Online Charging System (OCS) Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

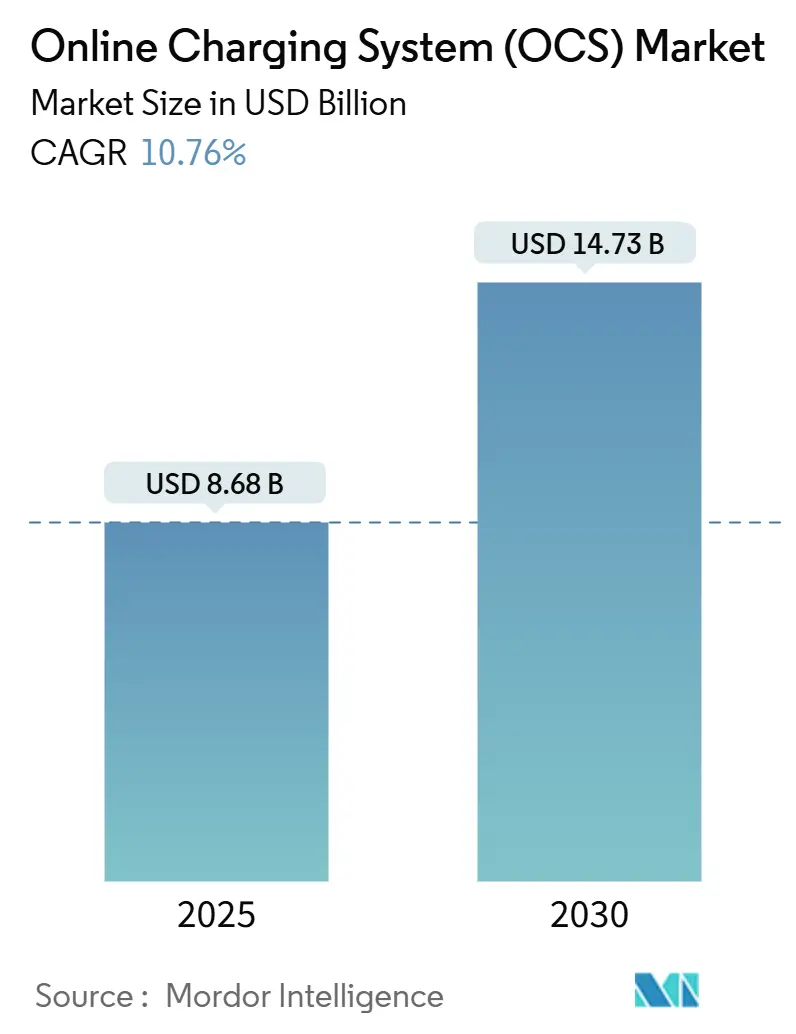

| Market Size (2025) | USD 8.68 Billion |

| Market Size (2030) | USD 14.73 Billion |

| Growth Rate (2025 - 2030) | 10.76% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Online Charging System (OCS) Market Analysis by Mordor Intelligence

The online charging system market size reached USD 8.68 billion in 2025 and is projected to hit USD 14.73 billion by 2030, expanding at a 10.76% CAGR as operators replace legacy billing with real-time convergent platforms. Demand is underpinned by 5G standalone rollouts that require sub-millisecond policy decisions, cloud-native architectures that enable dynamic pricing, and the monetization of network APIs for third-party services. Event-based charging retains the largest installed base, yet convergent charging is scaling faster as it unifies voice, data, and digital revenue streams. On-premises deployments dominate today but cloud implementations are accelerating where regulators clarify data-residency requirements. Competitive intensity remains measured because the top five vendors hold only 45% combined share, leaving scope for niche players that address IoT, edge, and cross-industry use cases.[1]TM Forum, “Assessing CSPs’ progress toward an open digital architecture,” tmforum.org

Key Report Takeaways

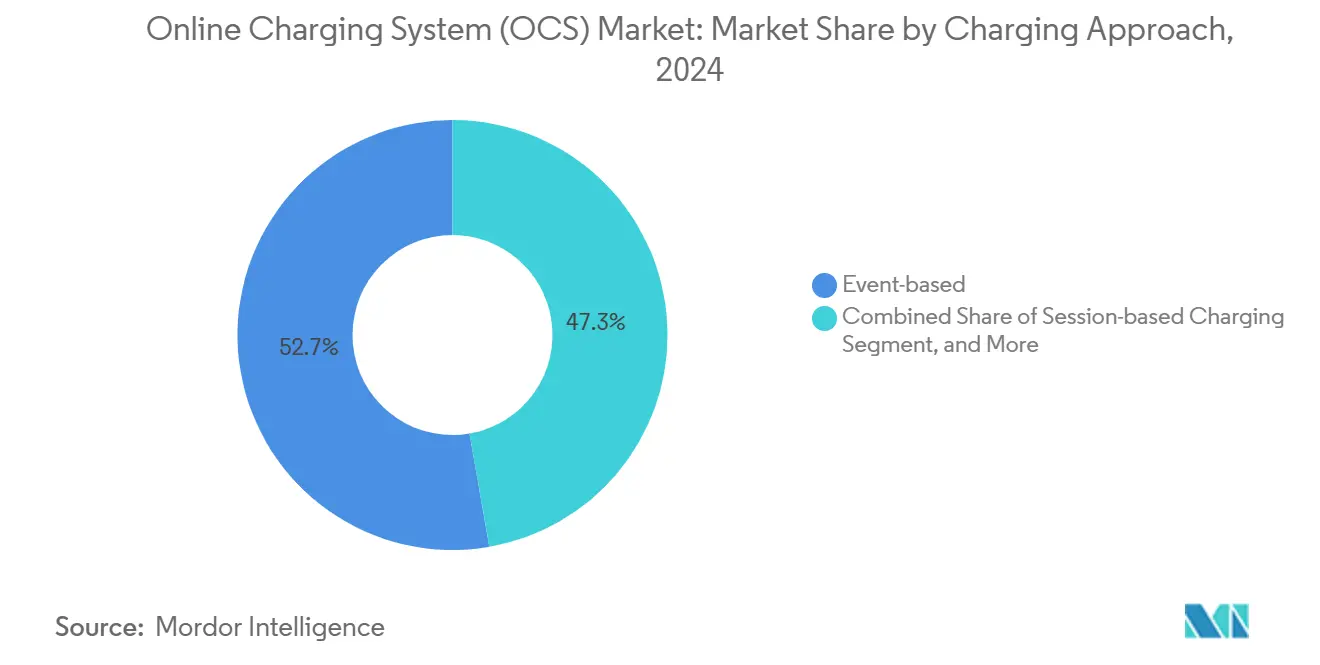

- By charging approach, event-based models led with a 52.73% online charging system market share in 2024. convergent charging systems are forecast to expand at an 11.78% CAGR to 2030.

- By deployment mode, on-premises solutions held 60.94% of the online charging system market size in 2024, while public cloud is advancing at a 12.21% CAGR through 2030.

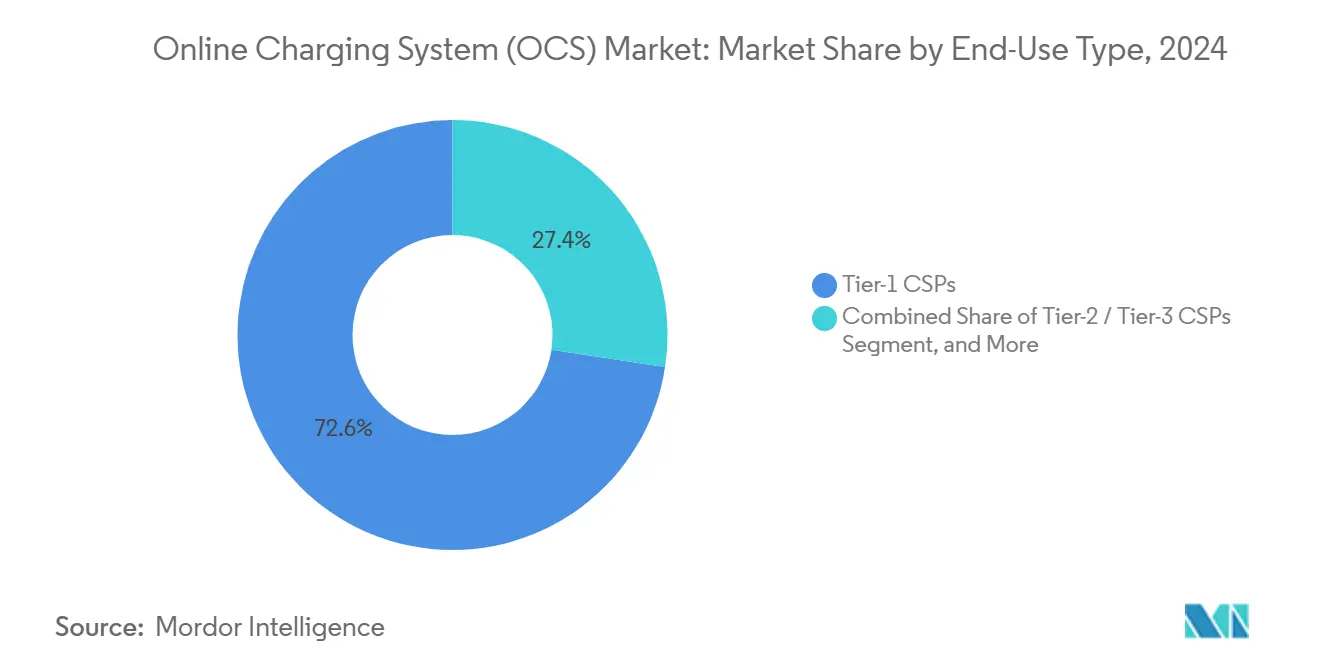

- By end-user type, Tier-1 communication service providers controlled 72.63% revenue in 2024 in the online charging system market; digital service providers are growing fastest at a 12.44% CAGR.

- By network technology, 4G/LTE controlled 46.73% revenue in 2024 in the online charging system market; 5G stand-alone (CCS) is growing fastest at a 12.44% CAGR.

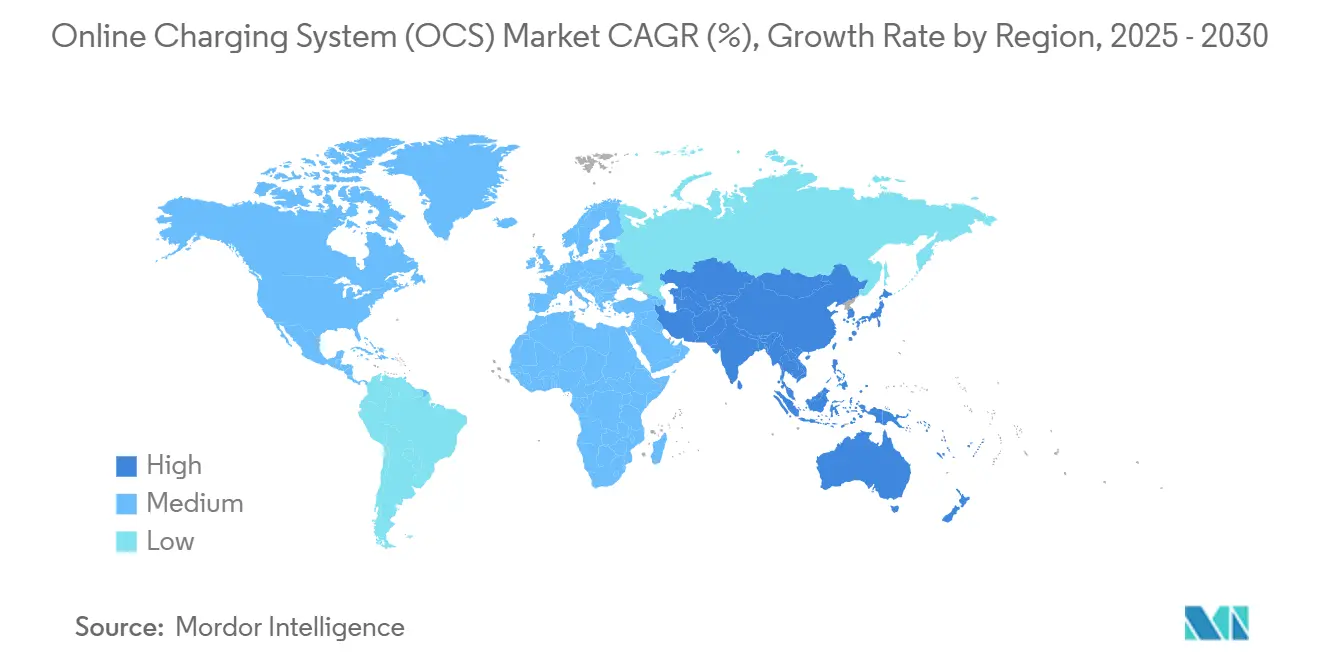

- By geography, North America accounted for a 34.82% online charging system market share in 2024, yet Asia-Pacific is climbing at an 11.56% CAGR toward 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Online Charging System (OCS) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G standalone roll-out necessitating convergent real-time charging | +2.8% | Global, with early gains in North America, EU, and APAC core markets | Medium term (2-4 years) |

| Proliferation of IoT/M2M connections demanding per-device rating | +2.1% | APAC core, spill-over to North America and MEA | Long term (≥ 4 years) |

| Cloud-native OSS/BSS adoption for cost and agility | +1.9% | Global, with regulatory constraints in EU and China | Short term (≤ 2 years) |

| Speed-based mobile data tariffs unlocking new billing dimensions | +1.4% | North America and EU, expanding to APAC | Medium term (2-4 years) |

| Plug-and-Charge PKI frameworks enabling cross-industry monetisation | +1.2% | EU and North America, with pilot deployments in APAC | Long term (≥ 4 years) |

| Non-firm grid-connection incentives spurring edge-deployed OCS | +0.8% | EU and select North American markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

5G Standalone Roll-out Necessitating Convergent Real-time Charging

Commercial 5G standalone networks depend on service-based architecture that triggers charging events within 100 milliseconds, forcing operators to retire offline mediation in favor of online systems that span legacy 3G/4G and new 5G services.[2]Ericsson, “Ericsson celebrates 50th 5G Charging CSP customer,” ericsson.comMore than 50 live deployments already handle over 150 million subscribers on cloud-native platforms. Real-time monetization now extends to network slicing, where prices adjust according to guaranteed latency and bandwidth. Releases 16 and 17 of 3GPP specifications formalize new trigger points, making comprehensive platform upgrades unavoidable.[3]3GPP, “3GPP Specifications,” 3gpp.org Operators prioritizing these upgrades report faster product launches and fewer revenue-leakage disputes, validating convergent charging as the foundational layer for 5G business models.

Proliferation of IoT/M2M Connections Demanding Per-device Rating

Billions of intermittently connected devices create micro-transactions that previously overwhelmed batch-oriented billing. GSMA guidelines call for life-cycle management that can park dormant devices, reactivate them instantly, and invoice combined fleets under multi-tier price plans.[4]GSMA, “IoT Monetization Guidelines,” gsma.com India’s M2M regulation obliges separate billing pools for machine traffic while retaining a single customer view. Low-power networks such as NB-IoT and LoRaWAN transmit only a few bytes monthly, yet they demand sub-second authentication and rating to prevent service denial. Operators therefore deploy scalable rating engines that process thousands of events per second but settle invoices only when thresholds are met, preserving profitability on ultra-low-value traffic.

Cloud-native OSS/BSS Adoption for Cost and Agility

Microservices and container orchestration shrink release cycles from months to weeks, cutting operating expense by up to 40% through automated scaling. Open Digital Architecture prescribes API-centric charging components that coexist with legacy stacks during phased migrations. Optiva demonstrated the commercial payoff by embedding Gemini-based autonomous agents that fine-tune price plans and detect anomalies in real time. The shift also unlocks public-cloud analytics and AI services, yet data-sovereignty rules push many operators toward hybrid architectures that keep customer data on-premises while offloading compute-intensive rating functions to hyperscalers.

Speed-based Mobile Data Tariffs Unlocking New Billing Dimensions

Unlimited data bundles eroded revenue, so operators began pricing guaranteed throughput and latency instead of volume. Real-time performance data now feeds directly into rating engines that adjust tariffs when measured speed drops below contract levels, ensuring fairness and compliance with net-neutrality exemptions. Subscribers can view live performance dashboards within self-care apps, aligning perceived service quality with the bill. Pilot programs in the United States and Europe achieved higher average revenue per user because customers willingly pay premiums for assured service levels, validating the model’s commercial viability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy-system integration complexity and capex burden | -1.8% | Global, with highest impact in mature markets with extensive legacy infrastructure | Short term (≤ 2 years) |

| Data-sovereignty rules slowing public-cloud deployments | -1.2% | EU, China, and select emerging markets with strict data localization requirements | Medium term (2-4 years) |

| Low TLS / PKI penetration in field devices hindering automation | -0.9% | Global, with particular impact in IoT/M2M deployments across all regions | Medium term (2-4 years) |

| Shortage of ISO-15118 / CCS skilled talent delaying projects | -0.7% | North America and EU, expanding to APAC as cross-industry charging adoption increases | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Legacy-system Integration Complexity and Capex Burden

Many operators still run more than 50 billing components that evolved over decades, generating intertwined data flows that complicate modern replacements. A full rip-and-replace can exceed USD 100 million and necessitate three-year migration windows. Overlay strategies reduce initial risk but extend parallel-system expense and technical debt. Dual operations inflate support costs, and every additional interface multiplies integration testing effort. The result is deferred transformation that hinders agility exactly when 5G monetization opportunities are strongest, compressing operator margins.

Data-sovereignty Rules Slowing Public-cloud Deployments

The EU Data Act, China’s Cybersecurity Law, and related localization statutes dictate where charging records reside and how they move across borders. Compliance forces hybrid architectures that partition customer identifiers and financial data inside national boundaries while offloading stateless functions to hyperscalers. Operators incur extra encryption, audit, and regional redundancy expenses that erode the cost advantages of pure public cloud. Vendors must therefore ship modular charging stacks that can split along data-flow lines and prove jurisdictional compliance during procurement.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Charging Approach: Convergent Systems Drive Future Growth

The convergent charging segment captured a 2025 revenue baseline of USD 4.24 billion and is forecast to record an 11.78% CAGR, outpacing the overall online charging system market. Although event-based engines still process most legacy voice and SMS traffic, operators favor convergent platforms to consolidate customer balances and enable cross-service bundles. This consolidation eliminates data reconciliation errors that plague dual-stack environments, cuts license fees, and enables single-view analytics for marketing teams.

Convergent engines also support sophisticated 5G slice billing, IoT fleet rating, and partner settlement in one runtime, capabilities that event-based stacks lack. Early adopters report shorter product-launch cycles because developers configure new price plans through declarative APIs. Regulators appreciate the simplified audit trail that convergent systems generate, reducing compliance costs. As a result, the online charging system market size for convergent platforms is projected to contribute more than 55% of total revenue by 2030.

By Deployment Mode: Public Cloud Gains Despite On-premises Dominance

On-premises solutions retained 60.94% market revenue in 2024 because operators prefer local control over sensitive billing data. Even so, public-cloud deployments are growing at 12.21% annually and could exceed 35% share by 2030, propelled by hyperscaler cost efficiencies and native AI services. Operators in Japan, Australia, and Brazil already run production-grade rating engines in multi-zone cloud regions without latency penalties.

Cloud-hosted charging cuts capex, introduces pay-as-you-grow economics, and accelerates disaster-recovery testing. Yet it imposes new responsibilities for secure key management and regulatory reporting. Vendors respond with SaaS offers that include built-in compliance dashboards and geo-fencing to satisfy regulators. The online charging system market size for public-cloud instances will rise in lockstep with clearer localization rules and growing confidence in cloud security controls.

By End-User Type: Digital Service Providers Emerge as Growth Engine

Tier-1 CSPs accounted for 72.63% revenue in 2024, reflecting their national footprints and need for high-availability charging. Nevertheless, digital service providers, ride-hailing, video-streaming, fintech, and gaming platforms, will be the fastest-growing customer group, expanding 12.44% per year through 2030. These firms rely on telecom connectivity yet demand granular, on-the-fly monetization unencumbered by legacy voice-centric billing.

DSPs favor cloud-native subscription models that scale elastically with user growth and integrate seamlessly with in-app payment gateways. Their success pressures smaller CSPs and MVNOs to adopt equally agile charging stacks to defend their niches. The online charging system industry now spans far beyond telcos, validating vendor strategies that package charging as an independent SaaS layer for any digital business.

By Network Technology: 5G Standalone Drives Premium Growth

4G/LTE still generated 46.73% of 2024 revenue, but 5G standalone captured most new deals and is projected to expand at an 11.65% CAGR, benefiting from network-slice billing, edge-compute monetization, and ultra-low-latency applications. Non-standalone 5G lacks these capabilities, so operators expedite upgrades to full standalone cores.

Standalone charging integrates with NFV and SDN controllers, allowing real-time resource pricing down to individual user planes. It also underpins API-based revenue models such as quality-on-demand and guaranteed jitter for industrial automation. As release 18 standards introduce additional chargeable events, the online charging system market size tied to standalone networks will continue to widen its lead over legacy technologies.

Geography Analysis

North America delivered 34.82% revenue in 2024 owing to early standalone launches and pragmatic data-regulation regimes that accept hybrid cloud. Operators monetize premium network slices for media, automotive, and healthcare clients who pay for deterministic performance, pushing adoption of AI-aided rating engines. Competition among three nationwide players keeps innovation brisk and churn low, cementing the region’s leadership.

Asia-Pacific is the fastest-growing territory with an 11.56% CAGR forecast through 2030, driven by greenfield 5G buildouts across India, Vietnam, and Indonesia. Governments there promote domestic cloud facilities, enabling operators to bypass legacy mainframes entirely and leapfrog to containerized charging. China’s localization mandates funnel business to domestic cloud providers, yet the scale of its subscriber base makes it a critical revenue pool for global vendors that partner with local integrators.

Europe and the Middle East continue to modernize under strict privacy and payment-transparency laws. The Alternative Fuels Infrastructure Regulation, for example, obliges real-time reporting of charging-point pricing, which telcos view as a template for cross-industry API products. Africa and South America pursue cost-optimized cloud strategies to compensate for lower ARPU, selecting SaaS charging that trades license fees for usage-based subscriptions, thereby diversifying the global online charging system market.

Competitive Landscape

The online charging system market features a moderate concentration: Oracle, Amdocs, SAP, Ericsson, and Huawei jointly control 45% revenue. These incumbents exploit long-term BSS contracts, but their monolithic architectures face pressure from pure-cloud challengers such as MATRIXX Software, Optiva, and Cerillion. Smaller vendors excel in rapid deployments and AI features, winning greenfield 5G or IoT projects where agility matters more than product breadth.

Equipment manufacturers bundle charging with core-network functions, offering single-vendor accountability that appeals to operators seeking to compress procurement cycles. Ericsson’s success with 50 live 5G charging networks exemplifies this synergy. At the same time, Optiva differentiates by embedding large-language-model agents that autonomously tune price plans and handle customer queries. Such AI-native capabilities reshape evaluation criteria from feature checklists to time-to-value metrics.

Mergers and partnerships accelerate as vendors strive for vertical integration and API standardization. The operator-led joint venture with Ericsson to commercialize network APIs spotlights a new revenue stream that requires convergent charging for partner settlement. As cross-industry monetization grows, suppliers that can prove compliance in both telecom and adjacent sectors will outpace rivals confined to legacy voice-data rating.

Online Charging System (OCS) Industry Leaders

Amdocs Limited

Oracle Corporation

SAP SE

Telefonaktiebolaget LM Ericsson

Huawei Technologies Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Optiva integrated agentic AI running on Google Gemini into its charging engine, rolling out autonomous agents for care, operations, and sales across Middle-East and American operators.

- October 2024: Ericsson surpassed 50 customers for its 5G Charging solution, with 20 live networks supporting 150 million subscribers.

- September 2024: A consortium of global telcos formed a joint venture with Ericsson to commercialize standardized network APIs aligned with CAMARA specifications, requiring unified charging interfaces for developer billing.

- September 2024: Allego began Europe-wide deployment of ISO-15118 Plug-and-Charge technology using encrypted certificates for automatic EV billing.

Global Online Charging System (OCS) Market Report Scope

| Event-based Charging |

| Session-based Charging |

| Convergent Charging System (CCS) |

| On-Premises |

| Public Cloud |

| Private Cloud |

| Hybrid Cloud |

| Tier-1 Communication Service Providers |

| Tier-2 / Tier-3 CSPs |

| Mobile Virtual Network Operators (MVNOs) |

| Digital Service Providers (DSPs) |

| 3G and Earlier |

| 4G / LTE |

| 5G Stand-Alone (CCS) |

| IoT / LPWAN |

| North America |

| South America |

| Europe |

| Asia-Pacific |

| Middle East and Africa |

| By Charging Approach | Event-based Charging |

| Session-based Charging | |

| Convergent Charging System (CCS) | |

| By Deployment Mode | On-Premises |

| Public Cloud | |

| Private Cloud | |

| Hybrid Cloud | |

| By End-User Type | Tier-1 Communication Service Providers |

| Tier-2 / Tier-3 CSPs | |

| Mobile Virtual Network Operators (MVNOs) | |

| Digital Service Providers (DSPs) | |

| By Network Technology | 3G and Earlier |

| 4G / LTE | |

| 5G Stand-Alone (CCS) | |

| IoT / LPWAN | |

| By Geography | North America |

| South America | |

| Europe | |

| Asia-Pacific | |

| Middle East and Africa |

Key Questions Answered in the Report

What revenue will the online charging system market generate by 2030?

Forecasts show the market reaching USD 14.73 billion by 2030 on a 10.76% CAGR.

Which charging approach is growing fastest in telecom billing?

Convergent charging systems are advancing at an 11.78% CAGR thanks to their ability to unify voice, data, and digital services.

How are 5G standalone networks influencing charging upgrades?

5G SA mandates real-time, sub-100 millisecond policy decisions that only online charging platforms can deliver, accelerating modernization programs.

Why are operators shifting charging to public cloud?

Hyperscale platforms lower total cost of ownership by up to 40% and provide built-in AI analytics, although data-sovereignty rules often require hybrid setups.

What role do digital service providers play in the charging ecosystem?

DSPs such as streaming or ride-hailing platforms need telecom-grade billing for connectivity-dependent services and are the fastest-growing customer segment at 12.44% CAGR.

Page last updated on: