Paper Stretch-Wrap And Paper-Based Unitization Materials Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

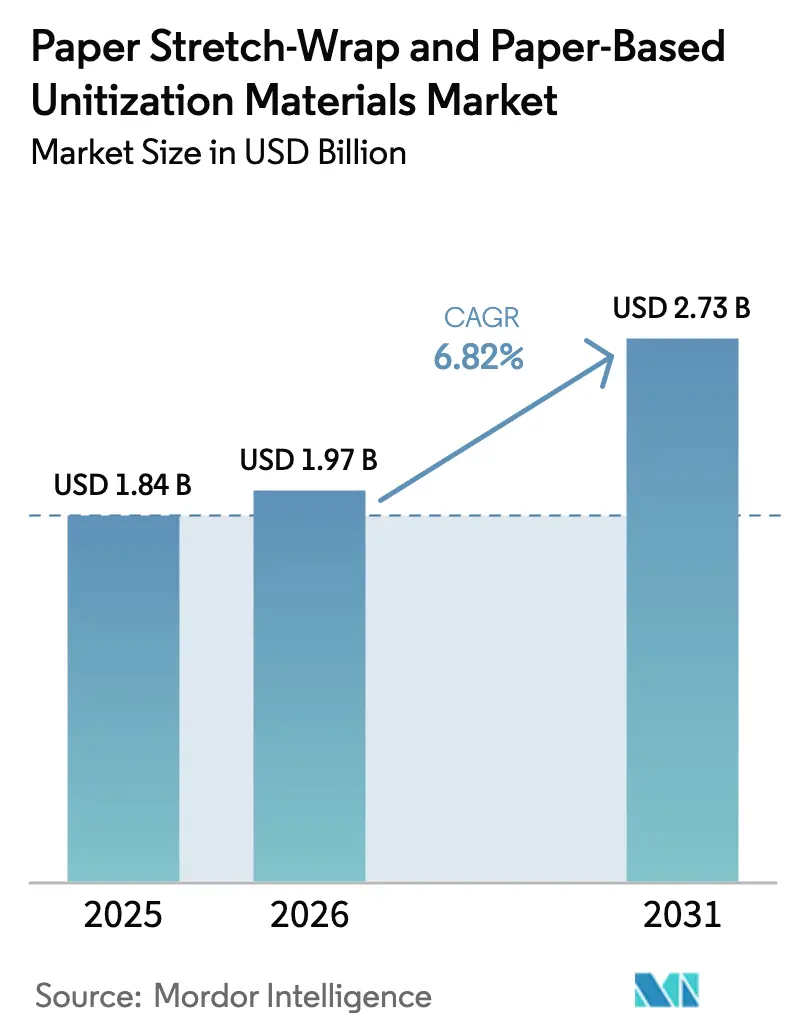

| Market Size (2026) | USD 1.97 Billion |

| Market Size (2031) | USD 2.73 Billion |

| Growth Rate (2026 - 2031) | 6.82% CAGR |

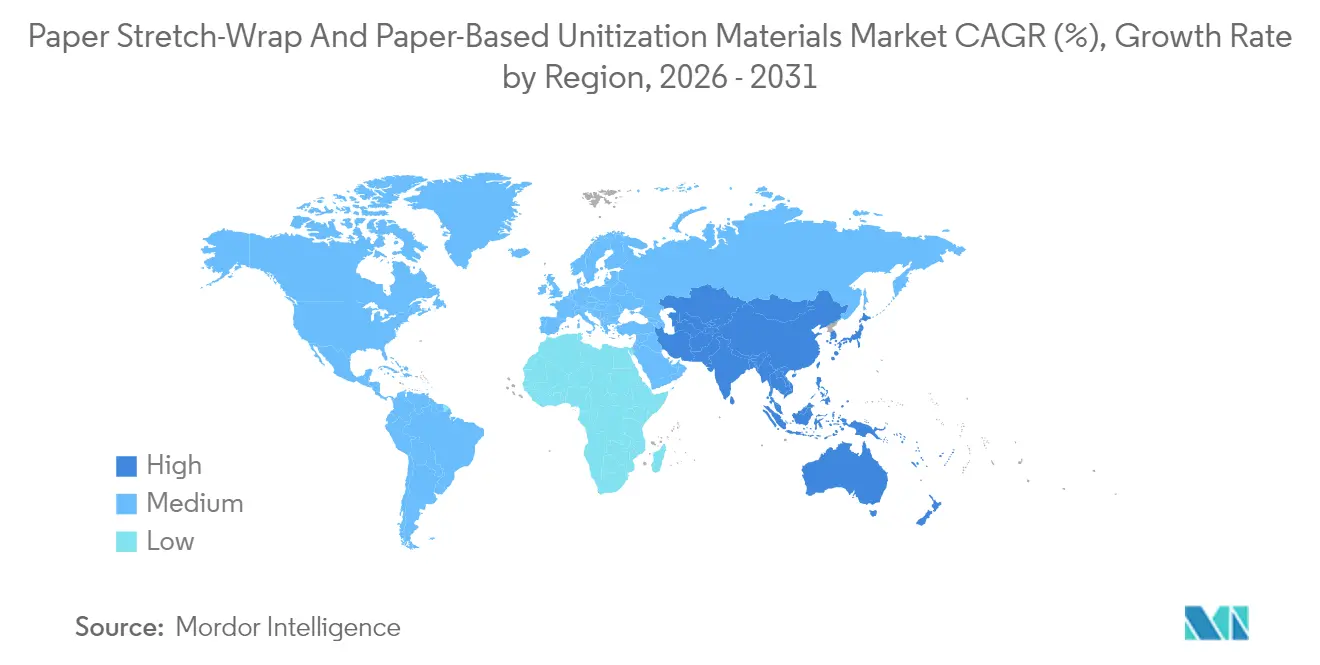

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

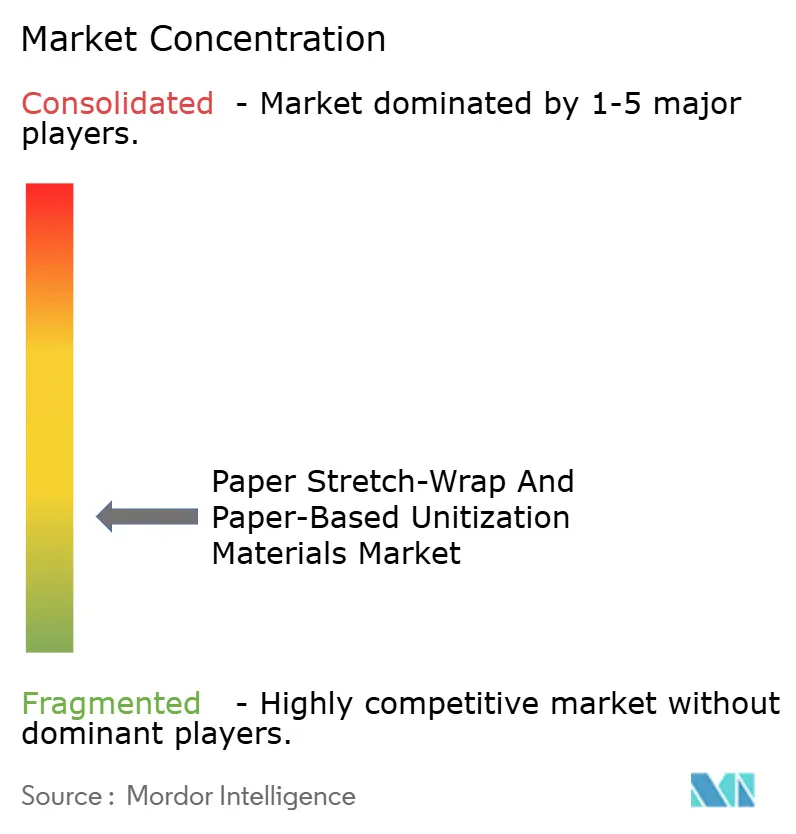

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Paper Stretch-Wrap And Paper-Based Unitization Materials Market Analysis by Mordor Intelligence

The Paper Stretch-Wrap and Paper-Based Unitization Materials market size is expected to grow from USD 1.84 billion in 2025 to USD 1.97 billion in 2026 and is forecast to reach USD 2.73 billion by 2031 at 6.82% CAGR over 2026-2031. Rising corporate sustainability mandates, tightening laws on single-use plastics, and breakthroughs in bio-coating technology are propelling this growth trajectory. Logistics networks are transitioning to paper-based wraps because new plant-derived barrier layers deliver moisture resistance that rivals polyethylene, while preserving recyclability. E-commerce fulfillment centers prefer modular tapes and straps that simplify reverse logistics workflows and satisfy brand owner mono-material targets. Suppliers investing in machine-compatible paper formulations and water-resistant coatings command premium pricing, while legacy commodity players face margin pressure. Regulatory momentum toward extended producer responsibility accelerates adoption, but it also raises compliance costs for small converters.

Key Report Takeaways

- By product type, paper stretch-wrap captured 40.95% of the paper stretch-wrap and paper-based unitization materials market share in 2025.

- By material basis, the market size for recycled paper is forecast to advance at a 7.55% CAGR through 2031.

- By end-use industry, food and beverage captured 30.88% of the paper stretch-wrap and paper-based unitization materials market share in 2025.

- By geography, the market size for the Asia-Pacific region is forecast to advance at an 7.79% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Paper Stretch-Wrap And Paper-Based Unitization Materials Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Corporate Sustainability Mandates to Replace Fossil-Based Stretch Films | +1.5% | Global, with early adoption in North America and EU | Medium term (2-4 years) |

| Regulatory Bans and Eco-Taxes on Single-Use Plastics | +1.2% | North America and EU core, expanding to APAC | Short term (≤ 2 years) |

| Rapid Growth of E-Commerce Palletised Shipments | +0.8% | Global, concentrated in urban logistics hubs | Short term (≤ 2 years) |

| Brand-Owner Demand for Mono-Material Packaging Solutions | +0.7% | Global, led by multinational FMCG companies | Medium term (2-4 years) |

| Breakthrough Water-Resistant Bio-Coatings Enabling Paper Stretchability | +0.9% | North America and EU initial deployment, APAC scaling | Long term (≥ 4 years) |

| National EPR Laws Targeting Tertiary Packaging Waste | +1.1% | EU leadership, North America following, APAC emerging | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Corporate Sustainability Mandates to Replace Fossil-Based Stretch Films

Large retailers and logistics providers have issued 2025-2027 timelines for phasing out petroleum-based stretch films. Guaranteed volume contracts de-risk supplier investments in paper lines and shrink historic cost gaps. Load-stability metrics now dominate procurement criteria, shifting the conversation away from pure price. Multinationals report that aligning tertiary packaging with Scope 3 emissions targets delivers measurable progress toward net-zero pledges. As mandates spread from high-profile brands to tier-two suppliers, volumes for paper stretch-wrap scale quickly.[1]Seaman Paper, “Seaman Paper Launches SeaStretch, a Lightweight Paper-Based Alternative to Plastic Pallet Wrap,” PaperAge, paperage.com

Regulatory Bans and Eco-Taxes on Single-Use Plastics

California’s SB 54 and parallel EU directives require single-use packaging to be recyclable or compostable, spotlighting industrial films previously exempt from scrutiny. Graduated eco-taxes in several EU states add up to USD 1,000 per metric ton on non-recyclable pallet wrap, tipping total cost of ownership in favor of paper. Enforcement includes surprise audits and escalating fines, nudging even late adopters toward compliant materials. Jurisdictional variance drives global companies to harmonize on the strictest rules to streamline supply chains. The legislation accelerates equipment upgrades as converters chase demand spikes.

Rapid Growth of E-Commerce Palletised Shipments

Online retail warehouses turn pallets over multiple times per week and favor unitization materials that can be removed cleanly for returns processing. Approximately 18% of online orders are returned through reverse channels, increasing wrap usage rates and driving demand for recyclable options. Modular paper straps support mixed-SKU loads and reduce film waste. Fulfillment centers also value wraps that display sustainability messaging, enhancing brand perception. E-commerce is on track to eclipse food manufacturing as the largest demand vertical by 2027.

Brand-Owner Demand for Mono-Material Packaging Solutions

Consumer goods leaders are cutting packaging SKUs and aligning primary, secondary, and tertiary materials. Using paper across all layers simplifies recycling streams and reduces audit complexity across dozens of markets. Mono-material pallets integrate with closed-loop fiber recovery programs that recirculate material up to seven times before downgrading. Brand owners cite double-digit reductions in landfill diversion fees after conversions. Suppliers able to bundle wrap, tape, and corner protection in compatible grades win multi-year contracts.[2]Pyxera Global, “Optimizing Circular Logistics: A Revisited Approach,” Pyxera Global, pyxeraglobal.org

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher Unit Cost of Paper Wrap Relative to PE Stretch Film | -0.8% | Global, most acute in price-sensitive emerging markets | Short term (≤ 2 years) |

| Limited Moisture and Puncture Resistance in Humid Logistics Chains | -0.6% | Tropical and coastal regions, cold-chain logistics | Medium term (2-4 years) |

| Retrofitting Costs for Existing Pallet-Wrapping Machinery | -0.4% | Established logistics hubs with legacy equipment | Short term (≤ 2 years) |

| Fiber-Supply Tightness due to Competing Paper Packaging Applications | -0.5% | Regions with limited forestry resources, APAC manufacturing centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Higher Unit Cost of Paper Wrap Relative to PE Stretch Film

Paper-based wraps carry 15-25% premiums driven by costlier fibers, coating steps, and lower scale. Small logistics firms struggle to justify upgrades without regulatory push. Price gaps widen in regions reliant on imported pulp, forcing converters to blend recycled content to manage costs. As automation boosts output and fiber supply loosens, the differential is expected to narrow but remain material through 2027. Cost-sharing models, where large customers guarantee minimum volumes, are emerging to mitigate capex barriers.[3]IMPACK, “Pricing,” IMPACK, impack.ca

Limited Moisture and Puncture Resistance in Humid Logistics Chains

Humidity above 70% degrades uncoated paper wraps, causing fiber swelling and load shifting. Cold-chain routes add condensation risk that can halve tensile strength within 48 hours. Bio-coated grades improve water vapor resistance yet price at 20-30% premiums, limiting penetration outside high-value goods. Sharp-edged metal parts and glass products continue to rely on plastic films for puncture defense. Suppliers are testing hybrid fiber-polymer webs, but recyclability hurdles delay commercialization.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Stretch-Wrap Dominance and Tape Momentum

Paper Stretch-Wrap captured 40.95% of 2025 revenue, underscoring its role as the go-to substitute for polyethylene films in mainstream palletizing lines. Roughly 78% of new high-speed wrappers installed in North America during 2024 featured paper-capable tension controls. The Paper Stretch-Wrap and Paper-Based Unitization Materials market size for stretch-wrap is forecast to reach USD 1.09 billion by 2031, tracking a 6.31% CAGR. Suppliers highlight lower material usage per pallet because crepe structures enable tighter turns with fewer revolutions, thereby reducing overall fiber demand.

Strapping and Banding Tapes are on pace for the fastest expansion at 7.08% CAGR, driven by e-commerce hubs seeking selective reinforcement that eases de-skidding during cross-docking. Tapes also serve as brandable bands that carry QR codes for inventory scanning. Wrap-Around Corrugated Sleeves maintain niche traction in industrial goods where rigid containment protects high-value components. Integration trends suggest hybrid pallets, combining a thin stretch-wrap base with strategic tape placements, will define next-generation unitization standards.

By Material Basis: Virgin Strength and Recycled Upside

Virgin Paper delivered 56.15% of 2025 sales because high-speed automated lines demand fiber uniformity that recycled furnish struggles to match. The material delivers consistent elongation at break, minimizing film breaks and downtime. Composite bio-coated virgin grades enable deployment in chilled warehouses, achieving 95% wrap integrity after 48-hour humidity tests. Nevertheless, Recycled Paper’s 7.55% CAGR signals circular economy pressure reshaping fiber sourcing. Brand owners pledge to source 30-50% post-consumer content by 2028, forcing converters to refine their de-inking and strength additives.

Composite/Bio-Coated Paper sits in the premium tier, priced approximately 25% above its uncoated equivalents. The Paper Stretch-Wrap and Paper-Based Unitization Materials market share for bio-coated formulations is projected to double from 6.25% in 2025 to 12.40% by 2031, reflecting the wider acceptance that will follow once line trials confirm the moisture performance. Regional legislation mandating recycled content in tertiary packaging, especially across the EU, accelerates the shift toward high-performance recycled substrates.

By End-Use Industry: Food Leadership and Logistics Upswing

Food and Beverage maintained 30.88% of demand because paper avoids migration fears associated with plasticizers, while supporting compostable waste streams in grocery distribution centers. Fresh produce exporters in Spain report 12% lower rejection rates after adopting breathable paper wrap that mitigates moisture suction. Consumer Goods brands use paper strapping to create tamper-evident bundles that support shelf-ready displays.

Logistics and 3PL Warehousing is the fastest-growing sector at 7.34% CAGR, as fulfillment operators consume larger wrap volumes per order cycle. The Paper Stretch-Wrap and Paper-Based Unitization Materials market size for logistics applications is forecast to hit USD 742 million by 2031, driven by reverse logistics flows and urban micro-fulfillment nodes. Industrial Goods follow, harnessing puncture-resistant composite paper for heavy components, while pharmaceuticals adopt selective use for non-sterile accessories to avoid complex validation cycles.

Geography Analysis

Asia-Pacific held a 37.40% share in 2025, with China alone accounting for more pallets wrapped in paper than the entire EU. The regional CAGR of 7.79% reflects state-led green procurement rules and the fast-growing e-commerce ecosystem. Japan’s top three logistics firms are expected to shift 60% of their volume to paper wraps by mid-2025, citing superior recyclability under local waste management rules. South Korean converters leverage domestic starch-based coatings to defend against high humidity. Southeast Asia benefits from abundant fiber but faces quality dispersion, prompting multinationals to enter into dual sourcing agreements to hedge against variability.

North America combines mature infrastructure with regulatory escalation. California drives early adoption, and over 55% of new high-throughput distribution centers west of the Rockies specify dual-material wrappers that default to paper. Industry coalitions lobby for federal incentives mirroring EU eco-modulation fees. Canada’s extended producer responsibility scheme, effective as of 2025, reimburses up to 80% of recycling system costs for certified paper wraps, thereby boosting competitiveness.

Europe leads on policy sophistication. France applies a EUR 0.20 (USD 0.21) per kilogram penalty on non-recyclable pallet film starting in 2026, while Germany’s VerpackG amendment grants fee discounts for mono-material solutions. Bio-coated recycled grades are gaining traction in Benelux cold-chain corridors, where humidity hurdles previously favored plastic. Eastern Europe presents cost-sensitive pockets, but benefits from EU funding for sustainable packaging lines, steering converters toward paper-based solutions.

South America’s early movers include Brazil’s supermarket chains, which are testing paper straps for groceries. Import tariffs on coated paper challenge pricing, but domestic mills are partnering with European tech providers to license barrier formulations. Middle East demand hinges on diversification programs that push sustainability in logistics free zones. Africa remains nascent; however, pan-regional retailers are piloting paper wrap initiatives in South Africa as part of their extended value assurance schemes.

Competitive Landscape

The Paper Stretch-Wrap and Paper-Based Unitization Materials market comprises a moderately fragmented field, with the top five players accounting for approximately 32% of the global revenue. Integrated pulp-to-wrap giants, such as Mondi, Smurfit Kappa, and International Paper, utilize their mill networks to ensure a stable fiber supply and drive cost efficiencies. Specialty players, including Mosca and Signode, differentiate through application engineering, offering retrofit kits that adapt existing plastic lines to paper. Ranpak’s 2025 PaperWrap launch positions the company as an innovation leader, bridging cushioning and palletizing portfolios.

Technology developers are focusing on starch-modified bio-coatings that retain fiber recyclability while matching the moisture barriers of polyethylene. Seaman Paper’s SeaStretch features crepe micro-folds that increase stretch by 20%, leading to rapid adoption at automated sites. Equipment manufacturers unveil dual-material palletizers featuring auto-calibration sensors that switch tension profiles between plastic and paper, improving transition flexibility.

Strategic moves include M&A for regional scale. Seaman Paper’s 2024 acquisition of Julius Glatz GmbH establishes a European foothold amid tightening EU regulations. Antalis Packaging adds paper straps to its catalog, facilitating bundled sales. Start-ups are pursuing niche opportunities in reverse logistics by offering reusable paper bands embedded with RFID technology, which enables efficient tracking and management of goods. Negotiations center on multi-year offtake agreements that lock in bio-coated paper volumes, insulating producers from pulp price volatility.

Paper Stretch-Wrap And Paper-Based Unitization Materials Industry Leaders

Mondi plc

Smurfit WestRock plc

International Paper Company

Billerud AB

Mosca GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Ranpak Holdings Corp introduced PaperWrap, a pallet solution designed to replace plastic stretch film and boost transport security while cutting emissions.

- December 2024: Seaman Paper acquired Julius Glatz GmbH, adding European capacity for recyclable unitization grades.

- November 2024: Antalis Packaging launched biodegradable paper strapping and document wallets for e-commerce fulfillment.

- March 2024: Seaman Paper rolled out SeaStretch, a 42 gsm FSC-certified crepe paper wrap compatible with automated palletizing lines.

Global Paper Stretch-Wrap And Paper-Based Unitization Materials Market Report Scope

| Paper Stretch-Wrap |

| Wrap-Around Corrugated Paper Solutions |

| Strapping and Banding Tapes |

| Other Product Types |

| Virgin Paper |

| Recycled Paper |

| Composite/Bio-Coated Paper |

| Food and Beverage |

| Consumer Goods and E-Commerce Fulfilment |

| Industrial Goods and OEM Spare Parts |

| Pharmaceuticals and Healthcare |

| Logistics and 3PL Warehousing |

| Other End-Use Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| Turkey | ||

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Product Type | Paper Stretch-Wrap | ||

| Wrap-Around Corrugated Paper Solutions | |||

| Strapping and Banding Tapes | |||

| Other Product Types | |||

| By Material Basis | Virgin Paper | ||

| Recycled Paper | |||

| Composite/Bio-Coated Paper | |||

| By End-Use Industry | Food and Beverage | ||

| Consumer Goods and E-Commerce Fulfilment | |||

| Industrial Goods and OEM Spare Parts | |||

| Pharmaceuticals and Healthcare | |||

| Logistics and 3PL Warehousing | |||

| Other End-Use Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| Turkey | |||

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What factors are driving corporate adoption of paper stretch-wrap in logistics?

Sustainability mandates, single-use plastic taxes, and cost avoidance under extended producer responsibility laws are helping companies justify upgrades despite higher unit costs.

How large will demand from logistics and 3PL warehousing become by 2031?

Logistics applications are projected to reach USD 742 million, advancing at 7.34% CAGR as e-commerce parcel flows accelerate.

Which region is forecast to lead growth through 2031?

Asia-Pacific posts the fastest 7.79% CAGR thanks to robust manufacturing output and progressive environmental rules in markets such as Japan and South Korea.

Why do brand owners prefer mono-material packaging?

Using paper across primary, secondary, and tertiary layers simplifies recycling, reduces contamination, and eases multi-market compliance.

What technological advance most improves paper wrap performance?

Bio-based barrier coatings increase moisture resistance and stretchability, enabling deployment in humid and cold-chain conditions while remaining recyclable.

How can companies manage higher unit costs during transition?

Volume-guaranteed contracts, dual-material equipment that allows phased changeovers, and participation in EPR fee rebates help offset the premium pricing of paper wraps.

Page last updated on: