Oncology Contract Research Organization (CRO) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 24.62 Billion |

| Market Size (2031) | USD 35.13 Billion |

| Growth Rate (2026 - 2031) | 7.36% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Oncology Contract Research Organization (CRO) Market Analysis by Mordor Intelligence

The Oncology Contract Research Organization Market size is projected to expand from USD 23.08 billion in 2025 and USD 24.62 billion in 2026 to USD 35.13 billion by 2031, registering a CAGR of 7.36% between 2026 to 2031.

Sponsor reliance on external partners keeps rising because oncology trials now blend adaptive designs, decentralized procedures, and AI-driven patient matching, all of which demand infrastructure that most developers can no longer justify maintaining in-house. Integrated CRO-CDMO platforms gained momentum in 2025 after Pfizer CentreOne and Samsung Biologics broadened combined development-to-manufacturing offerings, enabling smoother handoffs from discovery to commercial launch. Regulatory shifts also favor outsourcing: the FDA’s 2024 guidance normalized decentralized oncology trials, and China’s NMPA streamlined approvals for innovative therapies, allowing simultaneous multinational studies with fewer administrative delays. Together, these trends shorten cycle times, widen geographic trial access, and reinforce the long-run expansion of the oncology contract research organization (CRO) market.

Key Report Takeaways

- By clinical phase, Phase III trials led with 39.5% revenue share in 2025, while Phase I studies are forecast to expand at a 7.89% CAGR through 2031.

- By service type, clinical services accounted for 30% of 2025 revenue, whereas pre-clinical services are expected to grow at 7.5% CAGR between 2026 and 2031.

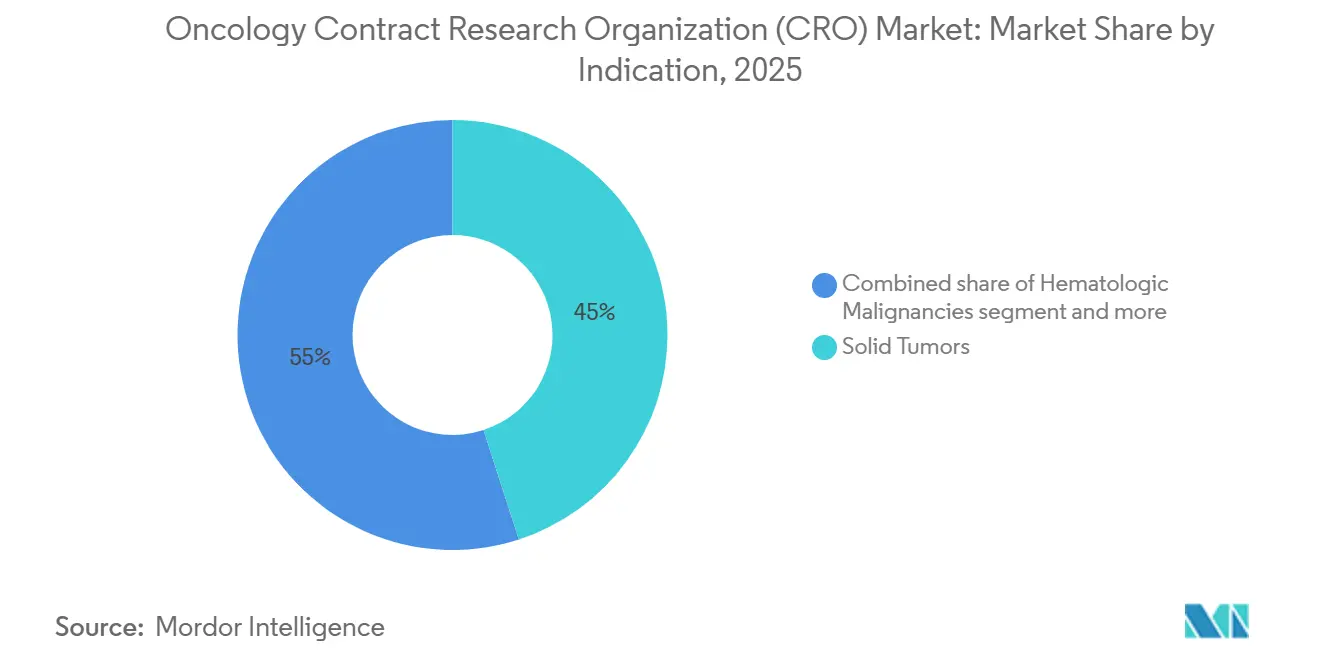

- By indication, solid tumors claimed 45% revenue share in 2025, while rare and pediatric cancers are projected to post a 7.5% CAGR to 2031.

- By end user, pharmaceutical and biopharmaceutical companies held 40.8% share in 2025, and their spending is set to grow at 7.4% CAGR over the same horizon.

- By geography, North America delivered 47.78% market share in 2025, whereas Asia-Pacific is on track for an 8.0% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Oncology Contract Research Organization (CRO) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Precision-oncology pipelines boosting outsourcing demand | +1.8% | Global, strongest in North America and Europe | Long term (≥ 4 years) |

| Rising use of complex adaptive trial designs | +1.2% | North America, Europe, Japan | Medium term (2-4 years) |

| Scale-out of decentralized / hybrid oncology trials | +1.5% | Global, early adoption in North America and Western Europe | Medium term (2-4 years) |

| AI-enabled patient-matching and site-selection efficiencies | +1.0% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Near-shoring of toxicology capacity after biosecurity rules | +0.9% | North America, Europe | Short term (≤ 2 years) |

| Convergence of CRO-CDMO one-stop oncology offerings | +1.1% | Global hubs in North America, Europe, South Korea | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Precision-Oncology Pipelines Boosting Outsourcing Demand

Molecularly targeted assets such as antibody-drug conjugates, CAR-T therapies, and bispecific T-cell engagers require narrow biomarker-based cohorts that few sponsors can recruit alone. The FDA cleared 16 precision-oncology medicines in 2024, and more than 1,200 targeted agents were in the global pipeline by early 2025, sustaining demand for CROs with translational research, companion diagnostic, and decentralized-site capabilities. Sponsors increasingly choose vendors that verify biomarkers during pre-clinical work, execute adaptive dose-finding designs, and maintain relationships with diagnostics developers. North America and Europe dominate current activity thanks to mature regulatory pathways, but Asia-Pacific labs are scaling fast to support regional trials. Given every new target spawns numerous combination and resistance-mechanism studies, the long-term pull on the oncology contract research organization (CRO) market remains strong.

Rising Use of Complex Adaptive Trial Designs

Basket, umbrella, and seamless Phase I/II protocols let sponsors refine dose and cohort composition in real time, cutting both sample size and development cycles. The FDA released draft guidance on master protocols in 2024, while the EMA followed with recommendations in 2025, giving sponsors clearer rules for adaptive oncology designs [1]U.S. Food and Drug Administration, “Decentralized Clinical Trials Guidance,” fda.gov. Adaptive execution demands sophisticated biostatistics, continuous data review, and flexible budgets, pushing work to CROs that already own these capabilities. IQVIA applied its Decentralized Trials platform to 12 adaptive oncology studies during 2025, demonstrating commercial traction. Most uptake centers on the United States, Europe, and Japan, where regulatory acceptance and early-stage pipelines align.

Scale-Out of Decentralized / Hybrid Oncology Trials

Hybrid protocols combine home nursing, telemedicine, and local laboratory sampling to reduce patient travel burden. A 2024 Lung-cancer survey showed 68% of respondents favored at least half of visits conducted remotely, prompting 40% of new oncology studies in 2025 to include decentralized elements [2]LUNGevity Foundation, “Patient Perspectives on Decentralized Trials,” lungevity.org Restraints. CROs such as Parexel and Medpace secured incremental awards after investing in proprietary eConsent, ePRO, and direct-to-patient drug-shipping tools, which help retention in multiyear trials. FDA and EMA guidance clarified remote-assessment integrity and cross-border telemedicine standards, accelerating adoption in North America and Western Europe first, with Asia-Pacific markets following as broadband and reimbursement infrastructures mature.

AI-Enabled Patient-Matching & Site-Selection Efficiencies

Platforms that mine electronic health records and genomic databases improve enrollment velocity. ICON’s TrialMatchAI cut median time-to-first-patient-in from 180 days to 120 days across eight oncology programs initiated in 2024–2025. Consortia such as SYNERGY-AI linked 2.5 million de-identified cancer records in 2025, enabling real-time scouting for rare cohorts. Faster recruitment lowers per-patient cost and positions AI-rich vendors to win fixed-price contracts. Adoption remains highest in regions with mature EHR penetration and stringent privacy rules that reinforce the need for ISO 27001-certified information security.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity of oncology-savvy investigators in mature regions | -0.8% | North America, Western Europe | Medium term (2-4 years) |

| Sponsor concerns over cross-border data security | -0.6% | Global, acute in Europe and Asia-Pacific | Short term (≤ 2 years) |

| Escalating vivarium-compliance and animal-welfare costs | -0.5% | North America, Europe | Long term (≥ 4 years) |

| Heightened FDORA inspection frequency for oncology trials | -0.4% | United States, spillover to global trials | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Scarcity of Oncology-Savvy Investigators in Mature Regions

High trial density in the United States and Western Europe has overtaken investigator supply. An ACRP survey reported 62% of U.S. oncology sites faced capacity constraints in 2024, lengthening contract-signature cycles to 68 days, up from 45 days in 2022 [3]Association of Clinical Research Professionals, “Investigator Capacity Survey,” acrpnet.org. Sub-specialty fields like pediatric solid tumors feel the pinch most. Sponsors and CROs are widening site networks into Eastern Europe and Latin America to ease pressure, but those regions often lack the lab infrastructure necessary for complex biomarker assays. Without new investigator training pipelines, bottlenecks could moderate enrollment speed and temper growth in the oncology contract research organization (CRO) market.

Sponsor Concerns Over Cross-Border Data Security

GDPR in Europe and China’s PIPL place strict conditions on moving patient data abroad. A 2024 ransomware breach at a mid-tier CRO exposed 120,000 oncology records and triggered litigation, pushing many sponsors to demand ISO 27001 certification and local data centers for every jurisdiction. Compliance lifts fixed costs and removes smaller vendors from bid lists if they lack cyber-resilience. The short-run effect is sharpest in Europe and East Asia, yet global studies must still satisfy the toughest rule set, keeping information-security investment front and center.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Clinical Phase: Early-Phase Precision Trials Gain Momentum

Phase III programs captured 39.5% of 2025 revenue, reflecting many late-stage immunotherapy and antibody-drug conjugate studies that still rely on large, randomized survival endpoints. However, the oncology contract research organization (CRO) market size associated with Phase I work is set to rise fastest at a 7.89% CAGR to 2031 as precision assets demand molecularly defined dose-escalation cohorts. Seamless Phase I/II designs, endorsed by FDA and EMA guidance, let sponsors jump directly from safety to efficacy arms once a threshold is met. This evolution favors CROs with early-phase units skilled in adaptive enrollment and rapid biomarker turnaround.

Growth in pre-clinical outsourcing also supports early-phase momentum. Sponsors leverage integrated discovery-to-IND packages that combine target validation, translational research, and GLP toxicology, cutting months off IND submission timelines. The near-shoring wave tightened U.S. vivarium supply yet spurred capital projects by Charles River and Labcorp that will unlock fresh capacity in 2026. Together, these developments anchor long-run expansion of the oncology contract research organization (CRO) market in first-in-human studies.

By Service Type: Integrated Platforms Capture Share

Clinical services delivered 30% of revenue in 2025, driven by site management, data monitoring, and patient recruitment across global networks. Still, pre-clinical and discovery activities are pacing ahead, each forecast at 7.5% CAGR through 2031, as drug makers value single-vendor support that validates targets, produces animal efficacy data, and handles IND-enabling safety assays. WuXi AppTec’s platform shepherded 45 oncology programs from discovery to Phase I in 2025, illustrating the pull toward integrated offerings. Central laboratory and biomarker work captured notable share of 2025 revenue and continues to expand as regulators insist on prospective biomarker-development plans for targeted drugs. Large sample-processing players processed tens of millions of oncology specimens last year and have built genomic sequencing and flow-cytometry suites to keep ahead of demand. Real-world evidence services also grow, powered by claims and EHR aggregation tools that feed payer submission packages. These complementary capabilities help full-service vendors cross-sell, boosting their oncology contract research organization (CRO) market share.

By Indication: Rare Cancers Outpace Solid Tumors

Solid tumors remained the largest slice at 45% of 2025 revenue, anchored by high-incidence lung, breast, colorectal, and prostate cancers that attract multi-arm late-stage studies. Yet rare and pediatric cancers are projected to clock a 7.5% CAGR, outstripping the broader oncology contract research organization (CRO) market as orphan incentives and accelerated pathways shrink trial sizes and time to approval. Orphan designations climbed in 2024, and Project Orbis permitted concurrent reviews among multiple agencies, adding to momentum. Hematologic malignancies held significant share of revenue in 2025, buoyed by a robust CAR-T and bispecific antibody pipeline of more than 200 clinical candidates. CROs with cryogenic logistic support and cell-processing expertise command premium pricing in this niche. Meanwhile, sponsors exploring ultrarare oncogenic fusions partner with global academic networks and patient foundations, which depend on CROs to navigate complex biomarker screening and compassionate-use protocols. These dynamics collectively broaden indication diversification within the oncology contract research organization (CRO) market.

By End User: Pharma Dominance Persists

Pharmaceutical and biopharmaceutical companies contributed 40.8% of end-user spend in 2025 and should rise at 7.4% CAGR to 2031 as they trim internal development units and pivot to variable-cost outsourcing models. Large drug makers initiated more than 300 oncology trials in 2024, outsourcing roughly 70% of operational tasks, while small biotechs externalize even more due to limited headcount. Academic and research institutes held significant share of 2025 revenue through investigator-initiated and cooperative-group studies backed by the U.S. National Cancer Institute and similar bodies worldwide.

Foundations and government agencies fund trials in neglected indications, and their grants increasingly stipulate CRO participation to ensure on-time execution. Cross-sector collaborations emerge as pharma firms co-sponsor academic studies to access novel biomarkers, blending public and private capital in ways that sustain the oncology contract research organization (CRO) market.

Geography Analysis

North America commanded 47.78% of 2025 revenue, supported by dense investigator networks, proximity to the FDA, and reimbursement models that encourage domestic pivotal trials. The United States recorded more than 1,800 oncology trial starts in 2024, equal to around 40% of global activity. Canada and Mexico add incremental volume, offering ICH-aligned regulations and cost-efficient sites that keep studies within the region. Near-shoring of toxicology work under the BIOSECURE Act pushed even more early-phase dollars into U.S. and European hubs, straining capacity in mid-2025 but promising long-term upside for local vendors.

Asia-Pacific is the fastest-growing geography, projected at an 8% CAGR through 2031. China’s NMPA approved 23 oncology agents in 2024 and continues to permit conditional marketing while post-approval studies run in parallel, accelerating timelines. India halved median clinical-trial review time to nine months in 2024, and its vast treatment-naïve patient pool makes it highly attractive for enrollment-intensive Phase III work. Japan and South Korea bring high-quality data sets and synchronized submissions with the FDA and EMA, while Australia’s fast-track early-phase schemes and R&D tax rebates pull first-in-human work southward.

Europe held significant share of revenue in 2025, anchored by Germany, the United Kingdom, and France. The EU Clinical Trials Regulation, fully operational in 2025, simplified multi-country approvals, and the EMA PRIME scheme granted priority status to 14 oncology projects last year. Emerging regions round out the map: the Gulf Cooperation Council invests in oncology research hubs, South Africa provides diverse genetic pools, and Brazil and Argentina supply cost-efficient sites paired with experienced investigators. Although smaller today, these regions offer future enrollment relief as mature markets saturate.

Competitive Landscape

The oncology contract research organization (CRO) industry shows moderate concentration: IQVIA, Labcorp Drug Development, Parexel, ICON, and Charles River Laboratories together captured a significant share of oncology-specific revenue in 2025. These multinationals leverage global reach, multiphase service breadth, and heavy digital investment to win large strategic outsourcing partnerships. Mid-tier specialists such as Medpace, Syneos Health, and Novotech build share by fielding therapeutic-focused teams, promising faster start-up, and offering flexible project pricing. Niche players like Precision for Medicine, BioAgilytix, and Jubilant Biosys supply depth in biomarkers, immunogenicity assays, or medicinal chemistry, filling capability gaps for large sponsors.

Convergence with CDMO services defines a new battleground. Pfizer CentreOne, Samsung Biologics, and Lonza have aligned manufacturing muscle with clinical operations to give clients a single path from toxicology to commercial supply, compressing timelines and forcing pure-play CROs to consider similar alliances. Technology is another differentiator. IQVIA integrates AI for site selection, risk-based monitoring, and predictive enrollment, while ICON’s TrialMatchAI automates eligibility checks. Parexel’s purchase of Triomics adds machine-learning dose-optimization to its toolbox. Smaller firms lacking scale partner with third-party software vendors to stay competitive, but that dependency may erode margins.

Regulatory compliance underpins the competitive field. Sponsors increasingly require ISO 9001 quality management, ISO 27001 data security, and proven inspection readiness. Vendors with robust systems gain preferred-provider status, while those that fail inspections risk exclusion from future bids. The combined market dynamics sustain healthy rivalry, yet no single player dominates enough to stifle innovation, keeping barriers to entry moderate and technological differentiation in constant flux within the oncology contract research organization (CRO) market.

Oncology Contract Research Organization (CRO) Industry Leaders

IQVIA

Labcorp Drug Development

Parexel

ICON

Charles River Laboratories

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: IQVIA announced a USD 200 million expansion of its Asia-Pacific oncology network, adding 150 investigator sites and a Singapore regional hub to support multinational trials

- January 2026: Worldwide Clinical Trials agreed to acquire Catalyst Clinical Research, broadening its oncology footprint and integrated service model.

- January 2026: Avance Clinical purchased LumaBridge to strengthen global oncology capabilities.

Global Oncology Contract Research Organization (CRO) Market Report Scope

As per the scope of the report, oncology contract research organization (CRO) is a specialized service provider that partners with pharmaceutical and biotechnology companies to manage the complex development of cancer therapies. These organizations provide end-to-end support across the drug development lifecycle, from preclinical research and early-phase dose-finding studies to large-scale Phase III trials and post-market safety monitoring.

The oncology contract research organization (CRO) market is segmented by clinical phase, service type, end-users, indication, and geography. By clinical phase, it is segmented into Pre-clinical, Phase I, Phase II, Phase III, and Phase IV. By service type, the market is segmented into discovery & translational research services, pre-clinical services, clinical services, central laboratory & biomarker services, real-world evidence & late-phase, and others. By indication, the market is divided into solid tumors, hematologic malignancies, rare & pediatric cancers. By end-users, the segmentation includes pharmaceuticals and biopharmaceutical companies, academic & research institutes, and others. Geographically, the market is segmented across North America, Europe, the Asia-Pacific region, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Pre-clinical |

| Phase I |

| Phase II |

| Phase III |

| Phase IV |

| Discovery & Translational Research Services |

| Pre-clinical Services |

| Clinical Services |

| Central Laboratory & Biomarker Services |

| Real-World Evidence & Late-Phase |

| Others |

| Solid Tumors |

| Hematologic Malignancies |

| Rare & Pediatric Cancers |

| Pharmaceuticals and Biopharmaceutical companies |

| Academic & Research Institutes |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Clinical Phase | Pre-clinical | |

| Phase I | ||

| Phase II | ||

| Phase III | ||

| Phase IV | ||

| By Service Type | Discovery & Translational Research Services | |

| Pre-clinical Services | ||

| Clinical Services | ||

| Central Laboratory & Biomarker Services | ||

| Real-World Evidence & Late-Phase | ||

| Others | ||

| By Indication | Solid Tumors | |

| Hematologic Malignancies | ||

| Rare & Pediatric Cancers | ||

| By End Users | Pharmaceuticals and Biopharmaceutical companies | |

| Academic & Research Institutes | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the oncology contract research organization (CRO) market in 2031?

The market is forecast to reach USD 35.13 billion by 2031, expanding at a 7.36% CAGR.

Which clinical phase is expected to grow fastest through 2031?

Phase I studies should post the highest growth, advancing at a 7.89% CAGR as precision-oncology assets enter first-in-human testing.

Why is Asia-Pacific growing faster than other regions?

China and India offer expanding investigator networks, lower per-patient costs, and streamlined regulatory pathways, supporting an 8% CAGR for the region

How are integrated CRO-CDMO platforms changing sponsor outsourcing?

By combining discovery, clinical development, and manufacturing under one roof, integrated platforms cut handoff risk and compress timelines, particularly valuable for small biotechs.

Page last updated on: