Organic Infant Formula Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 11.24 Billion |

| Market Size (2031) | USD 13.62 Billion |

| Growth Rate (2026 - 2031) | 4.35% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Organic Infant Formula Market Analysis by Mordor Intelligence

The Organic infant formula market size is projected to expand from USD 10.21 billion in 2025 to USD 11.24 billion in 2026 and to USD 13.62 billion by 2031, registering a CAGR of 4.35% between 2026 and 2031. Parents are checking ingredient lists more closely, and that behavior keeps shifting demand toward certified organic products in North America and Western Europe, where organic food spending and premium baby nutrition demand stayed firm in 2025 and 2026. The Organic infant formula market is also gaining support from direct-to-consumer subscription models and online retail because these channels lower the barrier for trial, repeat purchase, and national expansion for specialist brands. Regulatory review is also raising the quality bar, and the FDA’s 2025 request for information on infant formula nutrients and contaminants favors producers that already operate with tighter sourcing and formulation controls. Demand is widening beyond the most mature countries as premium nutrition spending rises in parts of Asia, with Danone reporting that its super premium infant milk formula segment in India grew 2 times faster than the broader market in FY2024. The Organic infant formula market still faces a measured growth path because certified organic dairy supply remains limited, product prices stay well above conventional formula, and household budget pressure can slow repeat purchases even when trial demand is healthy

Key Report Takeaways

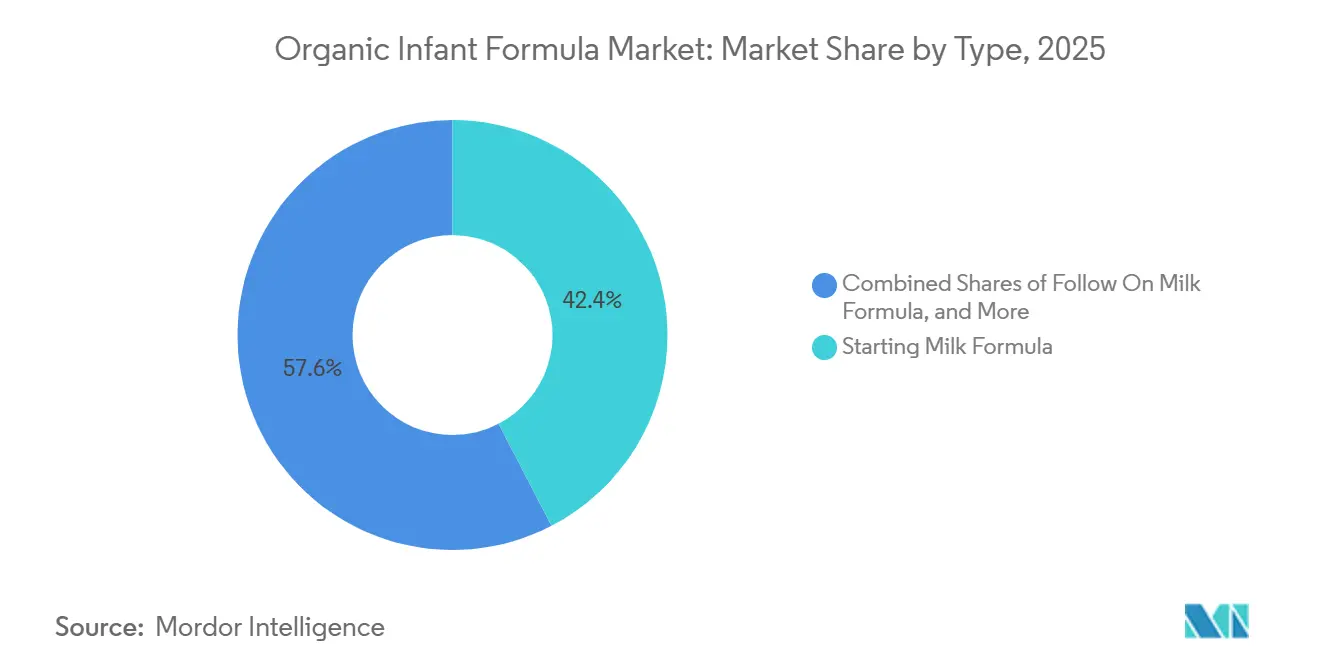

- By type, Starting Milk Formula held a 42.38% share in 2025, while Follow-On Milk Formula is projected to expand at a 5.56% CAGR through 2031.

- By form, Powder accounted for 85.52% of the Organic infant formula market size in 2025, while Liquid is forecast to grow at a 6.02% CAGR through 2031.

- By geography, North America held 46.21% of the Organic infant formula market share in 2025, while Asia-Pacific is projected to expand at a 6.5% CAGR through 2031.

- By geography, North America held 46.2% of the Organic infant formula market share in 2025, while Asia-Pacific is projected to expand at a 6.548 CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Organic Infant Formula Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Consumer Preference for Organic Nutrition | +0.9% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Increasing Birth Rates in Emerging Economies | +0.5% | South and Southeast Asia, Middle East and Africa, South America | Long term (≥ 4 years) |

| Rising Disposable Income and Premiumization Trends | +0.7% | Asia-Pacific, especially China and India, and North America | Medium term (2-4 years) |

| Product Innovation and Specialized Formulations | +0.6% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Growing Demand for Clean-Label and Non-GMO Products | +0.5% | North America and the European Union, with early signals in East Asia | Short term (≤ 2 years) |

| Growth of E-commerce and Direct-to-Consumer Channels | +0.4% | Global, with Asia-Pacific as the core market and spillover to the Middle East and Africa | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Consumer Preference for Organic Nutrition

The Organic infant formula market is benefiting from a change in how parents define acceptable product quality, especially in early life nutrition. Organic status is no longer viewed only as a premium feature, because many households now connect it with lower exposure to synthetic additives, pesticide residues, and genetically modified inputs. Germany’s organic food and beverage spending rose 6.7% in 2025, which shows that premium food purchasing remained resilient in a large and closely regulated consumer base[1]Source: Bund Ökologische Lebensmittelwirtschaft, “Umsatzentwicklung, Absatz und Importe beim deutschen Bio-Markt,”, boelw.de. The same shift is visible in infant nutrition, where parents are paying closer attention to certification breadth, ingredient sourcing, and manufacturing standards. Nara Organics used that demand pattern in its January 2026 Target launch, presenting a Germany-made formula that met both U.S. and European food safety expectations while also carrying USDA organic certification. This makes the Organic infant formula market more favorable for brands that can combine certification credibility, premium positioning, and repeat purchase systems.

Rising Disposable Income and Premiumization Trends

The Organic infant formula market is also being lifted by higher spending power in urban households that treat infant nutrition as a priority category rather than a discretionary one. That pattern is strongest where middle-income and upper-income parents are trading up to products that signal both safety and superior nutrition. Danone reported that its super-premium infant milk formula segment in India grew 2 times faster than the broader market in FY2024, which supports the view that premium early life nutrition is finding a larger customer base in South Asia. The effect is not uniform across countries, because mature Western markets still lean toward value-anchored premium tiers, while faster-developing Asian markets can support sharper jumps into ultra-premium positioning. Even so, the Organic infant formula market gains from both paths, because one supports household penetration and the other supports higher revenue per buyer. This creates room for brands to build tiered portfolios that range from core certified organic lines to more advanced premium variants without weakening the category’s quality image.

Product Innovation and Specialized Formulations

The Organic infant formula market is moving beyond a simple clean-label proposition and toward products that combine organic sourcing with more tailored nutritional positioning. Whole milk formulations have become more visible in 2025 and 2026, which reflects demand for products that align more closely with premium European formula styles and fuller fat profiles. Bobbie launched the first USDA Organic Whole Milk Infant Formula manufactured in the United States in April 2025, and the company highlighted naturally occurring milk fat globule membrane and extensive batch-level safety checks as part of its value proposition. Little Spoon entered the category in March 2026 with an organic grass-fed whole milk formula that used New Zealand whole milk, prebiotics, and plant-based DHA, which shows that new entrants are trying to pair premium sourcing with broader nutrition claims. Holle’s portfolio also supports this direction because it spans classic infant formula, goat milk options, and ready-to-feed offerings within a premium organic framework. As a result, the Organic infant formula market is becoming more segmented by formulation philosophy, clinical use case, and convenience level, which gives brands more ways to widen revenue without competing only on price.

Growth of E-commerce and Direct-to-Consumer Channels

The Organic infant formula market is seeing a structural channel shift because online retail now serves both as a sales route and as a discovery engine for new brands. Direct-to-consumer models matter in this category because subscription purchasing improves demand visibility and reduces the risk tied to inventory planning, especially for smaller brands. Bobbie’s expansion into Costco and other national retailers followed strong online demand signals, and the company stated that its Costco.com launch in July 2025 doubled weekly sales goals before it secured in-store placement. Nara Organics followed a similar sequence, first building its presence through direct sales and then moving into Target for its first retail launch in January 2026. This pattern improves access, supports repeat buying, and gives specialist brands a route to national coverage without relying first on heavy shelf placement spending. The Organic infant formula market is therefore becoming more open to younger brands that can build trust online before they scale into mass retail.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Product Prices Compared to Conventional Formula | -0.6% | Global, with the highest friction in South Asia, the Middle East and Africa, and South America | Long term (≥ 4 years) |

| Strict Regulatory and Certification Requirements | -0.4% | Global, with the highest friction in China, the European Union, and the United States | Medium term (2-4 years) |

| Limited Consumer Awareness in Developing Markets | -0.4% | Sub-Saharan Africa and rural South and Southeast Asia | Long term (≥ 4 years) |

| Economic Uncertainty and Inflationary Pressures | -0.5% | Global, with acute pressure in Europe and South America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Product Prices Compared to Conventional Formula

The Organic infant formula market continues to face a clear price barrier, and that barrier is rooted in both production economics and premium brand positioning. Bobbie priced its USDA organic whole milk formula at USD 28 per 14-ounce can in April 2025, while Nara Organics entered Target at USD 44.99 per can in January 2026, which shows how large the price gap can remain even within the premium tier. Bellamy’s Organic has also highlighted the scarcity of certified organic dairy inputs, and that limited supply base keeps raw material costs structurally high. High prices narrow the addressable customer base in emerging economies, where rising birth rates do not automatically translate into premium formula adoption. They also create churn risk later in the feeding cycle because households that start with organic products may not sustain the premium through follow-on stages. This means the Organic infant formula market can grow in value even when volume expansion remains restrained.

Strict Regulatory and Certification Requirements

The Organic infant formula market also faces a heavy compliance burden because infant formula is already tightly controlled, and organic certification adds another layer of documentation, audits, and ingredient discipline. In the United States, the FDA opened a formal request for information on infant formula nutrient requirements in May 2025, which was the first comprehensive review of this kind in decades[2]Source: U.S. Food and Drug Administration, “Infant Formula Nutrient Requirements, Request for Information,” Federal Register, federalregister.gov. That review raised the focus on nutrient standards, heavy metals, and contaminant testing, which can trigger reformulation work and further validation costs for producers. In Europe, the category already operates against a high-quality backdrop, and premium brands such as Holle differentiate further through biodynamic and advanced organic credentials that are not easy for new entrants to match. This raises the threshold for participation and slows the pace at which smaller firms can move from niche direct sales into larger-scale retail distribution. The Organic infant formula market therefore rewards brands with stronger regulatory capability, deeper supplier control, and more patient capital.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Starter Formula Holds Scale While Follow-On Milk Formula Expands Faster

Starting Milk Formula held 42.38% of the Organic infant formula market share in 2025, while Follow-On Milk Formula is projected to grow at a 5.56% CAGR through 2031. The first stage remains the volume anchor because infants in the 0 to 6 month window consume formula more intensively when breastfeeding is not the sole nutrition source. Parents also face the highest emotional and clinical stakes at this point, so they tend to favor established organic brands with clear certifications and strong safety signals. This pattern keeps starter products central to shelf space, pediatric trust, and early subscription enrollment across the Organic infant formula market. It also shows how the organic infant formula industry still depends on trust built at the beginning of the feeding journey.

Follow-On Milk Formula is growing faster because many parents who start with organic products prefer continuity rather than a switch to conventional alternatives later. That continuation effect is commercially important, since it extends customer lifetime value and gives brands more time to build loyalty, cross sell, and protect retention. Special Milk Formula remains smaller, but it is strategically important because clinically driven needs can reduce price sensitivity and support stronger margins. Holle’s goat milk range points to demand for alternatives that sit at the intersection of premium sourcing, digestibility claims, and organic positioning. Other product types, including goat milk and plant influenced variants, are widening the Organic infant formula market by serving households that want differentiated nutrition rather than only a standard organic offer.

By Form: Powder Retains Scale While Liquid Gains Urban Appeal

Powder held 85.52% share in 2025, making it the clear base form across the Organic infant formula market. Powder keeps its lead because it is easier to store, easier to ship, and less demanding for retailers and distributors than liquid formats. Those practical advantages matter even more in markets where cold chain capacity is limited, and parents are already accustomed to powder preparation. This also reflects the underlying structure of the organic infant formula industry, where cost control and distribution reach still depend heavily on shelf-stable products. Powder therefore remains the default format for brands trying to scale nationally or enter newer markets without excessive logistics costs.

Liquid is forecast to grow at a 6.02% CAGR through 2031, driven by parents who value speed, convenience, and preparation control. Ready-to-feed formats remove the need for water mixing, which appeals to hospital discharge channels, travel use, and urban households with less time for preparation. Holle’s ready-to-feed organic products reflect this demand, and they show that convenience is becoming a stronger premium factor within the category. Liquid also benefits from a stronger safety perception in some households, since sealed and premeasured packs reduce the chance of preparation error. Over time, that should give the Organic infant formula market a wider mix of premium price points, even if powder continues to dominate total volume and value.

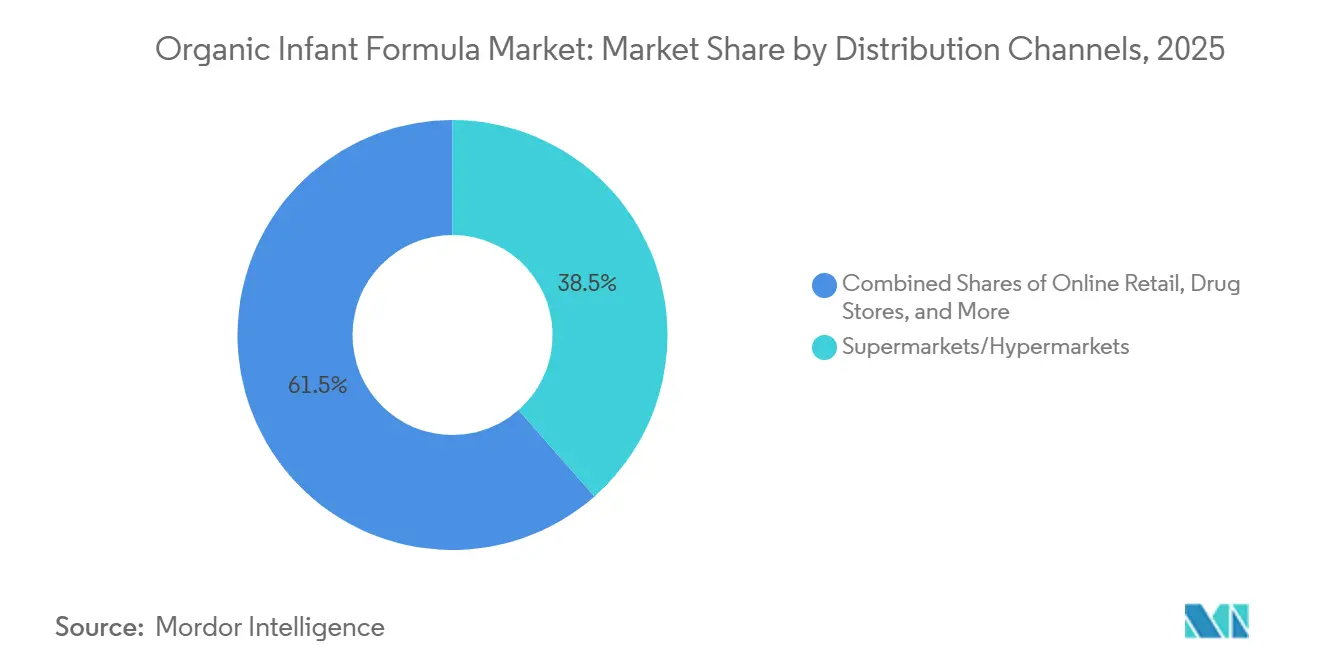

By Distribution Channels: Supermarkets Lead While Online Retail Widens Reach

Supermarkets and hypermarkets held a 38.52% share in 2025, which kept them as the largest distribution route in the Organic infant formula market. Large format stores still matter because first-time buyers often want to inspect certifications, compare labels, and buy from visible national retailers before they commit to repeat purchases. This keeps physical retail important for trust building, especially in a category where safety and authenticity shape almost every purchase decision. The same pattern illustrates a broader feature of the organic infant formula industry, because premium products still need offline visibility to convert mainstream households. National chain launches from Bobbie and Nara Organics show how retail placement remains a major milestone for scale and brand validation.

Online retail is projected to grow at a 5.76% CAGR through 2031, and its role goes well beyond simple transaction volume. Direct sales channels help brands test pricing, read consumer feedback quickly, and build subscriptions before committing to a large retail rollout. Bobbie used that model effectively, first growing through direct sales and then widening reach through Costco, Walmart, Meijer, Wegmans, and other national accounts. Nara Organics followed a similar path from direct launch to Target placement, which supports the view that digital first entry is becoming a standard route for premium specialist brands. This gives the Organic infant formula market a more flexible channel mix, where online platforms generate demand and physical stores confirm legitimacy at scale.

Geography Analysis

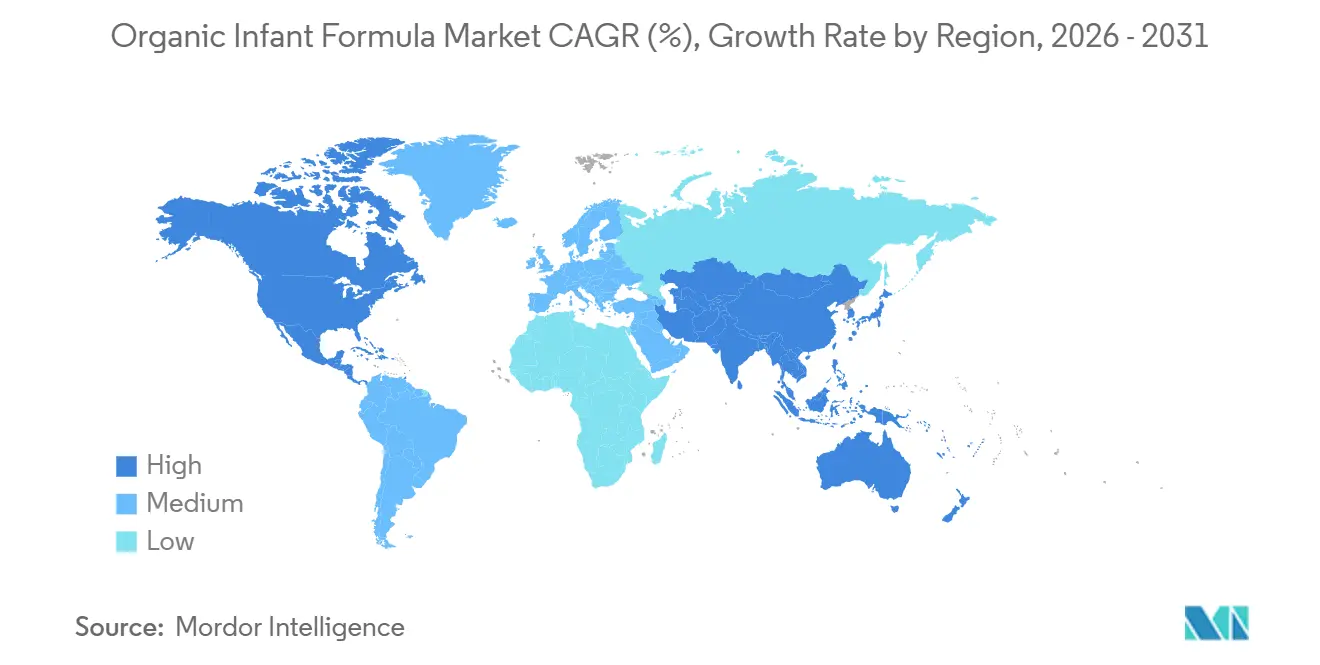

North America held 46.21% of the Organic infant formula market share in 2025, which made it the largest regional contributor. The region benefits from a mature certification framework, higher health spending, and faster acceptance of direct-to-consumer subscription models. The United States remains the core market, and FDA review activity has raised the visibility of nutrient standards and contaminant control across the category. Bobbie also opened a new manufacturing facility in Heath, Ohio, in July 2024, which strengthened domestic supply capability and added redundancy after the industry’s earlier supply disruption. Canada adds a smaller but aligned premium demand base, while Mexico presents a more developing opportunity as modern retail and middle-income demand improve access to imported and premium baby nutrition.

Asia-Pacific is projected to grow at a 6.48% CAGR through 2031, making it the fastest-growing region in the Organic infant formula market. Growth in this region is being supported by rising disposable income, stronger premium nutrition demand, and wider use of digital shopping channels. India stands out because Danone reported that its super-premium infant milk formula segment grew 2 times faster than the broader market in FY2024, which points to expanding headroom for premium offerings. Southeast Asian markets are still earlier in their development path, but online platforms give specialist brands a practical route to reach urban households before they build broad store level distribution. Japan remains important for value, yet slower birth trends keep unit growth more restrained than in faster growing parts of Asia.

Europe remains the global quality benchmark for the Organic infant formula market, supported by long standing organic standards and the presence of premium specialists such as Holle. Holle’s positioning around advanced organic credentials and goat milk variants helps explain why European products continue to carry strong credibility in export markets[3]Source: Holle Baby Food AG, “Organic Infant Formula Product Range,” Holle, holle.ch. Germany’s organic food and beverage market grew 6.7% in 2025, which provided a supportive spending backdrop for premium infant nutrition. South America and the Middle East and Africa remain smaller and more price sensitive, so growth is likely to stay concentrated in affluent urban households and premium pharmacy or modern retail channels.

Competitive Landscape

The Organic infant formula market is moderately fragmented, with multinational formula groups, European specialists, and newer premium challengers all competing for shelf space and digital loyalty. Nestlé, Danone, and Abbott still bring the broadest distribution reach, the deepest manufacturing capability, and the strongest ability to absorb compliance costs. Even so, pure-play organic and premium specialist brands are reshaping the field because they speak more directly to ingredient transparency, sourcing, and subscription convenience. This has made the Organic infant formula market more dynamic than conventional formula, where scale alone can often secure a stronger advantage. It also means product story, certification depth, and channel execution carry more weight than simple breadth of portfolio.

Danone has used acquisitions to widen its nutrition exposure, completing the Kate Farms acquisition in July 2025 after acquiring Functional Formularies in 2024, which extended its reach into plant-based and organic clinical nutrition. Bobbie has taken a different route, building around domestic manufacturing, subscription demand, and stepwise retail expansion. The company opened its Ohio facility in 2024, launched U.S. manufactured USDA organic whole milk formula in April 2025, and expanded into Target nationwide in April 2026. Nara Organics also used a digital first model before moving into retail, which shows how newer brands are building traction without relying on the old store first playbook. These moves make the Organic infant formula market more competitive at the premium end, where trust and differentiation can offset the scale advantage of the largest incumbents.

European specialists continue to hold a strong position because they pair long standing organic credentials with product formats that already carry premium recognition among informed buyers. Holle is a clear example, because its portfolio supports both standard organic demand and specialized interest in goat milk and ready to feed products. At the same time, challenger brands in the United States are expanding the market rather than only taking share, since they bring new shoppers into the category through clearer messaging and stronger digital engagement. That balance between large incumbents, premium specialists, and fast growing challengers is why the Organic infant formula market remains active, investable, and open to further share shifts through 2031.

Organic Infant Formula Industry Leaders

Nestlé S.A.

Abbott Laboratories

Danone S.A.

Holle Baby Food AG

HiPP GmbH and Co. Vertrieb KG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Bobbie launched its 100% USDA Organic Whole Milk Infant Formula at Target nationwide across approximately 1,900 stores, marking the first American-made organic whole milk formula to achieve this level of mass retail distribution and significantly broadening access beyond its initial DTC debut.

- March 2026: Little Spoon entered the infant formula category with the launch of its Organic Grass-Fed Whole Milk Infant Formula, formulated with New Zealand grass-fed whole milk, prebiotics, and plant-based DHA. The product is the first American-made formula using grass-fed whole milk from New Zealand and extends the brand's feeding ecosystem from newborns through age 6.

- February 2026: Munchkin launched its first-ever infant formula range, including a Made with Organic Milk variant at USD 39.99, sourced from USDA-certified organic milk from New Zealand. The product launched exclusively at Target and munchkin.com.

- July 2025: Nara Organics officially launched its organic whole milk infant formula DTC in the United States after securing USD 32 million in funding. The product, the first FDA-registered, USDA-certified organic whole milk formula using no skim milk manufactured in Germany to EU food safety standards, was available as a starter bundle at USD 36.

Global Organic Infant Formula Market Report Scope

| Starting-Milk Formula |

| Follow-On Milk Formula |

| Special Milk Formula |

| Other Product Types |

| Powder |

| Liquid |

| Supermarkets/Hypermarkets |

| Convenience/Drug Stores |

| Conline Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Vietnam | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Type | Starting-Milk Formula | |

| Follow-On Milk Formula | ||

| Special Milk Formula | ||

| Other Product Types | ||

| By Form | Powder | |

| Liquid | ||

| By Distribution Channels | Supermarkets/Hypermarkets | |

| Convenience/Drug Stores | ||

| Conline Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Sweden | ||

| Poland | ||

| Belgium | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Vietnam | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the organic infant formula market by 2031?

The Organic infant formula market is projected to reach USD 13.62 billion by 2031, up from USD 11.24 billion in 2026.

What is driving demand for organic infant formula the most?

Parent focus on clean ingredients, trusted certifications, and premium nutrition is the main demand driver, especially in North America and Europe.

Which product type is growing the fastest through 2031?

Follow-On Milk Formula is the fastest growing type, with a projected CAGR of 5.56% through 2031.

Which form still dominates sales today?

Powder remains dominant, holding 85.52% share in 2025 because it offers better shelf life, lower logistics cost, and familiar preparation habits.

Page last updated on: