Packaging Robots Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

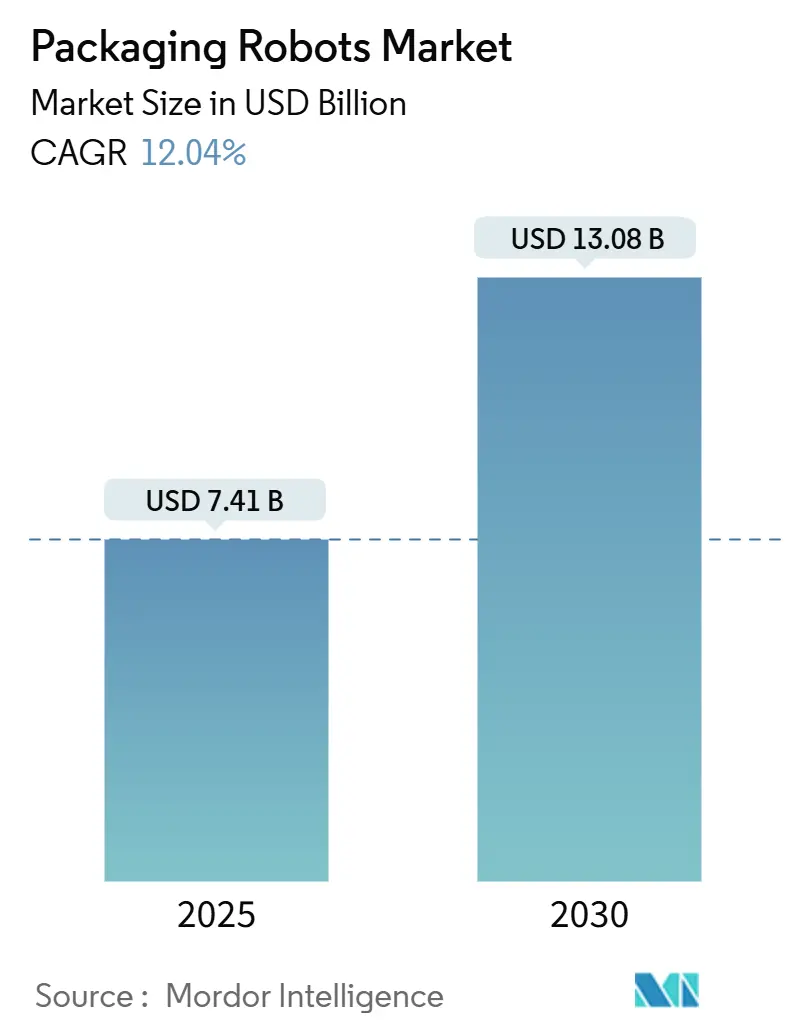

| Market Size (2025) | USD 7.41 Billion |

| Market Size (2030) | USD 13.08 Billion |

| Growth Rate (2025 - 2030) | 12.04% CAGR |

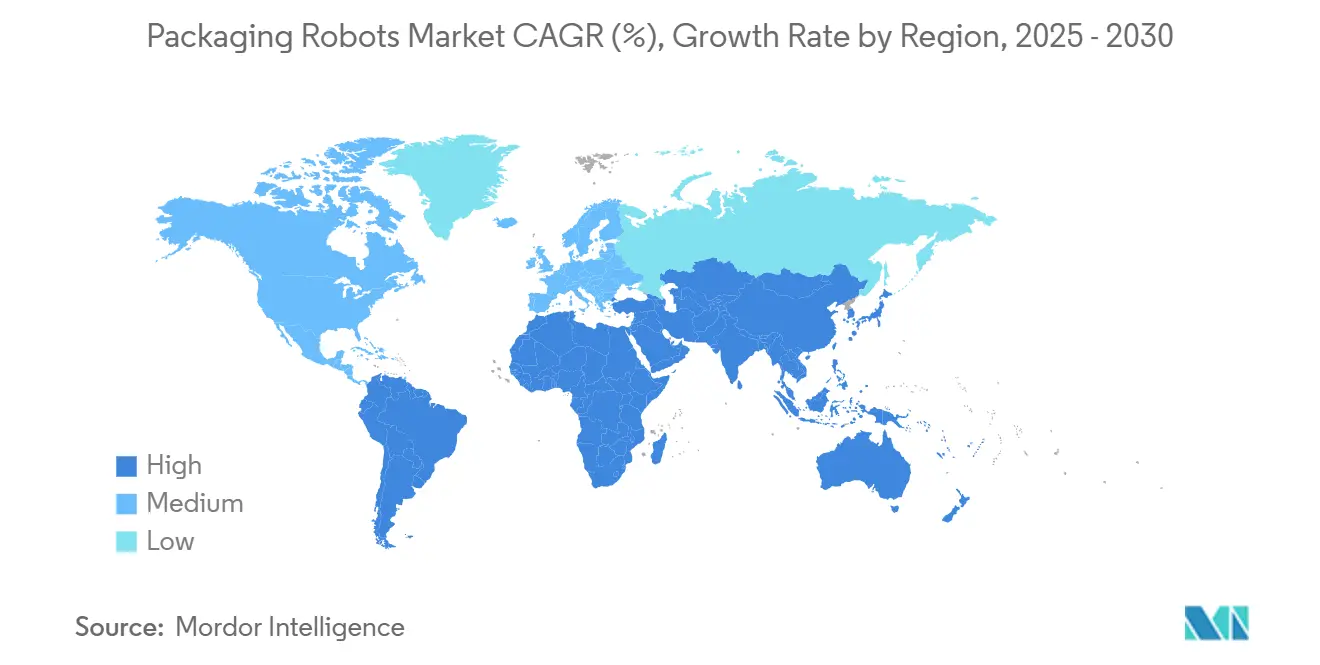

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

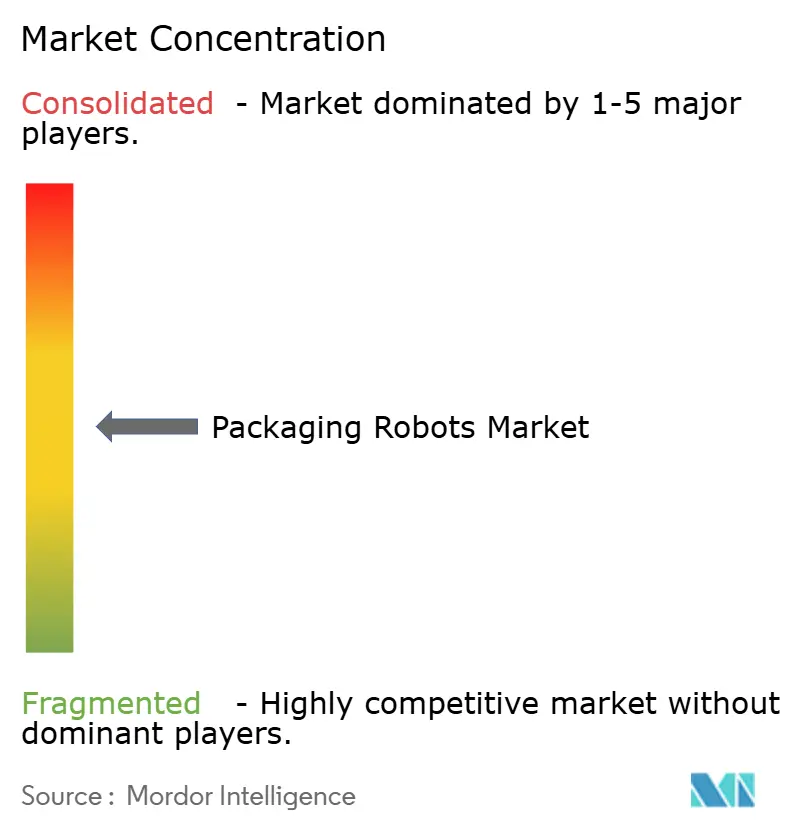

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Packaging Robots Market Analysis by Mordor Intelligence

The global packaging robots market size stands at USD 7.41 billion in 2025 and is projected to reach USD 13.08 billion by 2030, registering a 12.04% CAGR over the forecast period. Growth is fueled by rising e-commerce fulfillment volumes, sustained labor shortages, and Industry 4.0 retrofits that elevate automation demand. Subscription-based Robotics-as-a-Service agreements ease capital constraints, while AI-enabled predictive-maintenance platforms trim unplanned downtime as much as 30%, improving return on investment. Versatile articulated robots dominate complex packaging duties, and collaborative models gain favor for safe human-robot interaction, helping manufacturers bridge talent gaps and meet tighter turnaround targets.

Key Report Takeaways

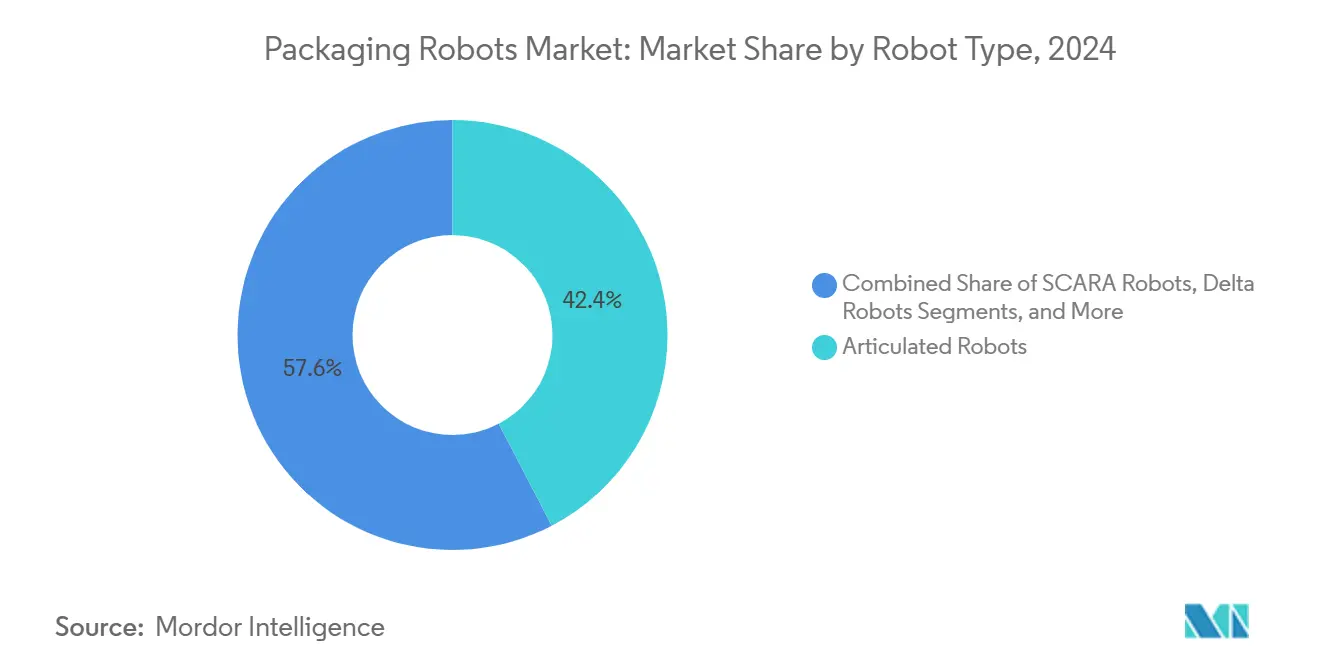

- By robot type, the articulated systems segment captured 42.37% of the packaging robots market share in 2024.

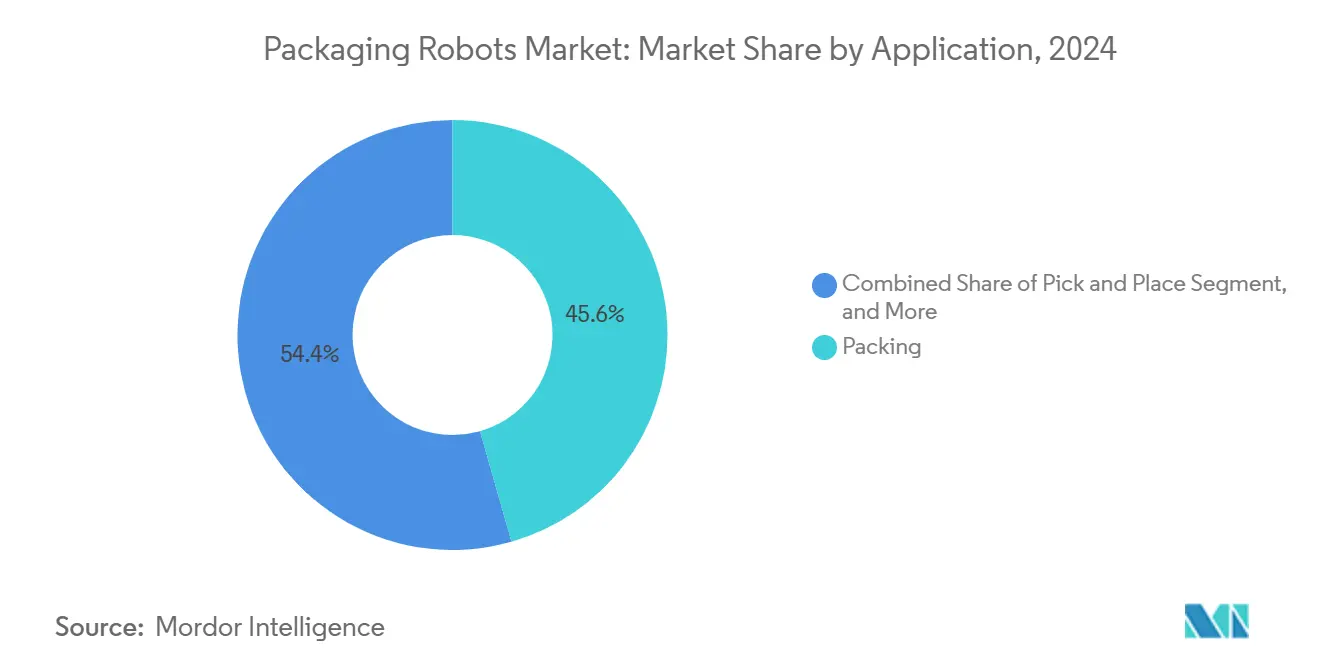

- By application, the packaging robots market size for pick-and-place solutions is projected to grow at a 15.39% CAGR between 2025–2030.

- By gripper type, the clamp technology segment captured 37.63% of the packaging robots market share in 2024.

- By geography, the packaging robots market size for the Middle East and Africa region is projected to grow at an 18.68% CAGR between 2025–2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Packaging Robots Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce order-fulfillment boom | 3.2% | Global, with a concentration in North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| Chronic labour shortages and wage inflation | 2.8% | North America, Europe, and developed APAC markets | Long term (≥ 4 years) |

| Industry 4.0-driven smart-factory retrofits | 2.1% | Europe, North America, and advanced manufacturing hubs in APAC | Medium term (2-4 years) |

| Stricter food-safety and pharma traceability rules | 1.7% | Global, with early adoption in the EU, North America | Short term (≤ 2 years) |

| Subscription-based "Robotics-as-a-Service" models | 1.4% | Global, particularly beneficial for SMEs in emerging markets | Medium term (2-4 years) |

| AI-enabled predictive maintenance is slashing downtime | 1.2% | Advanced manufacturing regions globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-commerce Order-Fulfillment Boom

Surging online retail transactions force fulfillment centers to automate packing lines capable of handling mixed-SKU workloads at high speed. Amazon plans to field 520,000 robotic units across its network by 2024. A clear signal of scale is now expected across the industry.[1]Amazon, “Amazon Robotics: 10 Years of Innovation,” About Amazon, aboutamazon.com Third-party logistics firms deploy collaborative arms outfitted with vision systems that quickly learn new stock-keeping units, eliminating costly re-programming delays. The migration from batch to real-time parcel workflows increases the demand for flexible robots that can switch between single-item picks and multi-unit orders without interrupting production.

Chronic Labor Shortages and Wage Inflation

The National Association of Manufacturers recorded 2.1 million unfilled factory roles in 2024 and escalating wages for skilled operators. Packaging tasks that once relied on manual dexterity are increasingly being performed by collaborative robots able to work safely beside limited staff. RaaS contracts let factories sidestep heavy capital outlays and access advanced automation on subscription terms that mirror monthly output, sustaining productivity while headcounts stagnate.

Industry 4.0-Driven Smart-Factory Retrofits

Connected sensors, edge computing, and cloud analytics integrate legacy lines into smart cells. Siemens Digital Factory pilots demonstrated 20–30% efficiency gains from real-time data loops linking robots with supervisory control systems. Packaging robots now feature onboard processors that analyze inspection images locally, thereby shortening feedback cycles. Combined with emerging 5G private networks, plants gain remote visibility across multiple sites and schedule service proactively before minor faults escalate.

Stricter Food-Safety and Pharma Traceability Rules

The U.S. FDA’s Food Safety Modernization Act and EU drug-serialization laws oblige manufacturers to document every handling step. Robots equipped with vision cameras compile digital audit trails while minimizing human contact, lowering contamination risk for temperature-sensitive or sterile goods. Blockchain interfaces secure immutable records that regulators can verify instantly, driving adoption in life-science cleanrooms and prepared-meal packing sites.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront CAPEX for SMEs | -2.3% | Global, particularly acute in emerging markets and SME-heavy regions | Medium term (2-4 years) |

| Scarcity of integration and maintenance skills | -1.8% | Global, with varying intensity based on technical education infrastructure | Long term (≥ 4 years) |

| Rare-earth magnet supply-chain price volatility | -1.1% | Global, with particular impact on precision robotics applications | Short term (≤ 2 years) |

| Cyber-security risks in IIoT-connected lines | -0.9% | Advanced manufacturing regions with high connectivity adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront CAPEX for SMEs

Capital requirements for a full packaging cell range from USD 200,000 to USD 800,000, including safety cages, conveyors, and programming. Smaller firms often encounter payback periods exceeding typical lending horizons. Subscription robotics models mitigate this barrier, turning a lump-sum purchase into an operating expense aligned with seasonal production peaks.

Scarcity of Integration and Maintenance Skills

Modern packaging robots incorporate AI software, cybersecurity patches, and multi-axis motion controls, which require specialized technicians. Integration projects may stretch 6–12 months, and competition for talent drives salaries to levels many mid-sized plants cannot match. Outsourced managed-service contracts and remote diagnostics help alleviate the shortfall, but they add cost layers that temper the adoption speed.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Robot Type: Articulated Systems Drive Versatility

Articulated robots accounted for 42.37% of 2024 revenue within the packaging robots market. Their six-axis range covers tasks from high-speed bottle loading to heavy pallet stacking. Collaborative models record a 15.43% CAGR, propelled by intuitive drag-and-drop programming and built-in force-sensing that lets them share workspace without cages.

SCARA platforms retain relevance in precise top-loading operations, whereas delta robots remain prized for lightweight, rapid picking in confectionery flow-wrap lines. Across categories, embedded AI vision enhances part recognition accuracy, eliminating manual changeovers and improving uptime.

By Gripper Type: Clamp Technology Leads Market

Clamp designs secured 37.63% of 2024 revenue, serving rigid cartons and cans that dominate fast-moving consumer goods lines. Evolution toward soft-touch silicone pads addresses recyclable thin-wall packaging without deforming surfaces.

Claw variants growing at a 14.29% annual rate excel at grasping irregular SKUs common to e-commerce assortments. Hybrid end-effectors combine vacuum, mechanical, and magnetic gripping to minimize tooling swaps, improving the mean time between changeovers and boosting overall equipment effectiveness.

By Application: Packing Operations Retain Leadership

Packing stages, covering primary to tertiary containment, generated 45.57% of the revenue in 2024. Continuous motion top-load carton packing and wrap-around case erecting favor articulated arms with coordinated multi-axis control.

Pick-and-place routines are expected to increase by 15.39% per year as omnichannel retailers automate order assembly. AI field-learning allows one robot to alternate between bubble-wrapped electronics and bagged apparel with no offline programming.

By End-user Industry: Food Industry Maintains Lead

Food processors commanded 44.15% of the usage share, thanks to hygiene requirements and high throughput. Robots in wash-down stainless housings perform deboning, tray sealing, and end-of-line palletizing while logging lot codes for traceability compliance.

E-commerce fulfillment is the fastest-growing segment at 18.91% CAGR, driven by SKU diversity and the demand for one-piece flow in parcel hubs. Pharmaceutical firms invest in serialization to comply with regulations, and beverage bottlers streamline repetitive crate loading processes where payload and cycle time demands exceed human capacity.

Geography Analysis

The Asia-Pacific region dominated with 34.29% of 2024 revenue, as dense manufacturing ecosystems in China, Japan, and South Korea integrate packaging robots across electronics and automotive supply chains. Rising wages and government incentives accelerate payback, and domestic vendors, such as SIASUN, broaden their affordable offerings.

North America emphasizes collaborative formats to support flexible, short-run consumer goods, while Europe prioritizes material-saving automation aligned with circular economy directives. The Middle East and Africa region, buoyed by Saudi Vision 2030's industrial diversification, is expected to achieve the fastest expansion at an anticipated 18.68% CAGR through 2030.[2]Vision 2030 Kingdom of Saudi Arabia, “Vision 2030,” vision2030.gov.sa

Saudi Arabia's Vision 2030 program includes substantial investments in automated manufacturing capabilities, while the United Arab Emirates positions itself as a regional logistics hub, requiring advanced packaging and fulfillment technologies. The region's growth potential stems from relatively low current automation penetration, creating opportunities for rapid adoption as manufacturing sectors develop and labor costs increase.

Competitive Landscape

Market concentration is moderate, with ABB, FANUC, KUKA, and Yaskawa leveraging broad portfolios and global service footprints. ABB’s investment in additional collaborative-robot capacity in Sweden and China, announced in September 2025, targets soaring demand for packaging-specific units. FANUC’s CRX-25iA model, launched in August 2025, increases the payload to 25 kg, supporting larger e-commerce parcels.[3]FANUC Corporation, “Packaging Industry Solutions,” fanuc.com Universal Robots’ July 2025 integration of MiR mobile platforms combines autonomous carts with cobot arms to create fully mobile packing cells. Rising patent activity in AI vision and human-robot interaction, as tracked by the USPTO database, underscores the technology's differentiation.

Mid-tier players, such as Omron, Mitsubishi Electric, and Stäubli, widen the competitive pressure by releasing gripper upgrades and safety-certified cobots that address niche hygiene or precision requirements. These vendors often collaborate with regional system integrators to bundle turnkey packaging cells that shorten commissioning times for small manufacturers. Service-driven models, including Robotics-as-a-Service subscriptions, enable newer entrants like Ready Robotics to compete on operational flexibility rather than hardware scale. As a result, buyers gain leverage to negotiate performance-based contracts that tie monthly fees to uptime metrics.

Regional specialists contribute further fragmentation. SIASUN supplies cost-optimized articulated robots to Chinese food and beverage plants benefiting from government automation subsidies. In the Middle East, Gulf Integration Services partners with KUKA to localize palletizing solutions that suit high ambient temperatures and wide product mixes. European OEMs prioritize sustainability features, embedding energy-recovery drives that cut power draw up to 15%, while North American vendors emphasize open-software ecosystems that let factories layer third-party AI analytics on existing cells.

Packaging Robots Industry Leaders

ABB Ltd.

FANUC CORPORATION

KUKA AG

Yaskawa Electric Corporation

Mitsubishi Electric Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: ABB committed USD 150 million to expand collaborative-robot production in Sweden and China, adding AI features for high-mix packaging.

- August 2025: FANUC released the CRX-25iA cobot tailored for irregular-shape product handling in distribution centers.

- June 2025: Yaskawa opened a USD 75 million AI robotics R&D center in Singapore focused on Southeast Asian packaging needs.

- May 2025: KUKA partnered with Microsoft Azure to embed cloud-based predictive maintenance, aiming to cut downtime by 35%.

Global Packaging Robots Market Report Scope

| Articulated Robots |

| SCARA Robots |

| Delta Robots |

| Cartesian / Gantry Robots |

| Collaborative Robots |

| Others Robot Type |

| Clamp |

| Claw |

| Vacuum |

| Other Gripper Type |

| Packing |

| Pick and Place |

| Palletizing |

| Other Applications |

| Food |

| Beverage |

| Pharmaceutical |

| Personal Care and Cosmetics |

| Electronics and Semiconductor |

| E-commerce and Logistics |

| Others End-user Industry |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Robot Type | Articulated Robots | ||

| SCARA Robots | |||

| Delta Robots | |||

| Cartesian / Gantry Robots | |||

| Collaborative Robots | |||

| Others Robot Type | |||

| By Gripper Type | Clamp | ||

| Claw | |||

| Vacuum | |||

| Other Gripper Type | |||

| By Application | Packing | ||

| Pick and Place | |||

| Palletizing | |||

| Other Applications | |||

| By End-user Industry | Food | ||

| Beverage | |||

| Pharmaceutical | |||

| Personal Care and Cosmetics | |||

| Electronics and Semiconductor | |||

| E-commerce and Logistics | |||

| Others End-user Industry | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How big is the packaging robots market in 2025?

The packaging robots market size reaches USD 7.41 billion in 2025.

What is the forecast CAGR for packaging robots through 2030?

The market is expected to grow at a 12.04% CAGR from 2025 to 2030.

Which robot type leads current adoption?

Articulated robots hold 42.37% market share, owing to multi-axis versatility.

Which region will grow the fastest by 2030?

The Middle East and Africa region is projected to post an 18.68% CAGR.

Why are collaborative robots gaining traction?

Cobots work safely beside humans, addressing labor shortages and enabling flexible, quick-change packaging lines.

Page last updated on: