Office Pods Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1 Billion |

| Market Size (2031) | USD 1.65 Billion |

| Growth Rate (2026 - 2031) | 10.56% CAGR |

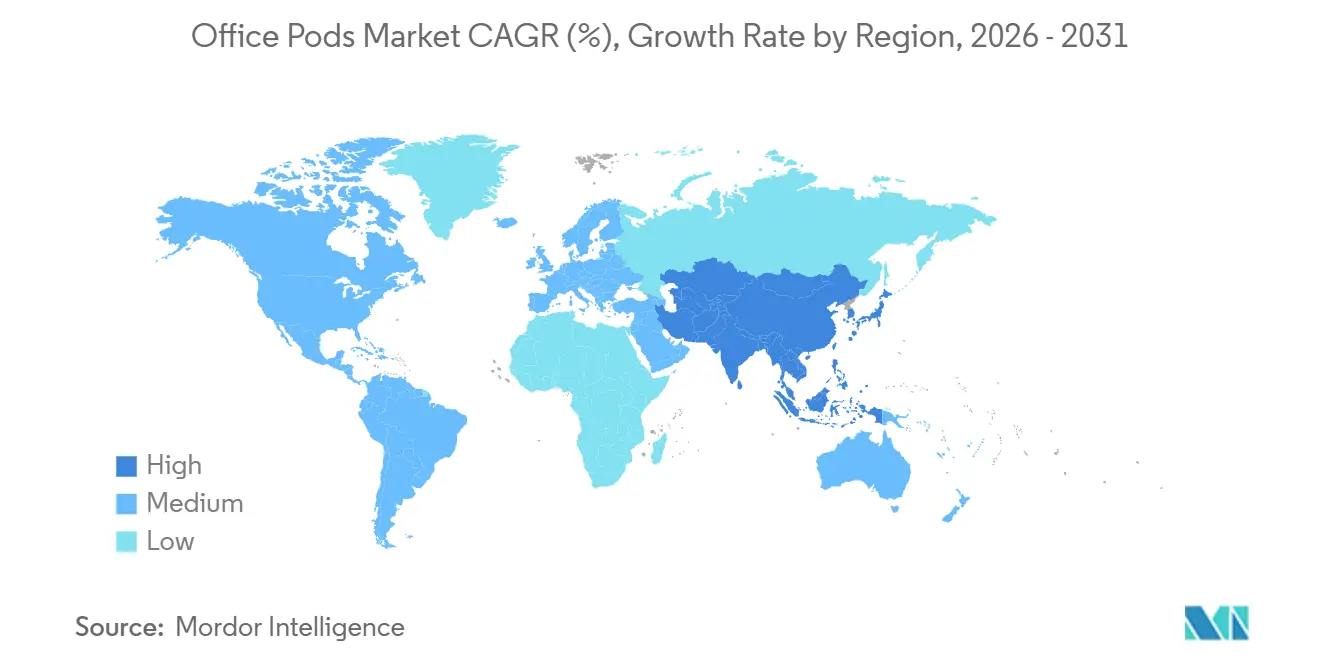

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Office Pods Market Analysis by Mordor Intelligence

The global office pods market size is expected to increase from USD 0.92 billion in 2025 to USD 1.00 billion in 2026 and reach USD 1.65 billion by 2031, growing at a CAGR of 10.6% over 2026-2031. As hybrid work becomes the norm in large enterprises, demand is rising for modular, acoustically private spaces that can be deployed quickly without permanent construction. Capital spending on smart and connected workplace infrastructure is also strengthening in 2026, which supports technology-ready pods that integrate with occupancy analytics and building-management platforms. Wider adoption of ISO 22955-compliant planning and ISO 3382-3 privacy metrics is shifting pods from discretionary amenities to required elements in fit-outs [1]Editorial Team, “ISO Standards for Acoustics in Offices,” International Organization for Standardization, iso.org. As organizations compress footprints while improving space quality, relocatable enclosures are positioned as a cost-effective way to add quiet rooms, phone booths, and focus areas within the global office pods market.

Key Report Takeaways

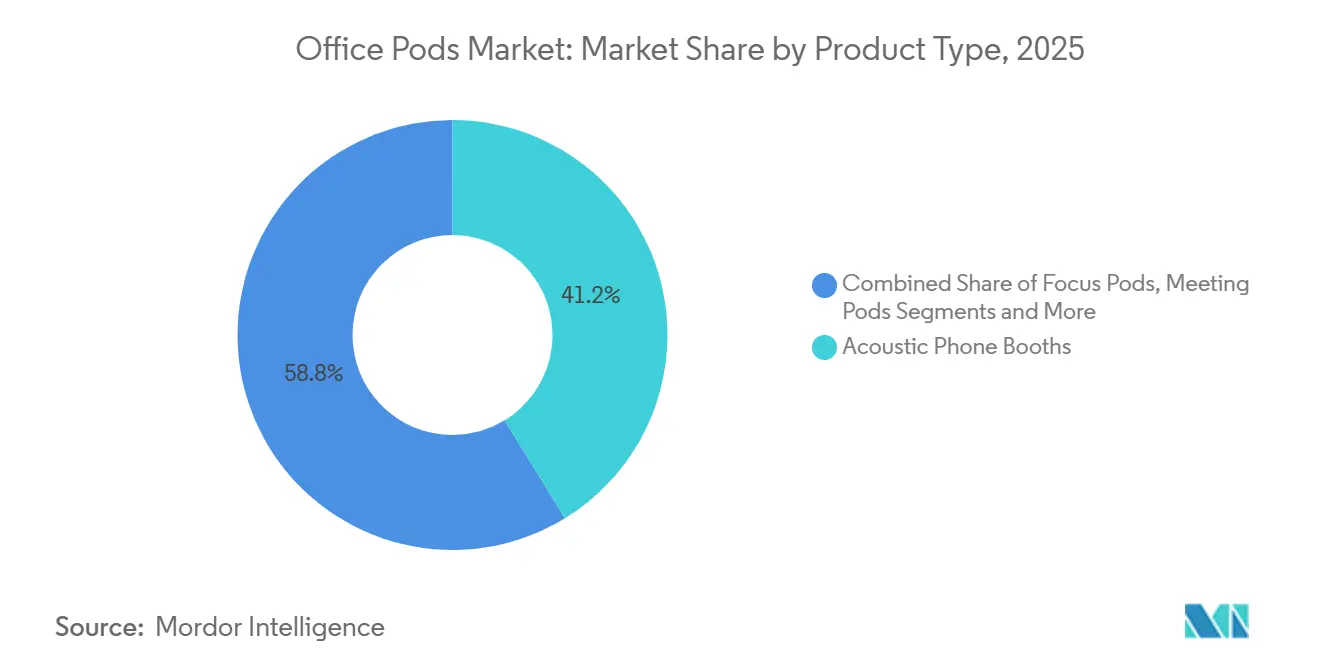

- By product type, Acoustic Phone Booths led the global office pods market with 41.23% share in 2025, while Focus Pods are projected to expand at a 12.69% CAGR through 2031.

- By capacity/occupancy, Single Person Pods accounted for 26.63% of the global office pods market share in 2025 and are forecast to grow at a 11.35% CAGR through 2031.

- By geography, North America held 63.31% of revenue in 2025, while Asia-Pacific is expected to post a 13.69% CAGR through 2031.

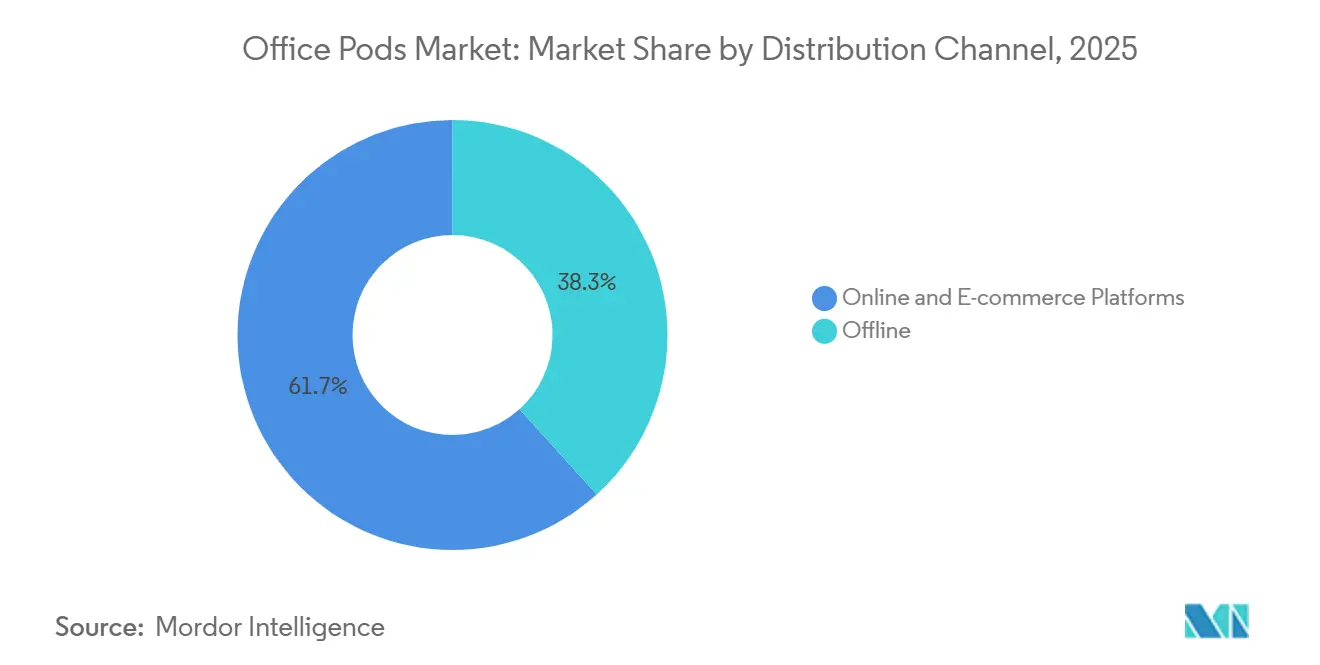

- By distribution channel, Offline captured 38.25% of sales in 2025, and Online and E-commerce Platforms are set to grow at a 14.78% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Office Pods Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hybrid work model institutionalization driving activity-based workspace reconfiguration | +3.2% | Global, with the highest penetration in North America & Europe | Medium term (2-4 years) |

| Acoustic privacy deficit in open-plan offices compelling immediate retrofit solutions | +2.8% | Global | Short term (≤ 2 years) |

| Agile workplace strategies prioritizing modular flexibility and space optimization | +1.9% | North America & Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Workplace wellness certifications mandating quantifiable acoustic comfort interventions | +1.2% | North America & European Union, early adoption in Asia-Pacific core cities | Long term (≥ 4 years) |

| Technology-integrated collaboration infrastructure aligning with smart building investments | +0.9% | Asia-Pacific core, spill-over to Middle East and Africa | Long term (≥ 4 years) |

| Sustainable rapid-deployment solutions supporting corporate ESG and circular economy commitments | +0.6% | European Union (strongest), North America, Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Hybrid Work Model Institutionalization Driving Activity-Based Workspace Reconfiguration

By 2025, hybrid work will be formalized across large employers and reshape space planning into activity-based layouts with on-demand privacy [2]Editorial Team, “Global Workplace & Occupancy Trends,” CBRE, cbre.com . Utilization data shows a persistent midweek surge pattern, with office attendance concentrated from Tuesday to Thursday, which stresses meeting rooms and call areas on peak days. Pods function as a flexible surge capacity within this pattern, as confirmed by platform analytics: most sessions occur during peak work hours, and the majority occur midweek. Enterprises report space optimization as a top objective for hybrid programs and deploy pods within neighborhood seating zones so teams can solve for intermittent peaks without adding permanent rooms. As fit-out costs rose in 2026, organizations prioritized modular elements that install in hours and can be moved multiple times throughout the lifecycle to protect capital and avoid landlord-driven construction cycles. These shifts are supporting sustained adoption across the global office pods market.

Acoustic Privacy Deficit in Open-Plan Offices Compelling Immediate Retrofit Solutions

Open-plan environments often fail to meet recognized privacy thresholds, leading to cognitive disruption that organizations seek to mitigate promptly. The ISO 3382-3 standard formalizes performance through metrics like Distraction Distance, which quantifies how far intelligible speech travels across open floors. Modular pods offer factory-verified speech reduction that meets ISO 23351-1 Class A performance, enabling them to localize calls and video meetings without a full ABC program of absorption, blocking, and masking. Targeted remediation can be more cost-effective than ceiling and partition retrofits when a small share of noisy use cases generate most complaints. Employees indicate that better access to individual focus spaces would increase office visits, which reinforces moves to add quick-deploy enclosures near team zones. This practical approach is expanding the installed base in the global office pods market as tenants triage noise with minimal disruption.

Agile Workplace Strategies Prioritizing Modular Flexibility and Space Optimization

Corporate portfolios are contracting while per-square-foot investment rises, which places agility at the center of design and procurement. Workplace leaders plan near-term updates, and many are migrating to higher-tier buildings to raise performance and employee experience, which favors relocatable pods over permanent hard walls. In the United States, pods can qualify for first-year expensing under Section 179, which supports cash flow versus conventional construction. Case studies show that multi-move scenarios over several years cost less than a single drywall renovation and cut embodied carbon by a third compared with sheetrock rooms, strengthening the financial and ESG case. Development pipelines are projected to thin in select Asia-Pacific cities from 2027, so relocatable pods help companies preserve optionality while testing layouts before committing to longer leases. These use cases reinforce steady adoption vectors for the global office pods market as space becomes a tool for adaptability.

Workplace Wellness Certifications Mandating Quantifiable Acoustic Comfort Interventions

The WELL Building Standard v2 prescribes acoustic performance, including reverberation control and sound masking ranges, which turns speech privacy from a soft perk into a verified requirement. Research from public health institutions links poor acoustics and elevated CO₂ levels to lower cognitive function and increased challenges to well-being, underscoring the value of quiet zones. Pods reduce floor-wide reverberation by removing talkers from open areas and provide certified speech reduction inside the enclosure, which supports ISO 3382-3 targets for privacy distance. Organizations also aim for neuro-inclusivity with environments that temper sensory overload, supported by products recognized for reducing distraction in sensitive user groups. Wellness-aligned spaces have been linked with lower absenteeism and higher job satisfaction, which sustains demand for modular enclosures. These wellness imperatives are now a persistent pull factor in the global office pods market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront capital investment is limiting SME adoption rates | -1.4% | Global, particularly acute in South America & Africa | Short term (≤ 2 years) |

| Space allocation challenges in existing office footprints and building code compliance | -0.9% | North America & Asia-Pacific (high real estate density markets) | Medium term (2-4 years) |

| Acoustic performance variability and standardized testing protocol gaps | -0.5% | Global, with a higher impact in emerging markets | Medium term (2-4 years) |

| Market fragmentation with inconsistent quality standards across regional manufacturers | -0.3% | Asia-Pacific, South America, MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capital Investment Limiting SME Adoption Rates

Pods concentrate capital into a single item that competes with broader real estate and IT budgets, which can slow purchase decisions for small and medium enterprises [3]Editorial Team, “Pod Pricing and Tariff Dynamics,” Office Design Works, officedesignworks.com . Rising fit-out costs in 2026 and constrained tenant improvement allowances put pressure on self-funding upgrades, so buyers scrutinize value against other priorities. Some markets offer accelerated expensing that improves cash flow, but this is not universal, leading to uneven adoption across regions. Installation labor advantages can narrow the gap with drywall in real terms, since pods assemble in hours with minimal disruption compared to permitted construction. Inflation and tariff dynamics have also raised prices in select categories, which can delay purchases to the next budget cycle. These factors weigh on the speed of adoption in cost-sensitive segments of the global office pods market.

Space Allocation Challenges in Existing Office Footprints and Building Code Compliance

Legacy floor plans can limit where pods fit due to accessibility clearances and egress paths, which may require special configurations to serve all users. Building codes and landlord rules often treat enclosed pods as rooms, which can trigger sprinkler, smoke detection, and lighting integration, thereby increasing complexity. Structural limitations, such as raised access floors with lower point-load ratings, may require surveys or reinforcement before installation, which extends timelines. Ventilation is another constraint, as passive designs can cause stuffiness during longer sessions, pushing buyers toward active systems with higher airflow. In premium buildings, owner approvals often require specification packages and insurance documentation, adding weeks to the process and potentially stalling projects. These constraints create planning friction that can delay rollouts within the global office pods market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Focus Pods Accelerate as Hybrid Work Redefines Solo Concentration Infrastructure

Acoustic Phone Booths held the largest share at 41.23% in 2025, while Focus Pods are projected to record a 12.69% CAGR through 2031, underscoring a pivot toward deep-work configurations in the global office pods market. Reduced individual desk space and rising expectations for quiet zones are driving the adoption of single-user enclosures with ergonomic seating and adjustable work surfaces. Focus Pods are being specified alongside meeting booths to rebalance floorplates where enclosed rooms were used twice as much as open collaboration areas in 2025. Larger meeting and collaboration pods remain part of team workflows but face scrutiny when ghost bookings and lower utilization create space inefficiencies on non-peak days. Newer product lines include accessible and lounge configurations to support inclusivity and comfort, which expands the addressable base [4]Editorial Team, “Hybrid Utilization Benchmarks,” Framery, framery.com .

Procurement teams are also aligning specifications with ISO privacy metrics and WELL features for reverberation and masking, which supports the selection of pods with verified acoustic and IAQ performance. This verification reduces risk and drives consistency when rolling out multi-site programs across regions. As companies standardize on connected units that report occupancy and environment data, analytics inform the right mix between phone booths, focus pods, and small collaboration enclosures. These trends reinforce Focus Pods' expansion path as a cornerstone of solo productivity in the global office pods market.

By Capacity/Occupancy: Single Person Pods Dominate as Hybrid Compression Elevates Individual Privacy

Single-person pods accounted for 26.63% in 2025 and are forecast to grow at a 11.35% CAGR through 2031, reflecting how teams plan for peak-day activity in the global office pods market. Attendance compresses midweek in many cities, so single-user units absorb call and video load without adding permanent rooms. As a result, organizations optimize for flexible, on-demand occupancy instead of building for baseline averages. Two-to-four-person pods support small-group collaboration and hybrid meetings, and usage peaks during core productive hours as teams synchronize schedules. Larger enclosures serve executive and client sessions but compete with traditional conference rooms where available.

Accessible single-person variants reduce barriers for mobility-impaired users, and mid-capacity accessible pods can accommodate mixed-ability teams without sacrificing layout. This inclusive design path encourages public-sector, education, and corporate buyers to broaden their capacity mixes. In flexible space and coworking, operators deploy 2–4-person pods to justify premium tiers and attract hybrid professionals returning from home offices, thereby diversifying use cases. Single-occupancy formats remain the anchor as buyers balance cost, acoustic performance, and adaptability in the global office pods market.

By Distribution Channel: E-commerce Platforms Surge as Direct-to-Consumer Models and Subscription Services Disrupt Traditional Dealerships

Offline captured 38.25% of 2025 revenue through direct sales, dealers, contract suppliers, and specification pathways, while Online and E-commerce Platforms are projected to grow at 14.78% CAGR through 2031 in the global office pods market. Direct-to-consumer storefronts and configuration tools enable transparent pricing and shorter lead times without dealer layers, which improves speed to value for smaller orders. Refurbished product channels and branded online shops are expanding and tie into circular commitments. For multi-site rollouts, buyers still rely on contract suppliers for MEP coordination and phased delivery, but digital onboarding is becoming standard even in dealer-mediated transactions. Subscription and rental options bundle maintenance and refresh cycles, which fit OPEX budgets and reduce lock-in risk during business change.

Regional purchase habits differ. North America and Europe are more likely to use online channels for pilot orders, while emerging Asia relies on local dealers for multi-language support and after-sales service. Macro dynamics also matter. Tariffs on select categories have highlighted the advantages of domestic sourcing, which supports direct channels for manufacturers with local production. As borrowing costs normalize more slowly than expected, the appeal of OPEX models and rapid-deploy e-commerce increments continues to build. These channel shifts are broadening reach and compressing decision cycles across the global office pods market.

Geography Analysis

North America led with 63.31% of 2025 revenue, supported by activity-based retrofits in trophy buildings and a pipeline of smart workplace upgrades in large hubs, which sustain adoption momentum in the global office pods market. Class A demand concentrated in key metros drove significant absorption, encouraging tenants to upgrade existing space with plug-and-play privacy rather than relocate. Hybrid policies and midweek peaks continue to put pressure on video and call capacity, strengthening the case for relocatable enclosures on team floors. Smart building investments in 2026 include connected pods with sensors and dashboards that advance usage analytics and performance monitoring. Policy and standards adoption, including WELL and ISO-based acoustic planning, influences specification and increases the share of certified products. Domestic production and sourcing are also tailwinds for lead time and price stability in select categories.

Europe shows steady growth, with modernization of older stock, as occupiers move to higher-tier space and prioritize verified sustainability and acoustic performance. European Union-level directives on efficiency and zero-emission buildings elevate the value of modular, energy-smart components that can be reconfigured over time. Materials transitions, including fossil-free steel in next-generation pods, are gaining traction in Nordic and DACH markets. Accessible and neuro-inclusive designs are becoming increasingly important as employers plan for diverse user needs across open areas and shared neighborhoods. Circular procurement, take-back programs, and subscription-based models are more common in BENELUX and the Nordics than in Southern Europe, where preferences for traditional enclosures persist. These themes align with enterprise ESG roadmaps and keep global office pods central to retrofit toolkits.

Asia-Pacific is the fastest-growing region through 2031, underpinned by India’s GCC expansion and renewed leasing in select financial centers, which reinforces demand for hybrid-ready, technology-enabled spaces. Grade-A office stock has expanded across major cities, and flight-to-quality trends increase the use of smart, modular components during fit-outs. China’s Tier 1 markets, Japan’s large business hubs, and South Korea’s R&D-driven campuses are deploying pods to add acoustic privacy and flexibility without structural work. Southeast Asia’s rapid development creates opportunities to specify enclosures in new builds rather than retrofits, accelerating standardization. In South America, the Middle East, and Africa, adoption is growing from a smaller base. It is concentrated in business capitals and public-sector programs that emphasize wellness and performance targets. These regional developments point to a long-term runway for the global office pods market as standards and technology mature.

Competitive Landscape

The category remains fragmented, with a wide range of regional specialists and global brands competing on acoustics, connectivity, service coverage, and sustainability. Leading manufacturers integrate sensors, occupancy analytics, and API-ready platforms to create consistent management at scale. Smart pod utilization has climbed since 2023, with the majority of sessions recorded during core hours and most activations completed online, which reflects the shift to connected ecosystems. Network and collaboration stacks continue to evolve with radar-based room sensors and integration into enterprise platforms, which brings pods into broader digital workflows. Workplace data on utilization and air quality is now a factor in procurement scoring, which favors brands with robust telemetry and integrated masking and ventilation.

Materials innovation is a second battleground as firms adopt fossil-free metals and high-recycled-content polymers to cut embedded emissions and signal ESG progress. Connected product roadmaps are converging on unified dashboards and service models that simplify deployment across portfolios with hundreds of units. Product families increasingly include accessible variants and lounge formats that complement task seating and support neuro-inclusivity. Partnerships and joint ventures in acoustics and modular construction are adding capacity and IP across regions, which should shorten lead times and diversify options. These moves underpin an innovation cycle that keeps the global office pods market dynamic.

Specialist entrants are exploring low-frequency control and thinner wall assemblies that promise performance gains without increases in weight or footprint. Room-in-room systems are expanding configuration tools within design platforms to shorten specifications and speed quotes to architects and designers. Direct-to-consumer sustainability-focused collections and high-airflow enclosures that support longer sessions are catering to user comfort and environmental goals. As WELL and ISO-aligned acoustics become common in RFPs, brands with independent lab reports and compliance documentation can command higher pricing. At the same time, price challengers compete on basic enclosures for SMEs. This tiering will likely persist as buyers standardize headquarters and maintain flexible vendor rosters for secondary sites in the global office pods market.

Office Pods Industry Leaders

Framery Oy

Mikomax Smart Office (Hushoffice)

Steelcase Inc. (incl. Orangebox pods)

SnapCab

Persy Booths

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Sonexos and Vandewiele Group announced a strategic collaboration to industrialize Plasmapanel active noise control for enclosed workspace applications, targeting pilot production in 2026 and volume manufacturing by mid-2027.

- February 2026: Vicoustic and United Acoustic Private Limited formed UniVicoustic, merging operations across Portugal and India to scale recycled PET acoustic solutions using VMT technology.

- January 2026: Lindner Group integrated CAS Rooms and MUTE+ solutions into the pCon Community platform to streamline interactive configuration and specification.

- November 2025: URBANICA Furniture unveiled the Modular Eco-Adaptive Collection using FSC-certified wood, recycled aluminum, and low-VOC coatings, with integrated power and cable management.

Global Office Pods Market Report Scope

Office pods are self-contained, prefabricated, and portable structures designed to provide acoustic privacy and flexible, quiet spaces for focused work, reducing noise distractions in open-plan offices, shared workplaces, or home environments.

The Global Office Pods Market Report is Segmented by Product Type (Acoustic Phone Booths, Focus Pods, Meeting Pods, Collaboration Pods, and Specialized Pods), Capacity (Single Person, 2-4 Person, and 5-8 Person), Distribution Channel (Offline, and Online), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD Billion).

| Acoustic Phone Booths |

| Focus Pods |

| Meeting Pods |

| Collaboration Pods |

| Specialized Pods |

| Single Person Pods |

| 2-4 Person Pods |

| 5-8 Person Pods |

| Offline | Direct Manufacturer Sales |

| Office Furniture Dealers | |

| Contract Suppliers | |

| Workplace Design and Architectural Specification | |

| Online and E-commerce Platforms |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and the Philippines) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of the Middle East and Africa |

| By Product Type | Acoustic Phone Booths | |

| Focus Pods | ||

| Meeting Pods | ||

| Collaboration Pods | ||

| Specialized Pods | ||

| By Capacity/Occupancy | Single Person Pods | |

| 2-4 Person Pods | ||

| 5-8 Person Pods | ||

| By Distribution Channel | Offline | Direct Manufacturer Sales |

| Office Furniture Dealers | ||

| Contract Suppliers | ||

| Workplace Design and Architectural Specification | ||

| Online and E-commerce Platforms | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and the Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of the Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the global office pods market?

The global office pods market size is expected to increase from USD 0.92 billion in 2025 to USD 1.00 billion in 2026 and reach USD 1.65 billion by 2031 at a 10.6% CAGR over 2026-2031.

Which product and capacity categories are leading to adoption?

Acoustic Phone Booths led with 41.23% in 2025, and Single Person Pods held 26.63%, with both benefiting from hybrid scheduling and a focus on peak days.

Which regions are shaping demand patterns for office pods?

North America leads in revenue due to retrofit activity and smart-building investments. At the same time, Asia-Pacific is the fastest-growing region, driven by Grade-A supply and GCC expansion.

What features are most valued in enterprise-grade pods?

Verified acoustic performance under ISO standards, active ventilation, occupancy sensors with analytics, and compatibility with platforms like Microsoft Places and Cisco Spaces are leading buying criteria.

How do office pods align with wellness and ESG commitments?

Pods support WELL features related to acoustics and air quality and advance circularity through fossil-free materials, recycled content, and take-back programs, improving both performance and reporting.

Which channels are growing fastest for procurement?

Online and e-commerce platforms, including subscription and rental options, show the fastest growth as they compress lead times and shift spending to OPEX.

Page last updated on: