Norway Electric Vehicle Charging Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

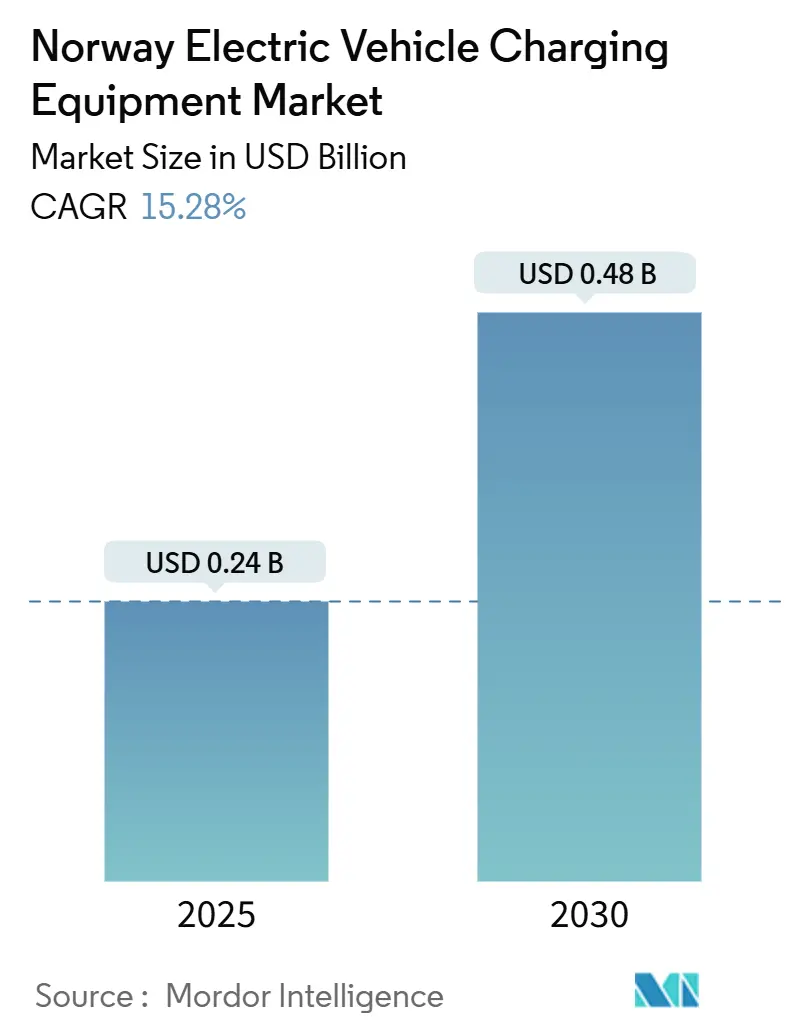

| Market Size (2025) | USD 0.24 Billion |

| Market Size (2030) | USD 0.48 Billion |

| Growth Rate (2025 - 2030) | 15.28% CAGR |

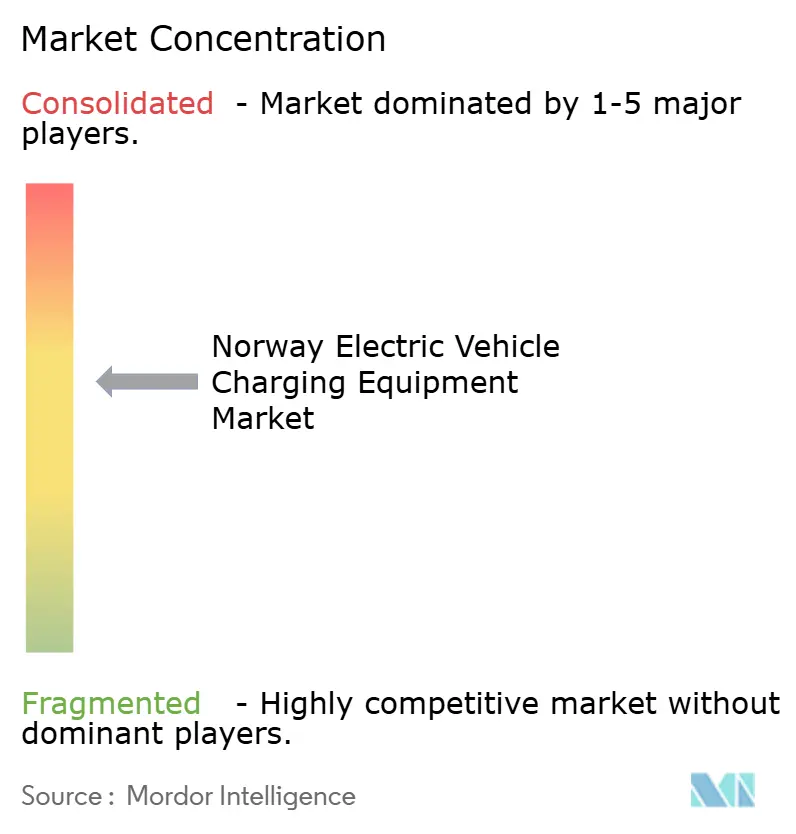

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Norway Electric Vehicle Charging Equipment Market Analysis by Mordor Intelligence

The Norway Electric Vehicle Charging Equipment Market size is estimated at USD 0.24 billion in 2025, and is expected to reach USD 0.48 billion by 2030, at a CAGR of 15.28% during the forecast period (2025-2030).

A near-universal switch to battery-electric passenger cars is shifting demand toward commercial vehicle, maritime, and high-power corridor solutions. Residential ownership still drives high baseline utilization because 88.9% of 2024 new-car sales were battery electric, yet upgrade cycles favor 11 kW and 22 kW wallboxes as households add second EVs. National hydropower keeps electricity tariffs low, reinforcing total-cost-of-ownership benefits for fleets that can schedule charging at night. Fiscal incentives funded by Enova reduce upfront costs for heavy-duty and maritime chargers, while grid-integration pilots monetize flexibility and vehicle-to-grid services. Payment-platform fragmentation and local grid-capacity bottlenecks temper growth, though both obstacles are being addressed through interoperability standards and new maturity rules for projects exceeding 1 MW.

Key Report Takeaways

- By charging level, Level 2 held 63.9% of Norway electric vehicle charging equipment market share in 2024, while Megawatt Class chargers are projected to rise at a 33.4% CAGR through 2030.

- By installation site, residential accounted for 72.5% of the Norway electric vehicle charging equipment market size in 2024, whereas transportation hubs are expected to post a 29.2% CAGR to 2030.

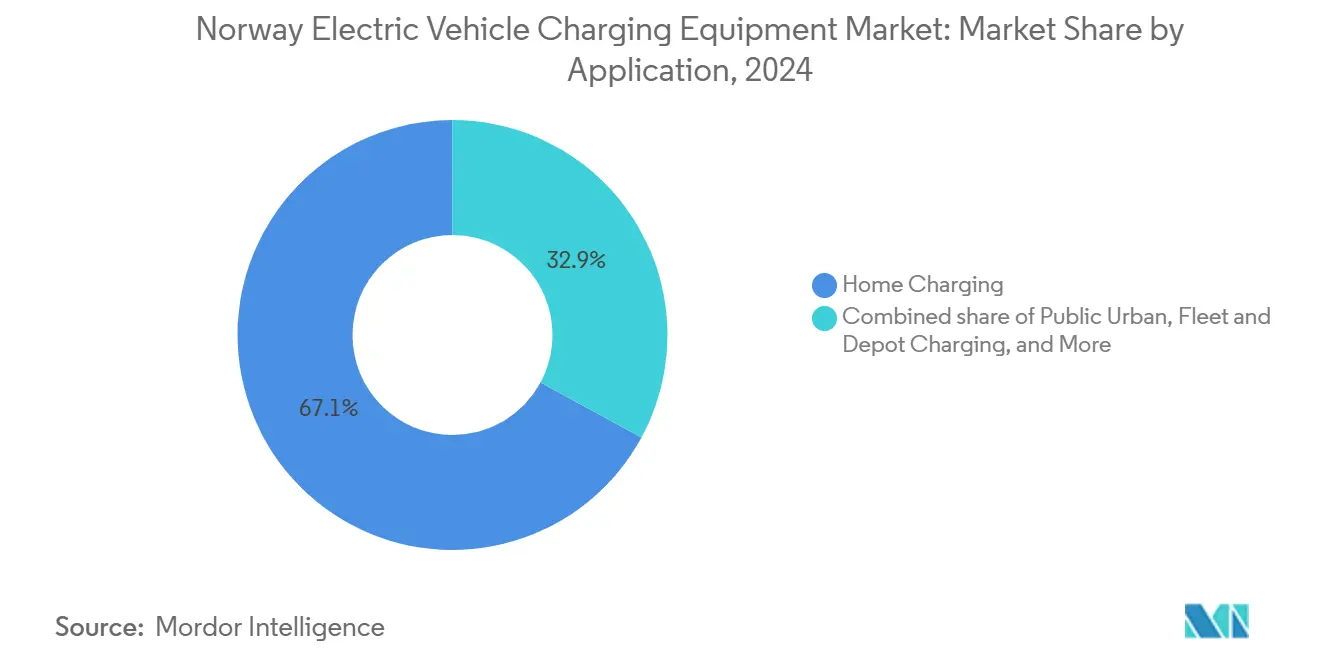

- By application, home charging delivered 67.1% of revenue in 2024, and fleet and depot charging is anticipated to grow at a 32.9% CAGR between 2025 and 2030.

- Zaptec, Easee, and ABB together controlled roughly 25% of public AC and DC deployments in 2024.

Relative standing becomes clear only when country-level and regional contributions are evaluated alongside one another at a global level. Mordor Intelligence's electric vehicle charging equipment market share coverage captures this comparative structure.

Norway Electric Vehicle Charging Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid EV adoption and national 2025 zero-emission vehicle target | 3.20% | Oslo, Bergen, Trondheim | Short term (≤ 2 years) |

| Comprehensive fiscal incentives for chargers and EVs | 2.80% | National urban municipalities | Medium term (2-4 years) |

| Grid-friendly hydropower keeping charging tariffs low | 2.10% | Vestland, Rogaland | Long term (≥ 4 years) |

| Monetization of vehicle-to-grid and flexibility markets | 1.90% | Oslo, Trøndelag pilot zones | Medium term (2-4 years) |

| Tourism-related demand for rural fast-charging corridors | 1.60% | Lofoten, Nordkapp routes | Medium term (2-4 years) |

| Battery-swap and depot fleet electrification pilots | 2.50% | Coastal ferries, Oslo-Bergen logistics | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid EV Adoption And National 2025 Zero-Emission Vehicle Target

Norway recorded a 97.6% plug-in share in November 2025, signaling that the 2025 mandate is effectively achieved ahead of schedule.[1]Geir Røed, “Bilsalget i Norge 2024–2025,” OFV, ofv.no Early Level 1 and low-power Level 2 devices installed between 2018 and 2021 are now being replaced with faster 11 kW or 22 kW units. Vendors are pivoting to commercial customers, including taxi cooperatives and municipal fleets, that require depot charging with automated billing and load management. The VAT exemption for EVs under NOK 500,000 remains through 2024, though it phases down in 2025.[2]Norwegian Ministry of Finance, “VAT Exemption for Electric Vehicles,” regjeringen.no Policy certainty guides private capital toward high-power solutions rather than incremental residential upgrades, sustaining momentum for the Norway electric vehicle charging equipment market.

Comprehensive Fiscal Incentives For Chargers And EVs

Enova allocated NOK 1.5 billion (USD 141 million) during 2023-2024, covering up to 40% of installation costs for workplace, public, and heavy-duty chargers.[3]Enova SF, “Annual Report 2024,” enova.no The fund now prioritizes megawatt-class maritime and truck sites, accelerating high-power deployments such as Circle K’s 400 kW hub at E18 Sekkelsten that opened in February 2025. Smaller operators outside the heavy-duty focus must rely on leasing or commercial finance, reshaping competition toward players with strong project-finance capabilities and global supply chains. The narrowed but still-generous subsidy regime keeps the Norway electric vehicle charging equipment market attractive for investors.

Grid-Friendly Hydropower Keeping Charging Tariffs Low

Hydropower supplied 88% of Norway’s 137.6 TWh generation in 2024. Capacity-based distribution tariffs introduced in 2022 let operators schedule off-peak charging, enabling depot rates near NOK 0.50 per kWh compared with NOK 1.20-1.80 for public highway fast charging. The low-cost energy foundation underpins fleet electrification economics and sustains high utilization across residential and workplace chargers. Wholesale price stability also reduces payback horizons for megawatt-class equipment, improving bankability for private investors.

Monetization Of Vehicle-To-Grid And Flexibility Markets

Statnett balancing markets allow aggregated EV fleets to provide frequency regulation, and pilot projects show 15.7% peak-demand reduction through bidirectional charging. The eNabo demand-response scheme pays customers for shifting load away from evening peaks. Although regulatory clarity on metering and battery degradation remains incomplete, commercial interest is strong because ancillary-service revenues shorten payback periods for depot installations. Standardized contracts and interoperable protocols are required before large-scale rollout, yet the flexibility opportunity strengthens the long-term outlook for the Norway electric vehicle charging equipment market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital expenditure for public fast-charging sites | -1.80% | Rural municipalities | Medium term (2-4 years) |

| Uneven charger density outside urban areas | -1.30% | Finnmark, inland Hedmark | Long term (≥ 4 years) |

| Fragmented apps and payment platforms hurting user experience | -1.10% | Cross-border routes to Sweden and Finland | Short term (≤ 2 years) |

| Local distribution-grid capacity bottlenecks | -2.00% | Oslo suburbs, Stavanger industrial zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Expenditure For Public Fast-Charging Sites

Site acquisition, civil works, and transformer upgrades push per-outlet costs beyond NOK 2 million (USD 190,000). Rural utilization volatility lowers return on capital, delaying private investment and requiring higher Enova grants or utility participation. Equipment vendors respond with modular systems that share power electronics across dispensers, reducing upfront cash outlay. Despite engineering innovations, capital intensity still constrains corridor expansion in low-traffic areas.

Uneven Charger Density Outside Urban Areas

In Finnmark, charger density is one-fifth of Oslo’s, resulting in range anxiety for residents and tourists. Seasonal tourism spikes create congestion at the few available stations, while winter downtime weakens operating margins. Public-private partnerships are filling gaps, yet long distances and harsh weather inflate maintenance costs. Grid reinforcement lags behind national averages, prolonging rural disparity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Charging Level: Megawatt Systems Reshape Commercial Infrastructure

Megawatt-class chargers are projected to capture 9.5% of the Norway electric vehicle charging equipment market size by 2030, up from 1.4% in 2024, and they will grow at a 33.4% CAGR. The segment targets 15-minute fueling for 500 kWh truck packs, aligning electric logistics with diesel timetables. ABB, Siemens, and Kempower dominate through liquid-cooled cable technology and scalable rectifiers. Level 2 remains the installed-base leader because it served 63.9% of 2024 demand, yet growth moderates in favor of higher power tiers. Ultra-Fast units between 150 kW and 350 kW account for most public-charging energy, despite a smaller share of installed points, because they maximize throughput on busy corridors. Level 1 serves legacy and emergency needs only. Diverging power tiers act as a proxy for user segments: Level 2 targets homeowners, DC Fast and Ultra-Fast serve corridor and destination needs, and Megawatt Class focuses on heavy freight and maritime operators.

Product differentiation aligns with these tiers. Zaptec and Easee integrate load balancing that lets housing cooperatives host multiple Level 2 chargers on one 63-amp circuit, while ABB’s Terra 360 platform scales from 180 kW to 360 kW by adding modules. Schneider Electric’s EVlink Pro DC addresses depot operators that need 120-180 kW flexible output, integrating with building-management systems for demand-response revenue. Competitive intensity, therefore, varies by tier, with domestic brands dominating Level 2 and global industrial leaders owning Megawatt and Ultra-Fast opportunities.

By Installation Site: Transportation Hubs Drive Next-Wave Growth

Transportation hubs are forecast to post a 29.2% CAGR through 2030, lifting their share from 4.7% in 2024 to an expected 11.8%. They benefit from predictable traffic and existing electrical capacity, making them prime targets under new grid-maturity rules that favor shovel-ready projects. Oslo Airport added 200 taxi and rental-car chargers in 2024, and Bergen Port Authority integrates shore power and battery swap to service coastal ferries. Residential sites still anchor revenue because they commanded a 72.5% share in 2024, yet their expansion slows as single-family adoption nears saturation and apartment retrofits face legal and cost hurdles. Housing boards may postpone resident requests if costs exceed NOK 50,000 per person, delaying rollouts.

Commercial and retail locations leverage free or subsidized charging as a customer-retention tool, with supermarkets reporting longer dwell times when chargers are available. Public municipal projects in Oslo, Bergen, and Trondheim add curbside capacity for residents without private parking, though utilization varies. The regulatory pivot toward large, financed projects amplifies the attractiveness of hub installations, leading to a hub-and-spoke model where high-power hubs handle commercial turnover and residential units provide overnight convenience.

By Application: Fleet And Depot Charging Outpaces Consumer Segments

Fleet and depot charging is expected to expand at a 32.9% CAGR, taking its share from 10.9% in 2024 to 28.4% by 2030, as municipal waste-collection contracts and last-mile delivery rules mandate zero-emission vehicles. Depot operators exploit off-peak tariffs and earn flexibility revenue in Statnett markets, shortening payback periods. Small and medium operators lag due to financing hurdles and grid-upgrade requirements, which opens white-space opportunities for charge-point operators that offer infrastructure-as-a-service.

Home charging retained 67.1% of 2024 revenue and remains essential for convenience, yet growth plateaus. Workplace installations rise steadily in urban office parks where employers support staff electrification and track carbon savings in corporate disclosures. Public urban chargers serve apartment dwellers, though comparative costs and competition from private garages limit utilization. Highway corridor stations, run by IONITY, Circle K, and Shell Recharge, supply long-distance travel, relying on high-power throughput and ancillary sales to raise margins. Application segmentation, therefore, reflects maturity: home charging is mature, workplace and public urban are steady, and fleet plus highway segments are in rapid expansion.

Geography Analysis

Oslo, Bergen, and Trondheim account for most deployments thanks to dense populations, high EV penetration, and robust grids. Oslo hosts more than 8,000 public charge points, including the first megawatt-ready truck hub at E18 Sekkelsten that opened in February 2025.[4]NOBIL, “Public Charging Statistics,” info.nobil.no Western counties Vestland and Rogaland enjoy hydropower proximity, letting depot operators secure tariffs below NOK 0.50 per kWh. Eviny operates over 2,000 regional points and is extending fast charging along the E39 coastal route.[5]Eviny AS, “Charging Network Expansion,” eviny.no

Northern Norway faces sparse populations and seasonal tourist peaks. Enova co-funds corridor sites every 50-70 km, yet utilization falls below 20% outside summer months. Solar-battery microgrids reduce grid-tie costs and improve resilience during winter storms. Cross-border corridors to Sweden and Finland see expanded fast charging, though payment fragmentation requires multiple apps and raises friction. New 1 MW maturity rules force project sponsors to prove financing before grid capacity is reserved, favoring well-capitalized urban hubs over speculative rural plans. Statnett’s NOK 150 billion investment plan will double national consumption to 260 TWh by 2050, focusing capacity on growth corridors. These regional disparities shape a competitive mosaic: urban areas feature fragmented private competition, while rural zones depend on utility-backed networks and public subsidies.

Analysis of the electric vehicle charging equipment market by Mordor Intelligence spans multiple other regional evaluations across Europe, North America, and South America, supported by country-level insights for Denmark, Netherlands, Belgium, Spain, Italy, and Sweden, wherein local market conditions keep varying from one country to another.

Competitive Landscape

Competition is moderate, with the leading operator holding about 25% of both AC and DC segments. Domestic hardware specialists Zaptec and Easee defend home and workplace niches through intelligent load-balancing, reporting NOK 935 million and NOK 1.7 billion in 2024 revenue and funding, respectively. ABB, Siemens, and Schneider Electric contest high-power depot markets, with ABB’s E-mobility division registering USD 400 million in Q3 2024 revenue and Schneider launching EVlink Pro DC in April 2024.

Utility-backed operators Fortum Recharge, Mer, and Eviny dominate public fast-charging corridors, while oil majors Circle K and Shell Recharge build highway networks, including Circle K’s plan for 15 truck hubs by the end of 2025. White-space opportunities include depot charging for small logistics firms and battery-swap infrastructure for ferries. Kempower leads modular megawatt systems, and Wallbox targets residential retrofits with compact app-enabled devices. Strategic focus is shifting from hardware margins to platform services such as energy-management software, carbon offsets, and renewable-certificate bundling. Tesla’s opening of its Supercharger network adds 1,000 high-reliability points but keeps proprietary pricing, reshaping corridor dynamics.

Norway Electric Vehicle Charging Equipment Industry Leaders

Zaptec ASA

Easee ASA

ABB Ltd.

Fortum Recharge AS

Mer Norway (Statkraft)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: NVE enforced grid-connection maturity rules that require projects above 1 MW to show financing and construction readiness before capacity allocation.

- February 2025: Circle K opened Norway’s first public truck hub at E18 Sekkelsten, featuring 400 kW dispensers and plans for 15 similar sites by year-end.

- December 2024: Enova allocated NOK 1.5 billion in grants and shifted focus from light vans to heavy-duty and maritime charging.

- August 2024: The Megawatt Charging System standard debuted at EVS 35 in Oslo, and Kempower partnered with Fastcharge for MCS-compatible depots in Oslo and Bergen.

Norway Electric Vehicle Charging Equipment Market Report Scope

The EV charging equipment industry encompasses the design, manufacture, supply, installation, and maintenance of hardware and systems essential for charging electric vehicles (EVs). This sector covers all components, ranging from physical devices to digital platforms, that facilitate energy transfer from the grid (or distributed energy resources) to a variety of electric vehicles, including cars, buses, trucks, and two- or three-wheelers.

The Norway electric vehicle charging equipment market is segmented into charging level, installation site, and application. The market is segmented by charging level into Level 1 (Up to 3 kW), Level 2 (3 to 50 kW), DC Fast (50 to 150 kW), Ultra-Fast (150 to 350 kW), and Megawatt Class (Above 350 kW). By installation site, the market is divided among residential, commercial and retail, public municipal, and transportation hubs (airports, ports). The market is segmented into home charging, workplace charging, public urban charging, highway corridor/en-route fast charging, and fleet and depot charging. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Level 1 (Up to 3 kW) |

| Level 2 (3 to 50 kW) |

| DC Fast (50 to 150 kW) |

| Ultra-Fast (150 to 350 kW) |

| Megawatt Class (Above 350 kW) |

| Residential |

| Commercial and Retail |

| Public Municipal |

| Transportation Hubs (Airports, Ports) |

| Home Charging |

| Workplace Charging |

| Public Urban Charging |

| Highway Corridor/En-Route Fast Charging |

| Fleet and Depot Charging |

| By Charging Level | Level 1 (Up to 3 kW) |

| Level 2 (3 to 50 kW) | |

| DC Fast (50 to 150 kW) | |

| Ultra-Fast (150 to 350 kW) | |

| Megawatt Class (Above 350 kW) | |

| By Installation Site | Residential |

| Commercial and Retail | |

| Public Municipal | |

| Transportation Hubs (Airports, Ports) | |

| By Application | Home Charging |

| Workplace Charging | |

| Public Urban Charging | |

| Highway Corridor/En-Route Fast Charging | |

| Fleet and Depot Charging |

Key Questions Answered in the Report

How large is the Norway electric vehicle charging equipment market in 2025?

The market stands at USD 0.24 billion in 2025 and is on track for USD 0.48 billion by 2030.

How fast will heavy-duty charging grow in Norway?

Megawatt Class systems are expected to expand at a 33.4% CAGR, driven by logistics and maritime electrification projects envisioned through 2030.

Which regions see the highest charger density?

Oslo, Bergen, and Trondheim lead with dense public networks, while Northern Norway relies on Enova-funded corridor projects and microgrids to close gaps.

What subsidy programs support commercial chargers?

Enova covers up to 40% of installation costs for workplace, public, and heavy-duty sites and is now prioritizing megawatt-class and maritime applications.

Are Norwegian electricity prices advantageous for fleets?

Yes, hydropower dominance and capacity-based tariffs let fleets access overnight rates near NOK 0.50 per kWh, reducing total operating costs.

What hinders rural fast-charging deployment?

High capital costs, low off-season utilization, and grid-capacity constraints slow private investment, so public-private partnerships remain essential.

Page last updated on: