Passover Humidifiers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

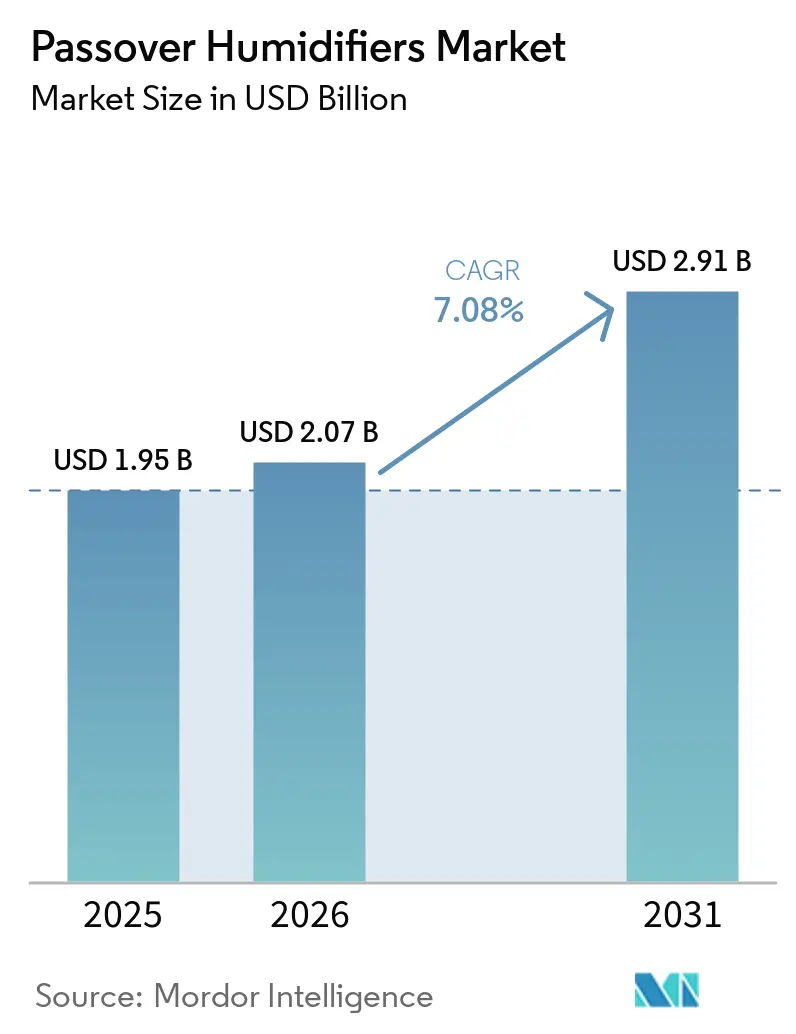

| Market Size (2026) | USD 2.07 Billion |

| Market Size (2031) | USD 2.91 Billion |

| Growth Rate (2026 - 2031) | 7.08% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Passover Humidifiers Market Analysis by Mordor Intelligence

The Passover Humidifiers Market size was valued at USD 1.95 billion in 2025 and is estimated to grow from USD 2.07 billion in 2026 to reach USD 2.91 billion by 2031, at a CAGR of 7.08% during the forecast period (2026-2031).

Robust diagnostic pipelines for obstructive sleep apnea (OSA), tariff-driven supply-chain reshoring, and the rise of connected care platforms are reinforcing demand even as reimbursement headwinds tighten gross margin. Manufacturers are pivoting toward single-use, pre-filled chambers that curb infection risk and simplify patient adherence tracking under Medicare’s MIPS measure #279. At the same time, integrated heated-humidifier CPAP platforms threaten the traditional accessories channel, pushing incumbents to embed artificial-intelligence humidity control and cloud connectivity. Supply-chain upheavals are equally pivotal: GE Healthcare absorbed USD 475 million in tariff costs and has begun localizing assembly in the United States and Mexico, mirroring moves by Medtronic and Boston Scientific.

Key Report Takeaways

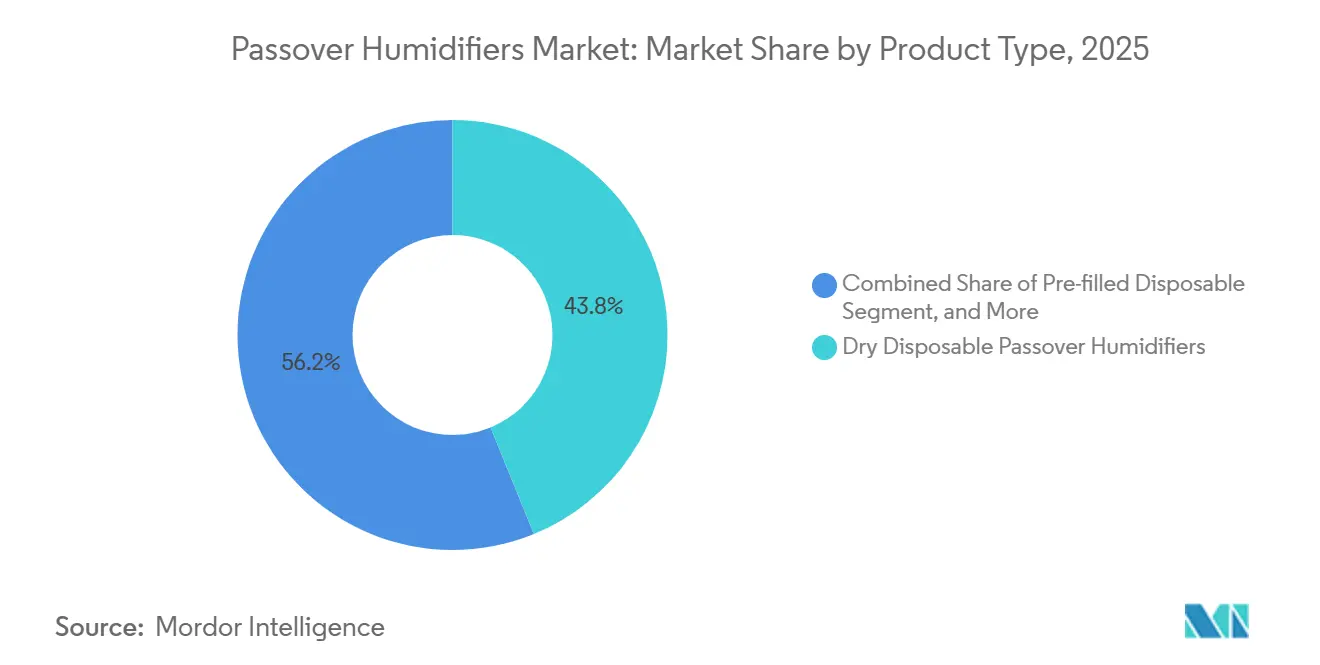

- By product type, dry disposable units held 43.81% of passover humidifiers market share in 2025. Pre-filled disposable variants are advancing at a 9.09% CAGR to 2031, the fastest pace within the product mix.

- By application, CPAP therapy led with 48.57% revenue share in 2025. High-flow nasal cannula and oxygen therapy are projected to grow at 11.78% CAGR through 2031.

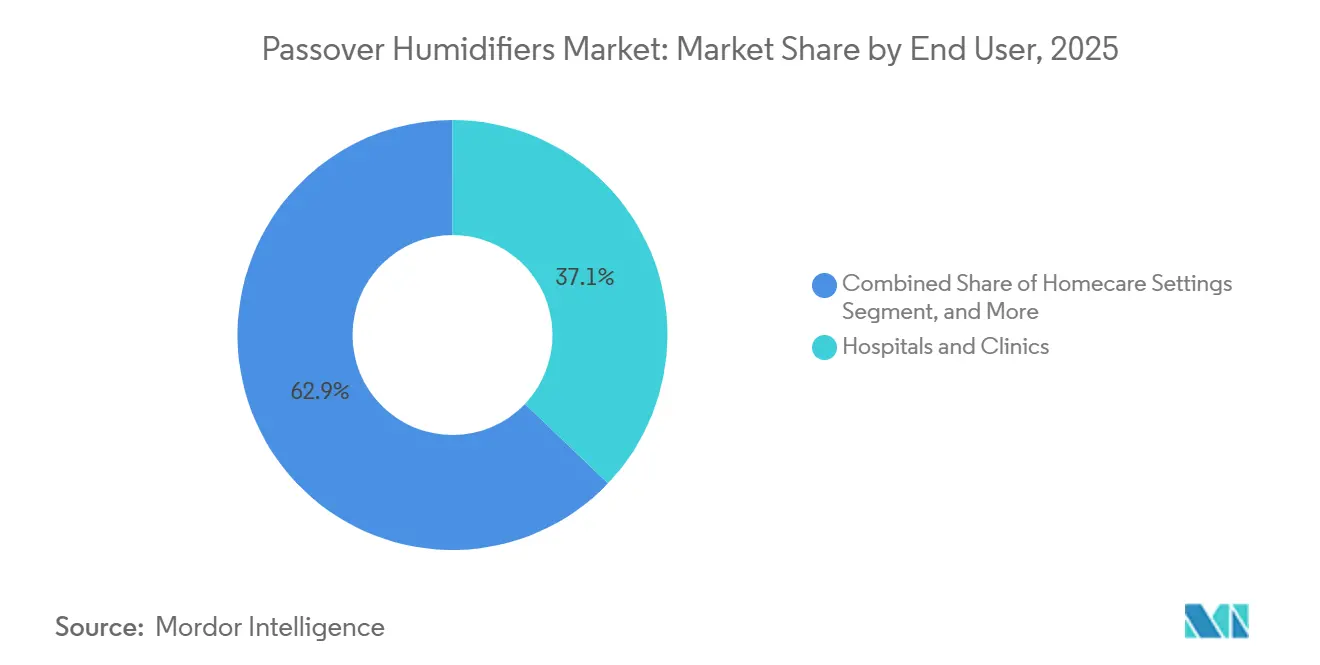

- By end user, hospitals and clinics captured 37.12% share in 2025. Sleep centers and other specialized facilities are expanding at a 10.69% CAGR to 2031.

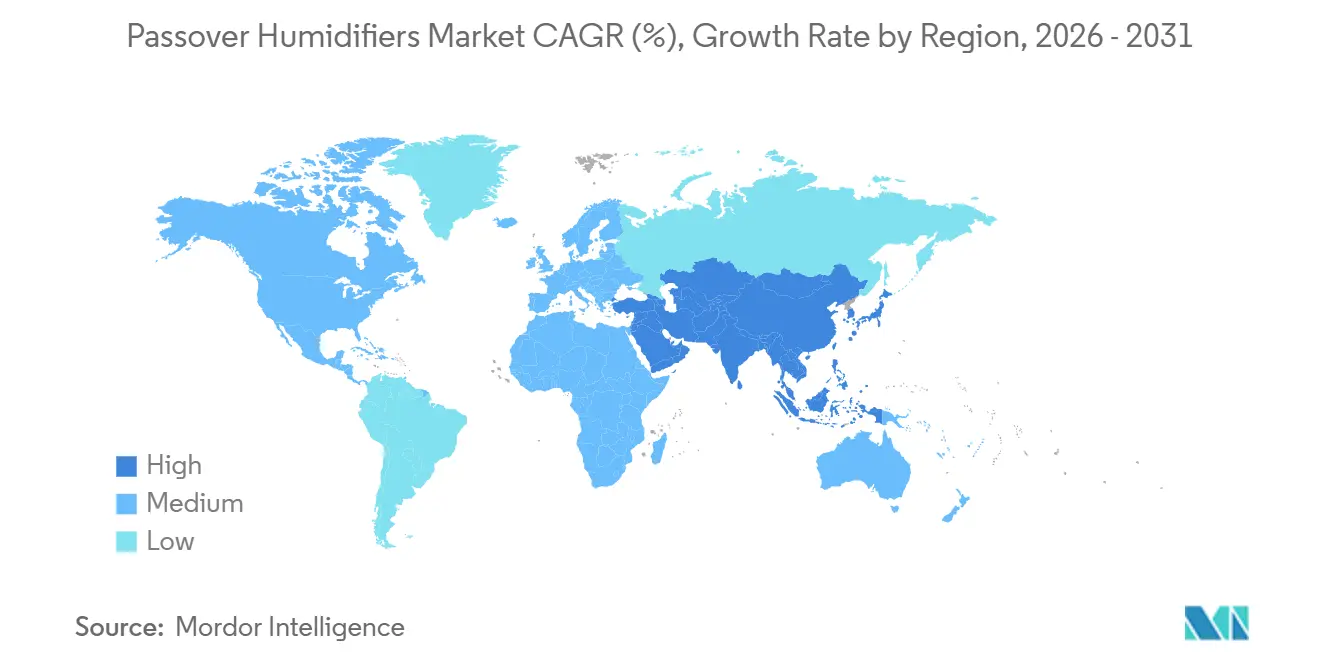

- By geography, North America retained 39.83% of global revenue in 2025. Asia-Pacific is the fastest-growing region at a 10.17% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Passover Humidifiers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of Sleep Apnea & CPAP Adoption | +1.8% | Global; high in North America & Western Europe | Medium term (2-4 years) |

| Growing Home Healthcare & Tele-Medicine Penetration | +1.5% | North America, Europe, Australia, Japan, South Korea | Short term (≤ 2 years) |

| Technological Advances in Disposable Water-Chamber Materials | +0.9% | Global; R&D nodes in China & Southeast Asia | Long term (≥ 4 years) |

| Aging Population with Higher Respiratory Comorbidities | +1.2% | Japan, Western Europe, North America, China, India | Long term (≥ 4 years) |

| Smart IoT-Enabled Passover Units Unlocking Value-Based Reimbursement | +0.7% | North America, Europe, pilot sites in Asia-Pacific | Medium term (2-4 years) |

| Tariff-Driven Reshoring of Humidifier Manufacturing | +0.5% | United States, Mexico, European Union | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Sleep Apnea & CPAP Adoption

Nearly 936 million adults worldwide live with obstructive sleep apnea, and U.S. diagnoses are forecast to reach 77 million by 2050, expanding the patient pool that relies on CPAP therapy and add-on humidifiers.[1]American Academy of Sleep Medicine, “AASM Analysis of the 2025 Medicare Physician Fee Schedule Final Rule,” aasm.org Adherence, however, falters when nasal dryness emerges; studies show 30-60% of patients quit within a year, but smart pass-through humidification raises five-year adherence to as high as 87%. CMS’s National Coverage Determination 240.4 enforces a 12-week trial with documented compliance, nudging suppliers toward disposable, pre-filled chambers that lower misuse risk. Sleep-test reimbursement is likewise shifting: CPT 95800 is under valuation scrutiny because disposable sensors are replacing reusable gear, which could further tilt procurement toward single-use consumables.

Growing Home Healthcare & Tele-Medicine Penetration

Home-health orders already account for 55% of durable respiratory equipment, and U.S. home-health aide employment is projected to grow 22% through 2034. New remote-patient-monitoring (RPM) codes 99XX4 and 99XX5 proposed for 2026 will reimburse device data capture and clinical interactions, complementing existing CPT 99453, 99454, and 99457.[2]Centers for Medicare & Medicaid Services, “CY 2025 Update: DMEPOS Fee Schedule,” cms.gov The MonitAir trial reported an 18-percentage-point reduction in CPAP discontinuation when real-time humidity alerts were deployed. Yet pandemic-era telehealth flexibilities may expire, restricting virtual care to rural zones and dampening RPM uptake in urban markets. Suppliers are therefore bundling humidifier analytics with adherence dashboards to safeguard reimbursement even if broader telehealth rules tighten.

Technological Advances in Disposable Water-Chamber Materials

Advanced polymers now match stainless-steel thermal efficiency while cutting chamber weight 40-50%, reducing freight cost and easing patient handling. Embedded heater plates and temperature sensors maintain the 44 mg/L humidity target for invasive ventilation without external controllers, streamlining setup for non-technical users.[3]Fisher & Paykel Healthcare, “F&P my820 Heated Humidifier Launch,” fphcare.com Fisher & Paykel’s F&P my820 uses adaptive algorithms that minimize tubing “rain-out,” raising comfort and adherence. Research into antimicrobial coatings could stretch disposable-chamber replacement from 6-12 to 18-24 months, lowering lifetime ownership cost and sharpening the competitiveness of higher-margin pre-filled designs.

Aging Population with Higher Respiratory Comorbidities

The WHO European Region reports 81.7 million people with chronic respiratory disease, and in Japan, 29% of residents are over 65—a demographic tilt that multiplies demand for humidified respiratory support beyond OSA. Medicare’s capped-rental structure refreshes humidifier accessories every 13 months, and the 2025 DMEPOS update raised the oxygen-equipment service fee to USD 87.82 per six-month interval, subtly boosting disposable-chamber economics. Post-acute settings prefer sealed, single-use chambers to curb cross-contamination, a habit ingrained during COVID-19 outbreaks. Manufacturers are answering with larger water-level indicators and simplified attachment clips that elderly caregivers can manage safely.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Device Approval & Post-Market Surveillance Requirements | -0.6% | United States, European Union, Japan | Medium term (2-4 years) |

| High Total Cost of Advanced CPAP Systems in Low-Income Regions | -0.8% | India, Philippines, Indonesia, Sub-Saharan Africa | Long term (≥ 4 years) |

| Infection Risk & Cleaning Non-Compliance | -0.5% | Global; heightened in North America & Europe | Short term (≤ 2 years) |

| Substitution Threat from Integrated Heated-Humidifier CPAPs | -0.7% | North America, Western Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Device Approval & Post-Market Surveillance Requirements

Passover humidifiers fall under FDA Class II (21 CFR 868.5450) and demand 510(k) clearance, ISO 13485 quality systems, IEC 60601 electrical safety, and a periodic safety report compliance package that can add USD 0.5-1 million and 12-18 months to launch timelines. CMS’s RAC Topic 0066 audits medical necessity for PAP devices, and an improper-payment rate of 12.5%—71.2% linked to documentation gaps—forces suppliers to invest in EHR integrations. Although February 2024 DME MAC guidance loosened wording on orders (“CPAP Mask” acceptable), the underlying evidence burden persists and deters smaller entrants.

High Total Cost of Advanced CPAP Systems in Low-Income Regions

A full CPAP kit in India can top INR 80,000 (USD 955), three to four months of median income in tier-2 cities, while the CGHS cap of INR 45,000 plus GST excludes humidifier consumables, forcing patients into high out-of-pocket spend. Disposable chambers cost INR 4,000-6,500 (USD 48-78); recurring fees spur abandonment and open doors to gray-market reuse. Trials in the Philippines show reprocessed bCPAP systems can match single-use safety, but the absence of regulatory clarity keeps circular-economy models niche. Manufacturers now market hybrid CPAP-oxygen concentrators drawing only 65-146 watts with >60-minute battery backup to accommodate unstable grids.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Pre-Filled Chambers Gain Ground Despite Dry Disposable Dominance

Dry disposable units held 43.81% of passover humidifiers market share in 2025, anchored in ICU and sleep-center protocols that demand daily water changes. The passover humidifiers market size for dry disposable products is forecast to grow at a steady clip, albeit slower than premium alternatives. Reusable designs continue to serve budget-sensitive home users, but infection alerts from FDA against ozone and UV cleaners have tempered enthusiasm.

Pre-filled disposable chambers, expanding at 9.09% CAGR, leverage sterile water fills to remove patient-side maintenance and slash Pseudomonas contamination risk documented in January 2025 case reports. Fisher & Paykel’s F&P my820 couples adaptive humidity with cloud titration, evidencing how IoT features accelerate uptake. As advanced polymers narrow cost gaps, pre-filled units are poised to contribute the majority of incremental passover humidifiers market revenue by 2031.

By Application: High-Flow Nasal Cannula Outpaces CPAP Therapy Growth

CPAP therapy retained 48.57% of the passover humidifiers market revenue in 2025, underwritten by Medicare’s structured pathway and an installed base of 30 million diagnosed U.S. OSA patients. Mechanical ventilation remains the second-largest slice, but demand has normalized post-COVID.

High-flow nasal cannula (HFNC) and oxygen therapy are projected to post an 11.78% CAGR through 2031, the highest within the passover humidifiers market, because HFNC can trim intubation rates 30-50% in acute respiratory failure. Hospitals eye USD 20,000-30,000 in ICU cost savings per avoided intubation, propelling dedicated passover humidifiers optimized for 30-60 L/min flow. Vyaire’s exit from ventilators and ZOLL’s October 2024 acquisition illustrate margin pressure that shifts R&D dollars toward non-invasive segments.

By End User: Sleep Centers Accelerate as Value-Based Care Rewards Adherence

Hospitals and clinics captured 37.12% share in 2025, reflecting their multirole use across CPAP titration, mechanical ventilation, and HFNC. Nevertheless, conversion-factor cuts of 2.83% in the 2025 fee schedule squeeze sleep-lab margins and encourage volume migration to lower-cost sites.

Sleep centers and specialty clinics, growing at 10.69% CAGR, harness new RPM codes and MIPS adherence metrics to monetize data streams from smart humidifiers. ResMed’s VirtuOx acquisition consolidates diagnostic and therapeutic workflows, underscoring the strategic edge of integrated virtual pathways. Home-care settings still benefit from 22% projected growth in aide employment, but telehealth rollbacks could cap near-term smart-humidifier penetration in dense metros.

Geography Analysis

North America preserved 39.83% of passover humidifiers market revenue in 2025, buoyed by Medicare’s 13-month capped rental model and a documented OSA population expected to more than double by 2050. The region faces a 12.5% improper-payment rate for CPAP claims, which cost USD 146.1 million in 2024 and spurred investments in automated compliance tracking. Tariff-induced reshoring is increasing lead times for subcomponents, yet USMCA incentives are attracting final assembly to Mexico, sidestepping a universal 10% tariff on non-US goods.

Asia-Pacific is the fastest-growing arena at 10.17% CAGR. In India, a basic CPAP retails for INR 18,000-22,000 (USD 215-263), whereas the CGHS cap leaves a yawning reimbursement gap, steering consumers toward low-cost dry disposable chambers. Japan’s super-aged society and South Korea’s digital-health policies are catalyzing early adoption of IoT-enabled humidifiers. The Philippines trial validating reprocessed bCPAP safety may inspire circular-economy supply chains if regulators set clear reuse standards.

Europe ranks second in global share, anchored by NHS reimbursement, German DRGs, and France’s Sécurité Sociale. EU MDR tightens post-market surveillance, inflating compliance overheads that favor established players. Fisher & Paykel’s pan-European launch of the F&P my820 in August 2024 showcases the region’s appetite for premium, connected humidifiers. The Middle East & Africa and South America remain nascent, yet affluent urban pockets in the GCC and Brazil are showing uptake for high-end pre-filled designs.

Competitive Landscape

The passover humidifiers market is moderately consolidated. ResMed, Fisher & Paykel Healthcare, and Philips Respironics dominate through proprietary algorithms and global distribution. Fisher & Paykel logged USD 951.2 million in first-half FY 2025 revenue, an 18% uplift, concurrent with the F&P my820 launch. ResMed’s Smart Comfort AI humidifier, FDA-cleared in December 2025, leverages machine learning to tailor humidity and is rolling out commercially in 2026.

Medtronic and GE Healthcare deepened their alliance in March 2026, integrating oximetry and capnography into CARESCAPE Canvas monitors, positioning bundled monitoring-humidification suites that could cannibalize standalone accessories. Material innovation is a competitive flashpoint: antimicrobial coatings promise 18-24-month replacement cycles, while lighter polymer shells cut freight costs. Emerging players pursue low-power CPAP-oxygen hybrids aimed at grids with rolling blackouts. Vyaire’s Chapter 11 and ZOLL’s 2024 purchase of its ventilator line highlight profit erosion in commoditized ICU gear.

Passover Humidifiers Industry Leaders

GE Healthcare

Hamilton Medical

ICU Medical (Smiths Medical)

Medtronic

Terumo Medical Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Medtronic and GE Healthcare expanded their multiyear global strategic alliance, integrating Medtronic's Nellcor pulse oximetry, Microstream capnography, INVOS regional oximetry, and BIS brain monitoring into GE HealthCare's FlexAcuity, CARESCAPE Canvas, and Carevance monitors, targeting bedside monitoring, telemetry, ambulatory monitoring, maternal-infant care, and advanced perioperative monitoring, with joint R&D to expedite next-generation wireless wearable technologies and anesthesia airway visualization.

- December 2025: ResMed secured FDA clearance for its Smart Comfort AI-enabled humidifier, incorporating machine-learning algorithms trained on millions of patient-nights to adjust humidity setpoints dynamically, with commercial rollout beginning in early 2026 and integration into ResMed's cloud platform for remote titration by clinicians.

- May 2025: ResMed acquired VirtuOx, a provider of virtual at-home sleep testing services, to integrate diagnostic and therapeutic workflows and enable sleep centers to offer end-to-end remote care pathways, reducing patient travel and improving engagement.

Global Passover Humidifiers Market Report Scope

The passover humidifiers work by directing (or "passing over") a stream of air across the surface of a reservoir of room-temperature water. As the air flows over the water, it picks up moisture through evaporation, delivering cooler, humidified air to the patient. Unlike heated humidifiers, it does not use electricity, a heater plate, or active warming, making it unpowered and relying solely on natural evaporation.

The passover humidifiers market report is segmented by product type, application, end-user, and geography. By product, the market is segmented into dry disposable, pre-filled disposable, and reusable. By application, the market is segmented into CPAP therapy, mechanical ventilation, high-flow nasal cannula & oxygen therapy. By end-user, the market is segmented into hospitals & clinics, homecare settings, sleep centers & others. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East & Africa, South America. The market forecasts are provided in terms of value (USD).

| Dry Disposable Passover Humidifiers |

| Pre-filled Disposable Passover Humidifiers |

| Reusable Passover Humidifiers |

| CPAP Therapy |

| Mechanical Ventilation (ICU & Critical Care) |

| High-Flow Nasal Cannula & Oxygen Therapy |

| Hospitals & Clinics |

| Homecare Settings |

| Sleep Centres & Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Dry Disposable Passover Humidifiers | |

| Pre-filled Disposable Passover Humidifiers | ||

| Reusable Passover Humidifiers | ||

| By Application | CPAP Therapy | |

| Mechanical Ventilation (ICU & Critical Care) | ||

| High-Flow Nasal Cannula & Oxygen Therapy | ||

| By End-User | Hospitals & Clinics | |

| Homecare Settings | ||

| Sleep Centres & Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large will the passover humidifiers market be by 2031?

It is forecast to reach USD 2.91 billion, reflecting a 7.08% CAGR from 2026.

Which product type is expanding fastest?

Pre-filled disposable chambers are advancing at 9.09% CAGR on the back of tighter infection-control protocols and payer support.

Why is high-flow nasal cannula therapy important for humidifier demand?

HFNC lowers intubation rates up to 50%, driving an 11.78% CAGR for humidifier systems tuned to 30-60 L/min flows.

What hinders adoption in emerging economies?

High up-front CPAP costs and lack of reimbursement for consumables create affordability barriers, especially in India and Southeast Asia.

How are regulations shaping product design?

FDA Class II requirements, ISO 13485 quality systems, and CMS adherence metrics push manufacturers toward connected, single-use humidifiers that automate compliance documentation.

Page last updated on: