Ocular Inflammation Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 8.21 Billion |

| Market Size (2031) | USD 10.78 Billion |

| Growth Rate (2026 - 2031) | 5.61% CAGR |

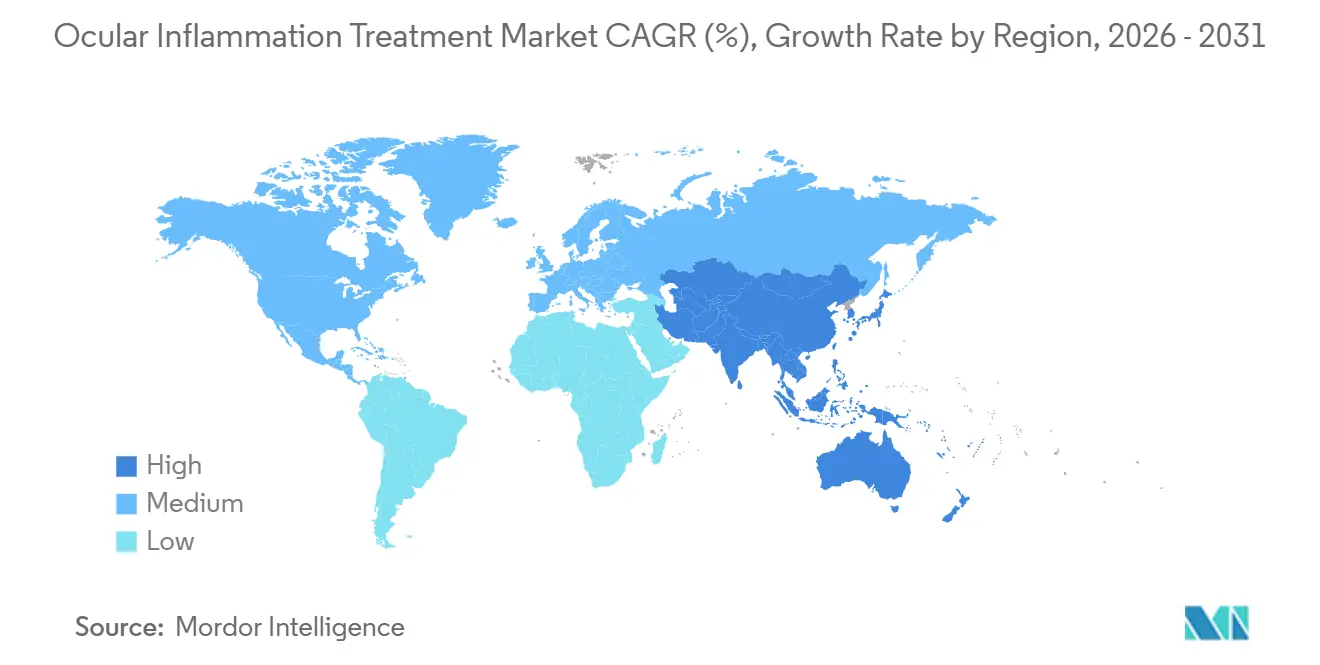

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

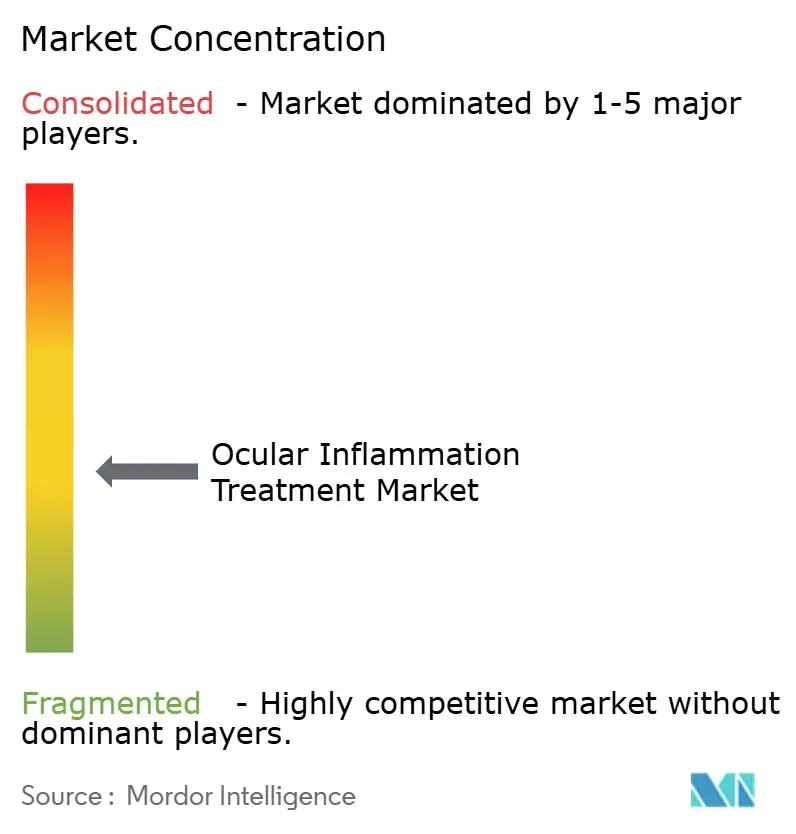

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ocular Inflammation Treatment Market Analysis by Mordor Intelligence

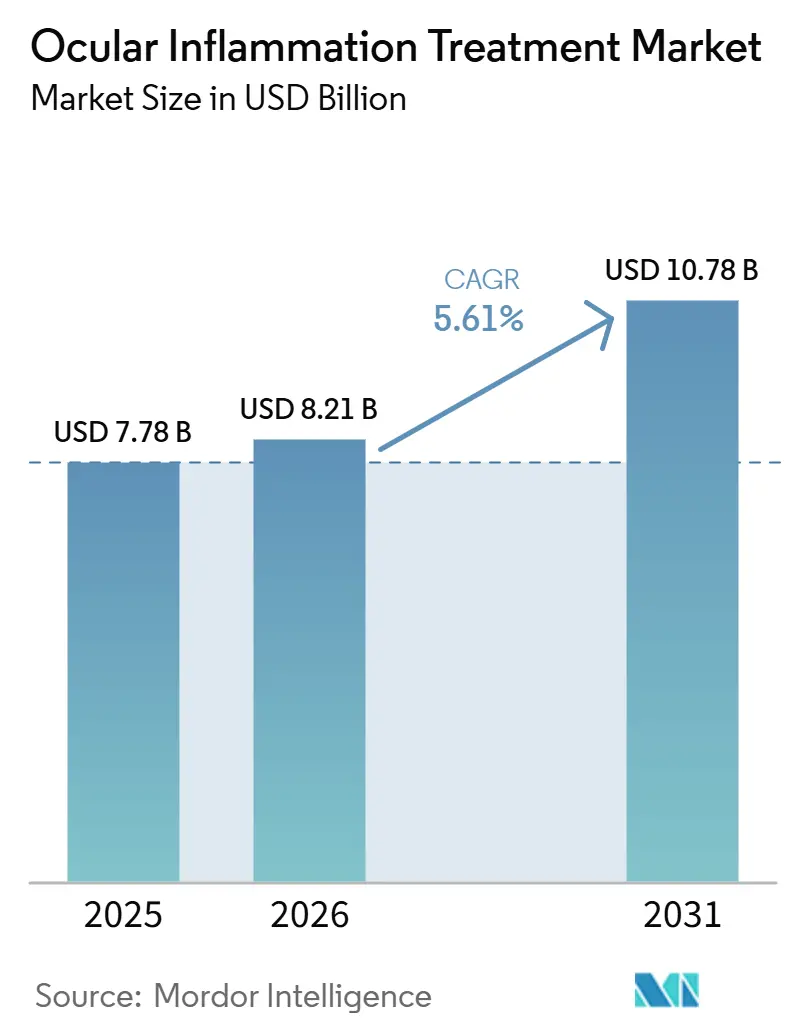

The Ocular Inflammation Treatment Market size was valued at USD 7.78 billion in 2025 and is estimated to grow from USD 8.21 billion in 2026 to reach USD 10.78 billion by 2031, at a CAGR of 5.61% during the forecast period (2026-2031).

The ocular inflammation treatment market is moving beyond its older corticosteroid and cyclosporine base as biologic therapies, sustained-release implants, and AI-supported monitoring continue to change treatment practice across major regions. North America led the ocular inflammation treatment market in 2025 because it had the deepest specialist base, established reimbursement support, and earlier use of advanced biologics and procedures. Asia-Pacific is set to post the fastest growth in the ocular inflammation treatment market as specialist access improves, hospital pharmacy networks widen, and newer approvals support broader uptake of suprachoroidal and topical anti-inflammatory treatments. Competition in the ocular inflammation treatment market remains moderate to high because large biopharma companies hold strong branded positions, while specialty firms are competing through delivery systems, oral targeted therapies, and long-acting implants. Growth in the ocular inflammation treatment market still faces pressure from high biologic costs, limited biomarker standardization, and sterile cold-chain constraints, which keep access uneven across lower-income settings and make treatment selection less precise than clinicians would prefer.

Key Report Takeaways

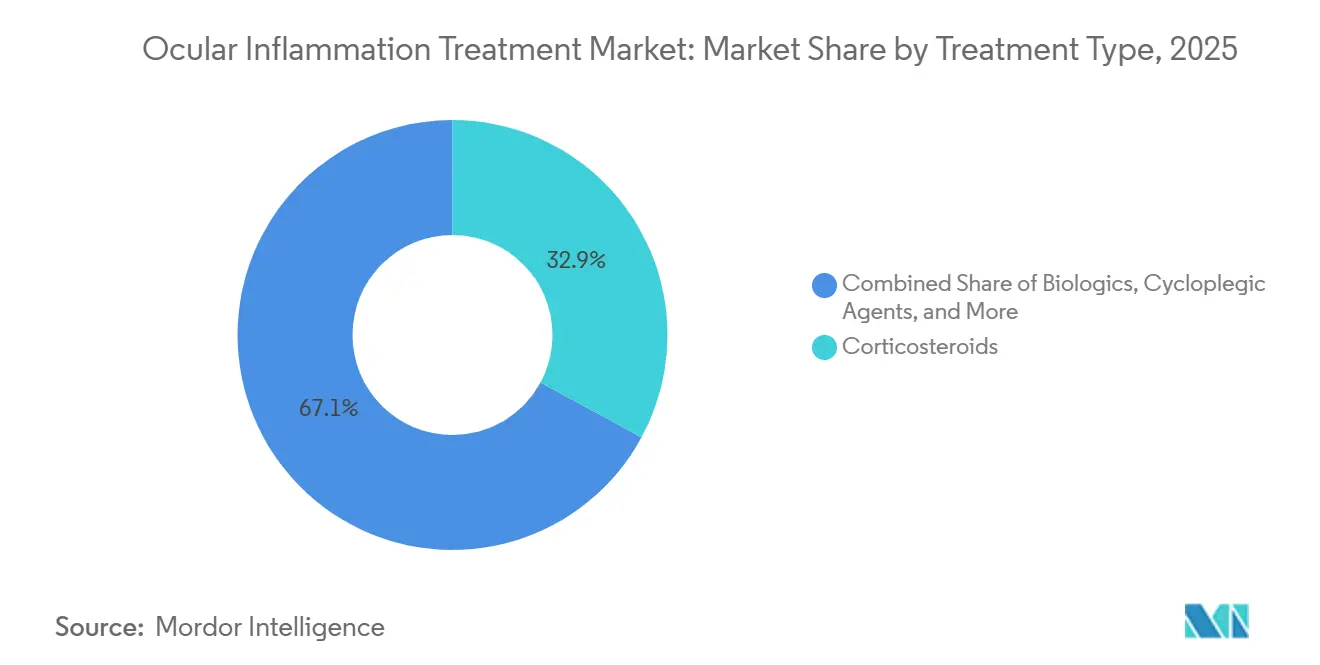

- By treatment type, corticosteroids led with 32.89% revenue share in 2025, while immunosuppressants and immunomodulators are forecast to expand at a 6.83% CAGR through 2031.

- By disease type, uveitis held 34.18% share in 2025, while conjunctivitis is projected to grow at a 6.36% CAGR through 2031.

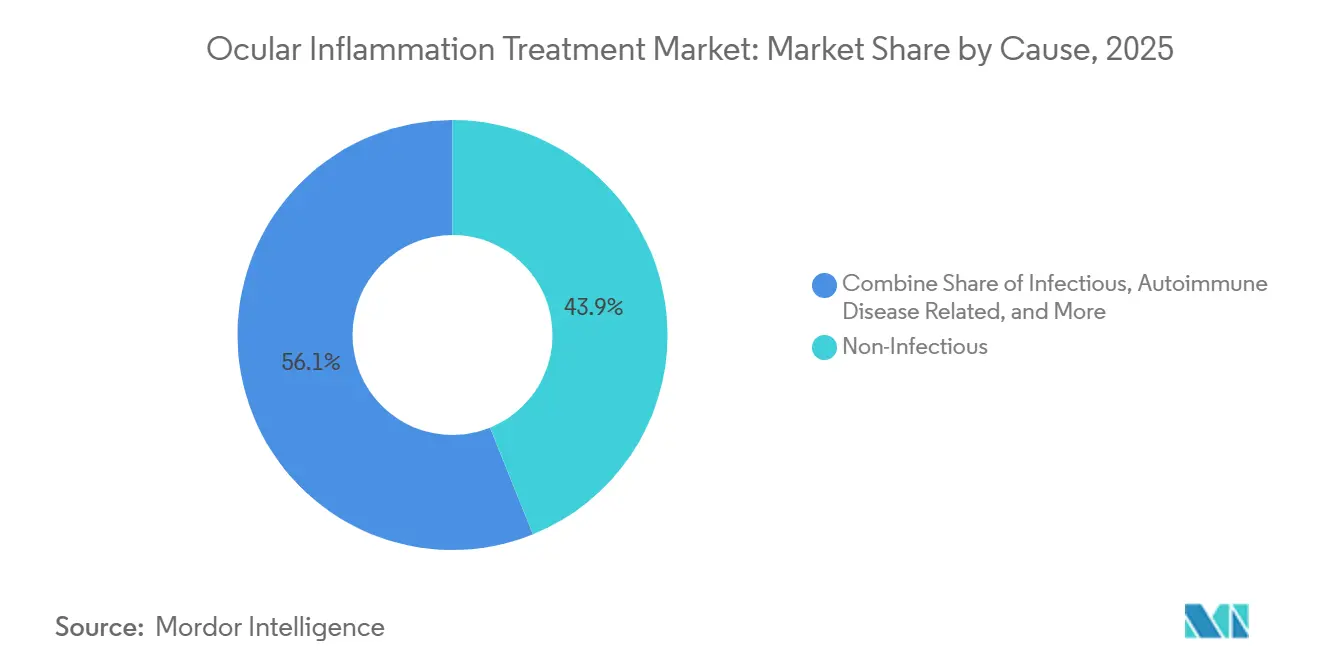

- By cause, non-infectious cases accounted for 43.89% share in 2025, while autoimmune disease-related cases are projected to advance at an 8.23% CAGR through 2031.

- By route of administration, topical therapies captured 58.36% share in 2025, while injectable therapies are expected to grow at an 8.10% CAGR through 2031.

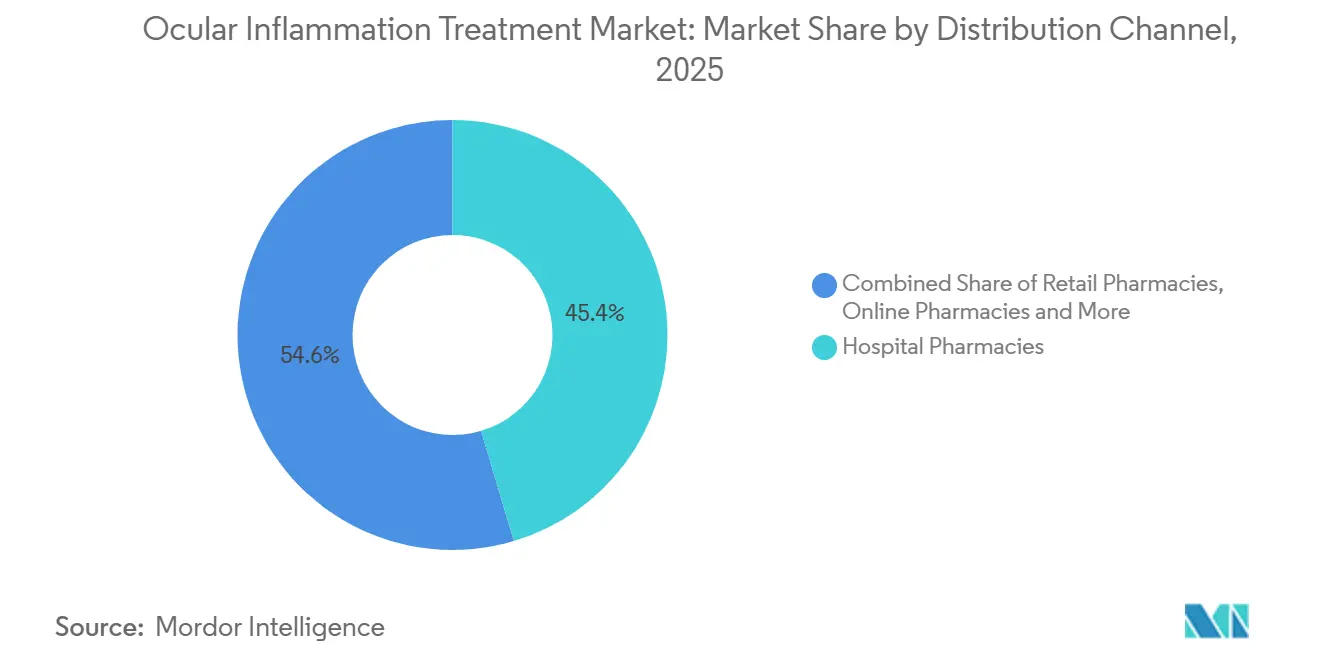

- By distribution channel, hospital pharmacies held 45.38% share in 2025, while online pharmacies are forecast to expand at an 8.34% CAGR through 2031.

- By geography, North America held 42.38% share in 2025, while Asia-Pacific is projected to grow at a 7.16% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Ocular Inflammation Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of Uveitis and Other Ocular Inflammatory Disorders | +1.2% | Global, with highest volume in North America, Western Europe, and South Asia | Medium term (2-4 years) |

| Higher Biologic Adoption in Refractory and Chronic Cases | +1.5% | North America and EU core, with emerging adoption in Asia-Pacific and GCC | Long term (≥ 4 years) |

| Sustained-Release and Depot Delivery Innovation | +1.0% | North America pioneer, with Asia-Pacific following through XIPERE and ARCATUS approvals | Long term (≥ 4 years) |

| AI-Guided Phenotyping and Imaging-Based Treatment Selection | +0.5% | United States, United Kingdom, Singapore, and South Korea, with spillover to urban Asia-Pacific and Middle East centers | Long term (≥ 4 years) |

| Office-Based Administration and Specialty Pharmacy Access Expansion | +0.4% | North America and Europe, with growing effect in Southeast Asia and GCC | Medium term (2-4 years) |

| Pediatric and Recurrent-Case Treatment Recurrence Creating Repeat Demand | +0.6% | Global, concentrated in North America, India, and East Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Uveitis and Other Ocular Inflammatory Disorders

The ocular inflammation treatment market continues to gain volume support from the burden of uveitis, which causes a level of vision loss that is much higher than its case count alone would suggest. A 2025 TriNetX analysis reported cumulative uveitis prevalence of 260.8 per 100,000 persons, and anterior uveitis made up 75.1% of cases, which keeps first-line anti-inflammatory therapy demand broad and persistent.[1]Incidence and Prevalence of Uveitis and Associated Ocular Complications in the United States TriNetX Database The same study linked many cases to systemic inflammatory disease, and that matters because wider diagnosis of inflammatory spondyloarthropathies is enlarging the population that eventually reaches ophthalmic care. Regional variation in etiology is also important because product demand in the ocular inflammation treatment market does not scale evenly across countries, and companies with local evidence are better placed to match therapy choice to patient mix. This keeps the ocular inflammation treatment market tied not only to headline case growth, but also to better detection and repeat treatment in recurrent disease.

Higher Biologic Adoption in Refractory and Chronic Cases

The ocular inflammation treatment market is also gaining support from earlier use of biologics and other steroid-sparing therapies in refractory and chronic disease. The United States immunomodulatory therapy trends showed that adalimumab use was already rising before formal approval in non-infectious uveitis, which indicates that clinical practice had started shifting before regulation caught up. That shift is now extending to new oral targeted options, as Priovant received FDA Fast Track Designation for brepocitinib in September 2024 and enrolled the first patients in the Phase 3 CLARITY trial in the same month. Phase 2 NEPTUNE data also showed a 29% treatment-failure rate at week 24 with brepocitinib 45 mg, which suggests that oral mechanism-based therapy may soon challenge injectable biologics in selected non-anterior cases. The September 2025 end of Humira pediatric orphan exclusivity also widened the path for biosimilar entry, which should increase the number of patients who can reach biologic therapy even as brand pricing comes under pressure. This pattern gives the ocular inflammation treatment market a broader middle layer of patients who may move beyond steroid-only care and into longer-duration systemic treatment.

Sustained-Release and Depot Delivery Innovation

The ocular inflammation treatment market is being reshaped by sustained-release and depot technologies that reduce the burden of daily dosing and frequent outpatient visits. In preclinical work published in 2025, polymer-free tacrolimus microspheres achieved up to 30-day corneal retention after subconjunctival injection and suppressed both TNF-α and VEGF, which shows that durable multi-target delivery is now technically feasible. Clearside Biomedical also extended commercial validation for the SCS Microinjector platform when Health Canada approved XIPERE for uveitic macular edema in July 2025, adding Canada to the United States, Australia, and Singapore. The reimbursement base for that route is still early because the CPT Category 1 code for the suprachoroidal procedure only became active in January 2024, which means current adoption likely understates future demand. Separate preclinical work on liposomes, hydrogels, and polymeric micelles has shown sustained loteprednol release over 12 days, which keeps a non-procedural path open for long-acting topical therapy. This creates a clear shift in the ocular inflammation treatment market toward duration, route, convenience, and better disease control between visits.

AI-Guided Phenotyping and Imaging-Based Treatment Selection

The ocular inflammation treatment market is also starting to benefit from AI tools that turn subjective inflammation scoring into more repeatable clinical measurements. A 2025 cross-sectional study using the Swin Transformer V2 algorithm on AS-OCT B-scans from 830 scans produced stable biomarker readings over 6 months, which supports the use of AI metrics in treatment monitoring and trial endpoints.[2]Novel Artificial Intelligence–Based Quantification of Anterior Chamber Inflammation Using Vision Transformers Moreover, A separate 2025 study showed that a multimodal reasoning agent using GPT-4o image analysis and retrieval-augmented guidance outperformed ophthalmology residents in real-world diagnostic cases, which points to near-term use in decision support rather than simple documentation. As these systems mature, the ocular inflammation treatment market should see better monitoring discipline in specialist centers that already rely on imaging-heavy workflows.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Biologics and Advanced Drug-Delivery Systems | -1.0% | Global, most acute in South America, Middle East and Africa, and lower-income Asia-Pacific markets | Medium term (2-4 years) |

| Steroid Safety Burden and Long-Term Compliance Issues | -0.6% | Global, particularly pronounced in pediatric and geriatric populations | Medium term (2-4 years) |

| Limited Biomarker Standardization for Precision Treatment Selection | -0.4% | Global, with highest clinical impact in North America and Europe | Long term (≥ 4 years) |

| Sterile Manufacturing and Cold-Chain Supply Vulnerability | -0.3% | Global, with highest exposure in emerging market distribution networks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Biologics and Advanced Drug-Delivery Systems

The ocular inflammation treatment market still faces a major access barrier because biologics and advanced delivery systems remain expensive for many patients and payers. A 2024 systematic review found annual medication costs for non-infectious uveitis ranging from USD 345 to USD 13,134, and prescription costs were 60% higher for blind patients than for patients with moderate vision loss.[3]Economic Burden and Cost-Effectiveness of Management of Non-Infectious Uveitis: A Systematic Review A 2025 American Journal of Ophthalmology study also found that prior authorization delays biologic initiation and is linked with a higher risk of disease exacerbation, which means the cost problem extends beyond list price and into timing of care. Biosimilar entry has not fully solved the issue because a 2025 Heliyon study reported that only around half of Medicare Part D plans covered adalimumab biosimilars, and fewer plans covered the higher-concentration versions used more often in practice. This keeps originator pricing power stronger than expected and leaves the ocular inflammation treatment market with a wider clinical opportunity than its reimbursed opportunity in many settings.

Steroid Safety Burden and Long-Term Compliance Issues

The ocular inflammation treatment market also remains constrained by the safety burden of corticosteroids, even though they still serve as the main first-line treatment across many disease settings. The 2025 Japanese J-CAT study showed that the glaucoma medication prescription rate reached 106 per 1,000 patient-years within the first year of non-infectious uveitis treatment, which points to the frequency of steroid-related intraocular pressure problems in real-world care. Tarsier Pharma moved its macrophage-modulating TRS01 eye drops into a second Phase 3 trial under FDA Special Protocol Assessment partly because the program aims to avoid the pressure-elevation issue tied to steroid pathways. Monitoring costs, frequent dosing, and repeated pressure checks also reduce persistence for older and lower-income patients, which keeps real-world adherence below what clinical guidance would ideally support. This means the ocular inflammation treatment market does not only need better efficacy, but it also needs safer long-term use and simpler follow-up demands.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Type: Corticosteroids anchor volume while biologics build long-term share

Corticosteroids held 32.89% of the ocular inflammation treatment market share in 2025, which made them the largest treatment type in the ocular inflammation treatment market. Their lead reflects broad use across post-surgical inflammation, anterior disease, and chronic posterior uveitis, where fast symptom control still matters in routine care. The Japanese J-CAT study reported that 68.7% of non-infectious uveitis patients were managed only with corticosteroid eye drops at the index date, which shows how much the ocular inflammation treatment market still depends on conservative first-line therapy even in advanced health systems.[4]Real-world treatment patterns for patients with non-infectious uveitis in Japan: a descriptive study using a large-scale claims database (J-CAT study) This keeps steroid volumes high because many patients never move immediately into systemic escalation, especially when the disease is detected early or remains anterior in location. The corticosteroid base also supports demand across hospital, retail, and online distribution channels, which helps the ocular inflammation treatment industry preserve a large recurring prescription pool.

Immunosuppressants and immunomodulators are the fastest-growing treatment group with a projected 6.83% CAGR through 2031, as steroid-sparing use moves earlier in chronic disease management. Methotrexate, mycophenolate, and related systemic options continue to gain relevance because they can support longer control in patients who are not good candidates for repeat steroid exposure. Biologics remain the most active innovation layer, led by adalimumab and newer mechanisms such as TYK2 and JAK1 inhibition, which could alter share over the medium term if Phase 3 programs read out well. Cycloplegic agents still hold a stable supporting role in anterior uveitis, while antibiotics and antivirals remain necessary for infectious disease subsets that require a different treatment path from non-infectious inflammation.

By Disease Type: Uveitis drives the core while conjunctivitis expands faster

Uveitis accounted for 34.18% share in 2025, which made it the largest disease category in the ocular inflammation treatment market. Its lead comes from high treatment intensity, recurrent episodes, and the threat of complications such as uveitic macular edema and glaucoma, which push patients into longer follow-up and higher medication use. Tarsier Pharma reported new 2025 data showing a sharp rise in vision loss from uveitis, which suggests current outcomes still leave room for safer and more durable treatment approaches. This keeps uveitis at the center of the ocular inflammation treatment market because it combines volume, severity, and repeat treatment need.

Conjunctivitis is the fastest-growing disease type at a 6.36% CAGR through 2031, supported by wider diagnosis of allergic and infectious forms across emerging markets. Urbanization, environmental allergen exposure, and easier access to evaluation are widening the treated patient base in the Asia-Pacific and South America. The 2025 Japanese Ophthalmological Society guideline update for viral conjunctivitis shows that treatment pathways are becoming more standardized, which can support more consistent prescribing. Keratitis, scleritis, and retinitis remain smaller but clinically important categories because they are often severe, require targeted therapy, and can carry higher value per treated patient than routine conjunctivitis.

By Cause: Non-infectious etiology leads volume, while autoimmune cases grow fastest

Non-infectious disease held 43.89% share in 2025, which made it the leading cause segment in the ocular inflammation treatment market. Its scale reflects the large population managed with corticosteroids and the rising subset of patients who later become candidates for immunomodulators, biologics, or durable delivery systems. Non-infectious care also tends to involve longer monitoring cycles, which keeps prescription continuity and follow-up intensity higher than in short-course disease. This makes the non-infectious base especially important for companies that rely on chronic therapy volume rather than episodic dispensing. The non-infectious share therefore gives the ocular inflammation treatment market a more durable revenue mix than a purely acute-care model would provide.

Autoimmune disease-related cases are projected to grow at an 8.23% CAGR through 2031, the fastest pace in this segmentation. Better coordination between rheumatology and ophthalmology is helping more patients reach an established systemic diagnosis earlier, which increases the chance that ocular inflammation is treated as part of a broader immune condition rather than an isolated eye episode. Infectious causes remain relevant in regions where herpesvirus, tuberculosis, toxoplasma, and fungal disease continue to shape case mix, which preserves a separate need for antibiotics and antivirals in the ocular inflammation treatment market. Trauma-related inflammation remains smaller in absolute volume, but its role is increasing as procedure counts rise and post-intervention inflammation becomes a more visible part of ophthalmic care.

By Route of Administration: Topical therapies lead while injectable platforms gain speed

Topical therapy captured 58.36% share of the ocular inflammation treatment market size in 2025, which kept it as the leading route of administration. That lead reflects the high frequency of anterior segment disease and the continued dependence on corticosteroid and NSAID eye drops as the first treatment step for many presentations. Topical therapy also remains the easiest route to distribute widely through hospitals, retail, and online channels, which protects volume even while advanced procedures gain attention. The route stays central to the ocular inflammation treatment market because it supports immediate access, low initial complexity, and familiar use in routine ophthalmology. It also aligns with the large base of patients who are still managed conservatively at diagnosis rather than escalated right away.

The ocular inflammation treatment market size for injectable therapies is projected to expand at an 8.10% CAGR through 2031, making injectables the fastest-growing route. Intravitreal, subconjunctival, and suprachoroidal delivery are gaining traction because they reach the posterior segment more directly and can offer longer effect between visits. The 2024 publication of consensus guidelines for suprachoroidal injection technique should reduce procedure variability and support more consistent use in specialist centers. Oral therapy still matters for systemic immunosuppressants, and newer oral targeted drugs could strengthen that route if late-stage programs succeed, but injectables currently hold the clearest momentum in advanced disease management.

By Distribution Channel: Hospital pharmacies retain control, while online pharmacies grow faster

Hospital pharmacies held 45.38% share in 2025, which kept them as the largest distribution channel in the ocular inflammation treatment market. This position fits the clinical reality of the category because many patients need specialist prescribing, baseline testing, pressure monitoring, and follow-up inside ophthalmology centers. Hospital channels also benefit from formulary control and group purchasing, which can favor branded biologics and advanced delivery products that are harder to place through general retail. That gives hospitals a lasting role in the ocular inflammation treatment market, especially for severe non-infectious uveitis and posterior segment treatment. It also means access to advanced therapies often depends on institutional processes rather than only on patient demand.

Online pharmacies are projected to grow at an 8.34% CAGR through 2031, the fastest pace among channels. Growth is linked to specialty pharmacy mail-order models that support chronic oral drugs, self-administered biologics, and patient services such as prior authorization help and adherence support. Retail pharmacies remain important for topical anti-inflammatories and related short-course products, but they are not expanding as quickly as specialty-linked online models. ANI Pharmaceuticals’ integration of ILUVIEN and YUTIQ into its rare disease commercial structure also shows how specialized distribution is becoming more important for long-acting ocular products across the ocular inflammation treatment industry.

Geography Analysis

North America held 42.38% of the ocular inflammation treatment market share in 2025, which made it the largest regional contributor. The region benefits from high biologic penetration, broad specialist coverage, and reimbursement systems that can support both self-injected and hospital-administered products. The United States remains the main launch market in the ocular inflammation treatment market because regulatory and reimbursement events continue to shape commercial access earlier than in most regions. The September 2025 end of Humira pediatric orphan exclusivity widened formal biosimilar entry in uveitis, while the January 2024 activation of the CPT Category 1 code for XIPERE improved reimbursement footing for suprachoroidal procedures. Canada continues to follow major U.S. approvals with a shorter lag in high-value ophthalmic products, as shown by the July 2025 XIPERE approval for uveitic macular edema.

Europe remains a strong but distinct region in the ocular inflammation treatment market because prescribers have used non-biologic immunosuppressants earlier in the treatment path than many United States centers. Germany, the United Kingdom, and France account for much of the region’s biologic volume because they combine specialist density with public or statutory reimbursement systems that can carry chronic therapy. Santen also holds an established ocular surface anti-inflammatory position in Europe through Verkazia, which gives it a practical base for broader ophthalmic inflammation activity. The region therefore supports steady uptake in the ocular inflammation treatment market, but its conversion into biologics often follows a more stepwise path than in North America.

Asia-Pacific is the fastest-growing region, and the ocular inflammation treatment market size there is projected to expand at a 7.16% CAGR through 2031. Growth is being supported by rising specialist density, broader diagnosis, and regulatory progress for new delivery systems and targeted therapies. Arctic Vision reported positive Phase 3 topline results for ARCATUS in uveitic macular edema in China in July 2024 and filed NDAs in Australia and Singapore, which shows that the ocular inflammation treatment market in Asia-Pacific is moving beyond generic topical care.[5]Clearside Biomedical’s Partner Arctic Vision Reports Positive Topline Results from Phase 3 Clinical Trial of ARCATUS® for Suprachoroidal Use in Uveitic Macular Edema Patients in China Santen’s December 2025 launch of Verkazia in China also expanded anti-inflammatory ophthalmic availability in the region’s largest eye-care market. Japan remains especially important because real-world data showed that 68.7% of non-infectious uveitis patients were still managed with corticosteroid drops alone, which suggests room for future escalation in a system that already has advanced specialist care.

Competitive Landscape

The ocular inflammation treatment market has a moderately concentrated structure in its biologic tier, but it is more mixed when topical, systemic, and procedural treatments are viewed together. AbbVie remains important through Humira and the opening biosimilar wave, while Regeneron and Sanofi hold a strong immune-inflammation position through Dupixent across adjacent inflammatory disease areas. Bausch + Lomb’s commercialization of XIPERE shows how delivery platform ownership can create a defensible niche in the ocular inflammation treatment market even when the active molecule itself is familiar. Clearside Biomedical has taken a different route by building platform value around the SCS Microinjector and partnering across geographies and indications instead of relying only on one finished branded product. This means the ocular inflammation treatment market is being shaped as much by control of route and procedure as by control of molecule.

Several strategic moves since 2024 show how companies are trying to lock in future share. ANI Pharmaceuticals expanded its rare disease ophthalmology position by acquiring Alimera Sciences and integrating ILUVIEN and YUTIQ into its commercial base, which strengthens specialist-channel access for long-acting implants. AbbVie and REGENXBIO also moved ABBV-RGX-314 toward a planned Phase 3 program using the SCS Microinjector, which shows that large companies now see the suprachoroidal route itself as a competitive asset in posterior segment disease. Santen strengthened its regional ophthalmic inflammation position by launching Verkazia in China in December 2025, adding another direct commercial foothold in Asia-Pacific. These moves keep the ocular inflammation treatment market active across branded drugs, route innovation, and regional expansion at the same time.

Smaller and mid-sized developers are now competing in narrower but meaningful spaces where unmet need is still clear. Priovant is focused on oral TYK2 and JAK1 inhibition through brepocitinib, which could offer an alternative for chronic non-anterior disease if Phase 3 data are supportive. Tarsier is targeting steroid replacement in anterior uveitis and uveitic glaucoma with TRS01, which directly addresses one of the clearest safety gaps in the ocular inflammation treatment market. EyePoint is now more focused on sustained-release retinal programs than posterior uveitis implants after earlier portfolio shifts, which leaves room for other firms to define the next long-acting inflammation platform. Academic and preclinical groups are also adding pressure through nano-formulation topical delivery and implant technologies that could lower procedure burden over time. As a result, the ocular inflammation treatment market is unlikely to settle around one treatment model, and competition should remain spread across biologics, oral immunology, and long-acting delivery systems.

Ocular Inflammation Treatment Industry Leaders

AbbVie Inc.

Bausch Health Companies Inc.

Johnson and Johnson Services, Inc.

Novartis AG

Pfizer Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: EyePoint Pharmaceuticals reported Phase 3 DURAVYU topline data in wet AMD (LUGANO trial) is expected to begin mid-2026, with COMO and CAPRI Phase 3 DME trials currently enrolling; DURAVYU's Durasert E sustained-release technology remains the most advanced bioerodible TKI platform in late-stage retinal disease development.

- January 2026: EyePoint entered 2026 with USD 223 million in cash, LUGANO trial fully enrolled, and LUCIA Phase 3 trial greater than 60% enrolled, establishing it as the lead candidate among investigational sustained-release programs for the largest multi-billion-dollar retina indications.

- December 2025: Santen launched Verkazia (ciclosporin eye drops) in China for severe vernal keratoconjunctivitis in children and young adults, extending the anti-inflammatory ophthalmic portfolio into Asia's largest market following earlier approvals in 11 countries, including France and the United Kingdom

- July 2025: Clearside Biomedical's XIPERE received Health Canada approval for suprachoroidal treatment of uveitic macular edema, bringing the product to its fourth approved market (US, Canada, Australia, Singapore), and positioning Arctic Vision's ARCATUS for pending multi-market regulatory review in China and other geographies.

Global Ocular Inflammation Treatment Market Report Scope

The Ocular Inflammation Treatment Market refers to the global market for pharmaceutical therapies used to prevent, manage, and treat inflammatory conditions affecting different parts of the eye. It includes medications prescribed for infectious and non-infectious ocular inflammatory diseases. The market encompasses both prescription and hospital-administered treatments aimed at reducing inflammation, preserving vision, relieving symptoms, and preventing disease progression.

The ocular inflammation treatment market is segmented by treatment, disease type, cause, route of administration, distribution channel, and geography. By treatment, it is further divided into corticosteroids, immunosuppressants and immunomodulators, biologics, cycloplegic agents, antibiotics, antivirals, and others. By disease type, it is segmented into uveitis, conjunctivitis, keratitis, scleritis, retinitis, and others. By cause, the market is segmented into non-infectious, infectious, autoimmune disease-related, trauma and injury-related, and others. By route of administration, the market is segmented into topical, oral, injectable, and others. By distribution channel, the market is segmented into hospital pharmacies, retail pharmacies, online pharmacies, and others. The geography segment is further divided into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market size and forecasts in value (USD) for the above segments.

| Corticosteroids |

| Immunosuppressants and Immunomodulators |

| Biologics |

| Cycloplegic Agents |

| Antibiotics |

| Antivirals |

| Others (Analgesics and Antifungals, among others) |

| Uveitis |

| Conjunctivitis |

| Keratitis |

| Scleritis |

| Retinitis |

| Others (Endophthalmitis and Optic Neuritis, among others) |

| Non-Infectious |

| Infectious |

| Autoimmune Disease Related |

| Trauma and Injury Related |

| Others (Drug-induced ocular inflammation and Post-surgical inflammation, among others) |

| Topical |

| Oral |

| Injectable |

| Others (Intravitreal and Subconjunctival, among others) |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| Others (Drug Stores and Specialty Pharmacies, among others) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Treatment Type | Corticosteroids | |

| Immunosuppressants and Immunomodulators | ||

| Biologics | ||

| Cycloplegic Agents | ||

| Antibiotics | ||

| Antivirals | ||

| Others (Analgesics and Antifungals, among others) | ||

| By Disease Type | Uveitis | |

| Conjunctivitis | ||

| Keratitis | ||

| Scleritis | ||

| Retinitis | ||

| Others (Endophthalmitis and Optic Neuritis, among others) | ||

| By Cause | Non-Infectious | |

| Infectious | ||

| Autoimmune Disease Related | ||

| Trauma and Injury Related | ||

| Others (Drug-induced ocular inflammation and Post-surgical inflammation, among others) | ||

| By Route of Administration | Topical | |

| Oral | ||

| Injectable | ||

| Others (Intravitreal and Subconjunctival, among others) | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| Others (Drug Stores and Specialty Pharmacies, among others) | ||

| By Region | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the ocular inflammation treatment market?

The ocular inflammation treatment market reached USD 7.78 billion in 2025 and is forecast to reach USD 10.78 billion by 2031, growing at a 6.83% CAGR.

Which treatment type leads ocular inflammation treatment revenue today?

Corticosteroids led treatment type revenue with a 32.89% share in 2025 because they remain the most common first-line option across many ocular inflammatory conditions.

Which disease area drives the most demand in ocular inflammation treatment?

Uveitis led with a 34.18% share in 2025 because it is recurrent, treatment-intensive, and linked with serious complications such as macular edema and glaucoma.

Why are injectable therapies growing faster than other routes?

Injectable therapies are projected to grow at an 8.10% CAGR through 2031 because suprachoroidal, intravitreal, and subconjunctival delivery can target posterior disease more precisely and for longer periods.

Which region offers the strongest growth opportunity through 2031?

Asia-Pacific offers the strongest growth outlook with a projected 7.16% CAGR, supported by regulatory progress, rising specialist access, and broader use of advanced anti-inflammatory therapies.

What is the main barrier limiting wider use of advanced ocular inflammation therapies?

High cost remains the biggest barrier because biologics and advanced delivery systems face reimbursement gaps, prior authorization delays, and uneven biosimilar coverage in real-world care.

Page last updated on: