OTC Pet Medication Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 10.20 Billion |

| Market Size (2031) | USD 13.5 Billion |

| Growth Rate (2026 - 2031) | 5.69% CAGR |

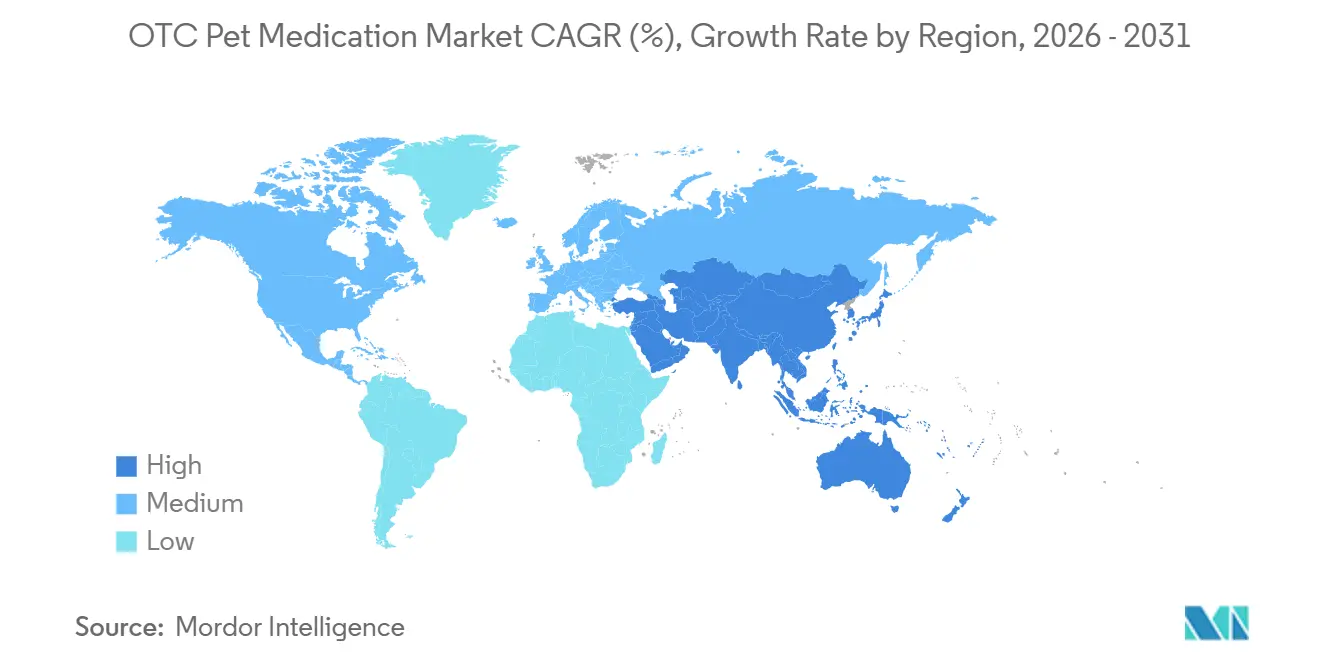

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

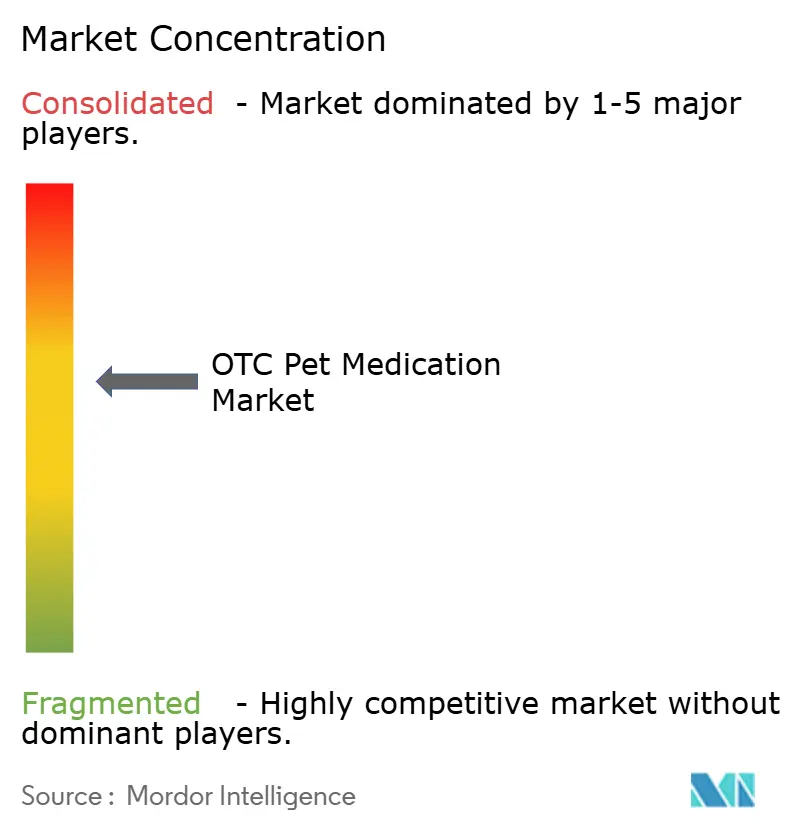

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

OTC Pet Medication Market Analysis by Mordor Intelligence

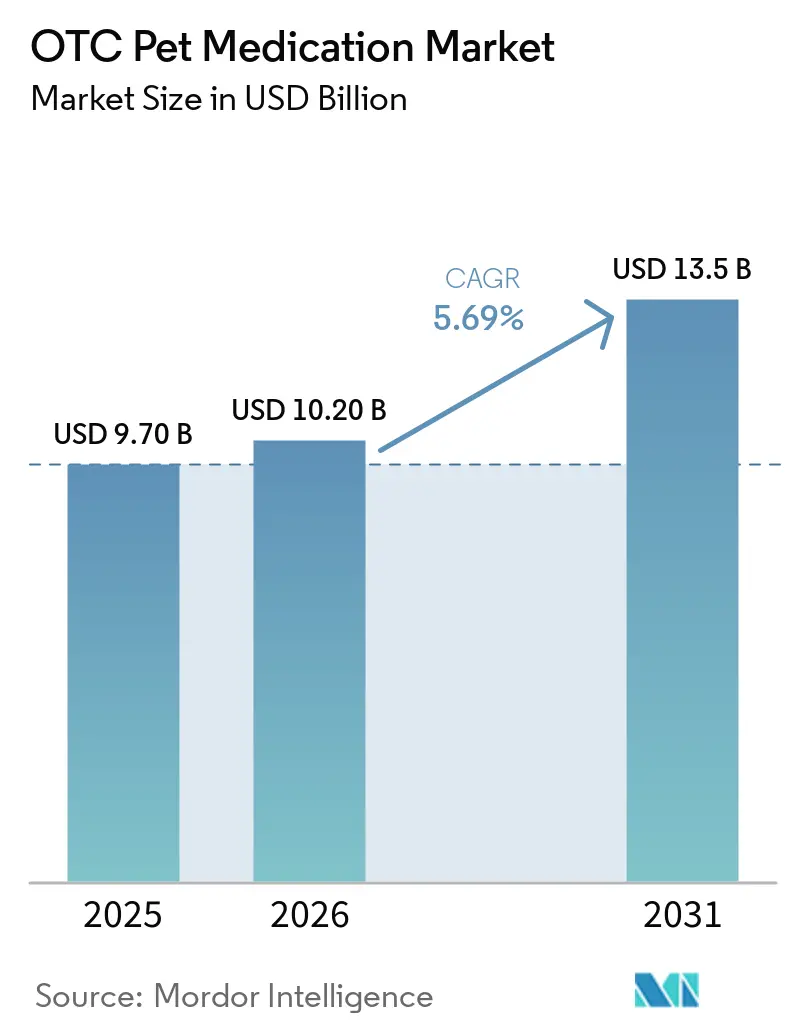

The OTC Pet Medication Market size is expected to grow from USD 9.70 billion in 2025 to USD 10.20 billion in 2026 and is forecast to reach USD 13.5 billion by 2031 at 5.69% CAGR over 2026-2031.

Shifting climate patterns are pushing tick and flea activity into what were once dormant months, converting seasonal buyers into year-round users and lifting baseline demand. Ongoing EPA and FDA scrutiny of older collar and spot-on chemistries is accelerating the transition toward longer-acting oral chewables, injectables, and microbiome-focused supplements. The online channel is rewriting retail economics through autoship programs that cut lapse rates and provide predictable sell-through for manufacturers. Meanwhile, private-label parasiticides are capping price ceilings in commoditized categories even as premium nutraceuticals command double-digit margins. Competitive responses range from Chewy’s vertical integration into clinics to Elanco’s expansion into functional supplements, signaling a market that is simultaneously consolidating and fragmenting in different price tiers.

Key Report Takeaways

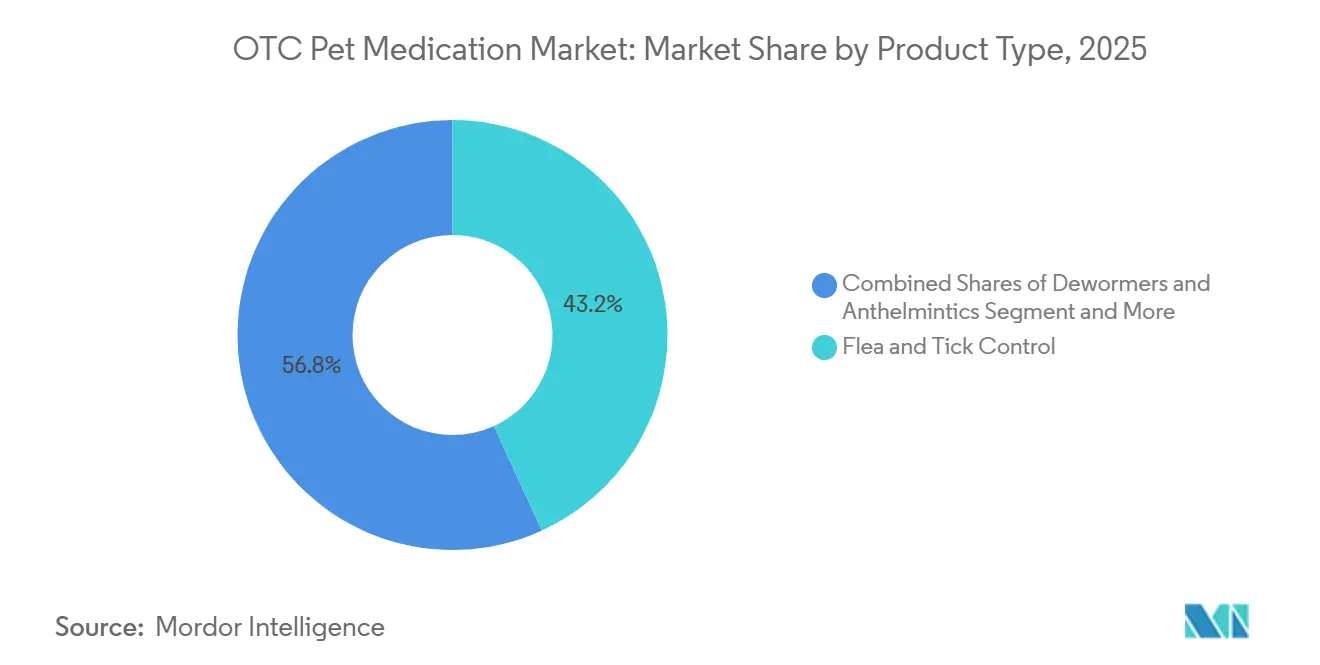

- By product type, flea and tick control led with 43.18% of OTC pet medication market share in 2025, while nutraceuticals and supplements are projected to expand at a 7.63% CAGR to 2031.

- By animal type, dogs accounted for 58.15% of 2025 revenue, whereas cats are advancing at a 7.43% CAGR through 2031 after the launch of palatable oral formulations.

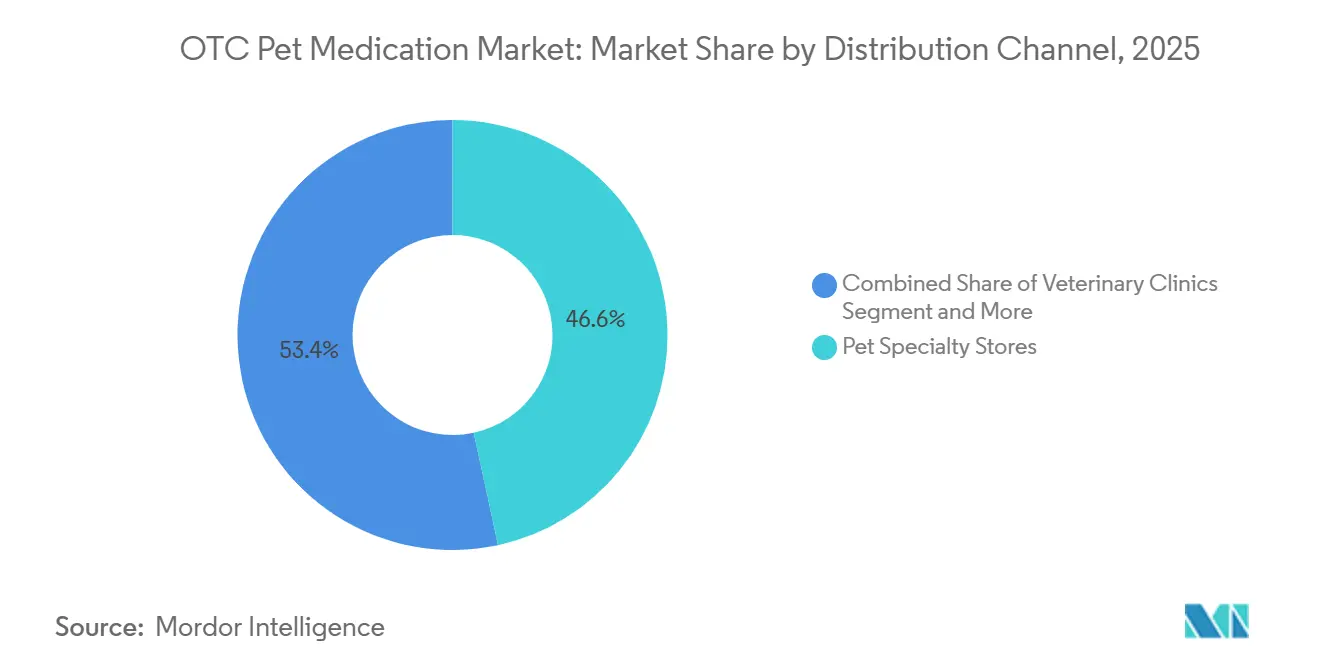

- By distribution channel, pet specialty stores held 46.61% share in 2025, yet online marketplaces record the fastest growth at 7.91% CAGR through 2031 due to autoship adoption.

- By form, topical spot-ons represented 41.35% of 2025 sales, while oral chews and tablets are gaining at a 7.37% CAGR on breakthrough palatability scores.

- By geography, North America dominated with 42.88% of 2025 value, yet Asia-Pacific is projected to post a 7.55% CAGR through 2031 on rapid pet ownership growth.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global OTC Pet Medication Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Climate-driven expansion of external parasites extends year-round prevention demand | +1.2% | Global, pronounced in North America and Europe | Medium term (2-4 years) |

| E-commerce autoship raises adherence to monthly dosing | +1.5% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Rising pet humanization sustains spend on convenient OTC care | +1.0% | Global, strongest in urban China and U.S. | Long term (≥ 4 years) |

| Longer-acting, easy-to-administer formats improve compliance | +1.3% | Global | Medium term (2-4 years) |

| Prospective EPA-to-FDA oversight shift could boost safety confidence | +0.4% | North America with international spillover | Long term (≥ 4 years) |

| Private-label scaling widens price access | +0.6% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Climate-Driven Expansion of Tick and Flea Prevalence Elevates Year-Round Prevention Demand

Warmer winters and higher humidity have extended the active seasons of key vectors such as Ixodes and Amblyomma ticks, prompting veterinarians to recommend twelve-month prevention protocols even in regions that once paused treatment in winter [1]Companion Animal Parasite Council, “CAPC Parasite Prevalence Maps,” CAPCVET.ORG. The geographic creep of the Asian longhorned tick into 21 U.S. states by 2025 underscores how climate forces are rewiring baseline demand. Long-duration injectables like Bravecto Quantum now offer 12-month coverage and remove monthly owner intervention. Continuous parasite pressure is therefore nudging the OTC pet medication market toward subscription models that lock in compliance and stabilize revenue flows.

E-Commerce and Subscription Autoship Normalize OTC Replenishment and Raise Adherence

Autoship’s behavioral lock-in reduced lapse rates across Chewy’s 21.3 million customers, with 83% enrolled as of fiscal 2025. Monthly dosing aligns naturally with subscription cadence, allowing online platforms to undercut brick-and-mortar pricing while still expanding total volume. Integrations with tele-veterinary services and price-comparison widgets further entrench these ecosystems, shifting channel power toward marketplaces that define reference pricing across the OTC pet medication market.

High Pet Ownership and Humanization Sustain Spend on Convenient OTC Care

Pet humanization is driving willingness to purchase premium OTC solutions that overlay basic parasite control. In major Chinese cities, average per-pet medical spend topped CNY 2,000 in 2026, and digestive or calming supplements account for more than one-quarter of that outlay. Similar sentiment in U.S. households is supporting microbiome-targeted chews that retail at two to three times the price of traditional vitamins. This demand elasticity underpins the growth of nutraceuticals within the broader OTC pet medication market.

Product Innovation in Longer-Acting, Easier-to-Administer OTC Formats

Formulators are converging on two design briefs: extend protection windows and improve palatability. Credelio Quattro combines three active ingredients to provide broad-spectrum cover in a single chew, reducing pill burden. Felxi-compressed soft chews scored 100% acceptance in 2025 canine field trials. These advances lessen the compliance friction that has historically capped penetration, particularly among cats, thereby expanding the addressable slice of the OTC pet medication market size.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened safety scrutiny of collars and spot-ons | -0.8% | Global, acute in U.S. and EU | Short term (≤ 2 years) |

| Counterfeit and illegal online OTC sales | -0.6% | Global, highest in Asia-Pacific | Medium term (2-4 years) |

| Resistance to legacy actives in hotspot regions | -0.4% | North America and Europe | Medium term (2-4 years) |

| Downturn-driven price sensitivity delays prevention cycles | -0.5% | Global, stronger in emerging markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Heightened Safety Scrutiny of Flea/Tick Collars and Spot-Ons Dampens Some Categories

Seresto adverse-event reports and FDA alerts on isoxazoline class products have prompted risk-averse owners to abandon collars in favor of oral or injectable options [2]U.S. FDA, “Neurologic Adverse Events Alert,” FDA.GOV. Sales data show collars sliding as much as 10% year on year within the OTC pet medication market, reinforcing the pivot to formats viewed as safer and easier to dose

Counterfeit and Illegal Online OTC Sales Erode Trust and Require Channel Gating

The seizure of over 1,400 counterfeit pet-medicine units in the U.K. and the takedown of 15,000 fake listings in the EU exemplify the scope of illicit trade. Brand owners now invest in QR-code serialization and restrict fulfillment to verified sellers, raising logistics costs that partially offset the growth dividend from e-commerce within the OTC pet medication market size.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Nutraceuticals Lead Growth Momentum

Nutraceuticals and supplements are advancing at a 7.63% CAGR and are expected to command an outsize slice of incremental OTC pet medication market size to 2031. Owners increasingly layer microbiome modulators, calming botanicals, and joint-health compounds onto routine parasite control, and brands that can cite peer-reviewed efficacy data are achieving premium price points. Although flea and tick control still generated 43.18% of 2025 revenue, growth is moderating as resistance to fipronil and imidacloprid emerges in field populations.

Manufacturers are broadening nutraceutical portfolios through science-backed ingredients such as postbiotic yeast fermentates, while food companies like Purina have crossed the aisle with probiotic-fortified kibbles that blur category lines[3]Purina, “Pro Plan AdvantEDGE Launch,” PURINA.COM. The diverse SKU mix cushions brands against regulatory shocks that periodically buffet chemical parasiticides, underscoring why nutraceuticals are central to long-run value creation in the OTC pet medication market.

By Animal Type: Feline Segment Closes the Innovation Gap

Dogs continued to dominate revenue with a 58.15% slice of the OTC pet medication market share in 2025. However, cat-specific innovation, particularly in palatable oral flea-and-tick treatments, has unlocked a 7.43% CAGR through 2031. Credelio Cat’s 99.5% owner-reported dosing success reflects how flavor-engineering can neutralize historical compliance barriers. Liquid solutions for feline hypertension and hyperthyroidism further illustrate the formulation shift toward precision dosing for smaller body weights. As the global cat population ages, demand for renal-support and mobility supplements is likely to accelerate, tightening the race for share capture inside the OTC pet medication market.

By Distribution Channel: Online Marketplaces Redefine Convenience

Pet specialty stores captured 46.61% of 2025 sales, yet online retailers are scaling fastest at 7.91% CAGR on the strength of autoship and tele-veterinary add-ons. The OTC pet medication market size for e-commerce grew by USD 1.2 billion between 2024 and 2026, reflecting the cost and convenience advantages of drop-ship logistics.

Brick-and-mortar outlets defend their turf through immediate product access and advisory services, but they face narrowing margins as price transparency resets consumer expectations. Platforms that pair clinical services with fulfillment, such as Chewy’s newly acquired clinic network, are setting the template for omnichannel integration across the OTC pet medication market.

By Form: Oral Chews Eclipse Topicals on Compliance Wins

Topical spot-ons held 41.35% of 2025 revenue, yet oral formats are growing 7.37% annually as beef-flavored matrices hit palatability scores above 99%. Lack of post-application oily residue, combined with reduced dermal-absorption concerns, makes chews the preferred choice for urban pet owners.

Combination chews that merge flea, tick, heartworm, and tapeworm protection in a single dose support once-monthly compliance, further tilting the revenue mix toward orally dosed products. This compliance edge ensures oral formats will claim a larger fraction of the OTC pet medication market size over the forecast window.

Geography Analysis

North America supplied 42.88% of 2025 value, benefiting from high per-pet spend and mature distribution infrastructure. North America’s high baseline spend provides fertile ground for premium upsell, and injectables delivering year-long coverage are rapidly adopting subscription billing models, reinforcing customer stickiness. Counterfeit mitigation initiatives spearheaded by the FDA and major brands are also raising online trust levels, sustaining digital channel momentum inside the region’s OTC pet medication market.

Asia-Pacific posts the sharpest trajectory at 7.55% CAGR through 2031. Asia-Pacific’s double-digit expansion in pet populations is intersecting with cross-border e-commerce, allowing owners in Tier-2 cities to access international brands previously confined to capital hubs. Yet the diversity of regulatory classifications from prescription-only rules in South Korea to loosely policed online sales in parts of Southeast Asia requires agile compliance strategy and localized education to secure durable footholds.

Europe benefits from coordinated customs enforcement initiatives such as Operation SHIELD VI, which removed thousands of counterfeit listings and reinforced consumer confidence. The region’s ongoing shift from collars to chewables is being shepherded by strict pharmacovigilance that favors companies with robust safety dossiers, effectively concentrating growth within the compliant subset of the OTC pet medication market.

Competitive Landscape

Market concentration is moderate: the top five suppliers, Elanco, Boehringer Ingelheim, PetIQ, Hartz Mountain, and Ceva, held the majority of the combined revenue. Incumbents are extending moats by embedding veterinary services or by licensing novel active ingredients before generics emerge. Chewy’s USD 125 million Modern Animal deal exemplifies the former, while Elanco’s Pet Protect nutraceutical line illustrates the latter.

Direct-to-consumer disruptors leverage social-media marketing and subscription curation to grab millennial wallet share, though scale economics remain challenging without clinical endorsement. Data partnerships, such as Boehringer Ingelheim’s tie-up with Trupanion, underline the strategic value of real-world treatment outcomes to refine product positioning and foster brand loyalty.

White-space opportunities include feline-specific liquid suspensions, microbiome-validated supplements, and hybrid chemistries awaiting clarity on unified FDA oversight. Early movers that secure regulatory clearance and intellectual property around these niches are likely to outperform the broader OTC pet medication industry.

OTC Pet Medication Industry Leaders

Elanco Animal Health

Boehringer Ingelheim Animal Health

PetIQ

The Hartz Mountain Corporation

Ceva Santé Animale

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Chewy entered into an agreement to acquire Modern Animal, Inc. for USD 125 million, adding physical clinics to its e-commerce ecosystem.

- January 2026: Cencora finalized its USD 3.5 billion merger with MWI Animal Health, consolidating distribution reach to clinics and retailers.

Global OTC Pet Medication Market Report Scope

As per the scope of the report, Over the counter (OTC) pet medications are products available without a formal prescription from a veterinarian, often used to manage minor health issues or preventive care. These include veterinary-specific items like flea and tick preventatives, dewormers, and multivitamins, as well as certain human medications that may be used extra-label under professional guidance.

The OTC pet medication market is segmented by product type, animal type, distribution channel, form, and geography. Based on product type, the market is segmented into flea & tick control, dewormers and anthelmintics, skin & coat treatments (medicated topicals, shampoos), dental & oral care OTC, calming & behavioral OTC, and nutraceuticals & supplements. By animal type, the market is segmented into dogs, cats, small companion mammals (rabbits, ferrets), birds, and others (fish and reptiles, among others). By distribution channel, the market is segmented into online retailers & marketplaces, pet specialty stores, mass merchandisers, grocery & club stores, veterinary clinics, and drug & pharmacy stores. By form, the market is segmented into topical (spot-ons, sprays), oral (chews, tablets), collars, shampoos & dips, and sprays & powders. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Flea & Tick Control |

| Dewormers and Anthelmintics |

| Skin & Coat Treatments |

| Dental & Oral Care OTC |

| Calming & Behavioral OTC |

| Nutraceuticals & Supplements |

| Dogs |

| Cats |

| Small Companion Mammals (rabbits, ferrets) |

| Birds |

| Others (Fish and Reptiles, among others) |

| Online Retailers & Marketplaces |

| Pet Specialty Stores |

| Mass Merchandisers, Grocery & Club |

| Veterinary Clinics |

| Drug & Pharmacy Stores |

| Topical (spot-ons, sprays) |

| Oral (chews, tablets) |

| Collars |

| Shampoos & Dips |

| Sprays & Powders |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Flea & Tick Control | |

| Dewormers and Anthelmintics | ||

| Skin & Coat Treatments | ||

| Dental & Oral Care OTC | ||

| Calming & Behavioral OTC | ||

| Nutraceuticals & Supplements | ||

| By Animal Type | Dogs | |

| Cats | ||

| Small Companion Mammals (rabbits, ferrets) | ||

| Birds | ||

| Others (Fish and Reptiles, among others) | ||

| By Distribution Channel | Online Retailers & Marketplaces | |

| Pet Specialty Stores | ||

| Mass Merchandisers, Grocery & Club | ||

| Veterinary Clinics | ||

| Drug & Pharmacy Stores | ||

| By Form | Topical (spot-ons, sprays) | |

| Oral (chews, tablets) | ||

| Collars | ||

| Shampoos & Dips | ||

| Sprays & Powders | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large will the OTC pet medication market be by 2031?

The OTC pet medication market size to reach USD 13.5 billion by 2031, reflecting a 5.69% CAGR from 2026 to 2031.

Which product category is growing fastest within OTC pet care?

Nutraceuticals and supplements top the growth table with a 7.63% CAGR through 2031, driven by microbiome and joint-health innovations.

Are oral chews overtaking topical spot-ons?

Yes, oral chews are advancing at 7.37% CAGR through 2031 due to superior palatability and compliance, while topical share is easing under safety scrutiny .

Which sales channel offers the highest upside?

Online marketplaces record the strongest growth at 7.91% CAGR through 2031, fueled by autoship programs that secure monthly dosing adherence.

Page last updated on: