OTT Documentary Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 15.69 Billion |

| Market Size (2031) | USD 22.76 Billion |

| Growth Rate (2026 - 2031) | 7.72% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

OTT Documentary Market Analysis by Mordor Intelligence

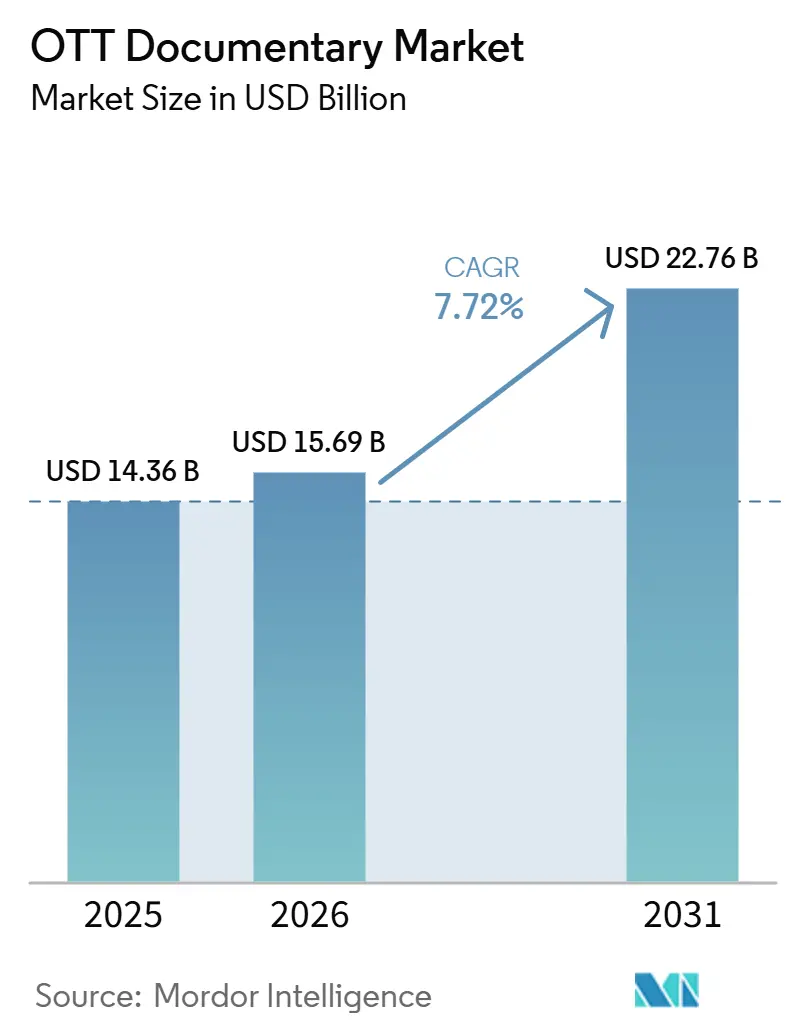

The OTT documentary market size was valued at USD 14.36 billion in 2025 and is projected to reach USD 22.76 billion by 2031, at a CAGR of 7.72% from 2026 to 2031. Growth continued because factual programming gave platforms a practical way to hold viewing time while managing tighter content budgets and lower tolerance for expensive scripted misses. The OTT documentary market also benefited from the shift toward exclusive nonfiction libraries, because platforms increasingly treated documentaries as a retention tool rather than as secondary catalog support. Another important change came from ad-supported tiers, where documentary audiences aligned well with brand-safe inventory and premium advertiser targeting. Competitive activity is increasingly centered on rights-backed partnerships, selective platform acquisitions, and wider reuse of documentary IP across subscription, advertising, and licensing channels. The strongest opportunity set remains in localized nonfiction libraries, smarter smart-TV discovery, and science-led programming that can extend engagement without taking on the scripted-style production risk.

Key Report Takeaways

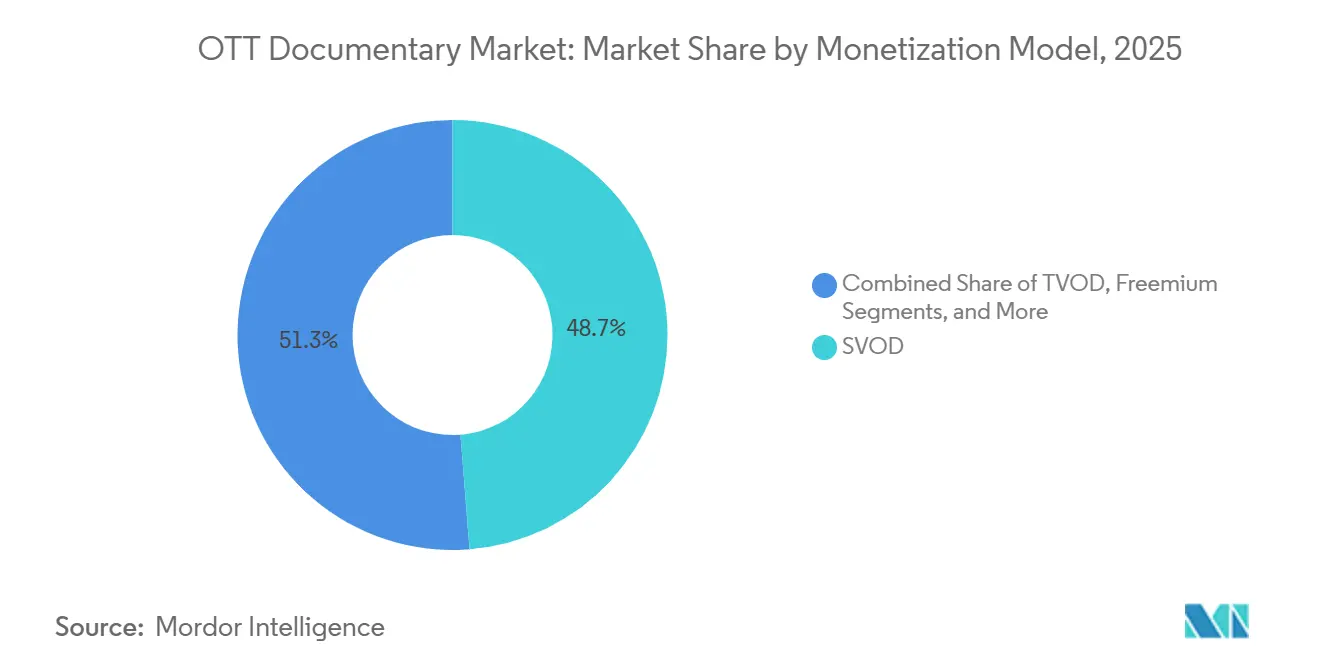

- By monetization model, SVOD held 48.74% of the OTT documentary market share in 2025, while the Hybrid tier is projected to expand at an 8.52% CAGR through 2031.

- By device type, Smartphones and Tablets accounted for 47.21% in 2025, while Smart TVs are projected to record the highest CAGR of 8.65% through 2031.

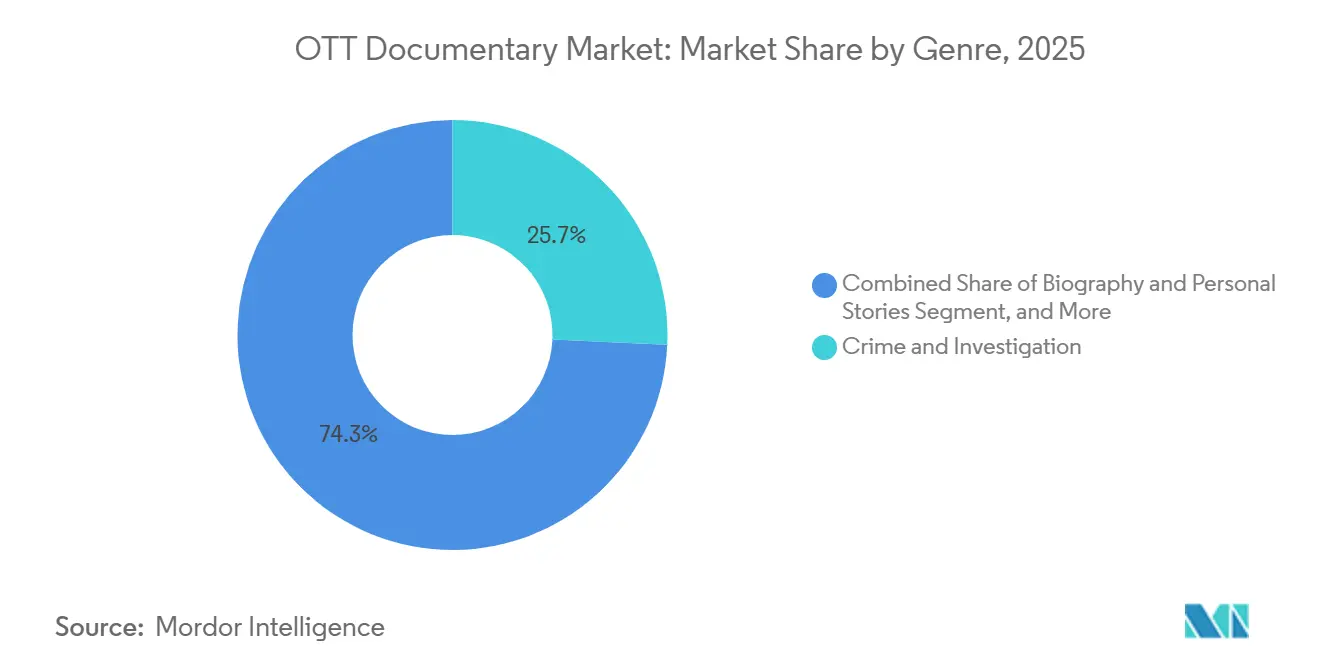

- By genre, Crime and Investigation accounted for 25.72% of revenue share in 2025, while Science and Technology is expected to grow at a 9.14% CAGR through 2031.

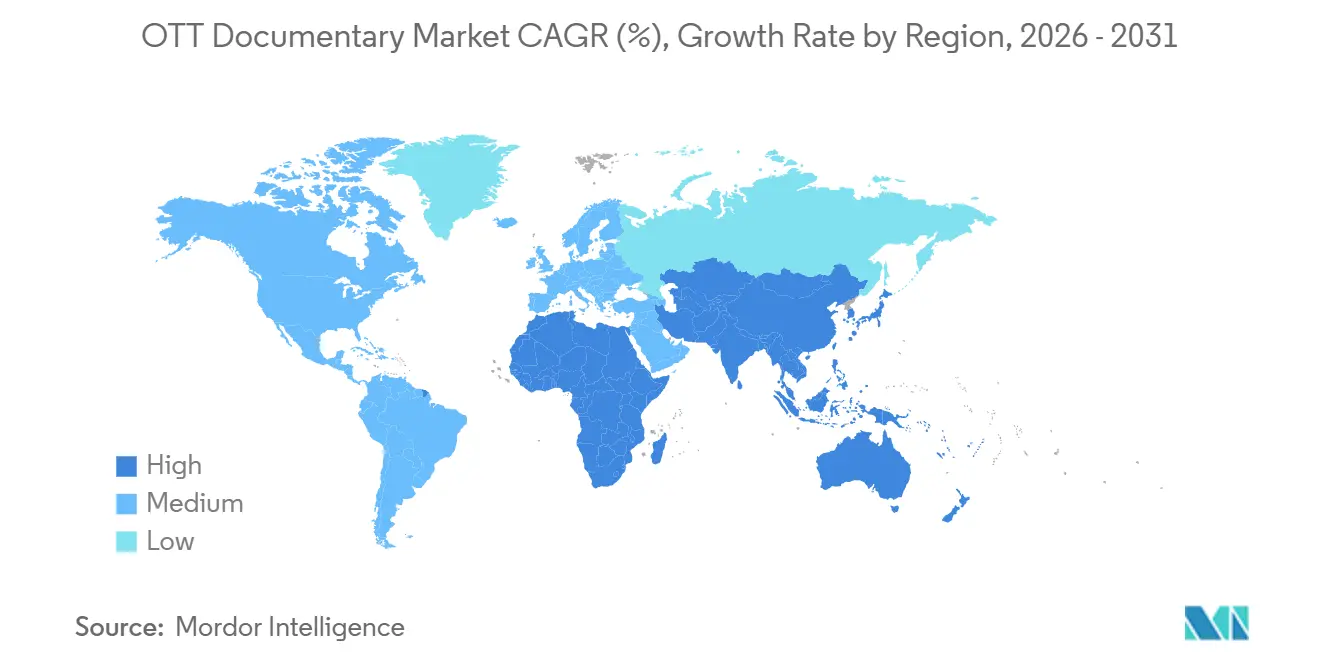

- By geography, North America accounted for 36.59% share in 2025, while Asia-Pacific is projected to grow at the fastest CAGR of 8.47% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global OTT Documentary Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Premium Long-Form Factual Content | +2.1% | Global | Medium term (2-4 years) |

| Exclusive Documentary Library Differentiation | +1.8% | Global, led by North America and Europe | Medium term (2-4 years) |

| Ad-Supported Inventory for Niche Audiences | +1.5% | Global, strongest in Asia-Pacific and South America | Short term (≤ 2 years) |

| Lower Production Risk Than Scripted Originals | +1.0% | Global | Short term (≤ 2 years) |

| International Demand for Localized True-Story Programming | +0.7% | Asia-Pacific, Middle East and Africa, South America | Long term (≥ 4 years) |

| Format Flexibility Across Documentary Lengths | +0.5% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Premium, Long-Form Factual Streaming Content

Premium factual viewing shifted from occasional prestige consumption to repeat mainstream use across the OTT documentary market, especially on platforms that needed reliable engagement without relying solely on expensive scripted launches. Netflix's H2 2025 engagement data showed that Sean Combs: The Reckoning drew 51 million views and Unknown Number: The High School Catfish reached 57 million views, which placed documentary titles much closer to mid-tier scripted performance than many buyers had expected.[1]Netflix, “Netflix Engagement Report - July to December 2025,” TV Central, tvcentral.com.au That viewing pattern matters because the OTT documentary market can support strong audience retention even when titles are produced with a lower risk profile than prestige dramas. Netflix also stated that music and investigative storytelling remained active documentary priorities within its wider original slate, suggesting a multi-year commitment rather than a short-cycle commissioning trend. As a result, the OTT documentary market is gaining a firmer place in retention planning, particularly among platforms that depend on mature audiences with steady nonfiction viewing habits.

Platform Differentiation Through Exclusive Documentary Libraries

Exclusive documentary libraries became a stronger point of differentiation in the OTT documentary market as scripted budgets leveled off and global platforms looked for catalog assets with longer viewing lives. In March 2026, Netflix and Warner Music Group signed a multi-year first-look agreement for documentary films and series built around artists including David Bowie, Cher, and Coldplay, demonstrating that rights-backed nonfiction partnerships are becoming repeatable pipelines. That shift improves the value of the OTT documentary market because exclusive libraries can create a defensible identity without forcing platforms to bear the full cost of constant scripted launches. It also supports more co-productions and library building in Europe, where streamers continue to deepen local factual catalogs as part of broader content obligations and regional positioning. The OTT documentary market now rewards services that can combine exclusive IP, global distribution reach, and local relevance in ways that keep nonfiction titles visible long after release.

Increasing Ad-Supported Streaming Inventory for Niche Audiences

Ad-supported tiers changed the monetization logic of the OTT documentary market because nonfiction audiences align well with premium, brand-safe, and interest-based advertising. In October 2025, the National Film Board of Canada launched TopDocs as a global FAST channel with more than 150 hours of documentary programming and a plan to add 20 hours of new content each month. That move showed that even publicly backed institutions viewed ad-supported distribution as a practical scale mechanism, not just as a secondary release outlet. In the OTT documentary market, this matters because longer viewing sessions and stronger completion rates can improve advertiser recall and help curated channels sustain higher-quality inventory than broad entertainment feeds. The result is a wider role for AVOD and FAST services that can attract viewers at the lower end of the price curve, then build monetization depth through selective upgrades and recurring ad demand.

Lower Production Risk Versus Scripted Originals

Lower production risk remained a direct support factor for the OTT documentary market, as streaming companies remained more selective in greenlighting and capital deployment. CuriosityStream reported fiscal 2025 revenue of USD 71.7 million, up 40% year over year, demonstrating that a focused nonfiction platform can expand while balancing subscription and licensing revenue streams. Those results matter because the OTT documentary market can still support content scale without the budget exposure normally tied to prestige scripted programming. That makes factual content especially useful for mid-tier and specialist platforms that need dependable volume, recurring engagement, and lower write-down risk. The OTT documentary market, therefore, remains attractive as a hedge against the volatility of expensive scripted renewals, slower payback periods, and abrupt cancellation cycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Mass-Audience Reach Versus Scripted Entertainment | -1.3% | Global | Medium term (2-4 years) |

| Rising Costs for Premium Factual Catalogs | -0.8% | North America and Europe | Short-term (≤ 2 years) and medium-term (2-4 years) |

| Discovery Risk in Content-Heavy OTT Interfaces | -0.5% | Global | Short term (≤ 2 years) |

| Creator Trust, Verification, and Factual Accuracy Constraints | -0.3% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Mass-Audience Reach Versus Scripted Entertainment

The OTT documentary market still faces a clear ceiling in broad audience reach because scripted franchises remain the strongest trigger for large subscriber sign-up events across general entertainment platforms. Even when true crime and celebrity investigations deliver strong viewing, documentaries do not usually generate the same event-driven momentum as top scripted releases. This limits the OTT documentary market's direct acquisition role, especially for services that depend on rapid audience spikes to support pricing and content recovery. The issue is more visible in lower-ARPU markets, where platforms often place broader entertainment bets ahead of niche nonfiction commissioning. As a result, the OTT documentary market grows more through retention, deeper monetization, and higher-quality audiences than through mass-market breakout moments.

Rising Rights Costs for Premium Factual Catalogs

Rising rights costs continue to pressure the OTT documentary market, particularly when premium projects depend on music rights, archival footage, sports access, or sensitive legal clearances that can shift late in production. Platforms have responded by leaning more heavily on owned originals and structured rights partnerships, rather than relying solely on third-party acquisitions. That change raises the burden on smaller producers, who must take on more early-stage development and clearance expenses before platform negotiations are complete. The OTT documentary market also becomes harder to scale for niche services when signature titles require rights packages that only well-capitalized buyers can secure at an acceptable cost. Over time, that friction favors companies with deeper legal teams, stronger balance sheets, and more direct access to rights holders across entertainment, news, and cultural archives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Monetization Model: SVOD Leads While Hybrid Tiers Broaden Revenue Capture

SVOD held 48.74% of the OTT documentary market share in 2025, maintaining its position as the largest monetization model and reflecting the continued strength of paid subscription access for premium nonfiction catalogs. That lead came from documentary-first services such as CuriosityStream and MagellanTV, as well as the factual libraries of larger general entertainment platforms that use documentaries to reinforce subscriber retention. The OTT documentary market still leans heavily on subscriptions because exclusive libraries and recurring docuseries give platforms a practical way to reduce churn among mature viewer groups. AVOD and FAST, however, widened the reach of documentary catalogs by lowering entry barriers for viewers who would not consistently add another paid service.

The Hybrid tier is projected to grow at a 8.52% CAGR from 2026 to 2031, making it the fastest-growing monetization layer in the OTT documentary market outlook and reflecting the move toward stacked access models. In March 2026, acTVe acquired Documentary+ and positioned the service across SVOD, AVOD, and FAST, with plans for daily original releases beginning in April 2026. In June 2026, Ionic Studios made a strategic equity investment in Documentary+ and became publisher of record for its ad-supported operations, which formalized a more specialized ad-monetization structure. These moves show that the OTT documentary industry is increasingly organized around layered revenue stacks, where the same title can support subscription value, ad yield, and wider viewer discovery without depending on a single release window.

By Device Type: Mobile Holds Scale While Smart TVs Improve Viewing Depth

Smartphones and Tablets accounted for 47.21% of the OTT documentary market in 2025, making mobile the primary access point for the OTT documentary market across price-sensitive and mobile-first viewing regions. That position reflected day-to-day streaming habits in Asia-Pacific and South America, where lower connected TV penetration and affordable data plans still support handheld viewing as the most convenient access route. Mobile screens also remain important for trailer sampling, casual discovery, and short-session engagement, which help nonfiction titles gain early visibility. For the OTT documentary market, this preserves the role of handheld devices even when deeper completion behavior tends to favor larger screens.

Smart TVs are projected to grow at an 8.65% CAGR from 2026 to 2031, driving the OTT documentary market's strongest device-side shift over the forecast period and changing how platforms think about documentary presentation. Larger screens are better suited to long-form investigations, event documentaries, and multi-part nonfiction series that depend on immersion and sustained viewing time. As living room streaming expands, platforms have a stronger incentive to improve documentary discovery on home interfaces rather than let nonfiction titles sit behind more predictable scripted recommendations. Laptops, desktops, gaming consoles, and streaming sticks still support search and access, but the center of gravity in the OTT documentary market is moving toward mobile discovery and smart TV completion.

By Genre: Crime Leads While Science Builds the Next Growth Layer

Crime and Investigation held 25.72% of the OTT documentary market share in 2025, making it the largest genre and confirming the category's ability to sustain repeat engagement. Netflix's H2 2025 engagement data showed strong performance from titles such as Sean Combs: The Reckoning, Amy Bradley Is Missing, and Cold Case: The Tylenol Murders, which reinforced the category's staying power in nonfiction streaming. That genre continues to perform well because viewers respond to serialized investigations, recognizable case structures, and strong completion patterns that are easy for platforms to program around. Biography and Personal Stories, History and Culture, and Nature and Environment also retain solid positions because they broaden the catalog and reduce overdependence on crime-heavy viewing cycles.

Science and technology are projected to expand at a 9.14% CAGR from 2026 to 2031, giving it the fastest growth outlook among OTT documentary genres and pointing to a broader shift in audience interest. CuriosityStream marked the 100th episode of Breakthrough in March 2026, using the milestone to reinforce its science-led programming on space and AI themes.[2]CuriosityStream, “Curiosity Stream Celebrates the 100th Episode of Breakthrough with a Powerful New Space Exploration Special,” FinancialContent via Access Newswire, markets.financialcontent.comApple Original Films also acquired global rights to The Last First: Winter K2 in February 2026, which showed continuing investment in premium factual storytelling outside the true crime core. This leaves the OTT documentary industry with broader room to grow through science, climate, exploration, and technology narratives that appeal to both specialist viewers and wider household audiences.

Geography Analysis

North America accounted for 36.59% of the OTT documentary market in 2025, making it the largest region and reflecting the concentration of global streaming leaders, premium rights networks, and mature nonfiction viewing habits. The region benefits from strong monetization across subscription, ad-supported, and licensing channels, making premium documentaries commercially viable even when they are not the main driver of customer acquisition. North American platforms also have deeper access to celebrity, music, sports, crime, and archive-based documentary material, which supports a steady flow of rights-backed releases. Asia-Pacific is projected to grow at an 8.47% CAGR from 2026 to 2031, making it the fastest-growing region in the OTT documentary market and reflecting rising paid streaming adoption across several large population centers. That growth is supported by broader local-language commissioning, improving smart TV use, and a wider shift from short mobile sessions to more intentional home viewing in key markets.

Europe remains central to the OTT documentary market because regional broadcasters, distributors, and global streamers continue to build nonfiction libraries that balance local cultural relevance with export potential. The European Audiovisual Observatory said Europe's audiovisual sector generated EUR 142 billion (USD 158 billion) in 2024, while on-demand services rose 15% as the fastest-growing part of the broader market.[3]European Audiovisual Observatory, “The European Audiovisual Sector Reaches EUR 142 Billion in Revenues as Streaming Reshapes Viewing Habits,” Cineuropa, cineuropa.org That environment supports more European documentary output because the economics of regional on-demand growth now align better with long shelf-life nonfiction programming. In South America, Brazil's 2025 VoD report counted more than 138,000 titles across 106 active platforms, which showed both the scale and fragmentation of the content supply base in one of the region's most active streaming markets.

The Middle East and Africa remain a smaller part of the OTT documentary market, but the region presents clear whitespace for local-language factual libraries and underserved viewing segments that are not yet deeply covered by global services. In March 2025, Warner Bros. Discovery invested USD 57 million in OSN Streaming, which signaled confidence in premium streaming demand across Gulf markets and added support for wider nonfiction reach in the region. Japan, South Korea, and China also influence the OTT documentary market through localized production pipelines, national factual traditions, and wider regional content distribution into Southeast Asia. Across all regions, the next phase of the OTT documentary market depends less on raw title volume and more on matching nonfiction libraries to local languages, device behavior, and cultural relevance.

Competitive Landscape

The OTT documentary market is moderately concentrated, with Netflix, Amazon, and The Walt Disney Company controlling most premium documentary spending and global audience reach. These companies compete through exclusive franchise development, stronger archive access, broad device distribution, and the ability to support documentaries across both subscription and ad-supported tiers. The OTT documentary market also includes specialist platforms such as CuriosityStream, MagellanTV, and DocuBay, which focus on depth of curation rather than mass-catalog scale. CuriosityStream reported in May 2026 that AI licensing revenue is expected to exceed subscription revenue for the full year, which showed how specialist nonfiction platforms are opening revenue paths that large general entertainment services have not yet prioritized. This gives the OTT documentary market a split structure, where global platforms compete on reach, and specialists compete on library focus, audience quality, and licensing flexibility.

Strategic moves in 2025 and 2026 showed how quickly competitive positions are being reshaped inside the OTT documentary market. Reuters reported that Netflix and Warner Music Group signed a multi-year first-look deal in March 2026, which gave Netflix a deep music-centered documentary pipeline with long franchise potential. Deadline reported that acTVe acquired Documentary+ in March 2026 to develop the service across SVOD, AVOD, and FAST windows, while Blue Ant Media acquired MagellanTV in October 2025 for USD 12 million to strengthen its nonfiction streaming position. In June 2026, Ionic Studios invested in Documentary+ and took operating responsibility for ad monetization, which separated content curation from advertising operations within the same platform structure.

The OTT documentary market still has open space in multilingual local-language commissioning, science-led programming, and smarter documentary discovery on smart TV interfaces. Platforms that solve discovery well can gain more from nonfiction because completion rates, repeat viewing, and catalog shelf life often remain stronger than raw title volume suggests. BBC Studios and Rogan Productions renewed their first-look deal in 2025, which showed that trusted distribution partnerships still matter for keeping premium documentary pipelines active across many territories.[4]World Screen Staff, “BBC Studios and Rogan Productions Renew First-Look Deal,” World Screen, worldscreen.com Overall, the OTT documentary market rewards companies that can combine exclusive rights, efficient monetization, and sharper curation without carrying the full budget burden of scripted entertainment.

OTT Documentary Industry Leaders

Netflix, Inc.

Amazon.com, Inc.

The Walt Disney Company

Comcast Corporation

Warner Bros. Discovery, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Netflix and Warner Music Group signed an exclusive multi-year first-look deal to produce documentary series and films centered on WMG's artist roster, including David Bowie, Cher, Fleetwood Mac, and contemporary acts such as Coldplay and Bruno Mars. The agreement grants Netflix access to one of the entertainment industry's deepest music IP vaults for long-form factual development.

- March 2026: acTVe acquired Documentary+, the documentary streaming platform available in over 70 countries and more than 100 million US households, with the stated goal of evolving it into a definitive documentary streaming platform for global audiences. The acquisition positioned Documentary+ for a hybrid SVOD-AVOD-FAST model with plans for daily original releases beginning April 2026.

- March 2026: CuriosityStream published its fiscal year 2025 results, reporting revenue of USD 71.7 million, a 40% year-over-year increase. The company completed 18 distinct AI training content fulfillments and secured rights to approximately 2 million hours of video and audio content, with management guiding for full-year 2026 revenue of USD 75 million to USD 80 million.

- October 2025: Blue Ant Media acquired Washington-based documentary streaming service MagellanTV for USD 12 million. MagellanTV operates an SVOD service and AVOD and FAST channels across history, nature, science, space, and true crime genres, with distribution partnerships spanning Roku, Amazon, Apple, Samsung, LG, Comcast, and Pluto TV across 13 countries.

Global OTT Documentary Market Report Scope

The OTT Documentary Market covers the distribution and monetization of documentary films and series through over-the-top streaming platforms delivered via the internet, including subscription-, advertising-, transactional-, and hybrid-based models. The scope includes documentary content across genres such as nature, history, crime, sports, biography, social issues, science, and culture, accessed through devices such as smart TVs, smartphones, tablets, laptops, and streaming media players.

The OTT Documentary Market Report is Segmented by Monetization Model (SVOD, AVOD, TVOD, Hybrid, and Freemium), Device Type (Smartphones and Tablets, Smart TVs, Laptops and Desktops, and Other Device Types), Genre (Biography and Personal Stories, History and Culture, Nature and Environment, Science and Technology, Crime and Investigation, and Other Genres), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| SVOD |

| AVOD |

| TVOD |

| Hybrid |

| Freemium |

| Smartphones and Tablets |

| Smart TVs |

| Laptops and Desktops |

| Other Device Types |

| Biography and Personal Stories |

| History and Culture |

| Nature and Environment |

| Science and Technology |

| Crime and Investigation |

| Other Genres |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Monetization Model | SVOD | |

| AVOD | ||

| TVOD | ||

| Hybrid | ||

| Freemium | ||

| By Device Type | Smartphones and Tablets | |

| Smart TVs | ||

| Laptops and Desktops | ||

| Other Device Types | ||

| By Genre | Biography and Personal Stories | |

| History and Culture | ||

| Nature and Environment | ||

| Science and Technology | ||

| Crime and Investigation | ||

| Other Genres | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected size of the OTT documentary market by 2031?

The OTT documentary market was valued at USD 14.36 billion in 2025 and is projected to reach USD 22.76 billion by 2031, growing at a 7.72% CAGR from 2026 to 2031.

Which monetization model currently leads documentary streaming revenue?

SVOD remained the leading model in 2025 with 48.74% share, while Hybrid tiers are expected to post the fastest growth at an 8.52% CAGR through 2031.

Which device category is shaping the next phase of documentary viewing?

Smartphones and Tablets led with 47.21% share in 2025, but Smart TVs are expected to grow faster at an 8.65% CAGR as living room viewing expands.

Which documentary genre is strongest today and which one is growing fastest?

Crime and Investigation led with 25.72% share in 2025, while Science and Technology is projected to expand at the fastest CAGR of 9.14% through 2031.

Which region leads global OTT documentary demand?

North America held the largest regional share at 36.59% in 2025, supported by major platform concentration, deeper rights access, and mature nonfiction viewing habits.

Where are the biggest future growth opportunities in OTT documentaries?

Asia-Pacific is projected to grow the fastest at 8.47% CAGR, while broader upside also exists in localized nonfiction libraries, science-led programming, and better smart TV discovery.

Page last updated on: