Oman Corrugated Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

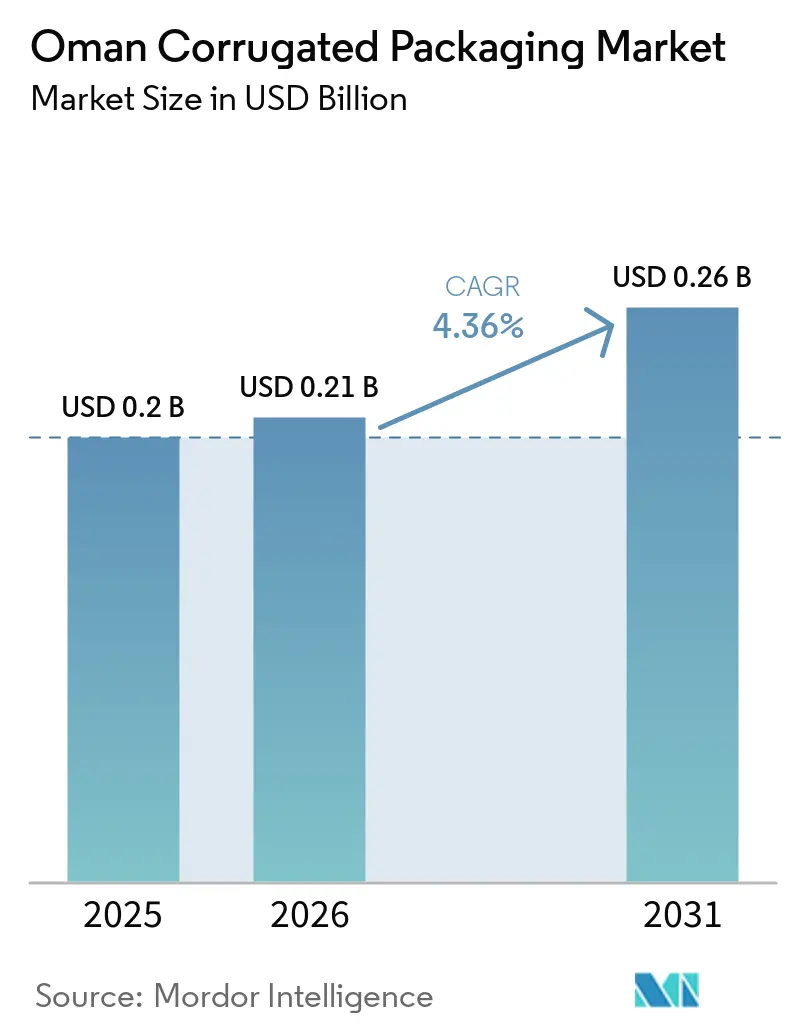

| Base Year Market Size (2025) | USD 0.2 Billion |

| Market Size (2026) | USD 0.21 Billion |

| Market Size (2031) | USD 0.26 Billion |

| Growth Rate (2026 - 2031) | 4.36% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Oman Corrugated Packaging Market Analysis by Mordor Intelligence

The Oman corrugated packaging market size is projected to expand from USD 0.2 billion in 2025 and USD 0.21 billion in 2026 to USD 0.26 billion by 2031, registering a 4.36% CAGR between 2026 and 2031. Muscat’s import-substitution incentives under Oman Vision 2040, the country’s emergence as a perishables air-freight hub, and rising e-commerce parcel volumes together anchor near-term demand. Converters are accelerating the switch from virgin kraft linerboard to recycled grades to hedge against Red Sea freight volatility, while investment in semi-chemical fluting and digital inkjet printing underscores the pivot toward lighter, high-graphics, shelf-ready formats. Regional giants are tightening a historically fragmented supplier base by deploying scale advantages in Sohar, Duqm, and Salalah free zones. At the same time, high electricity tariffs and limited domestic paper-recycling capacity temper expansion plans, forcing producers to balance capital spending with margin protection.

Key Report Takeaways

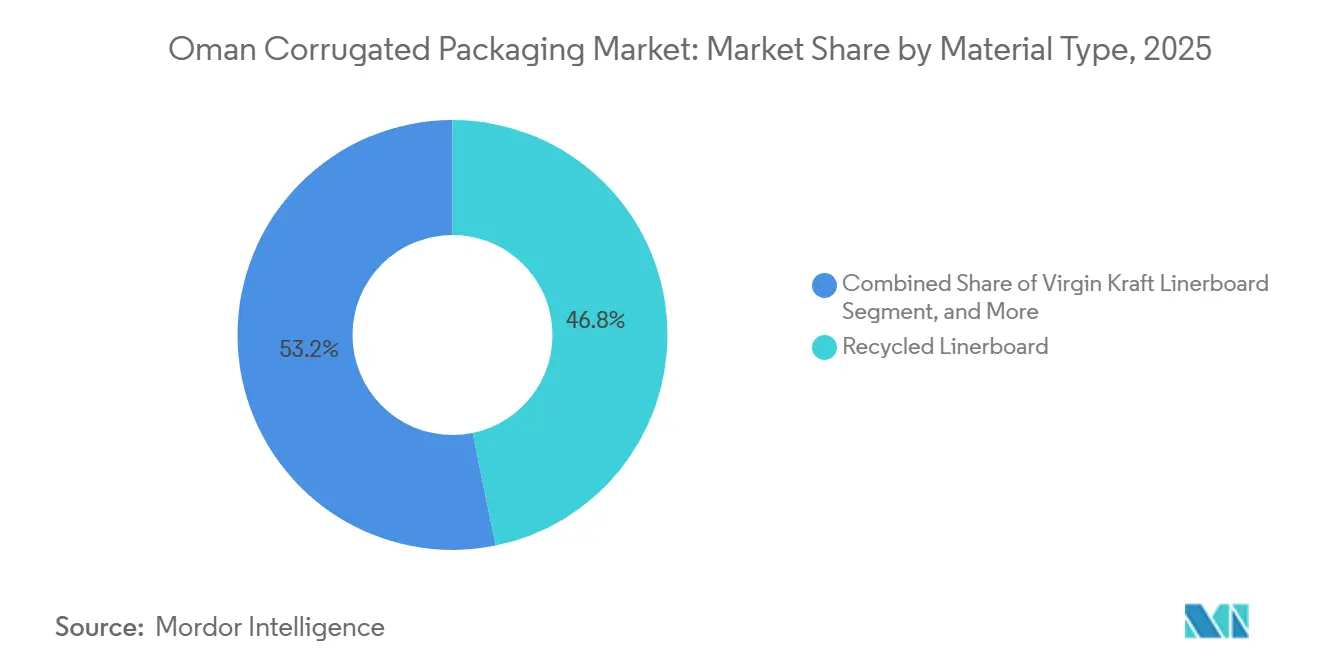

- By material type, the recycled linerboard segment captured 46.78% of the Oman corrugated packaging market share in 2025.

- By flute type, the Oman corrugated packaging market size for f flute is projected to grow at an 5.67% CAGR through 2031.

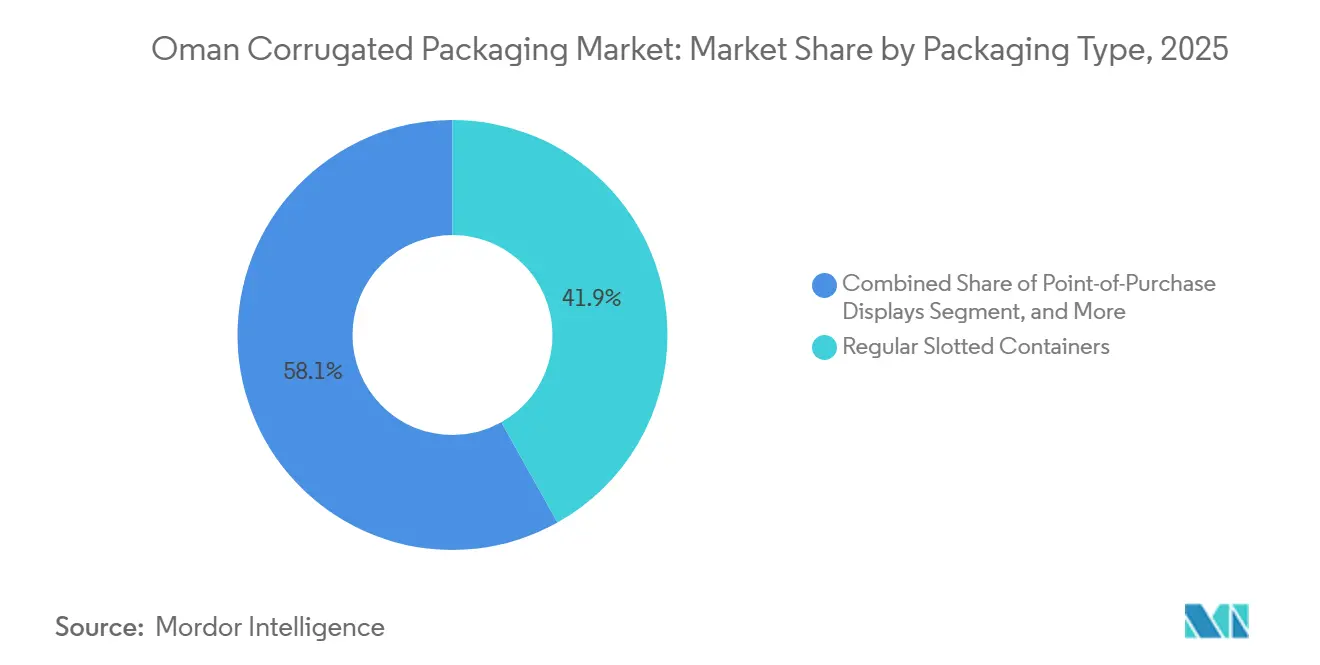

- By packaging type, the regular slotted containers segment captured 41.88% of the Oman corrugated packaging market share in 2025.

- By wall type, the Oman corrugated packaging market size for triple-wall is projected to grow at an 5.12% CAGR through 2031.

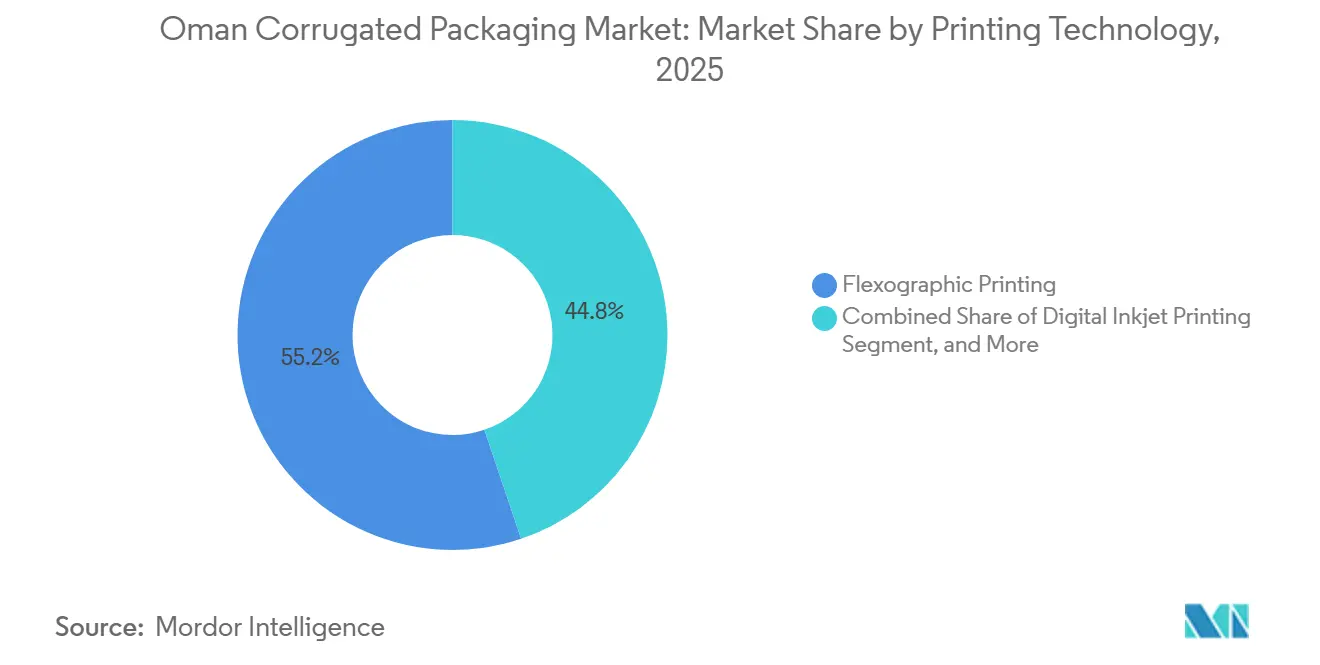

- By printing technology, the flexographic printing segment captured 55.17% of the Oman corrugated packaging market share in 2025.

- By end-user industry, the Oman corrugated packaging market size for e-commerce fulfillment centers is projected to grow at an 4.95% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Oman Corrugated Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising E-commerce Parcel Volumes | +1.2% | National – Muscat, Salalah, Sohar logistics hubs | Short term (≤ 2 years) |

| Government Push for Domestic Manufacturing Under Oman Vision 2040 | +0.9% | National – Sohar, Duqm, Salalah free zones | Medium term (2-4 years) |

| Mandatory Recycled-Content Targets for Packaging | +0.6% | National, aligned with GCC circular frameworks | Medium term (2-4 years) |

| Shift Toward Lightweight, High-Performance Fluting Combinations | +0.5% | National, spill-over to UAE and Saudi corridors | Long term (≥ 4 years) |

| Food Export Growth to GCC Neighbors | +0.4% | Regional – Saudi Arabia, UAE, Kuwait | Medium term (2-4 years) |

| Growth of Fresh Produce Air-Freight Corrugates via Oman Air Cargo | +0.3% | National with links to Europe and South Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising E-Commerce Parcel Volumes

Online retail sales are set to climb from USD 660 million in 2024 to USD 1.24 billion by 2029, an annual pace that far exceeds overall box demand. Dedicated e-commerce parks in Muscat and Salalah shorten delivery lead times, encouraging fulfillment operators to specify smaller, die-cut boxes and on-demand graphics. Digital inkjet presses capable of variable data and QR-code printing eliminate flexographic tooling costs for short runs of 5,000 units or fewer, matching the SKU proliferation seen in last-mile channels. Parcel-box designs now incorporate multi-temperature adhesives and high-performance fluting to survive desert heat, as only 40% of postal codes support doorstep service. As these logistics gaps narrow, the Oman corrugated packaging market should realize outsized gains from direct-to-consumer shipping demand.

Government Push for Domestic Manufacturing Under Oman Vision 2040

Oman Vision 2040 earmarks OMR 935 million (USD 2.43 billion) for polymer and packaging ventures, including a PTA and PET complex that lowers reliance on imported virgin kraft.[1]Oman Vision 2040, Oman Vision 2040 Secretariat, omanvision2040.com Free zones grant 30-year tax holidays and full foreign ownership, leading multinationals to commission new corrugating lines in Sohar and Duqm, where land is 60% cheaper than in Muscat. The Local Content Policy, which favors Omani-made packaging in public tenders, guarantees baseline volumes for domestic converters, especially in processed foods, where date and fisheries expansions keep corrugated uptake steady. Financing support through the Sharakah program further reduces borrowing costs, adding momentum to plant upgrades. Together, these levers underpin medium-term growth in the Oman corrugated packaging market.

Mandatory Recycled-Content Targets for Packaging

The National Waste Management Policy aims to divert 9 million tonnes of GCC packaging waste and unlock a USD 138 billion circular-economy prize by 2030. Although Oman has not set minimum recycled percentages, the UAE's extended producer responsibility rules and Saudi draft legislation already influence cross-border supply chains. Recycled linerboard’s 46.78% share in 2025 shows anticipatory compliance, yet feedstock scarcity inflates costs by 15-20% versus virgin alternatives. Keryas Paper Industry’s 180,000 tonnes-per-year mill in Sohar covers only a fraction of the need, and imported OCC prices remain volatile. Progress on waste-segregation pilots and Be’ah’s material-recovery upgrades will decide whether the Oman corrugated packaging market can meet future GCC content thresholds without eroding margins.

Shift Toward Lightweight, High-Performance Fluting Combinations

Semi-chemical fluting is growing faster than any other substrate because it delivers a superior strength-to-weight ratio ideal for cold-chain exports. Grades such as Mondi’s ProVantage Powerflute achieve 15% board weight savings while retaining 90% of edge crush requirements, which are essential for Oman’s perishables air-freight corridor. F flute adoption also accelerates because it accommodates 20-30% more sheets per pallet and provides a print surface comparable to that of folding cartons for cosmetics and pharmaceuticals. Exporters flying produce on Oman Air’s Amsterdam route face strict weight limits, making lightweight board a direct revenue lever. As converters install narrow-flute tooling, double-digit adoption rates should lock in long-term efficiency gains for the Oman corrugated packaging market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Kraft Linerboard Import Prices Linked to Red Sea Shipping Disruptions | -0.8% | National – Muscat and Sohar port-dependent sites | Short term (≤ 2 years) |

| Limited Domestic Paper Recycling Infrastructure | -0.5% | National, most severe in interior regions | Medium term (2-4 years) |

| High Electricity Tariffs for Corrugators | -0.3% | National – Muscat and Salalah zones | Long term (≥ 4 years) |

| Competition From Rigid Plastics in Industrial Bins | -0.2% | National – automotive and electronics users | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Kraft Linerboard Import Prices Linked to Red Sea Shipping Disruptions

Houthi-linked attacks forced 30% of global box ships to reroute via the Cape of Good Hope, pushing freight to USD 3,101 per 40-foot container, triple the pre-crisis level. War-risk premiums jumped from 0.07% to over 1% of hull value, adding USD 50-70 per tonne to linerboard landed in Muscat. Smaller converters lacking hedging must either pass through 10-15% cost increases or accept margin erosion, while larger GCC peers lock in allocation from integrated mills. Temporary sourcing from Turkey and Egypt offers only partial relief and at a 20-25% price premium. Until domestic recycling reaches scale, the Oman corrugated packaging market remains exposed to volatility in shipping routes.

Limited Domestic Paper Recycling Infrastructure

Outside Keryas’s Sohar complex, Oman has no large-scale de-inking or pulping capacity and recovers less than 10% of post-consumer corrugated waste. Importing pre-sorted OCC from Europe at USD 150-180 per tonne eliminates much of the cost advantage usually enjoyed by recycled linerboard. Private investments totaling USD 40 million for UAE capacity come online only in 2027, leaving a multi-year supply gap. Without EPR legislation, brand owners lack financial incentives to co-fund collection programs, forcing municipalities to shoulder costs. In the medium term, constrained feedstock availability caps the upside of recycled grades within the Oman corrugated packaging market

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Recycled Grades Hold Sway, Semi-Chemical Fluting Rises

Recycled linerboard secured 46.78% of 2025 demand, making it the single largest slice of the Oman corrugated packaging market share because converters anticipate tougher GCC circular-economy rules that reward secondary fiber use. Virgin Kraft remains indispensable for export-grade pharmaceutical and triple-wall boxes, yet its growth is limited because freight-driven import costs continuously widen the price gap with recycled alternatives. Semi-chemical fluting is advancing at a 5.42% CAGR through 2031, as shippers of mangoes, seafood, and premium vegetables require a lighter board that still passes edge-crush tests for air-freight legs on the Muscat-Amsterdam corridor. This cost-to-performance balance positions semi-chemical grades as a pragmatic hedge against both freight volatility and domestic recycling bottlenecks. As a result, material mix decisions now pivot more on logistics economics than on traditional strength hierarchies.

Domestic supply from Keryas Paper Industry’s 180,000-tonne Sohar mill satisfies only 15-20% of recycled linerboard demand, yet still trims delivered cost by about 12% versus Asian imports during normal freight conditions.[2]Keryas Paper Industry to Invest 40 M USD in UAE Expansion, Gulf News, gulfnews.com That advantage evaporates when Red Sea disruptions push container prices past USD 3,000, leaving converters exposed until the company’s USD 40 million UAE expansion adds 200,000 tonnes in 2027. Coated liners with moisture barriers are gaining ground within the Oman corrugated packaging market size because cold-chain exporters need condensation control for flights that cross multiple climate zones. Brand owners now weigh coating fees against the risk of product spoilage, a calculation that often favors premium substrates.

By Flute Type: B-Flute Dominates, F-Flute Accelerates

B flute held 41.57% of 2025 shipments, reflecting its time-tested versatility across regular slotted containers and die-cut custom boxes delivered to Muscat hypermarkets. C flute retains modest traction in palletized heavy goods, yet weight-reduction mandates from food processors are steadily diverting orders toward narrower profiles that lower freight bills. F flute is expanding at a 5.67% CAGR through 2031 because its 1.1-millimeter profile allows 20-30% more blanks per pallet and delivers a near-carton printing surface demanded by cosmetics brands. Converters installing newer corrugators in Sohar increasingly choose F flute modules to leverage these dual logistics and graphics benefits. This preference will likely reshape the long-term flute mix in Oman's corrugated packaging market.

Retail-ready displays stocked by Carrefour and Lulu require crisp graphics and minimal shelf refilling, conditions perfectly matched to F flute’s smooth surface and stacking efficiency. E flute adoption follows similar logic, but the narrower profile occasionally struggles with drop-test requirements for heavier SKU combinations. D flute remains niche because most domestic machinery lacks compatible gearsets, though several free-zone investors have signaled willingness to fund retrofits if FMCG owners formalize folding-carton replacement targets. Meanwhile, B-flute persists as the default for fast-moving commodity packs, anchoring baseline tonnage even as premium niches diversify. Overall, flute-type evolution underscores how packaging formats now integrate marketing, logistics, and sustainability objectives into a single material decision.

By Packaging Type: RSCs Lead, Displays Surge

Regular slotted containers accounted for 41.88% of 2025 volume, underscoring their enduring cost advantage and compatibility with high-speed case erectors deployed at Sohar and Salalah factories. These boxes still dominate the Oman corrugated packaging market size within processed foods, beverages, and industrial components. Point-of-purchase displays are growing fastest, with a 5.98% CAGR, as hypermarkets seek shelf-ready units that cut labor by up to 40% during restocking shifts. Consequently, converters are combining F flute board with digital inkjet graphics to deliver vivid, quick-turn fixtures that promote seasonal promotions without requiring secondary cartons. This shift reallocates production capacity toward higher-margin, short-run jobs rather than only high-volume commodity orders.

Die-cut custom boxes meet the dimensional requirements of e-commerce parcels, enabling fulfillment hubs to lower void ratios and save on dunnage. Folding-carton substitution into E-flute and F-flute structures accelerates, as these grades achieve comparable graphics at roughly 30% lower material mass, thereby alleviating Oman Vision 2040 waste-reduction targets. Pallet boxes for bulk fruit exports maintain steady but unspectacular growth, yet still anchor triple-wall demand that downstream policymakers see as an enabler of export revenue. Other niche designs, such as wraparound cases for beverages, rise in relevance when brand owners seek warehouse automation compatibility. Altogether, packaging-type diversification illustrates how buyers are segmenting performance specifications by channel rather than by traditional industry silos.

By Wall Type: Single-Wall Dominates, Triple-Wall Gains in Export Corridors

Single-wall cartons accounted for 47.32% of 2025 shipments, benefiting from their balanced weight, cost, and compression ratings that suit everyday processed foods and parcel traffic. Double-wall designs capture spend in electronics and personal-care loads where drop protection must be guaranteed through desert-heat cycles between Muscat and interior governorates. Triple-wall board is posting a 5.12% CAGR through 2031 because re-export hubs in Salalah and Duqm rely on it for heavy machinery parts destined for African ports. Market watchers foresee triple-wall traction persisting as regional infrastructure projects demand oversized components boxed in moisture-barrier corrugated. This trend underscores the interplay between Oman’s logistics geography and wall-type specification choices.

Single-face rolls used as inner cushioning are losing share to molded pulp and recyclable air pillows because those options align better with corporate carbon-footprint targets. Nevertheless, single-face remains irreplaceable for some glassware shippers who need custom-contour wraps at a modest cost. Converters installing higher-flute corrugators often optimize changeover times so single-wall and double-wall can be produced sequentially, maximizing uptime under Oman’s relatively high electricity tariffs. Going forward, wall-type strategy will increasingly hinge on predictive analytics that align SKU fragility, transit distance, and tariff exposure. Such data-driven planning supports higher asset utilization even when import linerboard prices fluctuate unexpectedly.

By Printing Technology: Flexography Rules, Digital Inkjet Gains Momentum

Flexographic presses produced 55.17% of printed surface in 2025, capitalizing on meters-per-minute speeds that still outpace most inkjet platforms at volumes exceeding 10,000 impressions. Water-based inks remain essential for food-contact compliance across the Oman corrugated packaging market, reinforcing the technology’s entrenched status among snack and dairy brands. Plate costs, however, make short runs uneconomic, prompting converters to reserve flexo for staple SKUs with predictable monthly release cycles. Consequently, e-commerce parcels and point-of-purchase displays increasingly migrate to digital lines that eliminate tooling downtime.

Digital inkjet is advancing at a 5.61% CAGR because Oman’s online retail revenue is forecast to nearly double by 2029, necessitating configurable graphics, QR codes, and serialized barcodes for last-mile tracking HP. Litho-laminated topsheets still command a presence in premium chocolate and fragrance cartons, yet their share stalls as high-pass inkjet heads now approach 400 meters-per-minute throughput. Screen printing is well-suited to specialty displays that use metallic or fluorescent coatings, but its setup time limits it to very small campaigns. As converters spread capex between anilox rolls and inkjet bars, print-technology choice is becoming a channel-specific decision rather than a one-size-fits-all platform.

By End-User Industry: Processed Foods Lead, Fulfillment Centers Accelerate

Processed foods accounted for 34.19% of the 2025 uptake, a commanding Oman corrugated packaging market share stemming from government subsidies supporting date-palm value addition and expanded fishery cold stores. These state programs guarantee a stable carton baseline that partially offsets linerboard cost swings by locking in annual contracts under the Local Content Policy. Fresh produce exports occupy the second-largest slice, buoyed by Oman Air Cargo’s dedicated Amsterdam route moving high-margin perishables four times per week. Electrical and electronics assemblers in the Sohar free zone purchase double-wall or triple-wall boxes lined with anti-static treatment to protect circuit boards through 1,000-kilometer haulage runs. Beverage brands maintain moderate growth but lose value share because craft producers shift toward lighter multi-pack sleeves that use less board.

E-commerce fulfillment centers display the strongest forward trajectory, with a 4.95% CAGR, driven by online revenue targets of USD 1.24 billion by 2029, a figure that outpaces brick-and-mortar sales growth. Cosmetics and personal-care goods, though smaller in tonnage, command premium margins due to litho-quality or inkjet photo graphics on F-flute substrates. Pharmaceutical shippers remain wedded to virgin kraft and moisture-barrier coatings, ensuring stable though regulated demand that few local converters are certified to serve. Automotive aftermarket parts and construction hardware create lumpy yet lucrative orders during GCC infrastructure cycles, often specifying triple-wall cartons for sea freight into East Africa. This diversified mix means demand shocks in any single end-use are diluted across multiple, counter-cyclical verticals.

Geography Analysis

Muscat drives between 40 and 45% of total demand because it concentrates major food processors, FMCG warehouses, and the nation’s largest e-commerce fulfillment parks that together underpin high run-rates for single-wall boxes. The capital’s proximity to the Port of Sohar speeds linerboard arrivals by two days, yet port congestion during peak import months can still delay shipments, forcing converters to carry higher strategic inventory. Electricity tariffs in Muscat industrial zones average 12–18 baisa per kilowatt-hour, a premium against Saudi benchmarks that encourages manufacturers to maximize machine uptime. Local authorities now offer rental rebates inside the Rusayl and Khazaen economic zones to reinforce Muscat’s packaging cluster competitiveness. These incentives partially cushion converters from freight volatility but do not fully neutralize raw-material exposure.

Sohar Industrial Port absorbs roughly one quarter of national corrugated consumption, propelled by Keryas Paper Industry’s recycled mill and the Ladayn Polymer Program’s nine downstream plastics factories that need secondary cartons. Free-zone tenants enjoy 30-year tax holidays and customs exemptions that slash landed costs on German corrugator lines by almost 10%, drawing investors who once favored Sharjah or Jebel Ali. Sohar’s integrated rail-road-sea network provides a strategic launchpad for shipments into the UAE and Saudi Arabia, cutting lead times by a full day compared with Muscat road routes. However, the port is also vulnerable to Red Sea detours that amplify freight rates, compelling local players to hedge capacity with spot supply from Turkey or Egypt during crisis months. Expansion land remains plentiful, positioning Sohar as the logical hub for future high-graphics, value-added board plants.

Salalah Free Zone and Duqm Special Economic Zone together account for around 15 to 20% of current volume, yet their forward growth prospects appear brightest because both sites straddle emerging Africa-GCC trade lanes. Salalah’s bonded corridor status lowers transit paperwork for triple-wall boxes moving to Kenya and Tanzania, a feature that has already lured Arabian Packaging to establish a distribution depot for East African orders. Duqm’s greenfield plots cost roughly 60% less than Muscat real estate and carry comparable tax benefits, giving mid-size Saudi converters an economical springboard into new GCC customers. These coastal zones nonetheless contend with limited recycling infrastructure, meaning inbound linerboard must still move by sea, exposing operators to the same freight price whiplash that hammers Muscat and Sohar. Even so, local authorities plan a material-recovery facility before 2028, signalling policy resolve to close the collection loop and underpin truly circular corrugated supply chains.

Competitive Landscape

Regional powerhouses INDEVCO Paper Containers, Obeikan Paper Industries, and Arabian Packaging are tightening a once-fragmented market by leveraging integrated containerboard assets and pan-GCC logistics networks that smaller Omani firms cannot match. Omani Packaging Company SAOG, the only publicly listed domestic converter, posted a 90% plunge in profits in FY2025 after freight inflation tripled linerboard costs, an event that spotlighted its lack of upstream paper insulation. INDEVCO’s 2025 licensing of SCA Arcwise curved technology adds structural packaging priced 20–30% above commodity boxes, granting a margin hedge that most rivals lack.[3]INDEVCO Group Corporate News, INDEVCO, indevcogroup.com Obeikan’s new Heidelberg press boosts premium output by 50,000 tonnes per year, putting additional pressure on Muscat-based printers still operating legacy flexo lines.

Strategic expansion now centers on free-zone incentives that minimize tax and customs overhead, which explains why Sohar and Duqm collectively receive the bulk of new corrugator orders. Keryas Paper Industry’s USD 40 million recycled-mill project in the UAE aims to undercut Indonesian and Thai linerboard by 10–15%, offering GCC converters a locally sourced hedge against Red Sea disruptions. Packaging Corporation of America’s USD 1.8 billion acquisition of Greif assets signals that North American capacity may pivot toward export volumes into growth markets like Oman as domestic demand plateaus. Georgia-Pacific’s Mt. Olive closure freed 250,000 tonnes, some of which traders already offer into MENA spot markets, raising the competitive bar for integrated Gulf players. Such international maneuvers illustrate how global capital flows now shape supply balance in the Oman corrugated packaging market.

Technology differentiation further separates winners from laggards. Digital inkjet platforms like HP PageWide and EFI Nozomi allow fast graphic changeovers, critical for e-commerce SKUs that refresh packaging designs every promotion cycle. Small Omani converters struggle to finance these lines, making them potential acquisition targets for larger GCC groups seeking footprint consolidation. Meanwhile, joint ventures with logistics operators, such as DP World’s cold-chain hub in Egypt, create bundled service models where packaging supply contracts ride on integrated transport agreements. If these trends continue, bargaining power will continue migrating toward vertically integrated conglomerates that command containerboard, conversion, and freight assets under a single balance sheet.[4]DP World Press Centre, DP World, dpworld.com Consequently, market observers expect further mergers or selective exits as scale economics tighten around high-performance graphics and recycled-content mandates.

Oman Corrugated Packaging Industry Leaders

Omani Packaging Company SAOG

Power Carton L.L.C

Keryas Paper Industry

Pride Packaging LLC

Packaging Co. Ltd. (SAOC)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Ocean of Majan secured Sharakah financing to expand its PP woven-bag facility in Rusayl, adding 12,000 tonnes of annual capacity.

- January 2026: Al Ghurair Foods committed USD 130 million to a corn-milling plant and USD 20 million to a meat-coating line in the UAE, lifting GCC corrugated demand by up to 10,000 tonnes yearly.

- October 2025: DP World invested USD 29 million in an Egyptian cold-chain hub, creating need for triple-wall export boxes to handle 50,000 tonnes of annual throughput.

- March 2025: INDEVCO Paper Containers acquired SCA Arcwise licensing to produce curved corrugated for FMCG shelf-ready displays.

Oman Corrugated Packaging Market Report Scope

The Oman corrugated packaging market is the industrial sector focused on the production and conversion of paper-based packaging materials, consisting of a fluted corrugated medium bonded to flat linerboards. This market encompasses the manufacturing of various structural grades, such as single-wall, double-wall, and triple-wall boards, designed to provide high strength-to-weight ratios for protective transport.

The Oman Corrugated Packaging Market Report is Segmented by Material (Virgin Kraft Linerboard, Recycled Linerboard, Corrugating Medium, Semi-Chemical Fluting, and Other Materials), Flute Type (A Flute, B Flute, C Flute, E Flute, and F Flute), Packaging Type (Regular Slotted Containers, Die-Cut Custom Boxes, Folding Cartons, Point-of-Purchase Displays, Pallet Boxes, and Other Packaging Types), Wall Type (Single-Wall, Double-Wall, Triple-Wall, and Single Face), Printing Technology (Flexographic Printing, Digital Inkjet Printing, Litho-Lamination, Screen Printing, and Other Printing Technologies), End-User Industry (Processed Foods, Fresh Food and Produce, Beverages, Electrical Products, Personal Care and Cosmetics, E-commerce Fulfillment Centers, Pharmaceuticals, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Kraft Linerboard |

| Recycled Linerboard |

| Corrugating Medium |

| Semi-Chemical Fluting |

| Other Materials |

| A Flute |

| B Flute |

| C Flute |

| E Flute |

| F Flute |

| Regular Slotted Containers |

| Die-Cut Custom Boxes |

| Folding Cartons |

| Point-of-Purchase Displays |

| Pallet Boxes |

| Other Packaging Types |

| Single-Wall |

| Double-Wall |

| Triple-Wall |

| Single Face |

| Flexographic Printing |

| Digital Inkjet Printing |

| Litho-Lamination |

| Screen Printing |

| Other Printing Technologies |

| Processed Foods |

| Fresh Food and Produce |

| Beverages |

| Electrical Products |

| Personal Care and Cosmetics |

| E-commerce Fulfillment Centers |

| Pharmaceuticals |

| Other End-User Industries |

| By Material Type | Virgin Kraft Linerboard |

| Recycled Linerboard | |

| Corrugating Medium | |

| Semi-Chemical Fluting | |

| Other Materials | |

| By Flute Type | A Flute |

| B Flute | |

| C Flute | |

| E Flute | |

| F Flute | |

| By Packaging Type | Regular Slotted Containers |

| Die-Cut Custom Boxes | |

| Folding Cartons | |

| Point-of-Purchase Displays | |

| Pallet Boxes | |

| Other Packaging Types | |

| By Wall Type | Single-Wall |

| Double-Wall | |

| Triple-Wall | |

| Single Face | |

| By Printing Technology | Flexographic Printing |

| Digital Inkjet Printing | |

| Litho-Lamination | |

| Screen Printing | |

| Other Printing Technologies | |

| By End-User Industry | Processed Foods |

| Fresh Food and Produce | |

| Beverages | |

| Electrical Products | |

| Personal Care and Cosmetics | |

| E-commerce Fulfillment Centers | |

| Pharmaceuticals | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current size and projected growth of Oman’s corrugated packaging sector?

The market stands at USD 0.21 billion in 2026 and is forecast to reach USD 0.26 billion by 2031, reflecting a 4.36% CAGR.

Which material currently dominates box production in Oman?

Recycled linerboard leads with 46.78% share, largely because converters anticipate tighter GCC circular-economy mandates.

Why are shelf-ready point-of-purchase displays expanding so quickly?

Hypermarkets prefer displays that reduce restocking labor, driving a 5.98% CAGR for these formats through 2031.

How have Red Sea disruptions affected linerboard sourcing costs?

Detours around the Cape of Good Hope tripled container rates and added USD 50-70 per tonne to landed kraft prices.

Which printing technology is gaining the most momentum?

Digital inkjet is growing at a 5.61% CAGR because it supports variable graphics and eliminates flexo plate charges for short runs.

Where are the prime locations for new corrugated plants in Oman?

Sohar and Duqm free zones attract most new investment thanks to 30-year tax holidays, customs exemptions, and lower land costs.

Page last updated on: