow Meter | ||

| Smart/Connected Peak Flow Meter | ||

| By Indication | Asthma | |

| Chronic Obstructive Pulmonary Disease (COPD) | ||

| Cystic Fibrosis | ||

| Other Indications | ||

| By End-User | Hospitals & Clinics | |

| Home-Care Settings | ||

| Specialty Respiratory Centers | ||

| Sports Medicine & Fitness Centers | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the peak flow meter market in 2031?

The peak flow meter market is forecast to reach USD 104.05 million by 2031.

Which product segment is growing fastest?

Smart and connected meters are expanding at a 6.43% CAGR through 2031, the highest among product categories.

Which patient indication shows the strongest growth outlook?

Cystic fibrosis applications are expected to register a 6.54% CAGR to 2031 due to precision-medicine protocols mandating daily monitoring.

How are reimbursement policies influencing device adoption?

Medicare CPT 99454 and related codes reimburse 16 days of remote physiologic data per month, steering clinicians toward connected meters that automate uploads.

Which region is set to grow quickest?

Asia-Pacific holds the strongest regional CAGR forecast at 5.43%, propelled by pollution-driven disease prevalence and expanding digital-health infrastructure.

What strategic moves are competitors making?

Leading vendors are acquiring complementary respiratory businesses, embedding AI analytics into devices, and targeting home-care channels to secure recurring revenue.

Page last updated on: