Parametric Insurance Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

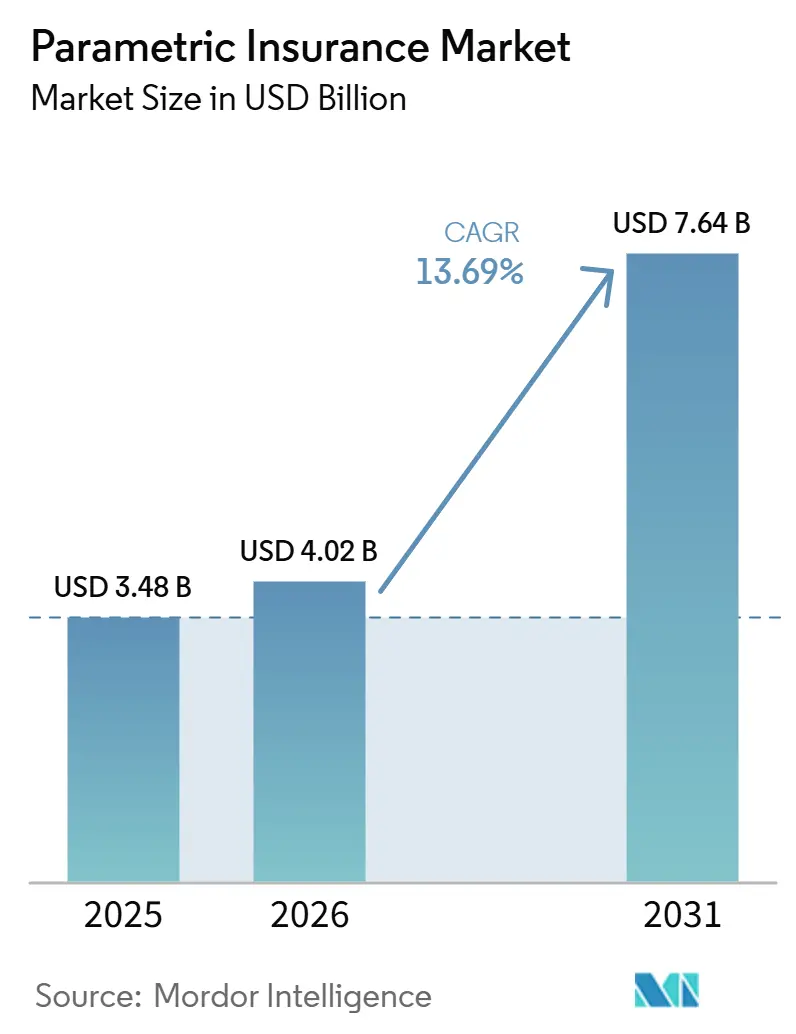

| Market Size (2026) | USD 4.02 Billion |

| Market Size (2031) | USD 7.64 Billion |

| Growth Rate (2026 - 2031) | 13.69% CAGR |

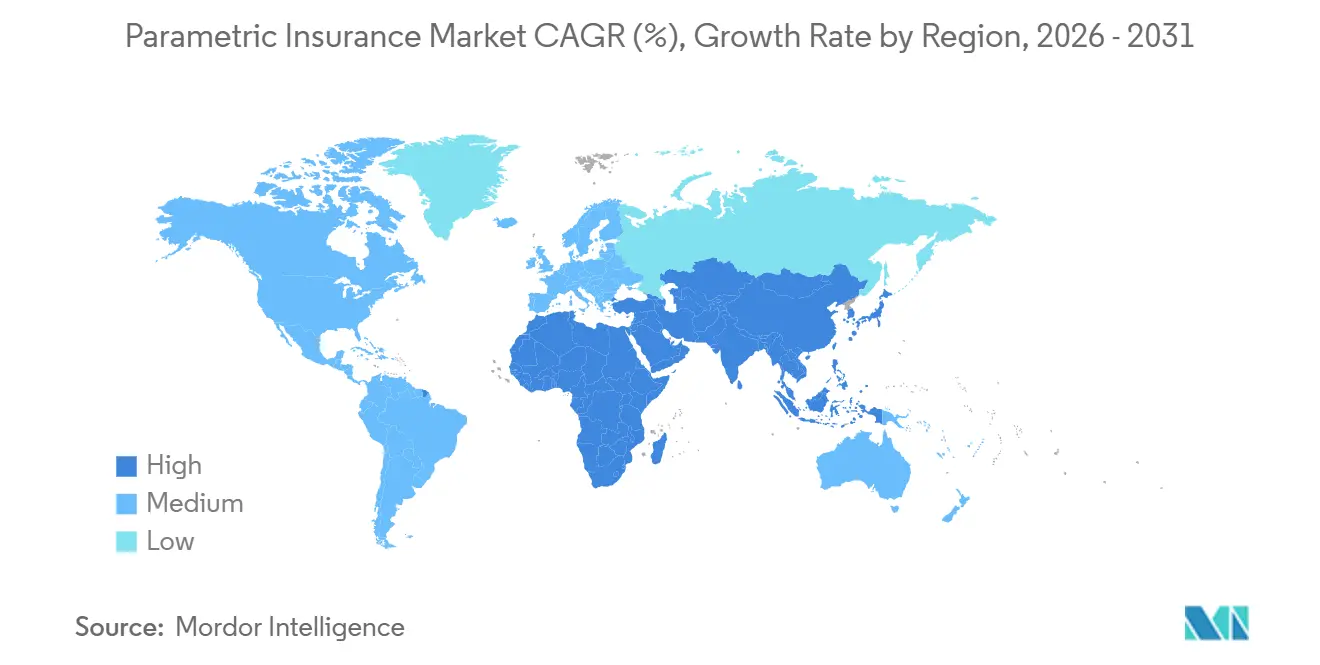

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Parametric Insurance Market Analysis by Mordor Intelligence

The Parametric Insurance Market size is expected to increase from USD 3.48 billion in 2025 to USD 4.02 billion in 2026 and reach USD 7.64 billion by 2031, growing at a CAGR of 13.69% over 2026-2031.

The parametric insurance market is gaining a stronger role in risk financing because climate losses are rising and buyers want capital support that can move quickly after a trigger event. Swiss Re Institute recorded global insured natural catastrophe losses of USD 107 billion in 2025, with secondary perils accounting for 92% of that total, which keeps attention on products built for rapid payouts and scalable deployment. In emerging economies, 80% to 90% of economic losses remained uninsured in 2025, which continued to support the case for index-based structures that do not depend on dense loss-adjustment networks. Competition in the parametric insurance market is widening across reinsurers, brokers, Lloyd's syndicates, and specialist insurtech firms, and this broader capacity base is already affecting pricing conditions. Aon's mid-2025 reinsurance review reported meaningful rate reductions on parametric solutions at the January 2026 renewals, pointing to a parametric insurance market moving from niche structuring toward more competitive placement terms.

Key Report Takeaways

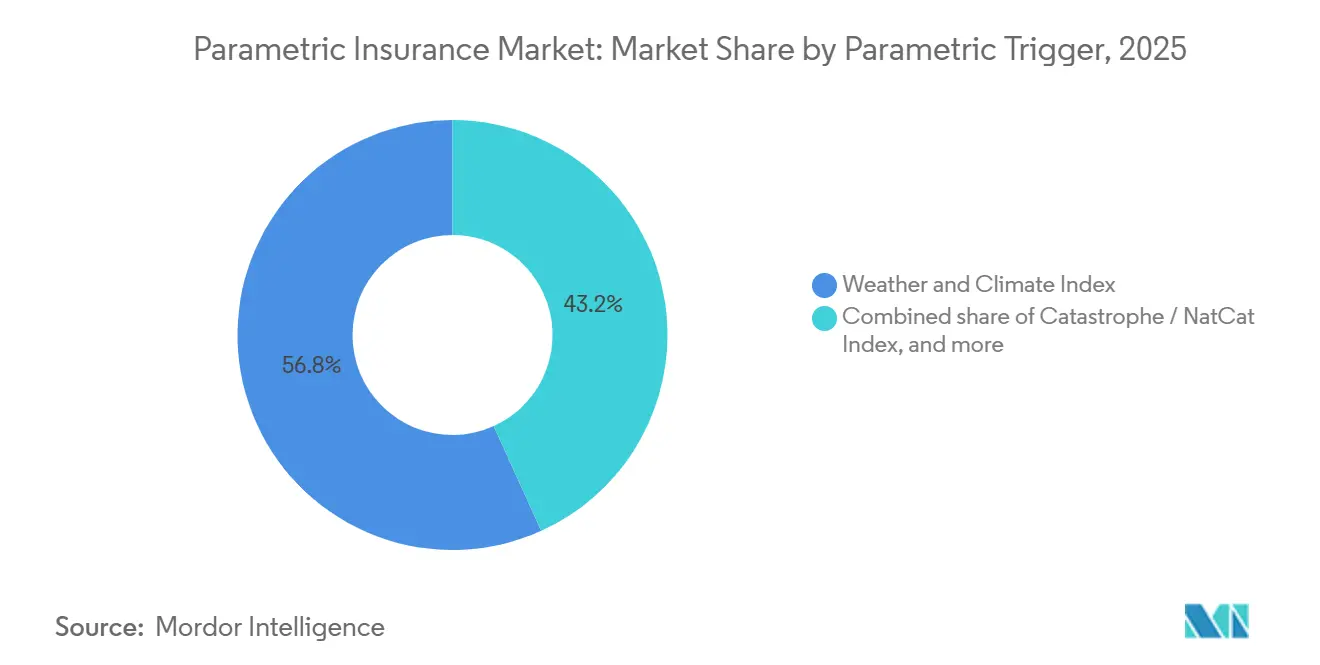

- By parametric trigger, weather & climate index captured 56.77% of the parametric insurance market share in 2025, while the catastrophe/natcat index is projected to grow at 15.89% CAGR through 2031.

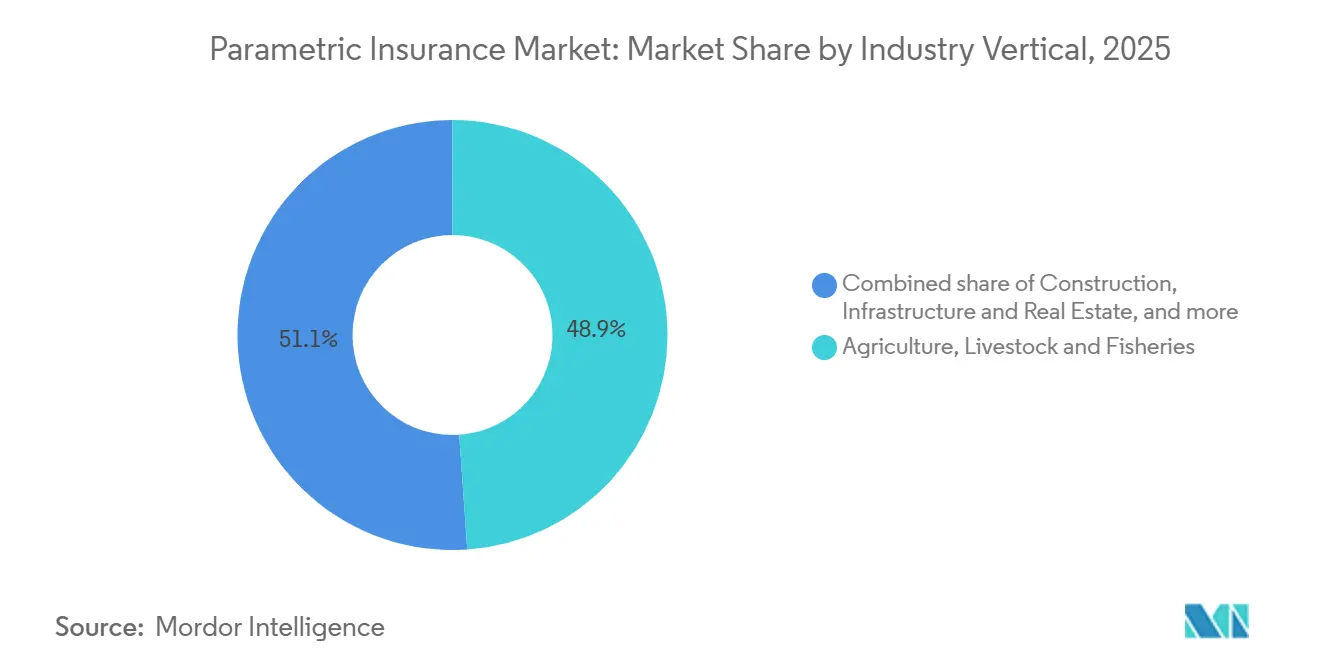

- By industry vertical, agriculture, livestock & fisheries accounted for 48.91% of the parametric insurance market share in 2025, while energy & utilities is projected to grow at 17.24% CAGR through 2031.

- By distribution channel, brokers & intermediaries held 41.25% of the parametric insurance market share in 2025, while digital/online platforms & aggregators are projected to grow at 18.46% CAGR through 2031.

- By geography, Asia-Pacific held 34.69% of the parametric insurance market share in 2025, while the Middle East and Africa region is projected to grow at 16.72% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Parametric Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Frequency of Climate-Linked Loss Events | +3.5% | Global, with stronger gains in Asia-Pacific, North America, and Middle East and Africa | Short term (≤ 2 years) |

| Faster Payout Expectations From Corporate Buyers | +2.2% | North America and Europe, with spillover into Asia-Pacific | Medium term (2-4 years) |

| Expansion of Agricultural Index Coverage | +2.5% | Asia-Pacific core, with spillover into South America and Sub-Saharan Africa | Medium term (2-4 years) |

| Adoption of Satellite, IoT, and Remote Sensing Inputs | +2.0% | Global, with faster gains in data-thin emerging markets | Medium term (2-4 years) |

| Growth of Non-Physical Risk Transfer Use Cases | +1.5% | North America and Europe for cyber and supply chain, and Asia-Pacific for digital commerce | Long term (≥ 4 years) |

| Reinsurer and Lloyd's Capacity Expansion | +1.0% | Global, with Lloyd's and Bermuda as origination hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Frequency of Climate-Linked Loss Events

The parametric insurance market is benefiting from a steady rise in climate-linked loss events, widening the gap between economic damage and insured recovery. Swiss Re Institute projected global insured catastrophe losses of USD 148 billion in 2026, with the total expected to reach USD 186 billion by 2030, extending a long pattern of annual real growth in disaster losses[1]Natural Catastrophe Insured Losses Hit $107 Billion in 2025 as Wildfire and Storm Risks Accelerate - Risk & Insurance : Risk & Insurance, RISKANDINSURANCE.COM. Wildfire has become one of the clearest examples of this pattern, and the January 2025 Palisades and Eaton wildfires in Los Angeles County generated USD 40 billion in combined insured losses. Aon's 2026 Climate and Catastrophe Insight report recorded global economic losses of USD 260 billion in 2025, and half of that total remained uninsured, with flooding events across South and Southeast Asia standing out as a major gap area. This loss pattern is supporting the parametric insurance market because buyers need faster liquidity, while suppliers also want broader diversification across perils and regions. The result is a parametric insurance market that is growing faster than broader premium pools because it addresses both liquidity timing and coverage gap pressures simultaneously.

Faster Payout Expectations from Corporate Buyers

The parametric insurance market is also being driven by a simple buyer requirement: faster access to funds after an event. Corporate risk managers are now comparing products not only by coverage scope but also by how quickly a payout can be moved to the balance sheet after a verified trigger. Aon's 2025 reinsurance review noted stronger corporate demand for parametric products, with buyers looking for rapid capital relief, immediate liquidity, and capital diversification at renewal. Willis Towers Watson's 2026 Capacity Revenue Protection launch for PJM energy producers showed how trigger-based structures are being tailored to specific revenue risks rather than broad damage scenarios[2]Insurance Business Magazine, “Willis Launches Parametric Solution to Plug Capacity Revenue Gap for PJM Energy Producers,” Insurance Business Magazine, insurancebusinessmag.com. This shift matters because settlement speed is now being treated as a product feature, and that expectation is helping the parametric insurance market move deeper into mainstream corporate procurement. The parametric insurance market is therefore benefiting from a demand profile that favors quick, predictable transfers of funds over slower claims processes.

Expansion of Agricultural Index Coverage

The parametric insurance market continues to draw major support from agricultural index coverage, especially in regions where smallholder farmers have little access to conventional claims infrastructure. Swiss Re stated that parametric agricultural insurance is growing at 15% to 20% annually, compared with 5% for traditional agricultural insurance, reflecting the scale of unmet demand across smallholder farming systems. Swiss Re also highlighted product structures based on soil moisture, NDVI, and area yield data, which allow standardized coverage across different farming regions using remote data inputs. Brazil's SUSEP-regulated parametric agricultural segment expanded from 4 to 14 registered products between 2020 and 2025, and coverage in 2025 reached 160 policies over 11,900 hectares, nearly double the prior year's area[3]Cobertura paramétrica avança em meio a desafios de escala e confiança | Seguros e Resseguros | Valor Econômico, VALOR.GLOBO.COM . Chile's August 2025 approval of commercial parametric insurance adds to the pattern that regulatory recognition often precedes full commercial scale, giving the parametric insurance market a clearer path for development in developing economies. For the parametric insurance market, agriculture remains both a large revenue base and a proven route for public and private expansion.

Adoption of Satellite, IoT, and Remote Sensing Inputs

The parametric insurance market is being reshaped by better observation tools, especially satellite data, sensor networks, and automated analytics. These tools are expanding the range of insurable perils and making it easier to launch products in areas with limited historical on-the-ground data. In June 2026, Liberty Mutual Reinsurance and ICEYE launched a building-level parametric wildfire product for assets in the United States and Australia that uses SAR satellite imagery to classify each property within hours of an event[4]ICEYE and Liberty Mutual Reinsurance, “Liberty and ICEYE Partner to Deliver Market-First Parametric Wildfire Insurance Cover,” ICEYE Press Release, iceye.com. A peer-reviewed Nature study discussed in July 2025 showed that multi-index triggers can reduce basis risk in tsunami covers when several observation points are used instead of a single input. That finding matters across the parametric insurance market because it supports more precise trigger design without changing the core product structure. The parametric insurance market is therefore moving toward an environment where data quality and data control matter as much as pure underwriting capacity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Basis Risk and Trigger Mismatch | -1.8% | Global, with the highest pressure in data-sparse emerging markets such as Sub-Saharan Africa and Southeast Asia | Medium term (2-4 years) |

| Regulatory Fragmentation Across Jurisdictions | -1.2% | Emerging markets globally and cross-border European structures | Medium term (2-4 years) |

| Limited Historical Data for Emerging Perils | -0.9% | Asia-Pacific, Middle East and Africa, and South America for newer perils such as cyber and NatCat structures | Long term (≥ 4 years) |

| Data Lineage, Auditability, and Model Governance Burden | -0.7% | European Union, United Kingdom, and regulated Asian environments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Basis Risk and Trigger Mismatch

Basis risk remains the main restraint on the parametric insurance market because buyers want confidence that a trigger outcome will closely track real financial loss. The Geneva Papers on Risk and Insurance published 2025 research showing that portfolio-level basis risk declines as the number of independent parametric contracts increases, suggesting the issue can be managed at scale rather than treated as a structural failure of the product. The same study identified spatial misalignment between exposure locations and weather stations as a key driver, suggesting that better trigger network design is a practical fix. The challenge is not only technical, as many buyers without deep risk teams struggle to assess the gap between index behavior and their expected loss patterns. That expectation gap can create dissatisfaction even when a contract performs exactly as written, and that risk slows adoption in parts of the parametric insurance market where mid-sized buyers are still learning the product.

Regulatory Fragmentation Across Jurisdictions

The parametric insurance market also faces a regulatory challenge, as legal treatment still varies by jurisdiction. In some places, parametric structures are regulated as insurance; in others, they are treated more like financial derivatives; and in several markets, there is still no clear category at all. The Bank for International Settlements Financial Stability Institute, based on a survey of 12 insurance supervisory authorities, found that inconsistent rules around trigger data sources, accreditation standards, and product complexity are slowing wider adoption beyond agriculture. That means market entry often depends on regulatory mapping before any broad distribution strategy can be finalized. New York only formally added parametric insurance as a covered category under state law in January 2025, which shows that even advanced insurance markets are still building their frameworks. For the parametric insurance market, this fragmentation raises compliance costs, slows product replication, and can alter economics across borders.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Parametric Trigger: NatCat Index Demand Accelerates as Weather Triggers Mature

Weather & Climate Index held 56.77% of the parametric insurance market share in 2025, while Catastrophe/NatCat Index is projected to grow at 15.89% CAGR between 2026-2031. Weather triggers remain the largest part of the parametric insurance market because they are supported by long meteorological records and easier standardization across buyers and territories. That maturity is also starting to compress margins, which is making product design more important than simple availability. Catastrophe and NatCat structures are gaining traction because sovereigns and corporate buyers need rapid liquidity for earthquake, cyclone, and wildfire events that can overwhelm traditional claims timelines. Swiss Re's projection of USD 148 billion in insured catastrophe losses in 2026 keeps demand focused on products that can closely align payout timing with the frequency of large events.

The parametric insurance market is also seeing trigger expansion beyond weather into cyber downtime, supply chain disruption, and other non-physical loss structures. These other index-based triggers remain smaller, but they are important because they reach risks that standard indemnity forms often cover only partially or not at all. Liberty Mutual Reinsurance and ICEYE's June 2026 wildfire solution demonstrated how SAR imagery can support more precise NatCat verification at the structure level, thereby improving confidence in trigger performance. The Bermuda Monetary Authority's work on a fully collateralized regulatory class for parametric structures also points to more capital support for NatCat products in the coming years. Research on multi-index design published in 2025 further supports the direction of travel in the parametric insurance industry, where trigger precision is becoming a core part of competition rather than a secondary technical feature.

By Distribution Channel: Brokers Retain Complexity Mandates While Digital Platforms Redefine Access

Brokers & Intermediaries accounted for 41.25% of the parametric insurance market size in 2025, while Digital/Online Platforms & Aggregators are projected to grow at 18.46% CAGR between 2026-2031. Brokers continue to lead because many government and corporate programs require bespoke trigger calibration, reinsurance placement, and regular index monitoring. That advisory layer remains difficult to replace when structures are large or cover multiple perils and jurisdictions. At the same time, digital platforms are becoming the fastest-growing route because they lower access barriers for smaller buyers and shorten placement timelines. EHAB's May 2026 WeatherWise Studio launch, built on 45 years of global weather data with automated structuring and API integration, showed how the parametric insurance market is moving toward faster digital product assembly.

The parametric insurance market is also showing that digital access does not mean brokers are losing relevance across all use cases. Parametrix's May 2025 embedded program inside endpoint detection and response vendor warranties showed that standardized digital triggers can be distributed directly at the point of sale without a broker-led process. Direct sales still matter for sovereign and supranational buyers such as African Risk Capacity and CCRIF, where multi-year program negotiation often happens directly with reinsurer groups. Willis Towers Watson's November 2025 fisheries program in the Philippines, launched with Rare and the Bureau of Fisheries and Aquatic Resources, also showed that direct partnership models can expand access in places commercial distribution networks do not cover well. Over time, the parametric insurance industry appears to be moving toward channel convergence, where advisory strength and platform capability increasingly work together rather than compete as separate models.

By Industry Vertical: Agriculture Anchors Volume as Energy Sector Drives the Next Growth Wave

Agriculture, Livestock & Fisheries accounted for 48.91% of the parametric insurance market in 2025, while Energy & Utilities is projected to grow at a 17.24% CAGR through 2031. Agriculture remains the largest vertical because government-backed crop programs in India, China, and Brazil continue to provide scale that other verticals do not yet match. Swiss Re's Opti-Crop platform, which combines satellite-based NDVI, soil moisture, rainfall indices, and crop yield modeling, shows how large reinsurers are turning proprietary data into distribution advantages across developing agricultural markets. That base is likely to remain important for the parametric insurance market because it aligns with protection gap needs and public policy support. Agriculture, therefore, anchors the current volume even as other verticals deliver faster incremental growth.

Energy & Utilities is growing faster because renewable developers increasingly need coverage that stabilizes cash flows and supports lender requirements. In September 2025, kWh Analytics closed a parametric Wind Proxy Hedge for Apex Clean Energy's 79MW Virginia project, with Munich Re providing the hedge and a financing structure that generated USD 7 of additional debt capacity per USD 1 of premium. Willis Towers Watson also reported a doubling of demand from Indian renewable developers since 2023, and Munich Re received initial requests from clean energy companies in China and India, which shows that expansion is broadening across major energy markets. Construction, infrastructure, and real estate are using trigger-based structures for project completion and weather revenue shortfalls, while manufacturing and logistics buyers are using non-physical damage business interruption covers for supplier and digital infrastructure disruptions. Government and public services also remain important through sovereign risk pools such as African Risk Capacity and SEADRIF, which are now extending program logic beyond sovereign buyers to household and SME levels.

Geography Analysis

Asia-Pacific accounted for 34.69% of the parametric insurance market in 2025, making it the largest regional contributor. The region leads because it combines high disaster exposure, large agricultural populations, and active government support for index-based insurance. Japan's established insurers are already moving from pilot work toward broader commercial deployment, with Tokio Marine offering EQuick for earthquake cover and Mitsui Sumitomo launching a weather index insurance product in 2025. Indonesia's March 2026 decision to launch a national parametric scheme for coffee and cocoa smallholder farmers showed that public programs remain central in Southeast Asian expansion. SEADRIF Insurance Company's 2025 household-level policy in Lao PDR, with USD 1.1 million of protection across floods, cyclones, earthquakes, and landslides, provides a model that can be extended to nearby markets with similar risk profiles.

North America and Europe remain major centers of premium concentration in the parametric insurance market, supported by corporate demand for wildfire, hurricane, and severe convective storm coverage. New York's January 2025 legal recognition of parametric insurance removed an important source of uncertainty for product structuring in the United States. In France, the parametric segment was estimated at EUR 130 million to EUR 500 million, which is equivalent to USD 143 million to USD 550 million at 2025 average rates, and the category was reported to be growing at double-digit annual rates. Howden France's 2026 market review also identified parametric solutions as one of the opportunity areas attracting added attention in French reinsurance. Lloyd's capacity reached GBP 56 billion in 2025, and the presence of dedicated parametric syndicates such as NormanMax Syndicate 3939 and Canopius Syndicate 4444's partnership with global parametrics shows how much innovation is concentrated in the London market.

The Middle East and Africa region is projected to grow at a 16.72% CAGR through 2031, giving it the fastest regional outlook in the parametric insurance market. Growth is being supported by sovereign risk pools, a large protection gap, and broader insurance infrastructure development in Gulf and African markets. African Risk Capacity has protected more than 26.4 million people and paid over USD 170 million in indemnities since inception, thereby strengthening the case for greater commercial reinsurance participation. South America is still earlier in commercial development, but Chile's 2025 approval of commercial parametric insurance and Brazil's 2025 expansion in agricultural products show that the regional pipeline is becoming more concrete. McKinsey's 2025 regional insurance review also noted 11% annual premium growth in Latin America between 2019 and 2024, which supports the underlying commercial infrastructure needed for wider parametric distribution.

Competitive Landscape

The parametric insurance market remains moderately fragmented, with global reinsurers, major brokers, Lloyd's syndicates, and specialist insurtechs all competing on different strengths. Munich Re, Swiss Re, and Hannover Re anchor much of the capacity base, while Aon, Marsh McLennan, and Willis Towers Watson play a leading role in program design and placement. Lloyd's syndicates extend specialty capacity, and firms such as Parametrix, FloodFlash, Global Parametrics, and Descartes Underwriting continue to set benchmarks in product design and data-led execution. A key feature of the parametric insurance market is that product differentiation increasingly comes from data ownership, modeling depth, and trigger architecture rather than from balance sheet size alone. This is changing the competitive pattern because smaller specialists with unique datasets can shape the direction of the broader parametric insurance market faster than their scale would normally suggest.

Parametrix's April 2026 placement of Cumulus Re III, a USD 35 million catastrophe bond for Hannover Re backed by cloud outage data, is a clear example of how proprietary information assets can support market position. NormanMax's May 2025 acquisition of FloodFlash combined IoT flood-depth sensor capability and Lloyd's coverholder strength into a single platform, improving both underwriting and distribution reach. Liberty Mutual Reinsurance and ICEYE's June 2026 wildfire launch demonstrated another competitive route, where a carrier and a data company combine to improve product performance and speed simultaneously. These moves show that competition in the parametric insurance market now depends heavily on who can build dependable trigger systems and turn them into repeatable commercial products. The parametric insurance market is therefore rewarding firms that combine capacity, distribution, and verified external data in a tighter operating model.

White-space opportunities still exist in the parametric insurance market, especially among SMEs without broker relationships, non-physical risk triggers such as cyber and supply chain disruption, and household-level extensions of sovereign risk programs in Africa and Southeast Asia. The Bermuda Monetary Authority's work on a fully collateralized regulatory class for parametric structures indicates additional support for capital-market-linked product forms. Established reinsurers are also facing pressure as weather index products become easier to access and compare, which reduces room for simple capacity-led differentiation. Their response is increasingly visible in crop modeling, trigger calibration, and platform development, where in-house processing capability can create pricing advantages that pure capacity providers cannot match. That response suggests the parametric insurance industry is entering a phase in which operating infrastructure matters as much as underwriting scale.

Parametric Insurance Industry Leaders

Allianz SE

AXA SA

Berkshire Hathaway Inc.

Chubb Limited

Munich Reinsurance Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Liberty Mutual Reinsurance and ICEYE launched a building-level parametric wildfire insurance product covering assets in the United States and Australia, using SAR satellite imagery to classify property damage within hours of an event without physical loss assessment. Structured for global scale, the program will expand into new territories as ICEYE extends its satellite constellation, representing the first commercially available structure-level, satellite-verified parametric wildfire cover.

- June 2026: Descartes Underwriting and Nextpower launched an integrated parametric solution for extreme straight-line wind events at solar power plants, providing up to USD 80 million in limits per policy globally and up to USD 100 million in the US, with triggers based on site-level wind data from Nextpower meteorological stations. The product addresses one of the most destructive and underinsured perils in the global solar sector and can be bundled with satellite-based tornado and hail products.

- April 2026: Parametrix structured and placed Cumulus Re III, a USD 35 million parametric catastrophe bond for Hannover Re covering cloud-outage event accumulation, a 75% increase over the USD 20 million 2025 issuance and 155% growth from the inaugural USD 13.75 million 2024 transaction. The bond's rapid scaling reflects deeper investor appetite for non-correlated parametric cyber risk as a mainstream ILS peril.

- March 2026: Indonesia's government announced a national parametric insurance scheme for coffee and cocoa smallholder farmers, co-funded by the InsuResilience Solutions Fund, the first sovereign commitment to sector-wide parametric coverage for commodity smallholders in Southeast Asia's largest economy.

Global Parametric Insurance Market Report Scope

| Weather & Climate Index |

| Catastrophe / NatCat Index |

| Other Index-Based Triggers |

| Direct Sales |

| Brokers & Intermediaries |

| Digital / Online Platforms & Aggregators |

| Other Channels |

| Agriculture, Livestock & Fisheries |

| Energy & Utilities |

| Construction, Infrastructure & Real Estate |

| Manufacturing & Supply Chain / Logistics |

| Transportation & Aviation |

| Government & Public Services |

| Other Industry Verticals |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Indonesia | |

| Thailand | |

| Malaysia | |

| Singapore | |

| Vietnam | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Parametric Trigger | Weather & Climate Index | |

| Catastrophe / NatCat Index | ||

| Other Index-Based Triggers | ||

| By Distribution Channel | Direct Sales | |

| Brokers & Intermediaries | ||

| Digital / Online Platforms & Aggregators | ||

| Other Channels | ||

| By Industry Vertical | Agriculture, Livestock & Fisheries | |

| Energy & Utilities | ||

| Construction, Infrastructure & Real Estate | ||

| Manufacturing & Supply Chain / Logistics | ||

| Transportation & Aviation | ||

| Government & Public Services | ||

| Other Industry Verticals | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Thailand | ||

| Malaysia | ||

| Singapore | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is driving growth in parametric insurance through 2031?

Growth is being supported by rising catastrophe losses, faster payout expectations, broader agricultural index coverage, and wider use of satellite and sensor data. The market is projected to grow from USD 4.02 billion in 2026 to USD 7.64 billion by 2031 at a 13.69% CAGR.

Which trigger type leads revenue today?

Weather & Climate Index led with 56.77% share in 2025 because it benefits from long historical datasets and easier product standardization across large buyer groups.

Which trigger type is growing the fastest?

Catastrophe/NatCat Index is the fastest-growing trigger type, with a projected 15.89% CAGR between 2026 and 2031, driven by demand for fast liquidity after earthquake, cyclone, and wildfire events.

Why does agriculture remain important for insurers and reinsurers?

Agriculture, Livestock & Fisheries accounted for 48.91% of revenue in 2025 because sovereign and government-backed crop programs still provide the largest volume base in many developing economies.

What is changing in distribution across buyers?

Brokers & Intermediaries led with 41.25% share in 2025, but Digital/Online Platforms & Aggregators are growing fastest at an 18.46% CAGR as automated structuring and API-based product access improve.

Which region shows the strongest expansion outlook?

The Middle East and Africa region has the fastest projected growth at a 16.72% CAGR through 2031, supported by sovereign risk pools, a wide protection gap, and expanding insurance infrastructure.

Page last updated on: