Oral Proteins And Peptides Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

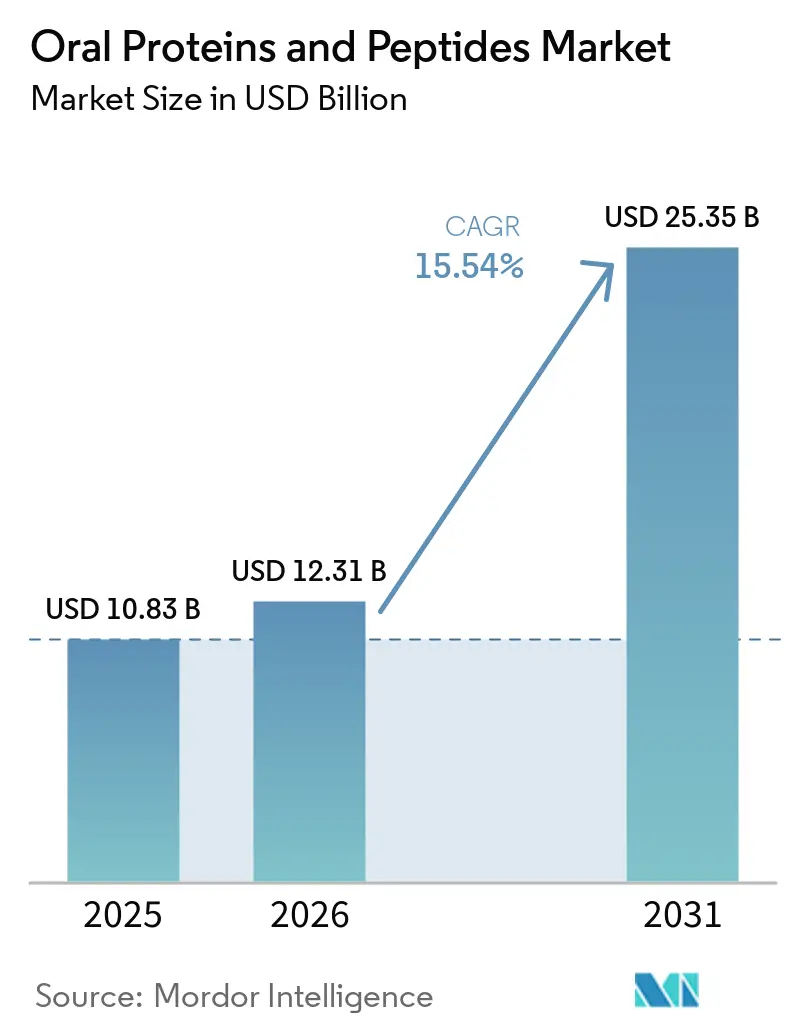

| Market Size (2026) | USD 12.31 Billion |

| Market Size (2031) | USD 25.35 Billion |

| Growth Rate (2026 - 2031) | 15.54% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Oral Proteins And Peptides Market Analysis by Mordor Intelligence

The Oral Proteins And Peptides Market size was valued at USD 10.83 billion in 2025 and is estimated to grow from USD 12.31 billion in 2026 to reach USD 25.35 billion by 2031, at a CAGR of 15.54% during the forecast period (2026-2031).

Sustained momentum in glucagon-like peptide-1 (GLP-1) tablet launches, federal reimbursement experiments that link adherence gains to total cost of care, and rapid validation of ingestible device platforms are collectively recasting chronic-disease treatment paradigms. Leading payers now treat oral incretins as a population-health lever, while investors funnel record venture and licensing capital into capsule-based injectors and permeation-enhancer chemistry. At the same time, improved imaging protocols have exposed a large pool of untreated exocrine pancreatic insufficiency (EPI) patients, driving double-digit growth for high-dosage enzyme products. Finally, Japan, the European Union, and the United States have each issued modality-specific regulatory guidance, cutting both time and uncertainty for first-in-class oral biologics.

Key Report Takeaways

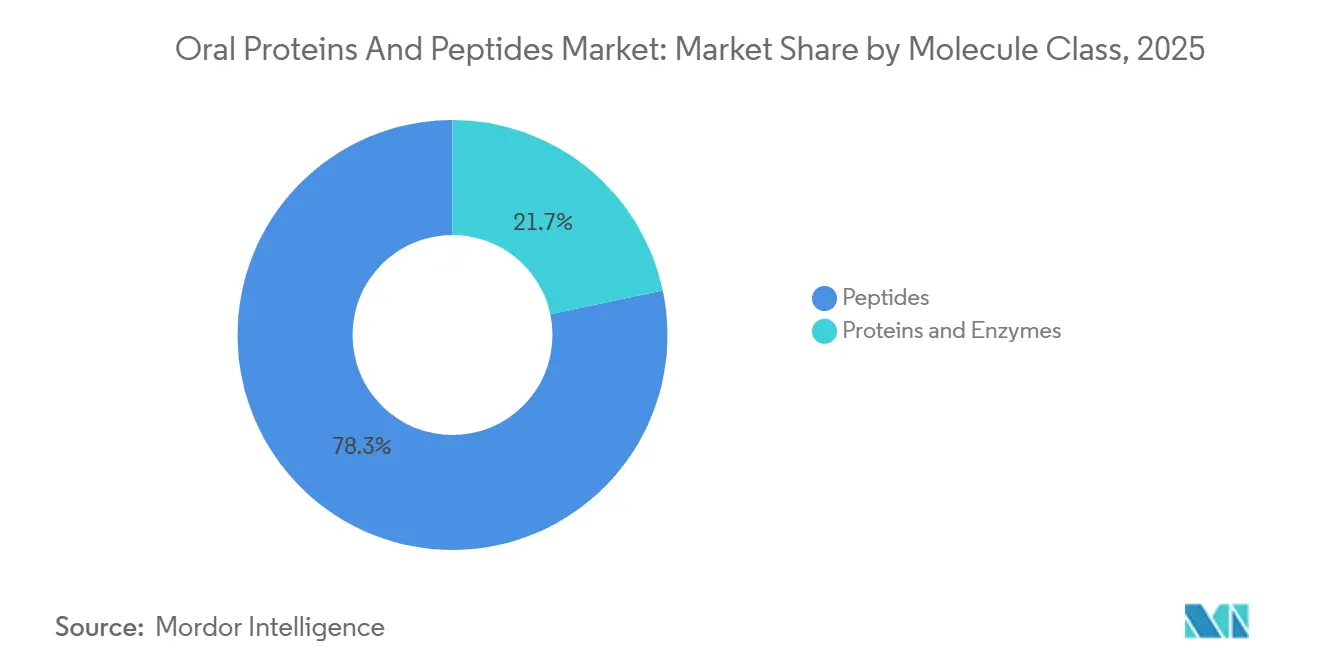

- By molecule class, peptides led with 78.31% of the oral proteins and peptides market share in 2025; proteins and enzymes are forecast to post a 16.32% CAGR to 2031.

- By drug class, GLP-1 receptor agonists dominated at 48.86% in 2025, whereas pancreatic enzymes are projected to advance at a 16.92% CAGR through 2031.

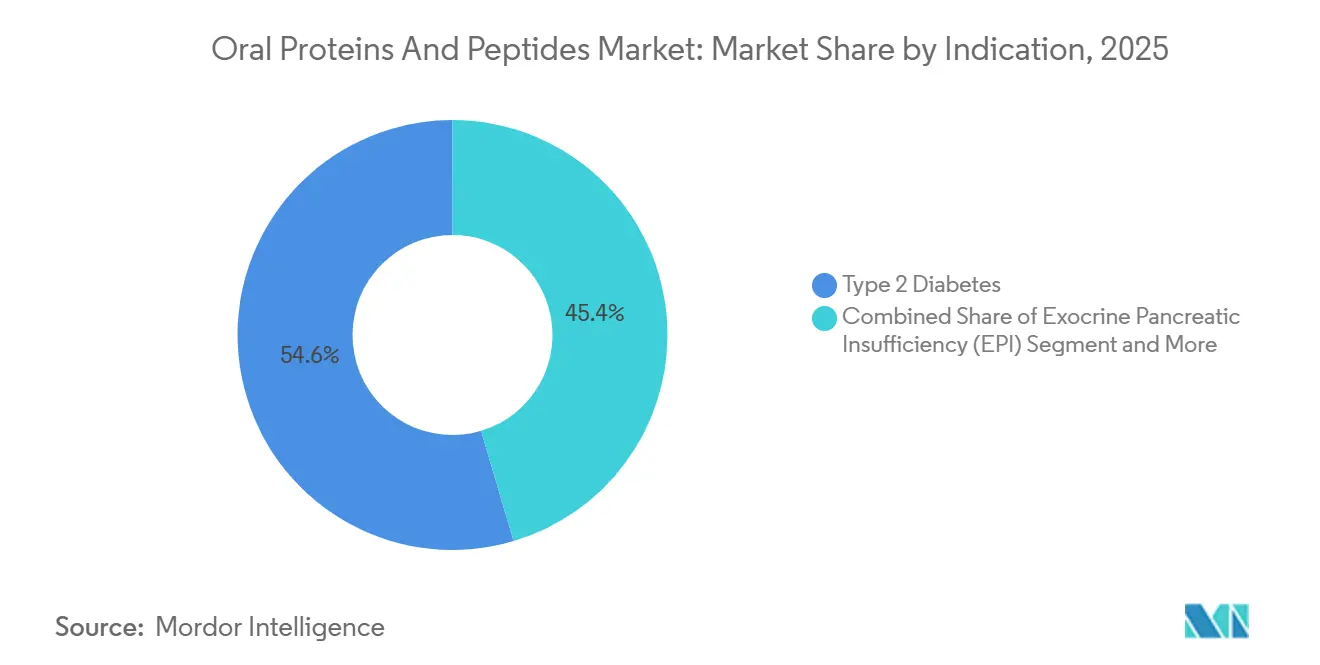

- By indication, type 2 diabetes accounted for 54.6% of 2025 revenue, while EPI is expected to record a 16.67% CAGR to 2031.

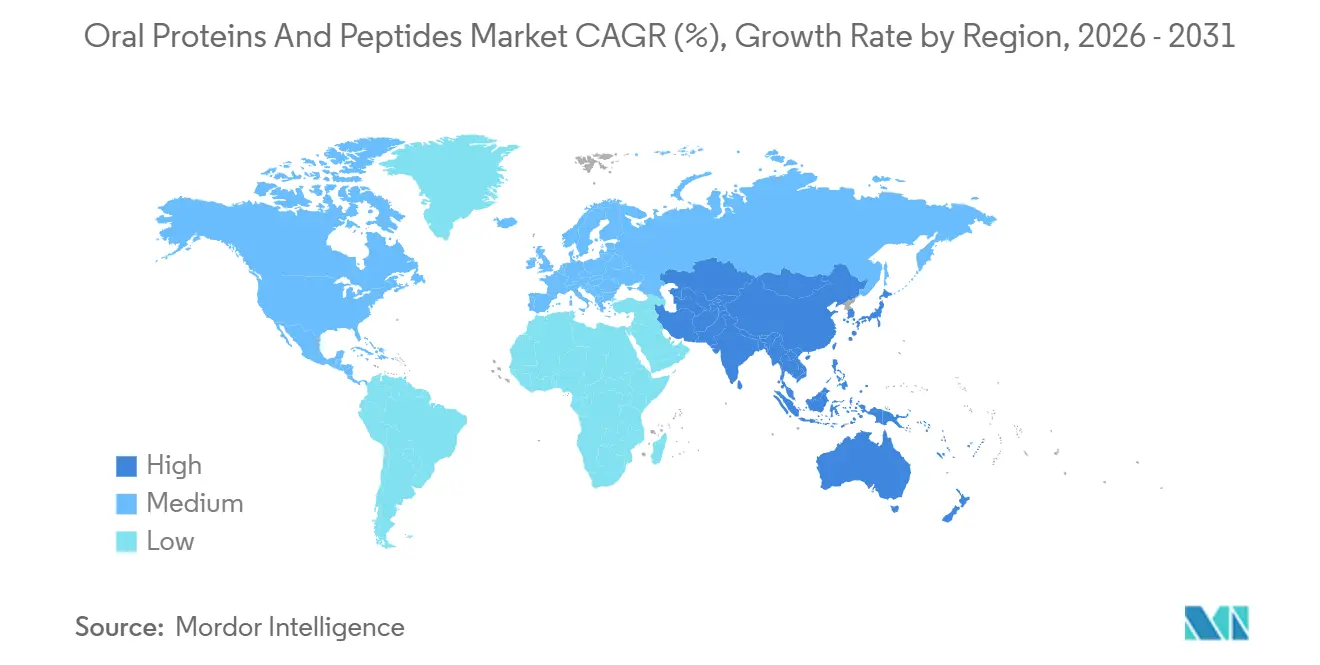

- By geography, North America captured 45.75% revenue in 2025, but Asia-Pacific is positioned to expand at a 16.12% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Oral Proteins And Peptides Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| GLP-1 oralization momentum and obesity pill launches | +4.2% | Global, early focus in North America and Europe | Short term (≤ 2 years) |

| Patient preference shift toward oral macromolecules | +2.8% | Global, especially urban Asia-Pacific | Medium term (2-4 years) |

| Regulatory tailwinds for oral peptides | +1.5% | U.S., EU, Japan | Medium term (2-4 years) |

| Next-generation ingestible devices | +2.1% | North America, Japan | Long term (≥ 4 years) |

| Colon-targeted delivery platforms | +1.3% | U.S., EU | Long term (≥ 4 years) |

| Ionic-liquid and novel excipient systems | +1.0% | North America, EU, China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

GLP-1 Oralization Momentum and Obesity Pill Launches Expand Addressable Market and Adherence

Eli Lilly’s Foundayo (orforglipron) won FDA approval in April 2026, and Novo Nordisk’s 25 mg oral semaglutide tablet reached U.S. pharmacies in January 2026, creating the first obesity-labeled peptide tablets to hit commercial scale[1]Centers for Medicare & Medicaid Services, “Medicare GLP-1 Bridge,” cms.gov. The Medicare GLP-1 Bridge demonstration, effective July 2026, reimburses both products at a USD 245 net monthly price with a USD 50 out-of-pocket cost, underscoring payer readiness to fund oral peptides that improve persistence. A 78,297-patient U.S. claims analysis found that oral semaglutide achieved 65.1% high adherence at 12 months versus 38.8% for injectables. However, an Italian observational study showed that 18-month persistence fell to 46.0% owing to gastrointestinal intolerance. The data suggest the oral proteins and peptides market will benefit when second-generation tablets reduce fasting windows and nausea rates.

Patient Preference and Adherence Shift from Injections to Oral Macromolecules in Chronic Diseases

High refill adherence correlates with lower disease activity across multiple chronic illnesses, and ease of administration drives that adherence. Real-world studies in inflammatory bowel disease linked 80% medication possession to a 70% fall in active-disease odds. Emerging oral peptides must therefore balance convenience with tolerability; strict “water-only” fasting rules and dose-related dyspepsia threaten persistence. Phase 2 and Phase 3 assets such as Structure Therapeutics’ GSBR-1290 and Hansoh Pharma’s HS-10535 aim to cut fasting windows below 10 minutes and reduce emetogenicity, suggesting future crowd-out pressure on weekly injectables.

Regulatory Tailwinds for Oral Peptides

The FDA’s December 2023 guidance spells out immunogenicity testing, hepatic-impairment protocols, and labeling specifics for peptide drugs, trimming filing risks[2]U.S. Food and Drug Administration, “Clinical Pharmacology Considerations for Peptide Drug Products,” fda.gov. Japan’s PMDA followed with a new-modalities webpage in October 2025, and Europe is harmonizing bioequivalence rules for excipient-rich tablets. Most notably, the Medicare GLP-1 Bridge demonstration reframes oral peptides as budget-impact tools rather than specialty outliers, a precedent likely to shape private-plan formularies.

Next-Generation Ingestible Devices Unlock Systemic Delivery of Large Proteins

Device-mediated capsules such as the RaniPill inflate a balloon in the jejunum and deliver microneedle injections that produced 84% bioavailability for an ustekinumab biosimilar in a Phase 1 trial[3]Rani Therapeutics, “Investor Presentation Q1 2026,” ranitherapeutics.com. A USD 1.085 billion licensing accord with Chugai in 2025 validated the economics of this approach. Biora’s BioJet and NaviCap platforms show similar promise but must address device reliability and cost-of-goods before wide payer adoption.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Very low and variable oral bioavailability | -2.5% | Global | Short term (≤ 2 years) |

| Complex CMC and enhancer/device safety evidence | -1.8% | U.S., EU | Medium term (2-4 years) |

| Long-term safety questions for potent enhancers | -1.2% | Global | Long term (≥ 4 years) |

| Molecule-specific enhancer effectiveness | -0.9% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Very Low and Variable Oral Bioavailability Drives High API Loads and Cost of Goods

Classic oral peptides rarely exceed 1% absorption, forcing 10–100× injectable doses and inflating both cost and gastrointestinal side-effects. Oral semaglutide requires 14 mg to match a 1 mg injection and still posts 50-60% coefficient-of-variation in exposure. Variability undermines the oral proteins and peptides market size economics.

Complex CMC and Stringent Regulatory Evidence for Enhancer/Device Safety

Every enhancer adds analytical, impurity, and stability tests; each ingestible device must clear drug and device rules plus human-factor engineering reviews. PMDA’s 2025 bioequivalence guidance excludes device-mediated products, pushing Japan launches past 2030 unless new frameworks emerge.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Molecule Class: Peptides Lead, Proteins Accelerate via Device Platforms

Peptides held 78.31% of the oral proteins and peptides market in 2025 thanks to entrenched GLP-1 and GC-C franchises. The oral proteins and peptides market size for proteins and enzymes is projected to expand at 16.32% CAGR as ingestible injectors sidestep gut-wall barriers. Ironwood’s LINZESS peptide reported USD 272.5 million Q1 2026 revenue, up 97% year over year, illustrating peptide resilience. In parallel, RaniPill achieved 84% bioavailability for ustekinumab biosimilar, validating protein delivery viability. The segment’s long-run upside hinges on scaling device manufacturing and proving repeat-dose intestinal safety.

Second-generation enzyme formulations also reinforce protein upside. Updated CREON and Pertzye labels now cite coefficients of fat absorption above 83%, providing clear efficacy endpoints that justify premium reimbursement. Still, proteins face steep cost-of-goods when classical oral formulations demand gram-level API loads, keeping device platforms central to growth.

By Drug Class: GLP-1 Dominance Meets Pancreatic Enzyme Acceleration

GLP-1 receptor agonists commanded 48.86% of oral proteins and peptides market share in 2025 on the back of Rybelsus and Wegovy tablets. The oral proteins and peptides market size linked to pancreatic enzymes, though smaller today, is forecast to advance 16.92% CAGR, reflecting underdiagnosis correction in EPI. CMS now reimburses Foundayo and Wegovy tablets for both diabetes and weight management, accelerating GLP-1 uptake. Yet gastrointestinal adverse events remain a leading discontinuation trigger, tilting development toward better-tolerated macrocyclics and dual-agonists.

GC-C agonists, led by LINZESS, posted a 97% top-line jump in Q1 2026 and provide a blueprint for segment durability. Somatostatin analogs and vasopressin derivatives remain niche, restrained by exposure variability that regulators struggle to reconcile with tight therapeutic windows.

By Indication: Type 2 Diabetes Leadership, EPI Fastest Growth

Type 2 diabetes generated 54.6% of 2025 revenue, but EPI is set to grow fastest at 16.67% CAGR through 2031. Obesity, now a distinct indication with Foundayo and Wegovy tablets, represents an expanding adjacency that converts injection-averse populations into oral peptide candidates. Meanwhile, IBS-C and chronic idiopathic constipation maintain mid-teen growth fueled by GC-C agonist adoption.

Label revisions for CREON and Pertzye that document fat-absorption improvements support pay-for-performance contracting, driving EPI therapy uptake. Conversely, acromegaly remains a limited market until variability challenges for oral octreotide are overcome.

Geography Analysis

North America retained 45.75% of 2025 revenue, bolstered by payer initiatives like the Medicare GLP-1 Bridge and clear FDA peptide guidance. The region also hosts most ingestible-device clinical sites, positioning it to capture early protein-delivery upside. Yet real-world adherence gaps driven by gastrointestinal side-effects cap long-term share gains.

Europe benefits from centralized health-technology assessments that welcome oral options when they lower nurse-administered costs. EMA alignment on peptide bioequivalence lowers filing risk, encouraging biosimilar entrants that could compress price points.

Asia-Pacific is projected to record a 16.12% CAGR to 2031, supported by China’s regulatory openness to incretin innovation and Japan’s modality-specific PMDA guidance. Local manufacturing pacts, such as AstraZeneca’s USD 1.2 billion CSPC agreement, aim to regionalize supply chains, cutting tariffs and shipping cost for high-dose tablets.

South America and the Middle East & Africa remain nascent, constrained by reimbursement hurdles and limited cold-chain infrastructure. Nonetheless, rising obesity prevalence and tele-pharmacy adoption point toward future opportunities once cheaper generic peptides arrive.

Competitive Landscape

The oral proteins and peptides market hosts a mix of incumbents and platform disruptors, producing a moderate concentration profile. Novo Nordisk and Eli Lilly controlled a significant share of peptide-based obesity revenue in 2025, yet Ironwood’s 2026 surge in GC-C agonists shows room for focused specialists. AstraZeneca’s USD 1.2 billion upfront to CSPC and Rani Therapeutics’ USD 1.085 billion Chugai pact illustrate Big Pharma’s buy-versus-build calculus.

Route hedging defines strategy. Lilly pursues both oral and weekly injectable incretins; Novo splits resources among SNAC-enabled tablets and once-weekly CagriSema combinations. Device pioneers such as Rani and Biora license out platforms rather than sell finished drugs, turning capsule injectors into toll-booth business models. Meanwhile, Structure Therapeutics, Hansoh, and Viking race to Phase 3 with macrocyclic oral GLP-1s that promise shorter fasting windows.

Regulatory leverage now shapes competitive timing. Early adopters that locked SNAC and C10 supplies hold cost and formulation know-how hard to replicate quickly. Yet any safety signal for chronic enhancer use could reset the field, advantaging device approaches that bypass chemical permeation entirely.

Oral Proteins And Peptides Industry Leaders

Novo Nordisk A/S

AbbVie Inc.

AstraZeneca

Johnson & Johnson

Eli Lilly and Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Novo Nordisk shipped Ozempic tablets (1.5 mg, 4 mg, 9 mg) to U.S. wholesalers, marking the only FDA-approved oral peptide GLP-1 for adults with type 2 diabetes.

- March 2026: Johnson & Johnson received FDA clearance for ICOTYDE (icotrokinra), the first oral IL-23 receptor-blocking peptide for plaque psoriasis in adults and adolescents.

Global Oral Proteins And Peptides Market Report Scope

As per the scope of the report, oral proteins and peptides are biological molecules composed of amino acids that are intended to be administered through the oral route, meaning they are ingested by mouth. Proteins are large, complex molecules that perform various functions in the body, while peptides are shorter chains of amino acids.

The segmentation for the oral proteins and peptides market is categorized by molecule class, drug class, indication, and geography. By molecule class, it includes peptides and proteins & enzymes. By drug class, it covers GLP‑1 receptor agonists, GC‑C agonists, somatostatin receptor agonists, pancreatic enzymes, and vasopressin analogs. By indication, the market is segmented into type 2 diabetes, obesity & weight management, IBS‑C, chronic idiopathic constipation (CIC), exocrine pancreatic insufficiency (EPI), acromegaly, and others (e.g., celiac disease, inflammatory bowel disease). By geography, the market is divided into North America, Europe, Asia Pacific, Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Peptides |

| Proteins & Enzymes |

| GLP-1 receptor agonists |

| GC-C agonists |

| Somatostatin receptor agonists |

| Pancreatic enzymes |

| Vasopressin analogs |

| Type 2 Diabetes |

| Obesity & Overweight Management |

| IBS-C |

| Chronic Idiopathic Constipation (CIC) |

| Exocrine Pancreatic Insufficiency (EPI) |

| Acromegaly |

| Others (Celiac Disease, Inflammatory Bowel Disease, etc.) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Molecule Class | Peptides | |

| Proteins & Enzymes | ||

| By Drug Class | GLP-1 receptor agonists | |

| GC-C agonists | ||

| Somatostatin receptor agonists | ||

| Pancreatic enzymes | ||

| Vasopressin analogs | ||

| By Indication | Type 2 Diabetes | |

| Obesity & Overweight Management | ||

| IBS-C | ||

| Chronic Idiopathic Constipation (CIC) | ||

| Exocrine Pancreatic Insufficiency (EPI) | ||

| Acromegaly | ||

| Others (Celiac Disease, Inflammatory Bowel Disease, etc.) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large will the oral proteins and peptides market be by 2031?

The oral proteins and peptides market size will reach USD 25.35 billion by 2031, growing at a 15.54% CAGR from 2026.

Which molecule class is expanding fastest?

Proteins and enzymes, propelled by ingestible injection capsules, are forecast to post a 16.32% CAGR through 2031.

What share do GLP-1 receptor agonists hold today?

GLP-1 receptor agonists commanded 48.86% of oral proteins and peptides market share in 2025.

Which indication is likely to outpace overall growth?

Exocrine pancreatic insufficiency revenue is expected to rise at a 16.67% CAGR between 2026-2031 on improved diagnosis and enzyme therapy adoption.

How are regulators shaping the competitive timeline?

FDA peptide-specific guidance and Japan's new-modality pathways shorten review cycles, while Medicare's GLP-1 Bridge accelerates uptake by subsidizing oral formulations.

Page last updated on: