Oxidation And Corrosion Control Chemicals Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

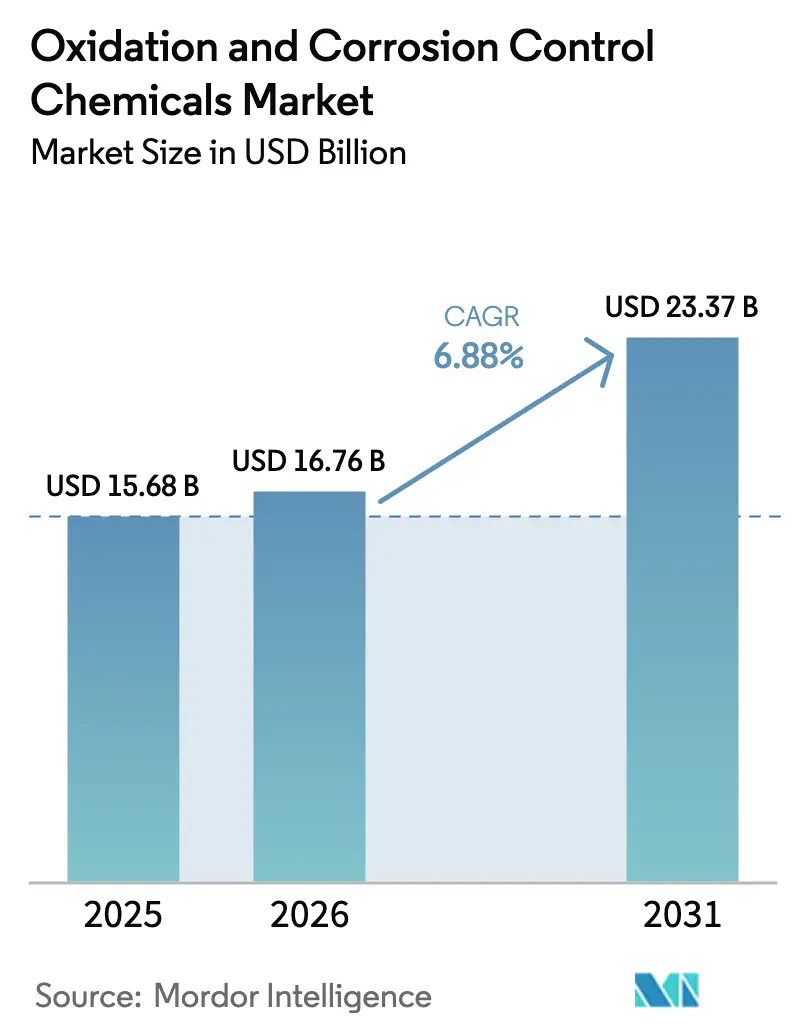

| Market Size (2026) | USD 16.76 Billion |

| Market Size (2031) | USD 23.37 Billion |

| Growth Rate (2026 - 2031) | 6.88% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Oxidation And Corrosion Control Chemicals Market Analysis by Mordor Intelligence

The Oxidation And Corrosion Control Chemicals Market size is expected to grow from USD 15.68 billion in 2025 to USD 16.76 billion in 2026 and is forecast to reach USD 23.37 billion by 2031 at a 6.88% CAGR over 2026-2031. Stricter worldwide drinking-water rules, rapid infrastructure renewal across North America and Europe, and the Asia-Pacific’s push for zero-liquid-discharge systems are converging to lift chemical dosing volumes. Corrosion inhibitors dominate because legacy municipal and industrial assets must control lead leaching and metal loss, yet advanced oxidation technologies are growing faster as utilities target PFAS, 1,4-dioxane, and other emerging contaminants. Regional manganese price spikes and selective phosphate bans are reshaping product formulation strategies, while semiconductor fabs create a premium niche that values ultrapure oxidants and phosphate-free inhibitors. Overall, suppliers that pair compliance expertise with cost-efficient logistics stand to capture rising procurement budgets over the next five years.

Key Report Takeaways

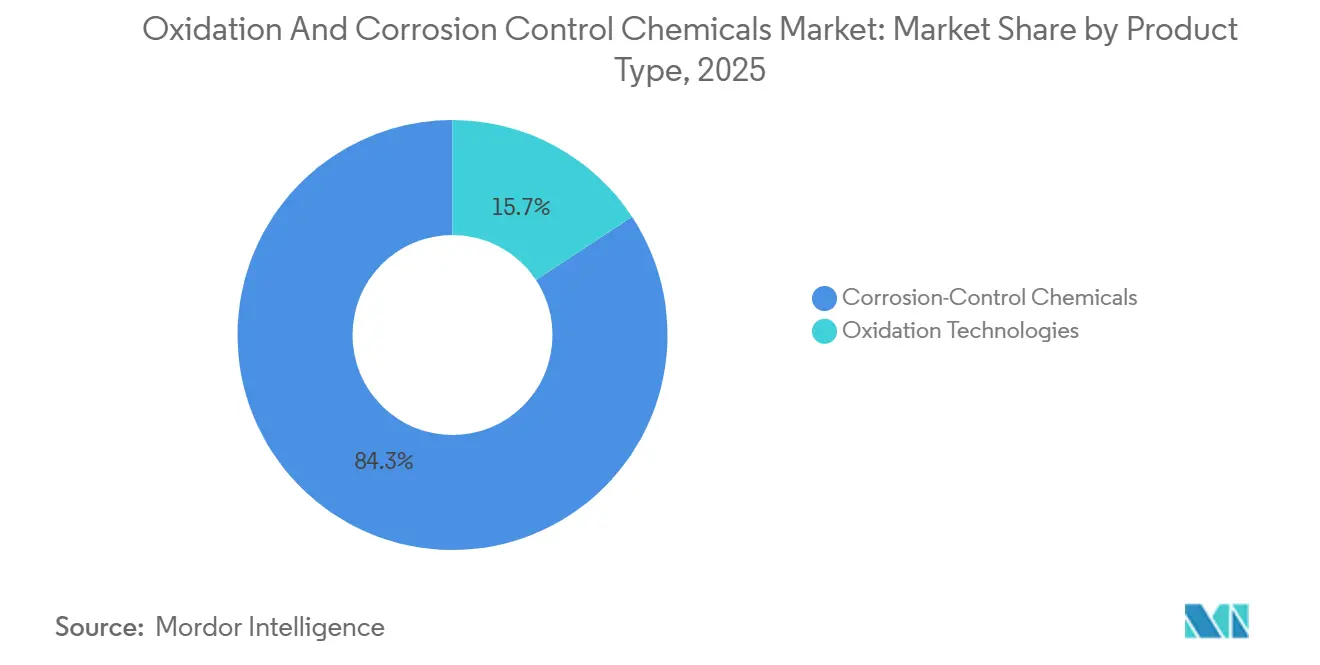

- By product type, corrosion-control chemicals led with 84.26% of the Oxidation and Corrosion Control Chemicals market share in 2025; oxidation technologies are projected to expand at a 7.94% CAGR through 2031.

- By end user, industrial water treatment accounted for a 62.18% share of the Oxidation and Corrosion Control Chemicals market size in 2025, while municipal water treatment is advancing at a 7.07% CAGR through 2031.

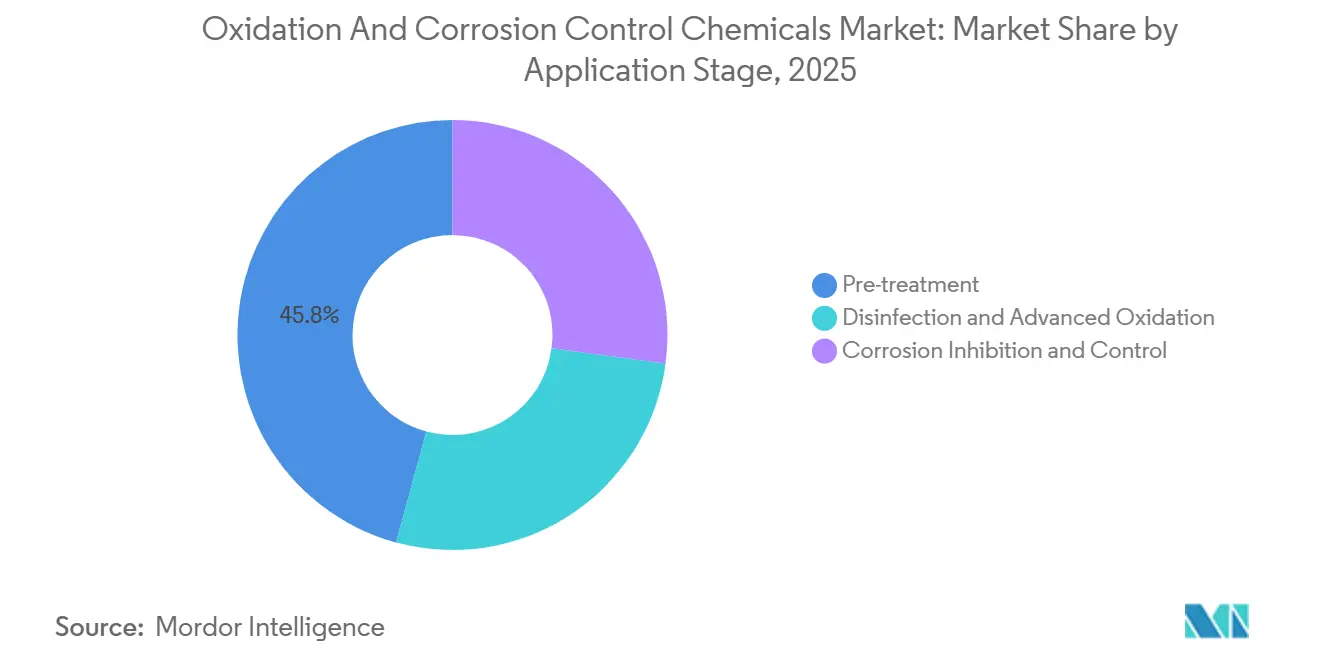

- By application stage, pre-treatment captured 45.77% of the Oxidation and Corrosion Control Chemicals market size in 2025; disinfection and advanced oxidation are projected to grow at an 8.06% CAGR over 2026-2031.

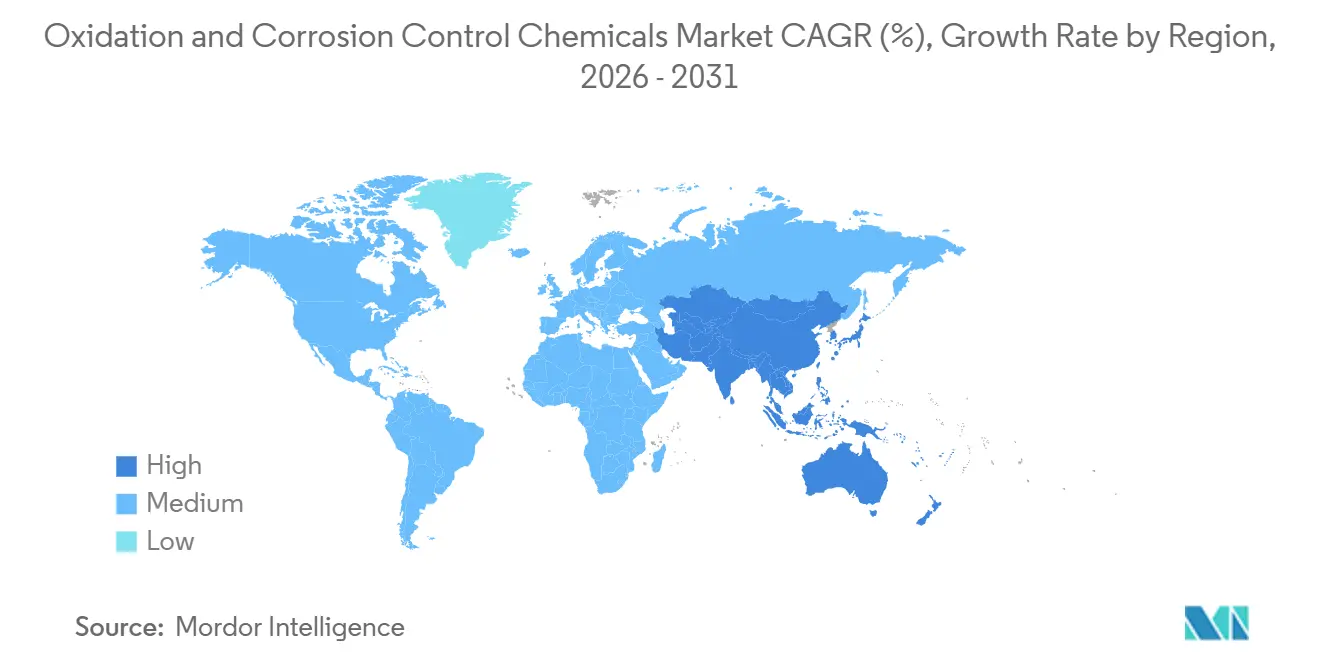

- By geography, Asia-Pacific held 40.33% of the Oxidation and Corrosion Control Chemicals market share in 2025 and is forecast to register an 8.30% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Oxidation And Corrosion Control Chemicals Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter global drinking-water and effluent regulations | +1.8% | Global, with early enforcement in EU, North America, and urban China | Short term (≤ 2 years) |

| Industrial expansion in water-intensive sectors | +1.5% | APAC core (China, India, Vietnam), spill-over to Middle East | Medium term (2-4 years) |

| Rising demand for advanced oxidation and corrosion-control solutions | +1.3% | North America, EU, Japan, South Korea | Medium term (2-4 years) |

| Municipal investment to replace aging water infrastructure | +1.1% | North America (US, Canada), Western Europe (Germany, UK, France) | Long term (≥ 4 years) |

| Accelerated adoption of ZLD systems in semiconductor fabs | +0.9% | Taiwan, South Korea, Japan, with emerging activity in Arizona and Germany | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stricter Global Drinking-Water and Effluent Regulations

Global chemical programs are undergoing a transformation due to tightening policies. In response to the EU Drinking Water Directive's reduction of the lead limit to 5 µg/L, utilities are increasing their dosing of orthophosphate and polyphosphate to create protective pipe scales[1]European Commission, “Directive (EU) 2020/2184 on Drinking Water,” ec.europa.eu. The U.S. EPA's Lead and Copper Rule Improvements mandate the replacement of lead service lines within a decade, driving a yearly phosphate demand surge through 2028. China's GB 5749-2022 standard expanded the range of covered contaminants and limited disinfection by-products. This has led plants to transition from using sodium hypochlorite to potassium permanganate and chlorine dioxide. In India, stricter turbidity and coliform thresholds under IS 10500:2012 have hastened the adoption of pre-oxidation in Jal Jeevan Mission schemes[2]Bureau of Indian Standards, “IS 10500:2012 Drinking Water Specification,” bis.gov.in. Collectively, these converging regulations set a durable compliance benchmark for the Oxidation and Corrosion Control Chemicals market.

Industrial Expansion and Semiconductor ZLD Adoption

Industrial water-treatment volumes are being driven by capacity additions in sectors like pulp, mining, power, and semiconductors. India's paper output saw an increase, leading to heightened use of hydrogen peroxide and corrosion inhibitors at newly established kraft mills. Vietnam's addition of coal capacity is set to uphold the demand for phosphate-based inhibitors in cooling loops. TSMC’s Fab 18 processes water using a ZLD circuit, dependent on hydrogen peroxide, chlorine dioxide, and HEDP-based inhibitors. Similarly, Samsung and Intel unveiled expansions in South Korea, Arizona, and Germany, emphasizing potassium permanganate and phosphate-free initiatives to adhere to ultrapure-water standards. These developments foster regional growth pockets that counterbalance the saturation seen in OECD markets.

Rising Demand for Advanced Oxidation and Corrosion-Control Solutions

Utilities are now layering UV treatments with hydrogen peroxide and potassium permanganate to comply with limits on PFAS and 1,4-dioxane. Responding to these challenges, the U.S. EPA set stringent caps on PFOA and PFOS at 4 ppt, pushing trials towards UV-sulfate radical processes, which have proven more effective than granular carbon. In Japan, the inclusion of 1,4-dioxane in the drinking-water list has hastened the adoption of UV-hydrogen peroxide systems in the impacted prefectures. Meanwhile, pharmaceutical facilities in Germany are turning to electrochemical oxidation, though they continue to pre-dose with chlorine dioxide to avert electrode fouling. On the corrosion front, Kemira’s polymer-modified phosphate is achieving a reduction in dosing, leading to significant logistics savings for distant utilities. These advancements are allowing for sustained premium pricing, even in a market that's sensitive to procurement costs.

Municipal Investment to Replace Aging Infrastructure

New asset designs in large capital programs now incorporate corrosion-control and oxidation chemistries. The U.S. Infrastructure Investment and Jobs Act allocates funding to water systems, designating a portion for lead line replacements and another for PFAS treatments. This move secures orders for phosphates and advanced oxidants. In 2025, Germany set aside funding to upgrade various plants and adhere to new nutrient caps, showing a preference for chlorine dioxide and hydrogen peroxide. Canada's infrastructure initiative earmarked funding for water renewals, specifically calling for NSF/ANSI 60-certified inhibitors. Ofwat greenlit a substantial expenditure in the U.K. for the 2025-2030 period, with a clear emphasis on bolstering corrosion-control resilience. These extensive, multi-year budgets not only stabilize demand but also shield suppliers from the fluctuations of industrial cycles.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory bans on selected oxidants and inhibitors | -0.7% | EU (phosphate detergent bans extended to industrial applications), select U.S. states | Medium term (2-4 years) |

| Technology shift to UV, membranes, and electro-chemical options | -0.5% | North America, Western Europe, Japan | Long term (≥ 4 years) |

| Manganese-ore supply-chain volatility hitting permanganate prices | -0.4% | Global, with acute impact in Asia-Pacific and North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Regulatory Bans on Selected Oxidants and Inhibitors

EU regulations are tightening their grip on phosphates, expanding from detergents to industrial uses. This shift is steering utilities towards organophosphonates, which can reduce phosphorus loading. In France, a bold move is underway: the nation aims for a phosphate cut by 2028 in its eutrophic basins. This initiative is poised to redirect demand towards polymer inhibitors. Meanwhile, in 2024, California added several chlorinated oxidants to its "chemicals-of-concern" roster. This action mandates plants to demonstrate that alternatives like chlorine dioxide or UV can match the disinfection efficacy before they can renew their permits. Additionally, while the volatility of manganese ore is driving up costs for permanganate use, the steep capital investments required for non-chemical substitutes are hindering swift transitions.

Technology Shift to UV, Membranes, and Electro-Chemical Options

Falling UV-LED costs and efficient electrochemical cells are enabling smaller utilities to cut chlorine use in disinfection. Japanese and South Korean plants now favor UV-LED reactors that cut energy and eliminate mercury lamps. Pharmaceutical sites in Germany and Switzerland deploy electrochemical advanced oxidation to avoid residual chlorine in effluent, while Singapore combines nanofiltration and reverse osmosis in compact membrane trains that need less pre-oxidation. Even so, chemical oxidants remain indispensable for iron and manganese removal and biofilm control, capping near-term displacement risk.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Corrosion Control Anchors Revenue as Oxidants Drive Growth

Corrosion-control chemicals represented 84.26% of 2025. This surge is attributed to the pressing need for continuous dosing of phosphates or organophosphonates in aging pipes and cooling systems, effectively curbing metal dissolution. While phosphates have traditionally dominated this segment, recent phase-downs in Europe are shifting the spotlight towards HEDP, PBTC, and polymer blends.

Oxidation technologies, while smaller, are growing at 7.94% each year, largely driven by stringent regulations on PFAS and 1,4-dioxane. In the realm of pre-oxidants, potassium permanganate is the go-to choice for taste-and-odor control in both China and India. However, in North America, sodium permanganate is carving out a larger market share due to its liquid handling advantages. As zero liquid discharge (ZLD) initiatives gain momentum, shipments of hydrogen peroxide to semiconductor fabs in Asia have increased. While sodium hypochlorite and chlorine dioxide continue to dominate price-sensitive municipal contracts, emerging technologies like UV and electrochemical methods are beginning to temper the growth of chlorinated oxidants in more established markets.

By End User: Industrial Dominance Meets Municipal Momentum

Industrial water treatment captured 62.18% of 2025 revenue, led by pulp, mining, power, and petrochemical sites that run closed-loop systems requiring relentless corrosion inhibition. India’s pulp mills, Vietnam’s new coal units, and Saudi petrochemical complexes are key growth engines that demand heavy phosphate and organophosphonate use.

Municipal demand, while smaller, is forecast to outpace industrial at a 7.07% CAGR through 2031. U.S. lead line replacement, India’s Jal Jeevan Mission roll-outs, and China’s GB 5749 upgrades are driving bulk orders for orthophosphate, potassium permanganate, and chlorine dioxide. This fast-moving municipal pipeline diversifies revenue streams for suppliers that traditionally leaned on industrial volumes.

By Application Stage: Pre-Treatment Anchors Volume, Disinfection Leads Growth

Pre-treatment held a 45.77% share in 2025, reflecting its universal role in iron, manganese, and sulfide removal before downstream processes. Plants dose potassium permanganate at up to 5 mg/L to avoid trihalomethanes, while Japan and South Korea pilot UV-hydrogen peroxide to break down taste-and-odor compounds.

Disinfection and advanced oxidation is the fastest-growing slice at 8.06% CAGR. Chlorine dioxide use is accelerating because it produces fewer by-products than sodium hypochlorite, and UV-sulfate radical systems are gaining footholds at PFAS-impacted sites in the United States. Corrosion inhibition remains resilient at roughly half of total spend, bolstered by new pipe networks that must meet updated lead rules in North America and Europe.

Geography Analysis

Asia-Pacific leads with a 40.33% 2025 share and an expected 8.30% CAGR to 2031, driven by China’s GB 5749 compliance, India’s rural water build-out, and semiconductor ZLD investments in Taiwan, South Korea, and Japan. Regional pulp, mining, and power projects add further impetus.

North America is on track to secure significant revenue. Demand for corrosion-control chemicals is bolstered by infrastructure acts in the U.S. and Canada, while PFAS regulations drive the adoption of UV-hydrogen peroxide. Furthermore, Mexico's automotive corridor contributes to the rising industrial volumes.

Europe is poised to capture a notable share of the sales. In Germany and the UK, capital programs are emphasizing chlorine dioxide, hydrogen peroxide, and phosphate inhibitors. Meanwhile, France's push for phosphate reductions leans towards organophosphonates, and desalination efforts in the Mediterranean present opportunities for high-salinity corrosion inhibitors.

South America, along with the Middle-East and Africa, rounds out the market. Brazil's sanitation initiatives and Argentina's mining expansion are sustaining demand for oxidants. Concurrently, Saudi Arabia's petrochemical sector and upgrades to South African plants are ensuring a steady stream of orders for corrosion inhibitors.

Competitive Landscape

The oxidation and corrosion control chemicals market is moderately fragmented. Regional challengers in China and India supply cost-competitive organophosphonates that comply with local discharge rules, pressuring global players on price. Technology disruptors are bundling membranes with advanced oxidation to cut overall chemical use, especially in decentralized plants. Semiconductor fabs remain a lucrative niche because buyers value high-purity oxidants and corrosion solutions that protect multimillion-dollar equipment.

Oxidation And Corrosion Control Chemicals Industry Leaders

Ecolab Inc.

Kemira

Solenis

Veolia

Veralto

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Arkema inaugurated a capacity expansion at Changshu that boosts organic peroxide output 2.5× for the Luperox® range, serving renewables growth.

- January 2025: Arkema reorganized to refocus on hydrogen peroxide, chlorate, and perchlorate after a salt-supply disruption, strengthening its core oxidation portfolio.

Global Oxidation And Corrosion Control Chemicals Market Report Scope

Oxidation and corrosion control chemicals are specialized agents designed to manage, reduce, or prevent material deterioration, particularly in metals, and to treat water by promoting beneficial oxidation reactions, such as disinfection, or inhibiting harmful corrosion processes. These chemicals are categorized based on their chemical composition and the industries that utilize them.

The oxidation and corrosion control chemicals market is segmented by product type, end-user industry, application stage, and geography. By product type, the market is segmented into oxidation technologies (potassium permanganate, sodium permanganate, hydrogen peroxide, chlorine and its compounds, and other oxidizing agents) and corrosion-control chemicals (phosphates and other corrosion inhibitors). By end-user industry, the market is segmented into municipal water treatment and industrial water treatment (pulp and paper, mining, power generation, oil and gas, chemicals and petrochemicals, food and beverage processing, and other industrial applications). By application stage, the market is segmented into pre-treatment, disinfection and advanced oxidation, and corrosion inhibition and control. The report also covers the market size and forecasts in 16 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of revenue (USD).

| Oxidation Technologies | Potassium Permanganate |

| Sodium Permanganate | |

| Hydrogen Peroxide | |

| Chlorine and Chlorine Compounds | |

| Other Oxidising Agents | |

| Corrosion-Control Chemicals | Phosphates |

| Other Corrosion Inhibitors |

| Municipal Water Treatment | |

| Industrial Water Treatment | Pulp and Paper |

| Mining | |

| Power Generation | |

| Oil and Gas | |

| Chemicals and Petrochemicals | |

| Food and Beverage Processing | |

| Other Industrial Applications |

| Pre-treatment |

| Disinfection and Advanced Oxidation |

| Corrosion Inhibition and Control |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Product Type | Oxidation Technologies | Potassium Permanganate |

| Sodium Permanganate | ||

| Hydrogen Peroxide | ||

| Chlorine and Chlorine Compounds | ||

| Other Oxidising Agents | ||

| Corrosion-Control Chemicals | Phosphates | |

| Other Corrosion Inhibitors | ||

| By End-user Industry | Municipal Water Treatment | |

| Industrial Water Treatment | Pulp and Paper | |

| Mining | ||

| Power Generation | ||

| Oil and Gas | ||

| Chemicals and Petrochemicals | ||

| Food and Beverage Processing | ||

| Other Industrial Applications | ||

| By Application Stage | Pre-treatment | |

| Disinfection and Advanced Oxidation | ||

| Corrosion Inhibition and Control | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current demand for oxidation and corrosion control chemicals, and their expected growth by 2031?

Worldwide consumption is USD 16.76 billion in 2026 and is projected to reach USD 23.37 billion by 2031, reflecting a 6.88% CAGR.

How fast is demand expected to rise for oxidation and corrosion chemicals in the Asia-Pacific?

Asia-Pacific revenue is projected to climb at 8.30% CAGR through 2031 as China, India, and semiconductor hubs expand treatment capacity.

Which product group currently generates the most revenue?

Corrosion-control chemicals led with 84.26% of 2025 sales, reflecting ongoing pipe and equipment protection needs.

What drives the strongest growth in the municipal segment?

Lead service-line replacement and PFAS rules in the United States, plus rural supply programs in India, are spurring adoption of phosphates and advanced oxidants.

How are semiconductor fabs influencing chemical selection?

Ultrapure water and ZLD requirements push fabs to specify high-purity hydrogen peroxide, chlorine dioxide, and phosphate-free inhibitors that resist chloride stress cracking.

Which regulations most affect product formulation in Europe?

The EU Drinking Water Directive and expanding phosphate phase-downs are steering utilities toward organophosphonates and polymer blends with lower phosphorus loading.

What substitution technologies pose a risk to chlorine-based oxidants?

Falling UV-LED and electrochemical oxidation costs allow small plants to meet disinfection targets with fewer chemicals, though oxidants remain essential for iron and manganese removal.

Page last updated on: