Passive Temperature Controlled Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

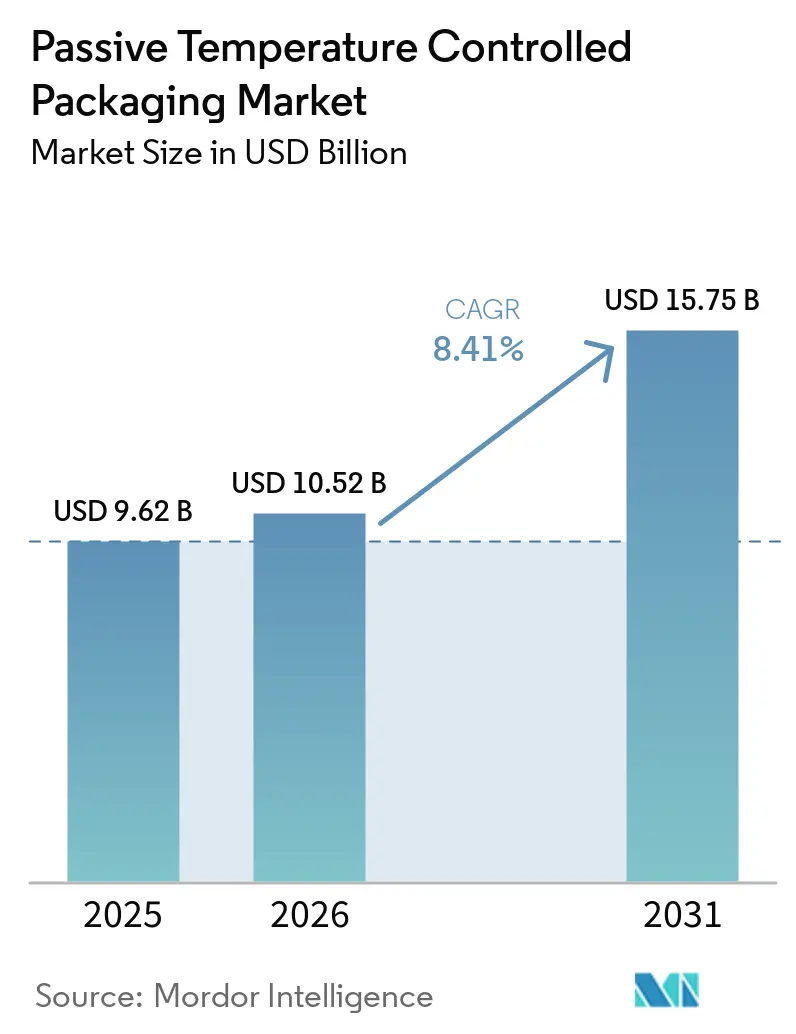

| Market Size (2026) | USD 10.52 Billion |

| Market Size (2031) | USD 15.75 Billion |

| Growth Rate (2026 - 2031) | 8.41% CAGR |

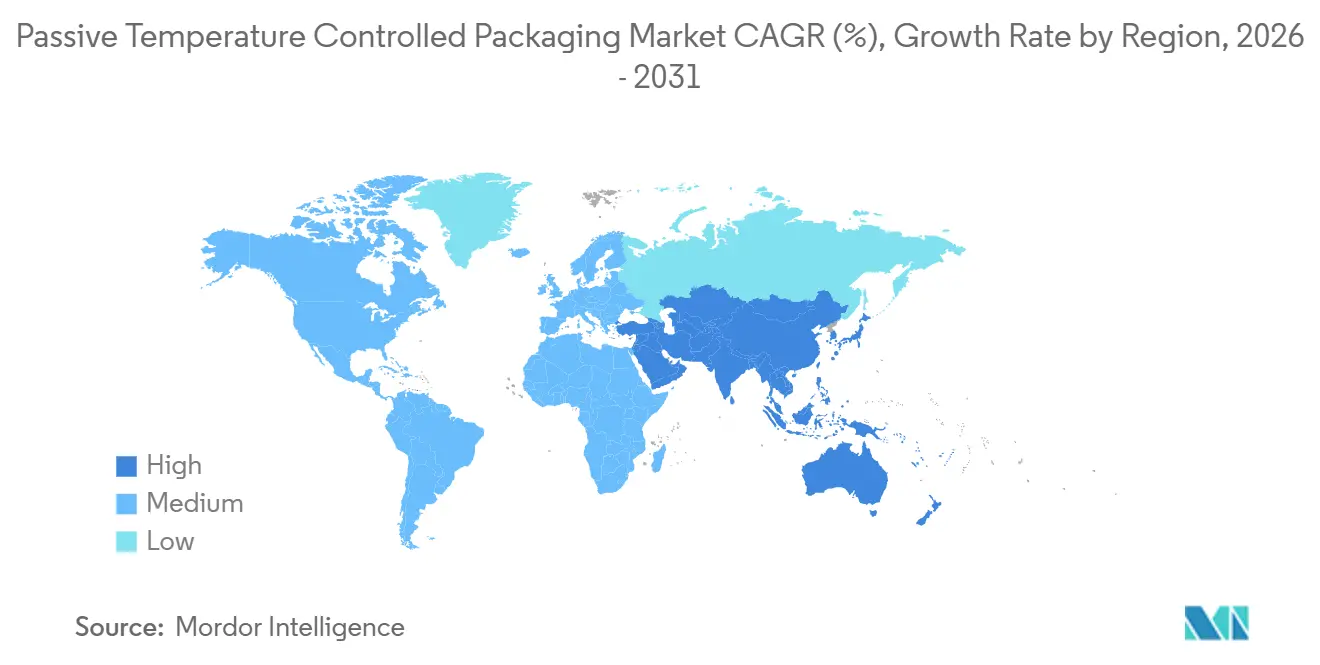

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Passive Temperature Controlled Packaging Market Analysis by Mordor Intelligence

The passive temperature controlled packaging market size is projected to expand from USD 9.62 billion in 2025 and USD 10.52 billion in 2026 to USD 15.75 billion by 2031, registering a CAGR of 8.41% between 2026 and 2031. The passive temperature controlled packaging market is expanding into a broader set of cold chain use cases as drug makers, food retailers, and logistics providers seek formats that do not rely on external power during transit. Demand is being reinforced by the growing mix of temperature-sensitive biologics, rising direct-to-patient pharmaceutical shipping, and a broader shift toward parcel-based cold chain fulfillment in food delivery. Procurement criteria are also changing, with buyers placing greater weight on validated performance, route-specific pack-outs, and documentation that supports pharmaceutical and food compliance requirements. Sustainability requirements are reshaping material choices and format design, pushing suppliers toward reusable assets, recyclable components, and bio-based insulation that maintain thermal performance. Competition is therefore moving beyond insulation quality alone, with suppliers trying to combine temperature reliability, service support, and easier qualification across more shipment lanes.

Key Report Takeaways

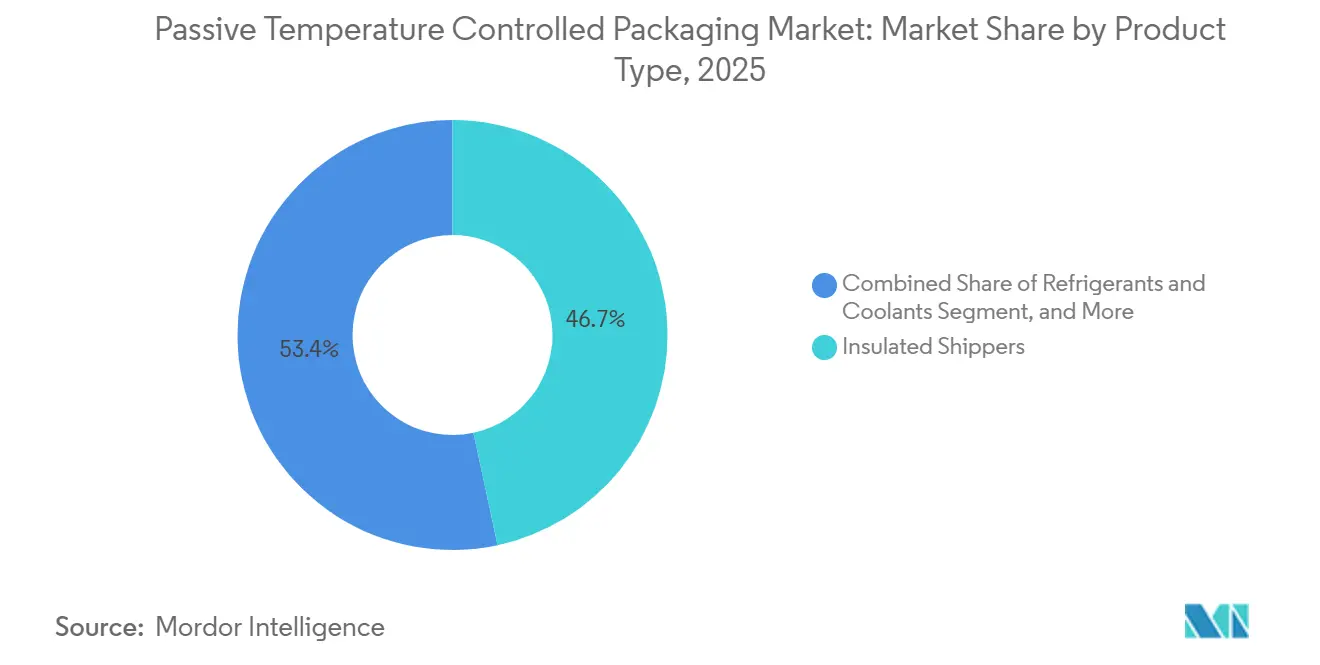

- By product type, insulated shippers held 46.65% of the passive temperature controlled packaging market share in 2025.

- By material type, the passive temperature controlled packaging market for bio-based insulation materials is projected to grow at a 9.18% CAGR over 2026-2031.

- By usability, single-use formats led with a 68.93% of the passive temperature controlled packaging market share in 2025.

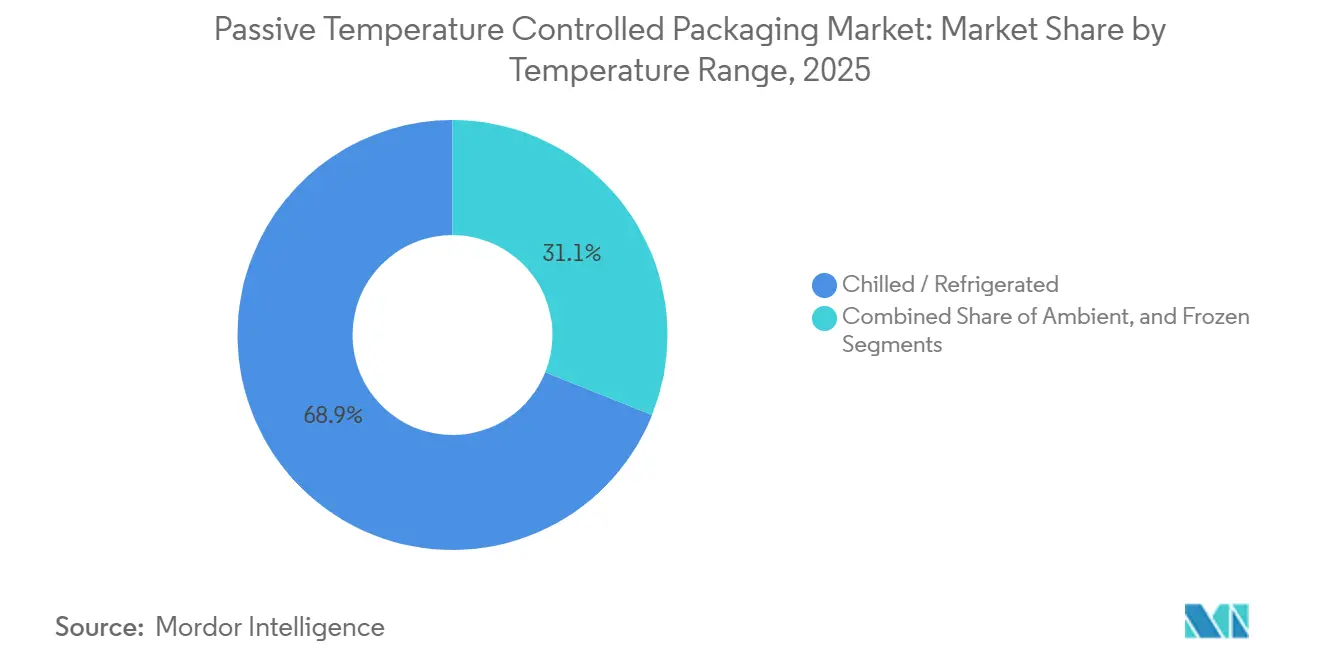

- By temperature range, the passive temperature controlled packaging market for frozen segment is projected to advance at an 8.84% CAGR over 2026-2031.

- By end-user industry, food and beverages held 49.67% of the passive temperature controlled packaging market share in 2025.

- By geography, the passive temperature controlled packaging market for Asia-Pacific is projected to grow at a 9.25% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Passive Temperature Controlled Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Biologics and Specialty Pharma Shipments | +2.8% | Global, concentrated in North America, Europe, and the Asia-Pacific | Medium term (2-4 years) |

| Growth in GLP-1 And Direct-To-Patient Refrigerated Parcel Flows | +1.9% | North America is dominant, with spill-over to Europe and Australia | Short term (≤ 2 years) |

| Expansion of Food E-Commerce and Meal-Kit Cold Chains | +1.5% | North America, Europe, Asia-Pacific core | Short term (≤ 2 years) |

| Tightening GDP, USP, And Food-Safety Compliance Standards | +1.2% | Global, early compliance gains in the EU, the US, and China | Medium term (2-4 years) |

| Shift Toward Reusable and Recyclable Passive Solutions | +0.8% | EU and North America early adopters, spill over to the Middle East and Africa | Long term (≥ 4 years) |

| Adoption of Lane-Specific Pack-Out Optimization and Connected Passive Packaging | +0.6% | North America and the EU, expanding into the Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Biologics and Specialty Pharma Shipments

Rising biologics volumes are changing the shipment mix that supports the passive temperature controlled packaging market. Many newer therapies are sensitive to both heat exposure and unintended freezing, which keeps the 2°C to 8°C range central to packaging design and lane qualification. The same trend is increasing the value of route-specific validation, as biologics require tighter control than traditional small-molecule drugs during transit. Cencora stated in November 2025 that nearly 50% of drugs expected to launch globally through 2027 would require cold chain storage, up from 37% a decade earlier, which shows how quickly cold chain dependence is widening across drug pipelines. As more of these products move through specialty distribution and direct dispensing channels, the passive temperature controlled packaging market benefits from larger recurring shipment volumes and more repeatable pack-out requirements. This favors suppliers that can offer validated payload protection, multiple duration options, and documentation that supports qualification across changing seasonal conditions.

Growth In GLP-1 and Direct-To-Patient Refrigerated Parcel Flows

GLP-1 therapies are creating a large parcel-based demand stream for the passive temperature controlled packaging market. These products fit a delivery model that relies on specialty pharmacies, telehealth channels, and home delivery, underscoring the need for compact, insulated formats rather than pallet systems. Nordic Cold Chain Solutions launched a GLP-1 and small-format packaging innovation lab in March 2026, indicating that suppliers now see this as a distinct packaging problem that requires its own validated configurations. TemperPack reported in 2025 that 12 EPS foam coolers used for GLP-1 shipments were being discarded in US landfills every minute, underscoring why this therapy category is also drawing sustainability concerns into the last-mile cold chain discussion.[1]“TemperPack Launches Qualified Shipper Program to Help Life Science Companies Replace EPS,” Business Wire, businesswire.com That combination of high shipment frequency and rising waste visibility is prompting buyers to review both pack size and insulation choice simultaneously. It also makes the passive temperature controlled packaging market more dependent on standardized, easy-to-pack shipper formats that can scale with prescription volume growth.

Expansion of Food E-Commerce and Meal-Kit Cold Chains

Food e-commerce continues to widen the customer base for the passive temperature controlled packaging market. Unlike pharmaceutical shipping, food fulfillment often requires lower-cost insulated mailers, liners, and refrigerants to protect the product during short delivery windows at a reasonable unit cost. This results in a high shipment frequency even when the thermal requirement is less demanding than that of a validated pharmaceutical lane. TemperPack expanded manufacturing in Michigan in December 2025 and said the added capacity was aimed at food and life sciences direct-to-consumer demand, which reflects how food e-commerce is now important enough to shape production decisions. The food channel also supports year-round ordering patterns because meal kits, fresh proteins, dairy, and frozen prepared meals move through regular household replenishment cycles rather than occasional bulk purchases. That steady order cadence gives the passive temperature controlled packaging market a broader demand base beyond healthcare and reduces overreliance on a single end-user group.

Tightening GDP, USP, and Food-Safety Compliance Standards

Compliance standards are raising the threshold for participation in the passive temperature controlled packaging market. Pharmaceutical buyers now expect more documentation on route mapping, qualification, and pack-out repeatability, which changes passive packaging from a simple supply item into a controlled logistics component. The European GDP Association noted in its transportation guidance that GDP implementation requires structured qualification and documented transport controls, reinforcing the importance of validated packaging in regulated shipment flows. This is making pre-qualified portfolios more valuable because suppliers that already hold seasonal or route-based validation can shorten adoption timelines for pharmaceutical shippers. It also gives vendors that combine hardware with guidance on conditioning, handling, and documentation an advantage. As these requirements become more common across the pharmaceutical and food supply chains, the passive temperature controlled packaging market should continue to shift toward established providers that can meet both performance and audit expectations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Hold Time Versus Active Systems on Long and Variable Lanes | -1.8% | Global, most acute on intercontinental pharma and frozen food lanes | Medium term (2-4 years) |

| High Cost of VIP and Advanced PCM Configurations | -1.4% | Emerging markets in Africa and South and Southeast Asia, SME shippers globally | Long term (≥ 4 years) |

| Reverse-Logistics Gaps Reducing Reuse Economics Outside Core Pharma Corridors | -0.9% | Africa, South America, and Southeast Asia | Long term (≥ 4 years) |

| Supply Risk in Qualified VIP, PCM, and Fiber-Based Input Chains | -0.7% | Global, concentration risk in East Asia manufacturing clusters | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited Hold Time Versus Active Systems on Long and Variable Lanes

Hold-time limits remain a practical constraint on the passive temperature controlled packaging market. Passive formats work well on many regional and single-leg international lanes, but they become harder to rely on when a shipment faces customs delays, missed connections, or long dwell time at transfer points. Peli BioThermal stated in 2025 that high-performance passive configurations can provide 96 to 168 hours of protection, which is strong for many use cases but still finite compared with active-powered systems. The constraint becomes sharper when the route spans different climates, as the same payload may require separate validation for hot and cold seasonal profiles. This reduces flexibility for shippers that operate across global multi-stop networks and lack reliable reconditioning points along the route. As a result, the passive temperature controlled packaging market is likely to remain strongest in short-to-medium-haul lanes, while the hardest intercontinental movements continue to play a larger role for active or hybrid approaches.

High Cost of VIP and Advanced PCM Configurations

The cost of advanced thermal configurations continues to slow part of the passive temperature controlled packaging market. Vacuum-insulated panels and specialized PCM sets can deliver tighter control, but they also raise the purchase cost, conditioning burden, and qualification effort for each design. Reusable high-performance systems become more attractive only when the shipper can recover units consistently and keep them circulating through a closed or semi-closed loop. Even so, that value case is harder to prove in emerging markets and smaller export lanes where return logistics and refurbishment infrastructure are less mature. This leaves the passive temperature controlled packaging market with a split structure, where premium, validated formats grow in regulated healthcare lanes, while many shippers still favor simpler, less costly alternatives for broader distribution needs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Insulated Shippers Anchor Volume in Pharma Direct-To-Patient Flows

Insulated shippers held 46.65% share in 2025, making them the largest product category in the passive temperature controlled packaging market. Their lead position comes from a strong fit with parcel-sized healthcare shipments and food e-commerce orders, where ease of packing and broad temperature coverage matter more than very large payload capacity. The product is especially well aligned with direct-to-patient programs because it supports small payloads, standardized pack-outs, and fast handling at distribution sites. Cencora announced a USD 1 billion investment through 2030 to expand and modernize its US distribution network, including major refrigerated and frozen storage additions at its Alabama specialty facility, which supports the underlying logistics infrastructure that keeps parcel and specialty cold chain traffic growing.[2]Cencora, “Cencora Announces USD 1 Billion Investment to Strengthen Its U.S. Distribution Network,” BioSpace, biospace.com As distribution networks add more cold storage and specialized handling capacity, insulated shippers remain the practical choice for many repeat-shipment programs because they are easy to scale across large delivery volumes.

Insulated containers remain important for bulk pharmaceutical flows and larger cold chain moves, especially where shipment value justifies a stronger packaging system and a more controlled reuse cycle. Thermal liners and covers still represent the smallest product slice, but the passive temperature controlled packaging industry is treating them less as low-value accessories and more as managed assets that can add lane flexibility. CSafe launched Silverskin RE in October 2025 as a reusable thermal pallet cover with lifecycle management, integrated tracking, and support for 2°C to 8°C and 15°C to 25°C ranges, which shows how this sub-segment is becoming more service oriented. Refrigerants and coolants are projected to grow at 9.26% CAGR through 2031, and that pace reflects the wider shift from basic gel packs toward PCM formats that offer better thermal stability and more repeatable documentation for regulated shipment lanes. The passive temperature controlled packaging market share tied to refrigerants also benefits from higher bill-of-materials content per shipment because more complex biologic and GLP-1 pack-outs often require carefully matched coolant configurations rather than a generic cold source.

By Material Type: Bio-Based Insulation Displaces EPS At The Performance Tier

Plastic accounted for 41.58% of the passive temperature controlled packaging market in 2025, reflecting the long-established use of EPS and polyurethane across pharmaceutical and food shipment formats. These materials have kept their position because they are familiar to packers, widely available, and already embedded in many validated pack-outs. EPS has remained common in parcel shipping because it balances thermal performance and cost in a way that still works for many standard cold lanes. Polyurethane also plays a role in higher-specification systems where structure and insulation value need to support more demanding transport conditions. This leaves plastic-based materials with a large installed base even as customer preferences begin to shift.

Bio-based insulation materials are projected to expand at a 9.18% CAGR through 2031, driven by a mix of sustainability pressures and improving proof of performance. TemperPack said its GreenCell Foam platform supports more than 60 pre-qualified shippers across 2°C to 8°C, 15°C to 25°C, and -20°C temperature profiles, indicating that buyers no longer see compostable insulation as a niche option only for light-duty applications. Landpack also promotes pre-qualified life science cooling solutions based on natural fiber materials, indicating that bio-based alternatives are moving into regulated use cases in Europe rather than remaining limited to food delivery. The passive temperature controlled packaging market is therefore seeing a gradual replacement path at the low-to-mid performance tier, where buyers want to reduce reliance on EPS without losing qualification confidence. This transition remains selective because the material must meet the same transit expectations as incumbent insulation before the buyer will approve a switch.

By Usability: Reusable Growth Reshapes Total Cost Of Ownership

Single-use formats held a 68.93% share in 2025, keeping them well ahead in the passive temperature controlled packaging market. Their scale reflects the fact that many residential, food-delivery, and direct-to-patient healthcare routes do not support reliable returns. Single-use systems are also operationally simple because they avoid retrieval, cleaning, refurbishment, and coordination with reverse logistics. That simplicity matters in GLP-1 and e-commerce channels where shipment volume is high, and the delivery destination is often a residence rather than a controlled business site. As long as the parcel cold chain continues to expand, single-use packaging should continue to play a strong role because it aligns with the logistics realities of those channels.

Reusable systems are projected to grow at a 9.69% CAGR through 2031, making them the fastest-growing segment of the passive temperature controlled packaging market. Growth is strongest in business-to-business pharmaceutical lanes, where return cycles are easier to manage, and users can track cost per trip across a defined network. va-Q-tec also reported in September 2025 that its reusable ThermoCare boxes supported 1 million pharmaceutical home deliveries with Swiss Post, showing that reuse can work at scale when the operating model is designed around controlled circulation. The passive temperature controlled packaging industry is therefore moving toward a dual model, with single-use formats serving dispersed last-mile networks and reusable systems gaining ground in structured pharmaceutical corridors where return efficiency is high.

By Temperature Range: Frozen Demand Broadens Beyond Traditional Lanes

The chilled and refrigerated range held a 47.56% share in 2025, making it the largest temperature band in the passive temperature controlled packaging market. This range remains central because it covers the majority of approved biologics, GLP-1 injectables, vaccines, and many chilled food items sold through e-commerce channels. The segment benefits from a wide overlap between healthcare and food use cases, providing suppliers with volume diversity across end-user groups. It also fits many common transit durations that passive solutions can handle reliably when the pack-out is properly qualified. For that reason, chilled and refrigerated formats remain the volume anchor even as more demanding shipment profiles attract attention.

The frozen segment is projected to grow at an 8.84% CAGR through 2031, reflecting the expanding need in both food delivery and advanced-therapy logistics. Peli BioThermal introduced the Crēdo Vault bulk shipper and Vēro One dry-ice shipper in April 2026, directly targeting higher-demand cryogenic and dry-ice use cases linked to cell and gene therapy and other specialized applications. The company also used the same launch to highlight stronger support for critical CGT movements, demonstrating how suppliers are expanding beyond standard chilled programs into deeper low-temperature coverage. In food logistics, frozen delivery windows are becoming more relevant as same-day and next-day services broaden consumer acceptance of home-delivered frozen products. The passive temperature controlled packaging market is therefore adding more specialized frozen capability, even though chilled formats still account for the largest base of recurring shipments.

By End-User Industry: Pharma Accelerates While Food and Beverages Keeps Scale

Food and beverages accounted for 49.67% in 2025, giving this group the largest end-user share in the passive temperature-controlled packaging market. The category benefits from sheer shipment volume because it includes chilled meal kits, dairy, proteins, fresh produce, and frozen prepared foods across both retail and direct-to-consumer channels. Many of these shipments use simpler passive systems, but the order frequency is high, and the volume base is broad. This gives food and beverages a scale advantage even when the average packaging value per shipment is below pharmaceutical levels. The segment also creates a steady baseline demand, as household replenishment patterns sustain recurring order cycles throughout the year.

Pharmaceuticals and biotechnology are projected to grow at a 9.41% CAGR through 2031, making them the fastest-growing end-user segment in the passive temperature-controlled packaging market. Peli BioThermal and OnAsset Intelligence announced in March 2026 that custom tracking had been integrated into the SmartCap of the evo DV10 shipper, showing how passive solutions for high-value therapies are becoming more data-rich and more closely monitored during transit. DGP Intelsius launched NUVEX in March 2026 for UN2915 Type A-compliant radiopharmaceutical transport, demonstrating how specialized pharmaceutical shipment needs are expanding beyond standard biologics into highly specific clinical and nuclear medicine applications. Central Pharma also partnered with Intelsius in October 2025 to expand cell and gene therapy support in the UK and Europe, reinforcing the broader shift toward specialized cold chain service models in healthcare. The passive temperature controlled packaging market is therefore seeing a clear divide in end-user economics, where food keeps shipment scale while pharmaceuticals bring stronger demand for validated performance, monitoring, and premium pricing.

Geography Analysis

North America held a 41.38% share in 2025, making it the leading region in the passive temperature controlled packaging market. The United States drives most of that scale by combining a dense pharmaceutical distribution system with strong direct-to-patient shipments and a large cold-chain e-commerce base. Cencora’s November 2025 plan to invest USD 1 billion through 2030 in its US distribution network, including major refrigerated and frozen expansion in Alabama, points to continued infrastructure build-out behind pharmaceutical cold chain flows. That investment supports the practical conditions that help passive solutions scale, including access to cold storage, handling capacity, and standardized specialty distribution lanes. The region also benefits from strong adoption of parcel-format healthcare shipping, which keeps demand high for insulated shippers, qualified refrigerants, and small-format solutions.

Asia-Pacific is projected to grow at a 9.25% CAGR through 2031, making it the fastest-growing regional segment in the passive temperature controlled packaging market. The region’s growth is tied to expanding pharmaceutical manufacturing, improving cold chain logistics, and stronger food e-commerce penetration across several large consumer markets. Australia and New Zealand are important early adopters in parcel cold chain formats, while China and India support the broad manufacturing and export base that is raising regional packaging needs. Nordic Cold Chain Solutions’ focus on GLP-1 and small-format innovation also has relevance beyond North America because the same parcel-based therapy model is spreading into other developed healthcare systems. This leaves Asia-Pacific with both healthcare and food demand drivers, which gives the regional growth story more balance than a single-sector expansion cycle.

Europe remained a major revenue base for the passive temperature controlled packaging market in 2025, supported by pharmaceutical manufacturing density and regulated logistics standards across Germany, the United Kingdom, France, Italy, and Spain. Landpack’s pre-qualified life science solutions and the broader move toward natural fiber insulation in Europe show how sustainability rules are starting to affect commercial packaging choice in addition to temperature performance.[3]Landpack GmbH, “Vorqualifizierte Kühlverpackungen für Life Science,” Landpack, landpack.de South America is still developing, but Peli BioThermal’s March 2026 distribution partnership with Polar Group in Brazil indicates growing supplier commitment to pharmaceutical cold chain expansion in the region. The Middle East and Africa remains earlier stage, with Gulf transit hubs, Turkey, South Africa, and Nigeria forming the main points of adoption as healthcare logistics networks become more structured and more compliance driven.

Competitive Landscape

The passive temperature controlled packaging market remains moderately fragmented, with specialist providers competing on validated performance, product breadth, and service support rather than a single dominant global position. Peli BioThermal, Cold Chain Technologies, Sofrigam, DGP Intelsius, and CSafe Global all hold visible positions in high-specification pharmaceutical packaging, but the available evidence still points to a market where leadership is distributed across multiple niches. That structure keeps competition active across parcel shippers, bulk systems, reusable formats, refrigerants, and specialized low-temperature solutions. It also means suppliers often build advantage through qualification data, reverse logistics capability, and customer support rather than raw manufacturing scale alone. The passive temperature controlled packaging market, therefore, rewards providers that can demonstrate reliability across specific lanes and shipment profiles.

Ownership changes and portfolio moves are reshaping the field. Sealed Air announced in November 2025 that it had agreed to be acquired by CD&R for an enterprise value of USD 10.3 billion, which shows that temperature-sensitive and protective packaging assets remain strategically important inside the broader packaging sector. Sonoco reported in February 2026 that it had completed the sale of its ThermoSafe business to Arsenal Capital Partners, further separating specialized temperature-assured packaging operations from broader paper and industrial packaging priorities. Peli BioThermal’s April 2026 launches of Crēdo Vault and Vēro One show a parallel product strategy, with one move aimed at bulk CGT needs and the other aimed at more sustainable single-use dry-ice shipping.[4]Ben, “OnAsset Intelligence and Peli BioThermal Unveil Next-Gen Smart Shipper Integration at LogiPharma 2026,” OnAsset Intelligence, onasset.com These actions suggest that suppliers are widening their addressable range instead of relying on a narrow core category.

Digital integration is becoming another clear line of competition in the passive temperature controlled packaging market. Intelsius outlined a “Green and Connected” strategy in May 2025 that combined recyclable insulation, cloud tracking, and rental models, which reflects the move toward managed packaging services rather than simple product sales. OnAsset’s SmartCap work with Peli BioThermal points in the same direction, with passive hardware increasingly paired with live data on payload condition and shipment handling. The most attractive openings now appear in GLP-1 parcel formats, radiopharmaceutical transport, and lower-impact insulation that can meet stricter performance thresholds without losing disposal or reuse advantages. Suppliers that can combine validated thermal control, data visibility, and operational support should be better positioned as pharmaceutical and food customers make procurement more selective.

Passive Temperature Controlled Packaging Industry Leaders

Cold Chain Technologies, LLC

Pelican BioThermal LLC

CSafe Global Coöperatief U.A.

Softbox Systems Limited

va-Q-tec Thermal Solutions GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Cold Chain Technologies opened a 100,000-square-foot facility in Bethlehem, Pennsylvania, consolidating refurbishment, conditioning for reusable containers, and kitting of single-use sustainable products.

- April 2026: Peli BioThermal launched the Crēdo Vault bulk shipper and Vēro One curbside-recyclable dry-ice shipper at LogiPharma Europe 2026 in Vienna, expanding its portfolio for cell and gene therapy and sustainable single-use applications.

- March 2026: OnAsset Intelligence and Peli BioThermal announced an integration of OnAsset's custom tracking solution into the SmartCap of the evo DV10 shipper, creating a real-time dewar "fuel gauge" that combines payload, ambient, and handling data to generate predictive temperature hold profiles for cell and gene therapy shipments.

- March 2026: Peli BioThermal entered a strategic partnership with Polar Group in Brazil to distribute reusable and single-use cold chain packaging solutions to pharmaceutical, biotechnology, and healthcare organizations, strengthening cold chain infrastructure access in a fast-growing healthcare market.

Global Passive Temperature Controlled Packaging Market Report Scope

The scope of the report covers the analysis of the Passive Temperature Controlled Packaging Market, including packaging solutions designed to maintain a consistent temperature for sensitive products without active cooling systems. These solutions are widely used in industries such as pharmaceuticals, food and beverages, and chemicals, where temperature stability is critical during storage and transportation. The study examines market trends, growth drivers, challenges, and opportunities, providing insights into the forecast period and the competitive landscape.

The Passive Temperature Controlled Packaging Market Report is Segmented by Product Type (Insulated Shippers, Insulated Containers, Refrigerants and Coolants, and Thermal Liners and Covers), Material Type{Plastic (Polystyrene, Polyurethane, and Polypropylene), Paper and Paperboard, and Bio-Based Insulation Materials}, Usability (Single-Use, and Reusable), Temperature Range (Ambient, Chilled/Refrigerated, and Frozen), End-User Industry (Pharmaceuticals and Biotechnology, Food and Beverage, Chemical, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Insulated Shippers |

| Insulated Containers |

| Refrigerants and Coolants |

| Thermal Liners and Covers |

| Plastic | Polystyrene |

| Polyurethane | |

| Polypropylene | |

| Paper and Paperboard | |

| Bio-Based Insulation Materials |

| Single-Use |

| Reusable |

| Ambient |

| Chilled/Refrigerated |

| Frozen |

| Pharmaceuticals and Biotechnology |

| Food and Beverage |

| Chemical |

| Other End-Use Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Product Type | Insulated Shippers | ||

| Insulated Containers | |||

| Refrigerants and Coolants | |||

| Thermal Liners and Covers | |||

| By Material Type | Plastic | Polystyrene | |

| Polyurethane | |||

| Polypropylene | |||

| Paper and Paperboard | |||

| Bio-Based Insulation Materials | |||

| By Usability | Single-Use | ||

| Reusable | |||

| By Temperature Range | Ambient | ||

| Chilled/Refrigerated | |||

| Frozen | |||

| By End-User Industry | Pharmaceuticals and Biotechnology | ||

| Food and Beverage | |||

| Chemical | |||

| Other End-Use Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current and forecast size of the passive temperature controlled packaging market?

The passive temperature controlled packaging market was valued at USD 9.62 billion in 2025, stands at USD 10.52 billion in 2026, and is projected to reach USD 15.75 billion by 2031 at an 8.41% CAGR.

Which product category leads demand in passive temperature controlled packaging?

Insulated shippers led product demand with a 46.65% share in 2025 because they are widely used in direct-to-patient pharmaceutical delivery and parcel-based cold chain fulfillment.

Which material trend is changing packaging selection the most?

Bio-based insulation is the fastest-growing material segment at a 9.18% CAGR through 2031, as buyers look for alternatives to EPS that can still meet thermal and qualification requirements.

Why is pharmaceutical demand rising faster than other end-user groups?

Pharmaceuticals and biotechnology are projected to grow at a 9.41% CAGR through 2031, supported by biologics, GLP-1 therapies, radiopharmaceutical transport, and tighter compliance requirements.

Which region offers the strongest growth opportunity through 2031?

Asia-Pacific is projected to expand at a 9.25% CAGR, helped by pharmaceutical manufacturing growth, improving cold chain infrastructure, and wider food e-commerce penetration.

What is the main challenge for wider adoption of passive cold chain solutions?

The biggest constraint is the limit on hold time and the higher cost of premium VIP and PCM systems, especially on long international lanes and in markets where reuse networks are still weak.

Page last updated on: