Pain Relief Patches Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

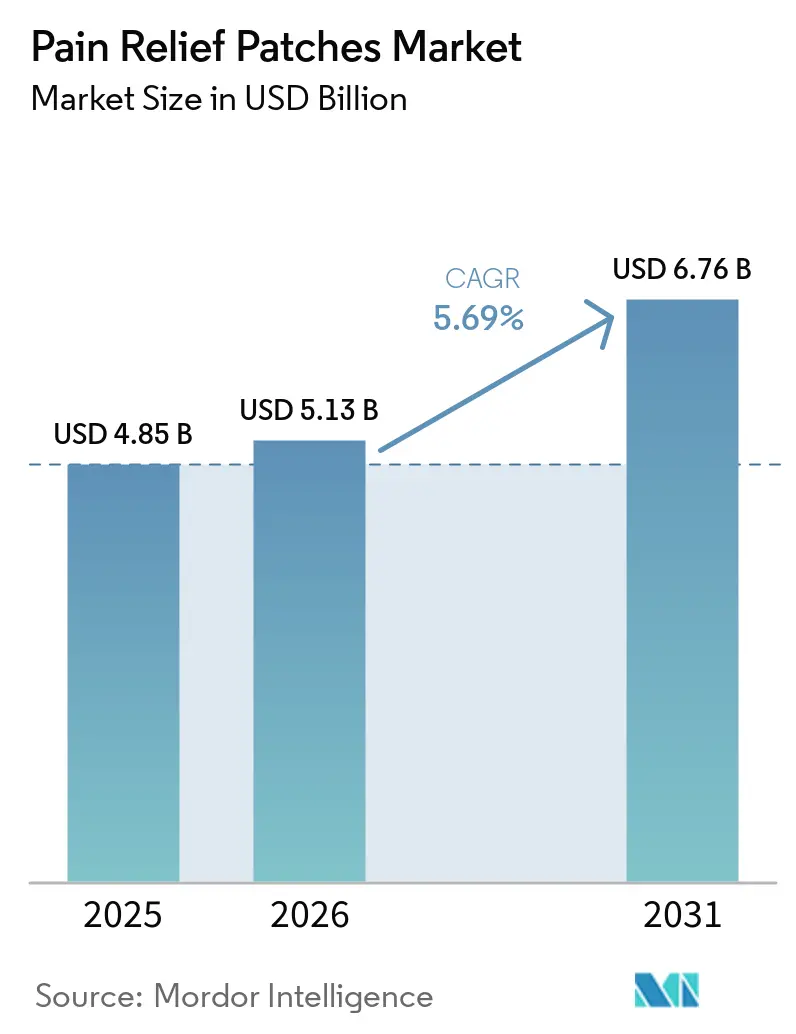

| Market Size (2026) | USD 5.13 Billion |

| Market Size (2031) | USD 6.76 Billion |

| Growth Rate (2026 - 2031) | 5.69% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pain Relief Patches Market Analysis by Mordor Intelligence

The Pain Relief Patches Market size is projected to expand from USD 4.85 billion in 2025 and USD 5.13 billion in 2026 to USD 6.76 billion by 2031, registering a CAGR of 5.69% between 2026 to 2031.

The expansion highlights a significant shift in pain management, emphasizing localized and sustained transdermal delivery methods. These approaches reduce systemic exposure and decrease reliance on oral medications. Regulatory updates in 2025 adopted a stricter stance on opioid risks, driving clinicians and payers to prioritize non-opioid alternatives for managing chronic musculoskeletal and neuropathic pain. Aging populations are influencing treatment strategies, increasing the need for solutions that maintain consistent plasma levels and minimize drug-drug interactions. Manufacturers are responding by offering bulk formats and packaging designed for mail delivery, aiming to improve patient adherence and convenience. Additionally, stricter quality and safety standards are favoring established suppliers with strong manufacturing capabilities and effective post-market surveillance systems.

Key Report Takeaways

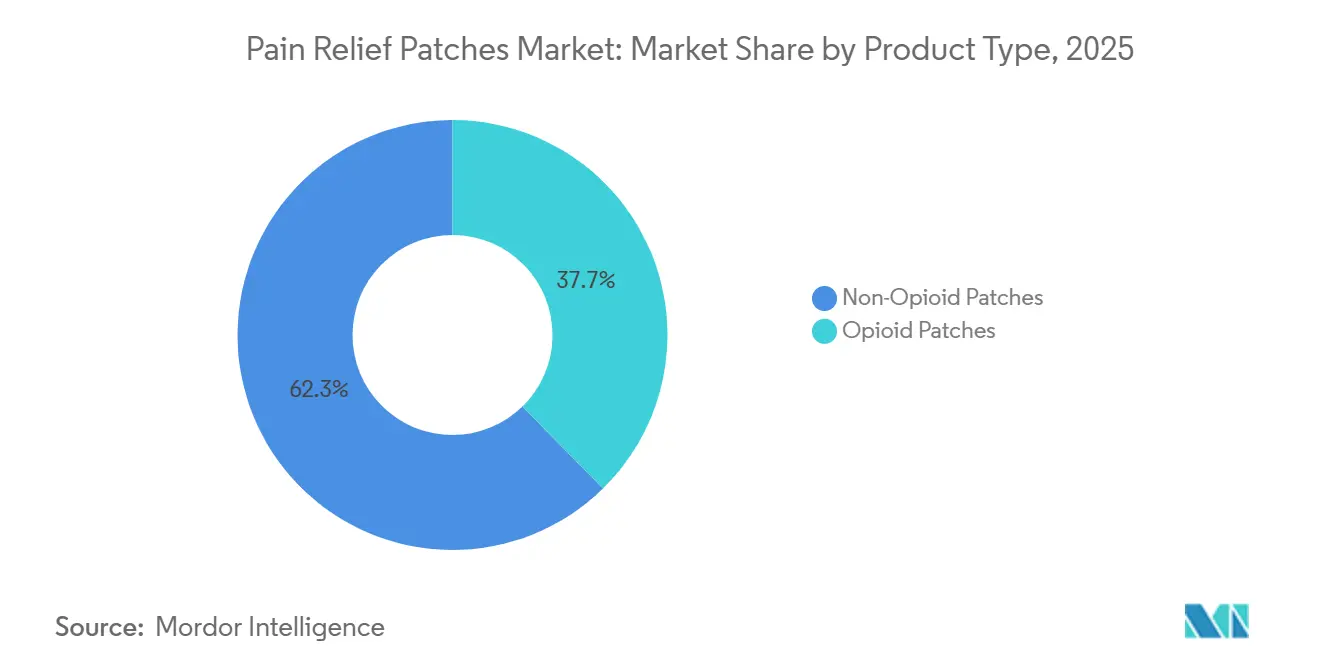

- By product type, non-opioid patches accounted for 62.34% of revenue in 2025, and they are projected to grow at 8.10% annually through 2031, outpacing opioid-based systems.

- By application, chronic pain held 44.23% share in 2025, while sports and injury-related pain is on track for the fastest expansion at 7.60% CAGR through 2031.

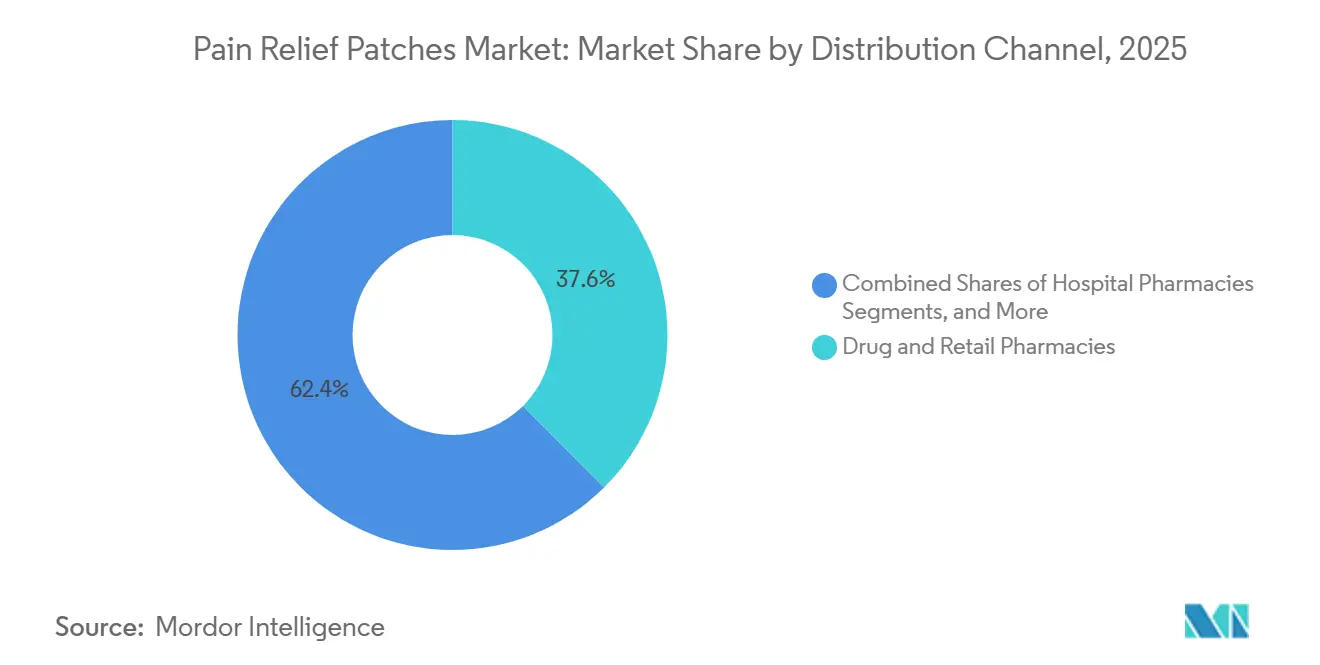

- By distribution channel, drug and retail pharmacies represented 37.56% share in 2025, and online providers are scaling at a 9.40% CAGR through 2031.

- By end user, hospitals held 41.54% share in 2025, whereas home-care settings are projected to advance at an 8.80% CAGR through 2031.

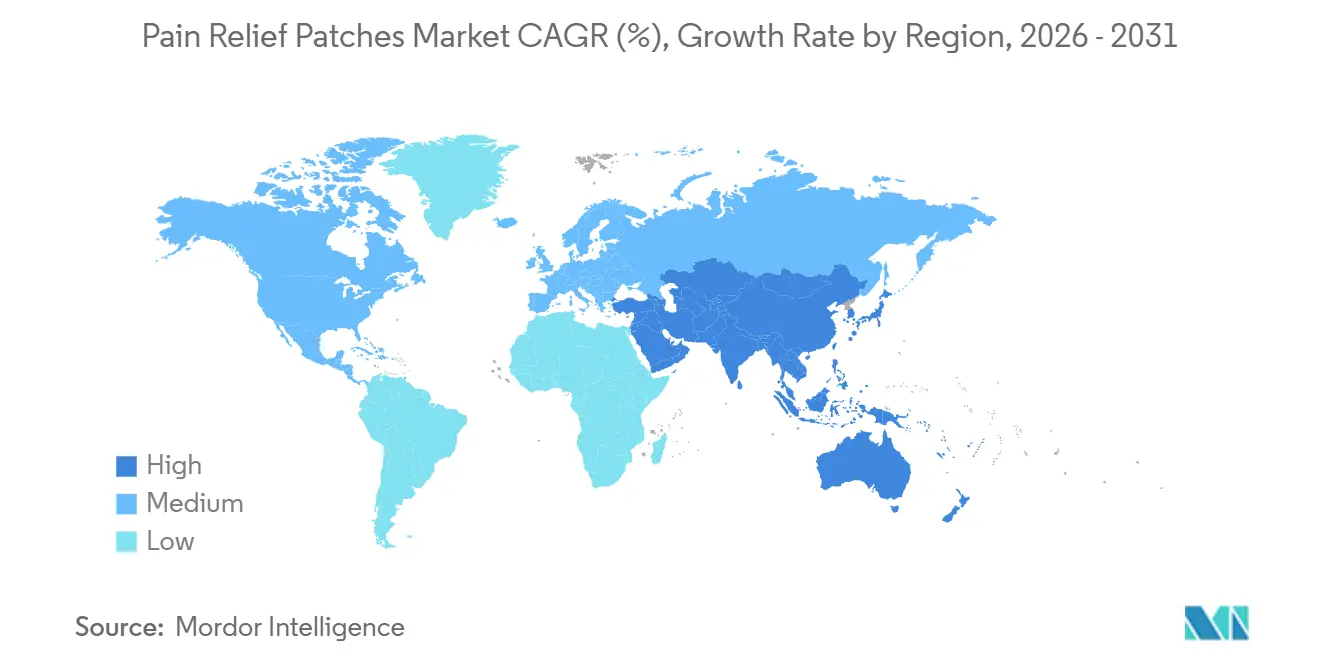

- By geography, North America contributed 39.67% of revenue in 2025, and Asia-Pacific is the fastest-growing region at an 8.50% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Pain Relief Patches Market Trends and Insights

Driver Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Accelerated OTC adoption in retail & e-commerce channels | +1.2% | Global, with early gains in North America, Japan, India | Short term (≤ 2 years) |

| Aging population driving chronic pain prevalence | +1.5% | Global, concentrated in North America, Europe, Asia-Pacific (Japan, China) | Long term (≥ 4 years) |

| Regulatory push away from systemic opioids | +0.9% | North America & Europe | Medium term (2-4 years) |

| Technological advances in drug-in-adhesive & microneedle patches | +0.8% | Global, R&D hubs in North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Smart patch R&D linking sensors with companion apps | +0.4% | North America, Europe, Asia-Pacific (China, South Korea) | Long term (≥ 4 years) |

| ESG-driven shift to bio-degradable patch substrates | +0.3% | Europe, North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated OTC Adoption in Retail & E-Commerce Channels

Over-the-counter transdermal products are increasingly moving from pharmacy shelves to digital marketplaces, streamlining the purchasing process and enabling larger unit sizes that improve cost efficiency for frequent users. Hisamitsu has introduced bulk-format e-commerce options designed to fit standard mailboxes, enhancing convenience for chronic users while reducing delivery-related emissions. The shift to online channels is also expanding access to specialty formats, as seen with Sonoma Pharmaceuticals’ launch of a burn-relief hydrogel patch in major U.S. retail chains. Larger pack sizes in e-commerce provide manufacturers with greater pricing flexibility and support subscription models that encourage adherence for long-term conditions. Updated U.S. quality standards for transdermal systems emphasize adhesion and dose consistency, favoring established players while supporting OTC market growth. These factors collectively strengthen the role of e-commerce and national retail in the pain relief patches market, driven by consumer demand for speed, convenience, and trusted brands.

Aging Population Driving Chronic Pain Prevalence

The aging global population is driving demand for localized, sustained pain relief solutions that minimize systemic exposure. By 2030, one-sixth of the global population is expected to be 60 or older, correlating with a rise in chronic musculoskeletal conditions requiring long-term pain management.[1]American Geriatrics Society, “2023 AGS Beers Criteria,” American Geriatrics Society, americangeriatrics.org In the U.S., chronic pain affects nearly a quarter of adults, with higher prevalence among older age groups. Guidelines caution against certain oral medications for seniors, increasing reliance on topical formulations like lidocaine, diclofenac, and capsaicin. Studies highlight the persistence of pain in older adults, emphasizing the need for personalized and multimodal approaches, including transdermal options. These trends sustain demand for pain relief patches as healthcare providers prioritize consistent treatment outcomes and reduced medication risks for aging patients.

Regulatory Push Away from Systemic Opioids

Regulatory measures are shifting focus from opioid patches to non-opioid alternatives for managing chronic pain. Updated labeling and stricter surveillance requirements highlight the long-term risks of opioid use, prompting a reevaluation of treatment protocols. European regulators have reinforced patient monitoring and risk management for fentanyl systems, while safety standards for skin-contacting devices ensure compliance with biocompatibility requirements. Although opioid patches remain essential in severe cases, the regulatory environment is encouraging broader adoption of non-opioid options. This shift is influencing prescribing practices and insurance policies, increasing the share of non-opioid products in the pain relief patches market.

Technological Advances in Drug-in-Adhesive & Microneedle Patches

Innovations in drug-in-adhesive designs have simplified product architecture and improved user comfort compared to traditional reservoir models. Recent studies demonstrate the effectiveness of these patches in delivering therapeutic levels of anti-inflammatory agents over extended periods. Multi-drug matrices are also emerging, enabling the delivery of multiple active ingredients through a single adhesive layer, expanding possibilities for integrated pain and symptom management. Progress in dissolving microneedle platforms shows promise for self-administered, painless solutions with bioavailability comparable to injections. These advancements enhance product diversity and patient compatibility, driving adherence and continuity in long-term pain management.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Skin-irritation & adhesion failures | -0.6% | Global | Short term (≤ 2 years) |

| Stringent FDA / EMA clinical-trial cost & timeline | -0.5% | North America & Europe | Medium term (2-4 years) |

| Disposal-related environmental scrutiny | -0.3% | Europe, North America | Medium term (2-4 years) |

| Counterfeit patches in low-regulation e-commerce | -0.4% | Global, concentrated in Asia-Pacific, Latin America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Skin-Irritation & Adhesion Failures

Dermal reactions and adhesion issues are key factors driving product discontinuation, with recalls underscoring the consequences of inadequate adhesion or release performance in practical use. In early 2025, specific fentanyl transdermal lots were recalled due to adhesion failures, which posed risks of residual drug exposure to caregivers and household members.[2]Alvogen, “Fentanyl Transdermal Patch Recall Notice,” Alvogen, alvogen.com Compliance issues identified in late 2024 highlighted the critical need for stringent adhesion testing protocols and batch-release controls for topical analgesics. Reports of adverse events, such as local skin reactions and contact dermatitis from OTC lidocaine products, have intensified the focus on hypoallergenic adhesives and consistent adhesion across various skin types. Manufacturers are increasingly adopting silicone- and hydrocolloid-based adhesive systems to balance tack and breathability, reducing irritation risks. Enhanced market surveillance and updated labeling practices aim to minimize discontinuities and recalls, supporting growth in the pain relief patches market.

Stringent FDA / EMA Clinical-Trial Cost & Timeline

Transdermal patches, categorized as combination products, must comply with both drug and device regulatory standards during development. Bioequivalence requirements for transdermals demand precise control of plasma profiles across application sites and populations, adding complexity to study designs compared to oral generics. Updated U.S. guidelines in 2025 emphasized the importance of in vitro release, adhesion standards, and stability under temperature variations, extending development timelines.[3]U.S. Food and Drug Administration, “MAUDE Adverse Event Reporting for Transdermal Patches,” U.S. Food and Drug Administration, fda.gov European regulators maintain strict oversight of high-potency transdermals, requiring comprehensive risk-management plans to ensure patient safety. These stringent requirements increase resource demands, particularly for smaller developers, driving a focus on lifecycle extensions and OTC innovations. While these measures enhance product reliability, they may slow the pace of new product launches in the pain relief patches market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Non-Opioid Formulations Lead Growth

In 2025, non-opioid patches captured 62.34% of the pain relief patches market, with an expected CAGR of 8.10% through 2031, driven by a shift from opioid-based treatments for chronic non-cancer pain. The market is supported by labeling changes and safety advisories encouraging non-opioid options, particularly for older patients with polypharmacy and comorbidities. Manufacturers are innovating drug-in-adhesive platforms to deliver thin, comfortable patches with consistent release over 12-to-24-hour windows, enhancing adherence and reducing the need for rescue medication. The industry is expanding non-opioid formulations and sizes to cater to diverse needs, supported by flexible packaging and long-wear designs that improve therapy persistence.

By Application: Chronic Pain Dominates, Sports Injury Accelerates

Chronic pain applications accounted for 44.23% of the market in 2025, driven by sustained-release delivery that stabilizes symptoms in conditions like osteoarthritis, lower back pain, and neuropathy. Clinical guidelines favor topical solutions for older adults, reducing risks associated with oral medications. Long-wear patches that enable daily activities while minimizing oral dosing are in demand, supported by improved adhesion and comfort in non-opioid designs, ensuring consistent relief and reducing variability.

Sports-related pain is the fastest-growing segment, with a projected CAGR of 7.60% through 2031, fueled by self-care trends, online availability, and localized delivery benefits during training or recovery. Patches applied directly to muscles or joints allow activity without frequent dosing interruptions. OTC formats with menthol, methyl salicylate, or lidocaine maintain strong retail presence, supported by subscription and multi-pack offers catering to training schedules, sustaining growth in this segment.

By Distribution Channel: Online Providers Surge

Drug and retail pharmacies held 37.56% of the market in 2025, reflecting established OTC behaviors and the convenience of in-person pickups for acute needs. Pharmacies play a key role in guiding product selection based on age, comorbidities, and medication profiles, ensuring adherence and promoting safe usage. However, economic constraints and shelf limitations restrict larger pack sizes in physical stores.

Online providers are growing at a 9.40% CAGR through 2031, driven by subscription services, flexible pack sizes, and bulk packaging that reduce logistics costs and streamline replenishment for chronic users. Direct-to-consumer programs educate users on application techniques and skincare, minimizing irritation and patch lift. National retail outlets also support the launch of specialized OTC patches, balancing immediate availability with convenient auto-ship models to ensure consistent supply.

By End User: Home-Care Settings Gain Share

Hospitals accounted for 41.54% of the market in 2025, driven by transdermal systems used in procedural and post-acute pain management. Hospital formularies evaluate labeling updates and quality benchmarks to standardize selections that align with discharge plans and caregiver capabilities. Safety standards for prolonged skin contact influence material choices, while the recovery of elective procedures and growth of ambulatory centers maintain hospital demand for prescription transdermals.

Home-care settings are projected to grow at an 8.80% CAGR through 2031, supported by transdermal patches that integrate into self-care routines for localized pain. The industry is introducing user-friendly formats with clear instructions, catering to older adults and caregivers. E-commerce and subscription services ensure routine replenishment, reducing usage lapses and stabilizing symptoms in chronic conditions. Transdermal patches align with self-management strategies, minimizing clinic visits and supporting virtual follow-ups.

Geography Analysis

In 2025, North America captured 39.67% of the pain relief patches market share, while Asia-Pacific emerged as the fastest-growing region with an 8.50% CAGR projected through 2031. In the United States, updated opioid patch labeling in 2025 encouraged a shift toward topical non-opioid analgesics for chronic non-cancer pain. The high prevalence of chronic pain among U.S. adults drives demand for long-wear patches that support daily functionality. Specialty patches remain critical for oncology and palliative care, addressing cases requiring consistent and strong analgesia.

In Europe, the pain relief patches market reflects stringent benefit-risk management by regulators and a growing focus on sustainable packaging and materials. Safety updates for high-potency transdermals in 2024 refined patient selection and risk mitigation practices. Environmental concerns are driving interest in recyclable or biodegradable materials, while product safety adheres to established biocompatibility standards. National initiatives are exploring producer responsibility programs to address healthcare waste. OTC and non-opioid patches are gaining traction in pharmacies and online platforms, supported by larger pack options and educational content.

Asia-Pacific, the fastest-growing region, benefits from rising incomes, aging demographics in countries like Japan, and improvements in retail and digital pharmacy reach. The market is projected to grow at an 8.50% CAGR through 2031, supported by strong brand presence and consumer familiarity with topical solutions. Companies like Hisamitsu leverage innovative product designs and e-commerce strategies, offering thin, mailbox-compatible packs for reliable delivery and repeat usage. Expanding healthcare access and self-care categories align with consumer preferences for targeted relief with minimal disruption to daily routines.

Competitive Landscape

The pain relief patches market is moderately fragmented, with multinational pharmaceutical companies dominating the prescription segment and specialized OTC brands competing in high-volume categories. Prescription opioid and high-potency non-opioid patches remain critical for strong and sustained pain relief, though chronic non-cancer pain management is increasingly favoring non-opioid alternatives. OTC topical analgesics are expanding through broader retail availability and e-commerce subscriptions, benefiting brands that deliver superior adhesion, comfort, and consistent dosing. Companies with advanced quality systems and surveillance capabilities maintain a competitive edge as the market demands higher standards in adhesion and release profiles. Suppliers are innovating by diversifying formats and sizes to address varying use durations and body sites.

Strategic initiatives are reshaping market positions and channel reach. Hisamitsu introduced large-count e-commerce packs designed for efficient logistics and bulk purchasing to support chronic use adherence. Sonoma Pharmaceuticals expanded its product range by securing national retail distribution for a burn-relief hydrogel patch, extending its reach beyond musculoskeletal pain to minor burn care. Grünenthal licensed Canadian rights for its high-concentration capsaicin patch, Qutenza, to Apotex’s Searchlight Pharma unit, showcasing a targeted market-access strategy. Technological advancements, including drug-in-adhesive systems, multi-drug matrices, and dissolving microneedle platforms, are gaining traction as self-administered, painless solutions. Compliance differentiation is becoming critical as regulatory standards for biocompatibility and dose validation tighten.

Pain Relief Patches Industry Leaders

Hisamitsu Pharmaceutical Co., Inc.

Johnson & Johnson (Janssen)

Teva Pharmaceutical Industries Ltd.

Viatris Inc.

Endo International plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: The U.S. International Trade Commission opened an investigation into unlicensed OTC lidocaine patches sold by J.A.R. Laboratories and other entities, alleging trademark infringement against Hisamitsu, Perrigo, and Chattem.

- March 2026: Sonoma Pharmaceuticals launched a burn-relief hydrogel patch at CVS and Walmart, securing national retail distribution for a specialty formulation positioned as a self-care solution.

- February 2025: Grünenthal licensed exclusive Canadian rights to Qutenza to Apotex’s Searchlight Pharma division and announced a plan to pursue Canadian marketing authorization with milestone and royalty terms.

- February 2025: Alvogen recalled fentanyl transdermal patches after reports of adhesion failures that could leave residual drug exposed, prompting heightened scrutiny of adhesive testing protocols.

Global Pain Relief Patches Market Report Scope

As per the scope of the report, A pain relief patch is a topical, adhesive patch applied directly to the skin to deliver medication such as lidocaine, NSAIDs, or menthol directly to a localized area of discomfort, offering targeted, long-lasting relief without digestive side effects. They are commonly used for muscle soreness, joint pain, strains, sprains, or arthritis.

The pain relief patches market is segmented into, by product type, application, distribution channel, end user, and geography. By product type, the market is segmented into opioid patches and non-opioid patches. By application, the market is segmented into chronic pain, acute pain, post-operative pain, and sports & injury-related pain. By distribution channel, the market is segmented into hospital pharmacies, drug & retail pharmacies, and online providers. By end user, the market is segmented into hospitals, home-care settings, and clinics & rehabilitation centers. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers estimated market sizes and trends for 17 countries across major regions worldwide. The report offers market size and forecasts in value (USD) for the above segments.

| Opioid Patches |

| Non-Opioid Patches |

| Chronic Pain |

| Acute Pain |

| Post-Operative Pain |

| Sports & Injury-Related Pain |

| Hospital Pharmacies |

| Drug & Retail Pharmacies |

| Online Providers |

| Hospitals |

| Home-Care Settings |

| Clinics & Rehabilitation Centres |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Opioid Patches | |

| Non-Opioid Patches | ||

| By Application | Chronic Pain | |

| Acute Pain | ||

| Post-Operative Pain | ||

| Sports & Injury-Related Pain | ||

| By Distribution Channel | Hospital Pharmacies | |

| Drug & Retail Pharmacies | ||

| Online Providers | ||

| By End User | Hospitals | |

| Home-Care Settings | ||

| Clinics & Rehabilitation Centres | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the growth outlook for the pain relief patches market through 2031

The category is projected to grow from USD 5.13 billion in 2026 to USD 6.76 billion by 2031 at a 5.69% CAGR, supported by aging demographics, non-opioid adoption, and multi-channel access.

Which product types are leading and expanding fastest in pain relief patches

Non-opioid patches led in 2025 with 62.34% share and are projected to grow at 8.10% annually through 2031, outpacing opioid-based systems.

Which applications are most important for pain relief patches today

Chronic pain accounted for 44.23% share in 2025, while sports and injury-related pain is the fastest-growing indication at a 7.60% CAGR through 2031.

How are distribution channels evolving for transdermal analgesics

Drug and retail pharmacies held 37.56% share in 2025, and online providers are advancing at a 9.40% CAGR as bulk packs and subscriptions improve adherence and convenience.

Which regions will contribute most to future growth

North America held 39.67% of revenue in 2025, and Asia-Pacific is the fastest-growing region at an 8.50% CAGR through 2031 due to demographic and access trends.

What regulatory themes most influence product strategy in this space

Updated opioid labeling, stronger quality guidance for transdermals, and ISO biocompatibility standards shape product design, surveillance, and channel choices across markets.

Page last updated on: