Paclitaxel Injection Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

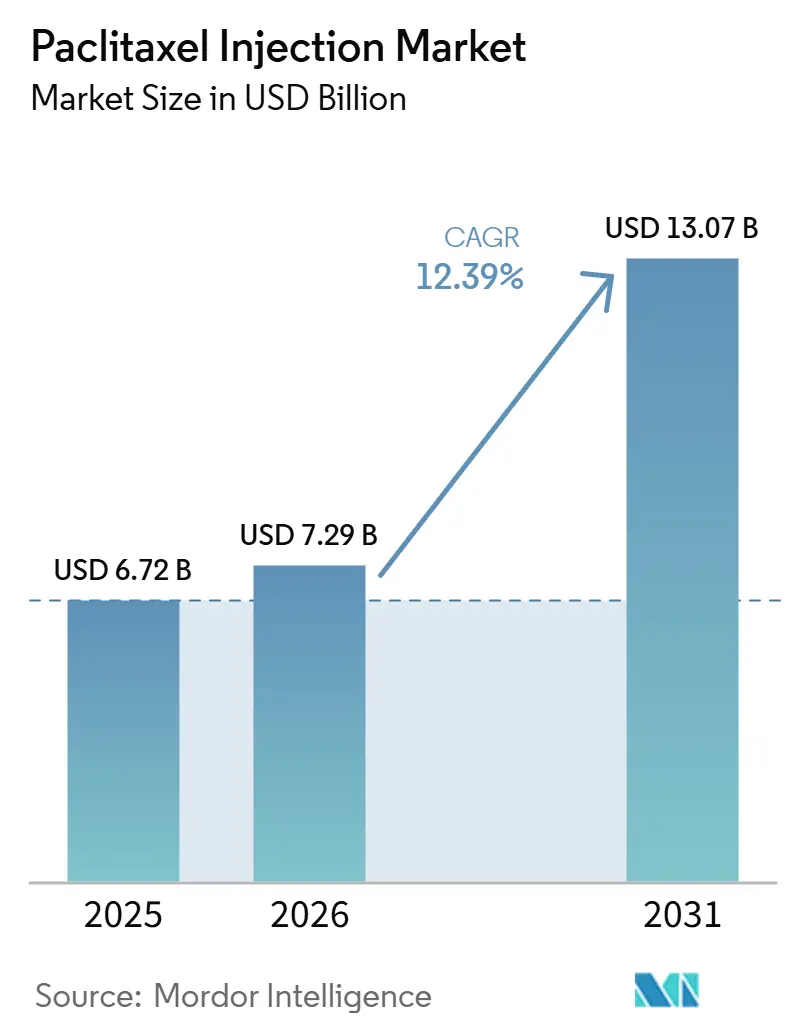

| Market Size (2026) | USD 7.29 Billion |

| Market Size (2031) | USD 13.07 Billion |

| Growth Rate (2026 - 2031) | 12.39% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Paclitaxel Injection Market Analysis by Mordor Intelligence

The Paclitaxel Injection Market size is expected to grow from USD 6.72 billion in 2025 to USD 7.29 billion in 2026 and is forecast to reach USD 13.07 billion by 2031 at 12.39% CAGR over 2026-2031.

The paclitaxel injection market continues to benefit from its multi-indication use across breast, lung, ovarian, and pancreatic cancers, even as antibody-drug conjugates and immuno-oncology regimens narrow frontline chemotherapy use in defined biomarker populations. Regulatory tailwinds are shaping supply and pricing, as the European Medicines Agency’s product-specific bioequivalence guidance for nab-paclitaxel is lowering barriers to multi-country generic entry and harmonizing payer acceptance of substitutable alternatives. Essential-medicine placement on national formularies, such as Zambia’s 2025 Essential Medicines List, signals ongoing institutional procurement priority for paclitaxel, where broad access to targeted therapies remains limited. Expanding generic availability in the United States and European Union is reinforcing supply redundancy and compressing net prices as tender systems adopt multi-winner awards and substitution norms. Rising cancer incidence, particularly in the Asia-Pacific region, sustains demand for chemotherapy backbones where biomarker-directed options are not reimbursed or clinically appropriate.

Key Report Takeaways

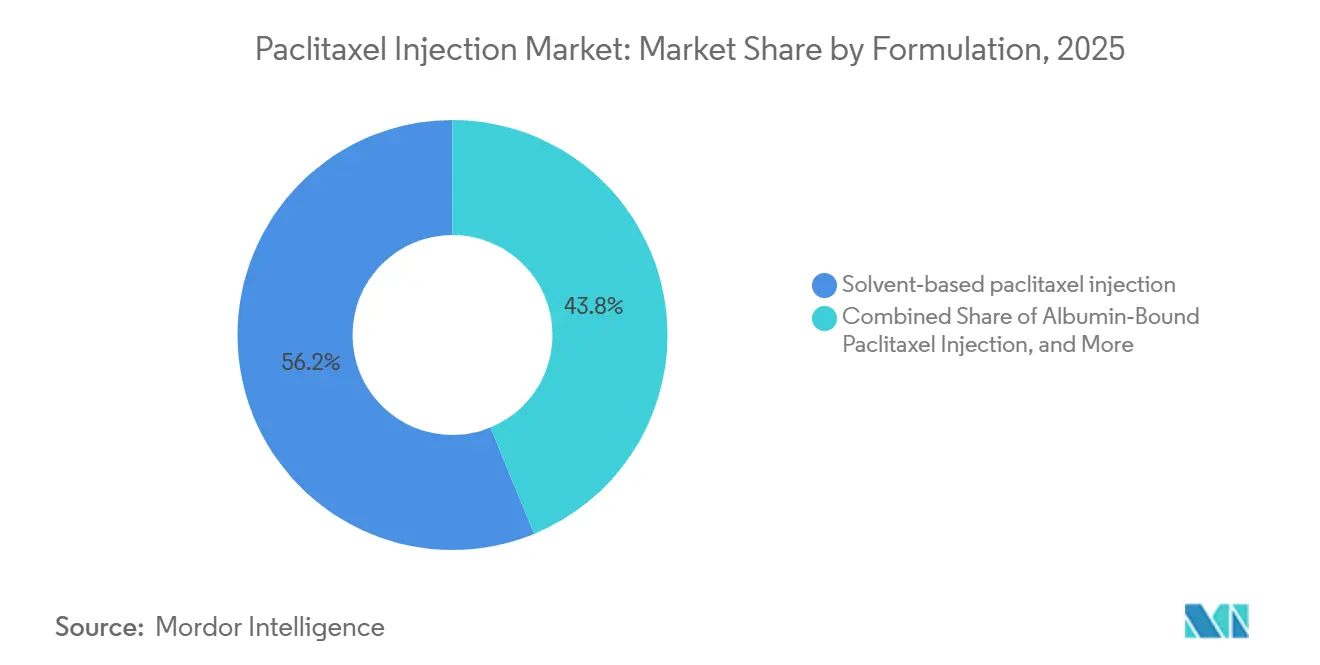

- By formulation, solvent-based paclitaxel led with 56.20% revenue share in 2025, while liposomal and polymeric-micelle variants are projected to expand at a 15.31% CAGR through 2031.

- By indication, breast cancer accounted for 36.50% of 2025 revenues, and pancreatic adenocarcinoma is forecast to grow at a 15.44% CAGR to 2031.

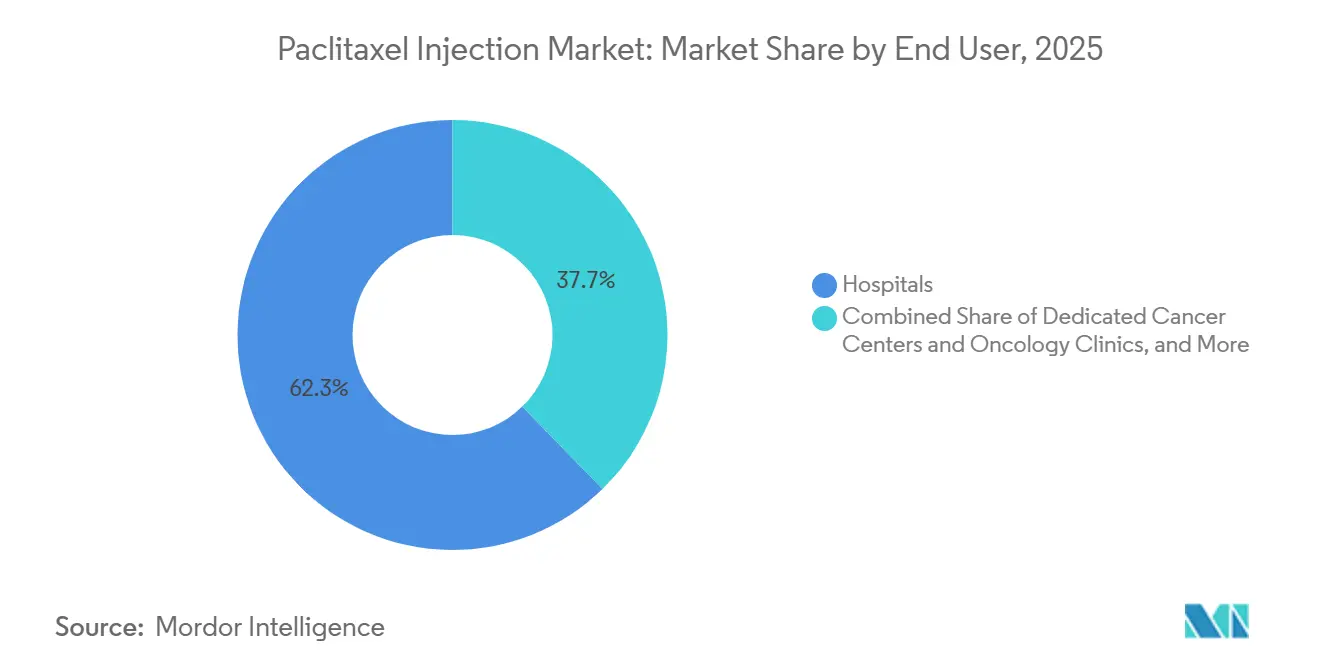

- By end user, hospitals held 62.30% of revenue in 2025, while ambulatory and day-care infusion centers are set to grow at a 13.89% CAGR through 2031.

- By distribution channel, hospital pharmacies captured 58.30% of revenue in 2025, and specialty pharmacies are projected to advance at a 13.88% CAGR through 2031.

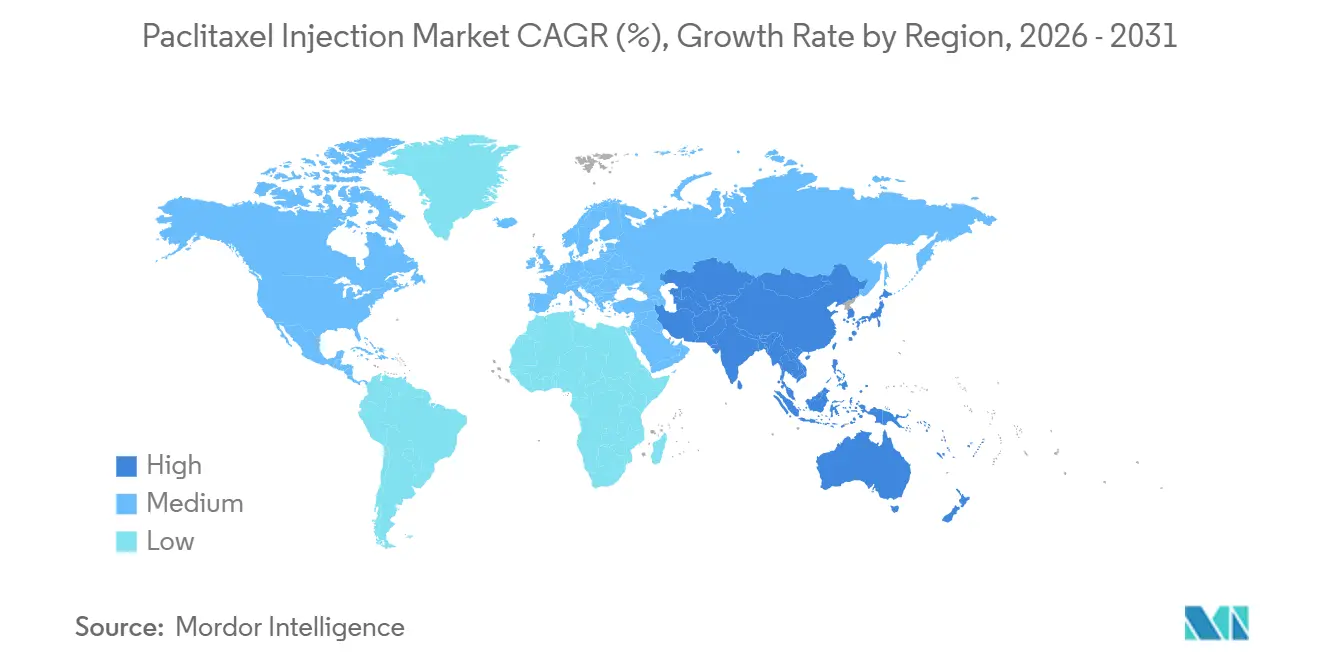

- By geography, North America captured 43.20% of revenue in 2025, and Asia Pacific are projected to advance at a 14.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Paclitaxel Injection Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global incidence of breast, lung, and ovarian cancers | +2.8% | Global, highest absolute growth in Asia-Pacific | Medium term (2-4 years) |

| Inclusion of paclitaxel on WHO Essential Medicines Lists and national formularies | +1.2% | Low- and lower-middle-income countries | Long term (≥4 years) |

| Institutional administration model concentrates demand in hospital oncology settings | +1.5% | Global, particularly North America and Europe | Long term (≥4 years) |

| Adoption of solvent-free and nano-enabled formulations expands eligible patient populations | +2.1% | High-income markets expanding to upper-middle-income Asia | Short term (≤2 years) |

| EMA bioequivalence pathway for nab-paclitaxel enables faster EU generic entry | +1.3% | Europe | Short term (≤2 years) |

| Broader availability from recent nab-paclitaxel generic launches (US/EU) | +1.5% | North America, Europe, with spillover to emerging markets | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Rising Global Incidence of Breast, Lung, And Ovarian Cancers

Global cancer incidence continues to increase, with breast cancer cases projected to reach 3.2 million annually by 2050, up from 2.3 million in 2022, which sustains the use of taxane-based regimens where biomarker-directed options are not suitable or reimbursed[1]International Agency for Research on Cancer, “Breast Cancer Cases and Deaths Are Projected to Rise Globally,” IARC, iarc.who.int. In the United States, 2026 care pathways remain anchored by chemotherapy in several settings, supported by an estimated 316,950 new breast cancer cases and 226,650 lung cancer cases reported for 2025, which underscores enduring demand for paclitaxel-based combinations when immune or targeted therapies are unavailable or suboptimal. Ovarian cancer’s global burden, with substantial mortality, reflects access gaps to companion diagnostics and maintenance therapies that keep paclitaxel relevant in first-line and recurrent protocols across many health systems. As population aging concentrates incidence in middle- and high-income markets and screening broadens in emerging economies, chemotherapy backbones remain critical adjuncts to evolving targeted and immuno-oncology regimens, which stabilize the paclitaxel injection market in core tumor types. These epidemiology trends reinforce formulary continuity for paclitaxel, where clinical guidelines still include taxanes for standard-of-care regimens or for patients who do not meet biomarker thresholds for newer agents

Inclusion Of Paclitaxel On WHO Essential Medicines Lists And National Formularies

Paclitaxel’s inclusion on national essential medicines lists anchors institutional purchasing in low- and middle-income countries, with Zambia’s 2025 Essential Medicines List classifying paclitaxel 6 mg/mL IV solution as vital for tertiary hospitals. Despite this inclusion, availability remains uneven, with access to cytotoxics such as paclitaxel significantly lower in low- and lower-middle-income settings compared with high-income countries, which highlights persistent infrastructure and financing gaps[2]American Cancer Society, “Cancer Facts & Figures 2025,” ACS, cancer.org. Essential-medicine designation supports multi-year tenders and pooled procurement, which contributes to steadier demand volumes and prioritizes stock protection where sterile-injectable shortages are a system risk. In practice, national formularies that emphasize broad-indication chemotherapies ensure backstop options when targeted pathways fail, or biomarker testing is incomplete, which sustains the paclitaxel injection market through varied lines of therapy. Over time, formulary placement, paired with local manufacturing and multi-supplier contracts, helps align cost containment with treatment continuity for hospital-based oncology, which supports more predictable purchasing across budget cycles.

Institutional Administration Model Concentrates Demand In Hospital Oncology Settings

Hospital settings dominate paclitaxel utilization because intravenous dosing requires infusion suites, pharmacy compounding, and immediate access to hypersensitivity management, which naturally concentrates volumes in tertiary care oncology programs. Premedication with corticosteroids, diphenhydramine, and H2 antagonists is recommended for solvent-based paclitaxel to reduce Cremophor EL–related reactions, which reinforces the need for protocolized inpatient or day-hospital administration and trained nursing oversight. Nab-paclitaxel offers shorter infusion times and omits solvent premedication, which supports throughput in outpatient infusion centers while keeping pharmacist verification and adverse event monitoring centralized. Many systems are adopting dual-sourcing and buffer inventories for sterile injectables to hedge against supply disruptions, an approach aligned with USP’s guidance for vulnerable medicines and considered good practice for oncology service continuity. As outpatient infusion infrastructure scales in large urban corridors, hospital procurement remains the anchor for multi-product tenders that bundle paclitaxel with platinum agents, which maintains negotiating leverage and supports consistent chair utilization.

Adoption Of Solvent-Free And Nano-Enabled Formulations Expands Eligible Patient Populations

Shifts toward solvent-free paclitaxel forms aim to reduce infusion reactions and neuropathy related to Cremophor EL, while addressing patients who previously required premedication or experienced dose-limiting intolerance. Real-world pharmacovigilance of nab-paclitaxel in the FDA FAERS database identified hematologic toxicity as the leading signal rather than hypersensitivity, which supports the positioning of solvent-free options for patients with prior infusion issues or steroid contraindications. As antibody-drug conjugates expand in breast cancer, solvent-free paclitaxel remains an alternative where ADCs are not accessible, contraindicated, or following progression, which preserves its role within sequencing strategies. Polymer-based micelle carriers and liposomal constructs are being evaluated in late-stage trials, with preclinical and early clinical evidence suggesting improved intracellular delivery and consistent pharmacokinetics that could mitigate peak concentration toxicity. In Europe, the availability of generic nab-paclitaxel across multiple member states is expanding formulary access for solvent-free options, supported by product-specific approvals and harmonized labeling under the EU regulatory framework.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Toxicity profile (myelosuppression, neuropathy) and solvent-related hypersensitivity | -1.9% | Global | Medium term (2-4 years) |

| Regimen displacement risk from targeted and immuno-oncology therapies | -2.3% | North America, Western Europe, high-income Asia-Pacific | Short term (≤2 years) |

| Sterile-injectable supply shocks and manufacturing/quality disruptions | -1.1% | North America with global spillover | Short term (≤2 years) |

| Price compression from tendering and China VBP on protein-bound paclitaxel | -1.6% | China with spillover to India and Southeast Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Toxicity Profile (Myelosuppression, Neuropathy) And Solvent-Related Hypersensitivity

Neutropenia remains a central dose-limiting toxicity for paclitaxel, with grade 3-4 events documented in patients receiving nab-paclitaxel regimens and necessitating regular monitoring and treatment holds when neutrophil counts fall below defined thresholds[3]Sandoz Inc., “Paclitaxel Protein-Bound Particles Prescribing Information,” Sandoz, us-sandoz-com.cms.sandoz.com. Peripheral neuropathy accumulates with exposure and can lead to dose reductions or discontinuations, which affects regimen adherence and patient quality of life in long courses of therapy. Solvent-based paclitaxel carries a known hypersensitivity risk linked to Cremophor EL, which requires steroid and antihistamine premedication and reinforces the need for supervised infusions in settings equipped for immediate reaction management. FAERS pharmacovigilance indicates that hematologic events are the leading safety signal for nab-paclitaxel, which highlights the importance of complete blood counts and supportive care across cycles. These risk factors shape clinician choice between solvent-based and solvent-free options and sustain the clinical rationale for regimen adjustments and dose intensity management in practice.

Regimen Displacement Risk From Targeted And Immuno-Oncology Therapies

Antibody-drug conjugates are moving earlier in treatment algorithms in breast cancer, with Enhertu’s approval for HER2-low and HER2-ultralow disease demonstrating superior progression-free survival versus chemotherapy that included paclitaxel, which narrows first-line chemotherapy use in eligible populations[4]AstraZeneca, “Enhertu Approved in the US for HER2-low or HER2-ultralow MBC,” AstraZeneca, astrazeneca.com. In PD-L1–positive metastatic triple-negative breast cancer, pembrolizumab plus Trodelvy reduced progression risk versus pembrolizumab plus chemotherapy that included paclitaxel, which signals class-level migration toward ADC combinations in frontline settings. Dual checkpoint combinations such as nivolumab plus ipilimumab have shown survival gains in NSCLC compared with chemotherapy, irrespective of PD-L1 expression, which further reshapes first-line choices away from taxane-based doublets in defined cohorts. Even so, chemotherapy remains critical after targeted therapy resistance or when biomarker-defined therapies are contraindicated, which helps maintain a durable baseline for the paclitaxel injection market in later lines. Over the forecast period, the balance between biomarker-driven therapies and chemotherapy backbones will hinge on eligibility rates and payer criteria, which will determine how much frontline displacement translates into total-course taxane volume changes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Formulation: Generic Nab-Paclitaxel Proliferation Reshapes Safety and Access Dynamics

Solvent-based paclitaxel held 56.2% of 2025 revenues, reflecting legacy protocols, broad availability, and established infusion practices that rely on prophylactic steroids and antihistamines to mitigate Cremophor EL–related reactions. The paclitaxel injection market size for liposomal and polymeric-micelle formulations is projected to expand at 15.31% CAGR between 2026 and 2031, as solvent-free delivery and improved intracellular uptake broaden patient eligibility and reduce chair time relative to three-hour solvent-based infusions. Nab-paclitaxel’s omission of solvent premedication and its 30-minute infusion profile align with high-throughput outpatient operations, which support faster turnover in cancer centers with constrained infusion chairs. Generic competition across the U.S. and EU has eroded the originator’s position and redirected purchasing toward multi-supplier panels, with EU approvals such as Naveruclif and Apexelsin reinforcing access in markets that run centralized tenders. As the paclitaxel injection market absorbs greater generic depth, clinical selection within solvent-free options will depend on local outcomes data, site of care protocols, and payer policies for substitution, rather than on branded differentiation.

The paclitaxel injection industry is likely to see further formulation innovation in micellar and liposomal carriers, contingent on Phase III evidence and regulator alignment on bioequivalence or superiority endpoints. Across 2026-2031, unit growth in solvent-free categories will reflect payer openness to generic substitution, guideline integration for specific tumor types, and the operational goals of infusion centers to increase chair throughput without sacrificing safety. These factors together reinforce the multi-year shift toward solvent-free platforms within the paclitaxel injection market.

By Indication: Pancreatic Adenocarcinoma Emerges as Growth Epicenter

Breast cancer contributed 36.5% of 2025 revenues, reflecting the persistent role of taxanes across neoadjuvant, adjuvant, and metastatic care when sequencing after anthracycline or when targeted options are exhausted. The paclitaxel injection market size for pancreatic applications is poised to grow at a 15.44% CAGR through 2031, anchored by the gemcitabine plus nab-paclitaxel doublet that improved median overall survival to 8.5 months versus 6.7 months in the MPACT study, which established the regimen as a standard for metastatic disease. In NSCLC, displacement by checkpoint inhibitors has reduced first-line taxane doublet use in eligible patients, although paclitaxel maintains relevance for those who do not meet immunotherapy criteria or require later-line chemotherapy. Ovarian cancer continues to support steady taxane volume, with paclitaxel plus platinum combinations used broadly in first-line settings and in defined recurrent contexts, especially where biomarker-directed maintenance is not feasible or reimbursed. Cervical cancer and AIDS-related Kaposi’s sarcoma represent smaller shares, but essential-medicine status in national formularies preserves procurement and clinical availability in resource-limited settings.

Across tumor types, guideline recommendations and payer policies will shape taxane use over time, with expansion likely in gastrointestinal and gynecologic settings where combination regimens with immunotherapy have gained approvals. Regulatory developments in Asia have recognized combinations that incorporate paclitaxel with checkpoint inhibitors in gynecologic malignancies, which signals continuing integration of taxanes within multi-agent protocols. The paclitaxel injection market therefore stays diversified across indications, with growth most visible in pancreatic cancer and in combination regimens that preserve or extend chemotherapy utility. Over the forecast period, real-world data and tolerability in routine practice will be central to sustaining regimen adherence and optimizing outcomes within each indication.

By End User: Ambulatory Infrastructure Scales Amid Hospital Dominance

Hospitals accounted for 62.3% of 2025 revenues, reflecting infusion infrastructure, pharmacist-led compounding, and on-site management of hypersensitivity and cytopenias that are essential for safe administration. Cancer centers and oncology clinics are adopting solvent-free paclitaxel to streamline 30-minute infusions where appropriate, which supports higher throughput and improves chair availability without sacrificing monitoring standards. Ambulatory and day-care infusion centers are growing fastest as payers promote site-of-care shifts and patients prefer non-hospital environments for routine cycles, which supports broader access in urban corridors. The paclitaxel injection market benefits when hospital-based protocols are replicated with equal rigor in outpatient settings, especially given solvent-based premedication requirements that remain common for legacy regimens. Over time, GPO participation by ambulatory networks can approach hospital pricing, which encourages further migration of stable patients to outpatient infusion.

Policy and reimbursement changes in major markets are also enabling certified outpatient facilities to deliver combination regimens that include paclitaxel, which expands infrastructure beyond tertiary hospitals. Hospital pharmacies retain advantages in inventory buffers and electronic verification workflows that reduce dosing and dispensing errors and help manage shortages. The paclitaxel injection industry will continue to balance capacity between high-acuity hospital care and scalable outpatient sites, guided by safety protocols and payer incentives. As staffing and training improve across both settings, adverse event management and adherence monitoring will remain core to preserving taxane dose intensity and clinical benefit. These operational improvements reinforce sustained utilization across care sites in the paclitaxel injection market.

By Distribution Channel: Specialty Pharmacies Gain Share via Complex-Regimen Coordination

Hospital pharmacies accounted for 58.30% share in 2025. Distribution as institutional tenders favor multi-supplier panels and buffer inventory commitments that support sterilized workflow continuity. The paclitaxel injection market size for specialty pharmacies is poised to grow at a 13.88% CAGR through 2031. Specialty pharmacies are gaining share as they coordinate benefits, prior authorizations for solvent-free formulations, and supportive medications such as antiemetics and G-CSF, which enables closed-loop adherence around infusion schedules. The paclitaxel injection market size is influenced by channel policies that determine whether complex regimens are steered to integrated health-system pharmacies or to external specialty networks with advanced patient services. Retail and online channels remain marginal due to injectable compounding requirements, though these outlets dispense supportive drugs that are complementary to taxane cycles. Over the forecast period, serialization and track-and-trace regulations will continue to favor larger specialty platforms that can absorb compliance costs and integrate with oncology EHRs.

Institutional integration remains a factor, as many cancer centers operate captive specialty pharmacies to retain continuity of care and data integration, which can slow external specialty share in some regions. As payers push for lower total care costs, site-of-care and channel strategies will direct complex regimens to networks that demonstrate measurable adherence and safety outcomes. Hospital-based distribution will continue to dominate first-cycle and high-acuity use, while specialty pharmacies expand coordination for stable patients under multi-agent regimens. The paclitaxel injection market will therefore reflect a hybrid channel model where institutional anchors and specialized networks both play roles in ensuring supply and patient support. This blended approach helps balance cost containment with reliability and clinical oversight.

Geography Analysis

North America accounted for 43.2% of 2025 revenues, supported by established treatment pathways, oncologist familiarity with taxane regimens, and reimbursement coverage across solvent-based and albumin-bound formulations. The paclitaxel injection market in the United States has shifted toward multi-supplier purchasing after 2024-2025 generic launches, which accelerated price competition and eroded the originator’s sales as hospital GPOs reinforced substitution to approved generics. Company disclosures show continued revenue pressure on the originator brand in late 2025, which illustrates how tender competition and formulary substitution drive rapid share shifts in hospital oncology. Canada and Mexico contribute smaller shares, with budget differences shaping the mix between solvent-based and solvent-free products across public and private providers. The paclitaxel injection market remains stable in North America as chemotherapy continues to complement biomarker-driven therapies and supports care sequences after targeted therapy resistance.

Europe represented an estimated 25.30% of 2025 revenues, led by Germany, France, Italy, Spain, and the United Kingdom. EMA marketing authorizations for generic nab-paclitaxel products such as Naveruclif and Apexelsin broadened options for hospitals that procure through centralized tenders and prefer multi-supplier awards for inventory resilience. Product-specific bioequivalence guidance is harmonizing evidence expectations across EU markets, which improves payer confidence in substitutable options and supports cross-border distribution under unified labeling standards. National-level updates to generic product characteristics and safety information continue through Type II variations, which keep labels aligned with originator references and pharmacovigilance requirements. Over 2026-2031, the paclitaxel injection market in Europe should maintain steady unit volumes on demographic drivers, with revenue growth moderated by generic saturation and price convergence under tender frameworks.

Asia-Pacific is the fastest-growing region for the paclitaxel injection market with a forecast CAGR of 14.12%, reflecting rising cancer incidence, expanding oncology infrastructure, and domestic manufacturing scale in China and India. In China, local approvals for albumin-bound paclitaxel have strengthened domestic supply, which supports broader access under public procurement rules and eases dependence on imports. Regulatory approvals for regimens that include paclitaxel in gynecologic malignancies, such as durvalumab-based combinations, broaden the addressable patient base for taxanes in hospital and certified outpatient settings. India’s role as a scaled manufacturer and exporter of oncology injectables reinforces regional and global supply, aided by global approvals that validate product quality and support hospital tenders. Japan, Australia, and South Korea generate higher per-capita revenues due to reimbursement environments that cover solvent-free options, with Japan integrating taxanes into combinations that sustain chemotherapy utilization in defined populations as immunotherapy expands. In the Middle East and Africa and in South America, lower shares reflect oncology infrastructure constraints and public funding limits, though government tenders and essential-medicine programs sustain baseline procurement when budgets permit. Over the forecast period, the paclitaxel injection market in emerging regions should gradually expand as universal health coverage programs evolve and as multi-supplier sourcing reduces stockout exposure.

Competitive Landscape

The paclitaxel injection market is moderately fragmented, with originator brands losing share to multiple generic entrants that compete on price, supply reliability, and substitution support in hospital protocols. In 2024-2025, the launch of generic nab-paclitaxel across the U.S. and EU expanded supplier choices for tenders and compressed premium pricing, which challenged the originator to demonstrate outcome advantages that could justify continued formulary preference. Public disclosures in early 2026 indicate significant revenue declines for the originator brand through late 2025, which aligns with accelerated generic penetration and multi-supplier awards among European and North American buyers. Supplier credibility is increasingly tied to inspection records, sterile capacity, and buffer-inventory commitments, which are decisive in oncology tenders that weigh price against continuity.

Strategic moves by leading generics manufacturers focused on rapid entry and portfolio breadth, including the first FDA-approved generic nab-paclitaxel in the U.S. and EU-facing approvals that enabled broad language coverage and cross-border supply. Additional U.S. launches during 2024 supported hospital formulary substitution norms and fortified redundancy, while portfolio press releases in early 2025 underscored continued investment in sterile manufacturing and oncology pipelines across major generics incumbents. For China-based players with approved albumin-bound paclitaxel, strong domestic sales underpin reinvestment in delivery platforms and regional expansion strategies that can complement EU market entries.

Innovation white space remains in solvent-free and advanced carriers that aim to reduce neuropathy and infusion reactions while preserving efficacy, which could help recapture margins if late-stage evidence supports superiority in defined populations. On the biologics side, next-generation ADCs under evaluation with novel cytotoxic payloads continue to influence the chemotherapy-to-targeted shift, which shapes taxane positioning in multiple tumor types. Portfolio optimization efforts by large generics manufacturers prioritize higher-margin sterile products and biosimilars, while maintaining essential oncology injectables to retain tender participation and hospital relationships. Over 2026-2031, competitive differentiation will center on inspection readiness, multi-site manufacturing, and real-time quality analytics, all of which influence tender scoring and channel preferences in the paclitaxel injection market.

Paclitaxel Injection Industry Leaders

Bristol-Myers Squibb Company

Pfizer Inc.

Fresenius Kabi AG

Teva Pharmaceutical Industries Ltd.

Sandoz Group AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: The FDA approved relacorilant with nab-paclitaxel for adults with platinum-resistant epithelial ovarian, fallopian tube, or primary peritoneal cancer who have undergone 1 to 3 prior systemic treatments, including at least one with bevacizumab.

- May 2025: Meitheal Pharmaceuticals, Inc. launched albumin-bound paclitaxel protein-bound particles for injectable suspension in the United States market. The product, a generic version of Abraxane, is introduced under an exclusive licensing and supply agreement with its parent company, Hong Kong King-Friend Industry Co., Ltd.

Global Paclitaxel Injection Market Report Scope

As per the scope of the market, paclitaxel injection is a chemotherapy medication used to treat various types of cancer. It contains the active ingredient paclitaxel, which works by inhibiting the growth of cancer cells. The injection is administered intravenously (IV) under medical supervision.

The Paclitaxel Injection Market Report segments the market by formulation, including solvent-based paclitaxel injection, albumin-bound paclitaxel injection, liposomal/polymeric-micelle paclitaxel injection, and others. It also categorizes the market by indication, covering breast cancer, non-small cell lung cancer, ovarian cancer, pancreatic adenocarcinoma, AIDS-related Kaposi's sarcoma, and others. The end-user segmentation includes hospitals, dedicated cancer centers and oncology clinics, and ambulatory/day-care infusion centers. Additionally, the distribution channel is segmented into hospital pharmacies, specialty pharmacies, retail and online pharmacies, and others. Geographically, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Solvent Based Paclitaxel Injection |

| Albumin Bound Paclitaxel Injection |

| Liposomal / Polymeric Micelle Paclitaxel Injection |

| Others (Polymeric Micelle Paclitaxel Injection, Emulsion Based Paclitaxel Injection) |

| Breast Cancer |

| Non-Small Cell Lung Cancer (NSCLC) |

| Ovarian Cancer |

| Pancreatic Adenocarcinoma |

| AIDS Related Kaposis Sarcoma |

| Others (Cervical Cancer, Endometrial Cancer) |

| Hospitals |

| Dedicated Cancer Centers & Oncology Clinics |

| Ambulatory/Day Care Infusion Centers |

| Hospital Pharmacies |

| Specialty Pharmacies |

| Retail & Online Pharmacies |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Formulation | Solvent Based Paclitaxel Injection | |

| Albumin Bound Paclitaxel Injection | ||

| Liposomal / Polymeric Micelle Paclitaxel Injection | ||

| Others (Polymeric Micelle Paclitaxel Injection, Emulsion Based Paclitaxel Injection) | ||

| By Indication | Breast Cancer | |

| Non-Small Cell Lung Cancer (NSCLC) | ||

| Ovarian Cancer | ||

| Pancreatic Adenocarcinoma | ||

| AIDS Related Kaposis Sarcoma | ||

| Others (Cervical Cancer, Endometrial Cancer) | ||

| By End User | Hospitals | |

| Dedicated Cancer Centers & Oncology Clinics | ||

| Ambulatory/Day Care Infusion Centers | ||

| By Distribution Channel | Hospital Pharmacies | |

| Specialty Pharmacies | ||

| Retail & Online Pharmacies | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected growth of the paclitaxel injection market through 2031?

The paclitaxel injection market is projected to reach USD 13.07 billion by 2031 at a 12.39% CAGR over 2026-2031.

Which tumor areas will most influence demand for paclitaxel-based regimens?

Breast and ovarian cancers sustain baseline demand in multiple lines, while pancreatic adenocarcinoma is the fastest-growing application due to the gemcitabine plus nab-paclitaxel standard.

How are solvent-free formulations changing clinical adoption?

Nab-paclitaxel and emerging micellar carriers reduce solvent-related reactions and shorten infusion times, which expands eligible patients and improves outpatient throughput.

What regulatory shifts are most impactful in Europe?

EMAs product-specific bioequivalence guidance for nab-paclitaxel is accelerating generic approvals and harmonizing substitutability across tenders and member states.

How are hospital and specialty pharmacies dividing distribution roles?

Hospital pharmacies dominate initial cycles and high-acuity care, while specialty pharmacies are gaining share by coordinating benefits, authorizations, and supportive medications around complex regimens.

Which factors will shape competitive positioning through 2031?

Multi-site manufacturing, inspection readiness, buffer inventories, and portfolio breadth will guide tender decisions as price competition intensifies across solvent-based and solvent-free products.

Page last updated on: