Orthopedic Fracture Repair Implants For Osteoporosis Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 6.60 Billion |

| Market Size (2031) | USD 8.90 Billion |

| Growth Rate (2026 - 2031) | 6.33% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

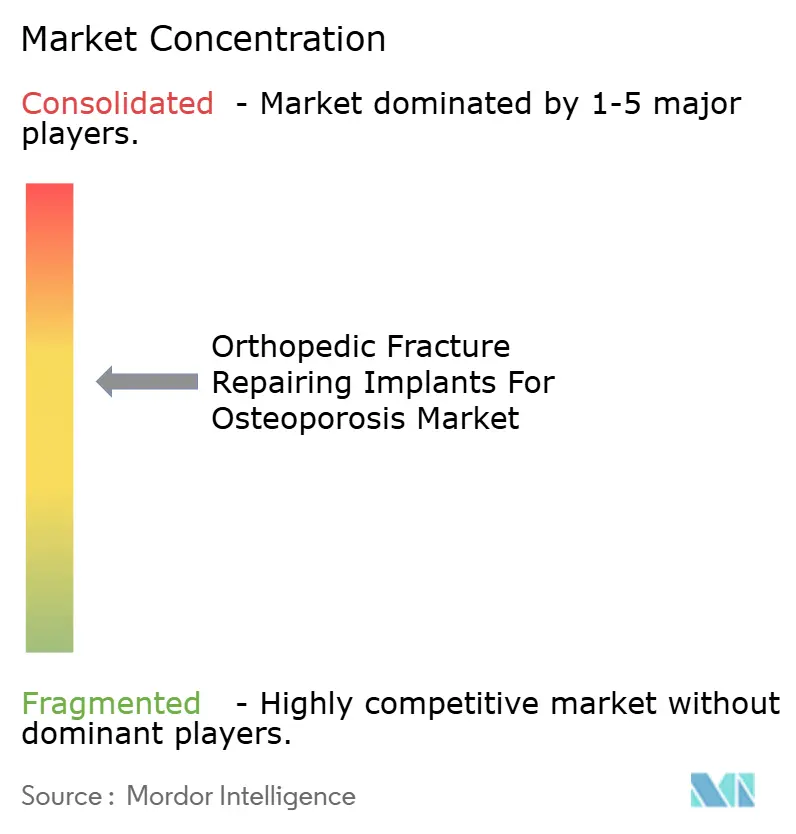

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Orthopedic Fracture Repair Implants For Osteoporosis Market Analysis by Mordor Intelligence

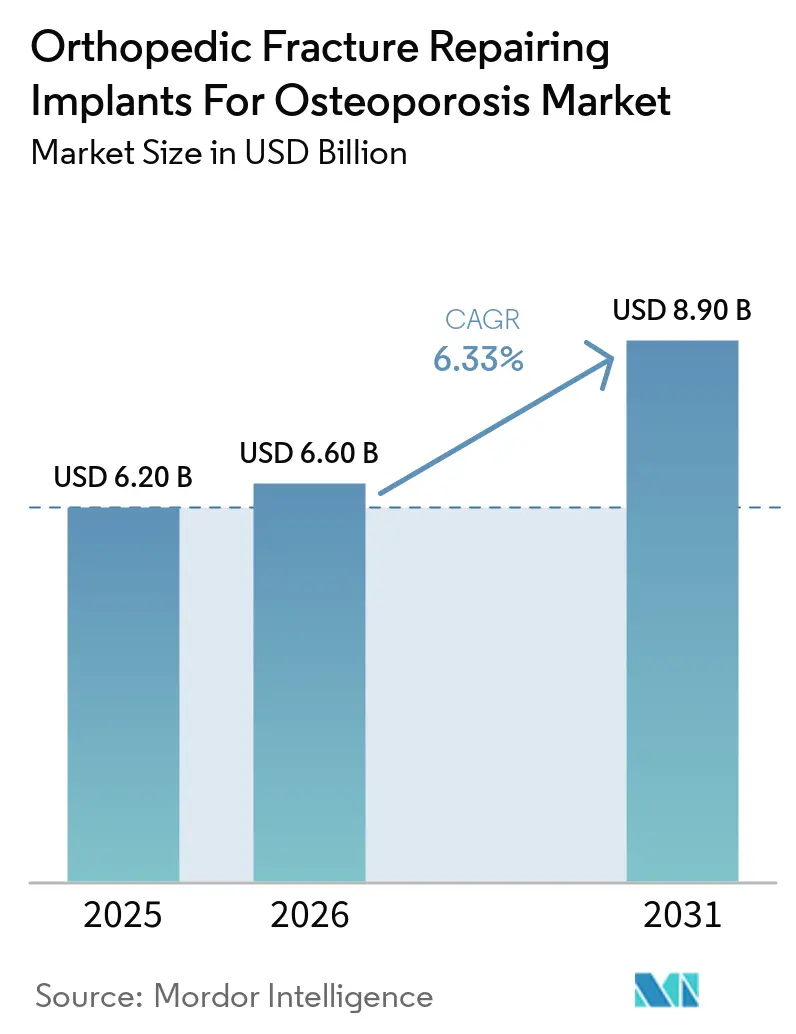

The Orthopedic Fracture Repair Implants For Osteoporosis Market size is expected to increase from USD 6.20 billion in 2025 to USD 6.60 billion in 2026 and reach USD 8.90 billion by 2031, growing at a CAGR of 6.33% over 2026-2031.

Volume demand continues to climb as global life expectancy lengthens, fragility‐fracture reporting improves, and minimally invasive vertebral augmentation moves into routine orthopedic practice[1]Bone Health & Osteoporosis Foundation, “Fracture Facts and Statistics,” BONEHEALTHANDOSTEOPOROSIS.ORG. Hospitals are under pressure to operate within fixed DRG bundles, so suppliers that can prove shorter theater time or fewer revisions are winning price concessions instead of across-the-board cuts. Specialist trauma centers are now bypassing hospital supply chains and purchasing directly from vendors, accelerating the migration of premium implants to higher-margin channels. Simultaneously, payers in North America and Western Europe are rewarding 24-hour hip-fracture surgery with financial bonuses, keeping unit economics supportive of premium implants even as metal price inflation tapers.

Key Report Takeaways

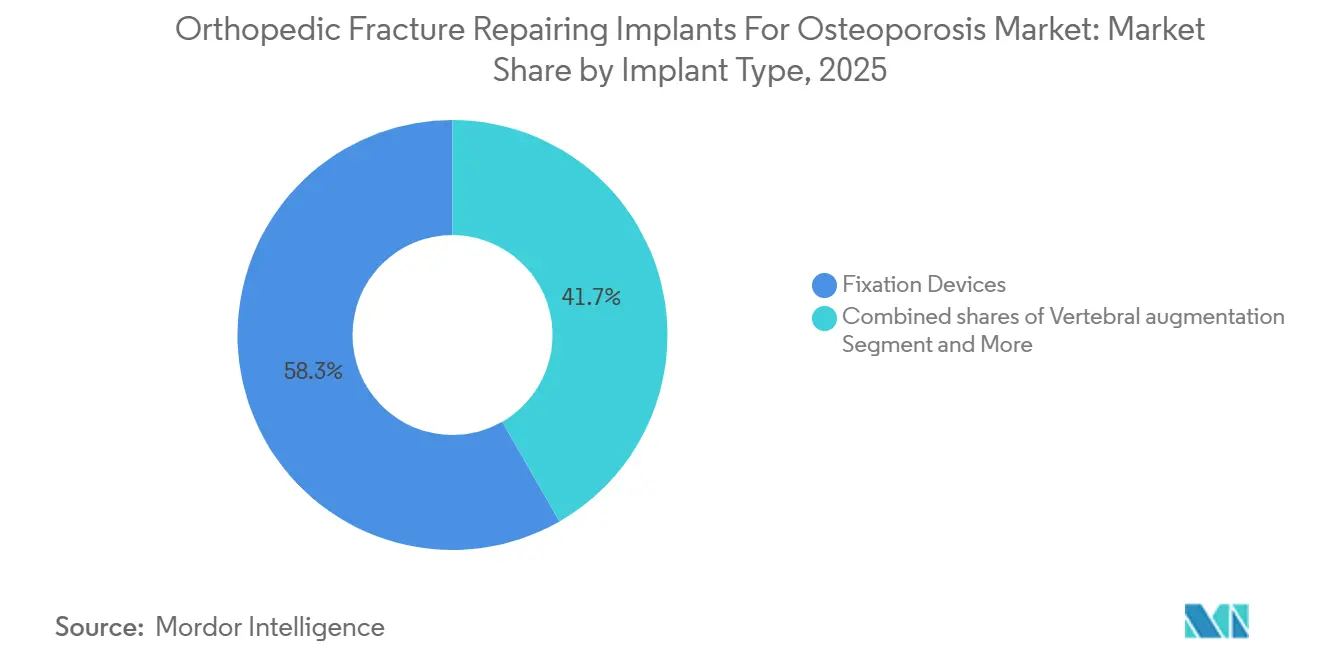

- By implant type, fixation devices led with 58.30% of orthopedic fracture repair implants in the osteoporosis market in 2025. However, vertebral augmentation is expected to register 6.76% CAGR by 2031.

- By fracture site, vertebral compression fractures are advancing at a 6.95% CAGR through 2031. Whereas the hip/proximal femur led with 38.63% market share in 2025.

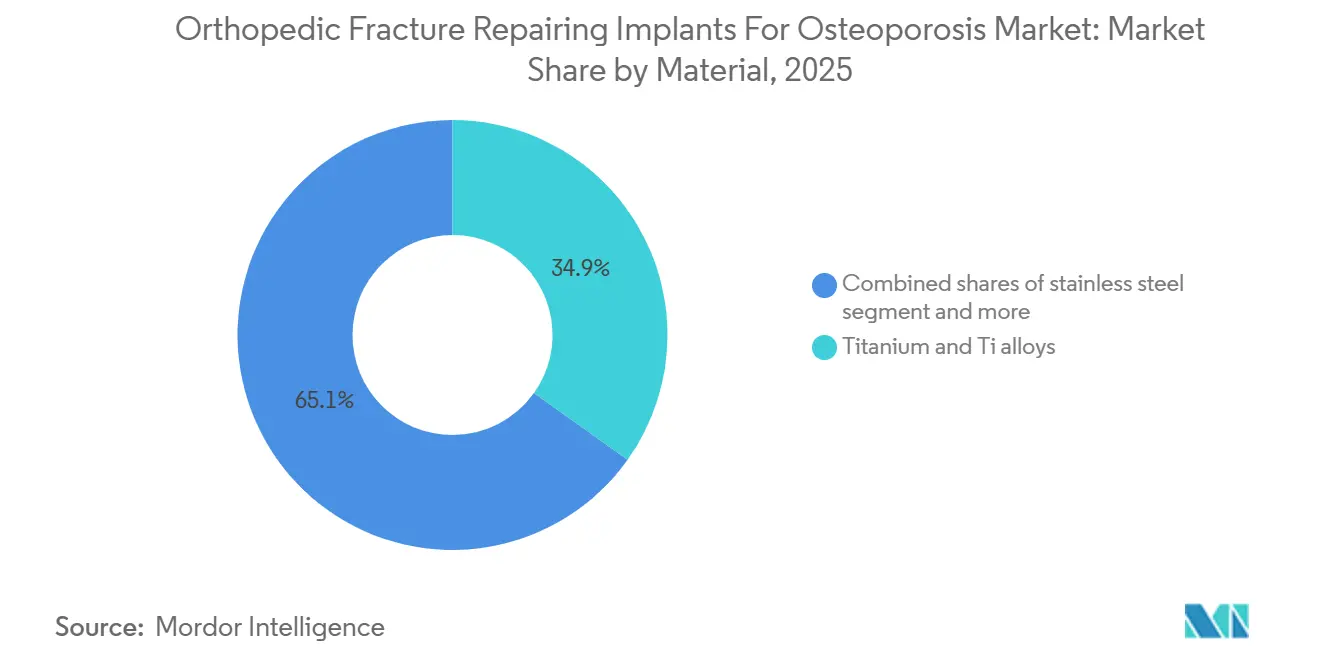

- By material, titanium accounted for 34.86% of the orthopedic fracture repair implants market share in 2025. However, PEEK & carbon fiber–reinforced polymers is advancing at 7.03% CAGR.

- By end user, specialty orthopedic centers are growing at 7.14% CAGR to 2031. Whereas, hospitals led with 57.18% market share in 2025.

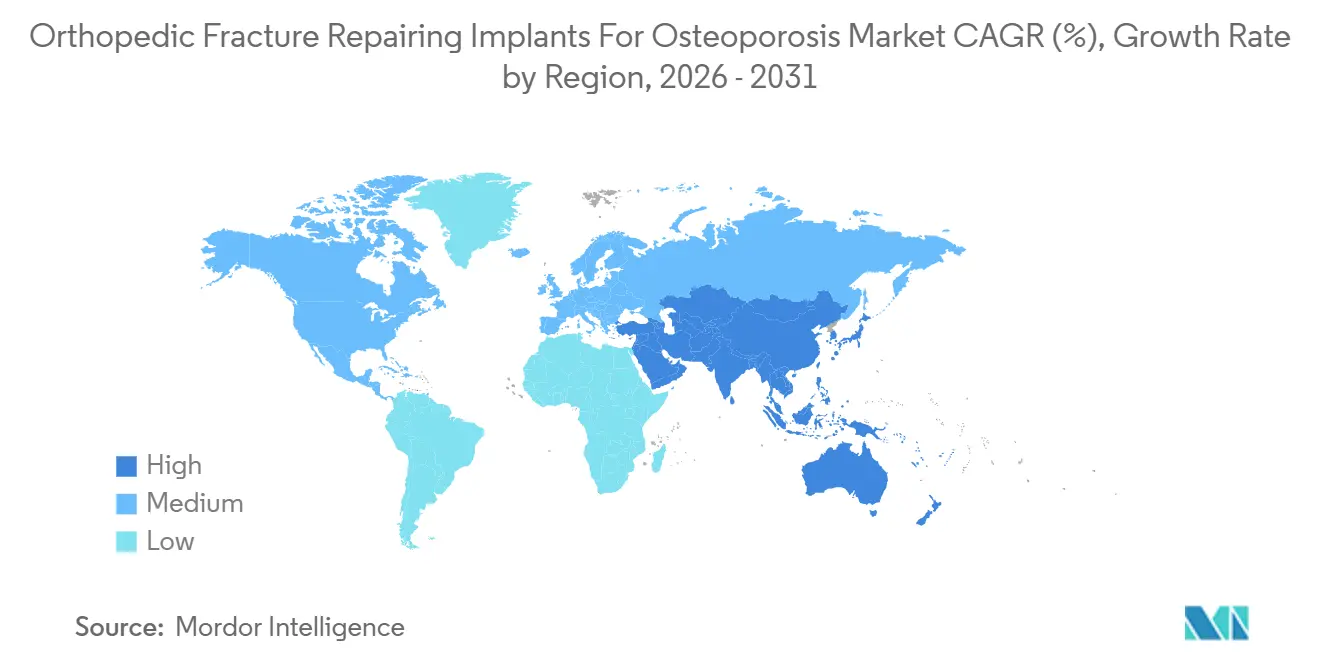

- Geographically, North America accounted for 43.18% of the market, yet Asia-Pacific is expected to grow by 6.95% by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Orthopedic Fracture Repair Implants For Osteoporosis Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging population and rising fragility fracture burden | +1.8% | Japan, Europe, North America | Long term (≥ 4 years) |

| Minimally invasive vertebral augmentation adoption | +1.3% | North America, Europe, APAC urban centers | Medium term (2-4 years) |

| Advances in osteoporotic fixation technology | +1.1% | Global, led by North America and Europe | Medium term (2-4 years) |

| Favorable reimbursement for early hip-fracture surgery | +0.9% | North America, Western Europe | Short term (≤ 2 years) |

| Fracture Liaison Services scaling surgical capture | +0.7% | Europe, Australia, Canada | Medium term (2-4 years) |

| Cement-augmented fixation expanding indications | +0.5% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aging Population and Rising Fragility Fracture Burden

Fragility fractures already reach more than 2 million episodes annually in the United States, and each hip fracture carries a one-year mortality above 20% with direct costs around USD 40,000. Japan reports 180,000 hip fractures per year, while 29.1% of its citizens are now at least 65 years old[2]Statistics Bureau of Japan, “Population Estimates by Age and Sex,” STAT.GO.JP. A 2024 hospital audit in northeastern China showed hip fractures made up a significant number of overall osteoporotic fractures and revealed that fewer than 9% of patients received anti-osteoporotic drugs afterward, setting the stage for refracture. These numbers confirm the demographic “locked-in” demand for orthopedic fracture-repairing implants for osteoporosis, but they also highlight the engineering challenge of anchoring implants securely in bone that has lost structural density.

Minimally Invasive Vertebral Augmentation Adoption

The North American Spine Society’s 2025 clinical guideline endorses vertebral augmentation after 4–6 weeks of failed conservative care, aligning payer policy with clinical preference[3]North American Spine Society, “Clinical Practice Guideline on Vertebral Augmentation,” SPINE.ORG. Systems such as Merit Medical’s DFINE StabiliT MX use steerable osteotomes and high-viscosity PMMA to cut leakage rates, while Stryker’s FDA-cleared SpineJack lifts the endplate with up to 1,000 N of force before cement fill. Because the procedure is percutaneous and lasts under 40 minutes, it is quickly moving into ambulatory surgical centers, where average payer savings are USD 2,602 per case and weekday block time is plentiful.

Advances in Osteoporotic Fixation Technology

Fenestrated screws that permit in situ cement injection, helical-blade cephalomedullary nails that compress cancellous bone, and locking plates tuned for low-density cortical purchase are rewriting fixation biomechanics. A 2024 meta-analysis of proximal humerus fractures showed that cement-augmented screws halved the rate of loosening compared with standard plates. Radiolucent PEEK plates, such as CarboFix’s Carbostick, let surgeons verify reduction on CT without metal artifact, and bioabsorbable composites approved by the FDA in 2023 remove the need for hardware retrieval in frail patients.

Favorable Reimbursement and Care Pathways for Early Hip-Fracture Surgery

North American and U.K. payment systems now penalize delay, rewarding hospitals financially when surgery happens within 24–36 hours. CMS preserved device-intensive add-on payments in its 2025 Physician Fee Schedule, allowing manufacturers to earn premiums for implants that shorten operating time or reduce transfusions. The U.K.’s Best Practice Tariff lowered 30-day mortality to 6.1% in 2023 by coupling fast surgery with orthogeriatric co-management.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Evidence controversy plus variable payer coverage | -0.6% | North America, Europe | Short term (≤ 2 years) |

| Cement leakage and perioperative safety risks | -0.4% | Global | Medium term (2-4 years) |

| Hospital tendering and DRG cost pressure | -0.5% | Europe, Asia-Pacific, Global | Short term (≤ 2 years) |

| Underdiagnosis of vertebral fractures | -0.3% | Low- and middle-income economies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Evidence Controversy and Variable Payer Coverage for Vertebral Augmentation

Early placebo-controlled trials showed limited benefit compared with sham procedures, so several U.S. regional plans still require advanced imaging evidence of a vertebral cleft before authorizing treatment. Denials force practices to spend administrative time on appeals, slowing the growth of procedures in lower-margin offices. Manufacturers are therefore underwriting large post-market registries to produce the real-world evidence that payers demand.

Cement Leakage and Perioperative Safety Risks

A 2024 systematic review put PMMA leakage incidence at 8.6–41% for vertebroplasty and 7–20% for kyphoplasty, with 5.2% becoming symptomatic and occasionally life-threatening pulmonary emboli. Vendors now pair high-viscosity cement with pressure-sensor delivery guns, but reimbursement cuts in the 2024 U.S. Outpatient Prospective Payment System trimmed package payments, leaving fewer dollars to fund these premium safety accessories.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Implant Type: Vertebral Systems Outpace Traditional Fixation

Vertebral augmentation systems are forecast to clock a 6.76% CAGR through 2031. Fixation devices generated 58.30% of 2025 revenue but now face generic competition in plating and nailing. Cement toolkits remain the smallest slice yet ride the shift toward fenestrated hardware and calcium-phosphate cements.

Surgeons are demanding expandable implants that restore height and use smaller cement volumes, opening the door to differentiated pricing. FDA clearance of Medtronic’s Catalyft PTC for tibial applications hints at expansion beyond the spine. Suppliers that harmonize delivery devices, PMMA cartridges, and fenestrated screws within a single kit are capturing purchasing-committee preference for integrated solutions.

By Fracture Site: Vertebral Compression Fractures Gain Diagnostic Visibility

Hip and proximal femur fractures still accounted for 38.63% of revenue in 2025, as emergency-department protocols ensure near-universal surgical intervention. Yet vertebral compression fractures logged the fastest growth, with a 6.95% CAGR, as opportunistic CT scanning and Fracture Liaison Services highlight silent wedge deformities. The orthopedic fracture-repairing implants for osteoporosis market share for vertebral cases is expected to surge significantly by 2031.

Distal radius practice is shifting toward low-profile volar plates, allowing immediate wrist motion, while proximal humerus management is turning to cement-augmented screws after randomized data confirmed lower varus collapse. Minimally invasive navigation-guided screws now make pelvic fixation possible in frail octogenarians, expanding a niche that once defaulted to bed rest.

By Material: PEEK and Bioabsorbables Challenge Titanium Hegemony

Titanium maintained a 34.86% revenue share in 2025, but PEEK plates, rods, and cages are growing at 7.03% annually as radiology departments prefer artifact-free images. The orthopedic fracture-repairing implants for osteoporosis market share of PEEK is set to cross USD 1.4 billion by 2031. Stainless steel is ceding Western markets but holding its ground in value-oriented segments across South Asia. Magnesium-alloy screws that fully resorb over 12–18 months provide infection mitigation in diabetic ankles and earned a CE mark in January 2025. Because no single material meets all indications, vendors now offer multi-material menus and in-service surgeons to guide selection algorithms.

By End User: Specialty Centers Capture Complex Cases

Hospitals delivered 57.18% of the 2025 spend by absorbing acute trauma, but specialty orthopedic centers are advancing 7.14% a year. Ambulatory surgical centers conduct almost 40,000 total knee replacements already, and are adding percutaneous fracture repairs under local anesthesia. For suppliers, a bifurcated channel requires stripped-down, single-use kits for cost-driven ASCs and robotics-integrated premium implants for innovation-seeking specialty centers.

Geography Analysis

North America generated 43.18% of global revenue in 2025, buoyed by Medicare’s separate payment for device-intensive procedures. Asia-Pacific is the growth engine, with a 7.5% CAGR by 2031 as China and India scale trauma infrastructure. Europe benefits from integrated secondary-prevention networks that funnel fragility-fracture patients to surgeons at a rate 20–30 points above minimally organized systems.

South America and the Middle East are trailing, but GCC governments are funding orthopedic centers of excellence, and Brazil’s aging urban cohort is driving demand for hip nails. The orthopedic fracture-repairing implants for osteoporosis market share in Asia-Pacific is forecast to surge significantly by 2031.

Competitive Landscape

Johnson & Johnson (DePuy Synthes), Stryker, Zimmer Biomet, and Medtronic collectively held the majority of 2025 revenue, giving the field a moderate concentration. All four align product roadmaps around three pillars: robotics, expandable cementable implants, and cross-portfolio kitting. Globus Medical’s ExcelsiusGPS surpassed 200,000 cumulative screw placements by September 2024, underscoring the flywheel in navigation-guided fixation. Stryker bought Vexim to secure its SpineJack technology, while Zimmer Biomet’s Rosa Knee update now tackles malunited fractures. Chinese challengers Weigao and Double Medical already control double-digit domestic market share in Tier-2 hospitals through lower pricing and greater agility in public tenders. Disruptors such as OSSIO and Bioretec target bioabsorbable niches that incumbent metal players have ignored, and Merit Medical pushes steerable cement cannulas that cut leakage. With the EU-MDR tightening post-market evidence requirements, small, pure-play companies must either expand their regulatory budgets or license their technology to larger partners.

Orthopedic Fracture Repair Implants For Osteoporosis Industry Leaders

Johnson & Johnson

Stryker Corporation

Zimmer Biomet Holdings, Inc

Medtronic Plc

Globus Medical

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: The University of Utah's Orthopaedic Innovation Center received FDA clearance for its CoAptix S 7.5mm System.

- January 2025: Stryker announced the proposed divestiture of its spine business, signaling a strategic refocusing of its orthopedic portfolio.

- January 2025: Zimmer Biomet reached an agreement to acquire Paragon 28, a move aimed at strengthening its foot and ankle portfolio, which is a high-growth area for osteoporotic fracture treatment.

Global Orthopedic Fracture Repair Implants For Osteoporosis Market Report Scope

As per the scope of the report, orthopedic implants for repairing osteoporotic fractures are specialized medical devices designed to provide immediate mechanical stability and promote healing in bone that has become brittle and thin due to low bone mineral density. Because osteoporotic bone often lacks the structural integrity to hold traditional hardware, surgeons frequently use locking plates and screws, which create a fixed-angle construct that does not rely solely on the surrounding bone for purchase.

The Orthopedic Fracture Repair Implants For Osteoporosis Market is segmented by implant type, fracture site, material, end users, and geography. By implant type, the market is segmented into fixation devices, vertebral augmentation, and cement delivery & augmentation toolkits. By fracture site, the market is segmented into hip/proximal femur (intertrochanteric, femoral neck, subtrochanteric), vertebral compression fractures (thoracic/lumbar), distal radius (colles/smith), proximal humerus, pelvic ring & acetabular fractures in the elderly, proximal tibia, and ankle fractures. By material, the market is segmented into titanium & Ti alloys, stainless steel, cobalt–chromium alloys, bioabsorbable polymers (PLLA/PGA), PEEK & carbon fiber–reinforced polymers, PMMA bone cement, calcium phosphate/calc. sulphate cements. By end users, the market is segmented into hospitals (acute-care), ambulatory surgical centers (ASCs), and specialty orthopedic & spine centers.

By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Fixation Devices |

| Vertebral augmentation |

| Cement delivery & augmentation toolkits |

| Hip/proximal femur (intertrochanteric, femoral neck, subtrochanteric) |

| Vertebral compression fractures (thoracic/lumbar) |

| Distal radius (Colles/Smith) |

| Proximal humerus |

| Pelvic ring & acetabular fractures in elderly |

| Proximal tibia |

| Ankle fractures |

| Titanium & Ti alloys |

| Stainless steel |

| Cobalt–chromium alloys |

| Bioabsorbable polymers (PLLA/PGA) |

| PEEK & carbon fiber–reinforced polymers |

| PMMA bone cement |

| Calcium phosphate/Calcium sulphate cements |

| Hospitals |

| Ambulatory Surgical Centers (ASCs) |

| Other End Users (Specialty orthopedic & spine centers) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Implant Type | Fixation Devices | |

| Vertebral augmentation | ||

| Cement delivery & augmentation toolkits | ||

| By Fracture Site | Hip/proximal femur (intertrochanteric, femoral neck, subtrochanteric) | |

| Vertebral compression fractures (thoracic/lumbar) | ||

| Distal radius (Colles/Smith) | ||

| Proximal humerus | ||

| Pelvic ring & acetabular fractures in elderly | ||

| Proximal tibia | ||

| Ankle fractures | ||

| By Material | Titanium & Ti alloys | |

| Stainless steel | ||

| Cobalt–chromium alloys | ||

| Bioabsorbable polymers (PLLA/PGA) | ||

| PEEK & carbon fiber–reinforced polymers | ||

| PMMA bone cement | ||

| Calcium phosphate/Calcium sulphate cements | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers (ASCs) | ||

| Other End Users (Specialty orthopedic & spine centers) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of orthopedic fracture repairing implants for osteoporosis in 2031?

The market is on course to reach USD 8.9 billion by 2031, expanding at a 6.33% CAGR from 2026 to 2031.

Which implant segment is growing fastest?

Vertebral augmentation systems are advancing at a 6.76% CAGR through 2031 as expandable implants and high-viscosity cements gain favor.

Why are PEEK and carbon fiber implants gaining share?

Surgeons prefer radiolucent materials for postoperative CT and MRI, and these polymers mitigate stress shielding in osteopenic bone.

Which region offers the highest growth opportunity?

Asia-Pacific is forecast to rise at 7.5% CAGR by 2031 due to rapid urbanization, demographic aging, and expanding private orthopedic capacity.

Page last updated on: