Pakistan Data Center Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

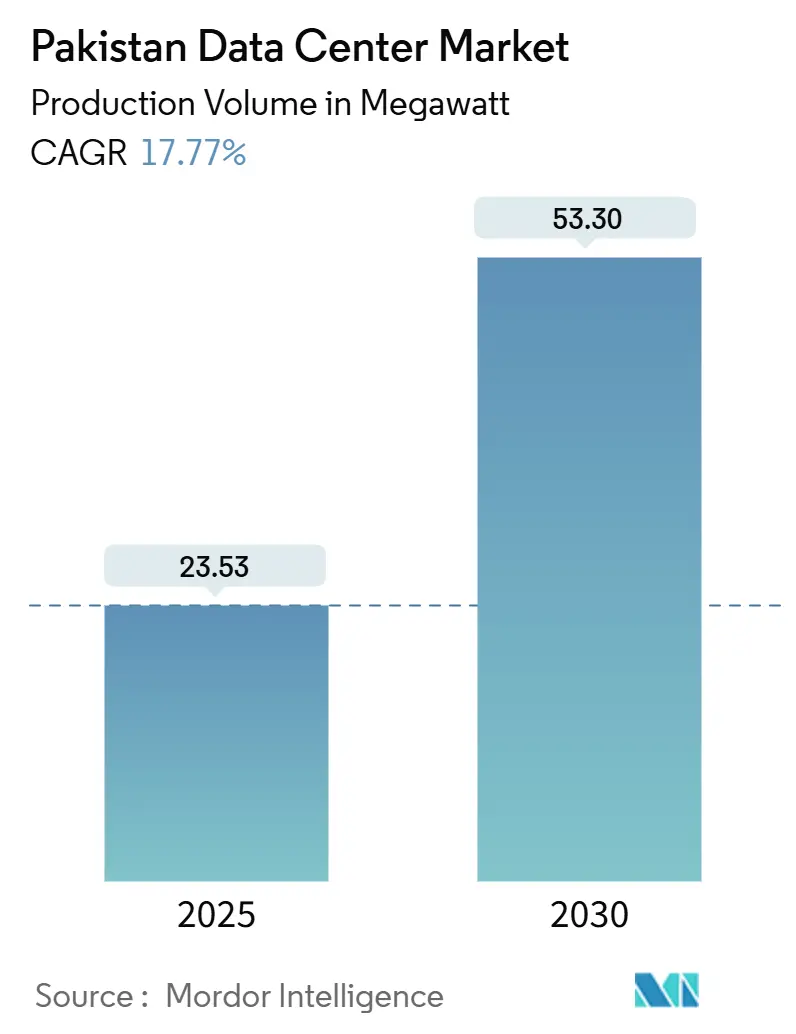

| Market Volume (2025) | 23.53 megawatt |

| Market Volume (2030) | 53.30 megawatt |

| Growth Rate (2025 - 2030) | 17.77% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pakistan Data Center Market Analysis by Mordor Intelligence

The Pakistan data center market size stands at an installed IT load of 23.53 MW in 2025 and is forecast to reach 53.30 MW by 2030, reflecting a 17.77% CAGR. Accelerated cloud adoption under the Digital Pakistan program, a sharp uptick in broadband users, and USD 400 million in foreign direct investment for telecommunications infrastructure are intensifying demand for carrier-neutral facilities. Surplus electricity earmarked for artificial-intelligence workloads, the roll-out of 4G and imminent 5G, and cross-border connectivity delivered by China-Pakistan Economic Corridor (CPEC) fiber routes position the Pakistan data center market for sustained double-digit growth. Heightened enterprise appetite for high-availability environments explains why Tier III facilities command a majority share, while mega-scale builds aimed at hyperscalers signal mounting preference for consolidated capacity. Competitive intensity remains moderate as incumbent telecom operators integrate tower assets, preparing bundled colocation and connectivity offers that lower switching costs for enterprise clients.

Key Report Takeaways

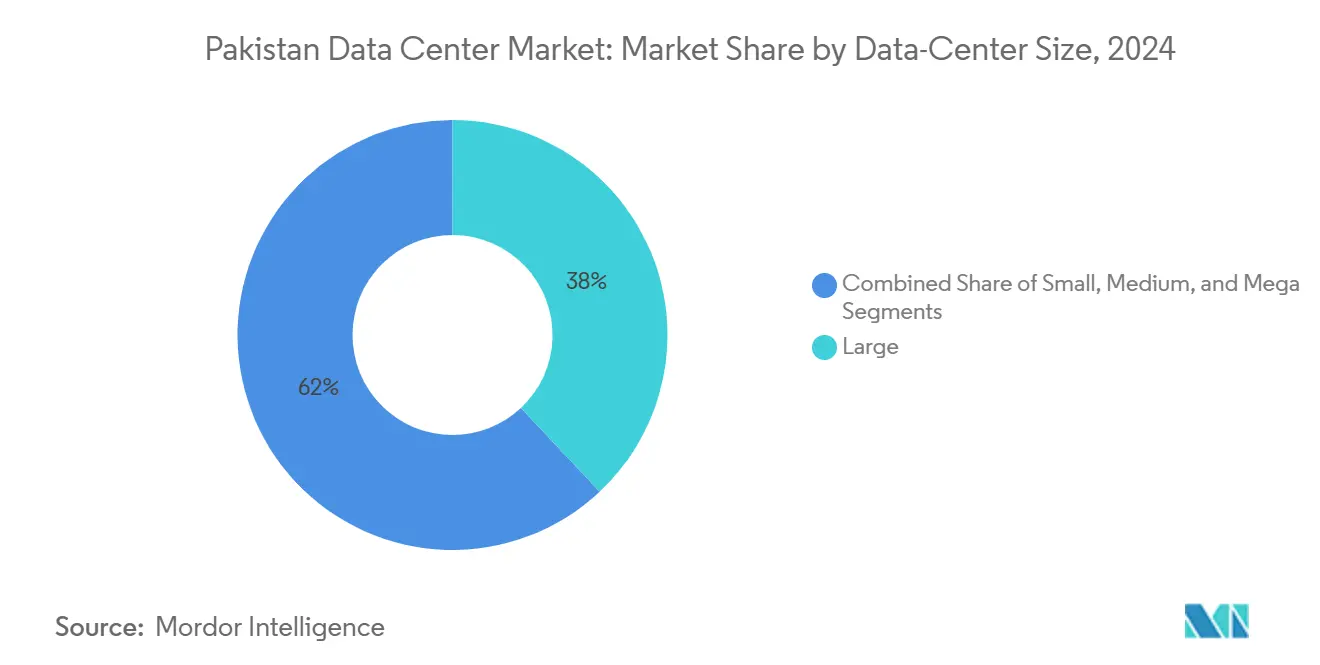

- By data-center size, large facilities led with 38% revenue share in 2024; mega sites are projected to expand at an 18.30% CAGR through 2030.

- By tier standard, Tier III installations accounted for 56% of the Pakistan data center market share in 2024 and Tier IV is advancing at a 16.40% CAGR through 2030.

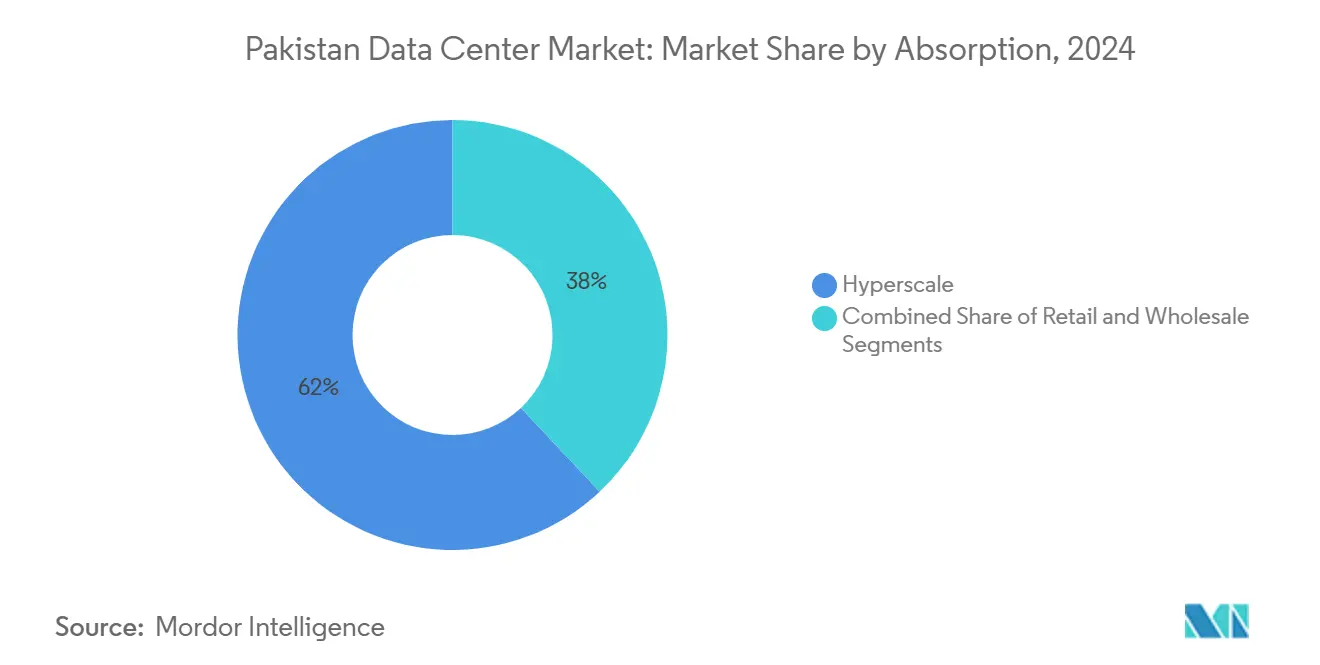

- By absorption, hyperscale colocation represented 62% of the Pakistan data center market size in 2024; cloud service providers record the fastest growth at 17.80% CAGR to 2030.

- By hotspot, Karachi held 49% market share in 2024, while Islamabad/Rawalpindi posts the highest projected CAGR at 18.70% through 2030.

Pakistan Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging mobile-data consumption and 4G/5G roll-out | +3.20% | National, early gains in Karachi, Lahore, Islamabad | Short term (≤ 2 years) |

| Government Digital Pakistan program accelerating cloud adoption | +2.80% | National, concentrated in federal and provincial capitals | Medium term (2-4 years) |

| Rapid e-commerce and fintech growth fueling low-latency demand | +2.10% | Urban centers, spill-over to Tier-2 cities | Medium term (2-4 years) |

| Entry of global cloud providers triggering hyperscale build-outs | +1.90% | Karachi and Islamabad primary, Lahore secondary | Long term (≥ 4 years) |

| CPEC fiber corridors lowering latency and improving dual-grid power | +1.50% | Northern Pakistan, extending to Karachi and Gwadar | Long term (≥ 4 years) |

| Diaspora back-haul OTT traffic localization | +0.80% | Major urban centers with international connectivity | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Digital Pakistan Program Accelerating Cloud Adoption

Federal and provincial ministries are migrating workloads to shared government clouds, driving steady rack take-up across public-sector–dedicated suites. The National Database and Registration Authority’s biometric platforms now process millions of daily transactions from Tier III sites that guarantee 99.982% availability. The National Data Center offers SaaS, PaaS, and IaaS for more than 100 agencies, compressing procurement cycles and encouraging a cloud-first mindset. Central bank rules for digital banking have spurred crypto custody and real-time payments engines hosted in Karachi and Islamabad facilities, pushing resilient power and connectivity requirements higher. Provincial initiatives such as Punjab Information Technology Board’s hyper-converged deployments underscore how devolved administrations now embed private-cloud capacity into citizen-service roll-outs. Together these moves translate into reserved power blocks that anchor multi-megawatt expansions across capital regions.

Entry of Global Cloud Providers Triggering Hyperscale Build-outs

International providers view Pakistan’s maturing internet backbone and low-cost land parcels as an opportunity to optimize South Asian latency budgets. A USD 544 million hyperscale agreement between Microsoft and regional carrier du highlights the scale of forthcoming single-tenant builds. Islamabad has reserved 2,000 MW of surplus generation explicitly for AI clusters, insulating power-hungry graphics-processing units from grid volatility.[1]IFC Press Office, “IFC-Led Consortium to Provide up to USD 400 Million to PTCL,” ifc.org CPEC’s 820-kilometer terrestrial fiber optic cable from Rawalpindi to the Khunjerab Pass offers a redundant reach into Western China, sidestepping Middle East chokepoints. Hyperscalers also value Karachi’s direct landing points on the PEACE and SEA-ME-WE 6 cables, which together exceed 200 Tbps of capacity. These physical underpinnings reduce round-trip times, enabling the meeting of strict service-level objectives for cloud databases and content delivery.

Rapid E-commerce and Fintech Growth Fueling Low-Latency Demand

App downloads reached 3.51 billion in 2023 as marketplace and financial services platforms gained ground among mobile-first consumers.[2]Zeeshan Aftab, “The Future of Digital Transformation,” dawn.com Daraz reports double-digit sales despite macro headwinds, catalyzing demand for sophisticated order-fulfillment algorithms that favor metro-proximate server halls. Major banks, such as Habib, MCB, and UBL, have embedded AI scoring models for credit and fraud detection, generating near-real-time computational bursts. Annual IT exports rose to USD 3 billion, with call-center and business-process-outsourcing clients contracting multi-rack capacity to service North American time zones. Ride-hailing and quick-commerce players deploy micro-edge nodes in Lahore and Faisalabad to shave milliseconds off dispatch applications, ensuring sustained occupancy for Class B facilities outside Tier-1 metros.

CPEC Fiber Corridors Lowering Latency and Improving Dual-Grid Power

The PLA-financed fiber spine now gives Islamabad a second international path, complementing Karachi’s submarine links and enabling path-diverse routing for mission-critical workloads. Phase II extensions toward Gwadar promise express hand-off to Middle-East exchanges without traversing congested Gulf loops. Chinese stake-holders are co-funding power-grid reinforcement, integrating new hydro and solar capacity into national dispatch protocols. Data-center developers capitalize on these projects by tapping dual substations, boosting uptime while trimming diesel-generator runtime. Cumulatively, the corridor positions northern Pakistan as a viable secondary core for cloud footprints serving Afghanistan, western China, and Central Asia.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid unreliability and high electricity tariffs | -2.40% | National, acute in industrial zones | Short term (≤ 2 years) |

| Limited submarine-cable redundancy | -1.60% | Coastal cities, primarily Karachi | Medium term (2-4 years) |

| Geopolitical-risk premiums on insurance and financing | -1.20% | National, affecting foreign investment | Long term (≥ 4 years) |

| Scarcity of certified DC-operations talent outside Tier-1 cities | -0.90% | Secondary cities, rural areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Grid Unreliability and High Electricity Tariffs

Electricity tariffs reached PKR 14.7 per kWh (USD 0.052 per kWh) in July 2022, a 160% year-on-year spike that compressed operator margins.[3].Ali Sarfraz, “Electricity Unit Cost Surge to an All-Time High,” dailypakistan.com.pk The January 2023 nationwide blackout, which affected 220 million residents, highlighted systemic transmission weaknesses, forcing facilities to rely on backup diesel for up to 18 hours. Imported liquefied natural gas generation costs have risen as high as PKR 28.4 per kWh (USD 0.10 per kWh), eroding the price advantage of on-net hosting and shaping pricing for hyperscale leases. With legacy grid hardware dating back to pre-independence, average transmission and distribution losses remain at 14%. Operators respond by installing N+1 gas turbines and lithium-ion battery arrays, but these investments increase build costs by around 20%, extending payback periods beyond seven years.

Scarcity of Certified DC-Operations Talent Outside Tier-1 Cities

Pakistan produces 35,000 IT graduates, against a stated requirement of 100,000 professionals, creating a talent shortfall that is evident in delayed commissioning schedules. Certification gaps are acute; only 42% of data science personnel hold expert-level credentials, and most are concentrated in Karachi, Lahore, or Islamabad. The resulting wage premium exceeds 25% for Uptime-accredited engineers, inflating operating expenses for regional builds. Businesses in smaller cities counteract this by financing graduate programs; Engro, for example, opened a training college in Ghotki District to develop talent pipelines. Without deliberate reskilling efforts, the Pakistan data center industry risks slower deployment timelines in secondary geographies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data-Center Size: Mega facilities drive future growth

Mega campuses account for 18.30% CAGR through 2030 after Jazz inaugurated an USD 8 million Tier III complex in Islamabad that runs high-density AI clusters. Large sites still delivered 38% revenue during 2024 because enterprises prize single-location deployments that flatten operational overheads. Medium builds cater to provincial agencies mandating sovereign-data residency within city limits, while small footprints serve edge cases such as streaming caches in university towns. The Pakistan data center market size for mega builds is projected to surpass 15 MW by 2028, reflecting hyperscale reservations lodged under multiyear take-or-pay contracts.

Consolidation within large sites unlocks operating-expense synergies near 15% via centralized chillers and bulk power tariffs. Mega blueprints also incorporate sustainability features like closed-loop water systems suited to Islamabad’s drier climate. As GPU utilization rates climb, rack power densities above 40 kW become standard, making legacy rooms uneconomical. Over the forecast horizon, mega campuses will house regional disaster-recovery footprints for GCC banks seeking Sharia-compliant jurisdictions, reinforcing their outsized influence on the Pakistan data center market.

By Tier Standard: Enterprise demand elevates Tier IV adoption

Tier III still dominated with 56% share in 2024 because it balances availability with capital efficiency. Financial regulators and telcos equate Tier III with regulatory compliance, hence the steady pipeline of upgrades in Karachi. Yet Tier IV footprints will grow 16.40% CAGR to 2030 as central-bank clearing houses and emergency-response networks stipulate zero single-points-of-failure. The Pakistan data center market share for Tier IV is expected to climb above 12% by 2030 on the back of mission-critical banking and defense projects.

Incremental cost deltas of 20% for Tier IV are offset by insurance discounts that shave 10 basis points from annual premiums. Operators reconcile upfront capex by layering value-added services such as sovereign-cloud enclaves. Tier I and II rooms persist for dev-test workloads but face obsolescence as power-cost headwinds favor higher-efficiency modern builds. The evolving mix reaffirms how resilience mandates now influence real-estate selection and backend-grid design across the Pakistan data center market.

By Absorption: Cloud providers reshape utilization patterns

Hyperscale tenants occupied 62% of booked white space in 2024, validating the swing toward single-tenant pods that guarantee differentiated power quality. Cloud service providers alone post 17.80% CAGR to 2030, overtaking BFSI as the largest user cohort by 2027. The Pakistan data center market size for cloud workloads reached 14 MW in 2024 and is forecast to double by 2028 alongside sovereign-cloud pilot roll-outs.

BFSI retains significant dedicated suites because domestic banks must archive high-frequency trading logs for seven years under State Bank directives. E-commerce and media platforms secure contiguous cages within retail colocation halls to scale seasonally. Manufacturing and energy companies contract wholesale modules close to refinery zones, leveraging private-line circuits for industrial IoT feeds. This mixed tenancy keeps revenue yields resilient, even as hyperscale rate cards drive unit-pricing down across the Pakistan data center market.

By Hotspot: Islamabad emerges as growth leader

Karachi preserved 49% share in 2024, supported by four submarine landings and entrenched financial-services hubs. However, the Pakistan data center market size pipeline in Islamabad accelerates at 18.70% CAGR because federal projects aggregate here and fiber-optic extensions shorten backhaul paths. The capital region’s share could climb to 30% by 2030 as new zones become operational.

Islamabad offers milder ambient temperatures that reduce chiller loads by up to 7% relative to Karachi, an advantage in power-pricing negotiations. Proximity to the CPEC route enables dual-homed fiber entries, a prerequisite for Tier IV certifications. Lahore plays a bridging role for Punjab’s manufacturing belt, leveraging the University of Lahore’s pioneering Tier III facility as an anchor tenant. Beyond these hubs, emerging cities such as Faisalabad and Peshawar begin to attract edge deployments that cache popular content, ensuring broad geographic dispersion across the Pakistan data center market.

Geography Analysis

Karachi anchors the network core, holding 49% of installed IT load in 2024 as well as direct access to PEACE and SEA-ME-WE 6 cable systems that together supply more than 200 Tbps external bandwidth. PTCL’s Tier III campus hosts primary transaction engines for United Bank Limited and the State Bank of Pakistan, proof that stringent uptime requirements push financial-services workloads toward the port city. Yet expansion faces land-use and grid-capacity constraints that prolong permitting cycles and elevate rental premiums.

Islamabad/Rawalpindi records the fastest growth trajectory at 18.70% CAGR to 2030, fueled by Jazz’s Tier III Digital Park and the National Data Center serving over 100 ministries. CPEC fiber endpoints give the twin cities latency advantage to western China, while the country’s first Internet Exchange Point trims domestic round-trip times. Government cloud adoption triggers sustained rack take-up and incentivizes domestic SaaS vendors to co-locate within the capital.

Lahore, Faisalabad, and emerging cities collectively contribute 19% of national load in 2024. Lahore’s University-led Tier III hall catalyzes academic-industry research clusters. Meanwhile, Punjab Information Technology Board’s hyper-converged stack enhances e-governance while seeding demand for backup-as-a-service. Gwadar’s development as a free-trade port under CPEC stimulates feasibility studies for micro-data centers to serve Middle-Eastern content exchanges within 30 milliseconds round-trip. Collectively, these regional vectors underscore how the Pakistan data center market continues to diversify away from a single-city footprint.

Competitive Landscape

The Pakistan data center market remains moderately concentrated as incumbent telecom carriers capitalize on tower footprints and long-haul fiber to integrate colocation offerings. PTCL’s USD 400 million acquisition of Telenor Pakistan consolidated control over 22,000 towers, enabling bundled dark-fiber and edge-compute products that lower provisioning lead times. Jazz channels capital into a Tier III Digital Park that already secures anchor tenants across BFSI and government verticals. Competitive dynamics center on differentiated power resilience and cross-connect richness rather than price wars.

Smaller players position on specialized services. WorldCall operates an AI and Big-Data Center of Excellence tapping proprietary GPU clusters for financial-risk analytics. Mari Petroleum leverages upstream gas assets to guarantee captive power for planned edge sites in oil-field provinces, converting energy expertise into data-center reliability. International cloud providers negotiate build-operate-transfer contracts with domestic real-estate groups, signaling entry paths that circumvent local licensing hurdles.

Price competition is tempered by high entry capex and scarcity of Uptime-accredited staff. As hyperscale commitments accumulate, operators sign 15-year energy deals indexed to inflation, shielding them from tariff volatility. Those dynamics suggest a gradual tilt toward oligopolistic structures, yet niche licensees retain room to innovate where incumbents shy away from low-density rural markets. Consequently the Pakistan data center market balances scale economies with specialty niches, producing a competition profile that remains stable yet responsive to vertical-specific demands.

Pakistan Data Center Industry Leaders

Multinet Pakistan

Pakistan Telecommunication Company Limited (PTCL)

Supernet Limited

Cybernet (RapidCompute)

Wateen Telecom

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Pakistan Telecommunication Authority released 5G auction timetable targeting commercial launch in June 2025, a move expected to heighten bandwidth demand nationwide.

- January 2025: WorldCall Telecom opened its Center of Excellence for AI and Big Data, reinforcing high-performance compute needs.

- September 2024: IFC-led consortium extended USD 400 million to PTCL for the acquisition of Telenor Pakistan and Orion Towers.

- September 2024: Mari Petroleum disclosed plans to develop data centers leveraging internal power assets.

- April 2024: sAi Capital invested in wAI Industries to accelerate proprietary AI model development hosted in local data centers.

Pakistan Data Center Market Report Scope

| Small |

| Medium |

| Large |

| Mega |

| Massive |

| Tier I-II |

| Tier III |

| Tier IV |

| Non-Utilized | ||

| Utilized | By Colocation Type | Hyperscale |

| Retail | ||

| Wholesale | ||

| By End-User | BFSI | |

| Cloud Service Providers | ||

| E-Commerce | ||

| Government | ||

| Manufacturing | ||

| Media and Entertainment | ||

| Telecom | ||

| Other End-Users | ||

| Karachi |

| Lahore |

| Rest of Pakistan |

| By Data-Center Size | Small | ||

| Medium | |||

| Large | |||

| Mega | |||

| Massive | |||

| By Tier Standard | Tier I-II | ||

| Tier III | |||

| Tier IV | |||

| By Absorption | Non-Utilized | ||

| Utilized | By Colocation Type | Hyperscale | |

| Retail | |||

| Wholesale | |||

| By End-User | BFSI | ||

| Cloud Service Providers | |||

| E-Commerce | |||

| Government | |||

| Manufacturing | |||

| Media and Entertainment | |||

| Telecom | |||

| Other End-Users | |||

| By Hotspot | Karachi | ||

| Lahore | |||

| Rest of Pakistan | |||

Key Questions Answered in the Report

How fast is data-center power demand growing in Pakistan?

Installed IT load is projected to rise from 23.53 MW in 2025 to 53.30 MW by 2030, equal to a 17.77% CAGR.

What role does the Digital Pakistan agenda play in capacity growth?

Government cloud mandates and e-services roll-outs are anchoring multi-megawatt reservations in Islamabad and provincial capitals, accelerating utilization.

Which city is emerging as the second hub after Karachi?

Islamabad/Rawalpindi posts the fastest growth at 18.70% CAGR as federal workloads and CPEC fiber endpoints converge in the capital.

Why are hyperscale operators interested in Pakistan?

Dedicated 2,000 MW surplus power, redundant CPEC fiber routes, and favorable land costs make Pakistan a strategic choice for serving South Asia.

What is the biggest operational challenge for facility developers?

Grid instability coupled with high electricity tariffs raises operating costs and necessitates significant investment in redundant power systems.

How concentrated is the competitive landscape?

The five largest providers control roughly 65% of capacity, reflecting moderate concentration that favors large incumbents yet leaves space for specialized entrants.

Page last updated on: