Oil And Gas Exhaust System Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Market Size (2025) | USD 0.67 Billion |

| Market Size (2030) | USD 0.82 Billion |

| Growth Rate (2025 - 2030) | 4.12% CAGR |

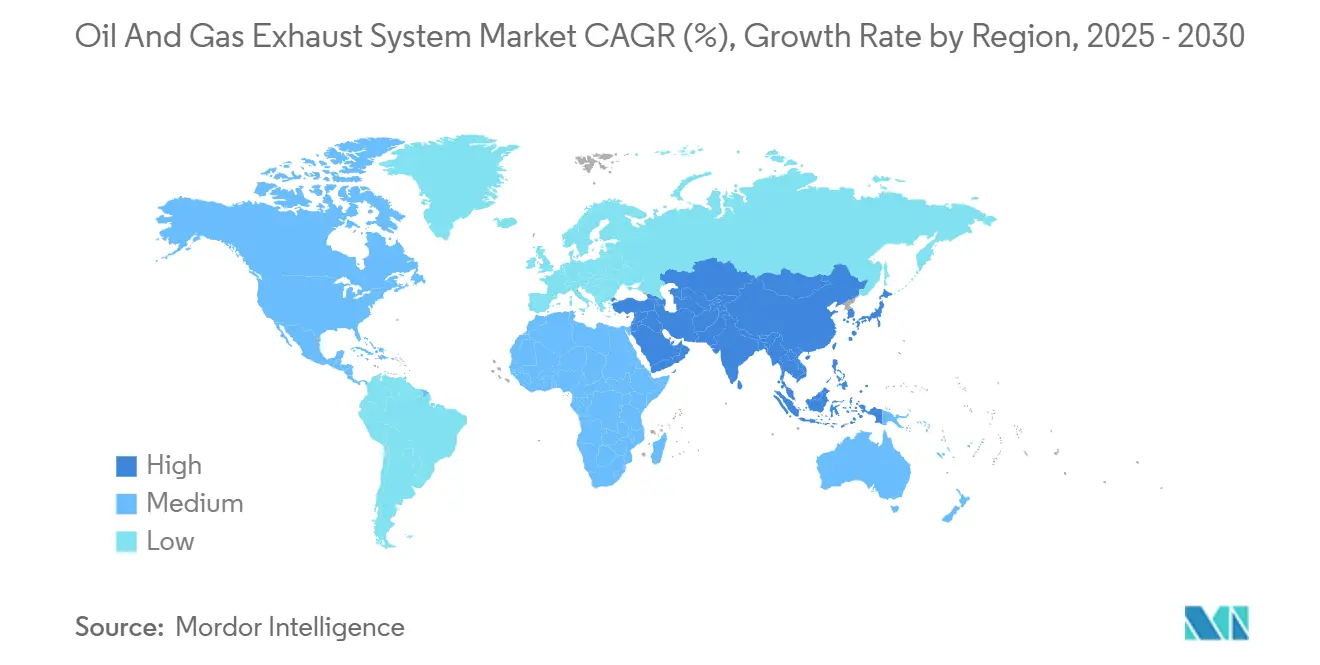

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

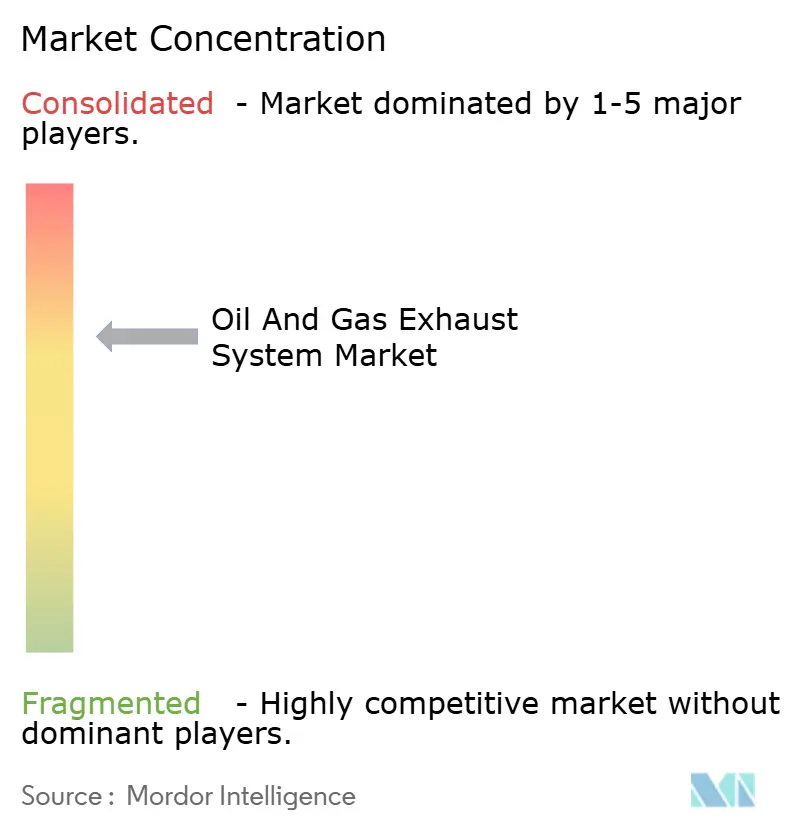

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Oil And Gas Exhaust System Market Analysis by Mordor Intelligence

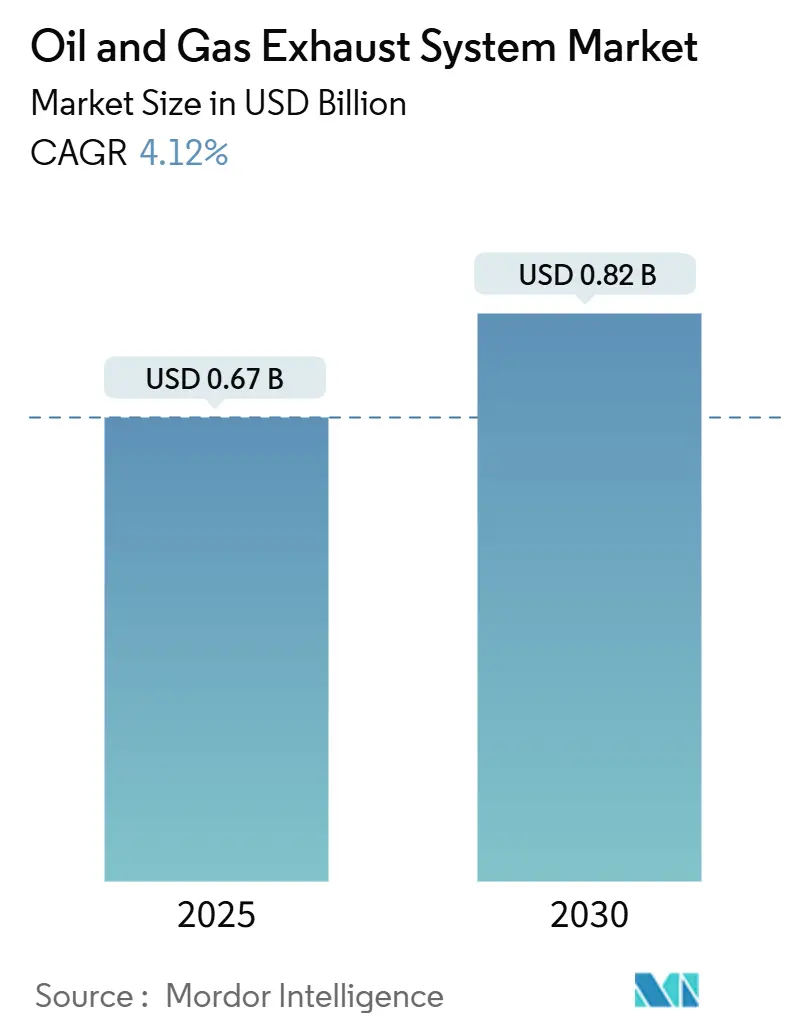

The Oil And Gas Exhaust System Market size is estimated at USD 0.67 billion in 2025, and is expected to reach USD 0.82 billion by 2030, at a CAGR of 4.12% during the forecast period (2025-2030).

Demand is shaped by Tier III nitrogen-oxide limits for new offshore engines, methane-charge rules for U.S. shale producers, and a measured wave of deepwater final investment decisions. Supply-side friction comes from nickel-alloy shortages and a mid-cycle pause in liquefied-natural-gas megaproject approvals, yet retrofits on aging fleets and turnkey skid orders for midstream stations keep baseline growth intact. Selective catalytic reduction (SCR) systems outpace the aggregate trend thanks to regulatory pull, while composite and ceramic substrates gain share where higher exhaust-gas temperatures oblige material upgrades. Regionally, Asia-Pacific delivers scale through Chinese coal-bed-methane compression and Indian city-gas build-outs, whereas the Middle East and Africa register the fastest expansion on the back of Saudi Arabia’s flaring-elimination plan and sour-gas monetization projects. Competitive intensity remains moderate as turbine OEMs leverage installed-base contracts to cross-sell exhaust packages, while catalyst specialists differentiate through low-temperature methane-oxidation formulations.

Key Report Takeaways

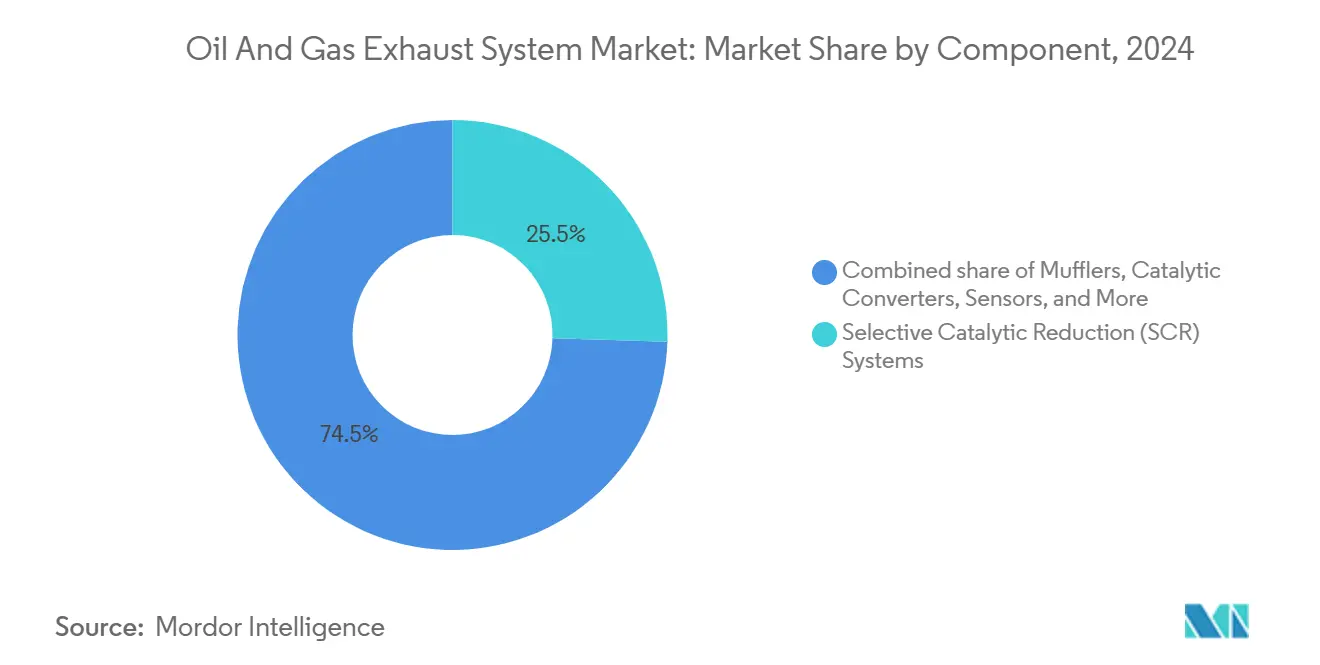

- By component, selective catalytic reduction systems held 25.5% of the oil and gas exhaust systems market share in 2024; mufflers trail, yet SCR is forecast to expand at a 5.1% CAGR to 2030.

- By material, stainless steel commanded 44.9% of the oil and gas exhaust systems market size in 2024, while composite and ceramic materials recorded the fastest 6.5% CAGR through 2030.

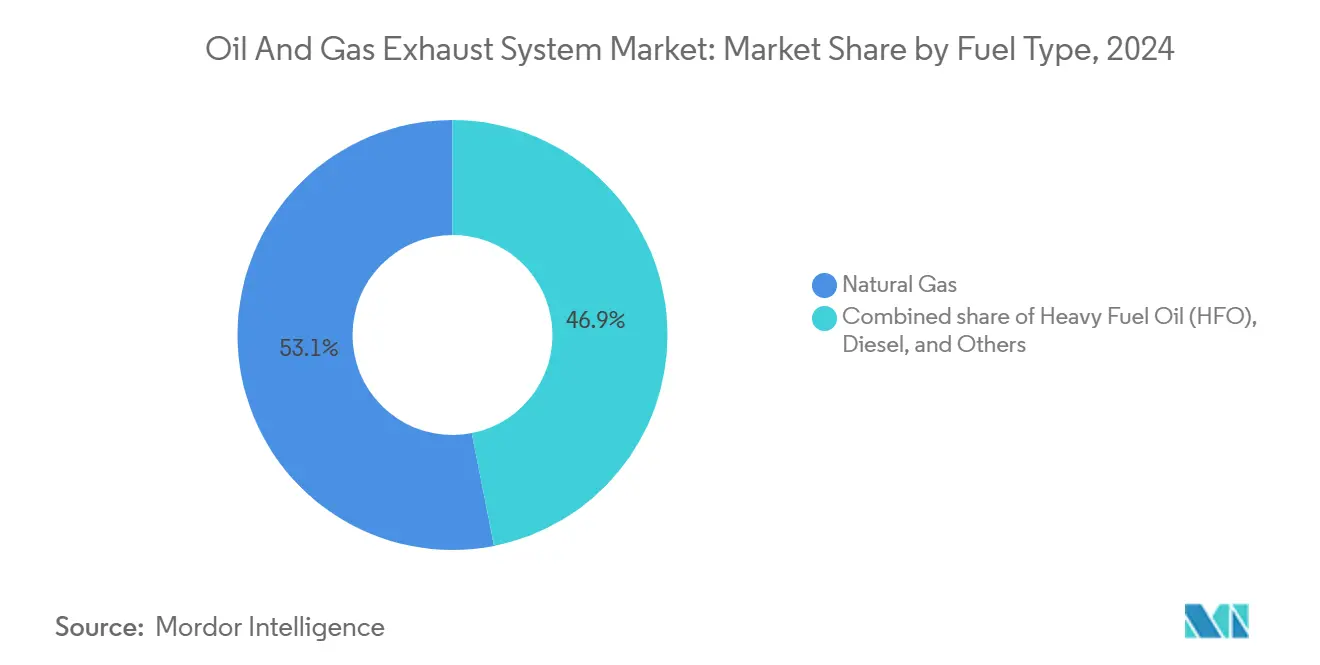

- By fuel type, natural-gas engines accounted for 53.1% of the oil and gas exhaust systems market size in 2024, and “Others” fuels, dual-fuel, and hydrogen-blend, advance at a 6.0% CAGR to 2030.

- By end-use application, onshore power and processing led with 35.7% revenue in 2024, yet offshore platforms and FPSOs show the steepest 6.8% CAGR this decade.

- By geography, Asia-Pacific captured 40.6% of 2024 revenue, whereas the Middle East and Africa grew at a 6.3% CAGR on sour-gas and gas-processing expansions.

Global Oil And Gas Exhaust System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening flare and venting restrictions in shale basins | 0.9% | North America (USA, Canada) | Medium term (2-4 years) |

| IMO Tier III offshore engine rules drive SCR retrofits | 1.2% | Global, with concentration in North Sea, Gulf of Mexico, Southeast Asia | Short term (≤ 2 years) |

| Corporate net-zero mandates by NOCs and super-majors | 0.7% | Global, led by Europe and Middle East | Long term (≥ 4 years) |

| Electrification of offshore platforms reduces exhaust demand | 0.3% | North Sea (Norway, UK), with pilot projects in Asia-Pacific | Medium term (2-4 years) |

| Methane slip reduction technology creates catalytic upgrade pull | 0.6% | North America and EU, spill-over to APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Tightening Flare and Venting Restrictions in Shale Basins

The U.S. Environmental Protection Agency began charging USD 900 per metric ton of excess flaring in January 2025, immediately turning routine flaring into a balance-sheet liability.[1]U.S. Environmental Protection Agency, “Oil and Natural Gas Sector Climate Review Rule,” epa.gov Canada’s 75% methane-reduction mandate amplifies the pressure, accelerating retrofit cycles for compression engines. Producers now favor modular exhaust skids that arrive ready for field hookup, bypassing long fabrication queues. Independent shale operators, lacking real-time sensor networks, are gravitating toward turnkey exhaust-plus-monitoring packages that integrate particulate filters and oxidation catalysts. Component suppliers expect a sustained backlog as basin-level regulations cascade to wellpad compliance reporting.

IMO Tier III Offshore Engine Rules Drive SCR Retrofits

The International Maritime Organization capped nitrogen-oxide emissions at 3.4 g/kWh for new offshore engines, pushing FPSO, drillship, and semi-submersible operators toward SCR integration.[2]International Maritime Organization, “NOx Technical Code 2025,” imo.org Norway alone has eighteen platforms in retrofit, each requiring custom manifold designs to squeeze catalyst chambers into tight engine rooms. Equinor’s Johan Castberg field illustrates the hybrid-power model: shore-based electricity meets baseload demand, while peaking turbines still need SCR to satisfy caps.[3]Equinor ASA, “Annual Report 2024,” equinor.com Vendors now bundle urea-injection skids, catalysts, and digital control to secure contracts before hull construction freezes equipment layouts.

Corporate Net-Zero Mandates by NOCs and Super-Majors

Shell’s 50% emissions-cut target for 2030 and BP’s USD 1 billion annual abatement budget redirect capital toward exhaust-system upgrades across refining and upstream assets.[4]Shell plc, “Energy Transition Strategy 2024,” shell.com Saudi Aramco’s routine-flaring ban for 2030 tightens specification envelopes for new burners and enclosed combustors. Procurement teams increasingly require ISO 14064 compatibility, spurring vendors to embed emissions accounting software in hardware quotes. The shift favors OEMs with digital ecosystems and sidelines pure-play fabricators lacking data-integration capabilities.

Methane-Slip Reduction Technology Creates Catalytic Upgrade Pull

Lean-burn gas engines emit up to 3% unburned methane, a greenhouse-gas pain point the Oil and Gas Climate Initiative flagged in 2024. Catalyst innovators now convert methane at only 350 °C, breaking a long-standing thermal barrier. Johnson Matthey recorded a 22% jump in methane-oxidation catalyst sales to North American midstream operators after the EPA charge took effect. Regulatory momentum in California and the EU suggests that slip-control retrofits will compress from decade-long cycles to under five years, pulling revenue forward for catalyst suppliers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mid-cycle downturn in greenfield LNG FIDs 2026-2028 | -0.8% | Global, concentrated in North America and East Africa | Short term (≤ 2 years) |

| High installed-base life exceeding 25 years slows replacement | -0.6% | Global, particularly mature basins in North America and North Sea | Long term (≥ 4 years) |

| Supply-chain bottlenecks for high-nickel alloys | -0.5% | Global, with acute pressure in Europe and Asia-Pacific | Short term (≤ 2 years) |

| Emerging battery-electric drilling rigs | -0.4% | North America land drilling, early adoption in Permian and Montney basins | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Mid-Cycle Downturn in Greenfield LNG FIDs 2026-2028

The sanction wave that financed U.S. Gulf Coast and Qatari megaprojects from 2021-2024 is entering construction, leaving a scheduling gap for new liquefaction trains. Papua LNG’s FID delay typifies the slowdown, deferring exhaust-equipment orders tied to large-frame turbines by at least eighteen months. Suppliers that expanded capacity during the boom now face under-utilization and may cut prices to keep lines running. Smaller fabricators without balance-sheet depth could consolidate or exit by 2028, reshaping the competitive pool.

High Installed-Base Life Exceeding 25 Years Slows Replacement

Gas turbines and reciprocating engines can operate for three decades with scheduled overhauls, postponing wholesale exhaust replacements. An International Association of Oil & Gas Producers survey shows 60% of North Sea platforms predate 2000, and most still use original ducting. Operators prefer life-extension projects at one-third the cost of new units, limiting fresh-build revenue for exhaust vendors. Battery-electric drilling rigs compound the restraint by removing diesel gensets altogether, shrinking the served market in early-adopter shale basins.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: SCR Systems Lead Compliance-Driven Growth

Selective catalytic reduction systems commanded 25.5% revenue in 2024, reflecting the most immediate path to IMO Tier III compliance. The oil and gas exhaust systems market size for SCR is projected to expand at a 5.1% CAGR through 2030, handily outstripping the aggregate trajectory. Mufflers, silencers, and oxidation-catalyst converters remain essential in noise-sensitive midstream corridors and diesel-engine applications facing local particulate limits. Sensors and control modules, while a smaller slice, are climbing fastest on the back of cloud-connected emission-monitoring platforms that optimize catalyst life and document regulatory compliance.

SCR growth keeps the oil and gas exhaust systems market on an innovation treadmill, encouraging suppliers to introduce low-temperature catalysts and modular skids that compress installation windows. Integrated OEMs bundle exhaust packages with new turbines, locking in aftermarket parts revenue, whereas specialty catalyst firms compete on regeneration cycles and platinum-group-metal loading. The result is a steady reshuffle of value-capture from iron-based ducting toward chemistry and software, reinforcing medium-term margin stability for technology holders.

By Material: Composite and Ceramic Innovation Challenges Stainless Dominance

Stainless steel continued to lead at 44.9% revenue in 2024, but composite and ceramic substrates are the breakout story, advancing at a 6.5% CAGR as operators chase weight savings and heat tolerance. The oil and gas exhaust systems market share for stainless faces incremental erosion in offshore projects where crane limits incentivize lighter catalyst housings. Nickel-rich alloys remain indispensable in ultra-high-temperature manifolds yet suffer from supply volatility tied to sanctions on Russian exports.

Composites and ceramics reduce component mass by roughly 40%, enabling larger catalyst volumes without breaching topside weight envelopes. Topsoe’s ceramic SCR elements now achieve 95% NOx conversion at 50 °C lower than legacy systems, cutting auxiliary heating loads. Qualification under revised ISO 6313 standards should unlock wider uptake, especially in deepwater assets with limited maintenance access. The oil and gas exhaust systems market, therefore, pivots toward a multi-material toolkit where cost, corrosion, and heat criteria dictate selection rather than legacy preference.

By Fuel Type: Natural-Gas Dominance Masks Dual-Fuel Momentum

Natural-gas engines captured 53.1% revenue in 2024, underscoring the global retreat from high-sulfur residual fuels. The oil and gas exhaust systems market continues to lean on gas-centric demand as pipeline build-outs in Asia and LNG import terminals in Europe advance. Diesel gensets cling to relevance in remote drilling and early-phase development, yet face substitution by battery-electric rigs and hybrid packages.

Dual-fuel and hydrogen-blend engines, grouped under “Others”, post a leading 6.0% CAGR as operators pilot low-carbon alternatives. Exhaust suppliers must juggle variable combustion chemistries, carrying broader catalyst inventories that dilute scale efficiencies. Nevertheless, early participation positions vendors for future standardization once hydrogen cost curves improve. The oil and gas exhaust systems market size for dual-fuel and hydrogen applications, while modest today, forms a strategic hedge against longer-term decarbonization mandates.

By End-Use Application: Offshore FPSO Growth Outpaces Onshore Base

Onshore power and processing maintained 35.7% revenue in 2024, anchored by the immense North American compression network and Middle Eastern gas plants. Yet offshore platforms and FPSOs chart the steepest 6.8% CAGR, buoyed by deepwater sanctions in Brazil, Guyana, and West Africa. Each new FPSO carries four to six turbines; each turbine requires SCR and noise-attenuation modules, lifting unit exhaust package values to USD 15 million-plus.

While battery-electric rigs threaten onshore upstream demand, ocean-floor distance and weather exposure keep offshore electrification partial at best, preserving exhaust opportunities. Vendors with ISO 9001 and API 618 credentials hold pricing leverage where downtime risks dwarf equipment cost. The oil and gas exhaust systems market is therefore skewing toward high-value offshore packages, even as onshore brownfield upgrades sustain a substantial revenue floor.

Geography Analysis

Asia-Pacific retained 40.6% revenue in 2024, powered by China’s coal-bed-methane compressor roll-out and India’s city-gas build-out. Bulk volumes of small-to-mid-range mufflers, catalysts, and silencers flow to these projects, anchoring factory throughput for global OEMs. Japan, South Korea, and Australia layer on high-specification orders that demand advanced materials and tight acoustic limits, supporting premium margins.

The Middle East and Africa race ahead at a 6.3% CAGR as Saudi Aramco’s Master Gas System expansion and UAE sour-gas projects require large-frame turbine packages. Egypt’s Zohr and Mozambique’s Coral South add FPSO demand in the Mediterranean and East African waters, respectively. Evolving national air-quality standards increasingly mirror WHO guidelines, guaranteeing a structural need for SCR and low-NOx burners across legacy facilities.

North America and Europe, though mature, generate steady retrofit business. EPA methane charges and Canada’s equivalency agreements accelerate catalyst swaps across the Permian and Montney basins. Europe’s Fit for 55 roadmap brings leak-detection regimes that pair naturally with continuous-monitoring exhaust sensors. South America’s outlook remains tightly coupled to Brazil’s pre-salt wave and Argentina’s Vaca Muerta midstream build-out, creating patchy yet high-value opportunities for suppliers with regional partnerships.

Competitive Landscape

Market leadership rests with the top five suppliers, Wärtsilä, GE Vernova, MAN Energy Solutions, Caterpillar Solar Turbines, and Rolls-Royce Power Systems, who collectively hold roughly 45-50% share through bundled turbine-plus-exhaust offerings. Each exploits long-term service agreements to lock in high-margin catalyst and sensor replacements. Catalyst specialists Johnson Matthey and Topsoe carve out niches by lowering light-off temperatures and extending regeneration cycles, selling directly to midstream operators.

Digitalization is reshaping rivalry. GE Vernova’s 2024 Asset Performance Management suite forecasts catalyst degradation, nudging buyers toward subscription models that raise switching costs. Wärtsilä’s cloud-connected exhaust-monitoring platform automates compliance reporting, embedding software revenue alongside hardware shipments. Acoustic-engineering boutiques and regional skid fabricators compete on lead time in midstream stations, a segment where delivery trumps brand inheritance.

Disruptive vectors loom at the energy-transition frontier. Battery-electric drilling-rig builders such as Nabors eliminate diesel gensets and the need for attendant exhaust stacks, while Kawasaki Heavy Industries pilots 100% hydrogen turbines that slash NOx to low double-digit ppm, potentially obviating SCR. Supplier resilience thus hinges on reallocating R&D toward hydrogen-ready manifolds, low-temperature catalysts, and data integration that keeps them relevant as combustion chemistries evolve.

Oil And Gas Exhaust System Industry Leaders

Wärtsilä Oyj Abp

GE Vernova (Gas Power)

Caterpillar Inc. – Solar Turbines

MAN Energy Solutions

Rolls-Royce Power Systems

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Tenaris, a global leader in manufacturing and supplying steel pipe products, unveiled a USD 85 million fume exhaust system at its Koppel, Pennsylvania, steel mill, underscoring its commitment to local community investment and environmental sustainability.

- May 2025: BorgWarner, a frontrunner in sustainable mobility solutions, has inked four volume contracts with a prominent North American automotive manufacturer. These contracts, set to run through the end of 2029, encompass the supply of Exhaust Gas Recirculation (EGR) systems, including valves, coolers, and modules, for a range of passenger and light commercial vehicle platforms.

- March 2025: Saudi engineers and specialists from GE Vernova, Inc. and Saudi Electricity Company (SEC) successfully planned and executed their inaugural gas turbine outage.

Global Oil And Gas Exhaust System Market Report Scope

In the oil and gas industry, an "oil and gas exhaust system" refers to specialized industrial exhaust systems. These systems are engineered to safely vent and manage harmful gases produced during combustion processes. In contrast, a standard vehicle exhaust system simply directs burned gases away from the engine. While the industrial exhaust system prioritizes protection against corrosion, heat, and explosions, vehicle exhaust systems emphasize noise reduction and pollutant minimization.

The global oil & gas exhaust systems market is segmented by component, material, fuel type, end-use application, and geography. By component, the market is segmented into mufflers, catalytic converters, particulate filters, SCR systems, EGR systems, sensors, and others. By material, the market is segmented into stainless steel, mild steel, titanium, nickel alloys, and composite and ceramic materials. By fuel type, the market is segmented into heavy fuel oil, diesel, natural gas, and others. By end-use application, the market is segmented into exploration and production, pipelines and stations, refineries and petrochemicals, onshore oil and gas power/processing, and offshore platforms and FPSO. The market forecasts are provided in terms of value (USD).

| Mufflers |

| Catalytic Converters |

| Particulate Filters |

| Selective Catalytic Reduction (SCR) Systems |

| Exhaust Gas Recirculation (EGR) Systems |

| Sensors |

| Others (Combination and Control Modules) |

| Stainless Steel |

| Mild Steel |

| Titanium |

| Nickel Alloys |

| Composite and Ceramic Materials |

| Heavy Fuel Oil (HFO) |

| Diesel |

| Natural Gas |

| Others |

| Exploration and Production (Upstream) |

| Pipelines and Stations (Midstream) |

| Refineries and Petrochemical (Downstream) |

| Onshore Oil and Gas Power/Processing |

| Offshore Platforms and FPSO |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Component | Mufflers | |

| Catalytic Converters | ||

| Particulate Filters | ||

| Selective Catalytic Reduction (SCR) Systems | ||

| Exhaust Gas Recirculation (EGR) Systems | ||

| Sensors | ||

| Others (Combination and Control Modules) | ||

| By Material | Stainless Steel | |

| Mild Steel | ||

| Titanium | ||

| Nickel Alloys | ||

| Composite and Ceramic Materials | ||

| By Fuel Type | Heavy Fuel Oil (HFO) | |

| Diesel | ||

| Natural Gas | ||

| Others | ||

| By End-use Application | Exploration and Production (Upstream) | |

| Pipelines and Stations (Midstream) | ||

| Refineries and Petrochemical (Downstream) | ||

| Onshore Oil and Gas Power/Processing | ||

| Offshore Platforms and FPSO | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the global oil and gas exhaust systems market?

The market stands at USD 0.67 billion in 2025 and is projected to reach USD 0.82 billion by 2030.

Which component category is growing fastest?

Selective catalytic reduction systems grow at a 5.1% CAGR thanks to IMO Tier III and methane-fee compliance.

Which region shows the highest growth rate?

The Middle East and Africa expand at 6.3% CAGR, propelled by gas-processing and sour-gas projects.

How will hydrogen blends affect exhaust-system demand?

Hydrogen co-firing up to 20% requires upgraded manifolds and modified catalysts, opening a niche for specialized systems.

What supply-chain risk could constrain market growth?

Tight nickel-alloy supply, linked to sanctions and slow Indonesian ramp-up, threatens catalyst and manifold availability.

Are battery-electric rigs a serious substitution threat?

Yes, in onshore drilling they remove diesel gensets entirely, reducing demand for conventional exhaust packages.

Page last updated on: