Office Furniture For Healthcare Settings Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.64 Billion |

| Market Size (2031) | USD 2.22 Billion |

| Growth Rate (2026 - 2031) | 6.20% CAGR |

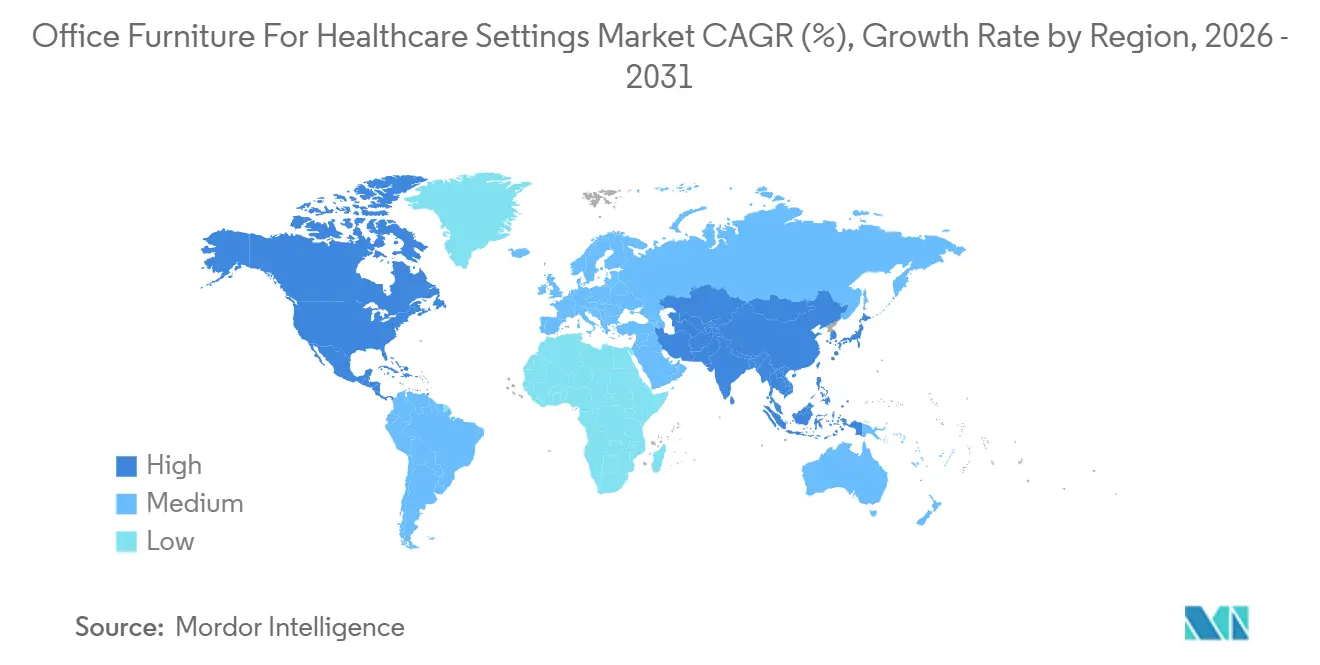

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Office Furniture For Healthcare Settings Market Analysis by Mordor Intelligence

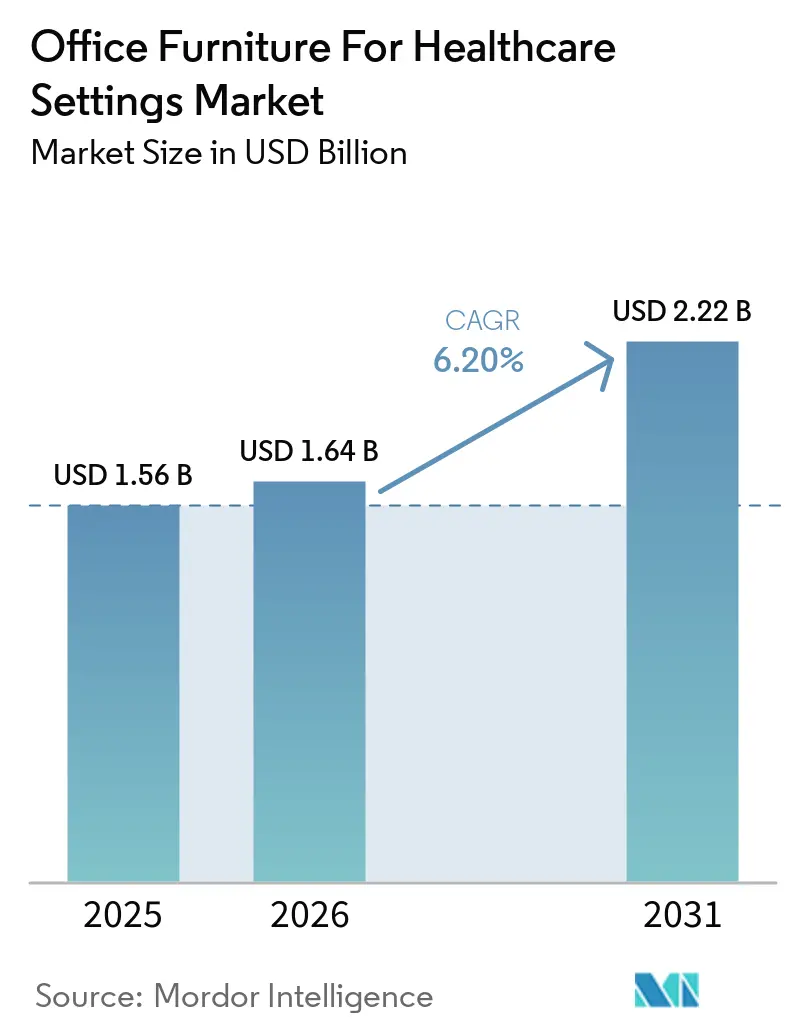

The Office furniture for healthcare settings market size is projected to expand from USD 1.56 billion in 2025 and USD 1.64 billion in 2026 to USD 2.22 billion by 2031, registering a CAGR of 6.2% between 2026 and 2031. The trajectory reflects a shift in how health systems specify, procure, and finance workspace solutions for administrative and clinical-support environments, supported by accelerated refresh cycles and a stronger focus on cleanability, modularity, and technology integration that aligns with digital care workflows. Compressed replacement cycles from 9.8 years to 6.3 years amplify recapitalization momentum while sustaining demand for antimicrobial finishes and ergonomic forms that reduce staff strain during long shifts. Procurement teams in mature systems prioritize frameworks that embed sustainability and social-value criteria into tenders, which elevate suppliers that can validate low-emission materials and end-of-life strategies. High import exposure for commercial furniture in the United States and tariff risk heighten cost and lead-time variability, reinforcing a premium on resilient supply partnerships and pricing stability.

Key Report Takeaways

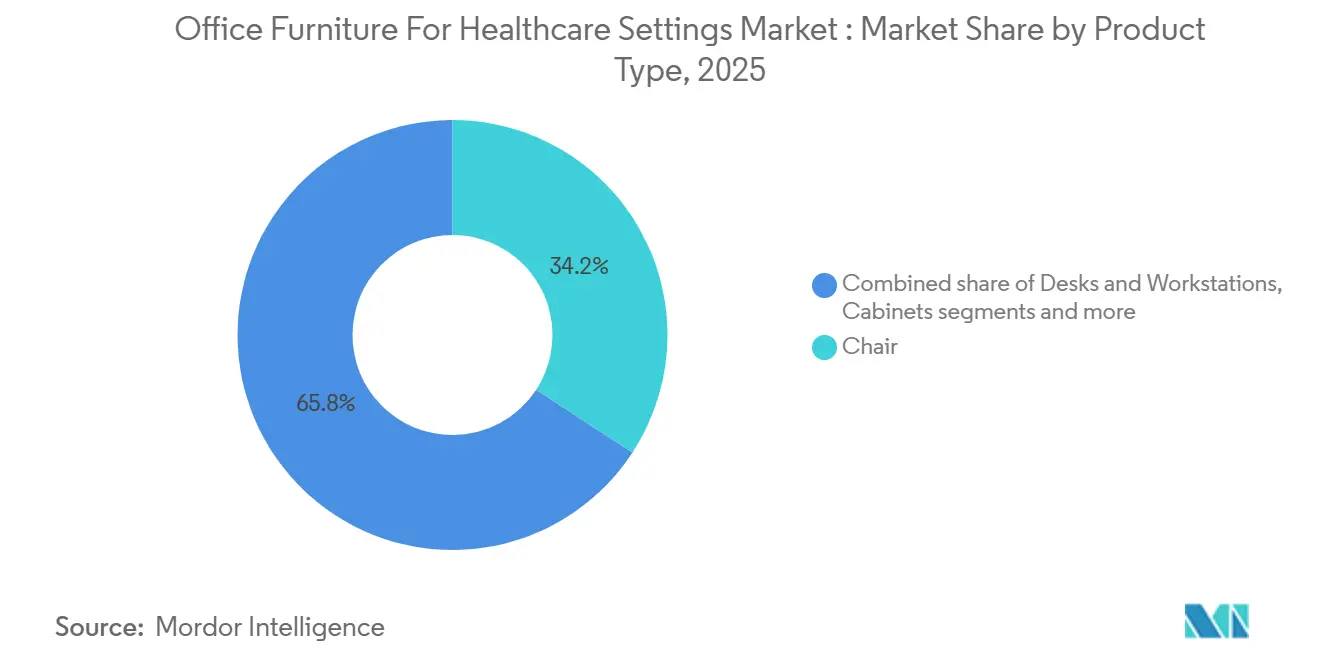

- By product type, chairs led with 34.21% of the office furniture for healthcare settings market share in 2025, while other product types are forecast to expand at a 7.48% CAGR through 2031.

- By material, metal held 41.50% of the office furniture for healthcare settings market share in 2025, whereas plastic and polymer materials are projected to grow at a 7.22% CAGR through 2031.

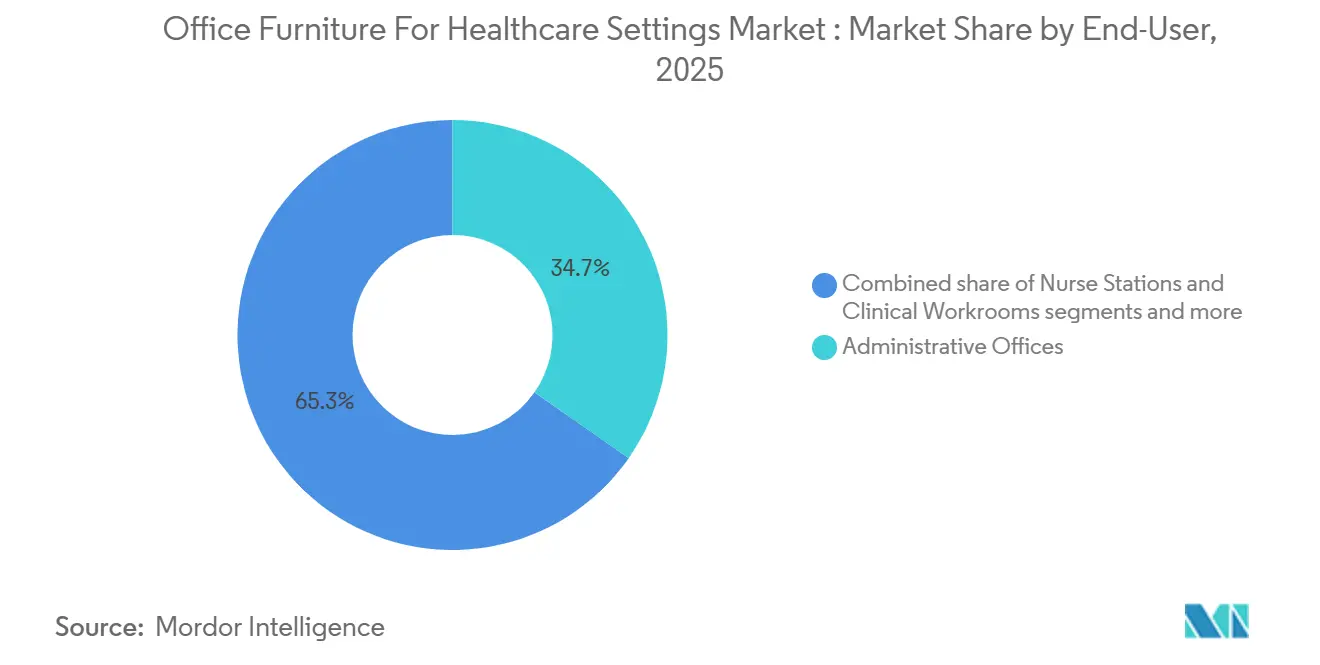

- By end-user, administrative offices accounted for 34.71% of the office furniture for healthcare settings market share in 2025, while tele-health and remote work hubs are set to expand at a 9.70% CAGR through 2031.

- By distribution channel, direct tender and institutional sales commanded 60.55% of the office furniture for healthcare settings market share in 2025. In contrast, e-commerce and catalog sales are projected to increase at a 7.40% CAGR through 2031.

- By geography, North America held 40.75% of the office furniture for healthcare settings market share in 2025, while Asia-Pacific is forecast to post a 7.68% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Office Furniture For Healthcare Settings Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Patient-Centric Design Elevates the Need for Ergonomic Reception and Admin Areas | +1.2% | Global, with early adoption in North America & the EU | Medium term (2-4 years) |

| Hybrid Work in Healthcare Boosts Demand for Modular, Reconfigurable Workstations | +0.9% | North America, Europe, Asia-Pacific metropolitan hubs | Short term (≤ 2 years) |

| Strict Infection-Control Standards Favor Easy-Clean, Antimicrobial Finishes | +1.4% | Global | Short term (≤ 2 years) |

| Digital-Health Growth Drives Tech-Integrated Desks and Device-Charging Furniture | +1.1% | North America & Asia-Pacific core, spill-over to Middle East and Africa | Medium term (2-4 years) |

| Sustainability and Green-Building Mandates Spur Low-VOC, Recyclable Furnishings | +0.8% | Europe (NHS net-zero), North America (LEED), Asia-Pacific emerging | Long term (≥ 4 years) |

| Furniture-as-a-Service Contracts Free Capex for Hospitals and Clinics | +0.6% | North America & EU advanced markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Patient-Centric Design Elevates the Need for Ergonomic Reception and Admin Areas

Health systems are upgrading reception and administrative spaces with ergonomic task seating, height-adjustable workstations, and calming aesthetics to support staff well-being and operational performance. The evolving brief draws from hospitality cues but prioritizes healthcare-grade materials, acoustic balance, and layouts that maintain visibility and access to daylight, as flagged in 2026 design guidance from a leading healthcare furnishings manufacturer. Distributed clinical support zones near patient rooms require compact, adjustable furnishings with power and data access to reduce unnecessary staff travel. These changes center on measurable outcomes such as reduced musculoskeletal complaints, fewer injury claims, and stronger staff retention, which steer specifications away from the lowest price and toward demonstrable performance. Administrative furniture choices now reflect clinical priorities for continuous operation, cleanability, and intuitive ergonomics, aligning back-office environments with quality-of-care goals[1]Furniture Concepts Editorial Team, “Healthcare Furniture: Top Design Trends,” Furniture Concepts, furnitureconcepts.com. This alignment sustains momentum in the Office furniture for healthcare settings market as decision makers connect ergonomics and ambiance to experience and productivity gains.

Hybrid Work in Healthcare Boosts Demand for Modular, Reconfigurable Workstations

Hybrid schedules for administrative teams and telehealth workflows require modular systems that can be reconfigured quickly without major renovations. Large providers are specifying functional, durable furniture systems that support routine moves and phased projects, reflecting needs documented in a metropolitan United States hospital’s multi-year furniture RFP. Design partners emphasize movable, stackable elements to accommodate therapy, group work, and private consultations within the same floorplate, thereby extending flexibility in multi-use zones. Centralized frameworks in the United Kingdom promote cost control and supply resilience while enabling organizations to adopt adaptable systems that meet sustainability and social value criteria. The first healthcare-grade privacy pod, introduced in April 2026, can be installed in about 1 hour. It reduces noise by 32 decibels, providing a rapid, compliant alternative to constructed rooms for telehealth and sensitive calls[2]ROOM x Carolina Press Team, “New Approach to Privacy in Healthcare,” Business Wire via mymotherlode.com, mymotherlode.com. Rapid pilot-and-scale approaches are now practical, allowing facilities to redeploy assets based on measured utilization and budget cycles, which supports steady expansion in the Office furniture for healthcare settings market.

Strict Infection-Control Standards Favor Easy-Clean, Antimicrobial Finishes

Procurement prioritizes smooth, non-porous surfaces and antimicrobial features that handle hospital-grade disinfectants without degrading structural integrity or appearance. Standards development is catching up with real-world use cases, including a new ASTM work item to evaluate bactericidal activity on dry and semi-porous surfaces where contamination often persists between cleanings. Sector-wide purchasing goals also drive material reformulation, with a major healthcare sustainability program requiring buyers to avoid chemicals of concern, such as PFAS and PVC, across a significant share of furniture spend. The United Kingdom frameworks pair infection prevention with clinical assurance requirements so that tech-enabled or multifunction furniture meets usability and safety thresholds relevant to frontline care settings[3]NHS Supply Chain Editorial Team, “Office and Outdoor Furniture for NHS Settings,” NHS Supply Chain, supplychain.nhs.uk. These expectations have normalized medical-grade powder coats, high-pressure laminates, and hygienic textiles that are bleach-cleanable and low-emitting, raising the table stakes for all vendors. As health systems index toward prevention and resilience, infection-control features remain central to specifications within the Office furniture for healthcare settings market.

Digital-Health Growth Drives Tech-Integrated Desks and Device-Charging Furniture

The increasing use of EHRs, telemetry, and remote consultation platforms underscores the need for furniture with embedded power, cable management, and cooling features. Alliances that integrate workplace analytics with furniture ecosystems now enable real-time visibility into occupancy, bookings, and environmental conditions across large campuses, allowing facilities to optimize staff work points and pods with evidence rather than assumptions. Clinical lounge and respite products introduced in late 2025 add mobility options and support device use in shared spaces, illustrating how comfort and utility converge in health environments. Central procurement processes in national systems bolster clinical assurance and user evaluation of tech-integrated solutions, which reduces adoption risk and waste from mis-specified items. The balance to strike is between future-readiness and near-term capital realities, prompting phased adoption patterns for tech-ready furnishings that align with refresh cycles. As digital care models scale, interoperable and power-friendly designs become the baseline in the Office furniture for healthcare settings market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tight Capital Budgets Post-Pandemic Squeeze Furniture Upgrades | -1.3% | Global, acute in the United Kingdom NHS and the United States safety-net systems | Short term (≤ 2 years) |

| Long Replacement Cycles Delay Repeat Purchases | -0.7% | North America, Europe, mature markets | Medium term (2-4 years) |

| Supply-Chain Volatility Inflates Steel, Laminate, and Foam Costs | -1.0% | Global | Short term (≤ 2 years) |

| Lack of Interoperability Standards Hinders Adoption of Smart Office Furniture | -0.4% | North America, Asia-Pacific early adopters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tight Capital Budgets Post-Pandemic Squeeze Furniture Upgrades

Elevated operating expenses and labor intensity limit discretionary spending for non-clinical assets, constraining refreshes of administrative and clinical-support furniture. The American Hospital Association’s reporting on unit economics underscores how higher labor costs shift priorities toward patient-facing equipment and essential infrastructure. In the United States, construction teams moved more projects forward in 2026. Still, many remain behind schedule and over budget relative to historical norms, which delays furniture packages and phase installations due to cash flow constraints. National frameworks in the United Kingdom incorporate net-zero and social value into procurement, strengthening governance but also increasing compliance effort that may extend timelines and resource needs for suppliers and buyers. As a result, procurement teams often extend lifecycles through repair and refurbishment while contracting for volume discounts to preserve standards across distributed campuses. These measures moderate spending while keeping environments safe and functional, although aging assets raise ergonomic and cleanability concerns over time.

Long Replacement Cycles Delay Repeat Purchases

Institutional-grade furniture is designed for durability, extending service life and reducing immediate replacement demand, even as refresh cycles shorten in some high-turnover areas. Maintenance-first strategies prioritize parts replacement and field-serviceable components, which suppresses new-unit sales but lowers total lifecycle cost. A leading healthcare seating program offers lifetime warranties for construction and finish and provides structured replacement support, encouraging repair decisions where practical. Many facilities still operate without robust capital forecasting and asset-risk modeling, resulting in reactive replacements that cluster after failures rather than planned refreshes[4]Edwards Jack, “Hospital Maintenance Budgeting Guide (2026),” Oxmaint, oxmaint.com. These patterns constrain manufacturers' visibility and make production planning more volatile, thereby influencing pricing and lead-time commitments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Chairs Lead on Ergonomic Mandates and Infection Control

Chairs command 34.21% share in 2025 and are set to grow at 7.48% CAGR through 2031, supported by infection-control requirements and ergonomic specifications tailored for long clinical and administrative shifts. This positions seating as the anchor category for the Office furniture for healthcare settings market, where bleach-cleanable materials, supportive geometry, and adjustability are now expected baselines in both front-of-house and back-office areas. Specifications increasingly call for hospital-grade cleanability and tactile controls that work with gloves, extending usability in fast-paced environments. Desks and workstations advance with height-adjustable configurations and cable management to support dual-monitor setups and peripherals tied to digital health workflows. Storage solutions prioritize secure access and seamless, non-porous surfaces in clinical-adjacent zones, aligning with hygiene and workflow needs. Tables and stools remain essential for multi-purpose areas and meeting rooms that flip between group sessions and focused tasks, aided by modularity and easy cleanability. Ergonomic accessories, such as monitor arms and keyboard supports, help facilities capture the full value of seating investments by reducing strain on posture during documentation-heavy work.

Compared with the overall Office furniture for healthcare settings market, chairs’ projected 7.48% growth through 2031 outpaces the category average. It reinforces the role of seating in mitigating risks to staff well-being. Telehealth expansion is reshaping demand for specialized privacy pods and meeting booths that install quickly and deliver meaningful acoustic control, including a healthcare-specific pod launched in April 2026 with 32-deibel noise reduction and healthcare-grade finishes. Lounge and sleeper seating introduced in late 2025 bring mobility and conversion features for family accommodations and staff respite, increasing utilization of public spaces without added floor area. Procurement teams lean on frameworks and clinical assurance to validate cleanability and durability claims for category leaders. These trends sustain an elevated share for seating and reinforce the segment’s centrality within the Office furniture for healthcare settings market.

By Material: Metal Dominates in Hygiene, Plastic Polymers Surge in Innovation

Metal furnishings hold a 41.50% share in 2025 due to their non-porous surfaces and corrosion resistance, which support repeated hospital-grade cleaning in high-risk zones. For clinical-adjacent and administrative areas, metal casework and frames pair with performance laminates and coatings that deliver longevity, visual consistency, and low-VOC emissions. Procurement teams choose finishes that meet sustainability targets while maintaining resistance to disinfectants, which helps standardize specifications across distributed campuses. Wood remains important for reception and executive spaces when aesthetics and warmth are central, often through engineered or high-pressure laminate surfaces that mimic natural grain and help with maintenance. Plastics and polymers are the fastest-growing segment, with a 7.22% CAGR, as antimicrobial and solid-core solutions address seam-free cleanability, impact resistance, and colorfastness in high-use areas. These developments broaden material choice and create tailored packages by zone while maintaining consistent clinical and sustainability performance.

The balance among materials reflects infection prevention, lifecycle cost, and procurement governance. Updated frameworks in national systems embed supplier assessments and carbon plans that favor materials with lower embodied impact and strong end-of-life options. Growth in polymers is driven by advances in materials science and cleaner chemistries that meet medical cleanability standards without relying on chemicals of concern flagged by healthcare buyers. Metal’s share remains anchored by sterility and durability requirements in equipment-adjacent zones, ensuring it continues to lead the Office furniture for healthcare settings market across clinical contexts. Cross-functional teams use decision matrices to align clinical needs, sustainability targets, and cost envelopes while maintaining a recognizable aesthetic across multiple facilities.

By End-User: Administrative Offices Anchor Demand, Tele-Health Hubs Fastest Growing

Administrative offices account for 34.71% of demand in 2025, reflecting the large footprint of non-clinical operations in integrated delivery networks. Specifications balance price discipline with durability, warranty coverage, and design cohesion across standardized workstation packages in multi-building campuses. Nurse stations and clinical workrooms emphasize compact footprints with embedded power for EHR work, supply access, and clinician collaboration, all under cleanability requirements. Waiting and reception areas serve as brand touchpoints and patient-calming zones, steering investments toward hospitality-grade solutions that meet healthcare cleaning protocols and bariatric capacity needs.

Telehealth and remote work hubs are the fastest-growing end use, with a 9.70% CAGR, enabled by acoustic pods with healthcare-grade finishes and fast installation that support private consultations without tying up exam rooms. Staff respite and training areas now use mobile and convertible seating to support multipurpose usage while maintaining cleaning and durability standards. Operating models that blend onsite and remote care drive adoption of reservation systems and shared workpoints, improving occupancy balance over time and across program areas. These shifts sustain the Office furniture for healthcare settings market by tying end-user configurations to access expansion, ergonomics, and workflow performance.

By Distribution Channel: Direct Tenders Dominate, E-Commerce Gains on Transparency

Direct tender and institutional sales hold 60.55% of the Office furniture for healthcare settings market share in 2025 as frameworks, group purchasing, and shared-services models concentrate spend and standardize compliance. In the United Kingdom, frameworks for office and medical furniture embed mandatory requirements for carbon plans, supplier assessments, and social value, which favor well-capitalized, compliance-ready suppliers. Canadian shared-services organizations manage procurement for large hospital redevelopments and behavioral health facilities, coordinating FF&E scope and multi-year deliveries. Dealer and distributor channels remain important for mid-market institutions that prefer local service and tailored support for installation and moves.

E-commerce and catalog sales are growing at a 7.40% CAGR as buyers leverage price transparency to purchase routine categories such as task seating and accessories that fall below centralized tender thresholds. Online medical-furnishings platforms distinguish themselves with healthcare-specific product guidance and support content for infection prevention and cleanability claims. Circular-economy lots within frameworks create options for reuse and refurbishment, compelling traditional channels to integrate take-back and asset grading into proposals. Hybrid channel strategies help systems meet service levels while managing total cost, sustaining diversification across the Office furniture for healthcare settings market.

Geography Analysis

North America retains a 40.75% share in 2025, supported by capital projects and mature procurement structures that consolidate spend, ensure compliance, and align pricing. The United States hospital construction teams report modest budget growth with continued schedule pressure, which shapes furniture deliveries, staging, and cash flow timing. Major United States systems continue to specify modular, reconfigurable solutions, as reflected in a large RFP spanning multiple campuses and program areas. Canada’s shared-services model executes complex, multi-year hospital redevelopments with defined FF&E workstreams and vendor oversight, anchoring standards for sustainability and clinical assurance. Behavioral health facilities in Toronto adopt anti-ligature and specialized furnishings through centralized procurement to manage scope and risk over multi-year builds. These frameworks and capital programs shape steady demand for compliant, durable, and tech-ready products within the Office furniture for healthcare settings market.

Asia-Pacific is the fastest-growing region, with a 7.68% CAGR to 2031, reflecting structural capacity gaps and ongoing investment in facilities supporting hybrid and digital care models. Investment in new beds and ambulatory capacity supports demand for cleanable, modular, and tech-integrated furniture packages across administrative and clinical-support settings. Localization strategies by global OEMs and regional suppliers help mitigate import dependence, shorten lead times, and stabilize pricing exposure in larger national markets. As systems scale, procurement governance and standardization raise baselines for cleanability, sustainability, and interoperability, reinforcing tailwinds for vendors that can document performance. Growth outpaces GDP in several markets due to prioritization of health infrastructure and preparedness, amplifying the outlook for the Office furniture for healthcare settings market. Supplier partnerships that balance price, warranty, and service support will play a decisive role in capturing multi-year frameworks across fast-growing metros.

Europe’s procurement landscape is shaped by net-zero commitments and social value, embedding mandatory supplier disclosures and assessments across furniture frameworks used in care settings. These governance structures elevate environmental criteria and lifecycle strategies, ensuring low-VOC, recyclable, and durable materials become standard practice in office and clinical-adjacent furnishings. Circular-economy lots for reuse and refurbishment provide a structure for asset recapture and grading, which can reduce total costs and waste streams as products are refreshed. Performance standards for infection prevention and cleanability are applied at the framework level to keep clinical assurance central in procurement. As regions vary in capital intensity and refresh cadence, governance and standards hold the market together, steering cross-country suppliers to maintain harmonized compliance files and certifications for tenders.

Competitive Landscape

The Office furniture for healthcare settings market presents moderate-to-high fragmentation tempered by active consolidation, with leading groups expanding portfolios and distribution capacity through targeted acquisitions. In December 2025, HNI Corporation completed the acquisition of Steelcase in a cash-and-stock transaction, creating a large-scale enterprise with an integrated dealer ecosystem. Portfolio expansion, digital transformation, and customer experience improvements are central to the integration thesis, as the combined entity seeks to leverage scale and complementary strengths across the health, education, and corporate segments. In April 2026, Flokk’s acquisition of Spec Furniture extended its reach in North America and sharpened its focus on healthcare, education, corporate, and behavioral health, advancing a balanced regional revenue strategy.

Technology partnerships differentiate market leaders as connected solutions broaden use cases and inform planning. A January 2026 alliance integrates AI-powered workplace analytics into furniture ecosystems to enable real-time occupancy, environmental monitoring, and booking optimization, giving facilities the levers to increase utilization and staff satisfaction while reducing space intensity. Category innovations include a healthcare-specific privacy pod launched in April 2026 that offers rapid installation and meaningful acoustic performance, enabling HIPAA-friendly telehealth environments without full construction. Late 2025 releases in lounge and sleeper seating underscore mobility and conversion features in health environments and caregiver respite zones, where cleanability and comfort are joint design priorities.

Standards-setting and clinical assurance are now competitive essentials in bids. Antimicrobial-surface testing development through ASTM and healthcare procurement frameworks that require clinical assurance helps normalize evidence requirements across suppliers. Sustainability programs push suppliers to meet low-emission and chemical-avoidance criteria, which, in turn, influence material choices and verification practices. National frameworks extend the requirements to all bidders, raising the minimum bar on documentation and compliance programs for Office furniture for healthcare settings market participants.

Office Furniture For Healthcare Settings Industry Leaders

Herman Miller Healthcare (MillerKnoll) / Nemschoff

Steelcase Health

KI (Healthcare)

Global Furniture Group (GlobalCare)

Haworth Health

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: ROOM and Carolina partnered to launch the ROOM x Carolina Phone Booth, the first privacy pod specifically designed for healthcare environments. It features 32 dB of noise reduction, proprietary hygienic interior fabrics, and rapid installation.

- January 2026: Spaceti joined the Steelcase Hybrid Solutions and Technology Partner Program as an Alliance Partner, integrating its AI-powered space reservations, occupancy analytics, and environmental monitoring with Steelcase’s hybrid workplace portfolio.

- December 2025: HNI Corporation completed its acquisition of Steelcase Inc. in a cash-and-stock transaction, uniting complementary brand portfolios and dealer networks serving the healthcare, education, and corporate segments.

- October 2025: Kimball International, through its Interwoven brand, launched the Havei recliner series. Informed by caregiver interviews, the launch included 3-position recliners, patient recliners, and gliders designed for clinical settings and corporate wellness spaces.

Global Office Furniture For Healthcare Settings Market Report Scope

Office furniture for healthcare settings is designed to meet the functional, ergonomic, and hygiene requirements of medical environments such as hospitals, clinics, and diagnostic centers. The office furniture for healthcare settings market is segmented by product type, material, end-user, distribution channel, and geography. By product type, the market is segmented into chairs, desks and workstations, cabinets and storage, tables and stools, ergonomic accessories, and others. By material, the market is segmented into wood, metal, plastic & polymers, and other materials. By end user, the market is segmented into administrative offices, nurse stations and clinical workrooms, waiting and reception areas, consultation/exam support offices, staff break and training rooms, and telehealth and remote work hubs. By distribution channel, the market is segmented into direct tender / institutional sales, dealer & distributor sales, and e-commerce & catalog sales. By geography, the market is segmented into North America, South America, Europe, Asia-Pacific, and the Middle East & Africa. The report provides the market size in USD for all the above-mentioned segments.

| Chair |

| Desks and Workstations |

| Cabinets and Storage |

| Table and Stools |

| Ergonomic Accessories |

| Others |

| Wood |

| Metal |

| Plastic & Polymers |

| Other Materials |

| Administrative Offices |

| Nurse Stations and Clinical Workrooms |

| Waiting and Reception Areas |

| Consultation/Exam Support Offices |

| Staff Break and Training Rooms |

| Tele-health and Remote Work Hubs |

| Direct Tender / Institutional Sales |

| Dealer & Distributor Sales |

| E-commerce & Catalog Sales |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and the Philippines) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of the Middle East and Africa |

| By Product Type | Chair | |

| Desks and Workstations | ||

| Cabinets and Storage | ||

| Table and Stools | ||

| Ergonomic Accessories | ||

| Others | ||

| By Material | Wood | |

| Metal | ||

| Plastic & Polymers | ||

| Other Materials | ||

| By End-User | Administrative Offices | |

| Nurse Stations and Clinical Workrooms | ||

| Waiting and Reception Areas | ||

| Consultation/Exam Support Offices | ||

| Staff Break and Training Rooms | ||

| Tele-health and Remote Work Hubs | ||

| By Distribution Channel | Direct Tender / Institutional Sales | |

| Dealer & Distributor Sales | ||

| E-commerce & Catalog Sales | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and the Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of the Middle East and Africa | ||

Key Questions Answered in the Report

What is the Office furniture for healthcare settings market size outlook through 2031?

The Office furniture for healthcare settings market size is projected to expand from USD 1.56 billion in 2025 and USD 1.64 billion in 2026 to USD 2.22 billion by 2031, reflecting a 6.2% CAGR over 2026-2031.

Which region leads and which grows fastest in this space?

North America leads with 40.75% share in 2025, while Asia-Pacific is the fastest-growing at a 7.68% CAGR through 2031.

Which product and end-user segments set the pace?

Chairs lead with 34.21% share in 2025 and grow at 7.48% CAGR to 2031, while tele-health and remote work hubs are the fastest-growing end use at 9.70% CAGR.

How are procurement frameworks influencing specifications and vendor selection?

National frameworks embed carbon plans, clinical assurance, and social value as mandatory requirements, favoring compliant, documented solutions and influencing supplier qualification and pricing.

What risks most affect cost and delivery?

Import exposure and tariffs raise input and finished-goods costs, while construction-schedule pressures and long-lead items can delay projects and stage installations.

Which strategic moves are reshaping competition?

HNI’s acquisition of Steelcase and Flokk’s acquisition of Spec Furniture expand portfolios and distribution, while alliances like Steelcase–Spaceti enable data-informed planning and utilization improvements.

Page last updated on: