OTT Kids Content Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 23.97 Billion |

| Market Size (2031) | USD 36.42 Billion |

| Growth Rate (2026 - 2031) | 8.73% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

OTT Kids Content Market Analysis by Mordor Intelligence

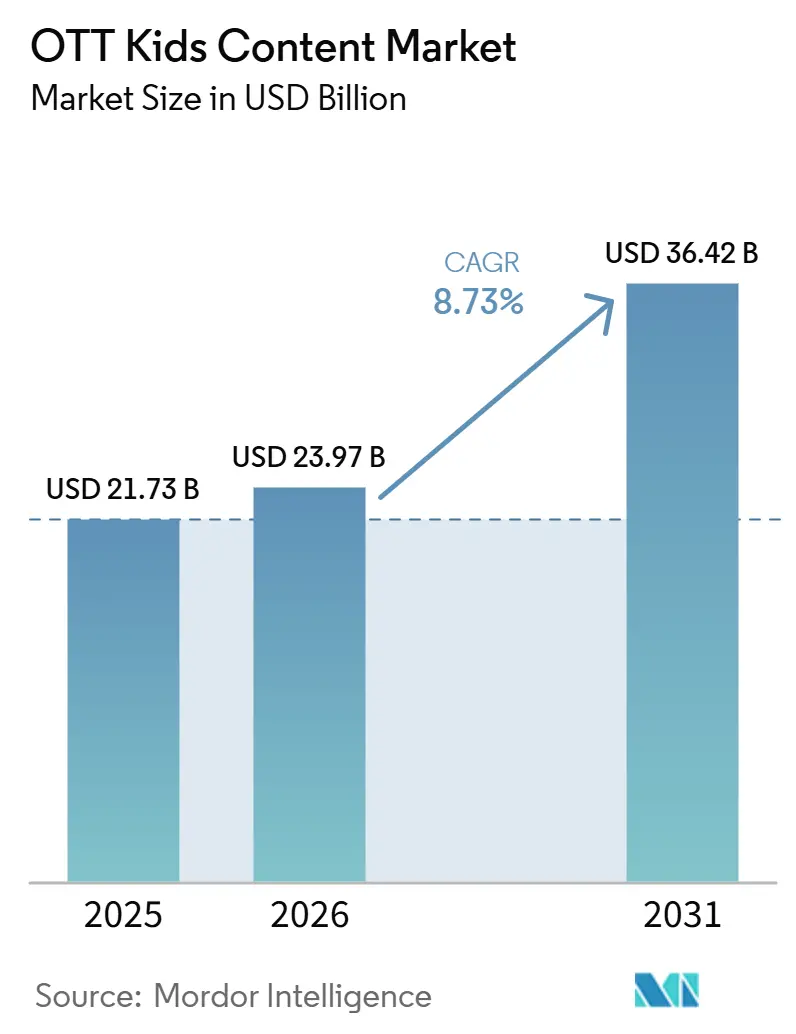

The OTT kids content market size is projected to expand from USD 21.73 billion in 2025 and USD 23.97 billion in 2026 to USD 36.42 billion by 2031, registering a CAGR of 8.73% between 2026 and 2031. The OTT kids content market is growing as parents place greater weight on safe viewing, age-appropriate curation, and controlled digital environments for children. The OTT kids content market is also benefiting from a shift toward educational and interactive viewing, as families increasingly treat screen time as a mix of entertainment, learning, and routine engagement. Device behavior is changing at the same time, with mobile viewing still large in scale and connected home viewing becoming more important for shared family use. Competition in the OTT kids content market is therefore centered on trusted brands, exclusive franchises, depth in regional languages, and product features that keep children engaged without weakening parental confidence. The strongest near-term opportunity in the OTT kids content market lies with platforms that can balance premium intellectual property, interactive formats, and localized libraries while managing tighter child privacy and advertising rules.

Key Report Takeaways

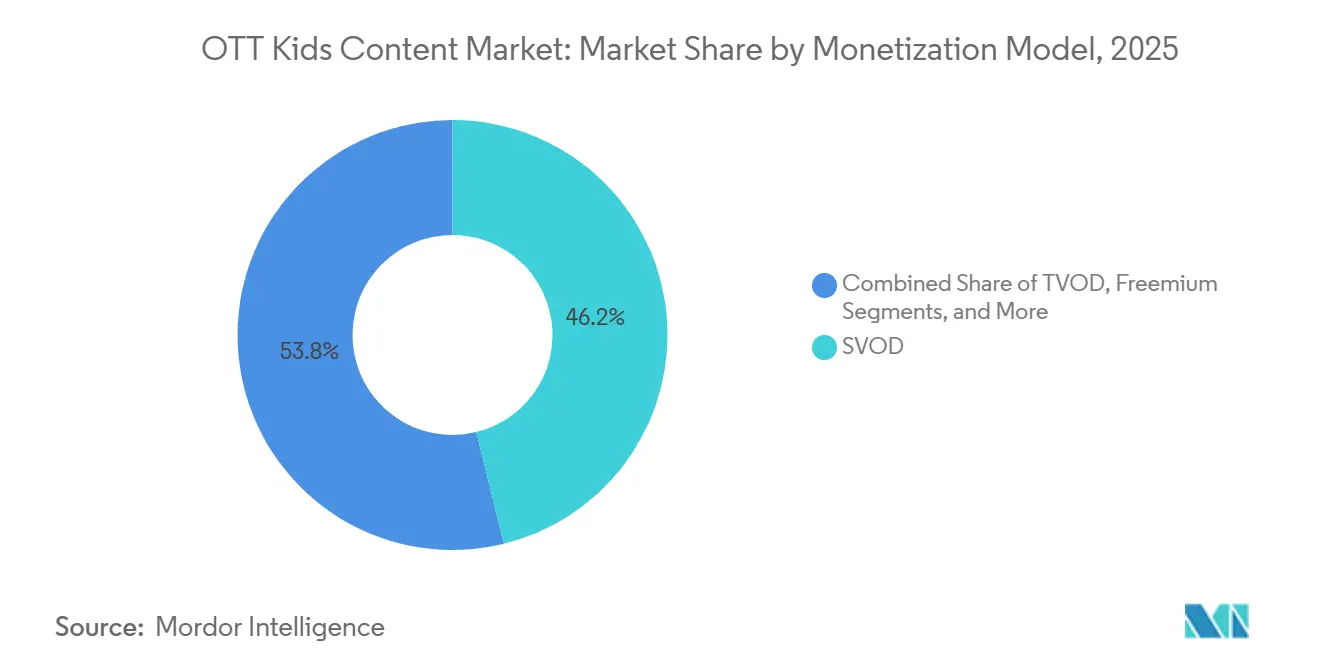

- By monetization model, SVOD held 46.17% of the OTT kids content market share in 2025, while the freemium segment is projected to expand at a 9.57% CAGR through 2031.

- By genre, animation and cartoons accounted for 68.81% of the OTT kids content market size in 2025, while interactive and gamified content is expected to grow at a 10.12% CAGR through 2031.

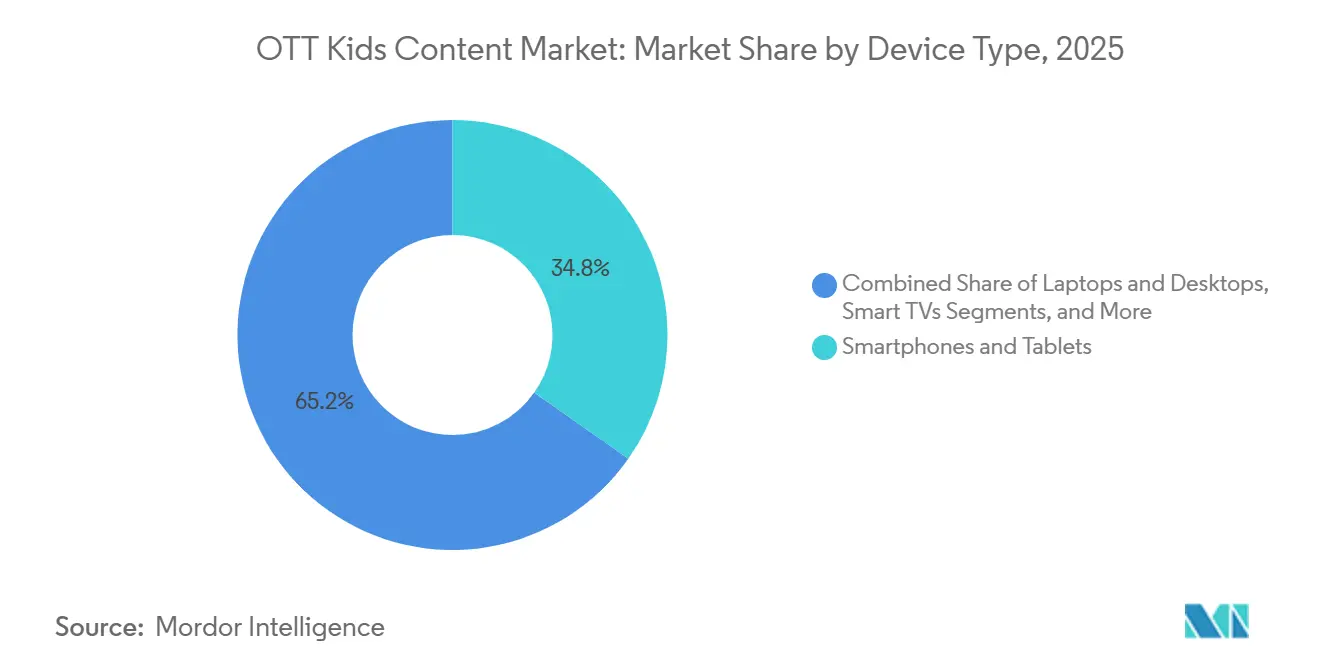

- By device type, smartphones and tablets led with a 34.77% share in 2025, while smart TVs are projected to grow at a CAGR of 10.34% during 2026-2031.

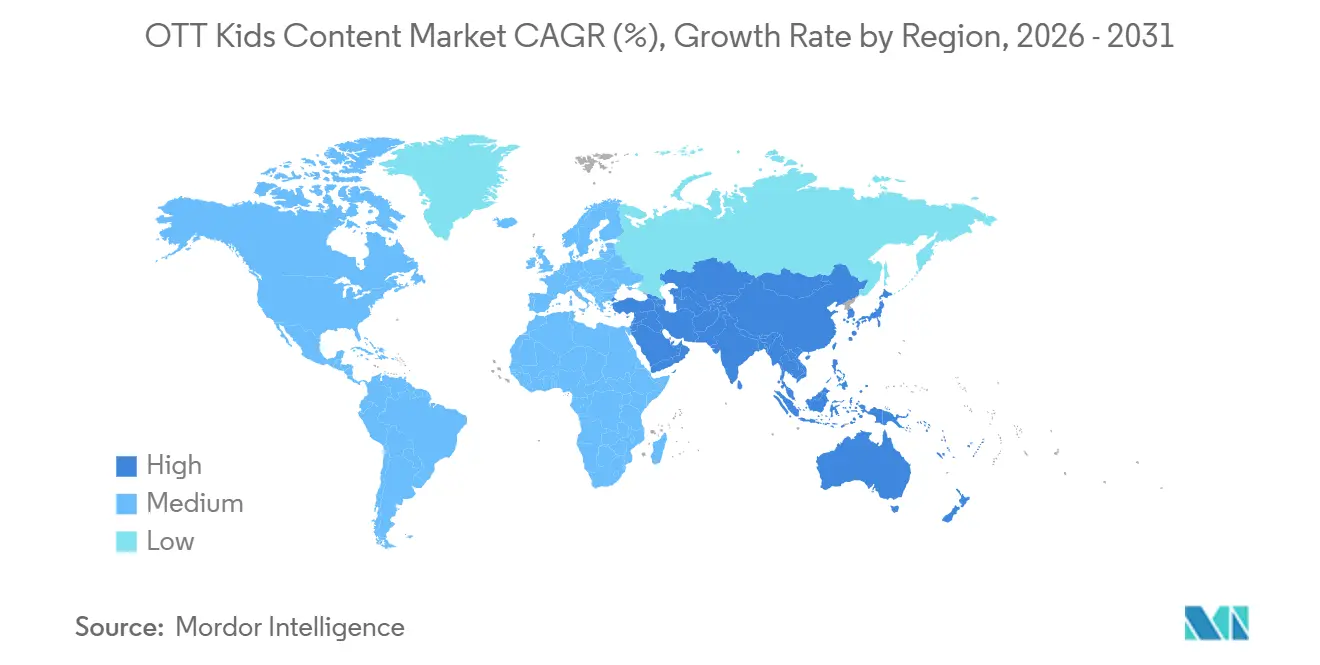

- By geography, North America captured 38.69% of global revenue in 2025, while Asia-Pacific is projected to expand at a 10.56% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global OTT Kids Content Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Parental Demand for Safe, Curated Kids Streaming | +2.1% | Global, with the highest intensity in North America and Europe | Short term (≤ 2 years) |

| Rising Educational Streaming Consumption Across Households | +1.8% | Global, with an early-stage surge in Asia-Pacific and South America | Medium term (2-4 years) |

| Accelerating Connected TV and Tablet Penetration in Family Homes | +1.6% | Global, core gains in North America, with spillover to Asia-Pacific and Middle East, and Africa | Short term (≤ 2 years) |

| Platform Differentiation Through Franchised Kids IP and Exclusive Originals | +1.2% | North America, Europe, and high-ARPU Asia-Pacific markets | Medium term (2-4 years) |

| Growth of Ad-Supported and Freemium Kids Monetization Models | +1.0% | Asia-Pacific core, with spillover to South America and Middle East, and Africa | Medium term (2-4 years) |

| Expansion of Localization and Regional Language Kids' Libraries | +0.8% | South America, Asia-Pacific, and the Middle East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Parental Demand for Safe, Curated Kids Streaming

Parental concern around digital safety has become one of the clearest demand signals in the OTT kids content market. A 2026 Lingokids survey found that 98% of U.S. parents surveyed allowed daily screen time for young children, while 87.7% ranked content safety as their top concern, and 84.6% reported some degree of screen time guilt.[1]Lingokids, “Kids Interactive Entertainment Report 2026,” Lingokids, lingokids.com That pattern is pushing households toward services where content selection, profile controls, and viewing environments feel more predictable. The OTT kids content market is, therefore, rewarding platforms that present trust as part of the product, not as an extra setting hidden in the interface. Dedicated children’s services and carefully managed kids zones have a stronger basis for retention because parents are more willing to permit repeat viewing in those environments. This makes safety and curation a direct commercial advantage, especially when parents compare closed libraries with open video platforms.

Rising Educational Streaming Consumption Across Households

Educational viewing is taking a larger role in the OTT kids content market as parents look for media that supports learning without fully replacing entertainment. Lingokids reported in 2026 that 64.8% of surveyed parents placed educational or skill-building value among their top 3 content priorities. That preference is changing how children’s libraries are designed because parents now expect songs, stories, games, and character-led activities to serve a learning purpose. The line between educational and entertainment apps is becoming less rigid when children engage with content independently and complete activities willingly. The OTT kids' content market is responding with more blended formats that use familiar characters to deliver literacy, language, and social development content. This shift supports platforms that can combine curriculum value with repeatable play patterns rather than relying only on passive episode viewing.

Accelerating Connected TV and Tablet Penetration in Family Homes

The device mix behind the OTT kids content market is broadening as family viewing extends across handheld and household screens. Smartphones and tablets remain important because they fit daily routines, travel needs, and mobile-first usage habits in many countries. At the same time, large-screen connected viewing is becoming increasingly relevant, as parents often prefer co-viewing in shared spaces rather than isolated use on personal devices. This raises the value of interfaces that are simple for children to use and clear for adults to supervise. The OTT kids content market is also seeing a stronger role for living room discovery because franchises gain more visibility when watched together by siblings and parents. As more families split their usage across mobile devices and smart TVs, platforms need content and product design that works well in both settings.

Platform Differentiation Through Franchised Kids IP and Exclusive Originals

Exclusive franchises remain one of the strongest tools for competitive separation in the OTT kids content market. In 2026, Netflix expanded its children’s lineup and introduced Playground, a kids' games app bundled with memberships, linking recognizable characters with interactive play rather than relying solely on streaming. This kind of strategy matters because children often return to known characters, while parents see familiar franchises as lower-risk viewing choices. When a platform controls long-running brands or secures multi-year access, it gains a stronger hold on family retention and cross-format engagement. The OTT kids content market is therefore moving toward deeper franchise ecosystems that connect series, shorts, games, and consumer products. That trend favors companies with strong intellectual property pipelines and makes renewal cycles more important for platforms that depend heavily on licensed content.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Content Production and Localization Costs for Kids Originals | -1.5% | Global, with the greatest pressure on North America and Europe-based producers | Short term (≤ 2 years) |

| Tightened Child Safety, Privacy, and Advertising Compliance | -1.2% | North America and Europe as core markets, with spillover to India, South Africa, and Brazil | Short-term (≤ 2 years) and medium-term (2-4 years) |

| Discoverability Friction in Fragmented Streaming Environments | -0.7% | Global, with an acute impact on markets with high FAST channel proliferation | Medium term (2-4 years) |

| Revenue Leakage from Platform Substitution and Free-Content Competition | -0.5% | Global, with the highest exposure in Asia-Pacific and South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Content Production and Localization Costs for Kids Originals

Production cost pressure is one of the most important limits on expansion in the OTT kids content market. Premium animation, especially series built for global release, requires large budgets, long development cycles, and steady creative investment before returns are visible. Cost pressure rises further when platforms localize shows into many languages because dubbing, scripting changes, and cultural adaptation all add expense. The OTT kids content market is, therefore, easier for companies that can spread those costs across merchandise, licensing, and multiple distribution windows. Smaller producers and regional specialists face a harder path when they need depth of original content but lack the scale to absorb the costs of global rollout. This cost divide is likely to strengthen the position of large owners of children’s intellectual property.

Tightened Child Safety, Privacy, and Advertising Compliance

Tighter child privacy rules are adding operational pressure across the OTT kids content market. The U.S. Federal Trade Commission finalized changes to the COPPA Rule in January 2025, with full compliance required by April 22, 2026, including separate verifiable parental consent for targeted advertising and stronger limits on data use and retention. These changes reduce the flexibility of platforms that once relied on targeted digital advertising to support free access. The effect is especially important for mid-tier services because compliance costs do not fall evenly across the market. The OTT kids content market is therefore becoming harder for companies that lack legal, technical, and moderation resources at scale. As privacy obligations tighten across several regions, subscription and contextual monetization become more practical than aggressive ad targeting in children’s environments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Monetization Model, SVOD Leads Revenue While Freemium Closes the Access Gap

SVOD captured 46.17% of segment revenue in 2025, giving it the largest position in the OTT kids content market. That lead reflects a household preference for ad-free access, stable curation, and predictable viewing rules for children. In many families, subscription payments are seen as a trade-off for lower exposure to unsuitable ads, reduced discovery risk, and stronger parental controls. This gives the subscription tier a strong foundation even when consumers review entertainment spending more closely. The SVOD portion of the OTT kids content industry also benefits from the fact that children often rewatch familiar content, which supports retention better than one-time adult viewing.

Freemium is the fastest-growing monetization segment, with the OTT kids content market size for this segment projected to expand at a 9.57% CAGR through 2031. Its appeal is different from classic advertising-led video because the model uses free access to build reach, then reserves deeper libraries, extra features, or ad-free experiences for paying households. That approach is useful in price-sensitive countries where families may hesitate to commit to a full monthly subscription at the outset. In the OTT kids content market, freemium also works as a bridge between discovery and paid conversion, especially when a platform already has strong character recognition. The model becomes more effective when companies can combine open access with careful curation rather than leaving discovery entirely to external platforms.

By Genre, Animation Dominates While Interactive Content Redefines Viewer Engagement

Animation and cartoons held 68.81% of the segment in 2025, making them the core content base of the OTT kids content market. Animated titles travel well across age groups and geographies because they can be dubbed more easily and often rely on repeatable visual storytelling. They also support stronger licensing ecosystems because characters can move into toys, books, live events, and branded learning products. This reinforces the role of animation as the safest large-scale investment format for children’s services. The OTT kids content market has, therefore, kept franchise animation at the center of both revenue generation and long-term platform identity.

Interactive and gamified content is set to grow faster than any other genre, with a forecast CAGR of 10.12% through 2031. Lingokids reported in 2026 that 63% of children's screen time ages 3-8 in its dataset was interactive rather than passive, showing how quickly engagement habits are changing. Netflix moved in the same direction in April 2026, launching Playground with children’s titles tied to familiar characters, extending engagement beyond linear viewing. The OTT kids content market is responding because interactive play supports both character discovery and longer session depth. That makes gamified content a useful extension for platforms that want stronger retention without relying only on constant episode volume.

By Device Type, Mobile Consumption Holds Scale While Smart TVs Capture Growth

Smartphones and tablets accounted for 34.77% of usage-based device revenue in 2025, maintaining their leading position in the OTT kids content market. Their lead is tied to portability, everyday convenience, and broad relevance in mobile-first countries where personal devices are the most reliable screen. They also remain important in homes with shared living arrangements because children can access content without needing the main television. Educational use also supports mobile demand, as parents often hand over tablets for structured learning sessions or short, supervised viewing blocks. This keeps handheld devices central to the OTT kids content market even as living room streaming expands.

Smart TVs are the fastest-growing device category, with the OTT kids content market size for smart TVs projected to advance at a 10.34% CAGR through 2031. Moonbug reinforced this direction in April 2026 when it launched The Moonbug Channel with KPN in Western Europe, bringing major children’s brands into a dedicated channel environment built for household viewing.[2]Moonbug Entertainment, “KPN and Moonbug Launch The Moonbug Channel,” Moonbug Entertainment, moonbug.com Large-screen viewing supports co-viewing, easier parental observation, and stronger franchise visibility within the home. In the OTT kids content market, that makes smart TVs an increasingly important environment for discovery, repeat viewing, and family-level retention. The result is a two-screen structure where handheld devices keep daily reach high while smart TVs carry more of the shared viewing experience.

Geography Analysis

North America held 38.69% of the OTT kids content market share in 2025, making it the largest regional contributor. The region benefits from deep household familiarity with paid streaming, broad franchise awareness, and high acceptance of subscription stacking within families. It also has a strong base of global platform operators, established children’s brands, and mature digital payment behavior. These conditions support premium pricing and make children’s programming a meaningful retention tool within broader streaming bundles. The OTT kids content market in North America is therefore driven more by engagement depth and content quality than by first-time household acquisition alone.

Europe remained the second-largest regional segment in the OTT kids content market, supported by a long tradition of public broadcasting and locally trusted children’s content. The region differs from North America because it combines established global platforms with country-specific viewing habits and stronger local language expectations. That raises the importance of dubbing, cultural fit, and public service credibility in children’s programming. WildBrain expanded its Sesame Workshop representation into the Nordic markets in July 2025, showing that specialist children’s intellectual property continues to attract investment in the region.

Asia-Pacific is the fastest-growing region, with the OTT kids content market size in the region projected to rise at a 10.56% CAGR through 2031. Growth is being led by large digital populations, rising streaming acceptance, and the need for content in several major languages within the same national markets. The OTT kids content market is especially dynamic in India, where scale, price sensitivity, and language diversity push platforms toward flexible content and product strategies. JioStar launched a conversational streaming interface for JioHotstar in February 2026, showing how operators in the region are using product innovation to improve content discovery across large libraries.[3]JioStar, “JioHotstar Launches ChatGPT-Branded Conversational Streaming in India,” JioStar, jiostar.com Asia-Pacific also benefits from strong export potential in children’s intellectual property, especially where studios build formats that can travel across regional and global audiences.

Competitive Landscape

The OTT kids content market is moderately concentrated, with Disney, Netflix, Amazon, and Alphabet holding a strong position in global family viewing, while specialist children’s platforms still compete on trust, format focus, and local relevance. Large, diversified players benefit from broad content budgets, well-known characters, and the ability to spread children’s programming across broader entertainment ecosystems. That gives them a clear retention advantage when parents want fewer apps with deeper, more reliable content. At the same time, the OTT kids content market still leaves room for focused operators that can move faster in niche genres, local language production, or free discovery models. This balance keeps the market from becoming fully consolidated even though global leaders remain highly visible.

Netflix has used product expansion as a strategic move inside the OTT kids content market, especially through its April 2026 launch of Playground, which tied games and character engagement to the existing membership base. Sesame Workshop also expanded distribution in January 2026 by bringing hundreds of full Sesame Street episodes to YouTube, extending reach while keeping the brand active in digital-first environments. Moonbug added another example in April 2026 through its KPN partnership for The Moonbug Channel, which strengthened linear and streaming presence in Western Europe. These moves show that major companies are not relying on a single route to growth. Instead, the OTT kids content market is being shaped by a mix of subscription bundling, free discovery, and cross-platform franchise expansion.

Specialist and mid-tier players remain relevant when they control strong characters or operate effectively across several viewing channels. WildBrain expanded its YouTube content-sharing partnership with Banijay Kids and Family in March 2026, reflecting a clear focus on extending children’s franchise reach through ad-supported digital video as well as premium distribution. Kartoon Studios reported 21% revenue growth in 2025, showing that smaller operators can still scale with a multi-format distribution strategy when they manage content carefully.[4]Kartoon Studios, “Kartoon Studios Reports 21% Revenue Growth in 2025,” Kartoon Studios Investor Relations, ir.kartoonstudios.com The OTT kids content market therefore favors scale, but it does not exclude focused companies that can use owned intellectual property, disciplined partnerships, and channel diversity to stay commercially viable. The biggest gap remains in localized interactive content for non-English audiences, where global giants and smaller specialists are still building out their long-term positions.

OTT Kids Content Industry Leaders

The Walt Disney Company

Netflix, Inc.

Alphabet Inc.

Amazon.com, Inc.

Paramount Skydance Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Netflix acquired two additional seasons, Seasons 8 and 9, of animated hit Masha and the Bear and extended rights to prior seasons and spin-offs across 100+ countries including the United States, Canada, France, Nordic and Benelux markets, India, Japan, South Korea, Malaysia, the Middle East, and South America, reinforcing its commitment to globally distributed kids franchise IP.

- May 2026: Moose Toys and Netflix expanded their master toy partnership to cover new animated series Young MacDonald and an animated film adaptation of Charlie and the Chocolate Factory, signaling a deeper link between streaming strategy and consumer products licensing.

- May 2026: Lingokids released its Kids Interactive Entertainment Report 2026, drawing on usage data from 20 million monthly users and surveys of over 2,000 U.S. parents, finding that 63% of children's screen time ages 3-8 was interactive and that parental safety concerns rose 14.3 percentage points year over year.

- March 2026: Banijay Kids and Family and WildBrain expanded their content-sharing partnership to distribute premium kids' intellectual property across both companies’ YouTube channels globally, targeting combined reach expansion for properties including Bluey, Miraculous Ladybug, and WildBrain’s own franchises.

Global OTT Kids Content Market Report Scope

The OTT Kids Content Market covers the creation, distribution, and monetization of children-focused video content delivered through over-the-top streaming platforms, including subscription-based, advertising-supported, and transactional services. The market includes animated shows, educational programs, movies, live-action series, and other age-appropriate digital content for children, accessible on connected TVs, smartphones, tablets, and other internet-enabled devices.

The OTT Kids Content Market Report is Segmented by Monetization Model (SVOD, AVOD, TVOD, Hybrid, and Freemium), Genre (Animation and Cartoons, Educational and Learning, Interactive and Gamified Content, and Other Genres), Device Type (Smartphones and Tablets, Smart TVs, Laptops and Desktops, and Other Device Types), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| SVOD |

| AVOD |

| TVOD |

| Hybrid |

| Freemium |

| Animation and Cartoons |

| Educational and Learning |

| Interactive and Gamified Content |

| Other Genres |

| Smartphones and Tablets |

| Smart TVs |

| Laptops and Desktops |

| Other Device Types |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Monetization Model | SVOD | |

| AVOD | ||

| TVOD | ||

| Hybrid | ||

| Freemium | ||

| By Genre | Animation and Cartoons | |

| Educational and Learning | ||

| Interactive and Gamified Content | ||

| Other Genres | ||

| By Device Type | Smartphones and Tablets | |

| Smart TVs | ||

| Laptops and Desktops | ||

| Other Device Types | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of OTT kids content?

The OTT kids content market size was USD 21.73 billion in 2025, is projected at USD 23.97 billion in 2026, and is forecast to reach USD 36.42 billion by 2031 at an 8.73% CAGR.

Which monetization model leads children’s streaming revenue?

SVOD led revenue with a 46.17% share in 2025 because families continue to value ad-free access, stronger curation, and safer viewing environments.

Which content genre is growing fastest for children’s streaming platforms?

Interactive and gamified content is projected to grow fastest at a 10.12% CAGR through 2031, supported by rising child engagement with game-based and activity-led formats.

Why do parents prefer dedicated kids streaming environments?

Parents are placing greater emphasis on safety, content control, and age-appropriate curation, which supports platforms that can offer trusted kids libraries and clear parental tools.

Which device category is driving the next stage of growth?

Smart TVs are projected to grow fastest at a 10.34% CAGR through 2031, while smartphones and tablets still held the largest 2025 share at 34.77%.

Which region is expected to expand fastest through 2031?

Asia-Pacific is expected to record the fastest growth at a 10.56% CAGR, supported by large digital audiences, language diversity, and expanding family streaming adoption.

Page last updated on: